Endodontic Files Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

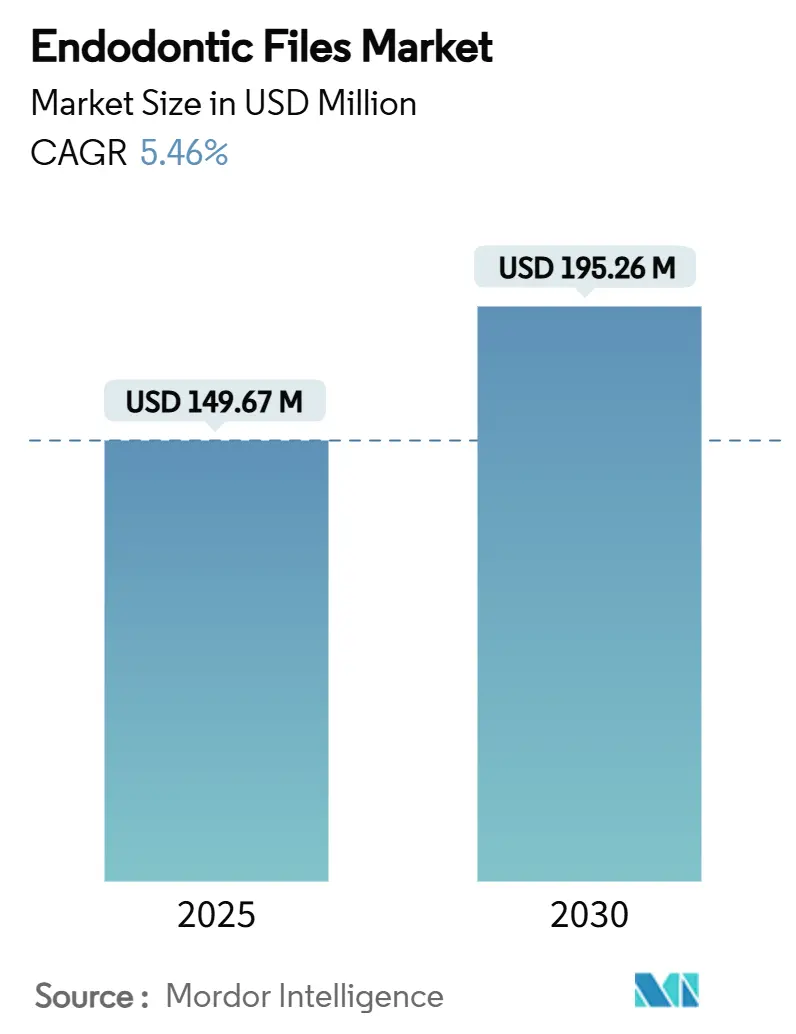

| Market Size (2025) | USD 149.67 Million |

| Market Size (2030) | USD 195.26 Million |

| Growth Rate (2025 - 2030) | 5.46% CAGR |

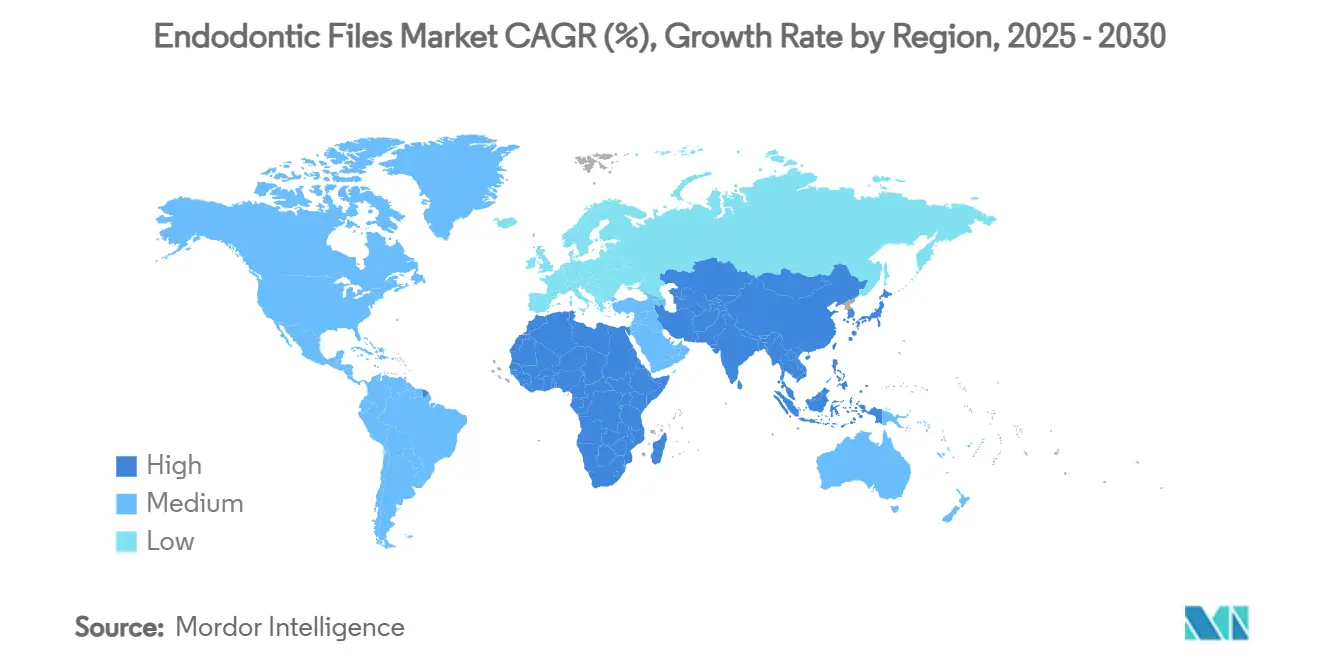

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

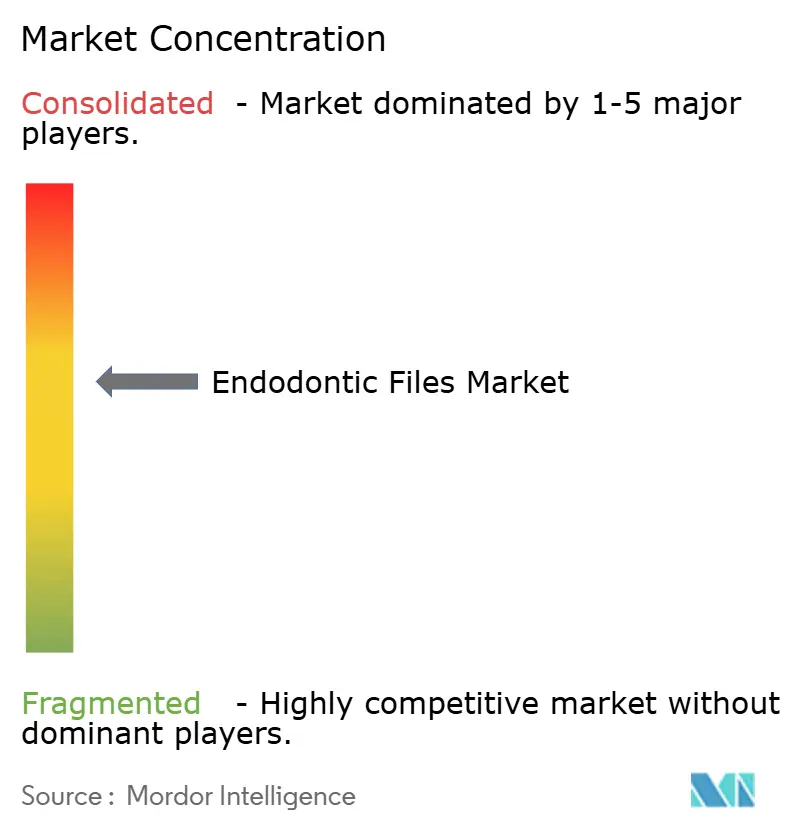

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Endodontic Files Market Analysis by Mordor Intelligence

The endodontic files market size reached USD 149.67 million in 2025 and is projected to rise to USD 195.26 million by 2030 at a 5.46% CAGR, highlighting a healthy demand trajectory that overrides short-term macro-economic slowdowns. A widening pool of root-canal patients, steady procedural volumes in mature economies, and sustained equipment upgrades in emerging regions are the central growth engines. Technological gains in nickel-titanium (NiTi) metallurgy, particularly heat-activated and controlled-memory designs, continue to cut chair-time and instrument breakage, strengthening practitioners’ preference for premium rotary lines. Parallel adoption of single-file systems is accelerating because the simplified workflow raises productivity in high-volume practices. Digital supply models—subscription auto-ship programs and AI-assisted torque-controlled motors—are tightening inventory management while extending instrument life, thereby deepening supplier-clinic integration. Competitive intensity remains moderate; incumbents invest in clinical education and bundled service agreements to protect share in the endodontic files market.[1]Nityanand Jain, “WHO's Global Oral Health Status Report 2022: Actions, Discussion and Implementation,” Wiley Online Library, onlinelibrary.wiley.com

Key Report Takeaways

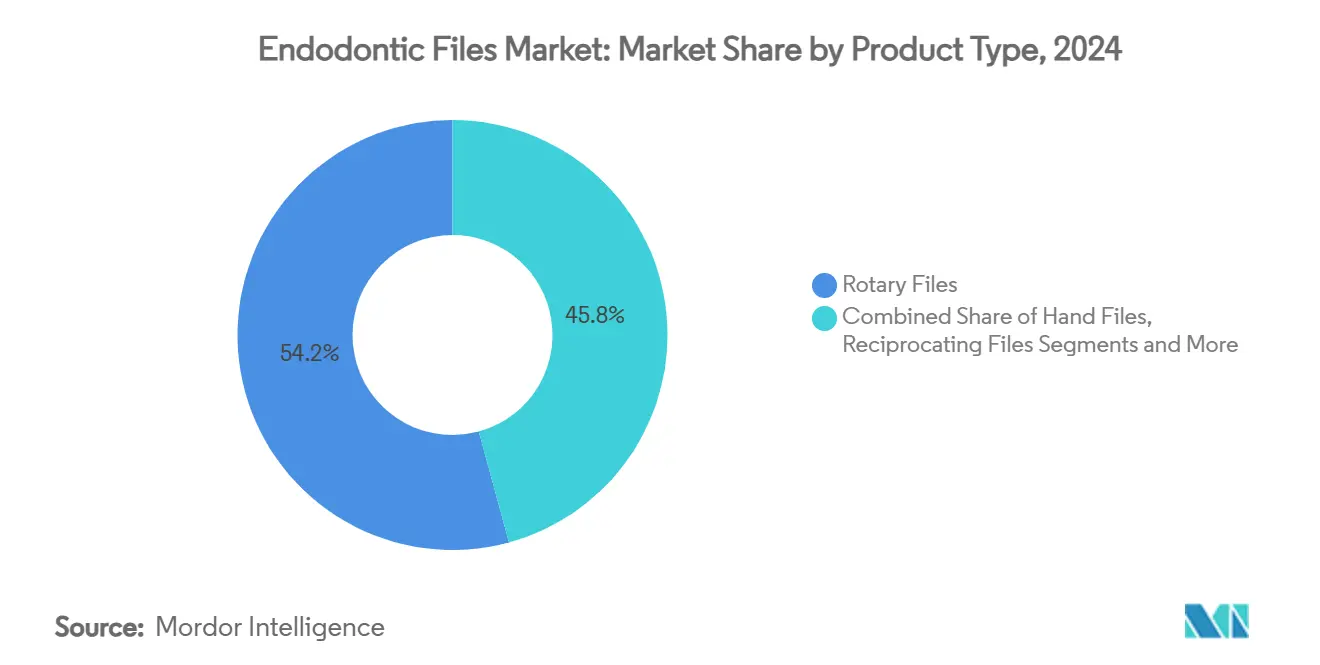

- By product type, rotary files captured 54.23% revenue share in 2024; single-file systems are projected to expand at an 8.23% CAGR to 2030.

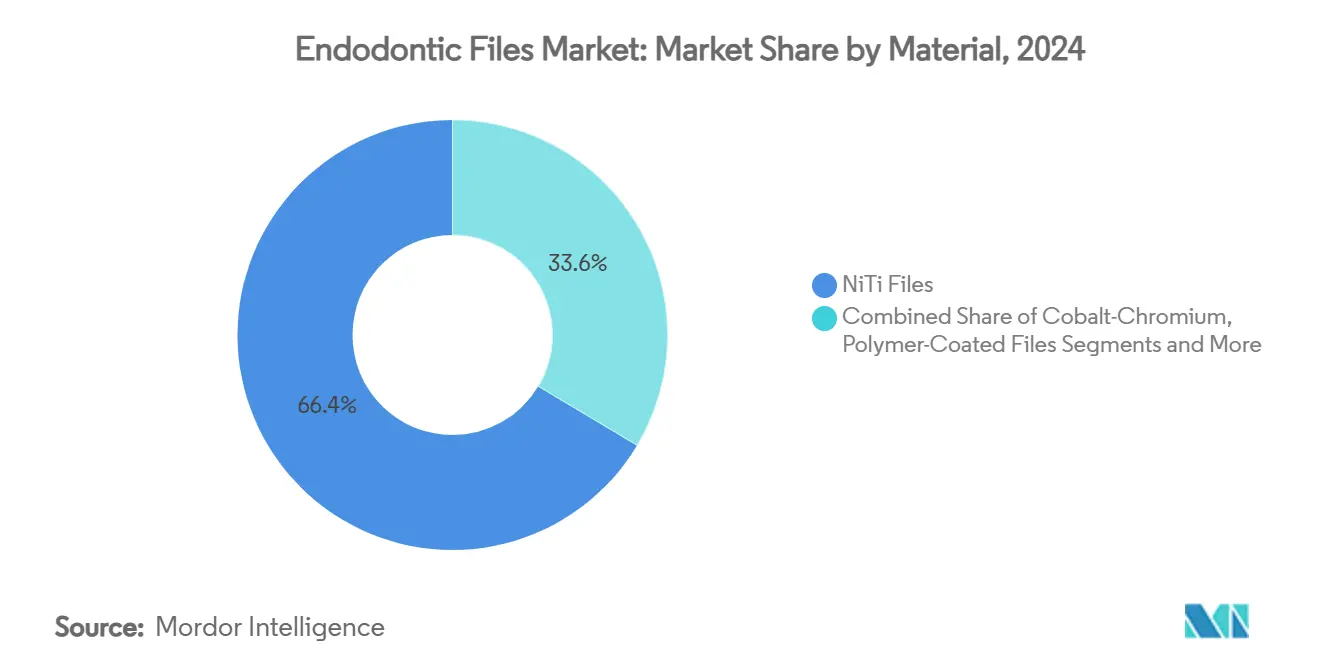

- By material, NiTi instruments accounted for 66.43% of the endodontic files market size in 2024 and are advancing at a 9.57% CAGR through 2030.

- By end user, dental clinics held 59.67% share of the endodontic files market in 2024, while dental service organizations are on track for the fastest 8.43% CAGR between 2025-2030.

- By geography, North America commanded 33.64% of global revenue in 2024; Asia-Pacific is forecast to deliver the highest 7.62% CAGR through 2030.

Global Endodontic Files Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of dental caries and root-canal procedures | +1.8% | Global, higher in APAC & MEA | Long term (≥ 4 years) |

| Technological advances in NiTi rotary file designs | +1.2% | North America & Europe; spill-over to APAC | Medium term (2-4 years) |

| Growing number of dental clinics and practitioners | +0.9% | APAC core; Latin America expanding | Long term (≥ 4 years) |

| Increasing adoption of single-file reciprocation systems | +0.7% | North America & Europe | Short term (≤ 2 years) |

| Growth of subscription-based auto-ship models | +0.4% | North America; early Europe | Medium term (2-4 years) |

| AI-assisted torque-controlled motors improving file longevity | +0.3% | North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Dental Caries and Root-Canal Procedures

Annual global incidence of permanent-tooth decay rose from 29,896 per 100,000 population in 2021 to a projected 30,414 by 2030, a trend that disproportionately affects 15-24-year-olds in lower-income economies and in turn drives sustained demand for root-canal therapy.[2]Fatemeh Shabazi, “Global Trends and Projection of Caries of Permanent Teeth Incidence from 1990 to 2030: A Modeling Study,” IntechOpen, intechopen.com Southern Latin America and South Asia recorded the steepest 2024 burden increases, while multimorbidity in older adults elevated root caries prevalence in the United States, locking in long-term treatment demand. Pediatric studies show nearly half of 6-12-year-olds needing endodontic intervention, establishing early-life treatment patterns that persist.[3]Sin Lee, Ya-Hsin Yu, Bekir Karabucak, “Endodontic Treatments on Permanent Teeth in Pediatric Patients Aged 6–12 Years Old,” PubMed, pubmed.ncbi.nlm.nih.gov Retrospective 2025 evidence found 28.7% of treated teeth presenting with pre-operative apical periodontitis, with caries as the primary factor in 84.07% of cases, further linking caries incidence to endodontic file usage. Collectively, these epidemiological pressures underpin volume growth in the endodontic files market.

Technological Advances in NiTi Rotary File Designs

Thermomechanical processing now customizes transformation temperatures, producing heat-activated files that flex inside severely curved canals while retaining cutting power. Cryogenic treatment raised fracture resistance of Neoniti instruments to 280,600 cycles, 19% higher than untreated controls, lowering replacement frequency and lifetime cost.[4]Firouz Zadfatah et al., “Effect of Cryotherapy on Fracture Resistance of Neoniti Rotary Instruments,” PubMed, pubmed.ncbi.nlm.nih.govNano-scale surface functionalization improves debris removal and secures smoother dentinal walls, reducing post-operative sensitivity. Controlled-memory (CM) metals enable pre-bent shaping, eliminating canal transportation and obviating extra shaping files. Manufacturers leverage these performance gains to justify premium pricing and elevate the endodontic files market value proposition.

Growing Number of Dental Clinics and Practitioners

WHO data confirm that 68% of member states still house fewer than 5 dentists per 10,000 population, which forces existing practitioners to handle heavier caseloads and replace files more frequently . Rapid private-practice expansion in Asia and Latin America, supported by government oral-health programs and rising disposable incomes, lifts instrument volumes. Specialized endodontic centers cluster in urban hubs, concentrating complex cases that rely on advanced rotary lines. Digital adoption—chair-side CBCT and electronic apex locators—prompts clinics to bundle compatible file systems, reinforcing repeat purchases in the endodontic files market.

Increasing Adoption of Single-File Reciprocation Systems

WaveOne Gold and similar reciprocating files streamline shaping to a single instrument, cutting instrumentation time without sacrificing cleaning efficacy. Comparative trials in oval canals show the XP-endo Shaper delivering lower bacterial counts than conventional systems, proving clinical equivalence while shrinking inventory loads. Shorter chair-time translates into more daily procedures, a critical gain for high-volume DSO clinics. Reduced fracture risk builds practitioner confidence, accelerating the shift toward single-file workflows and lifting this niche within the endodontic files market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of NiTi rotary instrumentation sets | -1.1% | Global, particularly emerging markets | Short term (≤ 2 years) |

| Limited reimbursement in emerging markets | -0.8% | APAC, Latin America, MEA | Medium term (2-4 years) |

| Environmental regulations on nickel waste disposal | -0.5% | North America & Europe | Long term (≥ 4 years) |

| Rise of minimally-invasive vital-pulp therapies | -0.4% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of NiTi Rotary Instrumentation Sets

Comprehensive rotary platforms—motor, handpiece, and multiple file batches—often exceed USD 10,000, a formidable upfront outlay for solo practitioners. The single-use recommendation of many premium files adds recurring spending that can erode practice margins unless offset by higher procedural fees. Smaller clinics in Southeast Asia and Africa frequently rely on legacy hand files to remain price-competitive, slowing adoption of advanced systems in those portions of the endodontic files market. Training fees and downtime for certification compound investment hurdles, stretching breakeven horizons.

Limited Reimbursement in Emerging Markets

Insurance programs in APAC, Latin America, and MEA prioritize extractions or basic fillings, leaving root-canal therapy either partially covered or entirely self-pay. The cost delta between rotary and hand-file procedures makes it difficult for practitioners to justify premium instrument use when patients are highly price-sensitive. The absence of standardized reimbursement codes for advanced instrumentation prolongs claim processing and introduces revenue-timing uncertainty, which discourages clinics from upgrading, dampening expansion in the endodontic files market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Single-File Systems Streamline Workflows

Rotary instruments dominated the endodontic files market share with 54.23% in 2024, reflecting entrenched clinical familiarity and proven efficiency. Single-file systems, however, posted the sector’s quickest 8.23% CAGR forecast, buoyed by studies showing comparable debridement and superior time savings. The endodontic files market size for single-file platforms is projected to grow steadily as DSOs standardize one-instrument protocols to maximize chair utilization. Reciprocating files consolidate demand because their alternate motion lessens torsional fatigue, extending life cycles. Hand files remain important for initial negotiation in pediatric or highly calcified canals, ensuring they preserve a modest but stable revenue stream inside the endodontic files market. Glide-path instruments—often overlooked—record incremental expansion because clinicians now recognize that smooth preliminary paths lower fracture risk in subsequent shaping stages.

Hybrid treatment approaches are emerging, wherein a glide-path file precedes a single rotary shaper, marrying safety with speed. Vendors differentiate through proprietary heat-treatment curves that tailor flexibility to canal morphologies, preserving loyalty in an increasingly commoditized product class. Marketing now emphasizes procedural simplicity and reduced sterilization overhead rather than pure cutting metrics. As global epidemiology elevates the need for efficient re-treatments, single-file systems gain further traction, underpinning robust dollar growth within the endodontic files market.

By Material: NiTi Commands Both Volume and Momentum

NiTi instruments accounted for 66.43% of the endodontic files market size in 2024, powered by transformational metallurgy that grants elastic memory and corrosion resistance. Continuous 9.57% CAGR through 2030 stems from incremental breakthroughs such as diamond or polymer surface coatings that slash friction and improve debris clearance. Stainless-steel lines survive in cost-sensitive niches, but lack the flexibility demanded for severely curved canals, restraining their advance. Cobalt-chromium variants offer stiffness advantages yet struggle to articulate a compelling premium over state-of-the-art NiTi, limiting share pick-up inside the endodontic files market.

Environmental scrutiny forces suppliers to experiment with biodegradable sheathings and in-clinic recycling kits to curb nickel discharge. Controlled-memory NiTi files, capable of cold pre-bending, enable safe passage through abrupt canal curvatures and are particularly valued in re-treatment scenarios. Procedural evidence demonstrates lower transportation and reduced post-operative pain with CM designs, reinforcing the premium NiTi category. As manufacturers integrate smart RFID chips for usage tracking, the material landscape enters a data-driven era that further raises entry barriers for low-cost substitutes.

By End User: DSOs Reshape Procurement Power

Dental clinics retained 59.67% of 2024 revenue but face a changing market as DSOs expand at an 8.43% CAGR to 2030, centralizing procurement and standardizing care pathways. The endodontic files market size controlled by DSOs gradually narrows the gap with independent practices through aggressive acquisition and greenfield projects in North America and, increasingly, Europe. Central purchasing committees negotiate bulk discounts and enforce formulary compliance, steering demand toward fewer, vertically integrated suppliers.

Hospitals keep a solid foothold for trauma-related or medically complex cases, yet many elective root-canal treatments migrate to outpatient settings for cost efficiency. Academic institutions contribute via research purchases and clinician education, seeding early adoption of next-generation files even if their direct volume remains limited. Vendors respond with turnkey service bundles—continuing education, maintenance contracts, inventory analytics—to embed themselves deeper in DSO supply chains and preserve share in the endodontic files market.

Geography Analysis

North America, representing 33.64% of global revenue in 2024, benefits from widespread insurance coverage, high practitioner density, and rapid uptake of AI-enabled motors. Regular FDA 510(k) clearances shorten commercialization cycles, allowing quick market entry for iterative file enhancements. DSOs’ consolidated purchases amplify bulk-buy leverage, pressuring price points yet expanding unit throughput across the endodontic files market. Rising environmental oversight encourages recycling partnerships that can serve as competitive differentiators.

Asia-Pacific is the growth engine, with a 7.62% CAGR forecast tied to population scale and rising household incomes. China’s Healthy China 2030 plan and India’s National Oral Health Program channel funds into clinic build-outs, widening access to advanced root-canal care. However, price sensitivity pushes practitioners toward value-engineered rotary kits or prolonged use cycles, challenging premium importers. Local manufacturing capacity is evolving, hinting at eventual cost competitiveness that could redistribute value pools within the endodontic files market.

Europe’s mature yet regulated environment favors premium priced, MDR-compliant innovations. Sustainability directives accelerate demand for recyclable packaging and take-back schemes, nudging manufacturers toward closed-loop supply chains. Middle East and Africa, though smaller in absolute revenue, attract investment in Gulf Cooperation Council nations where state insurers now reimburse endodontic therapy, unlocking pent-up demand. Political instability in parts of Sub-Saharan Africa, however, renders distribution riskier, thereby slowing full regional capture.

Latin America shows mixed prospects; Brazil and Mexico lead procedural volumes due to more robust private insurance penetration, whereas Andean and Central American markets lag because of economic volatility. Currency swings influence imported NiTi pricing, causing sporadic shifts in market share between international brands and emerging regional suppliers. Throughout all regions, tele-education platforms spread advanced technique adoption, harmonizing clinical standards and reinforcing consistent demand in the global endodontic files market.

Competitive Landscape

The endodontic files market remains moderately fragmented. Dentsply Sirona, Danaher’s Kerr Endodontics, and Coltene Holding anchor the leadership tier, leveraging global distribution, robust R&D pipelines, and extensive practitioner training. Dentsply Sirona’s August 2024 rollout of the X-Smart Pro+ motor paired with Reciproc Blue exemplifies a one-file approach that underscores integration between instrument and equipment portfolios. Strategic acquisitions—such as Coltene’s purchase of Komet Endo assets—add complementary SKUs while plugging geographic gaps.

Second-tier firms emphasize niche innovation: heat-treated CM alloys, micro-laser etched flutes, and RFID traceability. Patent filings, including King Saud University’s ultrasonic deformable obturation point, signal ongoing IP vitality and entry avenues for academia-industry spin-offs. Subscription auto-ship models reshape revenue logic from one-off sales to recurring service contracts, offering distributors defensible margins and predictable cash flows. Digital motor analytics build switching costs by embedding software into clinical workflow, ensuring steady file pull-through.

Competitive barriers gradually rise as regulatory scrutiny over nickel disposal and MDR documentation raises compliance costs. That favors well-capitalized players able to scale quality systems and furnish traceability audits. Yet localized production in India and China is on the rise, promising lower-priced comps that may disrupt mature-market pricing structures over the next five years. Midsized companies thus explore OEM partnerships to hedge geographic risk and secure cost advantages, sustaining dynamic competition across the endodontic files market.

Endodontic Files Industry Leaders

Dentsply Sirona

Danaher

Coltene Holding

Septodont

Mani Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Dentsply Sirona introduced the X-Smart Pro+ motor with integrated apex locator and the universal Reciproc Blue file, enabling a single-file endodontic workflow for United States practitioners.

- March 2024: Dentsply Sirona launched a comprehensive Indirect Restorative course series through DS Academy, incorporating advanced endodontics modules to support clinical adoption of its instrumentation range.

Global Endodontic Files Market Report Scope

| Hand Files |

| Rotary Files |

| Reciprocating Files |

| Single-File Systems |

| Glide Path Files |

| Stainless-Steel Files |

| Nickel-Titanium (NiTi) Files |

| Cobalt-Chromium Files |

| Polymer-Coated Files |

| Diamond-Coated Files |

| Dental Clinics |

| Hospitals |

| Academic & Research Institutes |

| Dental Service Organizations (DSOs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Hand Files | |

| Rotary Files | ||

| Reciprocating Files | ||

| Single-File Systems | ||

| Glide Path Files | ||

| By Material | Stainless-Steel Files | |

| Nickel-Titanium (NiTi) Files | ||

| Cobalt-Chromium Files | ||

| Polymer-Coated Files | ||

| Diamond-Coated Files | ||

| By End User | Dental Clinics | |

| Hospitals | ||

| Academic & Research Institutes | ||

| Dental Service Organizations (DSOs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current value of the endodontic files market?

The endodontic files market size was USD 149.67 million in 2025

2. How fast is the endodontic files market expected to grow?

Revenue is projected to reach USD 195.26 million by 2030, implying a 5.46% CAGR.

3. Which product type is growing the fastest?

Single-file systems lead growth with an 8.23% CAGR, thanks to streamlined workflows.

4. Why do NiTi files dominate the endodontic files market share?

NiTi’s flexibility, fracture resistance, and ongoing heat-treatment innovations drive a 66.43% share and 9.57% CAGR.

5. Which region offers the highest growth potential?

Asia-Pacific is forecast to expand at 7.62% CAGR due to improving access to dental care and rising oral-health awareness.

Page last updated on: