Tendon Repair Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

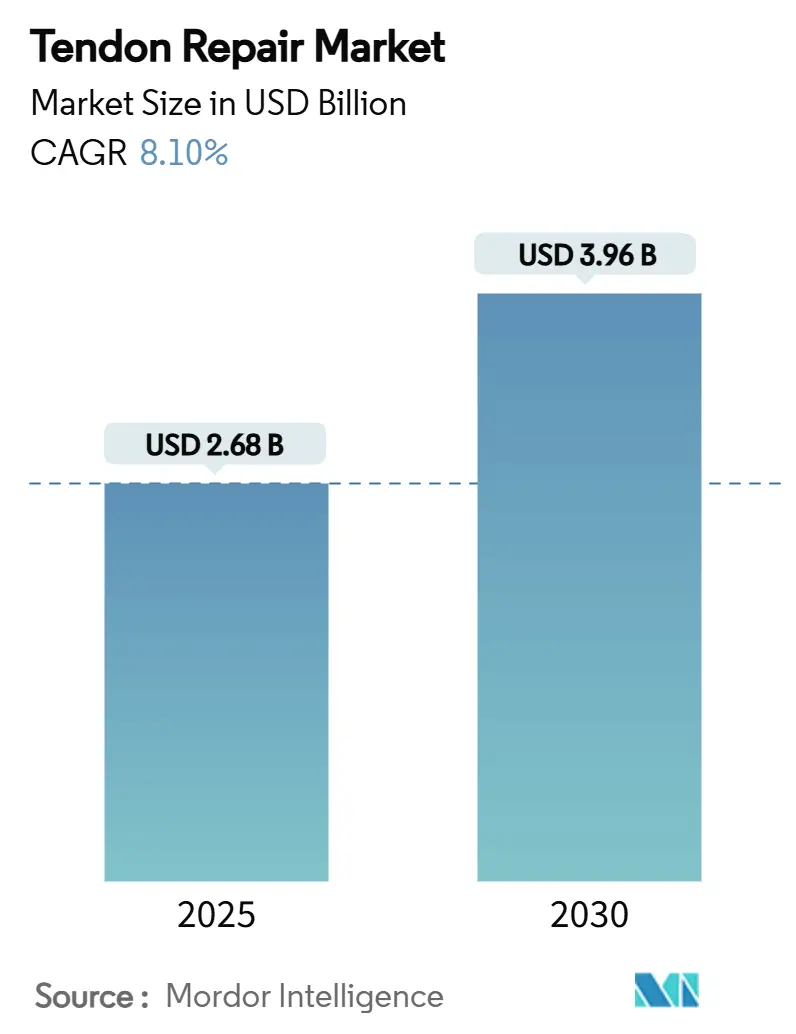

| Market Size (2025) | USD 2.68 Billion |

| Market Size (2030) | USD 3.96 Billion |

| Growth Rate (2025 - 2030) | 8.10% CAGR |

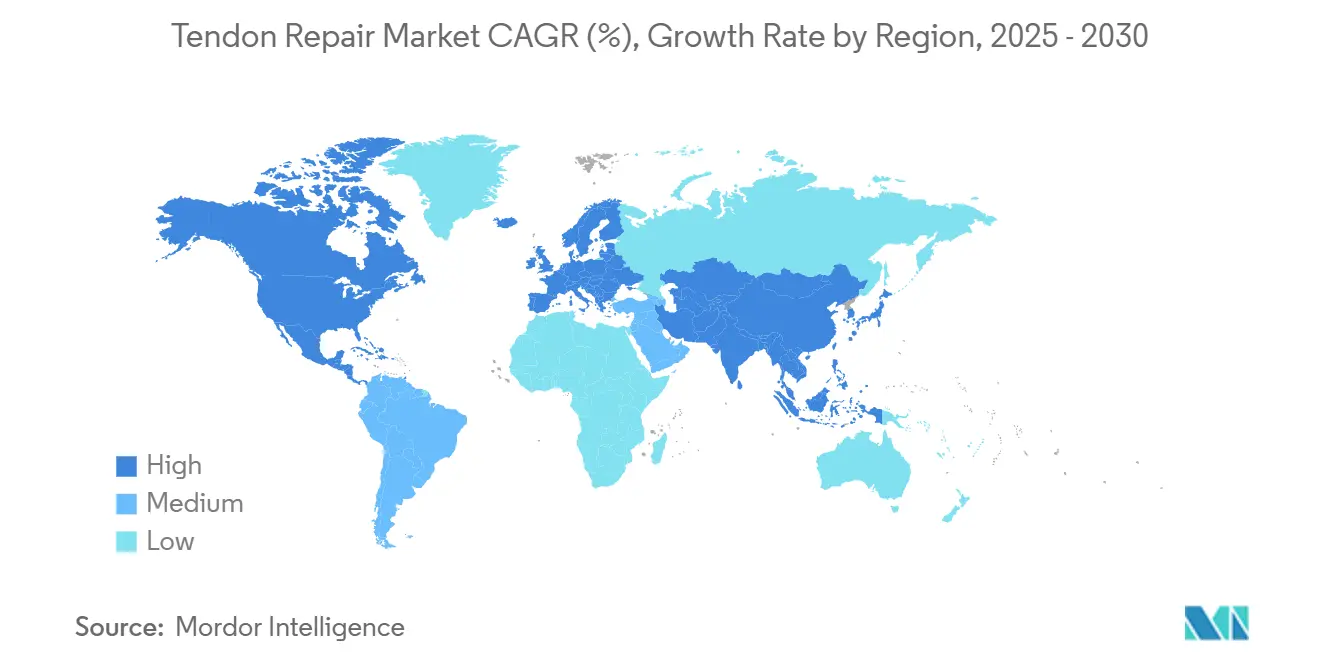

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tendon Repair Market Analysis by Mordor Intelligence

The tendon repair market size stood at USD 2.68 billion in 2025 and is forecast to reach USD 3.96 billion by 2030, expanding at an 8.1% CAGR. Demographic aging, escalating sports‐related injuries, and rapid diffusion of minimally invasive techniques combine to accelerate procedure volumes in every major care setting. Suture anchors currently anchor revenue streams, yet bio-scaffolds and hydrogels now attract investment because they shorten healing timelines and cut revision risk. Rotator cuff repairs preserve clinical primacy, but Achilles procedures are scaling fastest as Asian providers shift decisively toward surgery. Regional performance is bifurcating: North America safeguards leadership through reimbursement clarity, while Asia Pacific outpaces on procedure growth. Consolidation among device makers, typified by Stryker’s 2024 Artelon buyout, is aligning strong distribution networks with fast-moving biologics portfolios, keeping competitive intensity at a moderate level.

Key Report Takeaways

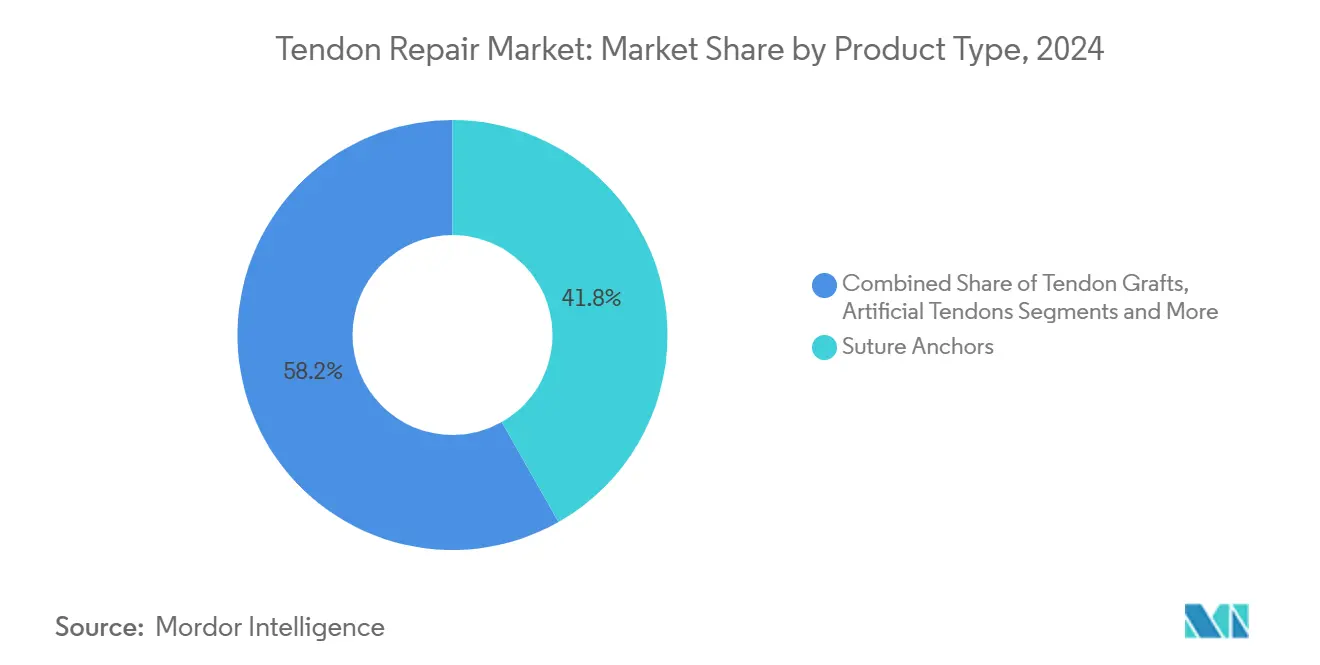

- By product type, suture anchors held 41.8% of the tendon repair market share in 2024, while bio-scaffolds and hydrogels are projected to expand at a 9.2% CAGR through 2030.

- By application, rotator cuff repairs accounted for a 47.5% share of the tendon repair market size in 2024; Achilles tendon procedures are advancing at a 10.9% CAGR to 2030.

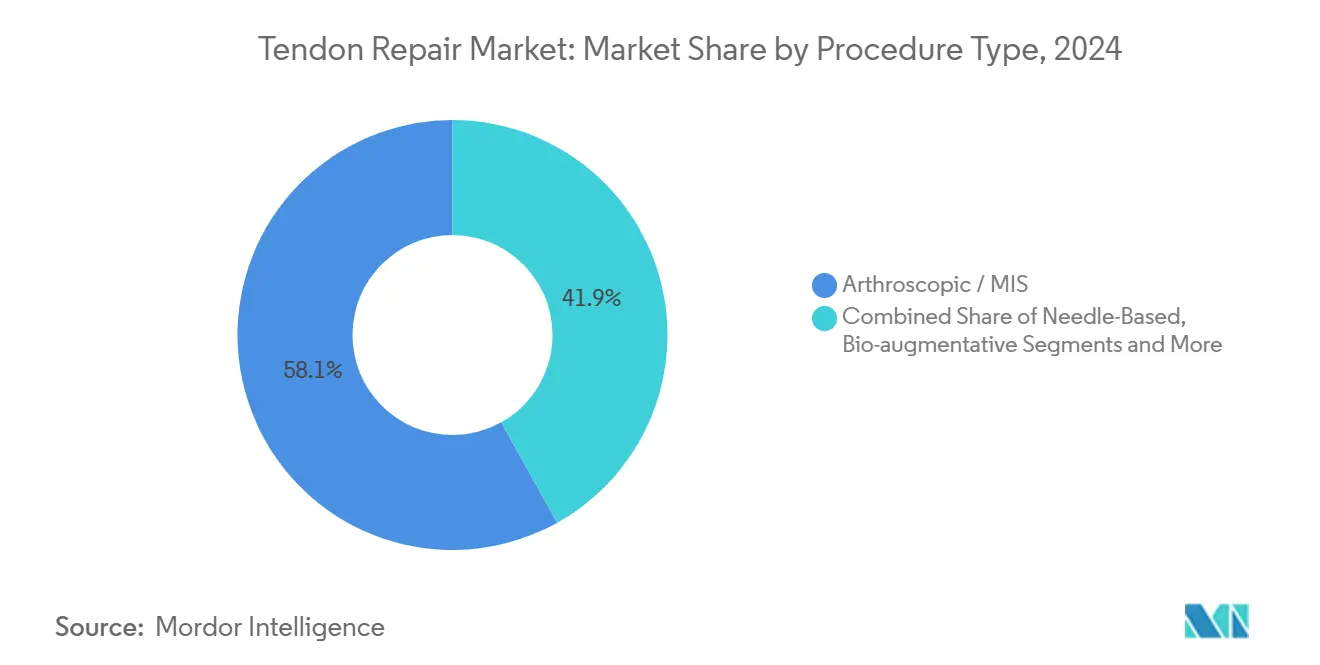

- By procedure type, arthroscopic and minimally invasive techniques captured 58.1% of all cases in 2024, whereas bio-augmentative methods are forecast to grow at an 11.1% CAGR through 2030.

- By end user, hospitals commanded 53.2% of 2024 revenue, while sports medicine and rehabilitation centers are poised for a 10.5% CAGR through 2030.

- By geography, North America led with 38.8% revenue share in 2024; Asia Pacific is projected to post a 9.8% CAGR between 2025 and 2030.

Global Tendon Repair Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sports-injury incidence surge | +1.80% | North America, Europe – spreading globally | Medium term (2-4 years) |

| Ageing-related tendon degeneration | +2.10% | APAC, North America – global significance | Long term (≥ 4 years) |

| Shift to minimally invasive & arthroscopic | +1.50% | North America, EU – rising in APAC | Short term (≤ 2 years) |

| Reimbursement expansion for outpatient care | +1.20% | North America, selective EU markets | Medium term (2-4 years) |

| Next-gen bio-scaffolds & hydrogels | +0.90% | North America, EU – adopted worldwide | Medium term (2-4 years) |

| Gene/RNA-based therapies enter pipelines | +0.60% | North America, EU – early adoption phase | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sports-Injury Incidence Surge

Participation in high-intensity athletics by both youth and older adults is widening the injury pool, making sports trauma a cornerstone demand driver for the tendon repair market. National Football League injury surveillance mirrors societal patterns, with Achilles ruptures trending upward and reinforcing device demand.[1]Timothy E. Hewett, “Have Achilles Tendon Injuries Significantly Increased in the NFL?” PubMed, pubmed.ncbi.nlm.nih.gov Lifestyle changes that favor year-round recreational leagues create steady case inflow and reshape design priorities toward performance preservation. Economic stakes are high: faster return-to-work shortens productivity losses and appeals to payers seeking quantifiable savings. Manufacturers, therefore, invest in implants that balance durability with biologic friendliness to meet the expectations of athletes and employers alike. Sports-medicine centers capitalize on these dynamics by bundling surgery with accelerated rehabilitation pathways that promise swift functional recovery.

Ageing-Related Tendon Degeneration

Longer life expectancy now coincides with active retirement, creating a large cohort whose tendons exhibit reduced cellular resilience. Studies show that tendon stem/progenitor cells from older adults enter premature senescence marked by p16 INK4A overexpression, impeding natural regeneration.[2]Julia R. Köhler et al., “Cellular Changes in Tendon Aging,” Wiley Online Library, onlinelibrary.wiley.com This biological constraint sustains premium demand for scaffolds and biologics that can jump-start healing. Policymakers increasingly reimburse preventive interventions, recognizing that durable repairs avert expensive revisions and preserve independence. Device developers are therefore tailoring implants to offset age-related deficits, integrating inductive coatings that prompt collagen synthesis even in senescent tissue. As populations in Japan, China, and Western Europe skew older, such technologies have moved from niche to mainstream inside the tendon repair market.

Technique Shift to Minimally Invasive & Arthroscopic Repair

Surgeons now favor arthroscopic portals that minimize trauma and shorten hospital stay. The Percutaneous Achilles Repair System (PARS) delivers outcomes equivalent to open techniques yet lowers wound complication risk. Cost studies confirm that high-volume ambulatory centers trim USD 16,987 per graft repair relative to inpatient settings.[3]Aslı Çalışkan Uçkun, “Predicting Reoperation After Hand Flexor Repair,” jag.journalagent.com These savings sway payers toward outpatient approvals, thereby reinforcing the procedure of migration. Device makers respond by miniaturizing instrumentation and offering comprehensive kits that simplify portal creation. Training demand has climbed, funneling surgeons into specialized courses that sustain brand loyalty and stabilize consumable sales within the tendon repair market.

Reimbursement Expansion for Outpatient Tendon Procedures

Medicare’s bundled payments now cover primary flexor tendon repairs at USD 2,700.87 and secondary cases at USD 6,264.95, validating the outpatient economic model. Private insurers shadow these schedules, smoothing adoption curves for novel implants that demonstrate reduced re-tear rates. Geographic variance persists, but markets with favorable codes witness rapid up-titration of advanced bio-scaffolds even at premium list prices. Value-based care contracts reward devices that curtail revision incidence, nudging providers toward evidence-rich platforms. This alignment of clinical outcomes and payment incentives propels the tendon repair market toward biologics that show quantified long-term benefit.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced fixation & biologics | -1.40% | Global – sharper in emerging markets | Short term (≤ 2 years) |

| Post-surgical re-tear & adhesion rates | -1.10% | Global | Medium term (2-4 years) |

| Shortage of specialized orthopedic surgeons | -0.80% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Regulatory uncertainty around cell implants | -0.50% | Global, jurisdiction dependent | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Fixation & Biologic Products

Budget-constrained systems in Latin America and Southeast Asia gravitate toward generic anchors that slash USD 1,397.51 per case but still meet baseline outcome metrics. Price resistance narrows adoption channels for premium biologics, forcing suppliers to deploy tiered offerings. Training fees and inventory logistics inflate the total cost of ownership, further deterring smaller ambulatory centers. Consequently, device makers craft value-based pricing models aligned to durability data to sidestep sticker shock and safeguard the tendon repair market’s margin profile.

Post-Surgical Re-Tear & Adhesion Rates

Rotator cuff failure hovers near 20% in select cohorts, inflating revision risk and dampening patient confidence. Each reoperation entails 114 lost workdays and an elevated complication probability. Surgeons increasingly pair mechanical fixation with biologic augmentation to stem these losses, yet evidence remains heterogeneous. The market, therefore, prizes implants backed by randomized trials such as the REGENETEN bioinductive patch that cuts re-tear by 68%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bio-Scaffolds Drive Innovation

Bio-scaffolds and hydrogels posted the fastest 9.2% CAGR through 2030 as surgeons pursue biologically active solutions that overcome intrinsic healing limits. Suture anchors still generated 41.8% of 2024 revenue because they remain indispensable for reliable fixation during early load cycles. Evidence shows that injectable bioactive glass-alginate hydrogels speed angiogenesis without heterotopic ossification. The tendon repair market consequently rewards vendors that bundle anchors with compatible bio-scaffolds to simplify procedure planning. Electrical stimulation research underscores tendons’ piezoelectric response, fueling prototypes that couple fixation with microcurrent delivery, adding another dimension of differentiation.

Fixation devices beyond anchors, tendon grafts, and emerging artificial ligaments round out portfolios addressing complex reconstructions. Autograft and allograft materials sustain relevance for large defects, while synthetic ligaments address traumatic tissue loss. Product roadmaps are shifting toward bio-hybrid constructs that merge collagen matrices with slow-release growth factors. Such versatility positions vendors to capture upgrade cycles as hospitals refresh instrument trays to stay at the front of the tendon repair market.

By Application: Achilles Procedures Accelerate

Rotator cuff repairs retained 47.5% of 2024 case mix owing to age-driven degeneration, but Achilles tendon procedures now post the highest 10.9% CAGR. Japan exemplifies the shift: surgeries rose from 67% to 72% between 2010 and 2017. Minimally invasive supine approaches cut operating time by 30 minutes and improve outcomes, amplifying surgeon adoption.

Hand flexor and extensor repairs sustain steady demand due to workplace trauma, while patellar and quadriceps cases concentrate in sports medicine. Niche repairs of biceps and peroneal tendons complete the spectrum, each requiring tailored implants and rehab protocols. As clinical evidence increasingly supports early Achilles surgery for active adults, device makers widen inventories of percutaneous repair kits, reinforcing diversification within the tendon repair market.

By Procedure Type: Bio-Augmentative Methods Lead Growth

Arthroscopic and percutaneous techniques commanded 58.1% of all procedures in 2024 because they align with payer incentives for outpatient care. However, bio-augmentative approaches—platelet-rich plasma, stem cell injections, and gene therapies—clock an 11.1% CAGR, reflecting clinician desire to address biologic deficits rather than rely solely on hardware. MicroRNA-infused hydrogels targeting CXXC4 illustrate the translational momentum of gene therapy platforms.

Open surgery remains essential for massive tears and chronic defects, but case share continues to slip as instrument innovation simplifies minimally invasive access. Revision surgeries form a meaningful volume segment, driven by primary repair failures and rising patient expectations, which in turn sustains demand for next-generation bio-patches. Together, these trajectories anchor procedural diversity at the core of the tendon repair market.

By End User: Sports Medicine Centers Gain Momentum

Hospitals generated 53.2% of global revenue in 2024 by handling complex trauma, but sports medicine and rehabilitation centers advanced at a 10.5% CAGR by focusing on rapid return-to-play protocols. High-volume ambulatory surgical centers combine cost efficiency with predictable throughput, channeling more routine tendon procedures away from inpatient wards.

Specialty orthopedic clinics serve as referral hubs, offering intermediate complexity care and fuelling ecosystem collaboration. Military and trauma units represent a smaller yet strategic end-user subset owing to stringent readiness requirements. As reimbursement models reward outpatient efficiency, vendors tailor product lines for sterile-field versatility, ensuring broad compatibility and cementing stickiness across end-user tiers in the tendon repair market

By Injury Site: Specialized Treatment Protocols

Achilles injuries headline growth at 10.9% CAGR due to procedural migration toward surgery and improved implant options. Rotator cuff cases still dominate volume, leveraging sophisticated arthroscopic portals and biologic augmentation for stronger repairs. Hand and wrist tendons, though smaller in market share, demand high-precision hardware and custom rehab, ensuring steady device turnover.

Each anatomic site influences implant choice, from load distribution to suture trajectory, prompting manufacturers to design site-specific toolkits. Research into enthesis biology guides tailored biomaterial selection, accentuating specialization trends that deepen competitive moats in the tendon repair market.

Geography Analysis

North America maintained a 38.8% revenue share in 2024, reflecting extensive insurer coverage, entrenched surgical expertise, and an innovation-friendly regulatory climate. Medicare’s dedicated codes for outpatient tendon repair accelerate the adoption of premium biologics and support the use of bundled payment models. Academic research consortia streamline multicenter trials, expediting proof-of-concept validation and keeping the tendon repair market vibrant with early-stage technologies. Corporate partnerships between providers and manufacturers promote clinician education, reinforcing North American leadership.

Asia Pacific delivered the highest 9.8% CAGR after 2025, propelled by rapidly aging populations, sports participation upticks, and widening access to tertiary care. Japanese surgeons’ preference for operative management of Achilles ruptures exemplifies procedure acceleration, bolstered by the October 2023 launch of Smith+Nephew’s REGENETEN implant. Chinese tier-one hospitals expand orthopedic floors, while Indian metropolitan centers invest in arthroscopy suites, widening the regional addressable base. These trends encourage global firms to locate R&D centers in APAC, cementing its role as the fastest-moving node of the tendon repair market.

Europe sustains solid growth through robust universal healthcare systems that reimburse minimally invasive techniques. CE marking pathways accommodate iterative product updates, expediting rollouts of advanced hydrogels. Germany and the United Kingdom spearhead clinical adoption thanks to high procedure volumes and extensive fellowship programs. Southern European nations add momentum as economic recovery funds modernize public hospitals. Middle East & Africa and South America trail but show steady improvement; targeted infrastructure spending and private insurance penetration nurture gradual uptake of advanced implants, opening frontier opportunities for agile entrants in the tendon repair market.

Competitive Landscape

The tendon repair market is moderately fragmented, with top players differentiated by biologic depth and surgical workflow integration. Stryker’s June 2024 takeover of Artelon added synthetic scaffold technology already deployed in 60,000 cases, amplifying its sports medicine franchise. Smith+Nephew leverages randomized evidence of a 68% re-tear reduction to position REGENETEN as the benchmark biologic augmentation patch, creating pricing power despite intensifying competition. Johnson & Johnson MedTech opted for a partnership, signing a November 2024 agreement with Responsive Arthroscopy to broaden its sports soft tissue catalog.

White-space still exists in personalized implants: FDA’s May 2024 clearance of the restor3d Total Talus Replacement validates 3-D printing’s orthopedic viability. Start-ups targeting microRNA delivery and piezo-electric stimulation attract venture funding by promising breakthroughs that incumbents have yet to monetize.

Competitive intensity centers on producing randomized clinical evidence—without it, market access is narrowing as payers demand outcome documentation. Players able to pair robust data with value-based contracts are positioned to capture disproportionate growth in the tendon repair market.

Tendon Repair Industry Leaders

Arthrex

Stryker

Johnson & Johnson

Smith & Nephew

Zimmer Biomet

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Johnson & Johnson MedTech entered a strategic agreement with Responsive Arthroscopy to enrich shoulder, foot, and ankle portfolios.

- August 2024: Anika Therapeutics gained FDA clearance for the Integrity Implant System, transitioning the firm beyond osteoarthritis pain products.

- June 2024: Stryker finalized the Artelon acquisition to reinforce soft tissue fixation capabilities.

Global Tendon Repair Market Report Scope

| Suture Anchors |

| Tendon Grafts (Autograft, Allograft) |

| Artificial Tendons & Ligaments |

| Bio-Scaffolds & Hydrogels |

| Fixation Devices & Others |

| Rotator Cuff |

| Achilles Tendon |

| Flexor/Extensor Hand Tendons |

| Patellar & Quadriceps Tendons |

| Others (e.g., Biceps, Peroneal) |

| Open Surgery |

| Arthroscopic / Minimally-Invasive |

| Percutaneous / Needle-Based |

| Bio-augmentative (PRP, Stem-cell, Gene) |

| Revision / Re-repair |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Orthopaedic Clinics |

| Sports Medicine & Rehabilitation Centers |

| Military & Trauma Facilities |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Suture Anchors | |

| Tendon Grafts (Autograft, Allograft) | ||

| Artificial Tendons & Ligaments | ||

| Bio-Scaffolds & Hydrogels | ||

| Fixation Devices & Others | ||

| By Application | Rotator Cuff | |

| Achilles Tendon | ||

| Flexor/Extensor Hand Tendons | ||

| Patellar & Quadriceps Tendons | ||

| Others (e.g., Biceps, Peroneal) | ||

| By Procedure Type | Open Surgery | |

| Arthroscopic / Minimally-Invasive | ||

| Percutaneous / Needle-Based | ||

| Bio-augmentative (PRP, Stem-cell, Gene) | ||

| Revision / Re-repair | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Orthopaedic Clinics | ||

| Sports Medicine & Rehabilitation Centers | ||

| Military & Trauma Facilities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the tendon repair market in 2025 and how fast is it growing?

The tendon repair market size reached USD 2.68 billion in 2025 and is projected to grow at an 8.1% CAGR to USD 3.96 billion by 2030.

Which product category currently leads global revenue?

Suture anchors dominate with 41.8% revenue share in 2024, driven by their essential role in mechanical fixation.

What is the fastest-growing application segment?

Achilles tendon procedures are growing at a 10.9% CAGR thanks to higher surgical intervention rates and minimally invasive techniques.

Which region is expanding quickest?

Asia Pacific is advancing at a 9.8% CAGR, fueled by aging demographics, rising sports participation, and broader access to advanced surgery.

What technology shows the greatest potential to cut re-tear rates?

Bio-scaffolds such as Smith+Nephews REGENETEN patch demonstrated a 68% reduction in full-thickness rotator cuff re-tears versus standard care.

How will reimbursement trends influence adoption of advanced implants?

Outpatient payment models that reward long-term outcomes are encouraging providers in North America and Europe to adopt premium biologic-augmented devices despite higher upfront costs.

Page last updated on: