HCM Software In The BFSI Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

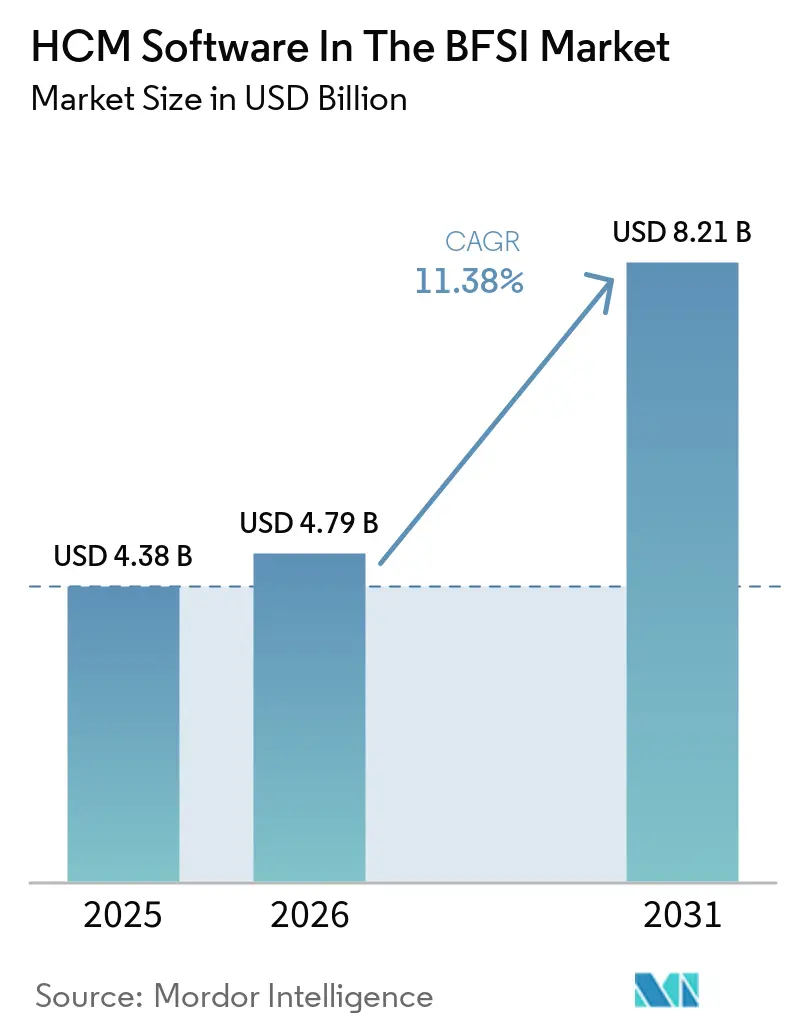

| Market Size (2026) | USD 4.79 Billion |

| Market Size (2031) | USD 8.21 Billion |

| Growth Rate (2026 - 2031) | 11.38% CAGR |

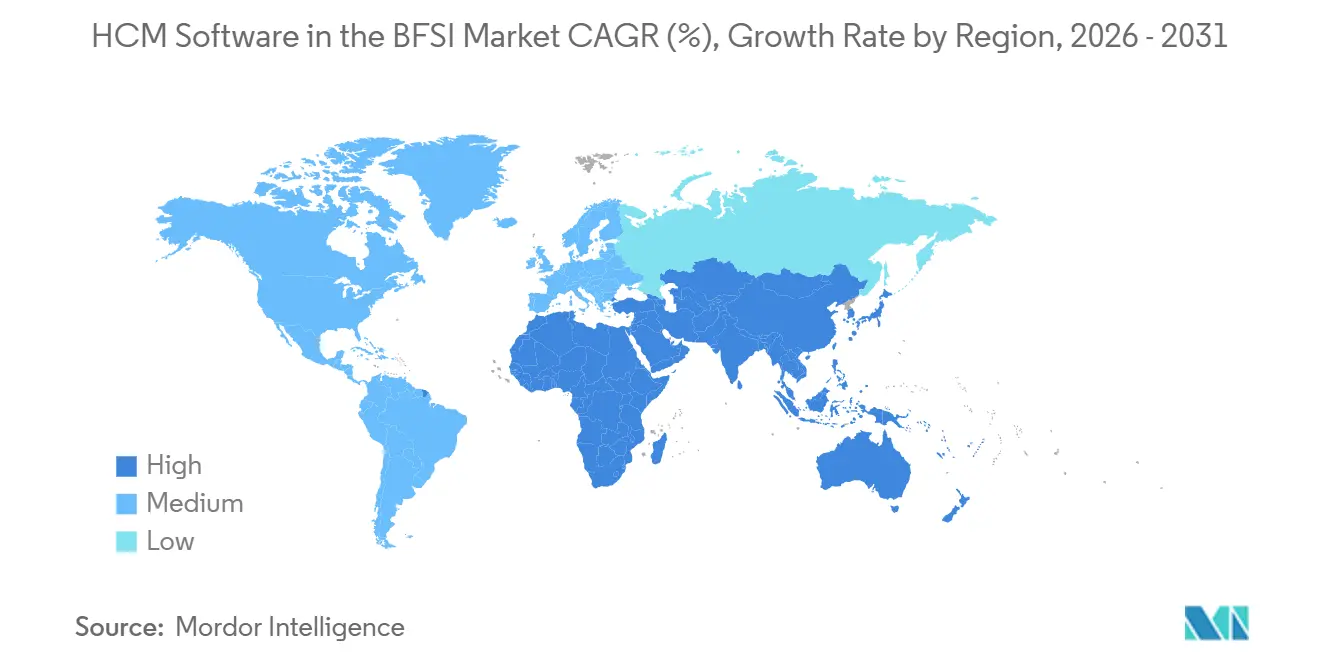

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HCM Software In The BFSI Market Analysis by Mordor Intelligence

The HCM software in the BFSI market size is expected to increase from USD 4.38 billion in 2025 to USD 4.79 billion in 2026 and reach USD 8.21 billion by 2031, growing at a CAGR of 11.38% over 2026-2031. The uptrend reflects financial institutions’ pivot from compliance-reactive toolkits toward predictive workforce-intelligence platforms that embed jurisdiction-specific rules at the data layer. Board-level scrutiny of cross-border labor costs, algorithmic-decision transparency, and real-time audit trails is forcing banks to retire mainframe-era on-premise suites and adopt API-first cloud architectures. Tier-1 banks now treat workforce data as strategic capital-allocation input rather than a historical cost ledger, while digital-only lenders embed HCM services alongside core banking stacks from day one. Vendor differentiation has therefore shifted to pre-built regulatory libraries, immutable audit logs, and conversational AI that short-circuits traditional business-intelligence bottlenecks.

Key Report Takeaways

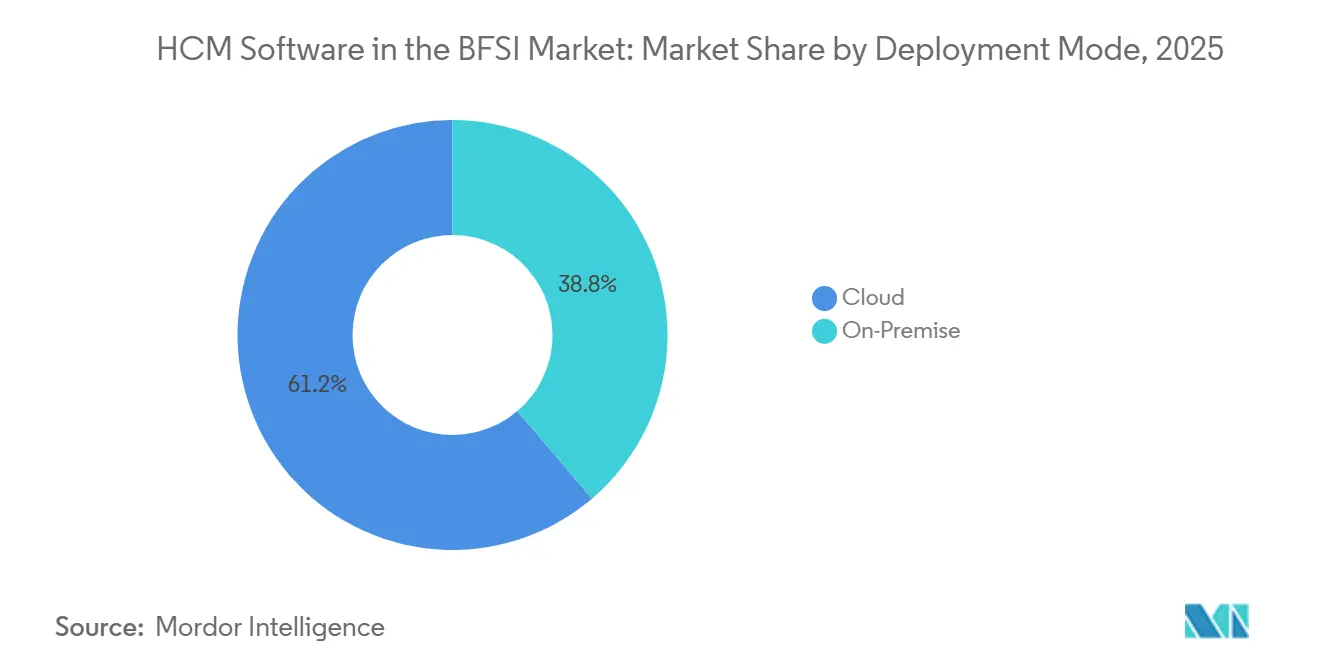

- By deployment mode, cloud commanded 61.23% share of the HCM software in the BFSI market in 2025 and is on track to grow at an 11.82% CAGR through 2031, fueled by the Digital Operational Resilience Act and similar mandates that reward native audit-log functionality

- By organization size, large enterprises accounted for 58.23% of revenue in 2025, but small and medium enterprises are expanding at an 11.89% rate as digital-only banks adopt SaaS HCM solutions from inception to bypass legacy constraints.

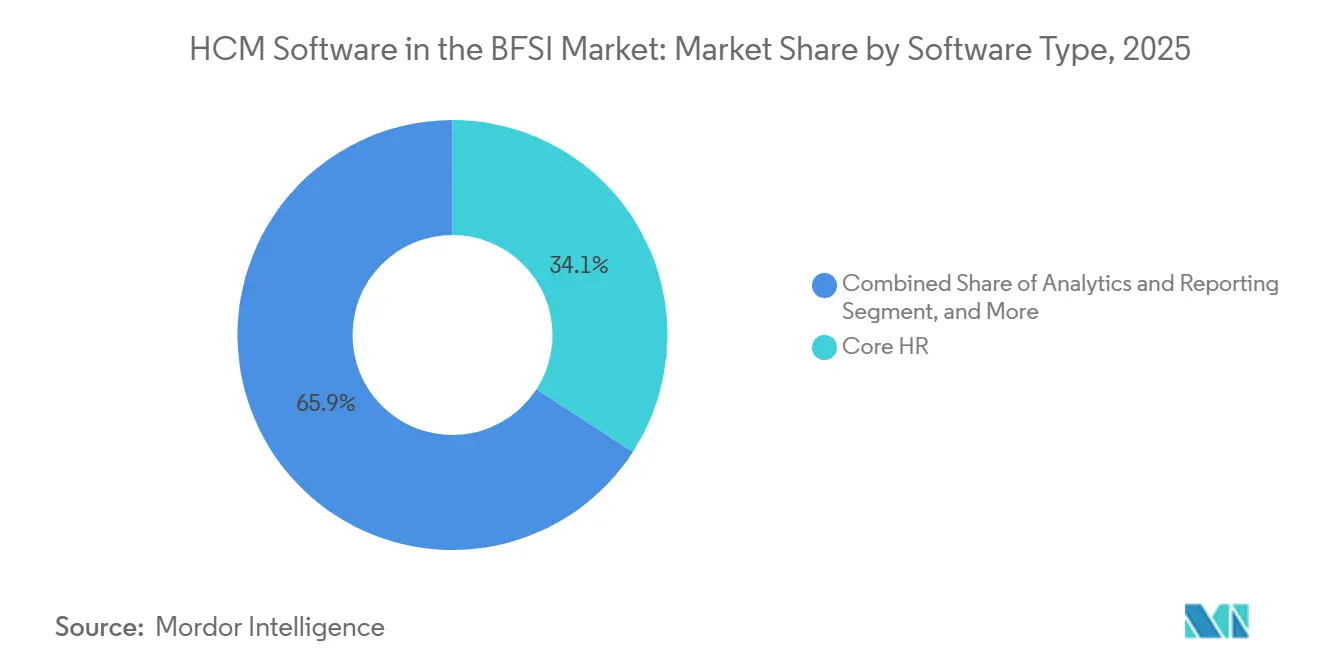

- By software type, core HR captured 34.19% of 2025 revenue, while analytics modules are accelerating at 12.43% due to Basel III Pillar 3 disclosure rules that demand granular workforce-cost transparency.

- By services, implementation and integration accounted for 46.13% of 2025 spending, yet managed services are climbing at 13.11% as banks outsource evergreen compliance monitoring.

- By geography, North America led with a 38.42% share in 2025, while Asia-Pacific was the fastest-growing region at 13.12%, propelled by rapid neobank proliferation across India, Indonesia, and the Philippines.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HCM Software In The BFSI Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Regulatory Complexity in Global Financial Services | +2.8% | Global, peak in EU, UK, North America | Medium term (2-4 years) |

| Accelerated Cloud Adoption by Tier-1 Banks | +2.5% | North America and Europe, rapid in Asia-Pacific | Short term (≤ 2 years) |

| Integration of AI-Powered Compliance Analytics | +2.1% | North America, Europe, Singapore, Hong Kong | Medium term (2-4 years) |

| Shift to Employee Experience-Centric HR Models | +1.6% | Global, early in North America and Western Europe | Long term (≥ 4 years) |

| Demand for Real-Time Payroll and Earned Wage Access | +1.3% | North America, UK, emerging Asia-Pacific | Short term (≤ 2 years) |

| Expansion of Digital-Only Financial Institutions | +1.1% | Asia-Pacific, South America, Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Regulatory Complexity in Global Financial Services

Financial regulators now weave workforce-data governance directly into prudential frameworks, turning HCM suites into front-line compliance systems. The EU Digital Operational Resilience Act obliges banks to map every third-party HR service provider and maintain exit strategies, a task suited to cloud platforms with immutable audit logs. Basel III Pillar 3 updates demand real-time reconciliation of payroll, benefits, and contractor spend, driving uptake of analytics modules. In the United States, New York’s Part 500 cybersecurity amendments extend encryption requirements to HR databases, lifting the compliance bar for vendors serving U.S.-regulated entities. This patchwork rewards providers that maintain jurisdiction-specific rule libraries, leaving smaller regional players scrambling for legal-engineering resources.[1]New York State Department of Financial Services, “Cybersecurity Requirements for Financial Services Companies,” DFS.NY.GOV

Accelerated Cloud Adoption by Tier-1 Banks

Total-cost-of-ownership studies increasingly favor subscription-based cloud HCM over data-center refresh cycles. BNY Mellon’s multi-year Workday rollout unified global payroll across 35 countries and trimmed month-end close by 40%, validating large-scale SaaS migration economics. In the Philippines, Chinabank Savings deployed Darwinbox, cutting branch-staff onboarding time by 40% and showcasing a mobile-first paradigm suited to emerging markets. These examples underscore how cloud HCM enables real-time workforce analytics that guide capital-allocation decisions, from branch rationalization to digital-channel staffing.

Integration of AI-Powered Compliance Analytics

Vendors now embed regulatory logic into AI agents that automate pay equity audits, overtime checks, and the generation of disclosures. SAP SuccessFactors’ 1H 2026 release introduced natural-language queries, such as “show staff whose overtime breaches local thresholds,” eliminating the need for bespoke scripting.[2]SAP, “SAP SuccessFactors 1H 2026 Release,” NEWS.SAP.COM Oracle’s AI agents flag compensation gaps that could violate the EU Pay Transparency Directive. Workday’s November 2025 acquisition of Sana Labs added conversational AI that converts executive questions into SQL queries against workforce data, shortening board report cycles. Such tools shift compliance from retrospective audits to real-time prevention.[3]Oracle, “Oracle Fusion Cloud HCM AI Agents,” ORACLE.COM

Shift to Employee Experience-Centric HR Models

Banks increasingly position HCM platforms as talent-retention levers amid shortages in cybersecurity, data science, and wealth-management expertise. Workday’s Spring 2025 update delivered personalized learning paths and internal gig marketplaces, fostering lateral mobility. UKG’s venture arm invested in Financial Wellness Labs, betting that integrated budgeting tools can ease early-career financial stress and curb attrition. A 2025 Jack Henry survey revealed that 68% of bank CEOs view talent scarcity as the primary obstacle to digital transformation, reinforcing the business case for experience-focused HCM.[4]Workday Investor Relations, “Workday to Acquire Sana Labs,” INVESTOR.WORKDAY.COM

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Data Residency and Sovereignty Requirements | -1.4% | EU, China, Russia, India, Middle East | Long term (≥ 4 years) |

| Legacy Core Banking System Integration Challenges | -1.2% | Global, acute in North America and Europe | Medium term (2-4 years) |

| High Switching Costs for Large Financial Institutions | -0.9% | Global | Long term (≥ 4 years) |

| Cybersecurity and Fraud Risks in HR Data | -0.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Data Residency and Sovereignty Requirements

Data-localization mandates are fragmenting the addressable market into regional islands. China’s Personal Information Protection Law requires banks to store employee data on mainland servers, prompting multinationals to maintain parallel HR instances. Russia’s 152-FZ imposes similar constraints, pushing Western vendors toward local hosting partners. India’s draft Digital Personal Data Protection Act, expected in 2026, would further restrict outbound data flows. These rules inflate vendor costs and complicate global platform harmonization.

Legacy Core Banking System Integration Challenges

Many banks continue to operate COBOL-based cores that lack modern APIs for bidirectional HR data exchange. Temenos T24 integrations often require bespoke middleware costing up to USD 2 million and adding 6–12 months to deployment. Oracle FLEXCUBE users sometimes rely on batch files for payroll feeds, undermining real-time analytics. A 2025 Finastra study found that 63% of surveyed banks identified HR system integration as a top obstacle to core modernization. These hurdles slow the adoption of next-generation HCM capabilities and perpetuate dual-system architectures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Platforms Capture Tier-1 Mandates

The cloud slice of the HCM software market in the BFSI sector accounted for 61.23% in 2025 and is forecast to grow at a 11.82% CAGR through 2031. Leading global banks selected cloud suites to meet DORA audit requirements and gain real-time workforce insights, while hybrid adoption ensures compliance, scalability, and resilience, driving long-term modernization across financial institutions worldwide.

Cloud adoption accelerates as banks retire mainframe-era HR engines; BNY Mellon and Chinabank Savings demonstrated 40% cycle-time reductions post-migration. Hybrid models bridge gaps where strict data-sovereignty rules persist, allowing analytics layers to reside in the cloud while sensitive payroll tables stay on-premise. This flexibility sustains momentum until universal API adoption removes integration bottlenecks.

By Organization Size: SME Segment Accelerates Through Digital-Only Lenders

Large enterprises commanded 58.23% of revenue in 2025, reflecting their dominance in the BFSI HCM market. Their scale allows them to negotiate bundled contracts and integrate complex modules across payroll, compliance, and workforce planning. However, growth is slowing as saturation sets in, with future expansion tied more to regulatory upgrades and advanced analytics than to fresh deployments.

SMEs in the market are advancing at an 11.89% CAGR, driven by digital-only lenders and community banks that deploy SaaS platforms from the outset. Levo Credit Union adopted Paylocity in 2026 to integrate earned-wage access, while Ujjivan Small Finance Bank leverages vernacular interfaces to reach rural talent pools. Faster procurement cycles and reduced customization burdens enable SMEs to roll out upgrades in weeks, positioning them as durable growth engines.

By Software Type: Analytics Modules Surge On Reporting Mandates

Core HR accounted for 34.19% of 2025 revenue, anchoring the HCM software in the BFSI market size by serving as the foundation for employee records and compliance. Its centrality ensures stability, but growth momentum is shifting elsewhere. Analytics and reporting modules are the fastest-rising segment, expanding at a 12.43% CAGR through 2031, as Basel III rules demand granular workforce-cost disclosure and transparent capital planning.

Workday Data Cloud and Oracle AI audits exemplify this shift, linking headcount metrics directly to capital allocation decisions and creating new feedback loops for CFOs. Payroll engines remain indispensable for disbursement accuracy, yet commoditization pressures are evident. Meanwhile, talent and workforce-management add-ons are emerging as premium differentiators, enabling banks and insurers to justify higher price points by embedding advanced recruitment, retention, and performance features into their HCM suites.

By Services: Managed Services Rise As Compliance Monitoring Outsources

Implementation and integration services accounted for 46.13% of 2025 spending, highlighting the complexity of data migration and the need for specialized expertise to harmonize legacy systems with modern HCM platforms. Managed services, however, are climbing at a 13.11% CAGR as institutions increasingly outsource continuous rule updates to specialists, converting unpredictable compliance costs into stable operating expenses while ensuring regulatory accuracy and system uptime.

Zalaris assumed quarterly tax updates for a 16,000-employee bank in Central Europe, proving the appeal of turning capex into predictable opex. Systems integrators now pitch annuity-based support contracts that align incentives around uptime and regulatory accuracy, deepening vendor-client entanglement across the HCM software in the BFSI market.

Geography Analysis

North America led the HCM software market in BFSI during 2025, driven by stringent cybersecurity rules and early SaaS adoption. BNY Mellon’s Workday rollout and Levo Credit Union’s Paylocity deployment illustrate how both top-tier and mid-tier institutions prioritize unified payroll and earned-wage access. Canada’s provincial labor-law variations and Mexico’s electronic payroll mandates add incremental demand.

Asia-Pacific is the fastest-growing region through 2031, fueled by rapid neobank proliferation and regulatory harmonization across ASEAN. Chinabank Savings, Tamilnad Mercantile Bank, and Ujjivan Small Finance Bank showcase mobile-first deployments that cut onboarding times and automate localized tax compliance. China’s data-localization rules fragment the landscape but create opportunities for domestic cloud providers, while India’s upcoming data-protection act will further boost demand for region-specific instances.

Europe balances aggressive cloud migration with strict oversight of data sovereignty. DORA drives platform upgrades, while GDPR and national residency rules slow cross-border standardization. Zalaris’ managed-services deal highlights appetite for outsourcing compliance. South America’s growth is steadier as banks weigh currency volatility, and the Middle East and Africa are opening via mobile-native vendors such as NexHRM and Ramco that integrate with local payment rails.

Competitive Landscape

The HCM software market in BFSI shows moderate concentration, with global ERP vendors such as Workday, SAP, and Oracle dominating multinational banks through bundled contracts that include finance modules. Pure-play providers like UKG, Ceridian, and ADP win mid-tier clients by shipping faster and embedding niche compliance libraries.

Technology differentiation now hinges on AI-driven compliance analytics and open APIs that integrate with core banking platforms. Workday’s Sana acquisition embedded conversational AI that turns natural-language prompts into SQL reports, cutting board-pack preparation from days to hours. SAP SuccessFactors integrated SmartRecruiters to surface internal candidates before external searches, reducing time-to-fill by 28 days.

Regional challengers exploit localization gaps: Darwinbox and Ramco succeed in Asia-Pacific with vernacular interfaces, while NexHRM addresses African banks needing offline payroll modes. Vendors that can quantify regulatory-penalty avoidance through real-time violation alerts often win competitive tenders, even against feature-rich incumbents.

HCM Software In The BFSI Industry Leaders

SAP SE

Workday Inc.

Oracle Corporation

UKG Inc.

Ceridian HCM Holding Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Paycom reported Q1 2026 results, citing 35% lower HR service-desk volume at BFSI clients after launching its IWant AI feature set.

- April 2026: AP released SuccessFactors 1H 2026, adding AI agents that cut regulatory-reporting cycle times by 50% for early-adopter banks.

- April 2026: Paycom secured a USD 2.125 billion revolving credit facility to fund AI-compliance acquisitions.

- April 2026: NexHRM launched a cloud HCM suite for African banks with mobile-money integration.

Global HCM Software In The BFSI Market Report Scope

The HCM Software in the BFSI Market refers to human capital management platforms and related services used by banks, financial institutions, and insurance companies to manage workforce operations, payroll, recruitment, compliance, performance management, employee engagement, learning, and workforce analytics. These solutions support regulatory reporting, cybersecurity compliance, talent retention, and operational efficiency within highly regulated financial environments. The market includes cloud based and on premises software, implementation and managed services, and AI driven workforce analytics tools designed to optimize employee productivity, automate HR processes, and strengthen workforce governance across global and regional BFSI organizations.

The HCM Software in the BFSI Market Report is Segmented by Deployment Mode (Cloud, On-Premise), Organization Size (Large Enterprises, Small and Medium Enterprises), Software Type (Core HR, Payroll Management, Talent Management, Workforce Management, and Analytics and Reporting), Services (Implementation and Integration Services, Consulting and Training Services, and Managed Services), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-Premise |

| Large Enterprises |

| Small and Medium Enterprises |

| Core HR |

| Payroll Management |

| Talent Management |

| Workforce Management |

| Analytics & Reporting |

| Implementation and Integration Services |

| Consulting and Training Services |

| Managed Services |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Software Type | Core HR | |

| Payroll Management | ||

| Talent Management | ||

| Workforce Management | ||

| Analytics & Reporting | ||

| By Services | Implementation and Integration Services | |

| Consulting and Training Services | ||

| Managed Services | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current market size of HCM Software In The BFSI Market?

The HCM software in the BFSI market size stands at USD 4.79 billion in 2026, rising from USD 4.38 billion in 2025.

Which deployment mode is growing fastest among financial institutions?

Cloud deployment is growing the quickest, registering an 11.82% CAGR through 2031 as banks adopt API-first architectures for regulatory audit readiness.

Why are analytics modules gaining traction within HR suites?

Basel III Pillar 3 rules require granular, line-of-business workforce-cost disclosure, pushing banks to add analytics and reporting modules that automate real-time reconciliation.

How do data-sovereignty laws affect vendor strategy?

Local residency mandates in China, Russia, India, and the Middle East force vendors to maintain jurisdiction-specific instances, increasing infrastructure costs and limiting cross-border harmonization.

Which regions present the strongest growth opportunities?

Asia-Pacific leads with a 13.12% CAGR through 2031, driven by neobank expansion and regulatory alignment across ASEAN markets.

What differentiates leading vendors in this space?

Providers that embed AI-driven compliance analytics, maintain robust API ecosystems, and offer managed services for continuous rule updates win competitive bids over feature-parity rivals.

Page last updated on: