Global Dental Consumables Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

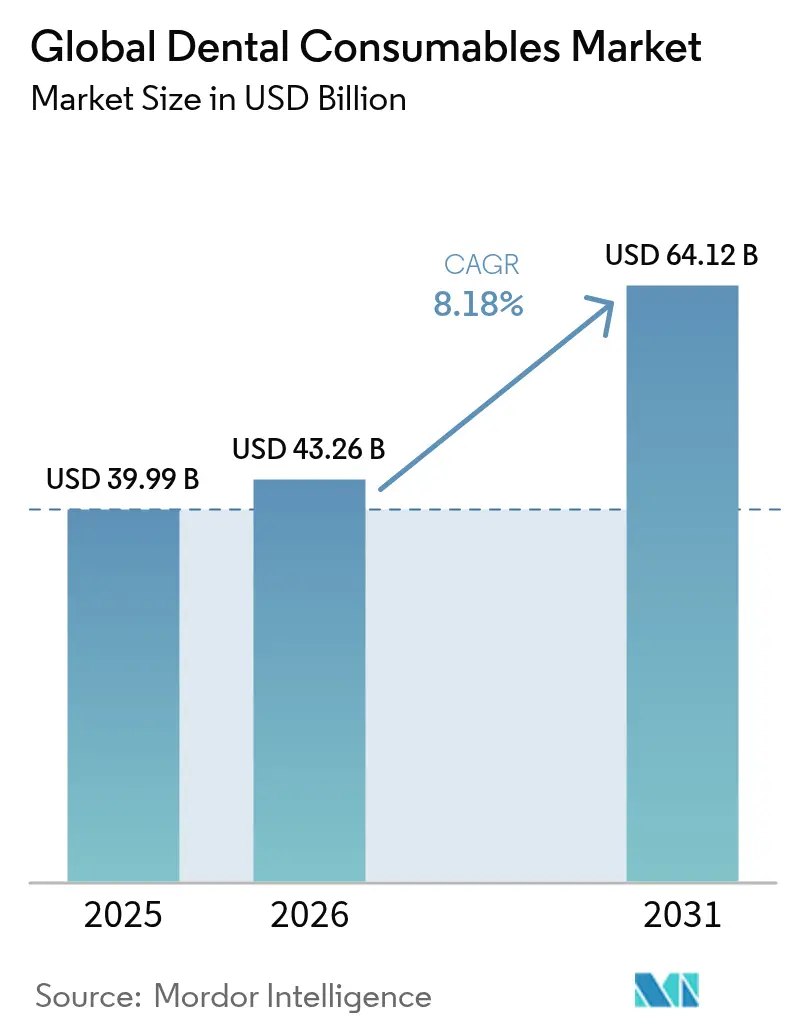

| Market Size (2026) | USD 43.26 Billion |

| Market Size (2031) | USD 64.12 Billion |

| Growth Rate (2026 - 2031) | 8.18% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Dental Consumables Market Analysis by Mordor Intelligence

The dental consumables market size was valued at USD 39.99 billion in 2025 and estimated to grow from USD 43.26 billion in 2026 to reach USD 64.12 billion by 2031, at a CAGR of 8.18% during the forecast period (2026-2031). Steady gains stem from digital chairside workflows, bioactive implant materials, and bulk-procurement models that shift volumes toward premium product lines. DSOs are scaling rapidly, influencing procurement standards, while North America remains the revenue leader even as Asia-Pacific posts the fastest regional advance. Demand for same-day restorations, preventive sealants, and regenerative materials collectively elevate per-patient spending and favors suppliers with integrated digital ecosystems.

Key Report Takeaways

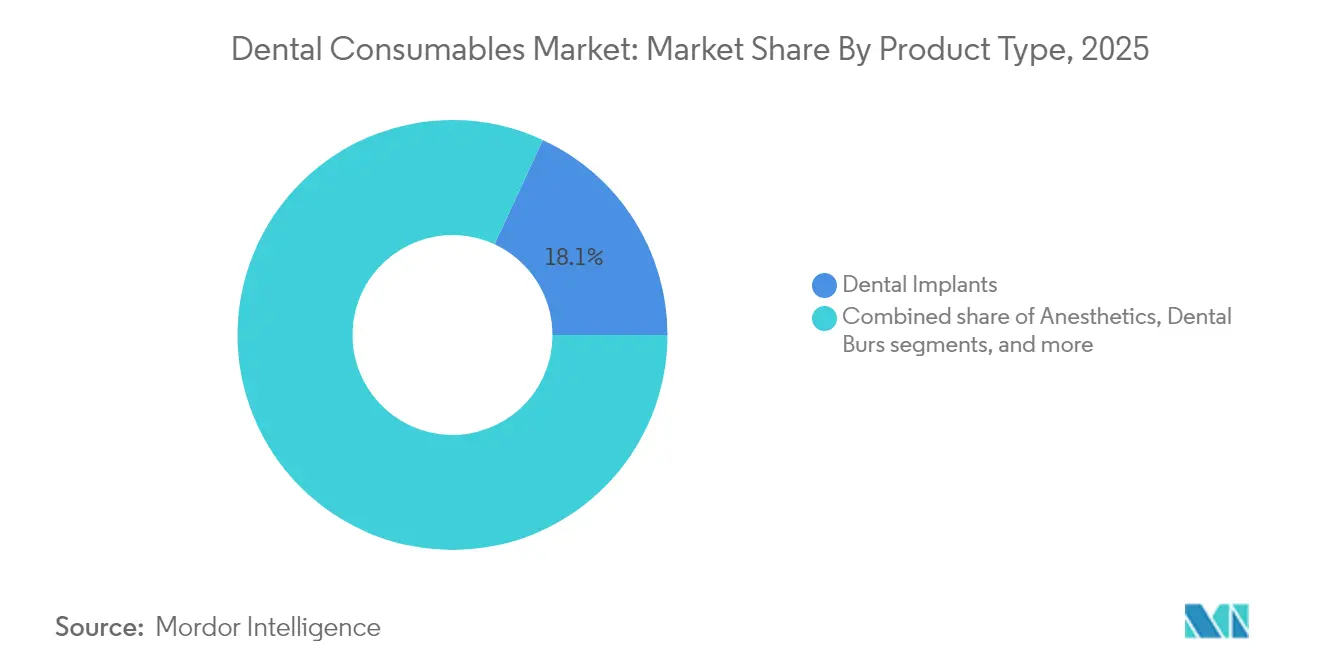

- By product type, dental implants held 18.10% of dental consumables market share in 2025; personal protective wear is projected to grow at a 9.74% CAGR to 2031.

- By treatment modality, prosthodontic procedures commanded 27.35% share of the dental consumables market size in 2025, while orthodontics is expected to expand at 9.42% CAGR through 2031.

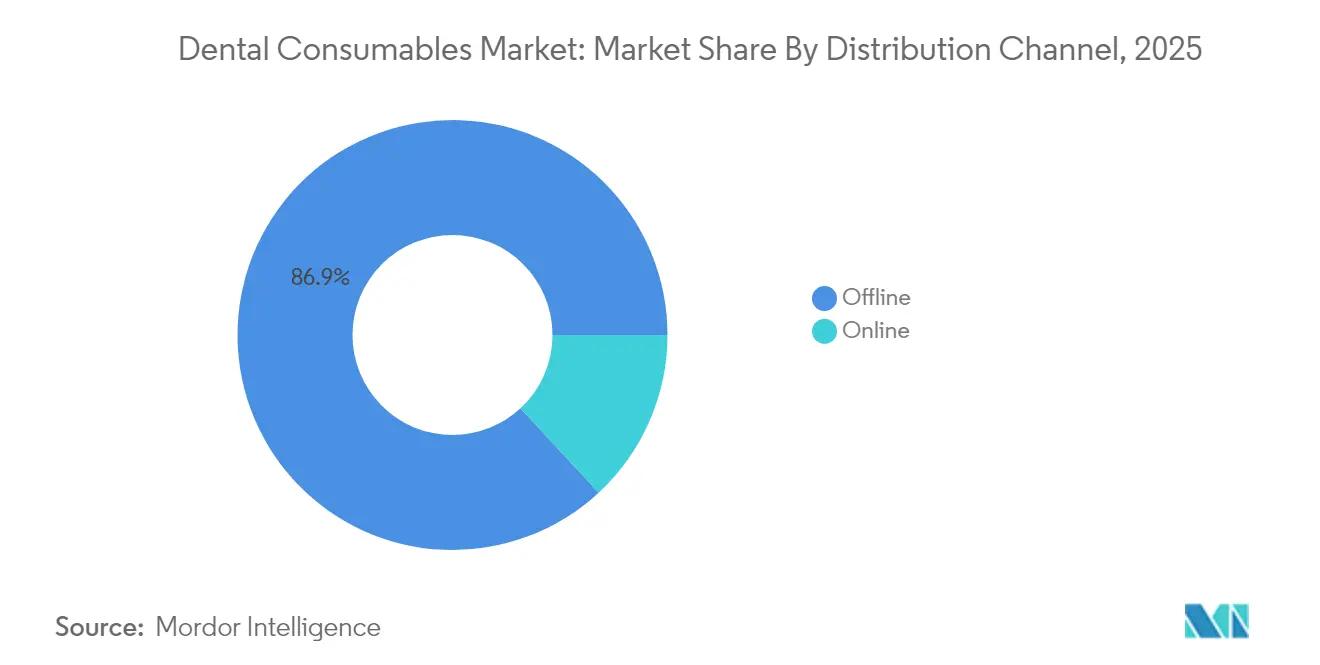

- By distribution channel, offline B2B transactions accounted for 86.90% of the dental consumables market size in 2025; the online channel is advancing at a 9.66% CAGR to 2031.

- By end-user, dental clinics captured 52.55% of dental consumables market share in 2025 as DSO/group practices exhibit the highest forecast CAGR of 9.52% through 2031.

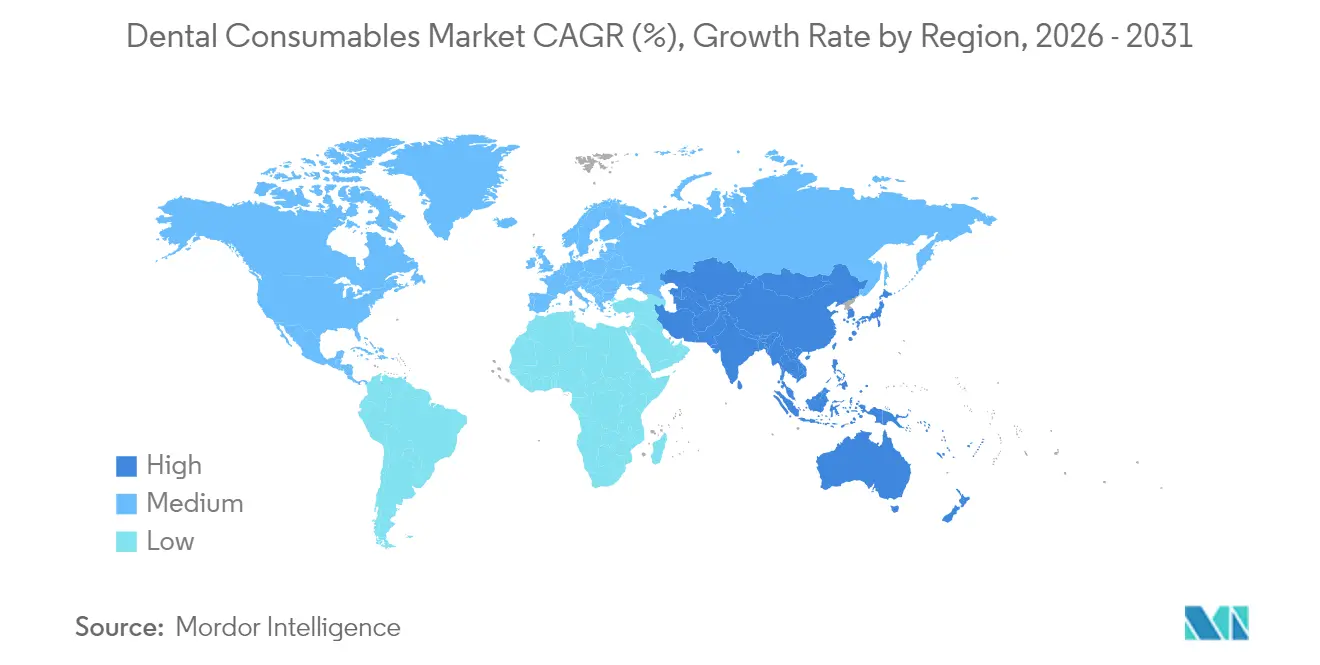

- By geography, North America led with 42.95% revenue share in 2025; Asia Pacific is projected to post the fastest 9.22% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dental Consumables Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for same-day CAD/CAM prosthetics | +1.8% | North America, Europe, Urban APAC | Medium term (2-4 years) |

| Elderly population growth increasing prosthodontic procedures | +1.6% | Japan, Europe, North America | Long term (≥ 4 years) |

| Expansion of DSOs driving bulk procurement | +1.5% | North America, expanding to Europe & APAC | Medium term (2-4 years) |

| Rapid adoption of clear-aligner orthodontics | +1.4% | Global, highest penetration in North America | Medium term (2-4 years) |

| Shift toward bioactive and regenerative implant materials | +1.2% | Global, early adoption in North America & Europe | Long term (≥ 4 years) |

| Preventive-oral care campaigns boosting sealant use | +0.8% | Developing markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for same-day CAD/CAM prosthetics

More than half of U.S. dental practices already employ intraoral scanners, shortening treatment cycles and expanding indications for premium restorative materials. Chairside milling paired with cloud design services lowers laboratory overhead and lifts profitability. AI-enabled design modules automate complex margin and contact adjustments, further reducing chairtime. Adoption accelerated by 18% in 2024, and with scanner integration set to improve imaging precision in 2025, material throughput is expected to rise in tandem. Suppliers capable of bundling scanners, mills, and validated material blocks are securing long-term contracts with DSOs.

Elderly population expansion increasing prosthodontic procedures

Adults aged 65 plus represent the fastest-growing patient cohort. Japan already allocates specialized reimbursement pathways for implant-supported overdentures, and the EU’s Silver Economy program earmarks funds for geriatric dental care. Digital denture workflows reduce appointment burden, improving acceptance among seniors with mobility constraints. Material suppliers are commercializing lightweight polymer bases and high-impact acrylics[1]Academy of Prosthodontics, “President’s Column,” academyofprosthodontics.org tailored to xerostomia-prone patients.

Growth of dental service organizations (DSOs) driving bulk procurement

DSOs are growing at 9.88% annually, consolidating practice ownership and centralizing purchasing decisions. Scale permits favorable long-term supply agreements that bundle implants, restorative kits, and chairside scanners. U.S. legal firm Dykema projects DSO penetration could reach 30% of all practices by 2030[2]Dykema, “Dental Service Organizations,” dykema.com, reshaping manufacturer–provider negotiations toward integrated value propositions.

Shift toward bioactive and regenerative implant materials

Clinical evidence shows that carbon-based bioactive coatings improve osseointegration and reduce bacterial adhesion, allowing implants to integrate in compromised bone. As outcome data accumulates, practitioners favor higher-priced surfaces that cut revision risk, expanding the total implantable base. Manufacturers are adding proprietary bioactive topologies to differentiate, and European regulators have cleared the first generation of carbon-coated titanium fixtures[3]Nazrah Maher et al., “An Updated Review and Recent Advancements in Carbon-Based Bioactive Coatings for Dental Implant Applications,” Journal of Advanced Research, doi.org for broad release in 2025.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited insurance reimbursement for cosmetic dentistry | -1.2% | North America, Europe | Medium term (2-4 years) |

| Skills gap in chairside CAD/CAM workflows | -0.9% | Emerging markets | Medium term (2-4 years) |

| Volatile resin and precious-metal prices | -0.7% | Global, higher impact in developing markets | Short term (≤ 2 years) |

| Regulatory delays for novel bio-ceramic approvals | -0.6% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited insurance reimbursement for cosmetic dentistry

Aesthetic veneers, bleaching, and gingival contouring remain predominantly self-pay. While Medicare will extend coverage to certain medically-linked dental procedures in 2025, elective cosmetic benefits remain constrained. This bifurcates the market, sustaining luxury segments yet limiting total unit volumes. Manufacturers counteract by offering tiered composite lines that balance price and polish retention.

Skills gap in chair-side CAD/CAM workflows

Transitioning from conventional impressions to intraoral scanners demands technician training unavailable in smaller practices. Emerging markets see slower technology uptake due to limited continuing-education budgets. Industry associations are funding modular e-learning, but a persistent proficiency gap tempers scanner shipments in low-resource settings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Premium Implants Anchor Revenue Growth

Dental implants accounted for 18.10% of the dental consumables market share in 2025. High-success bioactive coatings and digital surgical planning expand indications into softer bone situations. The dental consumables market size for personal protective wear is forecast to climb at 9.74% CAGR to 2031, notably buoyed by Asia Pacific’s geriatric cohorts. The segment's sharp trajectory is further propelled by infection-control protocols that demand ASTM-certified respirators and autoclavable eye shields.

The prosthetics sub-segment benefits from CAD/CAM workflows that fabricate zirconia and lithium-disilicate crowns in under one hour. Universal bonding agents streamline inventory by covering multiple etching strategies. Regenerative materials such as calcium-phosphate granules grow in tandem with ridge-augmentation procedures. Meanwhile, sutures and burs, although mature, enjoy marginal gains from ergonomic handle redesigns that reduce operator fatigue.

By Treatment Modality: Digital Workflows Redefine Clinical Practice

Prosthodontic procedures accounted for 27.35% share of the dental consumables market in 2025 as full-arch rehabilitation moves chairside through guided surgery and immediate loading. Orthodontics, driven by clear aligners, records the highest modality growth of 9.42%; cloud-planning software and in-house 3-D printed aligners reduce cycle time and boost case starts.

Restorative dentistry embraces minimally invasive preps using bioactive composites that release fluoride and calcium ions, prolonging restoration life. Endodontics innovates with bioceramic sealers and reciprocation-motion files that cut procedure time. Periodontics integrates regenerative membranes and enamel-matrix derivatives that encourage new attachment. Cosmetic procedures, although self-funded, gain momentum via social media exposure and rising tele-consultation convenience.

By Distribution Channel: E-Commerce Captures Routine Re-orders

Offline distributors still command 86.90% of 2025 revenue by bundling consumables, equipment financing, and technical service. However, the dental consumables market is witnessing online platforms grow at 9.66% CAGR as price-comparison transparency and automated ordering modules simplify replenishment. DSOs increasingly negotiate directly with manufacturers for large-volume contracts, pressuring traditional wholesalers to adopt hybrid digital storefronts with same-day fulfillment.

Digital portals integrate with practice-management software, allowing usage analytics to trigger auto-stocking for high-velocity items such as anesthesia carpules and etchants. Multinational distributors pilot subscription boxes for clear aligner auxiliaries and hygiene kits, smoothing demand patterns and enhancing customer retention.

By End-User: Consolidation Reshapes Buying Power

Dental clinics represented 52.55% of 2025 demand. Independent offices emphasize reliable supplier relationships and on-site education. The dental consumables market expectations shift as DSO/group practices show a 9.52% CAGR; procurement teams standardize formularies, pushing vendors to demonstrate cost-per-procedure efficiency. Hospitals, though smaller in count, procure high-value items for oncology or trauma-linked oral rehabilitation, positioning them as early adopters of advanced biomaterials.

Laboratories transition from casting alloys to milled and printed substructures, broadening material pallets and spurring demand for zirconia discs and resin pucks. Academic institutions set training norms, elevating digital workflow familiarity among new graduates and indirectly shaping future purchasing preferences.

Geography Analysis

North America generated 42.95% of global revenue in 2025. Implant therapy and clear-aligner cases command premium pricing, while insurers expand preventive benefits that lift sealant and fluoride varnish volumes. Regulatory clarity under FDA 510(k) accelerates product launches; however competition among a growing dentist workforce may intensify price sensitivity in commodity segments.

Asia Pacific is projected to grow at 9.22% CAGR through 2031, buoyed by urban middle-class expansion and inbound dental tourism. Governments in India and Thailand endorse public-private partnerships to equip rural clinics. Local manufacturers capitalize by offering cost-competitive scanners and implant systems while partnering with global majors for material validation, shortening supply chains and countering import tariffs.

Europe maintains steady 8.14% CAGR supported by robust reimbursement frameworks and rigorous product-quality standards. Germany’s precision-engineering base nurtures high-strength ceramic production, while the United Kingdom accelerates digital dentistry adoption via NHS modernization funds. The Middle East & Africa and South America post 7.52% and 7.63% CAGRs respectively as private insurance penetration and public oral-health campaigns broaden access.

Competitive Landscape

Top-five suppliers—Dentsply Sirona, Henry Schein, Envista, Straumann, and Ivoclar—collectively account for a large chunk of global revenue, indicating moderate concentration. These integrators cross-sell implants, restorative systems, and imaging hardware, leveraging service networks to lock in multi-year contracts. Straumann’s recent acquisition of an AI-planning start-up accelerates treatment-workflow integration, while Henry Schein expands European reach through distributor roll-ups.

Mid-tier specialists target niches: Coltene refines impression materials, GC introduces bioactive glass-ionomer innovations, and Septodont advances articaine anesthetics. Direct-to-patient disruptors like SmileDirectClub ignite aligner demand, compelling established orthodontic brands to enhance teledentistry capabilities. Sustainability emerges as a differentiator, with Ultradent piloting recyclable packaging and Young Innovations adopting solar-powered production lines.

DSO purchasing power alters negotiation leverage. Manufacturers able to bundle chairside units, consumables, and cloud support gain preferred-vendor status. In 2024, Benco Dental acquired two regional supply houses to boost logistics density in the U.S. Midwest, illustrating distributor consolidation aimed at defending share against online entrants.

Global Dental Consumables Industry Leaders

Dentsply Sirona

Envista Holdings

Henry Schein Inc.

Ivoclar Vivadent AG

Straumann Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The University of Washington School of Dentistry opened an oral-health training center in Spokane to address rural provider shortages.

- November 2024: Medicare confirmed expanded dental coverage for conditions associated with end-stage renal disease effective 2025.

- November 2024: Benco Dental acquired M&S Dental Supply and A-Dent Dental Equipment, strengthening its Midwest distribution footprint.

- May 2024: Senator Sanders introduced the Comprehensive Dental Reform Act of 2024, proposing broader Medicare and Medicaid coverage for essential dental care.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the dental consumables market as single-use or limited-life products a dentist employs to restore teeth, treat soft-tissue issues, or support preventive and aesthetic procedures. Items span implants, restorative materials, orthodontic appliances, anesthetics, burs, sutures, splints, and personal protective articles that must be replenished regularly. According to Mordor Intelligence, the global market was valued at USD 39.99 billion in 2025 and is forecast to reach USD 59.64 billion by 2030.

Scope exclusion: Retail oral-care staples sold direct to consumers, such as toothpaste and mouthwash, are outside this definition.

Segmentation Overview

- By Product Type

- Aligners & Braces

- Anesthetics

- Bonding Agents & Adhesives

- Dental Burs

- Dental Implants

- Dental Splints

- Dental Sutures

- Hemostats

- Personal Protective Wear

- Prosthetics

- Regenerative Materials

- Restorative Materials

- Other Product Types

- By Treatment Modality

- Restorative

- Prosthodontic

- Endodontic

- Periodontic

- Orthodontic

- Cosmetic / Aesthetic

- Others

- By Distribution Channel

- Offline

- B2B

- B2C

- Online

- Offline

- By End-User

- Dental Clinics

- Dental Hospitals

- DSO / Group Practices

- Other End-Users

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with practicing dentists, procurement heads at Dental Service Organizations, distributors, and material scientists across North America, Europe, Asia-Pacific, and Latin America clarify average selling prices, chair-time trends, and emerging material shifts.

Voice-of-customer surveys test our preliminary volume pools and reveal regional procurement cycles that desk work alone cannot expose.

Desk Research

We start with public datasets that anchor procedure volumes and spending, including WHO Global Health Observatory, FDI World Dental Federation surveys, Centers for Medicare & Medicaid dental claims dashboards, Eurostat trade codes, and UN Comtrade shipment flows. Company filings, investor decks, and trade-association newsletters add insight on unit pricing and material adoption. Paid databases that Mordor analysts access, such as D&B Hoovers for supplier revenues and Dow Jones Factiva for tender notices, refine input assumptions. The sources listed are illustrative; many additional references inform the model and cross-checks.

Market-Sizing & Forecasting

A top-down build draws on restorative and orthodontic procedure counts that we reconstruct from treatment claims and trade data, then multiplies them by validated consumables-per-procedure coefficients. Select bottom-up roll-ups of supplier revenues and sampled ASP × unit checks align the totals. Key variables feeding the model include implant placements per 1,000 population, clear-aligner adoption rates, elderly population growth, average DSO procurement budgets, and CAD/CAM chairside penetration. Multivariate regression plus scenario analysis projects these drivers forward, and gaps in bottom-up estimates are bridged through price interpolation and region-specific utilization proxies.

Data Validation & Update Cycle

Outputs pass three layers of analyst review, variance checks against external spend indexes, and re-contact of experts when material deviations appear.

Reports refresh each year, with mid-cycle updates after regulatory or technology events so clients receive the latest view.

Why Our Dental Consumables Baseline Earns High Trust

Published figures often diverge because firms choose different product baskets, input variables, and refresh cadences. By defining a clear clinical scope and pairing procedure pools with validated usage coefficients, Mordor Intelligence produces a balanced baseline buyers can retrace.

Key gap drivers include whether over-the-counter hygiene goods are counted, the breadth of emerging economies captured, and how currency translations are timed. Our annual refresh and dual cross-checks keep totals current, while some publishers rely on multi-year roll-forward factors.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 39.99 B (2025) | Mordor Intelligence | - |

| USD 43.85 B (2025) | Global Consultancy A | Includes infection-control disposables and consumer whitening kits, inflating scope |

| USD 39.18 B (2025) | Trade Journal B | Omits several emerging markets and uses historic price averages without mid-year FX updates |

In summary, the disciplined selection of variables, timely data refresh, and transparent triangulation steps applied by Mordor analysts deliver a dependable reference point that decision-makers can trust and replicate with confidence.

Key Questions Answered in the Report

How are dental service organizations (DSOs) reshaping purchasing strategies?

DSOs centralize procurement across large practice networks, favoring suppliers that can bundle implants, restorative kits, and digital workflow tools under volume-based contracts, which tightens margins for smaller distributors.

Why are bioactive implant materials attracting clinician interest?

Carbon-based coatings and regenerative surfaces actively promote osseointegration and reduce bacterial adhesion, helping practitioners lower revision rates and treat patients with compromised bone quality.

What is driving clinician adoption of same-day CAD/CAM workflows?

Intraoral scanners paired with chairside mills compress treatment time into a single visit, improve patient experience, and boost practice profitability by cutting reliance on external labs.

How does volatility in precious-metal prices impact restorative material choices?

Fluctuating costs for gold and palladium push labs and clinics toward zirconia and high-performance polymers, reducing exposure to commodity swings while preserving clinical outcomes.

What factors accelerate the migration to online purchasing platforms?

Widespread adoption of intraoral scanners and chairside mills accelerates same-day restorations, boosting usage of premium ceramics, bonding agents, and 3-D printable resins.

How do preventive-oral care campaigns influence consumable innovation?

Government and insurer emphasis on early intervention drives demand for sealants and fluoride varnishes, prompting manufacturers to develop faster-curing, higher-fluoride formulations tailored for school-based programs.

Page last updated on: