Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

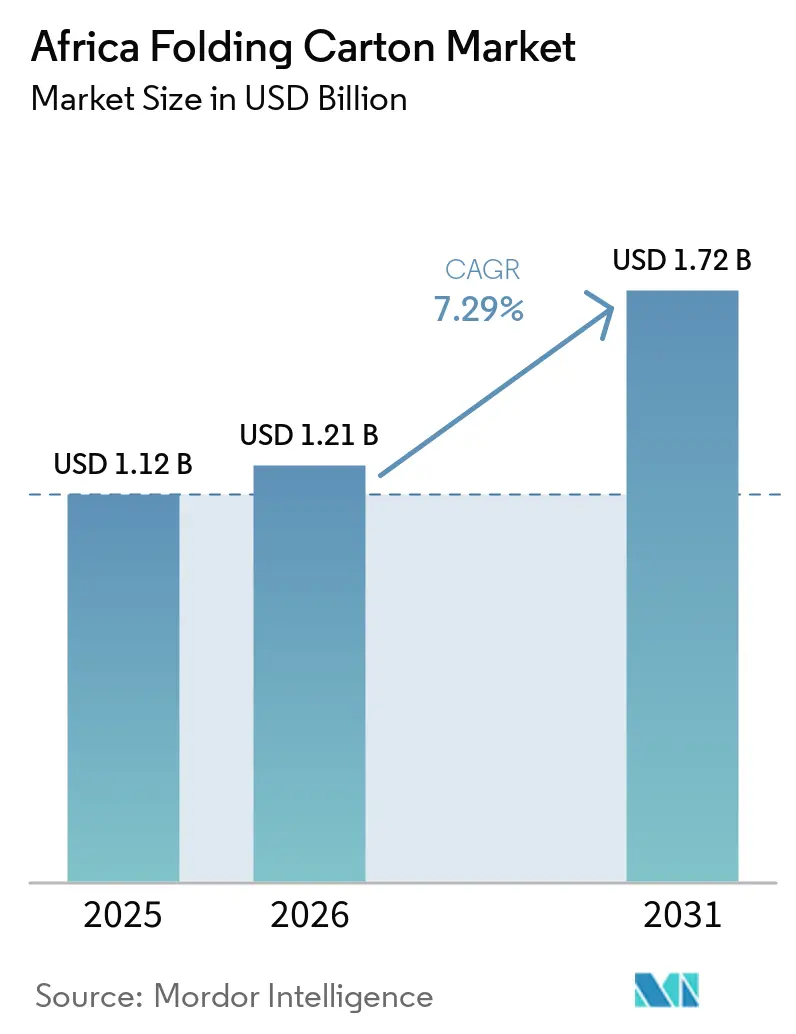

| Base Year Market Size (2025) | USD 1.12 Billion |

| Market Size (2026) | USD 1.21 Billion |

| Market Size (2031) | USD 1.72 Billion |

| Growth Rate (2026 - 2031) | 7.29% CAGR |

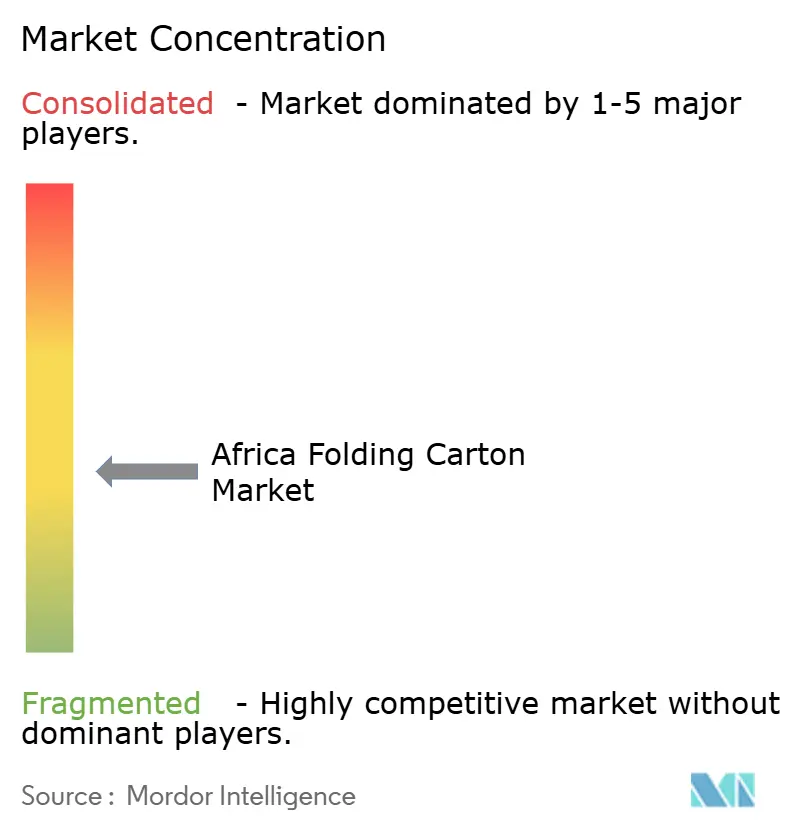

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Folding Carton Market Analysis by Mordor Intelligence

The Africa folding carton market size is expected to grow from USD 1.12 billion in 2025 to USD 1.21 billion in 2026 and is forecast to reach USD 1.72 billion by 2031 at a 7.29% CAGR over 2026-2031. Demand momentum is shaped by the African Continental Free Trade Area tariff phase-outs, which lower intra-regional trade costs and enable integrated paperboard supply chains. Extended producer responsibility rules in Kenya, South Africa, Egypt and Nigeria accelerate the shift toward mono-material, recyclable substrates that comply with food-contact and pharmaceutical standards. Substitution of banned polystyrene foam and restricted flexible plastics in foodservice and retail channels further amplifies uptake, while rapid e-commerce and quick-commerce growth boosts small-batch, branded carton volumes. Ongoing capital investment by both incumbents and digital-printing start-ups supports capacity expansion and technology upgrades that improve flexibility, reduce waste and protect converter margins amid input-price volatility.

Key Report Takeaways

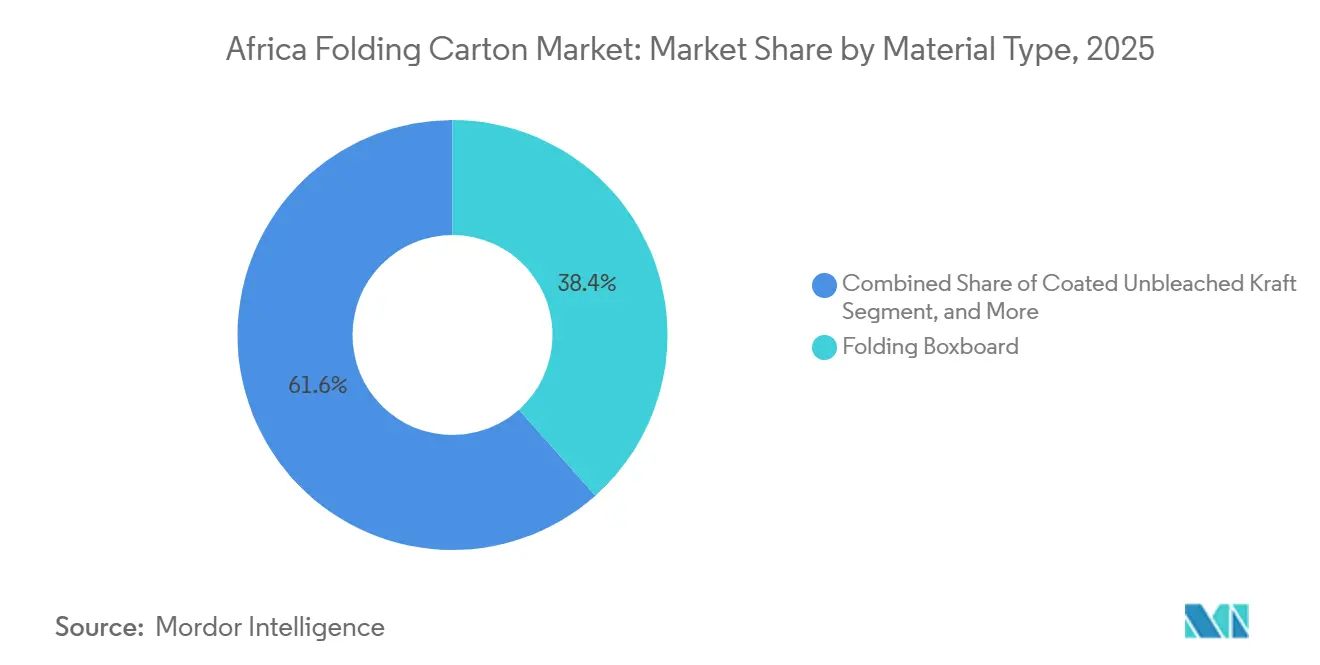

- By material type, folding boxboard captured with 38.43% of the Africa folding carton packaging market share in 2025.

- By printing technology, the Africa folding carton packaging market size for digital printing is projected to grow at a 8.78% CAGR to 2031.

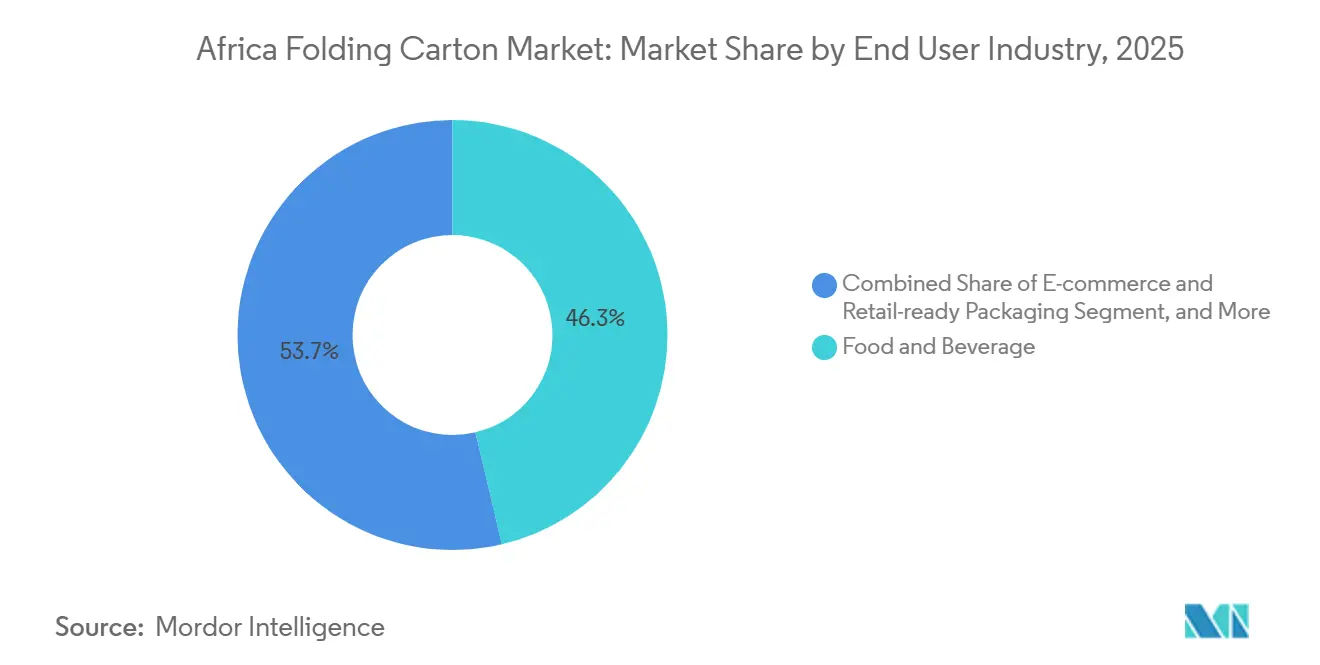

- By end-user industry, the food and beverage industry captured 46.32% of the Africa folding carton packaging market share in 2025.

- By geography, the Africa folding carton packaging market size for Nigeria is projected to grow at a 8.25% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand from the E-Commerce Sector | +1.8% | Nigeria, South Africa, Egypt, Kenya | Medium term (2-4 years) |

| Expansion of the Food and Beverage Industry | +1.5% | South Africa, Nigeria, Kenya | Long term (≥4 years) |

| Rising Adoption of Sustainable Packaging Regulations | +1.3% | South Africa, Kenya, Egypt, Nigeria, Ghana, Ethiopia | Short term (≤2 years) |

| Rapid Growth of Quick-Commerce Dark Stores | +0.9% | Lagos, Abuja, Nairobi, Johannesburg, Cape Town | Medium term (2-4 years) |

| Indigenous Digital-Printing Start-Ups | +0.7% | Morocco, Tanzania, Kenya, South Africa | Medium term (2-4 years) |

| AfCFTA Tariff Harmonization | +1.1% | East African Community, Southern African Development Community, broader Africa | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Demand from the E-Commerce Sector

Smartphone adoption, improved last-mile logistics, and expanding payment gateways are fueling double-digit online retail growth in Nigeria, South Africa, Egypt, and Kenya. Brand owners shipping fashion, electronics, and personal-care items now require protective, visually distinct folding cartons that enhance unboxing experiences and withstand the rigors of parcel networks. QR-code traceability demanded by customs modernization programs under AfCFTA raises print-resolution requirements and favors converters able to integrate security features. Digital presses shorten design cycles, allowing rapid artwork refreshes for promotion-heavy online channels, while smaller average order quantities reduce the economic appeal of long offset runs. The structural pull from e-commerce therefore expands short-run volumes, supports higher margins on premium substrates, and bolsters the Africa folding carton market outlook.

Expansion of Food and Beverage Industry

Citrus exports from South Africa exceeded 164.5 million 15-kilogram-equivalent cartons in 2024, anchoring steady demand for moisture-resistant folding cartons that meet European phytosanitary rules. Nigeria and Kenya are witnessing rapid rollouts of quick-service restaurants that replace banned polystyrene clamshells with grease-resistant paperboard packaging. Rising disposable incomes across urban households accelerate packaged-meal adoption and diversify SKU counts, pushing converters toward flexible production lines that balance food-contact compliance with cost control. Export-oriented fruit, seafood, and meat processors also demand cartonboard that endures cold-chain humidity without delamination. These intertwined export and domestic consumption trends reinforce the central role of food and beverages in scaling the Africa folding carton market.

Rising Adoption of Sustainable Packaging Regulations

South Africa’s Draft National Waste Management Strategy 2026 sets mandatory 20% post-consumer recycled content by 2027, rising to 40% by 2031. Kenya’s Legal Notice 176 of 2024 imposes per-item EPR fees and obliges importers to join producer-responsibility organizations. Egypt’s Decree 662 of 2025 adds a weight-based levy on plastic bags, signaling likely expansion to laminated cartons. These rules reward converters that can certify material composition, trace the origin of recycled fiber, and deploy water-based coatings compatible with mechanical recycling. Early compliance unlocks tax incentives and retailer procurement preference, accelerating market share gains for folding cartons designed as mono-material solutions.

Rapid Growth of Quick-Commerce Dark Stores in Urban Hubs

15-minute delivery promises in Lagos, Nairobi, and Johannesburg require shelf-ready primary packs that maximize storage density and visual clarity in small fulfillment centers. Variable-data digital printing supports frequent artwork updates for limited-time offers that appeal to young, digitally native consumers, as over 50% of East Africa’s population is under 25. Lightweighted dielines cut transport costs, while reinforced corner structures protect contents during scooter or bicycle delivery rounds. The resulting demand profile favors agile converters that invest in HP Indigo or Domino presses capable of high-opacity whites on colored substrates. This shift elevates flex-capacity utilization and enhances revenue diversity within the African folding carton industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Recycled Paper Pulp Prices | -1.2% | South Africa, Egypt | Short term (≤2 years) |

| Skilled Technician Shortage Limiting Automation Uptake | -0.9% | Nigeria, Kenya, Tanzania, Uganda | Medium term (2-4 years) |

| High Capital Expenditure Requirements | -0.6% | Nigeria, Kenya, Ghana | Long term (≥4 years) |

| Servo and PLC Import Bottlenecks | -0.4% | East and West Africa | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Volatility in Recycled Paper Pulp Prices

Recovered-paper exports from South Africa to Asia lifted domestic prices in late 2024, trimming Mpact’s paper gross margin by 2.7% points despite volume gains. Urban collection networks funnel post-consumer fiber into export channels, leaving converters exposed to spot-market spikes when local mills compete for supply.[1]Mpact Group Limited, “Interim Results H1 2025,” mpact.co.zaEgypt’s early-stage EPR program magnifies feedstock pressure by stipulating recycled-content labeling without parallel rural collection infrastructure. Long-term contracts with aggregators partly hedge costs, but smaller converters lack bargaining power. Until incremental capacity from initiatives such as Polysmart’s USD 60 million Lagos plant stabilizes regional supply, pulp price swings will remain a material drag on the Africa folding carton market.

Skilled Technician Shortage Limiting Automation Uptake

African converters imported roughly USD 1.5 billion of packaging machinery in 2024, yet chronic shortages of maintenance engineers slow commissioning and lengthen downtime. Customs delays for servo motors and PLCs add three-to-six-month lags, eroding the return on capital-intensive upgrades. Supplier-led training and government technical colleges are expanding, but near-term skill gaps still cap achievable throughput and slow adoption of Industry 4.0 controls, restraining productivity gains across the Africa folding carton market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: SBS Gains on Premium Positioning

Folding Boxboard captured 38.43% of the African folding carton market in 2025, owing to its multi-ply architecture that balances rigidity and lightweighting. Solid Bleached Board is forecast to rise at an 8.06% CAGR, reflecting cosmetics and pharmaceutical brands’ preference for pristine whiteness and hygienic fiber. Coated Unbleached Kraftboard is gaining traction among organic and fair-trade food producers eager to showcase natural aesthetics, while White-lined Chipboard remains the value option for dry-goods cartons despite narrower margin buffers.

Mondi’s 253,000 hectares of FSC-certified forestry in South Africa secure a virgin fiber supply, supporting SBS availability and traceability claims.[2]Mondi Group, “Integrated Report 2025,” mondigroup.com Concurrently, South Africa’s recycled-content targets are stimulating investment in de-inking and dispersion systems that upgrade recovered fiber for food-grade applications, tightening the linkage between recycling infrastructure and material-mix evolution in the Africa folding carton industry.

By Printing Technology: Digital Disrupts Offset Dominance

Offset lithography accounted for 44.37% of the Africa folding carton market share in 2025, valued for its color fidelity on long runs. However, digital printing is poised to expand at an 8.78% CAGR through 2031 as converters deploy single-pass inkjet and liquid-toner systems that eliminate plate-generation steps. Cost parity with offset emerges at around 5,000 to 10,000 impressions, aligning with the proliferation of short-run e-commerce and seasonal promotions.

Kenya’s recyclability design guidelines and the East African Community’s DEAS 1259:2025 laminate standard promote the adoption of water-based inks, narrowing the technology gap between digital and offset printing for food-contact compliance. Start-ups such as Morocco’s EZPac leverage refurbished HP Indigo units to service flexible MOQs, encouraging a more distributed manufacturing footprint and enhancing responsiveness across the Africa folding carton market.

By End User Industry: Healthcare Leads Growth as Food Holds Volume

Food and beverages retained 46.32% of the Africa folding carton market share in 2025, supported by export-oriented citrus cartons and ready-to-eat meal packaging. Cartons specified for chilled and frozen foods rely on Folding Boxboard for stiffness at a lower basis weight. In parallel, the healthcare and pharmaceuticals segment is projected to compound at 8.62% through 2031, driven by the expansion of vaccine vial and blister-pack distribution networks across East Africa.

Solid Bleached Board’s inert, ultra-smooth surface meets stringent pharmacopeia print-legibility standards and enables anti-tamper embossing, positioning it as the preferred substrate. Regulatory mandates for serialized, tamper-evident packaging amplify demand for high-resolution offset or digital printing, reinforcing volume growth. Personal-care cartons, while smaller in tonnage, benefit from premium finishing processes such as foil stamping that command higher margins and diversify converter revenue.

Geography Analysis

South Africa held 51.63% of the Africa folding carton market in 2025, supported by Mpact’s vertically integrated mills and Mondi’s FSC-certified forestry estate. The Draft National Waste Management Strategy 2026 mandates rising recycled-content thresholds, pushing converters to secure urban fiber and invest in testing labs. Mpact’s Springs mill experienced 18 days of utility-related downtime in early 2025, underscoring infrastructure risk despite the country’s manufacturing depth.

Nigeria is forecast to grow at 8.25% CAGR to 2031, underpinned by a USD 2.28 billion printing and packaging sector in 2024 and a nationwide ban on single-use plastics starting January 2025. Polysmart’s USD 60 million recycling complex and machinery imports exceeding USD 1.2 billion in 2025 signal industrial-scale capacity building.[3]Packaging Market Insights, “Nigeria Printing and Packaging Market Outlook,” packagingmarketinsights.com Skilled-labor shortages, however, still constrain automation penetration, moderating productivity gains.

Egypt and the Rest of Africa combine regulatory momentum with foreign direct investment. Egypt’s per-kilogram plastic-bag levy hints at forthcoming carton levies that could boost mono-material adoption, while Kenya’s EPR fees on carton imports drive local sourcing. Morocco’s draft tourism-sector packaging decree incentivizes the use of recyclable cartons in luxury retail, and Tanzania’s digital press deployments broaden regional printing capacity. AfCFTA digital customs windows further ease cross-border carton flows, knitting together a continent-wide supply web that benefits scale players in the Africa folding carton market.

Competitive Landscape

The Africa folding carton market is moderately fragmented. Mpact leads the region with USD 740 million in revenue in 2025, integrating paper, converting, and recycling operations to buffer input-cost swings. Multinationals Mondi, Smurfit WestRock, Huhtamaki, and Sonoco leverage certified fiber sourcing and export compliance to service multinational brand owners. Smurfit WestRock’s 2025 footprint rationalization delivered USD 400 million in savings, allowing the redeployment of capital into high-growth African nodes.

Private equity funds enter the field, as illustrated by the African Development Bank’s USD 15 million commitment to SPE Capital’s packaging vehicle targeting growth-stage converters. Indigenous digital-printing start-ups such as EZPac and nimax-equipped Tanzanian firms compete on turnaround and customization, eroding incumbents’ small-run margins but also expanding overall demand. Technology investment focuses on single-pass inkjet presses, CEPI-aligned recyclability labs, and rooftop solar arrays that mitigate grid instability.

Compliance with South Africa’s recycled-content rules and Kenya’s EPR fees favors players with documented material provenance and producer-responsibility memberships. Guala Closures’ January 2026 acquisition of Metal Crowns adds metal-closure capacity in Nairobi and Dar es Salaam, creating co-location pull for carton suppliers targeting spirits packaging.[4]Ecofin Agency, “Guala Closures Expands in Africa,” ecofinagency.com Overall, strategic differentiation hinges on certified sustainability, regional logistics agility and capital access for automation upgrades.

Africa Folding Carton Industry Leaders

Arabian Packaging Ltd.

Tetra Pak International SA

Mondi plc

International Paper Company

Huhtamaki Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: African Development Bank approved a USD 15 million equity stake in SPE Capital’s packaging-focused private-equity fund.

- April 2026: Coleus Packaging invested ZAR 200 million (USD 13.2 million) in advanced coating and punching lines at its Johannesburg site.

- February 2026: Mondi Group published its 2025 integrated report highlighting 88% revenue from reusable or recyclable products.

- January 2026: Guala Closures announced plans to acquire Metal Crowns’ Nairobi and Dar es Salaam facilities, pending COMESA review.

Africa Folding Carton Market Report Scope

The scope of this report covers the analysis of the folding cartons market in Africa. Folding cartons are paper-based packaging solutions widely used across various industries, including food and beverage, personal care, pharmaceuticals, and others. The report examines market trends, growth drivers, challenges, and opportunities, providing insights into the current market dynamics and future projections.

The Africa Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries), and Geography (South Africa, Nigeria, Egypt, and Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

By Printing Technology

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

By End-User Industry

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

By Geography

| South Africa |

| Nigeria |

| Egypt |

| Rest of Africa |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries | |

| By Geography | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

Key Questions Answered in the Report

What is the current size of the Africa folding carton market and how fast is it growing?

The Africa Folding Carton Market size is expected to grow from USD 1.12 billion in 2025 to USD 1.21 billion in 2026 and is forecast to reach USD 1.72 billion by 2031 at 7.29% CAGR over 2026-2031.

What is the forecast growth rate for Nigeria’s folding carton sector?

Nigeria is projected to expand at an 8.25% CAGR through 2031, driven by e-commerce, quick-commerce and a nationwide ban on single-use plastics.

Which end-user segment is expected to grow fastest through 2031?

Healthcare and pharmaceuticals are forecast to lead with an 8.62% CAGR as cold-chain distribution and blister-pack needs rise.

Why is Solid Bleached Board gaining share in Africa?

Brands in cosmetics and pharmaceuticals favor its pristine white surface and hygienic virgin fiber, supporting an 8.06% CAGR outlook.

How are sustainability regulations shaping material choice?

Rising recycled-content mandates and EPR fees push converters toward mono-material paperboard and documented recycled fiber usage.

What technology trend is disrupting traditional offset printing volumes?

Single-pass digital inkjet presses offer plate-free, rapid changeovers that capture the growing demand for short-run, customized cartons.

Page last updated on: