Orthopedic Braces And Supports Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

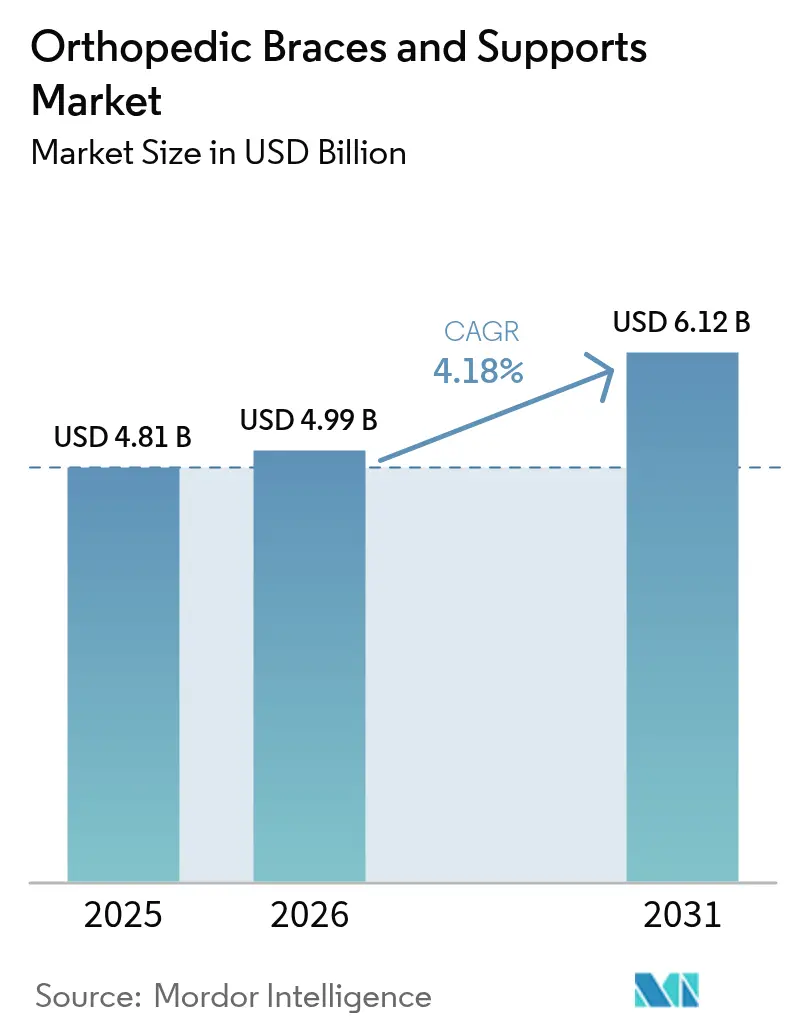

| Market Size (2026) | USD 4.99 Billion |

| Market Size (2031) | USD 6.12 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

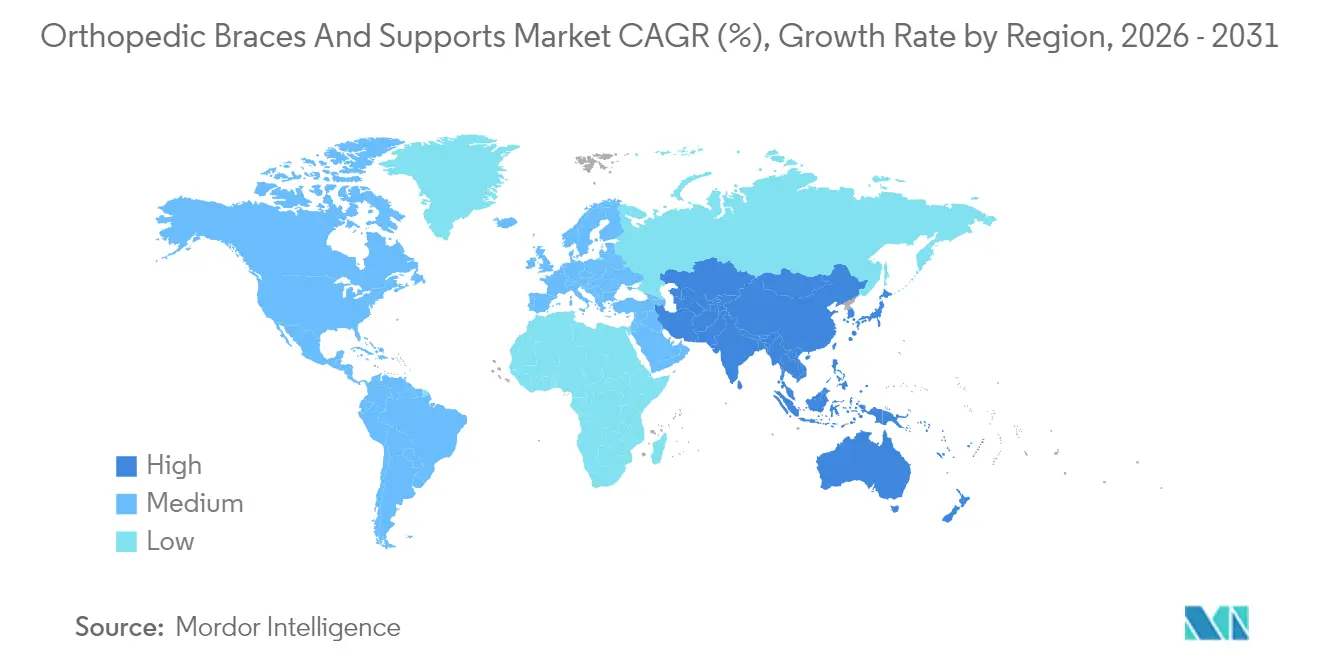

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

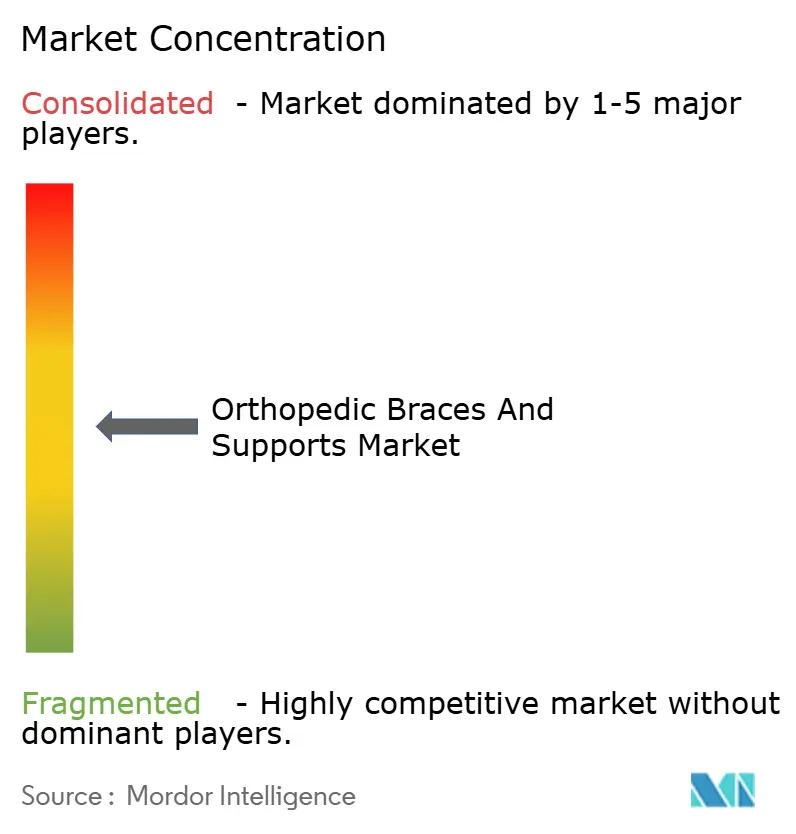

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Orthopedic Braces And Supports Market Analysis by Mordor Intelligence

The Orthopedic Braces And Supports Market size was valued at USD 4.81 billion in 2025 and is estimated to grow from USD 4.99 billion in 2026 to reach USD 6.12 billion by 2031, at a CAGR of 4.18% during the forecast period (2026-2031).

Growing musculoskeletal disease prevalence, demographic aging, and rapid materials innovation are steering the orthopedic braces and supports market away from commodity neoprene sleeves toward engineered, sensor-enabled devices that slot into post-acute care pathways. Nearly 595 million people worldwide were living with osteoarthritis in 2020, and the absolute case count is on course to approach 1 billion by 2050. Parallelly, the global population aged 60 and above reached 1.4 billion in 2025, concentrating demand in health-system-ready regions that reimburse durable medical equipment. Lighter carbon-fiber and PEEK constructions improve patient compliance by trimming brace mass 30-40% while retaining load dispersal, and early movers already embed inertial sensors that feed range-of-motion data into remote-therapy dashboards.

Key Report Takeaways

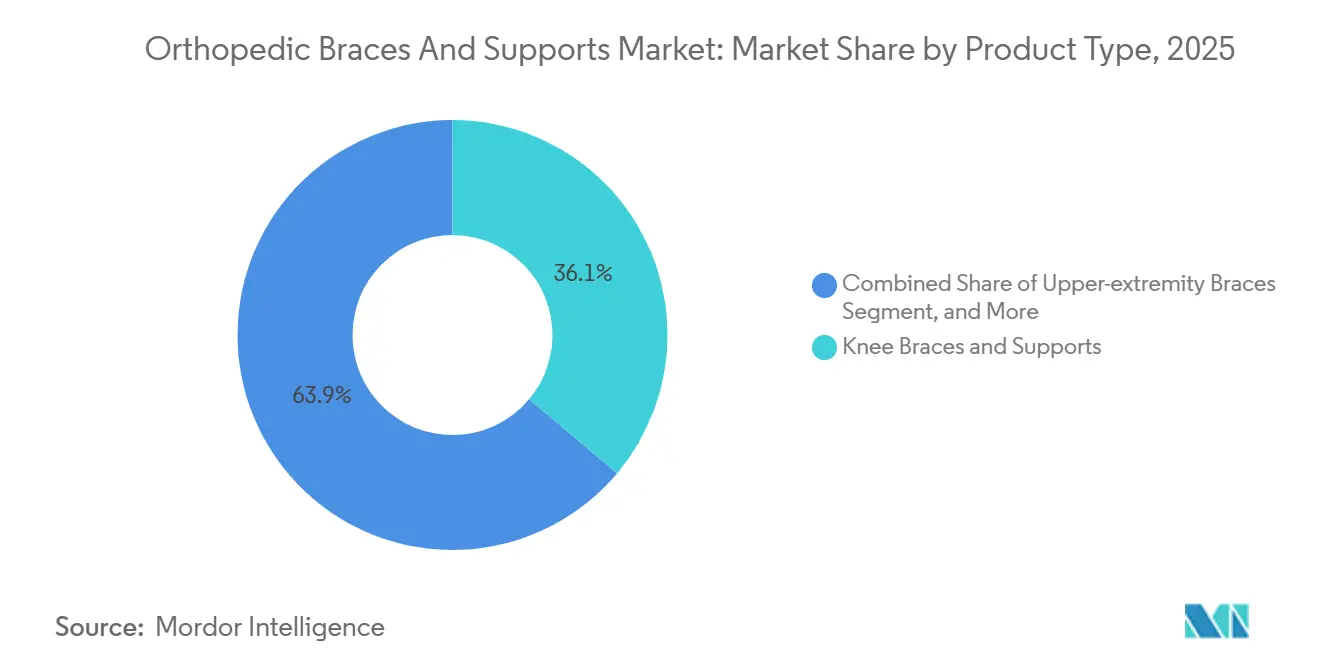

- By product type, knee braces and supports led with 36.11% of orthopedic braces and supports market share in 2025, and upper-extremity braces are forecast to post the fastest 6.06% CAGR through 2031.

- By application, ligament injury accounted for 39.27% revenue in 2025, and post-operative rehabilitation is projected to expand at an 8.63% CAGR to 2031.

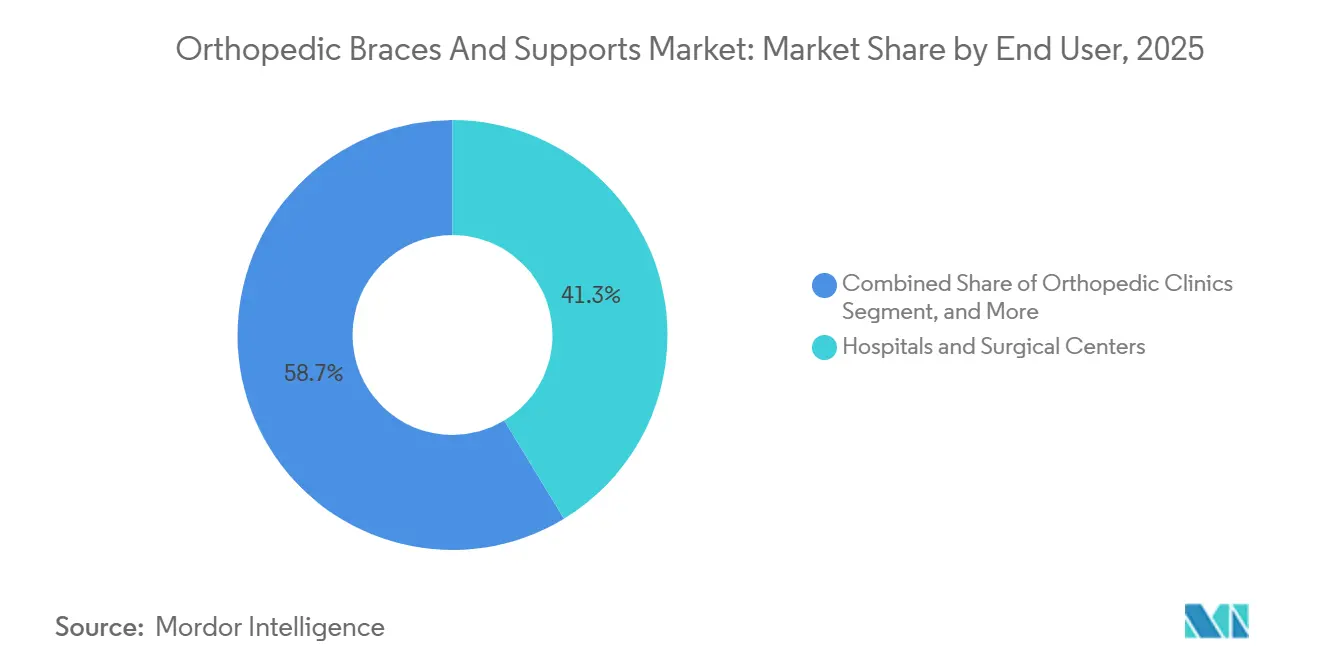

- By end user, hospitals and surgical centers accounted for 41.32% of the orthopedic braces and supports market in 2025, and orthopedic clinics posted the highest 8.18% CAGR through 2031.

- By geography, North America commanded 39.78% of the revenue share in 2025, and Asia-Pacific is expected to grow at a 7.27% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Orthopedic Braces And Supports Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Osteoarthritis & MSDs | +1.2% | Global, with concentration in North America & EU | Long term (≥ 4 years) |

| Growing Geriatric Population | +1.0% | Global, peak impact in Japan, EU, North America | Long term (≥ 4 years) |

| Increasing Sports-Related Injuries | +0.6% | North America, EU, APAC urban centers | Medium term (2-4 years) |

| Advancements in Lightweight Materials | +0.8% | Global, early adoption in North America & EU | Medium term (2-4 years) |

| IoT-Enabled Smart Braces Adoption | +0.5% | North America, EU, APAC tech hubs | Short term (≤ 2 years) |

| Direct-To-Consumer E-Commerce Channels | +0.4% | Global, led by North America & APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Osteoarthritis & MSDs

Global osteoarthritis prevalence climbed 113% between 1990 and 2020 and is projected to reach 1 billion cases by 2050, ensuring a large, recurring user base for knee and hip bracing. Middle-income Asia and Latin America will supply most net new cases, favoring low-cost sleeves, whereas mature payers in North America reimburse custom unloaders. In 2024 the CDC confirmed 58.5 million U.S. adults carried an arthritis diagnosis, underpinning a predictable brace replacement cycle.[1]Centers for Disease Control and Prevention, “Arthritis Data and Statistics,” cdc.gov Vendors that segment portfolios by price tier can capture both cash-pay demand and reimbursed premium demand. Disease-driven baseline turnover thus anchors the orthopedic braces and supports market.

Growing Geriatric Population

By 2025, 29% of Japan’s population was aged 65 and older, underscoring the need for lightweight ankle-foot orthoses compatible with robotic gait aids. Globally, the 60-plus cohort hit 1.4 billion in 2025 and will reach 2.1 billion by 2050. Older adults consume braces at higher per-capita rates, yet payers encourage preventive bracing that delays costly surgery. Europe’s dependency ratio, climbing from 34% in 2025 to 57% by 2050, heightens fiscal pressure, spurring policy support for home-based supports that maintain mobility.

Increasing Sports-Related Injuries

Eleven years of Olympic data show track and field athletes sustain 127 injuries per 1,000 athlete-days, with knee and ankle injuries dominating.[2]Soligard T. et al., “IOC Consensus Statement on Load in Sport,” bjsm.bmj.com Youth baseball’s Pitch Smart rules, now adopted in 38 U.S. states, recommend elbow bracing for pitchers exceeding 80 innings. CrossFit’s 15,000 gyms worldwide contribute to overuse injuries of the wrist and lumbar spine, driving demand for quick-release braces. Athlete safety mandates thus funnel fresh volume into the orthopedic braces and supports market.

Advancements in Lightweight Materials

PEEK and braided carbon-fiber shells cut brace weight up to 40% without compromising rigidity.[3]Zhang Y. et al., “PEEK in Orthopedic Applications,” springer.com Auxetic lattices under test for ankle supports absorb inversion energy better than neoprene while remaining breathable. Three-dimensional printing reduces custom-brace lead times from three weeks to five days. Material science is therefore widening the performance-price gap between premium and basic SKUs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Sophisticated Braces | -0.7% | Global, acute in LMICs | Medium term (2-4 years) |

| Reimbursement Hurdles for OTC Products | -0.5% | North America, EU | Short term (≤2 years) |

| Proliferation of Counterfeit Products | -0.3% | Global, intense in APAC & online | Short term (≤2 years) |

| Patient Non-Compliance Due to Discomfort | -0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Sophisticated Braces

Custom unloaders cost USD 600-800, while smart braces top USD 1,200, pricing out self-pay buyers in India, Indonesia, and Brazil. WHO data show out-of-pocket spending exceeds 50% of health expenditure in 35 LMICs, capping premium penetration. Tiered offerings, such as Össur’s polypropylene “Select” line, which trims bill-of-materials by 40%, aim to bridge the gap.

Reimbursement Hurdles for OTC Products

CMS excludes non-prescribed off-the-shelf braces from coverage and will roll nationwide competitive bidding to 2028, historically trimming payments 10-15%. 62% of U.S. commercial plans now require proof of failed conservative therapy before approving custom knee braces. Shrinking reimbursement threatens mid-tier innovation even as high-end devices secure new RTM codes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Upper-Extremity Gains Outpace Knee Dominance

Knee braces retained a commanding 36.11% share of the orthopedic braces and supports market in 2025, buoyed by widespread ACL injuries and medial knee osteoarthritis. However, upper-extremity devices, led by shoulder and elbow supports, are forecast to grow at a 6.06% CAGR through 2031, outstripping all other categories. Rotator cuff repairs in the United States rose 8% year-on-year in 2024, driving sustained demand for abduction pillows and slings. Youth baseball guidelines further normalize prophylactic elbow bracing, extending replacement cycles.

Ankle and foot bracing is polarizing between low-cost elastic sleeves and custom ankle-foot orthoses for drop-foot. Zimmer Biomet’s 2025 acquisition of Paragon 28 underlines its bet on specialty extremity growth. Lumbar-sacral orthoses face tighter CMS coverage, lengthening approval timelines. Niche hip and pelvic solutions remain tethered to post-surgery protocols and have limited uptake for osteoarthritis.

By Application: Post-Operative Rehabilitation Surges on ERAS Adoption

Ligament injury applications captured 39.27% of 2025 revenue but are slowing as accelerated ACL protocols shorten immobilization windows. In contrast, post-operative rehabilitation braces are projected to climb at an 8.63% CAGR to 2031, supported by ERAS pathways that mandate early, brace-assisted mobilization. A 2024 meta-analysis found that hinged knee braces trimmed the total knee arthroplasty length of stay by 1.2 days, reinforcing their clinical utility.

Preventive-care bracing underperforms due to high abandonment among asymptomatic users, while unloader knee braces continue to delay arthroplasty 2-4 years in early osteoarthritis. Chronic-disease orthoses for conditions like cerebral palsy sustain stable demand but face incremental share erosion from advances in biologic therapies.

By End User: Orthopedic Clinics Capture Outpatient Migration

Hospitals and surgical centers accounted for 41.32% of the orthopedic braces and supports market in 2025, driven by immediate post-surgical fitting. Nevertheless, orthopedic clinics are forecast to expand at an 8.18% CAGR through 2031 as payers migrate joint-preservation procedures to ambulatory settings. Outpatient orthopedic visits in the United States grew 11% in 2024, while inpatient volumes fell 3%. Almost half of private orthopedic groups now dispense braces on-site, capturing device margins and improving adherence.

Homecare settings gain momentum with CMS Remote Therapeutic Monitoring codes reimbursing clinicians for reviewing sensor data. Sports and rehab centers cater to a self-pay, performance-oriented clientele willing to invest in premium designs.

Geography Analysis

Asia-Pacific is projected to post a 7.27% CAGR from 2026-2031, outpacing every other region. China cut Class II orthotic review times to nine months in 2024, aligning documentation with ISO 13485 and lowering barriers for multinationals. India’s Production Linked Incentive scheme offers a 5% rebate on incremental domestic sales, encouraging global brands to set up local production lines. Japan’s super-aged society drives adoption of light, low-profile devices compatible with robotic exoskeletons, reinforcing the smart-brace frontier.

North America, anchored by Medicare DMEPOS reimbursement, retained a 39.78% share in 2025 but faces future margin compression from nationwide competitive bidding starting in 2028. Europe fragments along reimbursement lines; Wales’ GBP 7.6 million framework in 2024 sliced procurement costs 12% while standardizing pathways. The Middle East invests in sports clinics ahead of major events, whereas South America charts divergent paths: Brazil expands SUS reimbursement, while Argentina prioritizes locally made elastic supports amid currency curbs.

Mordor Intelligence provides coverage of the orthopedic braces and supports market across other key regional markets, including Middle East, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to India incorporating local coverage and market participation, as required.

Competitive Landscape

Top vendors Össur, Enovis (DJO), Bauerfeind, Zimmer Biomet, and 3M collectively accounted for a significant portion of global revenue in 2025, signaling moderate concentration. Zimmer Biomet’s USD 1.2 billion acquisition of Paragon 28 consolidated its foot-and-ankle franchise, while Johnson & Johnson will spin off the USD 9.2 billion DePuy Synthes unit by 2027 to sharpen its orthopedic focus. Smaller innovators exploit direct-to-consumer channels; Bauerfeind lifted online sales to 28% of European revenue in 2024 through instructional content.

Sensor integration is a pivotal battleground. Multiple smart braces cleared 510(k) loops in 2025, yet a lack of data-exchange standards fragments the ecosystem. Patent filings mentioning “negative Poisson’s ratio” or “thermoregulation” in brace designs jumped 34% year-over-year. Strategic investments such as Thuasne’s CAD 5 million stake in Bionic Power’s energy-harvesting Agilik knee orthosis blur lines between passive support and active exoskeletons.

Orthopedic Braces And Supports Industry Leaders

Zimmer Biomet

Ottobock SE & Co. KGaA

Össur

3M

Enovis (DJO)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: OrthoPediatrics Corp expanded its Specialty Bracing division with the OPSB Sensor System and MOVE-D brace.

- May 2024: Thuasne acquired Corflex Global to deepen U.S. coverage and streamline orthopedic bracing sales.

- April 2024: Solventum finalized its separation from 3M, launching as an independent healthcare enterprise with USD 8.2 billion revenue.

- January 2024: Enovis released the DonJoy ROAM OA knee brace featuring magnetic alignment clips and a ‘Set-and-Forget’ tension system.

Global Orthopedic Braces And Supports Market Report Scope

As per the scope of the report, orthopedic braces and supports are common under orthopedic supplies but are sometimes misunderstood as part of recuperative medicine. These are usually made of rigid materials, such as hard plastics, and soft materials, such as spandex, and are mostly used to immobilize joints, allowing them to heal in an effective position.

The Orthopedic Braces and Supports Market Report is Segmented by Product Type (Knee Braces & Supports, Ankle & Foot Braces, Back & Spine Braces, Upper-extremity Braces, Hip & Pelvic Braces, Others), Application (Ligament Injury, Preventive Care, Post-operative Rehabilitation, Osteoarthritis, Other Chronic Conditions), End User (Hospitals & Surgical Centers, Orthopedic Clinics, Homecare Settings, Sports & Rehabilitation Centers), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Knee Braces & Supports |

| Ankle & Foot Braces |

| Back & Spine Braces |

| Upper-extremity Braces |

| Hip & Pelvic Braces |

| Others |

| Ligament Injury |

| Preventive Care |

| Post-operative Rehabilitation |

| Osteoarthritis |

| Other Chronic Conditions |

| Hospitals & Surgical Centers |

| Orthopedic Clinics |

| Homecare Settings |

| Sports & Rehabilitation Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Knee Braces & Supports | |

| Ankle & Foot Braces | ||

| Back & Spine Braces | ||

| Upper-extremity Braces | ||

| Hip & Pelvic Braces | ||

| Others | ||

| By Application | Ligament Injury | |

| Preventive Care | ||

| Post-operative Rehabilitation | ||

| Osteoarthritis | ||

| Other Chronic Conditions | ||

| By End User | Hospitals & Surgical Centers | |

| Orthopedic Clinics | ||

| Homecare Settings | ||

| Sports & Rehabilitation Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the orthopedic braces and supports market?

The orthopedic braces and supports market size reached USD 4.99 billion in 2026 and is forecast to hit USD 6.12 billion by 2031.

Which product category is growing fastest?

Upper-extremity braces are projected to record the quickest 6.06% CAGR through 2031, buoyed by rising rotator cuff and elbow ligament procedures.

How significant is Asia-Pacific to future growth?

Asia-Pacific is forecast to expand at a 7.27% CAGR between 2026-2031, supported by streamlined regulations in China and manufacturing incentives in India.

Are smart braces reimbursed?

In the United States, sensor-enabled braces can qualify for Remote Therapeutic Monitoring codes introduced in 2024, providing a pathway to reimbursement.

What are the main barriers to adoption of premium braces?

High device cost, fragmented reimbursement for over-the-counter products, and persistent counterfeit circulation remain the primary hurdles.

Page last updated on: