Dentures Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

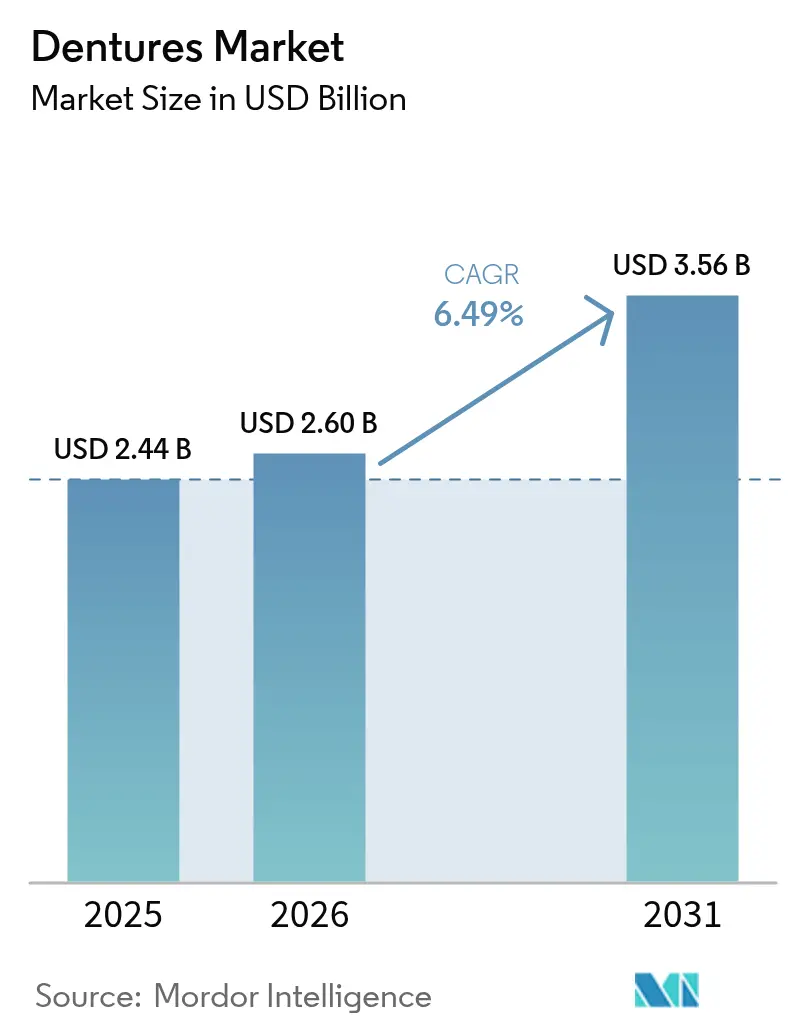

| Market Size (2026) | USD 2.6 Billion |

| Market Size (2031) | USD 3.56 Billion |

| Growth Rate (2026 - 2031) | 6.49% CAGR |

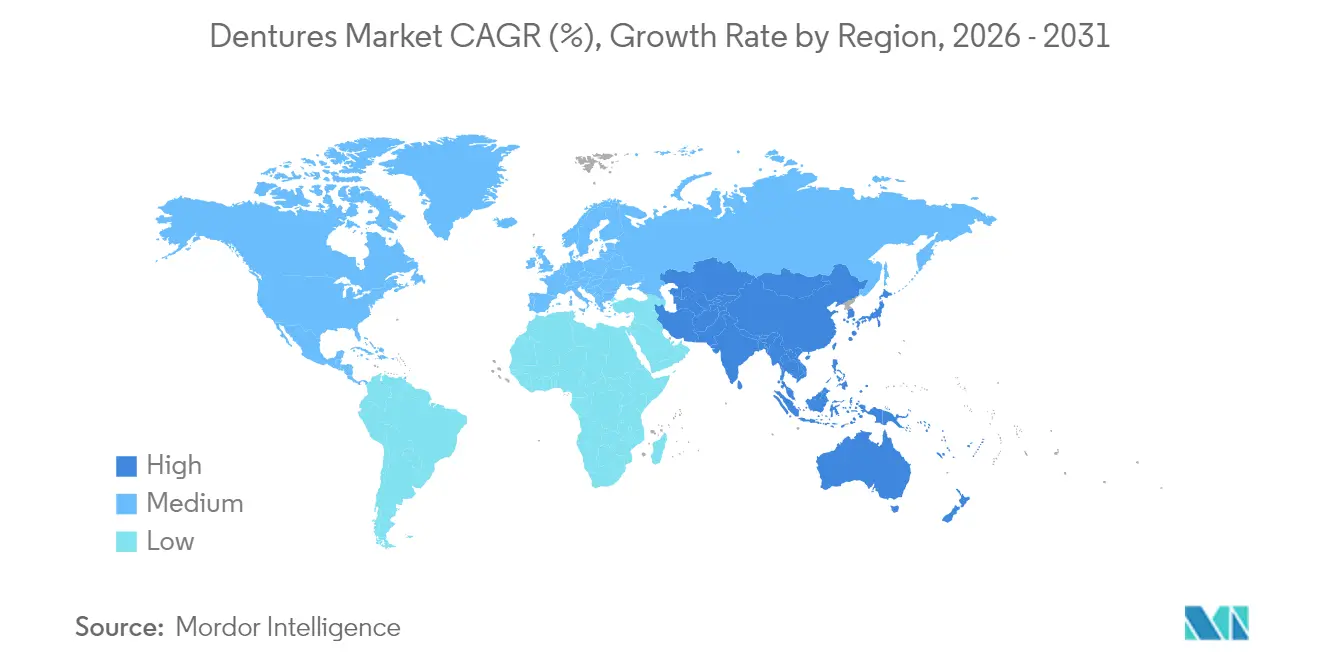

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dentures Market Analysis by Mordor Intelligence

The global dentures market size was valued at USD 2.44 billion in 2025 and estimated to grow from USD 2.6 billion in 2026 to reach USD 3.56 billion by 2031, at a CAGR of 6.49% during the forecast period (2026-2031). Growth rests on demographic momentum as the world’s senior population rises and tooth-loss prevalence remains high—more than 280 million older adults experience edentulism, directly supporting denture demand. Insurance expansion in mature economies, broadening healthcare access in emerging regions, and rapid adoption of digital manufacturing workflows reinforce the upward trajectory. 3D printing, CAD/CAM milling, and next-generation photopolymers shorten production cycles, enhance fit, and lower unit costs, attracting providers and patients alike. Simultaneously, greater public recognition of the link between oral and systemic health encourages seniors to seek timely prosthodontic therapy[1]Centers for Disease Control and Prevention, “Oral Health Surveillance Report 2024,” cdc.gov. Although alternative tooth-replacement solutions such as implants are gaining ground, advances in hybrid, implant-supported removable prostheses have kept conventional denture therapy relevant.

Key Report Takeaways

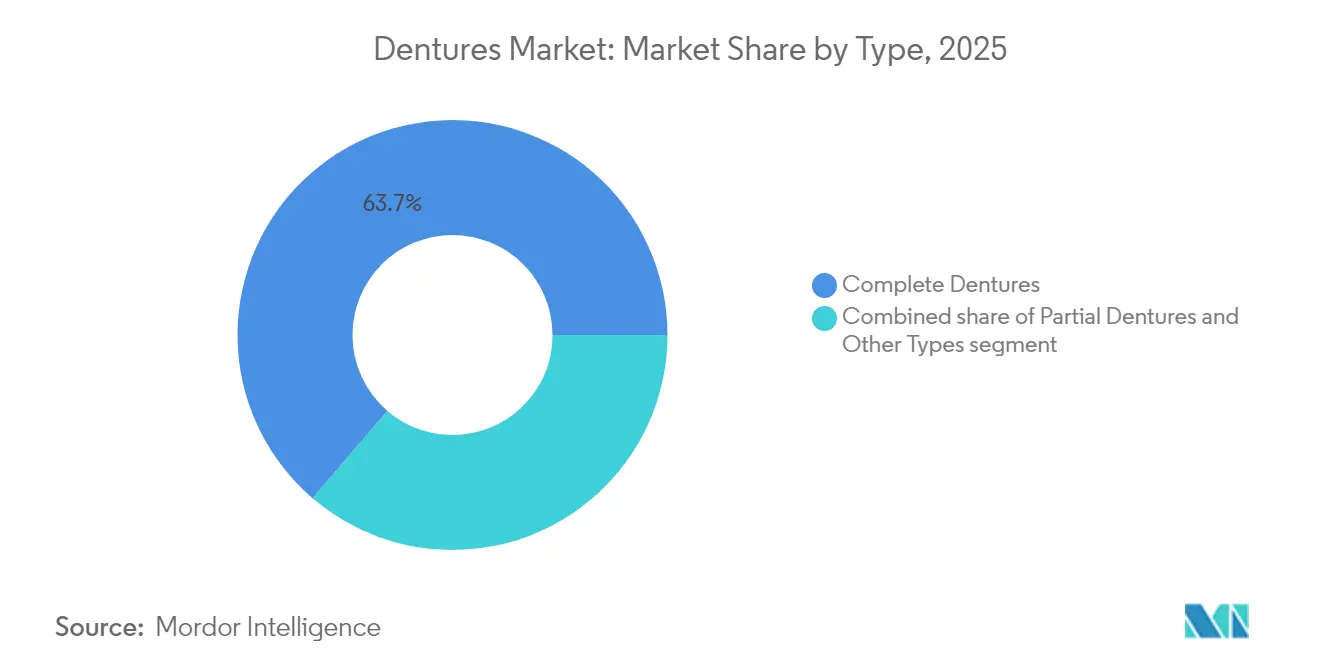

- By type, complete dentures led with 63.72% revenue share in 2025; Other Types are projected to grow at an 8.25% CAGR through 2031.

- By usage, the removable segment held 70.58% of the dentures market share in 2025, while fixed dentures are primed for a 7.72% CAGR to 2031.

- By material, acrylic resin captured 67.89% of the dentures market size in 2025; 3D-printed photopolymer materials are set to advance at an 8.29% CAGR over the forecast period.

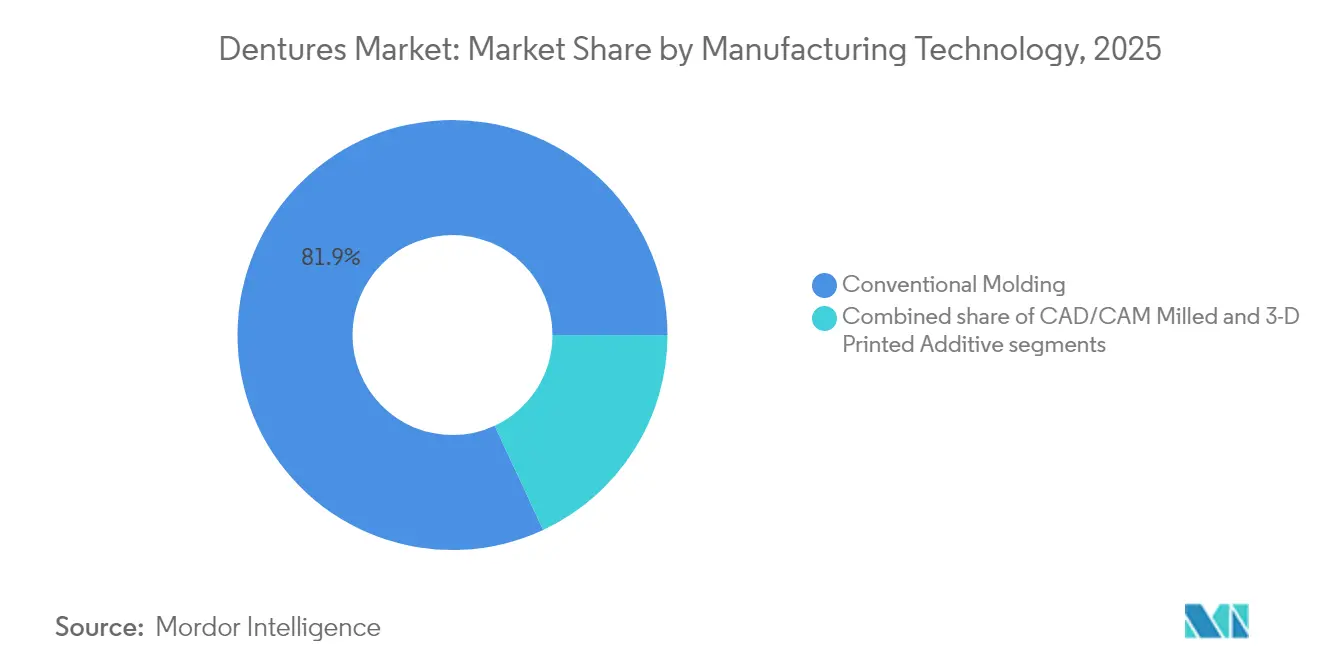

- By manufacturing technology, conventional molding controlled 81.93% share of the dentures market size in 2025, whereas 3D-printed additive manufacturing is projected to expand at an 8.88% CAGR through 2031.

- By end user, dental clinics and hospitals commanded 59.02% share of the dentures market size in 2025, while dental laboratories are expected to register a 9.33% CAGR between 2026 and 2031.

- By geography, North America captured 42.11% of the global dentures market share in 2025; Asia-Pacific is anticipated to post a 7.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dentures Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Prevalence Of Oral Health Disorders | +1.2% | Global, higher in developing regions | Long term (≥ 4 years) |

| Rapid Growth Of Aging Population | +1.8% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Technological Advancements In Digital Denture Manufacturing | +1.5% | North America & EU leading; APAC accelerating | Medium term (2-4 years) |

| Rising Demand For Aesthetic Dental Solutions | +0.9% | Global, premium markets leading | Medium term (2-4 years) |

| Expansion Of Dental Insurance Coverage | +0.8% | North America primary, EU secondary | Short term (≤ 2 years) |

| Growing Dental Tourism In Emerging Economies | +0.6% | Asia-Pacific core; spill-over to MEA & Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Oral Health Disorders

Chronic periodontal disease and untreated caries continue to push millions toward tooth loss each year, sustaining the dentures market as edentulism remains widespread despite preventive care investments. A Global Burden of Disease assessment projected persistent high edentulism prevalence through 2050, underscoring denture therapy’s long-term relevance. Geriatric oral-health programs now use multidisciplinary assessment models that flag complex prosthodontic needs earlier, channeling more candidates into denture workflow. Evidence also links poor oral status with chronic conditions such as diabetes and cardiovascular disease, adding urgency for timely prosthetic rehabilitation. Public perception is shifting 91% of adults rate dental visits as vital as annual physical exams, spotlighting oral treatment as preventive medicine. Ironically, broader preventive screenings reveal unmet tooth-replacement requirements, redirecting patients toward denture solutions.

Rapid Growth of Aging Population

Adults aged 65 and older represent the core consumer base for dentures, and their numbers are expanding faster than any other demographic group. Studies show that older adults who receive partial dentures experience slower cognitive decline, adding medical impetus to treatment. The current generation of seniors retains natural teeth longer, but once loss occurs, expectations for quality of life and dietary freedom drive demand for premium, digitally fabricated prostheses. Policymakers are likewise recognizing denture therapy as essential health maintenance rather than a cosmetic service, paving the way for improved reimbursement frameworks. As life expectancy rises, so does the cumulative period during which seniors require functional oral rehabilitation, making the dentures market a structural beneficiary of demographic aging.

Technological Advancements in Digital Denture Manufacturing

Digital workflows employing intraoral scanning, CAD/CAM design, and 3D printing have compressed denture delivery from weeks to days while elevating clinical precision. Comparative trials show digital dentures attaining average intaglio surface trueness of 176.9 µm versus 342 µm for conventional prostheses, drastically reducing post-delivery adjustments. Clinics report chairside time savings of more than 60 minutes per case and laboratory-cost reductions exceeding EUR 80, broadening affordability. Material-jetting systems now produce polychromatic bases and teeth in a single pass, enhancing esthetics and workflow simplicity. These efficiencies enlarge the addressable pool of providers capable of offering dentures, directly fueling dentures market expansion.

Rising Demand for Aesthetic Dental Solutions

Patient preference has shifted from mere functional replacement to natural-looking, confidence-enhancing prostheses. Oral-health quality-of-life studies document significant psychological gains when color, translucency, and tooth morphology mimic natural dentition. Interdisciplinary treatment planning now blends prosthodontics, periodontics, and esthetic dentistry, ensuring outcome harmony. High-strength ceramics and bioactive composites allow thinner, more lifelike tooth forms that maintain durability, while digital design tools enable chairside visualization for real-time aesthetic tweaks. Sophisticated coloration workflows once reserved for single crowns are now routine for full arches, elevating value perception and supporting premium pricing across the dentures market.

Expansion of Dental Insurance Coverage

Policies in the United States and parts of Europe are gradually broadening denture eligibility. The Centers for Medicare & Medicaid Services clarified in 2024 that dental services integral to systemic treatments—such as dialysis—will be reimbursable beginning 2025, directly lowering out-of-pocket burden for many seniors[2]Medicare Rights Center, “Expansion of Dental Coverage Under Medicare 2024,” medicarerights.org. Nine U.S. states have already classified full denture therapy as a covered adult Medicaid benefit, up from three in 2020. Commercial insurers have responded by enhancing prosthodontic benefits to remain competitive, collectively improving treatment reach and accelerating dentures market adoption.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Treatment And Product Costs | -1.4% | Global, more pronounced in developing regions | Short term (≤ 2 years) |

| Availability Of Alternative Tooth Replacement Options | -1.1% | Developed markets primarily | Medium term (2-4 years) |

| Limited Skilled Workforce For Advanced Denture Technologies | -0.7% | Emerging markets and rural areas worldwide | Medium term (2-4 years) |

| Stringent Regulatory Approval Processes | -0.5% | North America, Europe, selected APAC markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Treatment and Product Costs

Despite manufacturing advances, total treatment costs—including clinical time, imaging, and follow-up—remain a barrier, especially where insurance penetration is low. Traditional Medicare still excludes routine prosthodontics, leaving many seniors to self-fund denture therapy. Although Medicaid expansion has improved access in select U.S. states, fixed-income retirees in others continue to delay or forgo treatment. Smaller practices also struggle to justify capital outlays for digital equipment, reinforcing a cost gap between high-tech laboratories and conventional facilities. Even in Europe’s socialized systems, budget constraints create waiting lists that push patients toward cheaper, out-of-pocket international alternatives.

Availability of Alternative Tooth Replacement Options

The steady rise of implant therapy presents a substitute threat by offering superior retention and masticatory performance for eligible patients. FDA performance-based guidelines issued in 2024 have lowered clearance hurdles for innovative implant designs, accelerating product availability[3]Food and Drug Administration, “Safety and Performance Based Pathway: Dental Implants Guidance 2024,” fda.gov. Yet implant candidacy depends on systemic health, bone density, and patient willingness to undergo surgery, leaving a sizable cohort for whom conventional dentures remain the only feasible solution. Hybrid overdentures that blend implant support with removable functionality blur competitive boundaries, but they still rely on the underlying prosthetic base—sustaining long-term relevance of the dentures market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Complete Dentures Dominate Despite Hybrid Innovation

Complete dentures represented 63.72% of global revenue in 2025, anchored by a large edentulous population that demands full-arch rehabilitation. This category improves oral-health quality of life by more than 9% within a year of wear, according to systematic clinical reviews. Digital workflows now permit precise duplication of established occlusal schemes, boosting acceptance among practitioners and patients. Partial dentures remain important for mixed-dentition cases, serving as a conservative, tooth-preserving option. The Other Types segment—primarily implant-retained overdentures and fixed hybrid prostheses—advances at an 8.25% CAGR as implant surgery becomes more affordable. Superior stability and reduced gag reflex are key selling points, particularly for younger edentulous patients who demand higher functionality. Overall, shifting patient expectations and cross-specialty collaboration will continue to realign type preference, yet complete dentures are expected to retain a commanding role in the dentures market through 2031.

Growing acceptance of hybrid solutions does not cannibalize traditional sales fully; instead, it extends the dentures market size by drawing in candidates previously skeptical of removable appliances. Many clinicians now offer a two-phase treatment pathway, starting with complete dentures for tissue conditioning and progressing to implant-supported configurations once bone remodeling stabilizes. This staged approach balances cost, surgical risk, and adaptation, ensuring dentures market continuity across all income brackets.

By Usage: Removable Solutions Lead Traditional Market

Removable appliances captured 70.58% share in 2025, favored for their non-invasive nature and immediate reversibility. Digital impression systems reduce gag reflex incidence and improve accuracy, alleviating key patient objections. Lower unit costs make removable dentures the mainstay in insurance reimbursement schedules, keeping them relevant in both public and private healthcare environments. Fixed options, largely dependent on implant fixtures, are growing at a 7.72% CAGR as new mini-implant protocols expand the eligible patient base. Chewing-efficiency studies consistently show fixed restorations outperforming removable variants, but the gap is narrowing as precision attachments and soft-liner materials improve removable stability.

Hybrid overdentures illustrate convergence: they clip onto bar or locator attachments while retaining daily removability for hygiene. This model delivers much of the stability of a fixed system while preserving the affordability of removable therapy. As clinicians integrate chairside CAD/CAM systems, patients can trial virtual setups, boosting confidence and uptake of both usage types across the dentures market.

By Material: Acrylic Resin Dominance Faces Digital Disruption

Acrylic resin maintained 67.89% market share in 2025 due to decades of proven performance, straightforward processing, and acceptable esthetics at low cost. Its shock-absorbing traits reduce mucosal trauma, another contributor to ongoing preference. However, advances in photopolymer chemistry are eroding this lead. 3D-printed photopolymer bases are advancing at an 8.29% CAGR and already eclipse conventional polymethyl methacrylate (PMMA) in flexural-strength benchmarks. Water-absorption tests show markedly lower uptake, translating to odor and stain resistance over long service periods. Porcelain and metal-ceramic systems retain a niche role where wear resistance is paramount, such as for bruxism cases.

Regulatory clarity for biocompatible print resins has accelerated certification, fueling provider confidence. Post-cure optimization—elevating temperature to enhance polymer cross-link density—further improves mechanical integrity, making printed materials viable even for high-load mandibular applications. Consequently, the dentures market now offers a diversified material palette, enabling clinicians to tailor choices to patient allergies, esthetic preferences, and budget.

By Manufacturing Technology: Digital Revolution Accelerates

Conventional molding processes still account for 81.93% of production because they rely on ubiquitous equipment and skills. Yet the efficiencies unlocked by 3D printing and CNC milling are convincing laboratories to upgrade. CAD/CAM-milled dentures exhibit marginal gaps comparable to traditional cast frameworks, validating their clinical legitimacy. The 3D-printed segment, expanding at 8.88% CAGR, takes advantage of falling printer costs and resins engineered for rapid post-cure. These systems also streamline multi-unit production, allowing laboratories to batch-produce up to eight full arches in a single build, lowering cost per unit and shrinking delivery timelines.

Hybrid workflows that mill denture bases and print teeth or vice versa are gaining traction, marrying the surface quality of milling with the customization benefits of printing. Such flexibility widens the dentures market size by fitting diverse laboratory investment capacities and clinical objectives.

By End User: Dental Laboratories Drive Innovation Adoption

Dental clinics and hospitals held 59.02% share in 2025, serving as the patient’s primary care touchpoint. Nevertheless, the fastest expansion is in dental laboratories, charting a 9.33% CAGR as they become digital-manufacturing hubs for regional networks. Consolidation has seen multi-site laboratories leverage scale to acquire high-end milling centers and industrial-grade resin printers, differentiating on turnaround time and precision. Academic institutions, while a smaller revenue contributor, provide indispensable research validation and practitioner training, ensuring evidence-based diffusion of new workflows. Their role in clinical trials confirms safety and efficacy for regulatory submissions, indirectly buoying the dentures market.

Geography Analysis

North America dominated the dentures market with 42.11% revenue share in 2025, propelled by insurance reforms and broad adoption of chairside digital dentistry. Medicare rule changes taking effect in 2025 will reimburse medically necessary prosthodontic services linked to systemic treatments, lowering financial barriers. Medicaid’s adult dental benefit extensions in nine states have likewise widened access. Denture manufacturers benefit from a thick network of dental-support organizations that quickly roll out technology upgrades system-wide, reinforcing regional leadership.

Asia-Pacific is the fastest-growing geography with a 7.74% CAGR to 2031. China’s rapidly aging demographic and rising middle-class income underpin strong volume growth, while local manufacturers accelerate adoption of intraoral scanners and UV-cured resins to serve domestic clinics. Straumann Group recorded 82% year-on-year regional growth in early 2024, citing surging demand for scanners and implant-supported overdentures. Southeast Asian nations promote bundled tourism-plus-denture packages, leveraging lower labor costs to attract Western patients. Such cross-border traffic stimulates investment in advanced laboratory equipment, feeding back into regional dentures market expansion.

Europe sustains steady, technology-driven growth underpinned by mandatory health insurance and high practitioner skill levels. German and Spanish clinics led double-digit organic growth for Straumann’s EMEA segment in 2024. The European Union’s well-defined Medical Device Regulation fosters transparent approval pathways for new denture materials, encouraging faster market entry. Meanwhile, economic constraints in Southern and Eastern Europe extend case acceptance timelines, slowing overall regional CAGR relative to Asia-Pacific but preserving high digital-dentistry penetration.

The Middle East & Africa and South America collectively capture a smaller share today but exhibit expanding opportunities through urbanization and rising disposable income. Dental-school partnerships with Western universities are improving clinician capacity, laying groundwork for long-term dentures market development. Government-backed health-insurance pilots in the Gulf Cooperation Council are beginning to include fixed and removable prosthodontics, hinting at new reimbursable demand streams.

Competitive Landscape

The dentures market features moderate consolidation: global manufacturers and leading dental-service organizations dominate premium segments, while thousands of regional laboratories supply value-oriented products. DENTSPLY SIRONA, one of the largest players, reported USD 3.965 billion in 2024 sales—down 4.3% year on year—due primarily to Orthodontic and Implant segment softness and macro headwinds. Management has launched operational-efficiency programs aimed at restoring margins via streamlined supply chains and portfolio rationalization.

Straumann Group, in contrast, posted CHF 2.41 billion in 2023 revenue and remains on a growth trajectory supported by acquisitions in software, surface-treatment, and implant-cleaning technologies. The company’s strategy emphasizes full-workflow ownership—from intraoral scanners to final prostheses. Envista Holdings is repositioning around digital platforms, absorbing a one-time goodwill impairment that produced a temporary net loss but freeing resources for R&D in photopolymer resins.

The competitive frontier is increasingly defined by control over data and workflows rather than physical product only. Large players integrate cloud-based design portals and AI-driven occlusal analysis to lock-in clinical users, creating stickiness around material and hardware ecosystems. Start-ups target direct-to-consumer segments with at-home impression kits and centralized fabrication, but high regulatory scrutiny and clinical-fit liabilities limit penetration to non-complex cases. FDA guidance on patient-preference information supports iterative, user-centric product development, potentially enabling mid-sized firms to leapfrog established brands with highly customized offerings.

Dentures Industry Leaders

DENTSPLY SIRONA Inc.

Zimmer Biomet Holdings Inc.

Ivoclar Vivadent AG

Modern Dental Group Ltd.

COLTENE Holding AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: DENTSPLY SIRONA reported a 4.3% year-over-year decline in 2024 net sales and unveiled a turnaround plan focusing on EBITDA margin expansion through operational optimization.

- January 2025: The FDA updated CFR Part 872 to refine regulatory language around denture-related Class II devices, clarifying testing and labeling expectations for hydrophilic coatings.

- December 2024: CMS expanded Medicare dental coverage for medically necessary procedures, including prosthodontics tied to systemic treatments for dialysis patients, effective 2025.

- November 2024: DENTSPLY SIRONA announced a USD 494 million GAAP net loss for 3Q 2024 due to goodwill impairment and revised FY24 guidance to an organic sales decline of 2.5-3.5%.

- October 2024: The FDA issued final performance-criteria guidance for endosseous dental implants and abutments, facilitating market entry for implant-supported denture solutions.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study, according to Mordor Intelligence, defines the global dentures market as the annual value of complete or partial removable or fixed prostheses fabricated to replace missing natural teeth and surrounding oral tissues, irrespective of material or manufacturing technology. The evaluation covers factory-gate revenues flowing from dental labs and manufacturers to clinics, hospitals, and distributors across more than thirty countries.

Scope excludes chairside relines, over-the-counter whitening trays, and standalone implant fixtures that are not sold bundled with a denture base.

Segmentation Overview

- By Type

- Complete Dentures

- Partial Dentures

- Other Types

- By Usage

- Fixed

- Removable

- By Material

- Acrylic Resin

- Porcelain

- Metal-Ceramic

- Flexible (Nylon-Based)

- 3-D Printed Photopolymer

- By Manufacturing Technology

- Conventional Molding

- CAD/CAM Milled

- 3-D Printed Additive

- By End User

- Dental Clinics & Hospitals

- Dental Laboratories

- Academic & Research Institutes

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with prosthodontists, lab owners, and dental material experts across North America, Europe, and Asia-Pacific refined adoption curves for CAD/CAM milling, realistic replacement rates, and average selling prices. Short online surveys of senior patients complemented expert views on affordability thresholds that secondary sources rarely capture.

Desk Research

We first mapped the demand pool using publicly available anchors such as WHO oral-health burden tables, United Nations demographic outlooks, American College of Prosthodontists edentulism surveys, and customs shipment codes for acrylic dental plates. Trade association portals, including FDI World Dental Federation and European Dental Lab Confederation, supplied procedure trends and reimbursement notes, while company 10-Ks and investor decks clarified price corridors. Paid databases like D&B Hoovers and Dow Jones Factiva helped us vet company revenue splits and capture smaller regional producers. This list is illustrative; many other credible outlets were reviewed for corroboration.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-cohort build paired with sampled ASP × volume roll-ups (bottom-up once) formed the core model. Key variables like edentulous population growth, denture replacement cycle, clinic density, acrylic resin import prices, and CAD/CAM penetration drive yearly value estimates. Multivariate regression projected each driver through 2030, with scenario tweaks validated in follow-up calls. Data gaps in low-visibility countries were bridged by regional analogs after variance checks.

Data Validation & Update Cycle

Outputs pass a two-level analyst review, then software flags anomalies versus historical ratios before sign-off. Mordor refreshes models every twelve months and issues interim revisions if raw-material shocks or regulatory shifts move underlying costs materially.

Why Mordor's Dentures Baseline Stands Up to Scrutiny

Published figures often diverge because firms pick different base years, price assumptions, and product mixes. We remind clients early that such gaps are normal in a fragmented lab landscape.

Major gap drivers include: some studies fold digital implant bars into market totals, a few apply pre-COVID replacement rates without adjustment, and several convert regional revenues at static 2022 averages rather than rolling currency weights that Mordor updates quarterly.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.44 B (2025) | Mordor Intelligence | - |

| USD 2.43 B (2025) | Global Consultancy A | excludes Asia hospital labs, assumes flat ASP growth |

| USD 3.02 B (2025) | Industry Association B | bundles implant bars and chairside relines into value |

| USD 3.38 B (2025) | Trade Journal C | uses single exchange rate and projects uniform 6.5 % CAGR globally |

Taken together, the comparison shows that Mordor's disciplined scope choices, driver-linked modeling, and annual refresh cadence yield a balanced, transparent baseline that decision-makers can retrace and replicate with limited effort.

Key Questions Answered in the Report

What is the current size of the global dentures market?

The market is valued at USD 2.6 billion in 2026 and is projected to reach USD 3.56 billion by 2031.

What compound annual growth rate (CAGR) is forecast for the dentures market through 2031?

Industry revenue is expected to expand at a 6.49% CAGR over the 2026-2031 period.

Which regions are leading and growing fastest in the dentures market?

North America holds the largest share at 42.11% in 2025, while Asia-Pacific is the fastest-growing region with a 7.74% CAGR to 2031.

How are digital manufacturing technologies influencing market growth?

Adoption of CAD/CAM milling and 3D printing shortens production cycles, improves fit, and cuts laboratory costs, accelerating product uptake across clinics and laboratories.

What key barriers still limit denture adoption?

High out-of-pocket costs in markets with limited insurance coverage and competition from implant alternatives continue to restrict some patient segments.

How will evolving insurance policies affect future demand for dentures?

Expanded Medicaid adult dental benefits and new Medicare coverage for medically necessary prosthodontics are expected to lower financial barriers and increase treatment volumes from 2025 onward.

Page last updated on: