Orthopedic Prosthetics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.28 Billion |

| Market Size (2031) | USD 5.77 Billion |

| Growth Rate (2026 - 2031) | 6.17% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Orthopedic Prosthetics Market Analysis by Mordor Intelligence

Orthopedic Prosthetics market size in 2026 is estimated at USD 4.28 billion, growing from 2025 value of USD 4.03 billion with 2031 projections showing USD 5.77 billion, growing at 6.17% CAGR over 2026-2031.

Continuous growth is supported by rising diabetes-linked amputations, breakthrough neural-interface limbs, and widening access to lower-cost 3-D printing capabilities that shorten production cycles and improve customization. Demographic aging, coupled with osteoarthritis prevalence, enlarges the addressable user base, while defense-veteran rehabilitation programs in Asia-Pacific accelerate technology diffusion across emerging economies. Competitive differentiation now pivots on real-time sensory feedback, carbon-fiber alternatives, and cybersecurity readiness for connected devices, creating a dynamic landscape in which incumbents and start-ups pursue vertical integration and niche specialization. Tight reimbursement environments and titanium supply shortages temper near-term margins but also motivate manufacturers to streamline supply chains and localize additive manufacturing hubs.

Key Report Takeaways

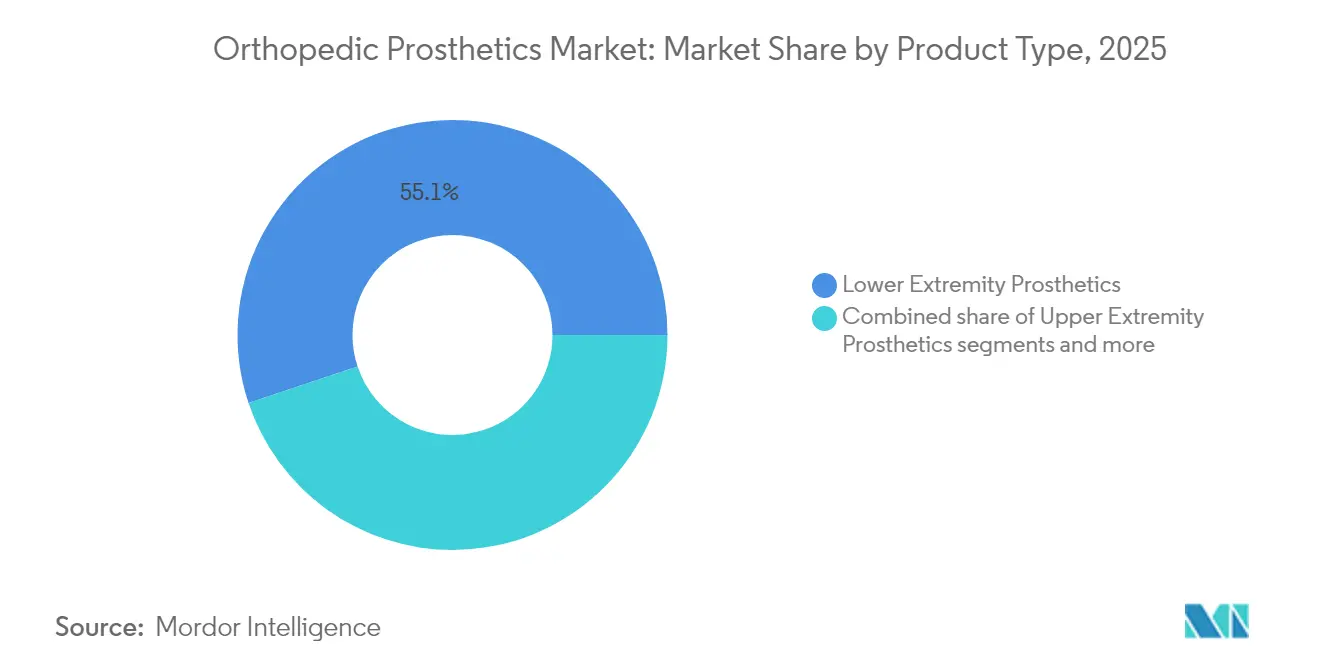

- By product category, lower-extremity prosthetics held 55.12% of the orthopedic prosthetics market share in 2025; liners are projected to post the fastest 9.52% CAGR through 2031.

- By technology, conventional systems led with 45.10% revenue share in 2025, while robotic and microprocessor-controlled devices are forecast to expand at a 9.91% CAGR to 2031.

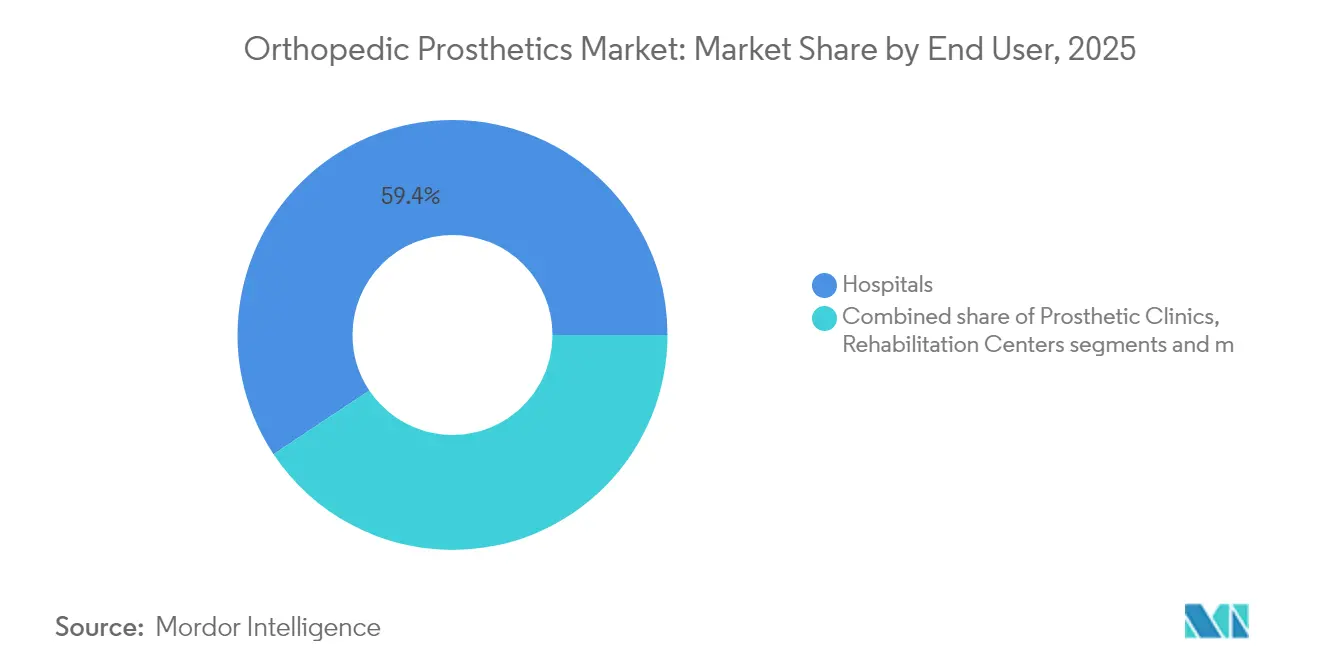

- By end user, hospitals commanded 59.35% of the orthopedic prosthetics market size in 2025, whereas home-care settings will grow the fastest at a 10.32% CAGR between 2026 and 2031.

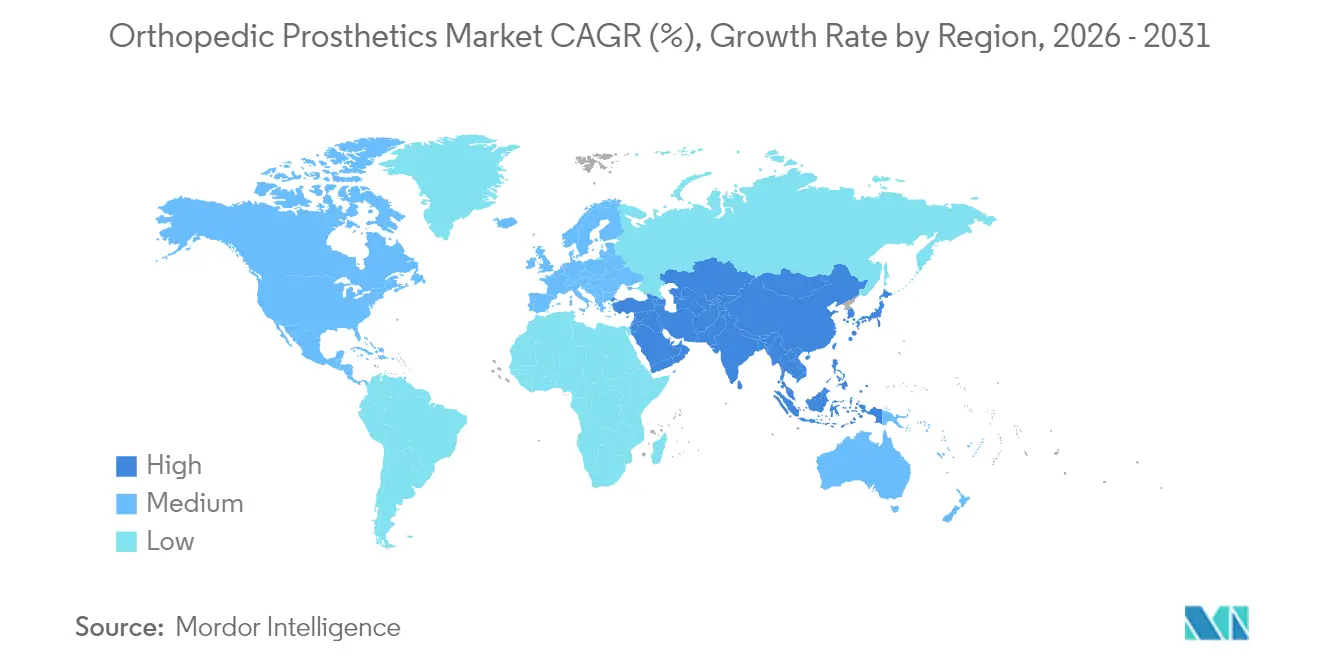

- By geography, North America accounted for 41.88% regional share in 2025; Asia-Pacific is set to record a 10.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Orthopedic Prosthetics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising diabetes-linked amputations | +2.1% | Global, with highest impact in North America and Asia-Pacific | Medium term (2-4 years) |

| Ageing population & osteoarthritis prevalence | +1.8% | Global, particularly developed markets | Long term (≥ 4 years) |

| Advancements in microprocessor & myoelectric limbs | +1.5% | North America, Europe, Asia-Pacific core markets | Medium term (2-4 years) |

| Expansion of 3-D printing service hubs in emerging markets | +1.2% | Asia-Pacific, Latin America, Middle East and Africa | Short term (≤ 2 years) |

| Defence-veteran rehab funding surge in Asia-Pacific | +0.9% | Asia-Pacific, with spillover to other regions | Short term (≤ 2 years) |

| E-commerce aftermarket component sales growth | +0.7% | Global, with early adoption in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Diabetes-Linked Amputations Drive Market Expansion

More than 1 million diabetes-related lower-limb amputations occur yearly, sharply lifting demand for sophisticated socket designs that reduce shear forces and improve infection control for fragile skin surfaces. Specialized foot-care pathways in the United States, China, and India now funnel patients toward earlier prosthetic intervention, bringing forward replacement cycles and expanding recurring component sales. Manufacturers responding to this volume uptick are investing in lighter carbon-composite pylons that accommodate neuropathic gait patterns and reduce energy expenditure. The phenomenon is particularly acute in urban Asia-Pacific where rapid lifestyle changes drive higher diabetes prevalence, aligning regional market expansion with public-health priorities and donor-funded limb-loss initiatives.

Ageing Population Amplifies Osteoarthritis-Related Demand

Median ages are climbing above 40 years in Northern Europe, Japan, and Australia, widening the pool of seniors requiring joint replacements and, in revision scenarios, partial limb prostheses. Baby-boomer cohorts differ from earlier generations by insisting on high-activity prosthetic knees that support golfing, hiking, and light-jogging. Consequently, design priorities have shifted toward adaptive damping microprocessor units that modulate swing phase in real time. Payers increasingly reimburse for such higher-end devices when linked to fall-reduction evidence, reinforcing the upgrade cycle for elderly athletes. Hospitals have introduced geriatric-orthopedics programs integrating bone-density screening with prosthetic selection, further supporting sustained device turnover.

Microprocessor and Myoelectric Technology Breakthrough

The MIT agonist–antagonist myoneural interface (AMI) surgery enables 41% faster ambulation, signaling a paradigm shift where brain-computer interfaces deliver proprioceptive feedback unmatched by legacy mechanical limbs. Start-ups are embedding AI classifiers that predict stride intent milliseconds ahead, smoothing transitions on uneven ground. Pilot reimbursement codes for powered knees, such as HCPCS L5827, establish clearer payment pathways and encourage supplier adoption. As algorithmic tuning occurs over the cloud, cybersecurity resilience becomes mandatory; the FDA’s 2025 guidance now treats threat-modelling documentation as a gating item for pre-market approval.

3-D Printing Democratizes Access in Emerging Markets

Low-cost additive manufacturing reduces socket production times from weeks to hours, enabling rural clinics to stock digital design libraries instead of physical inventories. Community fabrication labs in Vietnam and Indonesia utilize low-cost prosthetic fabrication workflows that achieve comfort outcomes comparable to those of overseas imports. Latin American municipalities now procure pediatric hands for USD 50 to USD 500, replacing legacy donations that once exceeded USD 50,000. Multinational vendors are partnering with local bureaus to validate polymer strength and create last-mile distribution networks, thereby embedding themselves inside nascent value chains long before income thresholds justify premium imports.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device cost & inconsistent reimbursement | -1.4% | Global, with highest impact in emerging markets | Medium term (2-4 years) |

| Shortage of certified prosthetists in developing nations | -0.8% | Asia-Pacific, Latin America, Middle East and Africa | Long term (≥ 4 years) |

| Titanium & carbon-fibre supply bottlenecks | -0.6% | Global, with particular impact on North America and Europe | Short term (≤ 2 years) |

| Cyber-security scrutiny of smart prosthetics | -0.4% | North America, Europe, Asia-Pacific core markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Reimbursement Inconsistencies Constrain Market Access

Medicare beneficiaries in the United States still pay USD 3,580 out-of-pocket per limb despite insurance, a barrier prompting device abandonment that reduces replacement cycles and aftermarket sales. France’s 25% reimbursement cut in 2025 led to supplier exits and sporadic implant shortages, underscoring how policy swings reshape supply availability. Start-ups counteract margin pressure by leasing rather than selling microprocessor knees, bundling software updates and maintenance into subscription plans aligned with payer budget cycles.

Workforce Shortages Limit Service Delivery Capacity

Australia records only 1.62 prosthetists per 100,000 inhabitants, a ratio even lower across Southeast Asia and sub-Saharan Africa, thereby capping procedural throughput regardless of device stock. Tele-fitting platforms using 3-D limb scanners mitigate rural gaps, yet regulatory frameworks for remote alignment remain immature. Government scholarships and fast-track certification modules are being piloted in Indonesia and Kenya, but impact will materialize over the long term. Vendors are therefore embedding clinician-guided video tutorials and AI-driven pressure-map analytics into their service offerings to de-skill certain adjustment tasks for community health workers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Lower-Extremity Dominance Faces Liner Innovation

Lower-extremity solutions represented 55.12% of the orthopedic prosthetics market size in 2025, anchored by high-incidence transtibial and transfemoral procedures. Demand concentration creates scale economies that manufacturers leverage to fund R&D for next-generation rotary adapters that tolerate higher torsional loads during sports. Liners, while a smaller revenue pool, deliver 9.52% CAGR through 2031 by addressing skin-sweat management and residual-limb volume fluctuation, two factors strongly correlated with device abandonment. New thermoplastic elastomer gels infused with antimicrobial nanoparticles extend liner replacement intervals, generating recurring sales with minimal clinical oversight. Specialty-sports prosthetics, though niche, attract premium pricing and act as branding showcases that inspire mainstream upper-limb upgrades. The orthopedic prosthetics market share for sockets climbs gradually as custom 3-D printed lattices displace hand-laminated fiberglass shells, reducing weight by 30% and improving airflow for marathon runners.

By Technology: Conventional Systems Yield to Robotic Innovation

Conventional passive limbs kept 45.10% revenue share in 2025 because of affordability and long-proven reliability in low-mobility users. Nonetheless, robotic and microprocessor-controlled platforms are accelerating at a 9.91% CAGR, expanding the orthopedic prosthetics market size for high-performance devices. Algorithmic knees such as BionicM’s unit, retailing near USD 51,000, integrate cloud-updateable firmware, allowing functionality enhancements without hardware swaps. Hybrid constructs merge myoelectric wrists with passive elbow locks to tailor value-to-cost ratios by activity class. Meanwhile, additive manufacturing slashes bill-of-materials by up to 40% for entry-level feet, enabling regional distributors to price aggressively while protecting margins through local resin sourcing.

Sensor miniaturization and low-power Bluetooth mesh further embed limbs inside hospital IoT ecosystems, enabling remote gait analytics yet also raising vulnerability to cyber intrusions addressed in the latest FDA guidance.

By End User: Hospital Dominance Shifts Toward Home Care

Hospitals and pharma-biotech research units held 59.35% of end-user revenues in 2025, reflecting concentration of surgical expertise and grant-funded clinical trials. However, home-care settings will capture disproportionate incremental growth at a 10.32% CAGR as tele-rehab software unlocks remote physiotherapy sessions and cloud-based gait tuning. Prosthetic clinics remain pivotal for custom fittings, yet their service mix adds subscription sensor-calibration packages that push recurring revenue.

Rehabilitation centers differentiate via VR-enabled balance-training modules that shorten inpatient stays. Ambulatory surgical centers expand revision capacity in urban belts, helping decongest tertiary hospitals. Military and veteran agencies continue to pour R&D funds—USD 150 million approved for FY 2025—directly shaping component specifications for harsh-terrain operability and waterproofing.

Geography Analysis

North America retained 41.88% regional revenue share in 2025, powered by insurance coverage that reimburses high-end microprocessor knees and arms, as well as dense networks of certified practitioners. The United States drives regional innovation, hosting landmark AMI and OMP research that secures technology-leadership halo effects across the orthopedic prosthetics market. Canada leverages cross-provincial tele-orthotics platforms to extend access to northern communities, whereas Mexico integrates maquiladora clusters to co-manufacture lightweight pylons for export.

Asia-Pacific, forecast to rise at a 10.71% CAGR, combines outsized diabetes prevalence with ambitious universal-health coverage rollouts. China’s local innovators accelerate low-cost 3-D printed sockets that undercut imports by 35%. India’s public procurement of modular feet for district-level trauma centers further lifts volume. Japan and South Korea push the frontier in sensory feedback, driving regional demand for advanced firmware upgrades. Australia, despite practitioner scarcity, maintains high adoption of AI-guided alignment tools that compensate for workforce gaps. Regional humanitarian projects, such as remote prosthetic aid in conflict zones, illustrate cross-border dissemination of design files over satellite networks. Europe presents a mature, regulation-intensive environment where price caps squeeze margins yet clinical practice standards remain rigorous. Germany pioneers carbon-fiber recycling initiatives to mitigate material scarcity, while the United Kingdom fast-tracks digital orthopedics pilots under the NHS Long-Term Plan. France’s reimbursement cuts create localized shortages, prompting parallel-import channels and sparking debate on sustainable pricing. South America, Middle East, and Africa collectively account for modest share today yet post high single-digit growth as 3-D printing hubs emerge in Brazil and the UAE, gradually reducing lead times for culturally attuned cosmetic covers and shock-absorbing feet.

Competitive Landscape

The orthopedic prosthetics market remains moderately fragmented, with regional specialists addressing local preferences. Össur posted 9% organic prosthetics growth in Q4 2023, boosted by its acquisition of neuro-orthotics firm FIOR & GENTZ, which expands vertical integration into peripheral-nerve stimulation accessories[1]Source: Össur, “Life Without Limitations,” ossur.com . Ottobock deepened its robotics pipeline by acquiring minority stakes in exoskeleton start-ups, aligning its limb and support-wear portfolios for bundled tenders. Zimmer Biomet secured FDA approval for its cementless partial knee, validating porous-titanium additive processes that may later migrate to transfemoral stems[2]Source: Zimmer Biomet, “Oxford® Cementless Partial Knee approval,” zimmerbiomet.com . Stryker opened an expanded Global Technology Centre in India to co-design cost-down microprocessor ankles aimed at ASEAN insurance formularies. Cybersecurity has emerged as the new battleground: vendors partner with SaaS providers to embed zero-trust architectures before regulators formalize software-bill-of-materials mandates.

Smaller entrants exploit white spaces: Japanese firm BionicM commercializes robotic knees at premium price points for active amputees, while a US-based company, Unlimited Tomorrow, crowd-funds low-cost 3-D printed arms personalized via smartphone scans. Component suppliers diversify alloys away from titanium toward high-manganese steels to mitigate geopolitical supply shocks. Across all tiers, strategic acquisitions remain the vehicle of choice for portfolio extension, illustrated by Stryker’s buyout of Artelon to gain exposure to soft-tissue augments that stabilize prosthetic limb integration.

Orthopedic Prosthetics Industry Leaders

Blatchford Ltd

Fillauer LLC

Willow Wood Global LLC

Ossur

Mobius Bionics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: MIT researchers unveiled a bionic knee that integrates directly with tissue, improving obstacle navigation for above-knee amputees.

- June 2025: Stryker gained FDA 510(k) clearance for its total ankle system, broadening orthopedic coverage.

Global Orthopedic Prosthetics Market Report Scope

Orthopedic prosthetics assist with artificial limbs, bones, and joints. Orthopedic prosthetics involve the use of artificial limbs (prostheses) to enhance the function and lifestyle of individuals with limb loss resulting from trauma, disease, or other medical conditions.

The orthopedic prosthetics market is segmented by product type, technology, end user, and geography. By product type, the market is segmented into upper extremity prosthetics, lower extremity prosthetics, liners, sockets, modular components, and specialty & sports prosthetics. By technology, it is segmented into conventional, electric-powered/myoelectric, hybrid, 3D-printed/additively manufactured, and robotic/microprocessor-controlled. By end user, the market is segmented into hospitals, prosthetic clinics, rehabilitation centers, ambulatory surgical centers, and home-care settings. By geography, the market covers North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The report offers the value (in USD) for the above-mentioned segments.

| Upper Extremity Prosthetics |

| Lower Extremity Prosthetics |

| Liners |

| Sockets |

| Modular Components |

| Specialty & Sports Prosthetics |

| Conventional |

| Electric Powered / Myoelectric |

| Hybrid |

| 3-D Printed / Additively Manufactured |

| Robotic / Microprocessor Controlled |

| Hospitals |

| Prosthetic Clinics |

| Rehabilitation Centers |

| Ambulatory Surgical Centers |

| Home-care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Upper Extremity Prosthetics | |

| Lower Extremity Prosthetics | ||

| Liners | ||

| Sockets | ||

| Modular Components | ||

| Specialty & Sports Prosthetics | ||

| By Technology | Conventional | |

| Electric Powered / Myoelectric | ||

| Hybrid | ||

| 3-D Printed / Additively Manufactured | ||

| Robotic / Microprocessor Controlled | ||

| By End-User | Hospitals | |

| Prosthetic Clinics | ||

| Rehabilitation Centers | ||

| Ambulatory Surgical Centers | ||

| Home-care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the value of the orthopedic prosthetics market in 2026 and how fast is it expanding?

The orthopedic prosthetics market is projected to reach approximately USD 4.28 billion by 2026, expanding at a compound annual growth rate (CAGR) of around 6.17%.

Which region grows the fastest for orthopedic prosthetics market?

Asia-Pacific, with a projected CAGR of 10.71%, grapples with a high diabetes prevalence while ambitiously pursuing universal health coverage.

What is the value in share of the orthopedic prosthetics market in north america in 2026?

The North American share of the orthopedic prosthetics market is expected to be approximately 41.88% of the global market.

What key restraint may slow market expansion?

Reimbursement inconsistencies constrain market access in the orthopedic prosthetics market

Page last updated on: