Saudi Arabia Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

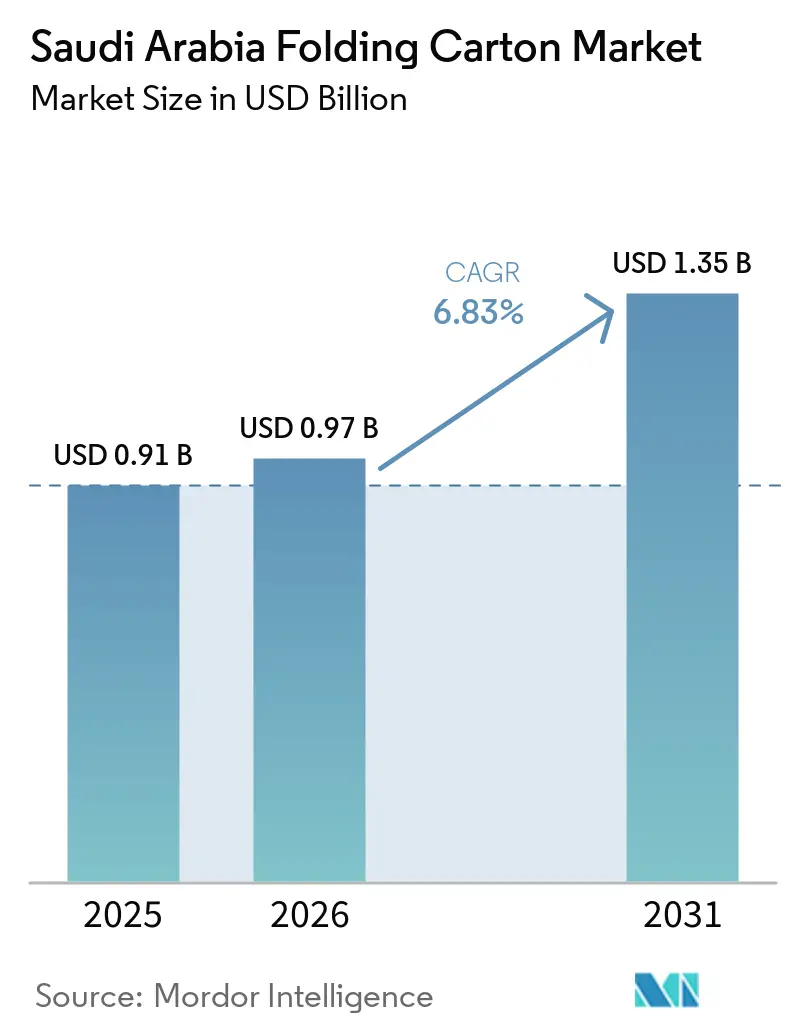

| Base Year Market Size (2025) | USD 0.91 Billion |

| Market Size (2026) | USD 0.97 Billion |

| Market Size (2031) | USD 1.35 Billion |

| Growth Rate (2026 - 2031) | 6.83% CAGR |

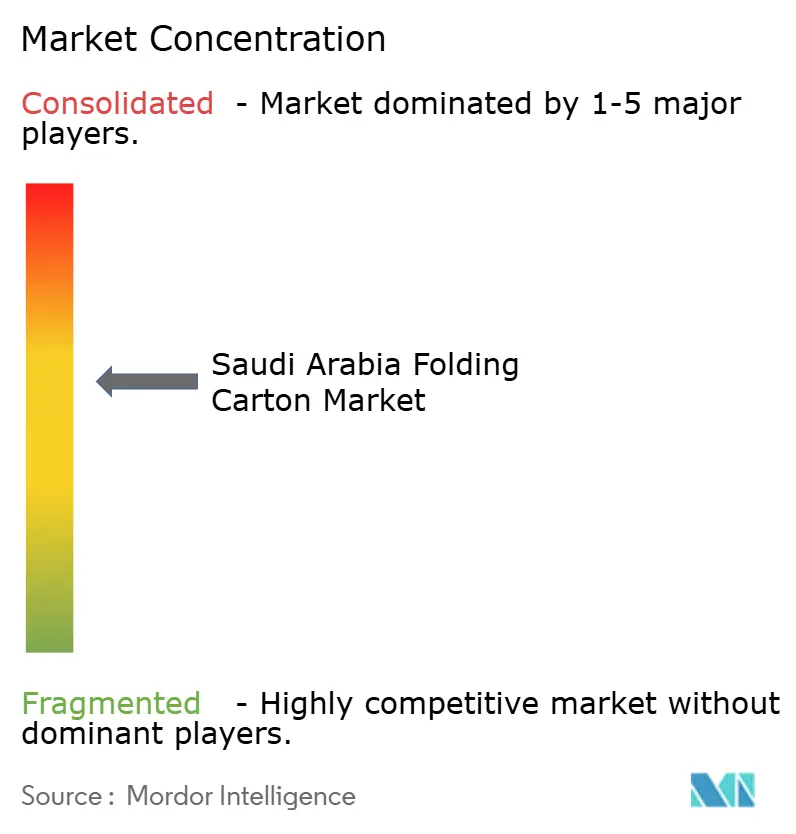

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Folding Carton Market Analysis by Mordor Intelligence

The Saudi Arabia folding carton market size was valued at USD 0.91 billion in 2025 and estimated to grow from USD 0.97 billion in 2026 to reach USD 1.35 billion by 2031, at a CAGR of 6.83% during the forecast period (2026-2031). Robust growth reflects the government’s National Industrial Strategy, which prioritizes converting capacity, offers 30-year zero-tax incentives to multinationals, and channels investment into secondary packaging hubs in Riyadh, Jeddah, and Dammam. Brand owners are adopting paperboard to comply with single-use-plastic regulations and reduce carbon footprints, while e-commerce platforms require right-sized, retail-ready cartons for automated fulfillment. Capacity additions such as MEPCO’s PM5 line and Obeikan Folding Carton’s five-offset-press complex widen domestic supply, lowering freight exposure and reinforcing sustainability credentials. Competitive pressure is rising as regional entrants build greenfield plants and incumbents integrate vertically to secure paperboard feedstock, digital workflows, and premium finishing.

Key Report Takeaways

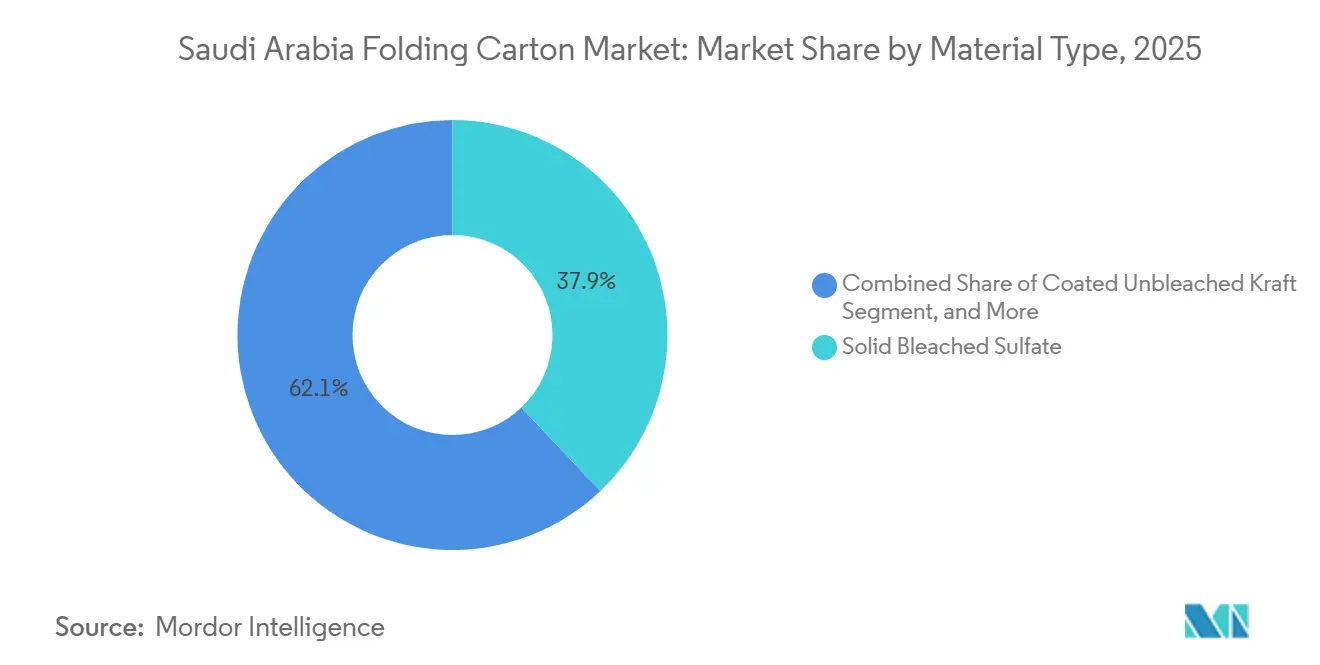

- By material type, solid bleached sulfate captured with 37.92% of the Saudi Arabia folding carton market share in 2025.

- By printing technology, the Saudi Arabia folding carton market size for digital printing is projected to grow at a 8.63% CAGR to 2031.

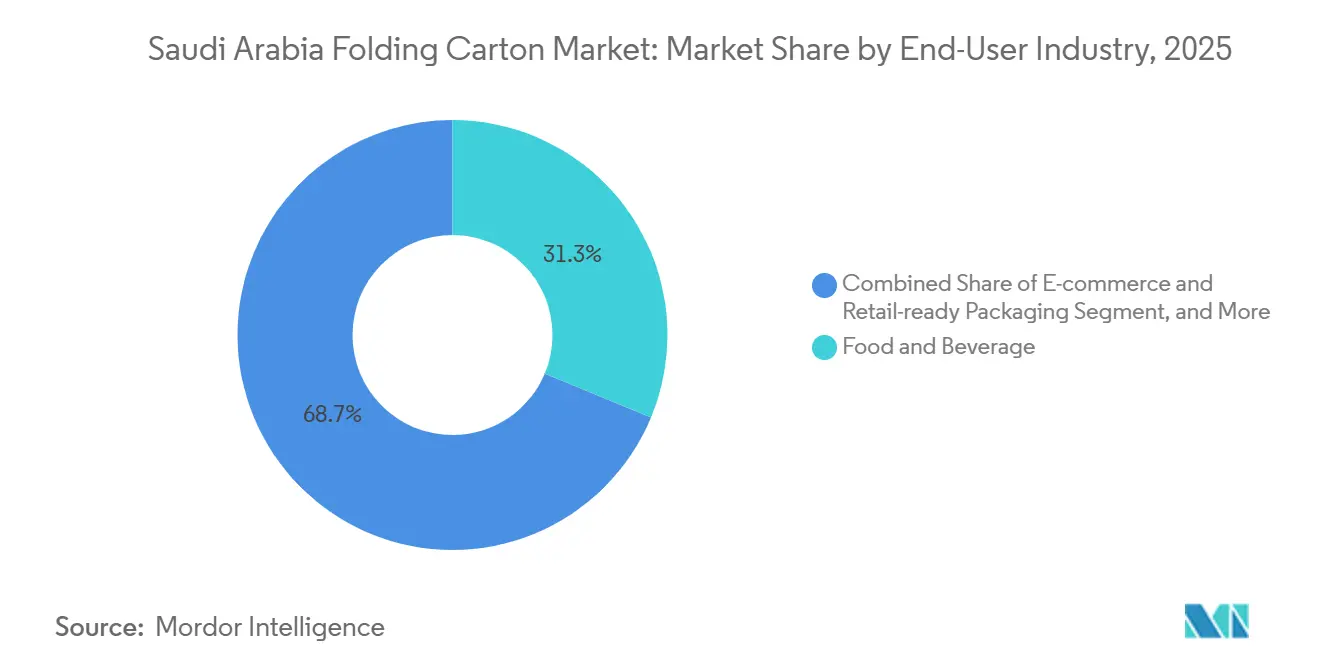

- By end-user industry, the food and beverage industry captured 31.27% of the Saudi Arabia folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Push for Local Manufacturing Under Saudi Vision 2030 | +2.1% | National, clustering in Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Rising Penetration of E-Commerce Platforms | +1.8% | National, strongest in major metros | Short term (≤ 2 years) |

| Expansion of Quick-Service Restaurant Chains | +1.2% | National, spill-over to GCC | Medium term (2-4 years) |

| Growing Demand for Premium Packaging in Confectionery Gifts | +0.7% | National, seasonal peaks | Short term (≤ 2 years) |

| Shift Toward Recyclable Mono-Material Packaging | +0.9% | National | Long term (≥ 4 years) |

| Integration of Digital Watermarks for Smart Sorting | +0.4% | Pilot projects in Riyadh and Jeddah | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Push for Local Manufacturing Under Saudi Vision 2030

Localization incentives under Vision 2030 reward converters that set up factories near food and pharma clusters, providing accelerated permitting, subsidized land, and higher local-content scores in government tenders. The Ministry of Industry signed an MoU with Sidel in May 2025 to evaluate made-in-Saudi packaging equipment, lowering the total cost of ownership for new lines.[1]FairsOnline, “Saudi Arabia and Sidel sign strategic MoU,” fairsonline.org Combined with MEPCO’s incoming 450,000 tons per year paperboard stream, these policies reduce reliance on imports and shorten lead times.

Rising Penetration of E-Commerce Platforms

In 2024, online sales surged to USD 52.64 billion, fueling a heightened demand for lightweight boxes, tamper-evident closures, and variable-data printing on return labels. Responding to this trend, Noon and Amazon Saudi Arabia have mandated the use of FSC-certified boards and QR codes for recycling instructions. This has led converters to channel investments into digital presses and on-demand box makers, enabling them to produce right-sized formats at an accelerated fulfillment speed.

Expansion Of Quick-Service Restaurant Chains

Chains such as Kudu and Sushi Sushi require grease-resistant, microwave-safe cartons, driving uptake of aqueous barrier coatings that replace polyethylene layers. Converter margins depend on automating folder-gluers and waste-reduction systems that can meet QSR price points without sacrificing food-contact compliance set by SASO. However, QSR chains' price sensitivity and high-volume procurement create margin pressure, favoring converters with automated folder-gluer systems and waste-minimization workflows that deliver sub-10% spoilage rates.

Shift Toward Recyclable Mono-Material Packaging

SASO's new regulation on degradable plastics is accelerating the shift to paper in the snacks, produce, and dairy sectors. Initiatives such as RIYcycle, a joint recycling facility backed by a USD 3.2 million investment, underscore the advantages of circular models, especially those that prioritize mono-material folding cartons. Meanwhile, MEPCO's recovery network is providing recycled fiber, helping brands meet their carbon-reduction goals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Virgin Fiber Pulp Prices | -1.3% | National, import-dependent | Short term (≤ 2 years) |

| Capital-Intensive Nature of High-Color Litho Presses | -0.9% | Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Limited Availability of FSC-Certified Wood in the GCC | -0.6% | Regional | Long term (≥ 4 years) |

| Rising Popularity of Rigid Boxes in Luxury Goods | -0.5% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility In Virgin Fiber Pulp Prices

Converters, lacking domestic pulp mills, turn to Nordic and North American suppliers. This reliance makes them vulnerable to fluctuations in freight costs and currency values. In 2025, a 15% surge in raw material costs compelled converters to either hedge their inventories or increase prices, particularly in sensitive food markets. While MEPCO’s recycled grades meet containerboard demand, they leave SBS and CUK without coverage.

Capital-Intensive Nature of High-Color Litho Presses

Smaller converters face challenges in upgrading due to the high cost, exceeding USD 5 million, of a seven-color offset press with inline coating. The closure of Manroland's factory in May 2026 raised concerns over parts supply. This led to stockpiling and a shift towards vendors offering regional services. However, the 12-18-month lead times from these vendors have hindered timely modernization efforts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Coated Unbleached Kraft Gains on Lightweighting

Solid Bleached Sulfate commanded 37.92% of the Saudi Arabia folding carton market share in 2025. Premium printability secures its role in pharma and cosmetics, but its price premium leaves room for alternatives. Coated Unbleached Kraft is forecast to rise at 9.34% CAGR through 2031, driven by e-commerce mailers and QSR meal boxes that value tear resistance over brightness. The Saudi Arabia folding carton market size for lightweight containerboard is expanding as MEPCO’s PM5 will produce 70-90 GSM grades, enabling converters to reduce board grammage while maintaining crush strength.

FSC compliance remains a bottleneck because certified fiber must travel from Nordic mills, which adds cost and increases lead-time risk.[2]SGS, “Guide to FSC Chain of Custody Certification in the Gulf Region,” sgs.com Volume growth also favors micro-flute corrugated added to folding-carton lines to meet parcel-shipping tests. Converters with in-house aqueous barrier and bio-based coatings replace PE laminates, supporting SASO food-safety mandates and enhancing recyclability. Solid Bleached Sulfate will remain dominant for luxury gifting during Ramadan and Eid, yet CUK’s alignment with sustainability, cost, and logistics makes it the structural growth engine.

By Printing Technology: Digital Printing Captures Serialization And Short Runs

Lithographic Printing held 43.61% of the Saudi Arabia folding carton market share in 2025, favored for long runs and color fidelity demanded by global FMCG brands. Offset’s economics remain compelling above 10,000 units, and existing press fleets continue to amortize. However, Digital Printing is growing at 8.63% CAGR, capturing pharma serialization, limited-edition SKUs, and e-commerce personalization. HP Indigo and Durst presses now top 100 m/min, narrowing the gap to offset, while variable-data workflows meet Saudi Food and Drug Authority tracking codes.

Hybrid lines that marry flexo bases, inkjet personalization, and inline die-cutting provide turnkey agility. Converters attending Labelexpo 2025 signed eight hybrid-press deals, signaling a shift toward automation, SKU agility, and waste reduction. Lithographic Printing will persist in high-volume cereal and detergent cartons, but digital’s penetration in healthcare, luxury, and on-demand fulfillment will continue to erode offset’s exclusive hold.

By End-User Industry: E-Commerce Reshapes Packaging Specifications

Food and Beverage contributed 31.27% of Saudi Arabia folding carton market size in 2025, anchored by dairy, confectionery, and poultry clusters financed under Vision 2030. QSR growth multiplies demand for grease-resistant clamshells and cup carriers. Yet E-commerce and retail-ready packaging is projected to grow at 8.21% CAGR, fueled by 19 million online shoppers and automated fulfillment centers that specify right-sized, void-minimizing cartons with tamper-evident seals. Healthcare requires high-barrier SBS with child-resistant closures, while personal care brands adopt soft-touch laminates and foils.

Electrical goods prioritize anti-static coatings and protective inserts, a niche where micro-flute integration can displace foam. Platform pressures extend beyond volume: Noon and Amazon Saudi Arabia require FSC labels and QR-based recycling guidance, pushing converters to upgrade digital workflows that merge sustainability documentation with graphics. Tetra Pak’s aluminum-free barrier carton, debuting in January 2026, illustrates how liquid-food formats converge with folding-carton technology, offering converters a path to future diversification.

Geography Analysis

Riyadh anchors the largest concentration of folding-carton capacity, housing Obeikan Folding Carton’s 50,000-ton-per-year complex and MEPCO’s integrated mill, both benefiting from proximity to government procurement and to dense food-processing clusters. Jeddah, the import gateway, hosts Nestlé’s USD 71.98 million plant, Tetra Pak’s aseptic line, and a luxury-goods hub that demands high-gloss cartons for confectionery and cosmetics.

Seasonal pilgrim influx in Makkah and Medina inflates demand for water, dates, and gift packs by up to 60% during Hajj and Umrah peaks. The Eastern Province, Dammam and Jubail, supports petrochemical complexes, pharmaceutical producers, and Napco National’s headquarters, supplying both domestic and GCC export markets via the King Fahd Causeway. United Carton Industries continues to expand a SAR 74 million (USD 19.73 million) plant in Ras Al Khaimah to serve cross-border demand while leveraging Saudi tax incentives.

The Northern and Southern regions, including NEOM and the Red Sea projects, are emerging hubs for protective cartons in construction, hospitality, and desalination equipment, though converter presence remains sparse. Regionally, Saudi Arabia commands roughly 25% of Middle East folding-carton demand, a share expected to rise as localization incentives lure multinationals from Dubai to Riyadh headquarters, reversing historical supply chains and concentrating future converting assets inside the Kingdom.[3]Towards Packaging, “Middle East folding carton packaging market size,” towardspackaging.com

Competitive Landscape

Competition is moderately concentrated. The top five converters, Obeikan Folding Carton, Napco National, MEPCO, United Carton Industries, and Tetra Pak Arabia, held an estimated 50-55% Saudi Arabia folding carton market share in 2025. Obeikan’s five-offset-press hub provides seven-color inline coating, embossing, and foiling, enabling service to cosmetics and pharma clients requiring strict color management.

Napco National’s August 2025 acquisition of Arabian Flexible Packaging broadened its substrate mix, supporting a one-stop supply for FMCG brands. MEPCO’s SAR 1.78 billion (USD 474.67 million) PM5 will double containerboard output to 875,000 tons per year by Q4 2027, integrating upstream board supply and driving cost advantages.[4]Sustainability Middle East and Africa, “Napco National acquires Arabian Flexible Packaging,” sustainabilitymea.com Strategic focus clusters around automation, sustainability certification, and hybrid press workflows.

Obeikan’s Microsoft Intelligent Manufacturing Award in 2025 signals digital-plant leadership, using predictive maintenance and real-time tracking to achieve sub-15-minute makeready. Hotpack’s planned USD 266.6 million sustainable-packaging plant threatens to blur boundaries between flexible and rigid substrates, intensifying price rivalry. Small converters, numbering more than 20, compete on regional distribution and 24-hour lead times but face capital constraints that hinder digital adoption, suggesting future consolidation.

Saudi Arabia Folding Carton Industry Leaders

Al Watania for Industries

Arabian Paper Products Co.

International Paper Company

Napco National CJSC

Obeikan Investment Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: MEPCO broke ground on PM5, investing SAR 1.78 billion (USD 474 million) to add 450,000 tons per year of lightweight board capacity by Q4 2027, doubling total output.

- March 2026: United Carton Industries posted Q1 net profit of SAR 24.2 million (USD 6.45 million) and approved a SAR 74 million (USD 19.73 million) expansion in Ras Al Khaimah.

- January 2026: Tetra Pak launched aluminum-free barrier cartons from its Jeddah facility, raising renewable content to 87% and enhancing recyclability.

- August 2025: Napco National acquired Arabian Flexible Packaging via Dubai subsidiary Napco Investment LLC for an undisclosed sum, extending into rotogravure substrates.

Saudi Arabia Folding Carton Market Report Scope

The Saudi Arabia Folding Carton Market encompasses the production, distribution, and application of folding cartons, paper-based packaging solutions designed for a variety of consumer and industrial goods. This report includes an analysis of key market dynamics, trends, and forecasts specific to Saudi Arabia.

The Saudi Arabia Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the 2026 value of the Saudi Arabia folding carton market?

The Saudi Arabia folding carton market size is projected at USD 0.97 billion in 2026, with a CAGR of 6.83% through 2031.

Which material type is expanding fastest in Saudi folding cartons?

Coated Unbleached Kraft is forecast to grow at a 9.34% CAGR through 2031, outpacing Solid Bleached Sulfate by 2.5 percentage points.

Why are digital presses gaining traction among Saudi converters?

Pharmaceutical serialization, e-commerce personalization, and shorter promotional runs require variable-data printing that digital platforms deliver more flexibly than offset.

How will MEPCO’s PM5 line affect local supply?

PM5 will add 450,000 tons per year of lightweight containerboard by Q4 2027, reducing import reliance and supporting downgauged folding-carton designs.

Which region hosts the largest folding-carton capacity in the Kingdom?

Riyadh leads capacity thanks to government procurement, dense food-processing clusters, and proximity to e-commerce fulfillment hubs.

What strategic moves are converters making to remain competitive?

Leading firms are integrating upstream paperboard supply, acquiring flexible-packaging assets, and installing hybrid presses to balance long-run efficiency with short-run agility.

Page last updated on: