Orthopedic Soft Tissue Repair Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

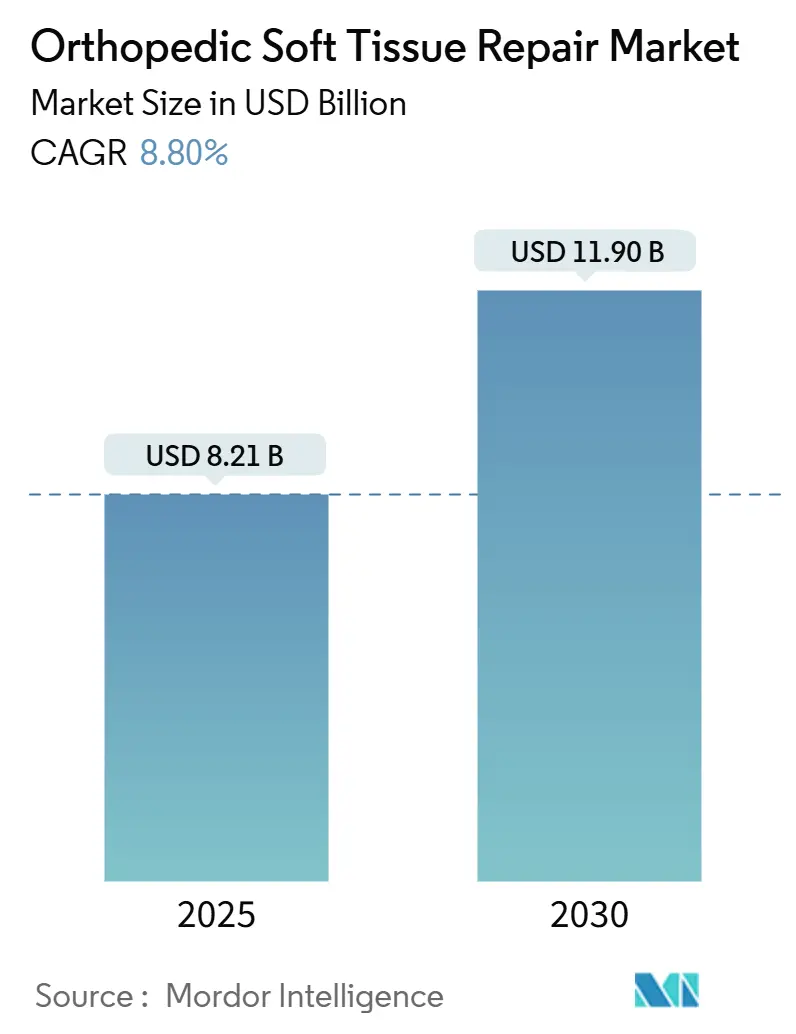

| Market Size (2025) | USD 8.21 Billion |

| Market Size (2030) | USD 11.90 Billion |

| Growth Rate (2025 - 2030) | 8.80% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Orthopedic Soft Tissue Repair Market Analysis by Mordor Intelligence

The orthopedic soft tissue repair market size stands at USD 8.21 billion in 2025 and is projected to reach USD 11.9 billion by 2030, reflecting an 8.8% CAGR across the forecast window. Demographic aging, rising sports participation, and accelerating surgeon adoption of bio-inductive scaffolds are amplifying procedure volumes. Hospitals and ambulatory surgical centers (ASCs) are expanding arthroscopic suites to capitalize on shorter stays and improved reimbursement, while original-equipment manufacturers (OEMs) intensify R&D in biologics that stimulate endogenous healing. Artificial-intelligence (AI) planning platforms that predict re-tear risk after rotator-cuff repair are further elevating procedural success rates. Together, these forces reinforce strong purchasing momentum for fixation anchors, bioresorbable implants, and specialty disposables used across shoulder, knee, and hip repairs.

Key Report Takeaways

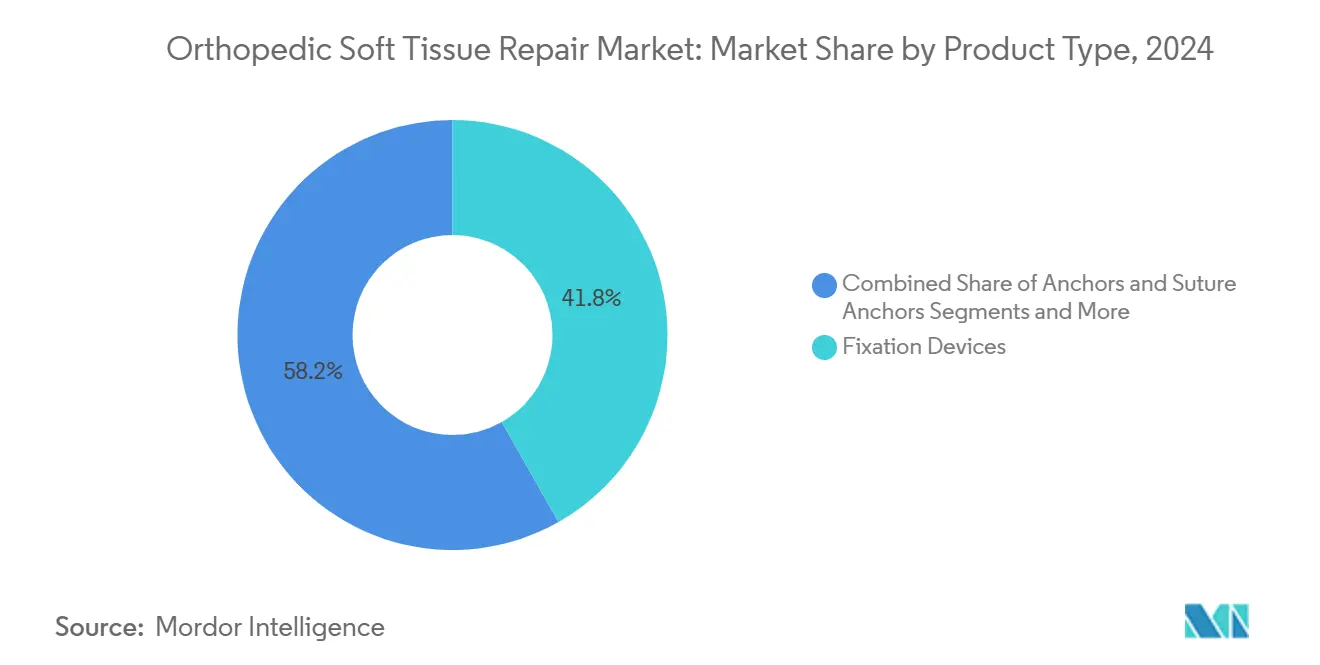

- By product type, fixation devices led with 41.8% of orthopedic soft tissue repair market share in 2024, while bio-inductive scaffolds are advancing at a 10.1% CAGR through 2030.

- By application, rotator-cuff repair accounted for 34.5% share of the orthopedic soft tissue repair market size in 2024 and hip-labrum repair is on track for a 10.4% CAGR to 2030.

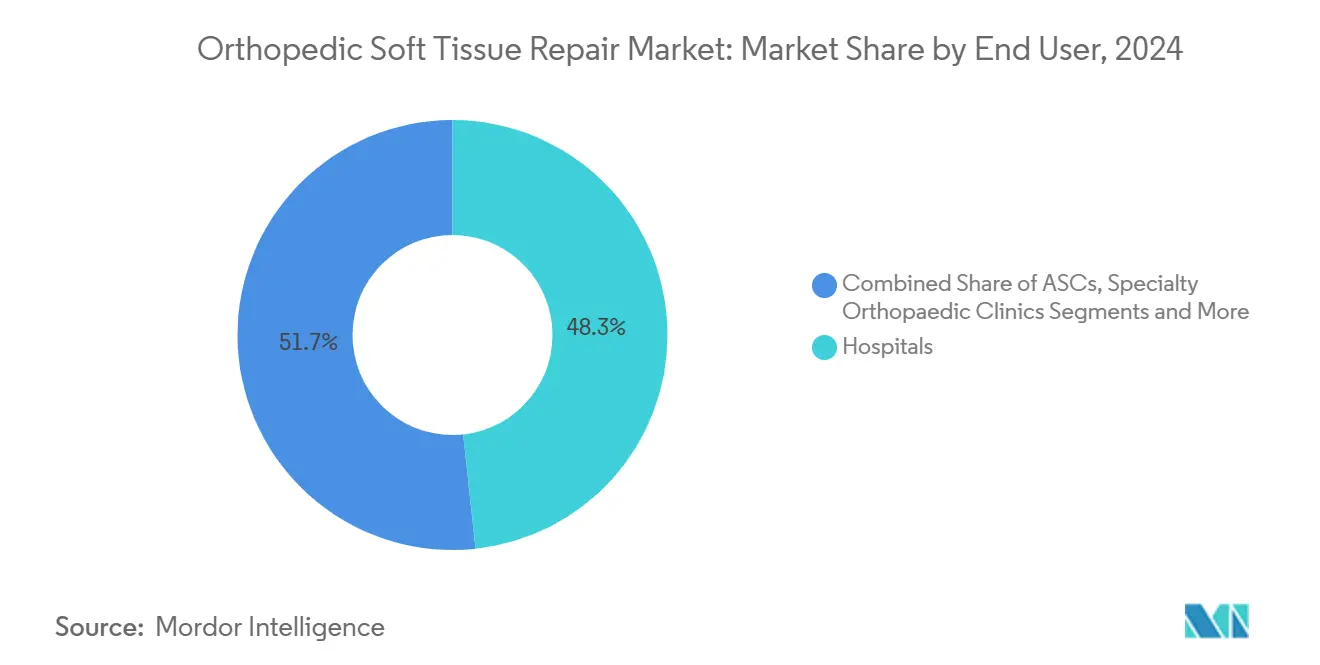

- By end user, hospitals held 48.3% revenue share in 2024, while ASCs are expanding at an 8.9% CAGR through 2030 under revised Medicare payment rules.

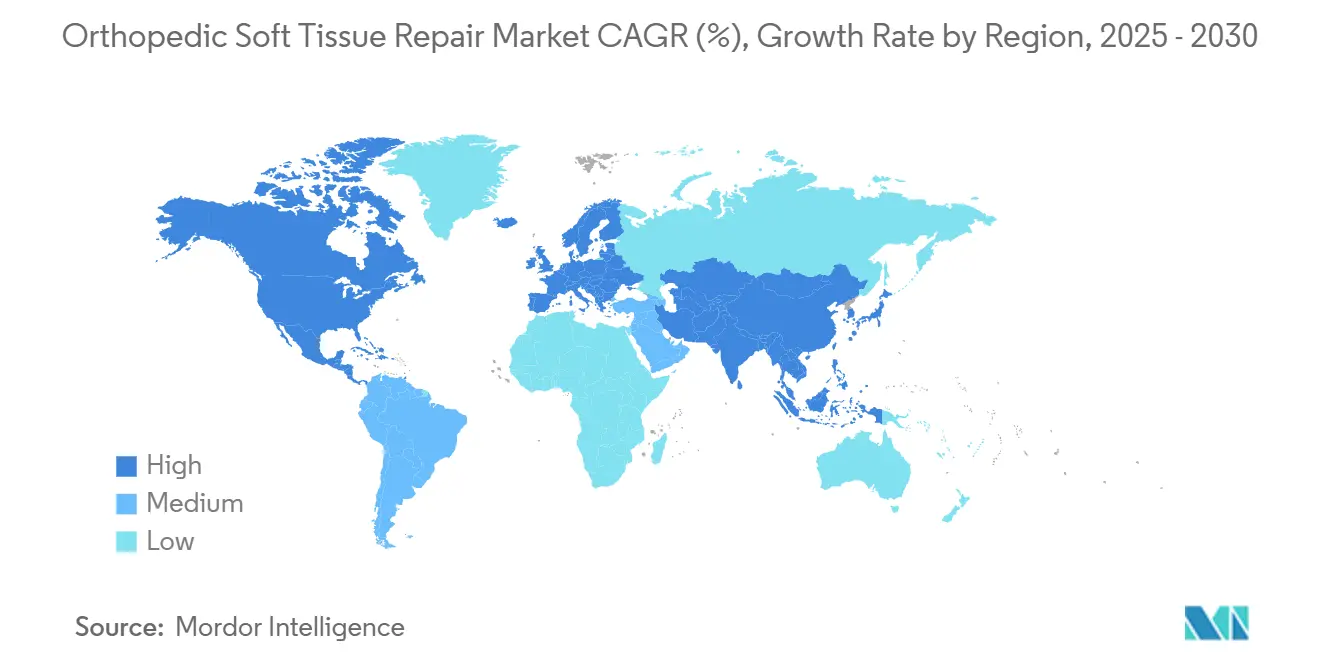

- By region, North America commanded 38.7% of orthopedic soft tissue repair market share in 2024, whereas Asia–Pacific is forecast to post an 8.1% CAGR to 2030 on the back of capacity additions and pro-manufacturing policies.

Global Orthopedic Soft Tissue Repair Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population & Sports-Injury Prevalence | +1.80% | Global, with concentration in North America & EU | Long term (≥ 4 years) |

| Shift To Minimally-Invasive Arthroscopic Procedures | +1.50% | Global, led by North America, expanding to APAC | Medium term (2-4 years) |

| Growth In Outpatient ASC Reimbursement Models | +1.20% | North America primary, limited EU adoption | Short term (≤ 2 years) |

| Emergence Of Bio-Inductive & Scaffold Technologies | +2.10% | North America & EU leading, APAC following | Medium term (2-4 years) |

| AI-Driven Pre-Op Planning Improving Repair Success | +0.90% | North America & EU core, selective APAC adoption | Medium term (2-4 years) |

| Regenerative Medicine Collaborations With OEMs | +1.00% | Global, with R&D concentration in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Population & Sports-Injury Prevalence

Rotator-cuff pathology affects more than 40% of individuals older than 60, and participation in organized athletics among adults over 50 continues to rise.[1]Zhewei Zhang et al., “Re-tear after Arthroscopic Rotator Cuff Repair Can Be Predicted Using Deep Learning Algorithm,” Frontiers in Artificial Intelligence, pubmed.ncbi.nlm.nih.gov The intersection of degenerative and acute injury mechanisms is therefore swelling the orthopedic soft tissue repair market. Healthcare systems are responding by opening combined sports-medicine and geriatric-orthopedic service lines that funnel high volumes of shoulder, knee, and hip repairs. In parallel, public-sector payers in Europe and North America have begun funding fall-prevention and musculoskeletal-screening programs, indirectly accelerating referral pipelines. Across emerging Asia, private hospitals cater to inbound medical tourists seeking low-cost arthroscopic procedures, widening global addressability for biologic grafts and fixation anchors.

Shift to Minimally Invasive Arthroscopy

Arthroscopic visualization, powered by 4K imaging and flexible instrumentation, is shortening the average length of stay from two days to same-day discharge for many tendon and labrum repairs. Vericel’s 2024 U.S. launch of MACI Arthro, an arthroscopically delivered chondrocyte implant, underscores the momentum toward smaller portals and biologic augmentation. Studies show surgeons reach proficiency in suprascapular-nerve decompression after about 50 cases, shrinking operative time from 29.5 minutes to 6.2 minutes.[2]Kotaro Yamakado, “Learning Curve for Arthroscopic Suprascapular Nerve Decompression,” Arthroscopy Journal, arthroscopyjournal.org As learning curves flatten, OEMs selling disposable cannulas, suture-passers, and smart anchors see expanding recurring revenue streams within the orthopedic soft tissue repair market.

Growth in Outpatient ASC Reimbursement Models

The Centers for Medicare & Medicaid Services lifted ASC payment rates by 2.6% for calendar 2025 and expanded its covered-procedure list to include additional arthroscopic knee, shoulder, and hip interventions.[3]Administrator. "CMS Begins Investigation into Hospital Cost-to-Charge Ratios, Hospital Outlier Payments, and Charge Description Masters." MHA, July 12, 2024. Revenue projections indicate orthopedic ASCs can double top-line income for certain ligament repairs once new rates are fully implemented. The bundling of implant costs into the global payment is compelling buyers to negotiate volume-based contracts with implant vendors, creating price elasticity in favor of bioresorbable anchors that eliminate later hardware removal. Device makers are reciprocating by co-investing in ASC build-outs, offering capital equipment on deferred-payment terms to secure implant pull-through across the orthopedic soft tissue repair market.

Emergence of Bio-Inductive & Scaffold Technologies

Regenerative implants are shifting the therapeutic goal from structural reinforcement to biologic restitution. Regenity’s collagen RejuvaKnee meniscus device received U.S. clearance in 2024 and targets more than 1 million annual meniscectomies. CONMED’s BioBrace earned expanded indications in April 2025, now covering 50+ procedures ranging from ACL to biceps-tendon repair. Pre-clinical work on manganese-silicate nanoparticle scaffolds has further demonstrated accelerated tendon-to-bone healing via stem-cell modulation in animal models. These advances intensify surgeon and patient interest, nudging conventional screw-and-anchor protocols toward hybrid constructs that combine fixation with biologic augmentation, bolstering future growth in the orthopedic soft tissue repair market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clinical Evidence Gaps For Novel Biologics | -1.40% | Global, with stricter enforcement in North America & EU | Medium term (2-4 years) |

| High Procedure & Device Costs Vs. Payer Pressure | -2.10% | North America primary, spreading to EU and APAC | Short term (≤ 2 years) |

| Surgeon Learning Curve For Advanced Anchors | -0.80% | Global, with higher impact in emerging markets | Medium term (2-4 years) |

| Regulatory Uncertainty For Allograft Sourcing | -0.60% | North America & EU primary, limited APAC impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Clinical Evidence Gaps for Novel Biologics

No new cartilage-repair biologic has gained FDA approval in more than 15 years, underscoring the stringent clinical-trial burden for 351-classified products. The agency has heightened surveillance of human-tissue derivatives, and the American Academy of Orthopaedic Surgeons now maintains a public biologics dashboard to track research status. Randomized trials are hampered by small sample sizes and ethical hurdles tied to placebo surgery, delaying commercial timelines for scaffold innovators. For hospitals, uncertain long-term efficacy data limit reimbursement coding beyond temporary new-technology add-on payments, constraining initial uptake inside the orthopedic soft tissue repair market.

High Procedure & Device Costs Versus Payer Pressure

Inflation-adjusted Medicare payments for primary hip and knee arthroplasties have fallen 55% since 2000, while supply-chain costs consume up to 20% of med-tech expenses. Orthopedic trauma reimbursement declined by nearly one-third over the same span. Episode-of-care pricing pressures lead surgeons to weigh premium scaffold implants against tighter margins. At the same time, ASCs standardize generic screws or negotiate capitated contracts with OEMs, slowing near-term revenue growth for high-specification biologics in the orthopedic soft tissue repair market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bio-Inductive Technologies Drive Innovation

Fixation devices retained 41.8% of the orthopedic soft tissue repair market share in 2024, underpinned by the ubiquity of anchors, screws, and tapes used across tendon and ligament procedures. Yet bio-inductive scaffolds are scaling at a 10.1% CAGR through 2030, signaling a paradigm shift toward regenerative healing constructs. Atreon received U.S. clearance in 2025 for a bioresorbable synthetic implant that provides temporary support during rotator-cuff healing and then dissolves, avoiding future hardware complications. OEMs are bundling growth factors, stem-cell carriers, and antimicrobial agents into composite designs, creating multifunctional products that command premium average-selling prices.

R&D priorities increasingly center on hybrid platforms that integrate fixation and biologic cues in a single delivery system. Three-dimensional printing enables patient-specific porosity gradients, while smart polymers respond to local pH or enzymatic activity to control degradation rates. Regulatory agencies have published guidance that stresses mechanical testing parity with legacy metals yet encourages innovative biocompatibility evidence pathways, giving first movers a timing advantage. Collectively, these advances position bio-inductive constructs as pivotal contributors to long-run expansion of the orthopedic soft tissue repair market.

By Application: Hip Labrum Repair Emerges as Growth Leader

Rotator-cuff interventions generated 34.5% of the orthopedic soft tissue repair market size in 2024 owing to high prevalence and well-established clinical pathways. Hip-labrum surgery, however, is growing fastest at 10.4% CAGR, propelled by improved femoroacetabular-impingement diagnostics and postless-traction arthroscopy that reduces pudendal-nerve risk. Surgeons now employ combined capsular plication and femoroplasty to restore hip kinematics, stimulating demand for low-profile suture anchors compatible with constrained anatomical corridors.

Meniscal preservation is also transitioning from partial meniscectomy toward scaffold-based regeneration after Regenity’s RejuvaKnee clearance, which targets an annual U.S. caseload exceeding 1 million. Anterior cruciate ligament (ACL) reconstructions benefit from multiphasic bone-ligament-bone scaffolds that accelerate graft incorporation. As outcome registries document durability gains for biologically enhanced repairs, payer algorithms may eventually favor tissue-conserving approaches, adding tailwinds to the orthopedic soft tissue repair market.

By End User: ASCs Capitalize on Reimbursement Advantages

Hospitals accounted for 48.3% revenue in 2024, reflecting their broad case mix and trauma coverage responsibilities. Nevertheless, ASCs are forecast to grow 8.9% annually through 2030 as Medicare and commercial insurers steer suitable cases to outpatient settings with lower facility fees. Surgeons appreciate control over scheduling and staffing, while patients value same-day discharge and reduced infection risk.

Specialty orthopedic centers are experimenting with bundled-payment contracts that cover implant, facility, and professional fees for a fixed price. Device vendors, in turn, offer consignment inventory and cloud-connected instrumentation that tracks utilization, permitting granular cost accounting. Mobile surgical pods and hybrid inpatient-outpatient facilities round out the “others” category, extending reach into rural catchment areas. All told, shifting site-of-service patterns deepens procedure volumes and diversifies buying channels inside the orthopedic soft tissue repair market.

Geography Analysis

North America retained 38.7% of the orthopedic soft tissue repair market share in 2024 on the strength of advanced imaging infrastructure and early biologic-implant adoption. Federal payment reforms that lift ASC rates enhance near-term revenue visibility; however, long-term growth is tempered by downward pressure on surgeon fees and hospital budgets. U.S. OEMs are responding via targeted acquisitions—Stryker’s purchase of Artelon being a prime example—to secure proprietary soft-tissue technologies.

Asia–Pacific is expected to log an 8.1% CAGR to 2030, buoyed by hospital expansion, rising disposable incomes, and government incentives for domestic device manufacturing. China’s National Medical Products Administration has streamlined Class III approval pathways under State Order 739, enabling local firms to launch orthopedic robots aimed at arthroscopy. India’s production-linked incentives likewise encourage home-grown implant fabrication, expanding regional supply and lowering cost barriers.

Europe shows steady, regulated growth as Medical Device Regulation (MDR) compliance deadlines synchronize clinical-evidence expectations across member states. Aging demographics and public-sector emphasis on day-case surgery sustain medium-term volume gains. Meanwhile, Latin America, the Middle East, and parts of Africa post double-digit procedure growth from a small base, though currency volatility and fragmented reimbursement slow premium-implant penetration. OEMs deploying tiered-pricing and surgeon-education programs are best positioned to harvest incremental demand in these frontier segments of the orthopedic soft tissue repair market.

Competitive Landscape

The orthopedic soft tissue repair industry displays moderate consolidation: the top five manufacturers collectively control roughly 52% of global revenue, with Johnson & Johnson alone holding 13% and Stryker about 3%. Large players leverage scale to fund pivotal trials that satisfy 351 biologic requirements, erecting barriers for smaller innovators. Recent deal activity—such as Smith+Nephew’s USD 180 million acquisition of Agili-C cartilage-regeneration technology—signals investor appetite for platforms that complement anchor portfolios with biologic augmentation.

Artificial-intelligence engines that map tear morphology and bone density onto implant placement plans are emerging as key differentiators. A deep-learning model recently achieved 96.9% accuracy in predicting re-tear risk after arthroscopic rotator-cuff repair, sharpening debate over pay-for-performance reimbursement. Robotic-assisted total-knee arthroplasty reached 13% of U.S. procedures in 2023, but long-term superiority over manual techniques remains inconclusive.

Start-ups focusing on bioresorbable polymers and cell-laden hydrogels continue to raise venture capital albeit at lower valuations than in 2021. Strategic partnering—Zimmer Biomet’s alliance with CBRE to develop ASC networks, for example—extends downstream control over procedure settings and implant formularies. As reimbursement systems pivot toward bundled payments and evidence-based authorizations, scale, product breadth, and data analytics will increasingly dictate share shifts within the orthopedic soft tissue repair market.

Orthopedic Soft Tissue Repair Industry Leaders

-

Arthrex

-

Smith & Nephew

-

Stryker

-

Zimmer Biomet

-

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: CONMED gained FDA clearance for expanded BioBrace indications covering 50+ tendon and ligament repairs, positioning the scaffold as a platform technology.

- February 2025: Atreon secured U.S. clearance for a bioresorbable rotator-cuff implant, offering surgeons a metal-free fixation option.

- August 2024: Vericel launched MACI Arthro, enabling arthroscopic delivery of autologous cultured chondrocytes on a porcine collagen membrane.

Global Orthopedic Soft Tissue Repair Market Report Scope

| Fixation Devices |

| Anchors & Suture Anchors |

| Biological Grafts |

| Synthetic Grafts |

| Sutures & Tapes |

| Others |

| Rotator Cuff Repair |

| ACL/PCL Repair |

| Meniscal Repair |

| Hip Labrum Repair |

| Shoulder Labrum Repair |

| Others |

| Hospitals |

| Ambulatory Surgical Centres (ASCs) |

| Specialty Orthopaedic Clinics |

| Sports-Medicine Centres |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Fixation Devices | |

| Anchors & Suture Anchors | ||

| Biological Grafts | ||

| Synthetic Grafts | ||

| Sutures & Tapes | ||

| Others | ||

| By Application | Rotator Cuff Repair | |

| ACL/PCL Repair | ||

| Meniscal Repair | ||

| Hip Labrum Repair | ||

| Shoulder Labrum Repair | ||

| Others | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centres (ASCs) | ||

| Specialty Orthopaedic Clinics | ||

| Sports-Medicine Centres | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the orthopedic soft tissue repair market?

The orthopedic soft tissue repair market size is USD 8.2 billion in 2025.

How fast is demand for bio-inductive scaffolds growing?

Bio-inductive scaffolds are expanding at a 10.1% CAGR through 2030 thanks to regenerative-healing benefits.

Why are ambulatory surgical centers gaining share in soft-tissue procedures?

Revised Medicare payment rates and same-day discharge convenience are pushing more arthroscopic repairs into ASCs.

Which application segment shows the fastest growth potential?

Hip-labrum repair leads with a projected 10.4% CAGR, driven by better impingement diagnostics and arthroscopic techniques.

How are reimbursement pressures influencing device selection?

Declining surgeon fees and bundled payments are steering clinics toward cost-effective, often bioresorbable, implant systems.

Page last updated on: