Dental Burs Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

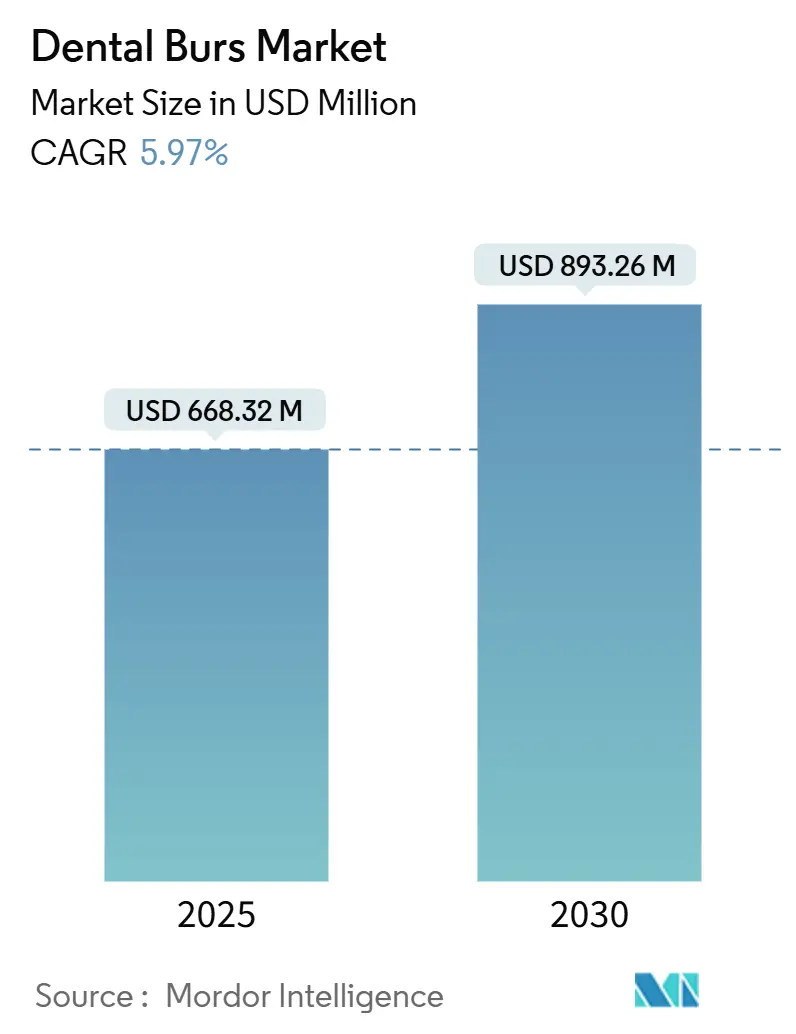

| Market Size (2025) | USD 668.32 Million |

| Market Size (2030) | USD 893.26 Million |

| Growth Rate (2025 - 2030) | 5.97% CAGR |

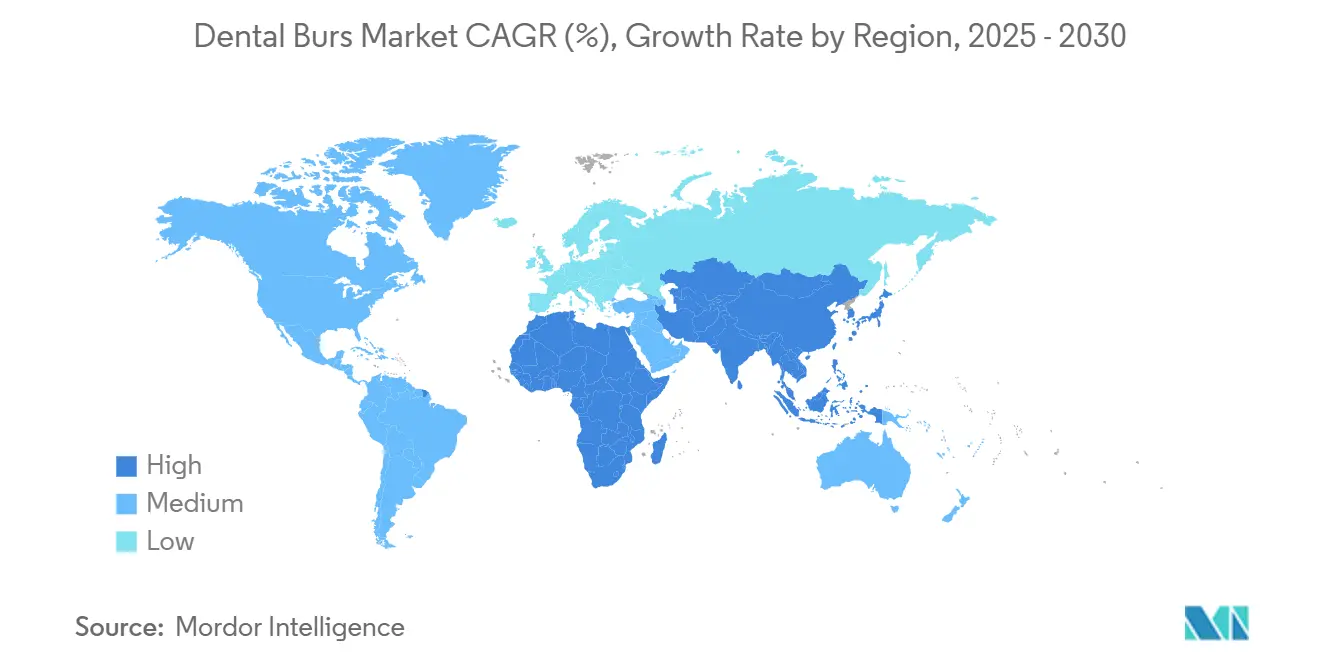

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Burs Market Analysis by Mordor Intelligence

The dental burs market size stood at USD 668.32 million in 2025 and is projected to climb to USD 893.26 million by 2030, reflecting a 5.97% CAGR over the forecast period. The upward curve mirrors three converging forces: a large unmet treatment need, rapid material-science innovation, and widening access to chair-side digital workflows. Rapid population aging in high-income countries, alongside sugar-rich diets in emerging economies, sustains a broad restorative workload that keeps high-speed diamond and carbide instruments in daily rotation. Technology upgrades—particularly multi-layer diamond coatings that extend cutting efficiency—allow clinics to lower per-procedure costs despite premium price points. At the same time, the Healthy China 2030 mandate and similar policies in India are turning Asia-Pacific into an equipment manufacturing hub, realigning supply chains and shortening replenishment lead times. Lastly, cosmetic dentistry’s rise as an elective service, supported by social-media-driven aesthetic norms, is steering innovation toward ultra-fine finishing burs and single-patient sterile packs that cut chair-time while ensuring compliance with tighter infection-control rules.[1]World Health Organization, “Oral Health,” WHO.INT

Key Report Takeaways

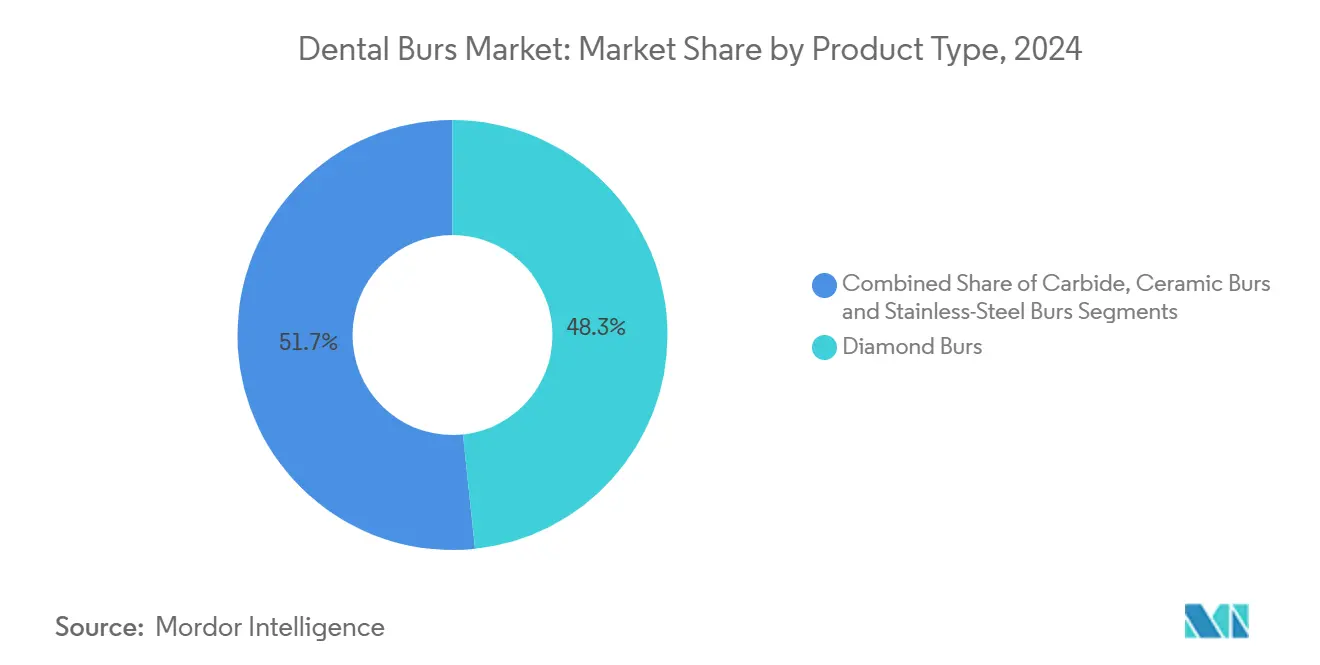

- By product type, diamond burs led with 48.33% of dental burs market share in 2024, while ceramic burs are pacing fastest at a 9.23% CAGR through 2030.

- By shape, round heads accounted for 28.34% of the dental burs market size in 2024, yet flame designs are advancing at an 8.36% CAGR.

- By speed class, high-speed instruments held 66.38% share in 2024; low-speed variants are the growth engine at a 9.12% CAGR.

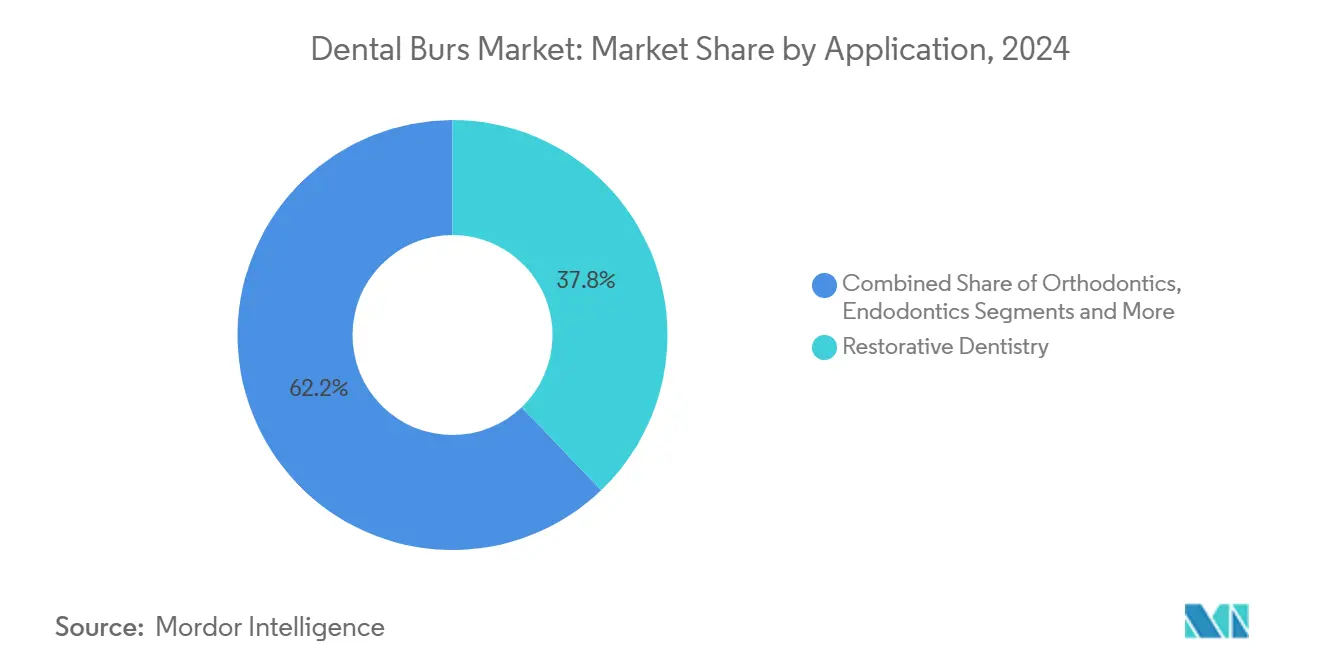

- By application, restorative dentistry retained 37.84% share in 2024 and cosmetic procedures are expanding at an 8.79% CAGR.

- By end-user, dental clinics commanded 57.89% share in 2024, whereas academic institutions show 7.33% CAGR momentum.

- By geography, North America dominated with 33.36% share in 2024, but Asia-Pacific leads the growth table at a 7.62% CAGR.

Global Dental Burs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging prevalence of dental caries & restorative procedures | +1.8% | Global, higher in APAC & MEA | Long term (≥ 4 years) |

| Rising demand for cosmetic dentistry | +1.2% | North America & EU core, APAC urban spill-over | Medium term (2-4 years) |

| Expansion of dental clinics in emerging markets | +1.0% | APAC core (India, China, Southeast Asia) | Medium term (2-4 years) |

| Technological advances in multi-layer diamond coatings | +0.8% | North America & EU manufacturing hubs | Long term (≥ 4 years) |

| Adoption of minimally invasive micro-burs for conservative prep | +0.6% | North America & EU, expanding APAC premium segments | Short term (≤ 2 years) |

| Chair-side CAD/CAM driving need for custom finishing burs | +0.4% | North America & EU, selective APAC uptake | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Prevalence of Dental Caries & Restorative Procedures

Global incidence of permanent-tooth caries is expected to reach 30,414 per 100,000 population by 2030, up from 28,154 in 1990. The burden is shifting toward adults aged 25-70, widening the restorative workload beyond pediatric cases. Lower socio-demographic index regions bear the greatest risk as limited fluoride exposure and inexpensive sugary snacks accelerate lesion progression. Clinical follow-up studies show that 69.2% of resin-composite restorations in primary teeth remain intact, yet secondary lesions often require revision using specialized cutting instruments.[2]Fangfei Zhang, “Clinical Outcomes of Direct Resin-Composite Restorations in Primary Maxillary Incisors,” DOI.ORGThis repeat-intervention cycle drives steady demand for diamond, carbide, and emerging ceramic burs optimized for mature enamel and deep-cavity geometries. Manufacturers respond by tailoring edge profiles and particle sizes to reduce heat and micro-fractures, thereby improving patient comfort and restoration longevity.

Rising Demand for Cosmetic Dentistry

Cosmetic procedures are tracking an 8.79% CAGR through 2030, outpacing all other clinical applications. Heightened aesthetic awareness among younger adults and higher discretionary income in North America and Western Europe have made enamel recontouring, veneer placement, and in-office whitening central to practice growth.[3]Olivia Lili Zhang, “Advanced Lasers and Their Applications in Dentistry,” DOI.ORG Digital smile-design software exported from leading laboratories now integrates with intraoral scanners, pushing demand for ultra-fine finishing burs capable of replicating virtual contours with micron-level fidelity. Er:YAG and diode lasers offer minimally invasive enamel preparation, yet operators still rely on multi-layer diamond instruments for polishing because they deliver predictable surface gloss in fewer passes. A constrained insurance reimbursement landscape favors premium burs that shorten appointment times, easing the overall cost burden on patients while preserving profitability for clinics.

Expansion of Dental Clinics in Emerging Markets

Rapid urbanization is widening the geographic footprint of private clinics across China, India, and Southeast Asia. In China’s megacities, urban residents are 1.57 times more likely to visit a dentist than rural peers. However, 30.4% of the population has never accessed professional care, underscoring pent-up demand. Healthy China 2030 explicitly calls for indigenous dental-equipment production, adding local competitors that challenge imported brands on price and service reach. In India, ratios range from 1 dentist:9,000 urban dwellers to 1:200,000 in rural districts, and only 5% of citizens can afford premium services. These gaps stimulate sales of rugged, cost-efficient carbide and stainless-steel burs capable of extended use in resource-strained settings, while premium diamond tools find an audience in tier-one cities.

Technological Advances in Multi-Layer Diamond Coatings

Composite diamond coatings now deliver 1.69 times longer service life than single-layer films, thanks to tighter adhesion and reduced particle pull-out. Arc-ion plating lets engineers fine-tune grain structure, giving burs higher hardness without sacrificing flexibility. Some researchers are experimenting with cerium-oxide nanoparticle additives that lower oxidative stress in adjacent tissues, hinting at future biocompatibility gains. Clinics adopting these tools report fewer bur changes per procedure, trimming consumable spend even as unit costs rise. Competitors, however, quickly standardize manufacturing methods, compressing the window for premium pricing and forcing continuous R&D investment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of premium diamond & ceramic burs | -0.9% | Global, stronger in emerging markets | Medium term (2-4 years) |

| Stringent sterilization / reuse regulations | -0.6% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Limited reimbursement for elective dental procedures | -0.5% | North America & EU, selective APAC impact | Long term (≥ 4 years) |

| Shift toward laser & ultrasonic cutting alternatives | -0.4% | North America & EU, gradual APAC uptake | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Premium Diamond & Ceramic Burs

Multi-layer coating processes and advanced ceramic sintering push manufacturing costs well above traditional tungsten-carbide levels. For high-volume community clinics in India or Brazil, the premium can erode operating margins when daily patient flow already tests chair capacity. Supply-chain volatility for industrial diamonds and rare-earth ceramic additives further complicates budgeting as spot prices swing sharply. To reach emerging-market practitioners, suppliers are trialing mid-tier SKUs that retain upgraded wear resistance while trimming accessory features such as color-coding or single-patient blister packs.

Stringent Sterilization / Reuse Regulations

CDC rules issued in 2024 stipulate heat sterilization for every critical rotary instrument between patients, imposing extra autoclave cycles that dull edges and weaken bonding layers. The FDA classifies dental burs as Class I devices, so any design tweak—such as grit change—requires premarket notification filings that add months to launch timelines. Clinics without on-site washer-disinfectors face higher labor costs or must switch to single-use burs, raising consumable spend and pressuring budgets, especially where insurance does not reimburse instrument overhead.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Diamond Dominance Faces Ceramic Challenge

Diamond burs commanded 48.33% of global revenue in 2024, reflecting their entrenched role in high-speed enamel preparation and polishing tasks. Ceramic burs, though smaller in absolute terms, are expanding at a 9.23% CAGR because they generate less heat and exhibit superior biocompatibility, reducing the risk of pulpal irritation during deep cavity work. The dental burs market continues to bifurcate: volume-driven general practices lean on cost-efficient carbide tools, while esthetic-focused clinics invest in premium multi-layer diamonds and zirconia-infused ceramics.

Manufacturers defending the diamond franchise are layering advanced coatings that extend lifespan by up to 70%, slowing the replacement cycle yet locking customers into branded systems. Ceramic innovators counter with nanoparticle reinforcement that elevates hardness without sacrificing fracture toughness. As both technologies converge on performance, purchase decisions hinge on per-procedure economics, sterilization durability, and supplier service levels.

By Shape/Head Design: Round Shapes Lead Conservative Trends

Round heads held 28.34% share in 2024 because they remain indispensable for initial caries excavation. Flame forms, however, are rising fastest at 8.36% CAGR, mirroring the profession’s shift toward minimally invasive access designs that spare healthy dentin. Conservative cavity outlines reduce postoperative sensitivity and prolong restoration life, but they require operators to steer slender flames along complex contours.

Pear and cylinder shapes sustain niche roles in crown preparation and parallel wall finishing, whereas wheel profiles handle labial reduction for veneer work. Polymer-based Smart Prep burs and chemomechanical gels compete for selective dentin removal, yet longer chair-time hampers widespread changeover from rotary instruments. The dental burs market sees steady SKU proliferation as suppliers bundle assorted shapes into procedural kits aligned with evidence-based preparation protocols.

By Speed Class: Low-Speed Innovation Accelerates

High-speed handpieces spinning above 200,000 rpm still account for 66.38% of use cases because they deliver swift enamel removal and efficient gross reduction. Yet the low-speed segment is gaining ground at 9.12% CAGR, powered by a growing emphasis on precision finishing, heat mitigation, and patient comfort. Clinics performing extended cosmetic sessions frequently downshift to 10,000–40,000 rpm ranges to avoid thermal stress on ceramics and soft tissue.

Ultrasonic and laser alternatives hover at the premium fringe; their adoption reinforces, rather than replaces, low-speed rotary finishing where tactile feedback remains critical. Handpiece makers are rolling out dual-drive systems with torque-tracking sensors, letting clinicians toggle between speed modes mid-procedure. This fluid workflow integration underpins the dental burs market’s ongoing transition toward modular instrumentation.

By Application: Cosmetic Procedures Drive Premium Demand

Restorative dentistry remained the core at 37.84% share in 2024, anchored by the global caries burden. Cosmetic procedures, though smaller, are charting an 8.79% CAGR and influencing product design priorities. Surface-polish consistency, shade-matching capabilities, and minimal chair-time are top selection criteria for burs targeting veneer margins, enameloplasty, and contouring.

Integrating digital smile-design outputs with rotary finishing places new emphasis on grit uniformity and color-coded sequence kits that streamline clinician workflow. Meanwhile, orthodontic debonding and implantology require specific head geometries and cutting angles, widening the dental burs market portfolio without eroding the primacy of restorative and cosmetic segments.

By End-User: Academic Institutions Pioneer Innovation

Dental clinics controlled 57.89% share in 2024 due to their sheer volume of routine care, but academic and research centers are logging a 7.33% CAGR as they expand postgraduate training and translational studies. Universities act as early adopters for nanoparticle coatings, single-patient sterile packs, and CAD/CAM-integrated workflow kits, giving suppliers real-world feedback before commercial rollout.

Hospital oral-surgery departments rely on sterile packaging and extended shelf life, accepting higher ASPs in exchange for traceability. Mobile and teledentistry units show nascent demand for compact, disposable burs that minimize cross-contamination risk in remote settings. Collectively, these trends nudge the dental burs market toward segmented SKUs tailored to distinct clinical environments.

Geography Analysis

North America retained a 33.36% share in 2024, buoyed by widespread insurance coverage for restorative care, high per-capita dental spending, and early adoption of advanced handpieces. Growth is steady but slower than in emerging territories because replacement purchases dominate; nevertheless, regulatory scrutiny under FDA Part 872 elevates compliance costs, reinforcing barriers to entry for newcomers.

Asia-Pacific is the expansion hotspot, delivering a 7.62% CAGR as public-health programs and rising incomes unlock pent-up demand. China’s Healthy China 2030 blueprint channels subsidies toward domestic manufacturing, shortening lead times and reducing exchange-rate risk for local buyers. India mirrors the trajectory with “Make-in-India” incentives, though urban-rural disparities mean cost-effective carbide burs still outsell premium diamonds outside metro areas. Japan and South Korea lean toward high-tech ceramics and micro-grain diamonds, aligning procurement with quality-of-life consumer expectations.

Europe offers balanced conditions: universal healthcare drives routine restorative volume, and sustainability mandates push suppliers to adopt recyclable blister packs. Currency swings post-Brexit complicate cross-border trade, yet high practitioner density in Germany, France, and Italy ensures stable replacement sales. Middle East and Africa are smaller but fast-opening due to private-equity-backed clinic chains in the Gulf Cooperation Council and public investments in North African training centers. South America remains price-sensitive; Brazil and Argentina generate most demand, though import duties and exchange-rate volatility dominate procurement planning.

Competitive Landscape

The dental burs market is moderately concentrated: established multinationals leverage strong branding, patent portfolios, and direct distribution. Dentsply Sirona posted USD 951 million in Q3 2024 sales, inching up 0.5% year-on-year despite macro headwinds. Envista Holdings saw Q2 2024 revenue dip 3.2% to USD 633.1 million, underscoring competitive intensity and variable procedure volumes.

Product differentiation revolves around coating durability, single-patient sterility, and integration with digital treatment plans. Recent patent filings cover gradient diamond particle layering and antimicrobial surface treatments, aiming to cut sterilization cycles and extend life. Market entrants from China and India are scaling carbide manufacturing for domestic supply, eroding price points in lower-tier segments while premium Western brands defend margins through continual R&D and procedural training programs.

Strategic collaborations are rising: coating specialists partner with handpiece makers to co-develop torque-matched burs, while dental-software vendors bundle finishing kits with CAD/CAM mills to lock customers into end-to-end ecosystems. White-space opportunities lie in disposable burs for field dentistry and antimicrobial-infused instruments for immunocompromised patient workflows, reflecting evolving infection-control priorities.

Dental Burs Industry Leaders

Prima Dental Group

Dentsply Sirona

Envista Holdings

MANI, Inc.

Gebr. Brasseler GmbH & Co KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Komet introduced Rocky, a crown-cutting diamond bur designed to improve operator control during complex extractions.

- March 2025: Abrasive Technology’s Prodia Dental launched Prodia Sport, a single-patient diamond engineered for high-speed efficiency.

- February 2024: Kerr Dental rolled out SimpliCut, a pre-sterilized single-use diamond bur line aimed at eliminating reprocessing time.

Global Dental Burs Market Report Scope

| Diamond Burs |

| Carbide Burs |

| Ceramic Burs |

| Stainless-Steel Burs |

| Round |

| Pear |

| Cylinder |

| Flame |

| Wheel & Others |

| High-speed Burs |

| Low-/Slow-speed Burs |

| Restorative Dentistry |

| Orthodontics |

| Endodontics |

| Oral Surgery & Implantology |

| Cosmetic / Esthetic Procedures |

| Dental Clinics |

| Hospitals |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Diamond Burs | |

| Carbide Burs | ||

| Ceramic Burs | ||

| Stainless-Steel Burs | ||

| By Shape/Head Design | Round | |

| Pear | ||

| Cylinder | ||

| Flame | ||

| Wheel & Others | ||

| By Speed Class | High-speed Burs | |

| Low-/Slow-speed Burs | ||

| By Application | Restorative Dentistry | |

| Orthodontics | ||

| Endodontics | ||

| Oral Surgery & Implantology | ||

| Cosmetic / Esthetic Procedures | ||

| By End-User | Dental Clinics | |

| Hospitals | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the dental burs market by 2030?

The sector is forecast to reach USD 893.26 million by 2030, expanding at a 5.97% CAGR from its 2025 base.

Which product type currently leads global sales?

Diamond burs hold the top position, capturing 48.33% of revenue in 2024.

Which geographic region is growing fastest in dental bur demand?

Asia-Pacific is advancing at a 7.62% CAGR, fueled by clinic expansion and supportive health-policy initiatives.

Why are ceramic burs gaining traction?

They cut with lower heat generation, enhance biocompatibility, and are registering the highest product-level CAGR at 9.23%.

How do sterilization rules influence purchasing decisions?

Mandatory heat-sterilization cycles shorten bur lifespan, prompting many practices to adopt single-use or longer-wear premium options.

What is the primary growth driver behind low-speed bur demand?

The shift toward conservative preparation techniques and precision finishing is lifting low-speed sales at a 9.12% CAGR.

Page last updated on: