Orthodontic Consumables Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

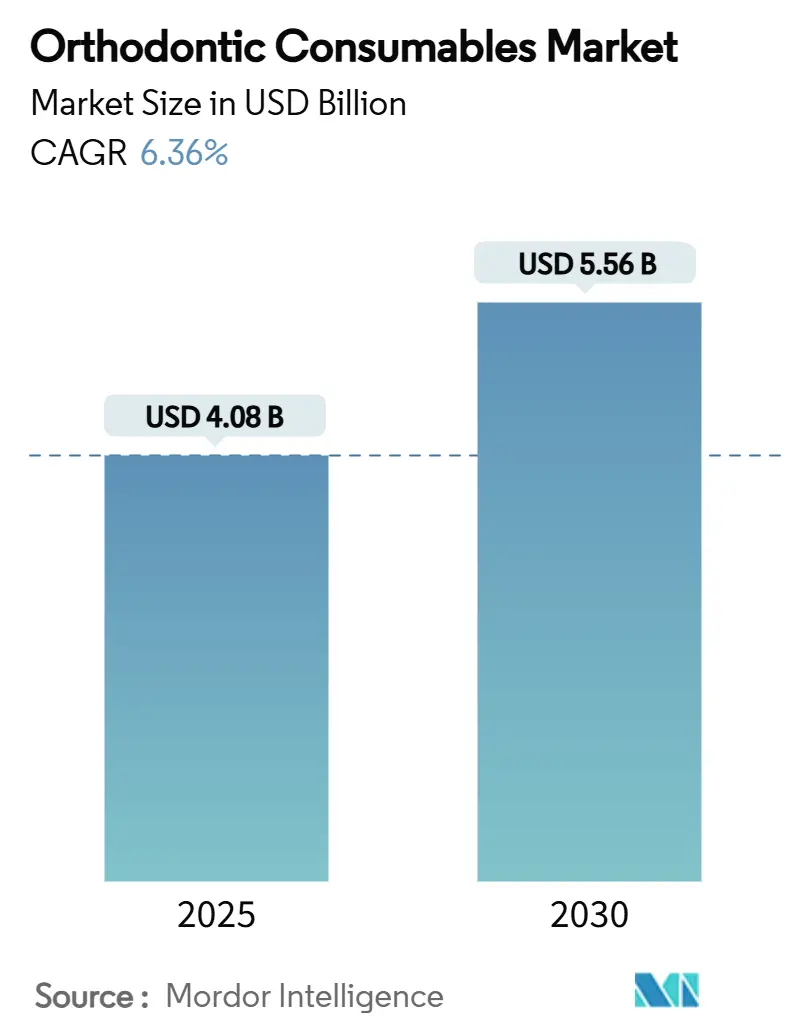

| Market Size (2025) | USD 4.08 Billion |

| Market Size (2030) | USD 5.56 Billion |

| Growth Rate (2025 - 2030) | 6.36% CAGR |

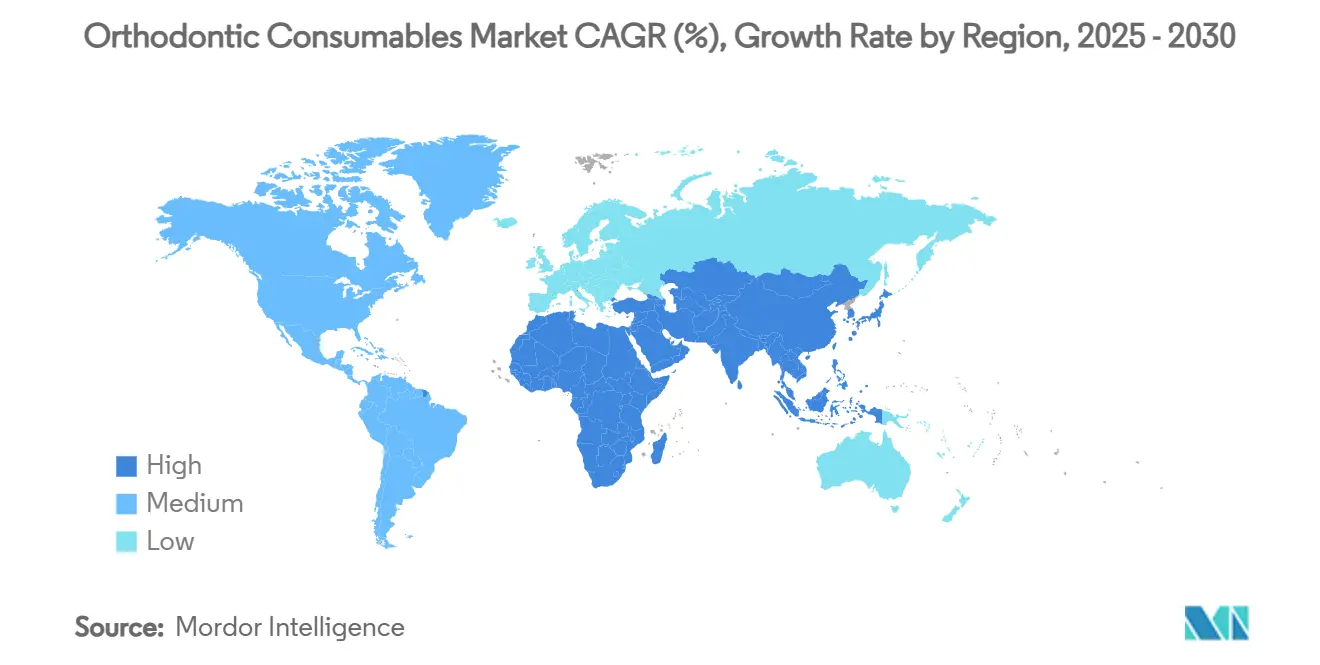

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Orthodontic Consumables Market Analysis by Mordor Intelligence

The orthodontic consumables market size reached USD 4.08 billion in 2025 and is projected to advance to USD 5.56 billion by 2030, reflecting a 6.36% CAGR during the forecast period. Rising aesthetic expectations, rapid uptake of 3-D printing, and the post-pandemic surge in adult procedures together reinforce steady volume growth. North America maintains clear leadership thanks to broad insurance coverage and high discretionary spending, while Asia-Pacific records the most rapid expansion as large middle-income populations embrace modern orthodontics. Technological differentiation now centres on AI-enhanced aligner platforms and self-ligating brackets that shorten chair time, prompting clinics to integrate digital workflows that cut material waste and raise precision. At the same time, raw-material price swings and shortages of trained orthodontists in low-income regions temper the overall growth outlook.

Key Report Takeaways

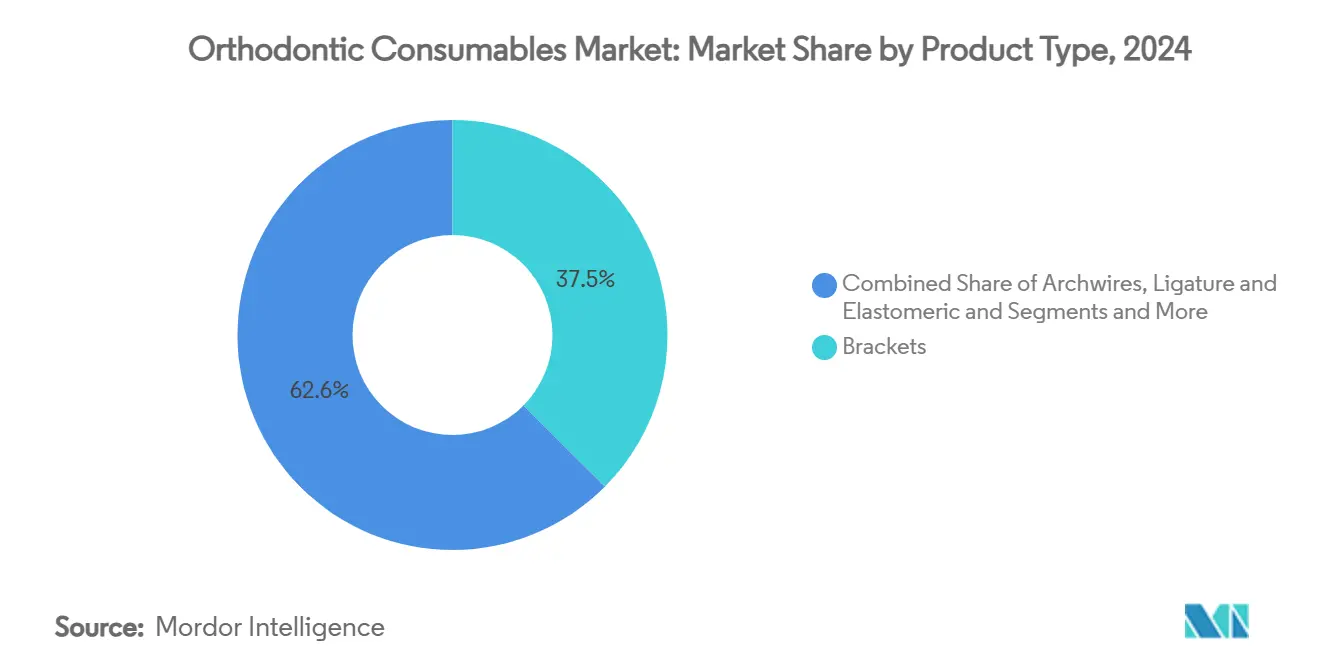

- By product type, brackets held 37.45% of the orthodontic consumables market share in 2024, and self-ligating variants are set to climb at an 8.38% CAGR to 2030.

- By material, stainless steel accounted for 44.68% share of the orthodontic consumables market size in 2024, whereas ceramic materials are forecast to expand at a 9.46% CAGR through 2030.

- By patient type, children and teenagers represented 61.22% of the orthodontic consumables market in 2024, while the adult segment is advancing at an 8.53% CAGR to 2030.

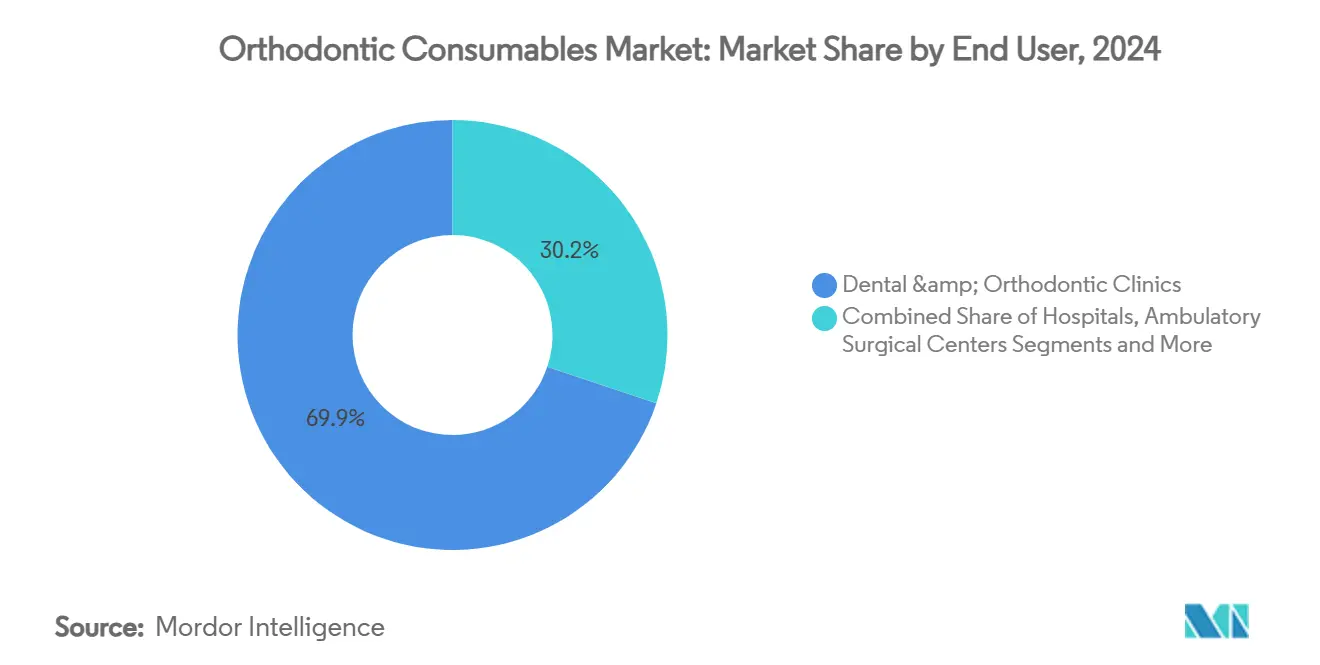

- By end user, dental and orthodontic clinics captured 69.85% revenue share in 2024, whereas online-enabled clinics record the highest projected CAGR at 9.58% up to 2030.

- By distribution channel, offline dealer networks dominated with 79.47% share in 2024; online platforms are growing at a 9.74% CAGR through 2030.

- By geography, North America led with 41.36% share of the orthodontic consumables market in 2024, but Asia-Pacific is advancing fastest at an 8.66% CAGR to 2030.

Global Orthodontic Consumables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of malocclusion & aesthetic focus | +1.2% | Global (strongest in North America & Europe) | Long term (≥ 4 years) |

| Surge in adult orthodontic procedures post-pandemic | +1.4% | Global, especially North America & Europe | Short term (≤ 2 years) |

| Growing adoption of self-ligating bracket systems | +0.8% | North America & Europe; expanding to APAC | Medium term (2-4 years) |

| Orthodontic consumables integration with digital workflow | +1.1% | North America & Europe leading; APAC following | Medium term (2-4 years) |

| National dental-insurance reforms expanding coverage | +0.9% | North America & Europe; selective emerging markets | Long term (≥ 4 years) |

| Near-term boom from social-media-driven orthodontic tourism | +0.7% | Global urban centres | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of malocclusion & aesthetic focus

Malocclusion now affects vast pediatric cohorts, including an estimated 260 million children in China alone, sustaining baseline demand for corrective therapies.[1]Xiaobing Li, “Expert Consensus on Pediatric Orthodontic Therapies of Malocclusions in Children,” Nature, nature.comHeightened aesthetic awareness increasingly motivates treatment among adults, with 72% of Gen Z actively comparing smiles online and willing to spend an average USD 2,960 on cosmetic procedures. Social platforms amplify these preferences and redirect consumer attention toward low-profile ceramic brackets and clear aligners. Practitioners report a steady shift from purely functional intervention thresholds to elective cosmetic acceptance, broadening the orthodontic consumables market. Public-health experts highlight earlier intervention as a pathway to lower lifetime malocclusion incidence, which underscores long-run consumables requirements. Together, escalating need and rising cosmetic expectations reshape product mix toward visually discreet and patient-specific solutions.

Growing adoption of self-ligating bracket systems

Passive self-ligating brackets reduce friction and shorten treatment duration, with clinical reviews noting upper incisor proclination of +5.2° and lower incisor proclination of +4.8° during alignment.[2]Corinna Seidel, “Inclination Changes in Incisors During Orthodontic Treatment with Passive Self-Ligating Brackets,” Journal of Clinical Medicine, mdpi.comThe Damon platform illustrates iterative design refinements, moving from mechanical hinges to lower-profile clips that improve patient comfort. CAD/CAM and in-office 3-D printing now allow customised slot dimensions that cut wire adjustments, lifting clinic profitability. Adoption momentum reflects chair-time savings and fewer elastomeric changes, even though scientific consensus on clear superiority over conventional brackets remains nuanced. Manufacturers continue to invest in passive clip durability and aesthetic coatings that resist staining, signalling an incremental shift toward friction-free biomechanics in the orthodontic consumables market.

Surge in adult orthodontic procedures post-pandemic

More than 70% of orthodontists report higher adult case volumes, attributing demand to greater screen exposure and video conferencing that highlight dental alignment. AI-assisted remote monitoring enables clinicians to reduce in-office visits while maintaining control over biomechanics, which aligns with adult scheduling constraints. Advanced adjuncts such as micro-osteoperforation triple tooth movement speed to 1.02 mm per month without raising root-resorption risk, making adult timelines more predictable. Adults gravitate toward clear aligners and ceramic brackets that disappear on video calls, driving premium consumables uptake. Extended treatment durations and higher-priced materials elevate revenue per patient, securing a durable uplift for the orthodontic consumables market.

Orthodontic consumables integration with digital workflow

End-to-end digital workflows convert stock parts into same-day customised appliances. Intraoral scanning accuracy reaches 98% for treatment planning, while AI tooth segmentation rivals that precision. 3-D printers fabricate patient specific aligner attachments that resist staining and deliver repeatable force application. CAD/CAM platforms generate tailored bracket bases that improve bond strength and simplify debonding. The shift repositions consumables as data-driven, premium assets rather than interchangeable commodities within the orthodontic consumables industry. As clinics adopt chairside printers, suppliers who bundle software, printers, and validated materials secure recurring revenue while reducing lead times for practitioners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement gaps in emerging markets | -0.7% | APAC, Latin America, Middle East & Africa | Long term (≥ 4 years) |

| Rising raw-material prices (Ni-Ti, ceramic) | -0.9% | Global, with strongest effect in North America & Europe | Medium term (2-4 years) |

| Clinical push-back against direct-to-consumer aligner models | -0.6% | North America & Europe; spill-over worldwide | Short term (≤ 2 years) |

| Skilled orthodontist shortage in low-income regions | -0.8% | APAC, Latin America, Middle East & Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reimbursement gaps in emerging markets

Insurance coverage remains patchy across many middle-income economies, forcing out-of-pocket payments that deter elective orthodontic care. A national survey in Palestine found 65% of children required intervention, yet access rates stay low due to cost barriers.[3]H. Amro, “A Comprehensive National Survey on Malocclusion Prevalence among Palestinian Children,” BMC Oral Health, biomedcentral.comSimilar preference studies in Poland and Chile show adult cohorts favour orthodontist-supervised care over do-it-yourself aligners, accepting higher prices for quality but still constrained by limited reimbursement. Government programmes often prioritise acute conditions, leaving orthodontics unfunded. The result is a concentration of the orthodontic consumables market in developed regions even as unmet need rises elsewhere. Manufacturers thus face volume ceilings in price-sensitive geographies until more comprehensive insurance schemes emerge.

Rising raw-material prices (Ni-Ti, ceramic)

Nickel-titanium alloys face supply disruption as Indonesian smelters pause production, exposing orthodontic wire costs to sudden spikes Titanium demand from aerospace crowds medical buyers, while ceramic component manufacturers operate near capacity, raising procurement risk. Stainless-steel markets swing on geopolitical tensions and tariffs that reach 54% on some imported dental items in the United States, squeezing unit margins for clinics and suppliers alike. Producers respond by diversifying sourcing and exploring surface-coated alternatives, yet alloy qualification and regulatory hurdles delay commercial rollout. Persistent volatility forces careful inventory management and may lift finished-goods prices, restraining downstream demand in the orthodontic consumables market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Efficiency gains propel self-ligating systems

Brackets accounted for 37.45% of the Orthodontic consumables market share in 2024, underscoring their role as the anchor component of fixed therapies. Archwires—especially super-elastic nickel–titanium designs—remain the essential complement, delivering continuous light force that shortens initial alignment phases. Ligatures and elastomerics still find favour where precise rotational control is required, although some practices now limit their use to complex torque corrections.

Self-ligating brackets are expanding at an 8.38% CAGR as clinics embrace lower chair-time and reduced friction benefits. Passive clip designs improve patient comfort and simplify hygiene while CAD/CAM custom slots reduce wire adjustments and emergency visits. Manufacturers funnel R&D toward slimmer metal profiles and stain-resistant ceramic housings, creating a pipeline of premium options that differentiate practices focused on adult aesthetics.

By Material: Aesthetic ceramics narrow the gap with stainless steel

Stainless steel represented 44.68% of the Orthodontic consumables market size in 2024, favoured for durability, malleability, and cost efficiency. Nickel–titanium alloys complement steel in situations demanding super-elastic recovery, whereas polymer blends power the clear-aligner boom by adding stain resistance and elastic memory.

Ceramic brackets are registering a 9.46% CAGR as adults prioritise low-profile appliances that match tooth shade. Recent formulations enhance fracture toughness and translucency, overcoming historic reliability concerns and allowing doctors to offer metal-free options in moderate-force cases. Surface treatments such as TiN–Cu nanocoatings further stiffen steel components, illustrating how established metals adopt high-tech upgrades to guard share amid ceramic momentum.

By Patient Type: Adult momentum complements pediatric core

Children and teenagers secured 61.22% of the Orthodontic consumables market share in 2024, reflecting well-established referral patterns and the clinical benefits of intervening during dental development. Preventive protocols, including interceptive extractions and palatal expansion, continue to support high bracket and archwire volumes in this cohort.

Adult treatments are advancing at an 8.53% CAGR, adding incremental revenue through longer regimens and premium clear or ceramic solutions. Workflow enablers such as AI-guided remote monitoring and micro-osteoperforation techniques further raise acceptability among busy professionals who demand predictable timelines. Together, the demographic mix enlarges the Orthodontic consumables market size by blending high-volume pediatric starts with higher-value adult courses.

By End User: Hybrid clinics integrate digital oversight

Dental and orthodontic clinics captured 69.85% of the Orthodontic consumables market size in 2024, supported by insurance alignment and established chair-side expertise. Hospitals continue to handle syndromic or surgical cases that require multidisciplinary coordination, sustaining demand for specialised archwires and anchorage units.

Online-enabled clinics are posting a 9.58% CAGR by embedding AI monitoring that cuts physical appointments without compromising supervision. Regulators’ insistence on in-office diagnostics following high-profile direct-to-consumer failures redirects case flow toward these hybrid models, bolstering consumable volume while reinforcing clinical standards. As a result, supply contracts increasingly bundle digital planning software with hardware to ensure practice loyalty and long-term throughput.

By Distribution Channel: E-commerce pressures but augments dealer reach

Offline dealer networks commanded 79.47% of the Orthodontic consumables market size in 2024, valued for technical support, training, and just-in-time inventory. In-person demonstrations remain critical when clinics evaluate advanced bonding systems or 3-D printers that require staff certification.

Online platforms are advancing at a 9.74% CAGR as buyers seek transparent pricing and rapid fulfilment for routine brackets, wires, and auxiliaries. Major distributors now extend storefronts into comprehensive digital marketplaces, blending next-day shipping with remote product tutorials to preserve service quality. The dual-channel approach ensures broad access while allowing practices to leverage e-commerce savings for commodity items and retain expert guidance for higher-risk purchases.

Geography Analysis

North America held a 41.36% share of the orthodontic consumables market in 2024, buoyed by strong insurance coverage and widespread adoption of premium therapies. Recent tariff hikes on imported alloys, however, add cost pressure and may encourage domestic manufacturing. The United States sees mature aligner penetration, while Canada leverages new public dental benefits to widen access.

Asia-Pacific records the fastest 8.66% CAGR as China and India scale up middle-class expenditure on elective healthcare. China alone hosts 260 million children with malocclusion and shows robust demand for advanced aligners. Regional manufacturers leverage local 3-D printing to supply tailor-made parts at lower cost, complementing international brands that open new production hubs.

Europe demonstrates steady expansion supported by rigid quality regulations and evidence-based practice culture. Germany’s orthognathic surgery volume rises 2.5% annually, confirming heightened acceptance of comprehensive correction. Wider European sustainability priorities spur interest in recyclable packaging and eco-friendly bracket materials.

Competitive Landscape

Competition is moderate but trending toward consolidation as leading suppliers integrate AI planning, 3-D printing, and rapid logistics. Align Technology’s acquisition of Cubicure advances mass-customisation capability, while Solventum debuts printed aligner attachments that simplify chair-side application. Ormco’s Spark platform introduces BiteSync Class II correctors and resin-free bonding that saves enamel. Venture-backed newcomers such as KLOwen Orthodontics secure fresh funding to scale custom self-ligating metal solutions, reflecting investor confidence in niche precision hardware.The global field also witnesses retreat of direct-to-consumer aligner models, following SmileDirectClub’s bankruptcy and Dentsply Sirona’s suspension of Byte sales, which underscores regulator insistence on chair-side diagnostics. Established suppliers now position remote monitoring as an adjunct to in-office care, rather than a replacement, to satisfy quality-of-care mandates and preserve professional trust. Midsize companies respond by forging distribution alliances with full-service dealers that offer bundled software and training packages, expanding reach without replicating large-scale infrastructure.

Price volatility in nickel, titanium, and ceramics prompts strategic sourcing arrangements and secondary-supplier qualification programmes designed to stabilise costs. Large players hedge exposure through vertical integration or long-term supply contracts, whereas smaller firms explore alternative alloys such as copper-nickel-titanium to balance performance with availability. Intellectual-property portfolios expand beyond hardware into AI algorithms for treatment planning, creating new competitive moats that reward data ownership.

Top suppliers leaving ample space for regional specialists that tailor products to local aesthetic norms and price points. Those firms often exploit fast-growing online channels and lighter regulatory frameworks to introduce incremental innovations. Overall, competition pivots from pure product superiority toward platform depth, service integration, and supply-chain resilience across the orthodontic consumables market.

Orthodontic Consumables Industry Leaders

Envista Holdings

Solventum

Align Technology

Dentsply Sirona

Straumann Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Ormco Corporation launched Spark Retainers and BiteSync Class II Corrector in the United States.

- April 2025: Ormco Corporation introduced EtchFree Bonding, a resin-free adhesive system.

- April 2025: Angel Aligner opened its first US manufacturing facility and unveiled the KiD aligner system for paediatric care.

Global Orthodontic Consumables Market Report Scope

| Brackets |

| Archwires |

| Ligatures & Elastomerics |

| Adhesives & Bonding Agents |

| Bands & Buccal Tubes |

| Others (Separators, Springs, etc.) |

| Stainless-steel |

| Nickel-Titanium (Ni-Ti) |

| Ceramic |

| Polymeric/Composites |

| Children & Teenagers |

| Adults |

| Dental & Orthodontic Clinics |

| Hospitals |

| Ambulatory Surgical Centers |

| Academic & Research Institutes |

| Offline Retail / Dealer Network |

| Online Platforms |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Brackets | |

| Archwires | ||

| Ligatures & Elastomerics | ||

| Adhesives & Bonding Agents | ||

| Bands & Buccal Tubes | ||

| Others (Separators, Springs, etc.) | ||

| By Material | Stainless-steel | |

| Nickel-Titanium (Ni-Ti) | ||

| Ceramic | ||

| Polymeric/Composites | ||

| By Patient Type | Children & Teenagers | |

| Adults | ||

| By End User | Dental & Orthodontic Clinics | |

| Hospitals | ||

| Ambulatory Surgical Centers | ||

| Academic & Research Institutes | ||

| By Distribution Channel | Offline Retail / Dealer Network | |

| Online Platforms | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current size of the orthodontic consumables market?

The orthodontic consumables market size stood at USD 4.08 billion in 2025 and is forecast to reach USD 5.56 billion by 2030.

2. Which product category leads global sales?

Brackets remain the largest category, accounting for 37.45% of revenue in 2024.

3. Why is Asia-Pacific the fastest-growing region?

Rapid urbanisation, expanding middle-income populations, and heightened aesthetic awareness drive an 8.66% CAGR in Asia-Pacific demand.

4. How are digital workflows changing consumable demand?

3-D printing and AI-driven planning convert standard parts into customised appliances produced on-site the same day, elevating demand for premium, patient-specific materials.

5. What risks could slow market growth?

Volatile raw-material prices, reimbursement gaps in emerging economies, and shortages of trained orthodontists in low-income regions may restrain wider adoption.

Page last updated on: