Orthopedic Regenerative Surgical Products Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

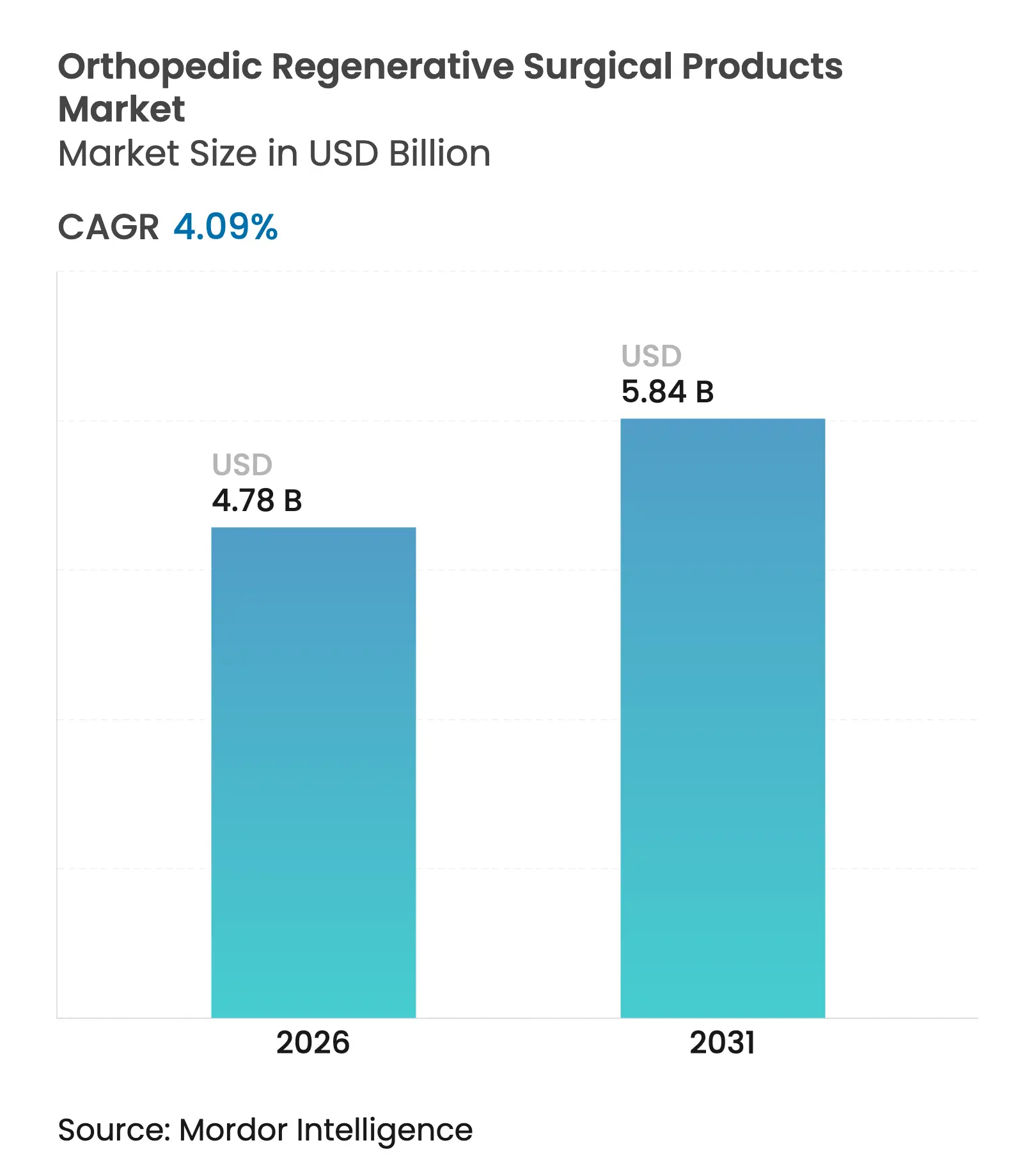

| Market Size (2026) | USD 4.78 Billion |

| Market Size (2031) | USD 5.84 Billion |

| Growth Rate (2026 - 2031) | 4.09 % CAGR |

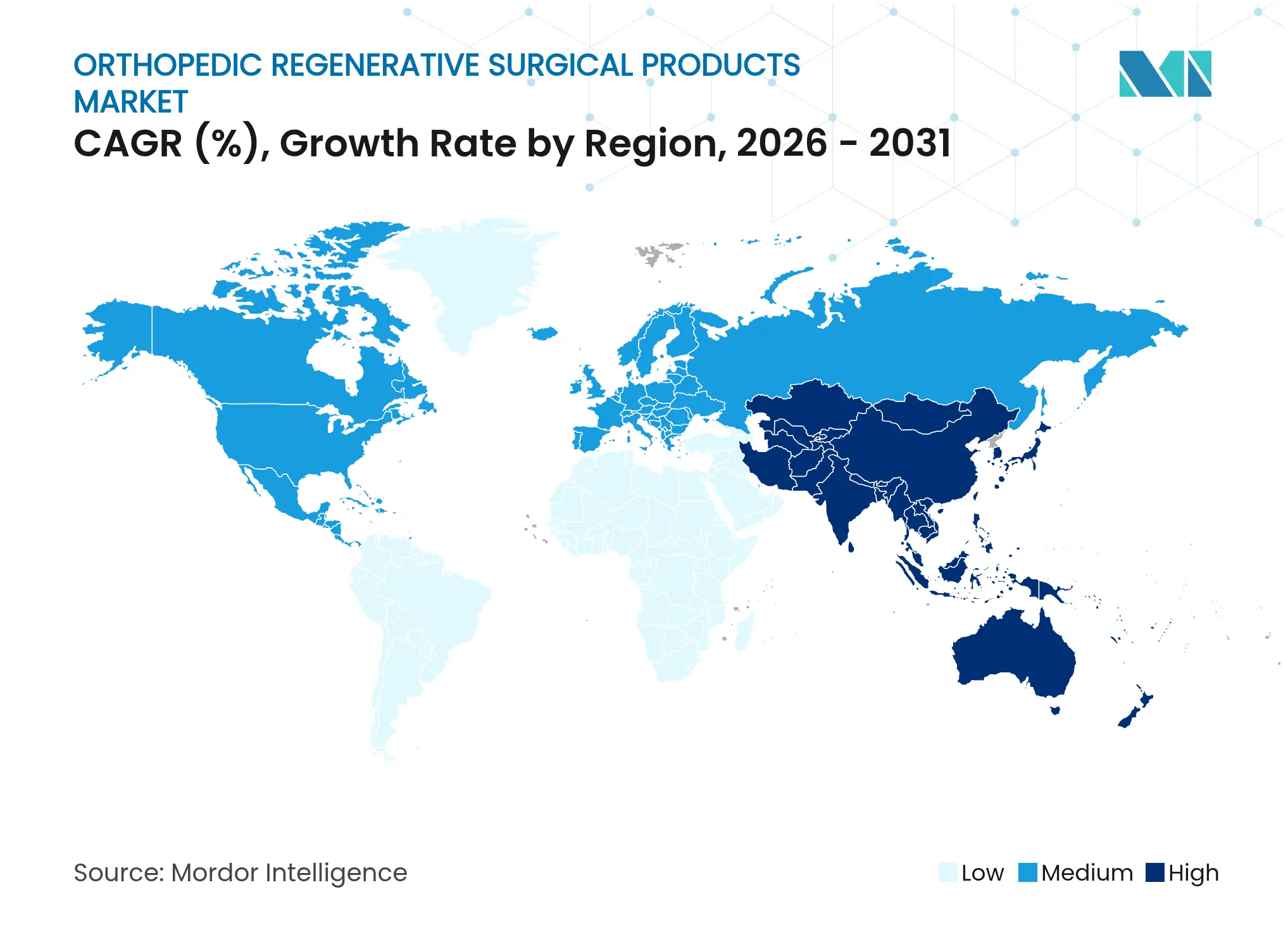

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Orthopedic Regenerative Surgical Products Market Analysis by Mordor Intelligence

The orthopedic regenerative surgical products market size is expected to grow from USD 4.59 billion in 2025 to USD 4.78 billion in 2026 and is forecast to reach USD 5.84 billion by 2031 at 4.09% CAGR over 2026-2031. Steady growth reflects a transition from experimental concepts to validated clinical solutions, underpinned by regulatory approvals such as Vericel’s MACI Arthro—the first restorative biologic cartilage repair product cleared for arthroscopic use in August 2024. Demographic pressures tied to an aging global population, the rising prevalence of obesity, and the surge in osteoarthritis cases are amplifying demand for biologic and synthetic alternatives that preserve native tissue longer than implants. Breakthroughs in biomaterials, notably Duke University’s hydrogel that exceeds natural cartilage strength, are broadening the clinical appeal of regenerative options. Meanwhile, point-of-care autologous biologics and 3D-bioprinted constructs are challenging implant-centric paradigms, enabling faster procedures and reducing procedural costs.

Key Report Takeaways

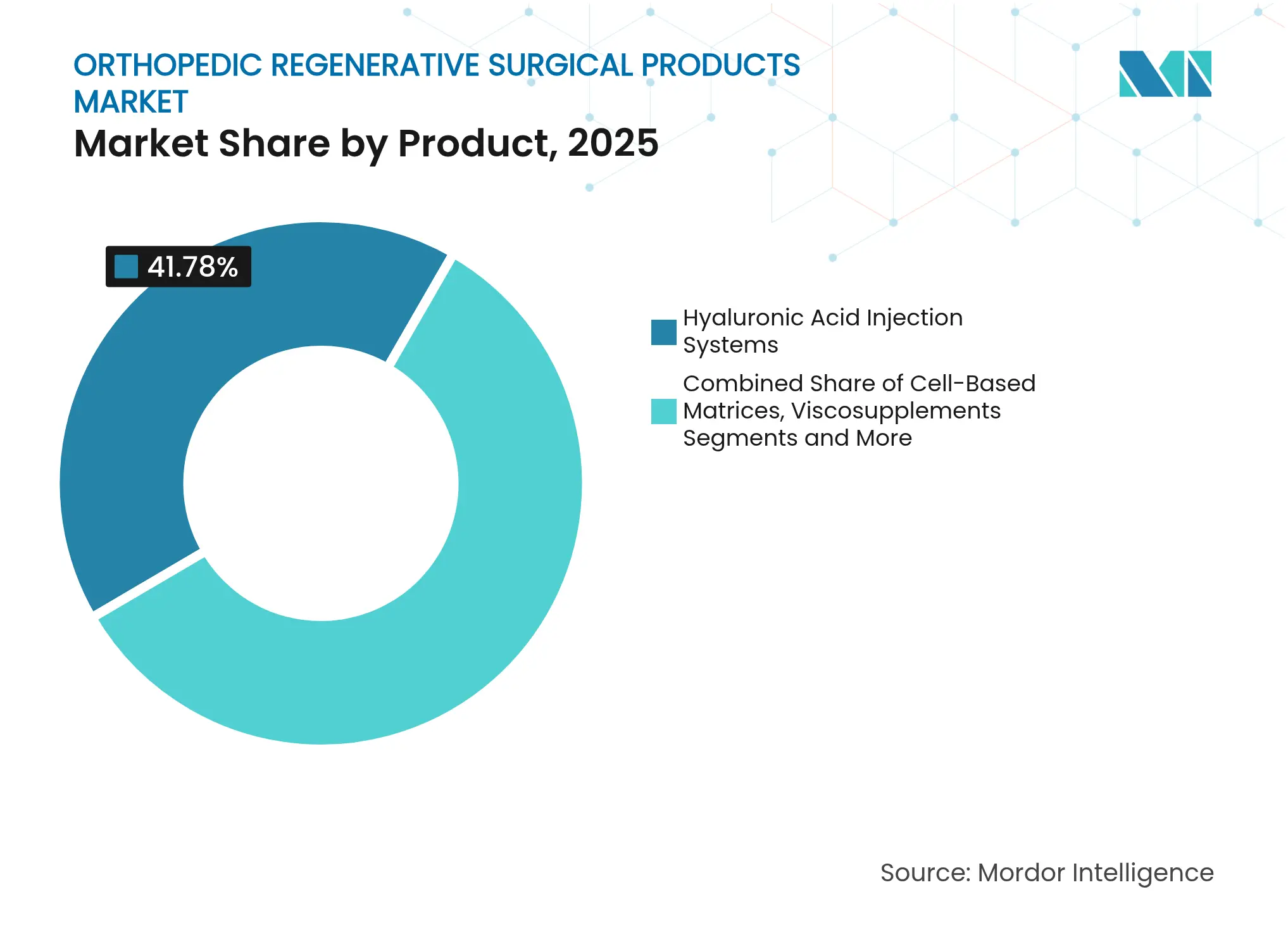

- By product, hyaluronic acid injection systems led with 41.78% of orthopedic regenerative surgical products market share in 2025, while cell-based matrices are projected to advance at an 7.88% CAGR to 2031.

- By application, cartilage & tendon repair accounted for 35.10% of the orthopedic regenerative surgical products market size in 2025, whereas sports injury management is poised to grow at a 9.28% CAGR through 2031.

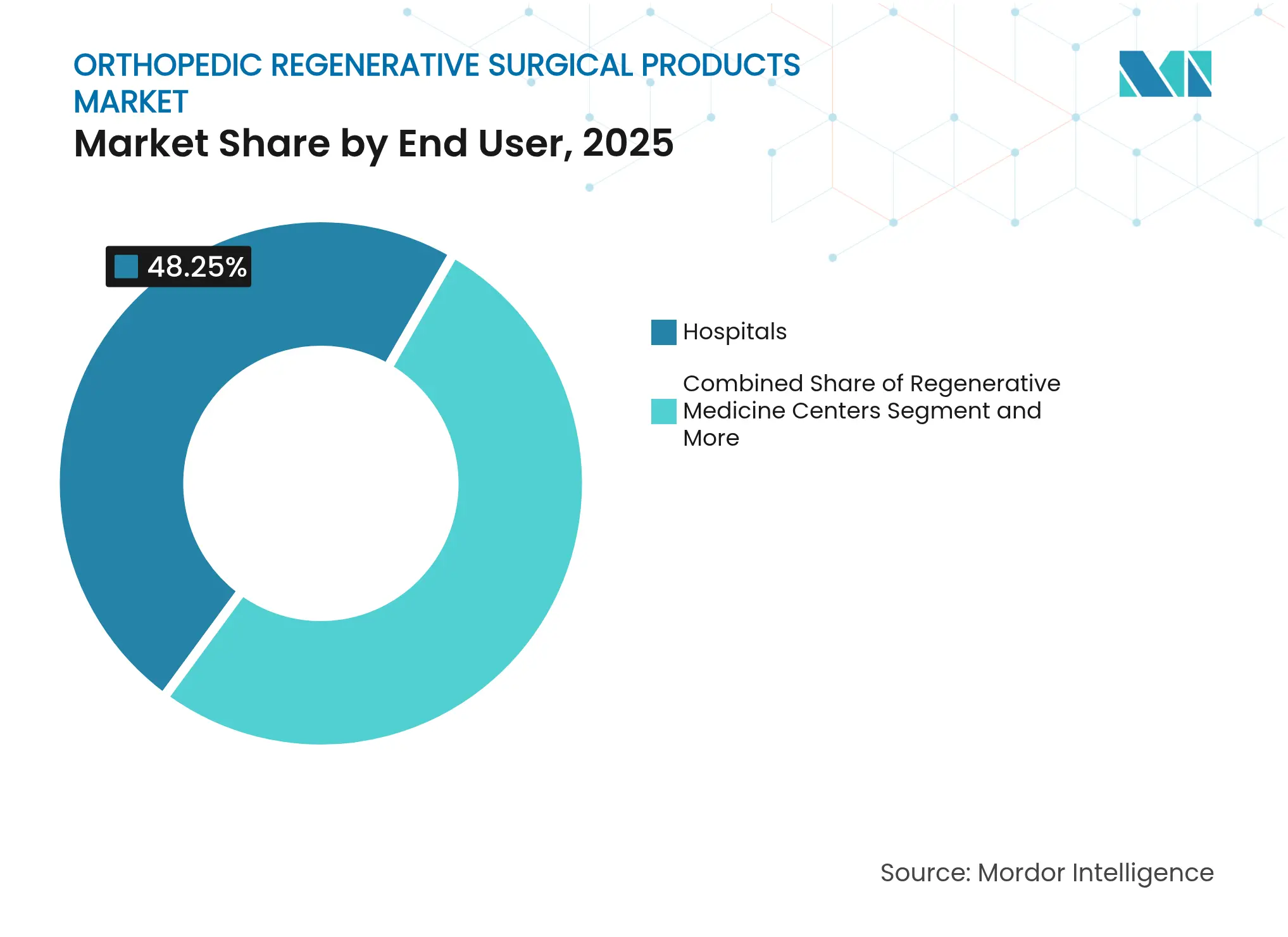

- By end user, hospitals held 48.25% share of the orthopedic regenerative surgical products market in 2025; regenerative medicine centers record the highest forecast CAGR at 7.96% to 2031.

- By geography, North America commanded 42.10% revenue share in 2025, yet Asia-Pacific is set to post the fastest regional CAGR of 6.95% during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Orthopedic Regenerative Surgical Products Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rise in prevalence of orthopedic degenerative conditions

Rise in prevalence of orthopedic degenerative conditions

| +1.2% | Global; highest in North America & Europe | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

+1.2%

| Geographic Relevance:

Global; highest in North America & Europe

| Impact Timeline:

Long term (≥ 4 years)

|

Rapidly aging population accelerating joint-replacement

volumes

Rapidly aging population accelerating joint-replacement

volumes

| +1.0% | Global; concentrated in developed markets | Long term (≥ 4 years) | |||

Breakthroughs in synthetic biomaterials

Breakthroughs in synthetic biomaterials

| +0.8% | North America & Europe expanding to Asia-Pacific | Medium term (2-4 years) | |||

Expansion of in-office point-of-care autologous biologics

Expansion of in-office point-of-care autologous biologics

| +0.6% | North America; early adoption in Europe | Short term (≤ 2 years) | |||

Commercialization of 3D-bioprinted osteochondral

constructs

Commercialization of 3D-bioprinted osteochondral

constructs

| +0.4% | North America & Europe; limited Asia-Pacific | Medium term (2-4 years) | |||

Favorable reimbursement for viscosupplement repeat cycles

in OECD markets

Favorable reimbursement for viscosupplement repeat cycles

in OECD markets

| +0.3% | OECD nations | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Rise in Prevalence of Orthopedic Degenerative Conditions

Global osteoarthritis cases exceeded 595 million in 2024 and are on a steep climb, putting sustained pressure on surgical systems and elevating demand for tissue-preserving solutions. Women and individuals over 95 are most affected, creating long-term momentum for biologics that can delay joint replacement. High BMI levels add to disease incidence, prompting preventive strategies that dovetail with regenerative protocols. Health-system economics now view biologics as a route to trim disability costs and revision surgeries, bolstering the orthopedic regenerative surgical products market.

Rapidly Aging Population Accelerating Joint-Replacement Volumes

Joint-replacement demand is rising faster than operating-room capacity, with forecasts of sharp total knee arthroplasty growth to 2040. Regenerative interventions that defer surgery by up to 10 years relieve capacity bottlenecks and accommodate active seniors seeking minimally invasive care. Sports medicine is benefiting as older adults remain athletically engaged, driving uptake of platelet-rich plasma and stem-cell-infused matrices that shorten rehabilitation timelines. Payers increasingly weigh these treatments as cost-effective when measured against multiple revision surgeries over a patient’s lifetime.

Breakthroughs in Synthetic Biomaterials

Hydrogel implants from Duke University demonstrate tensile strength 26% higher than native cartilage, eliminating donor-site morbidity[1]Duke University, “Hydrogel Implant Surpassing Natural Knee Cartilage Strength,” trial.medpath.com. Swansea University’s coral-inspired bone substitute promotes full integration within 12 months while dissolving naturally, reducing graft complications. Graphene-foam scaffolds cultivated at Boise State enhance chondrocyte activity through electrical stimulation, solving the architecture challenge of complex tissue engineering. These innovations remove supply chain constraints tied to donor tissue and simplify storage, propelling adoption in the orthopedic regenerative surgical products market.

Expansion of In-Office Point-of-Care Autologous Biologics

FDA-cleared devices such as Healeon Float PRP enable physicians to process platelet-rich plasma at the point of care, slashing treatment costs up to 60% versus hospital settings. Immediate processing avoids cold-chain risk and improves patient throughput, especially in sports clinics. Customizable protocols align platelet concentration with individual pathology, raising efficacy rates and fueling direct-to-consumer demand. Competition is sharpening as specialty regenerative clinics market convenience and rapid recovery over traditional hospital pipelines.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High procurement & procedure costs vs. traditional

implants

High procurement & procedure costs vs. traditional

implants

| -0.8% | Global; most acute in cost-sensitive markets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

-0.8%

| Geographic Relevance:

Global; most acute in cost-sensitive markets

| Impact Timeline:

Short term (≤ 2 years)

|

Stringent and lengthy FDA/EMA biologics approval pathways

Stringent and lengthy FDA/EMA biologics approval pathways

| -0.6% | North America & Europe; spillover worldwide | Medium term (2-4 years) | |||

Donor-tissue traceability rules tightening allograft

supply

Donor-tissue traceability rules tightening allograft

supply

| -0.4% | North America; expanding to regulated markets | Medium term (2-4 years) | |||

Cold-chain logistics gaps limiting cell-based uptake

Cold-chain logistics gaps limiting cell-based uptake

| -0.3% | Global; severe in emerging regions | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High Procurement & Procedure Costs vs. Traditional Implants

Regenerative options can cost 200-300% more than conventional hardware owing to complex manufacturing and storage, challenging payer budgets. Many insurers classify biologics as investigational, shifting costs to patients. However, long-term analyses reveal fewer revision surgeries and reduced disability expenditure, providing a counter-argument for broader coverage in the orthopedic regenerative surgical products market.

Stringent and Lengthy FDA/EMA Biologics Approval Pathways

Post-2023 tuberculosis outbreaks tied to live-cell allografts prompted stricter microbial screening, extending review timelines[2]Centers for Disease Control and Prevention, “Nationwide Tuberculosis Outbreak Caused by Bone Allografts,” cdc.gov. EMA’s advanced-therapy guidelines demand exhaustive quality data, stretching commercialization to 5-7 years and raising entry barriers. Smaller innovators often lack funds for lengthy trials, consolidating market power among established firms.

Segment Analysis

By Product: Cell-Based Innovation Drives Premium Growth

Hyaluronic acid injection systems retained 41.78% of orthopedic regenerative surgical products market share in 2025, benefiting from clinician familiarity and solid reimbursement. The segment’s maturation slows its expansion, yet repeat-cycle coverage safeguards revenue streams. Cell-based matrices, backed by 91% union rates in stubborn fractures, will register an 7.88% CAGR to 2031, the highest among product lines. This momentum positions cell therapies as the primary value driver in the orthopedic regenerative surgical products market. Demineralized bone matrix and BMPs face pressure from synthetic substitutes that bypass donor-tissue constraints. Platelet-rich plasma kits enjoy outsized growth as point-of-care devices ease in-office preparation, while coral-based and graphene-enhanced synthetics close functional gaps with cancellous bone.

Synthetic substitutes deliver predictable performance and remove infection risk, winning payer favor in cost-sensitive settings. The orthopedic regenerative surgical products market size related to synthetic bone substitutes is projected to outpace legacy allografts as traceability regulations tighten. FDA approvals of multiple PRP kits in 2024-2025 validate autologous therapies and enable rapid clinic adoption. Allograft suppliers must now implement end-to-end tracking systems, adding overhead that erodes price competitiveness.

Note: Segment shares of all individual segments available upon report purchase

By Application: Sports Medicine Accelerates Treatment Paradigms

Cartilage & tendon repair accounted for 35.10% of the orthopedic regenerative surgical products market in 2025, propelled by MACI Arthro’s arthroscopic approval and expanding MSC trial data. Sports injury management, spurred by demand for 40-60% faster recovery, will post the fastest 9.28% CAGR. Younger patients opt for biologics that enable earlier return to play, raising revenue visibility for specialty clinics. Orthopedic pain management remains a steady contributor as viscosupplements extend pain-free intervals, while trauma and joint reconstruction segments incorporate biologic adjuncts to enhance outcomes. The orthodontic regenerative surgical products market size tied to sports injury solutions is expected to swell in tandem with outpatient procedure volumes at ambulatory centers.

Spinal fusion applications leverage electrical stimulators such as the Xstim device, which lifts fusion success to 87% versus 64% placebo, showcasing how regenerative adjuncts can elevate hardware success. Bone defect filling shifts toward 3D-printed scaffolds that fit anatomical voids precisely, cutting OR time and donor-site morbidity. The orthopedic regenerative surgical products industry thus advances on the back of cross-disciplinary innovation linking biomaterials, biologics, and smart-device platforms.

By End User: Specialized Centers Reshape Care Delivery

Hospitals commanded 48.25% share in 2025, leveraging broad infrastructure and referral streams. Yet regenerative medicine centers are forecast to grow 7.96% annually, reflecting patient appetite for specialized expertise and faster scheduling. Ambulatory surgical centers gain traction as CMS green-lights more shoulder and knee procedures for outpatient settings, projecting a 13% rise in ortho cases this decade. The orthopedic regenerative surgical products market now aligns closely with these lower-cost venues where minimally invasive biologic procedures thrive.

Specialty orthopedic clinics increasingly integrate PRP and stem-cell protocols to differentiate from general hospitals and capture cash-pay consumers. New FDA quality-system rules that take effect in 2026 will require tighter documentation, favoring dedicated centers capable of rapid compliance. Consequently, product suppliers must bolster field-service and training units to support decentralized delivery models, especially for autologous devices that rely on point-of-care processing.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America held 42.10% of orthopedic regenerative surgical products market share in 2025, supported by FDA approvals such as Zimmer Biomet’s cementless partial knee and sustained reimbursement for viscosupplement cycles. Growth moderates amid payer austerity and procedure-volume plateaus, though point-of-care biologics mitigate revenue dips. Market consolidation, exemplified by Stryker’s Artelon buyout and Smith & Nephew’s USD 510 million regenerative spend, is realigning distribution and R&D pipelines.

Asia-Pacific posts the quickest 6.95% CAGR as China’s first stem-cell therapy approval in January 2025 legitimizes advanced biologics. South Korea’s February 2025 regenerative medicine law broadens experimental therapy access under strict oversight, fostering clinical-trial inflows. Japan’s harmonized QMS rules facilitate global submissions, shortening launch timelines. Rising healthcare spend and medical tourism augment regional procedure volumes, positioning Asia-Pacific at the forefront of growth within the orthopedic regenerative surgical products market.

Europe maintains a pivotal role amid MDR complexities. EMA’s stringent post-marketing surveillance sees 88% of advanced therapies under additional monitoring, reassuring clinicians and payers of safety. Enovis’s LimaCorporate acquisition expands 3D-printed titanium implant offerings, illustrating strategic bets on additive manufacturing. Research consortia, including Queen Mary University’s Agrin protein program, enhance the region’s innovation profile and could lift the cartilage repair sub-segment to USD 4.5 billion by 2027. Emerging economies in the Middle East, Africa, and South America invest in orthopedic centers, but logistic gaps and reimbursement hurdles slow adoption compared with developed peers.

Competitive Landscape

Market Concentration

The orthopedic regenerative surgical products market demonstrates moderate consolidation as major device firms acquire niche biologic innovators. Stryker’s 2024 acquisition of Artelon enriches its ligament-regeneration suites, while Enovis’s LimaCorporate deal secures proprietary trabecular titanium printing know-how. Smith & Nephew earmarks USD 510 million for regenerative R&D within a USD 3.92 billion medtech allocation, highlighting strategic prioritization. Technology differentiation drives competition; firms integrate AI for personalized graft sizing, adopt graphene-enhanced scaffolds for cell viability, and deploy smart bioreactors that monitor tissue maturation in real time.

Breakthrough regulatory wins can rapidly shift competitive positions. Regenity’s 2024 FDA clearance of a regenerative meniscus implant grants first-mover advantage in a high-revision niche. Vericel’s MACI Arthro arthroscopic label broadens its user base and reduces OR time, strengthening its foothold in cartilage repair. Smaller academic spin-outs such as ReFleks target under-served cartilage defects with cost-effective Agrin protein, challenging incumbents on price-to-outcome metrics.

Regulatory rigor favors incumbents with robust compliance infrastructures following CDC-prompted screening updates for live-cell allografts. Suppliers offering integrated quality-management support to clinics can gain stickiness. Competitive intensity is also rising in point-of-care devices, where speed, sterility, and usability determine surgeon loyalty. Synthetic bone substitute innovators leverage rapid integration timelines to win share from traditional allografts, further fragmenting product portfolios.

Orthopedic Regenerative Surgical Products Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Anika Therapeutics completed divestiture of its Parcus Medical business to Medacta Group SA, refocusing on hyaluronic acid technology and regenerative solutions.

- October 2024: Enovis partnered with Ossium Health to distribute OssiGraft and OssiGraft Prime cryopreserved viable bone matrices, broadening access to allograft alternatives.

Table of Contents for Orthopedic Regenerative Surgical Products Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rise In Prevalence Of Orthopedic Degenerative Conditions

- 4.2.2Rapidly Aging Population Accelerating Joint-Replacement Volumes

- 4.2.3Breakthroughs In Synthetic Biomaterials

- 4.2.4Expansion Of In-Office Point-Of-Care Autologous Biologics

- 4.2.5Commercialization Of 3D-Bioprinted Osteochondral Constructs

- 4.2.6Favorable Reimbursement For Viscosupplement Repeat Cycles In Many OECD Markets

- 4.3Market Restraints

- 4.3.1High Procurement & Procedure Costs Vs. Traditional Implants

- 4.3.2Stringent And Lengthy FDA/EMA Biologics Approval Pathways

- 4.3.3Donor-Tissue Traceability Rules Tightening Allograft Supply

- 4.3.4Cold-Chain Logistics Gaps Limiting Cell-Based Product Uptake

- 4.4Porter's Five Forces

- 4.4.1Threat of New Entrants

- 4.4.2Bargaining Power of Buyers

- 4.4.3Bargaining Power of Suppliers

- 4.4.4Threat of Substitutes

- 4.4.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Product

- 5.1.1Allografts

- 5.1.2Cell-Based Matrices

- 5.1.3Viscosupplements

- 5.1.4Demineralized Bone Matrix

- 5.1.5Bone Morphogenetic Proteins

- 5.1.6Platelet-Rich Plasma Kits

- 5.1.7Synthetic Bone Substitutes

- 5.1.8Hyaluronic Acid Injection Systems

- 5.2By Application

- 5.2.1Orthopedic Pain Management

- 5.2.2Trauma Repair

- 5.2.3Cartilage & Tendon Repair

- 5.2.4Joint Reconstruction

- 5.2.5Spinal Fusion

- 5.2.6Sports Injury Management

- 5.2.7Bone Defect Filling

- 5.3By End User

- 5.3.1Hospitals

- 5.3.2Ambulatory Surgical Centers

- 5.3.3Specialty Orthopedic Clinics

- 5.3.4Regenerative Medicine Centers

- 5.4Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4South Korea

- 5.4.3.5Australia

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East and Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East and Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Zimmer Biomet

- 6.3.2Stryker

- 6.3.3Smith & Nephew

- 6.3.4Johnson & Johnson (DePuy Synthes)

- 6.3.5Medtronic plc

- 6.3.6AlloSource

- 6.3.7Anika Therapeutics

- 6.3.8Baxter International

- 6.3.9Vericel Corp.

- 6.3.10MiMedx

- 6.3.11Arthrex

- 6.3.12Aptissen SA

- 6.3.13Integra LifeSciences

- 6.3.14Orthofix Medical

- 6.3.15RTI Surgical

- 6.3.16BioTissue

- 6.3.17Kuros Biosciences

- 6.3.18Osiris Therapeutics

- 6.3.19Regenity Biosciences

- 6.3.20Bone Therapeutics

7. Market Opportunities & Future Outlook

- 7.1White-Space & Unmet-Need Assessment

Global Orthopedic Regenerative Surgical Products Market Report Scope

Regenerative orthopedics helps to treat discomfort and pain of the musculoskeletal system and improve the healing of orthopedic conditions, such as ligament, injuries of a tendon, muscle, bone, meniscus of the knee, spinal disc, and cartilage. These body parts have a comparatively poor capability to heal on their own. Regenerative orthopedic surgical products help these tissues to heal better. Orthopedic regenerative surgical products may help some patients avoid orthopedic surgery completely.

The orthopedic regenerative surgical products market is segmented by Product (Allograft, Cell-based, and Viscosupplements), Application (Orthopedic Pain Management, Trauma Repair, Cartilage and Tendon Repair, Joint Reconstruction, and Others), End User (Hospitals, Ambulatory Surgical Centers, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers the value (in USD million) for the above segments.