Organic Personal Care And Cosmetic Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

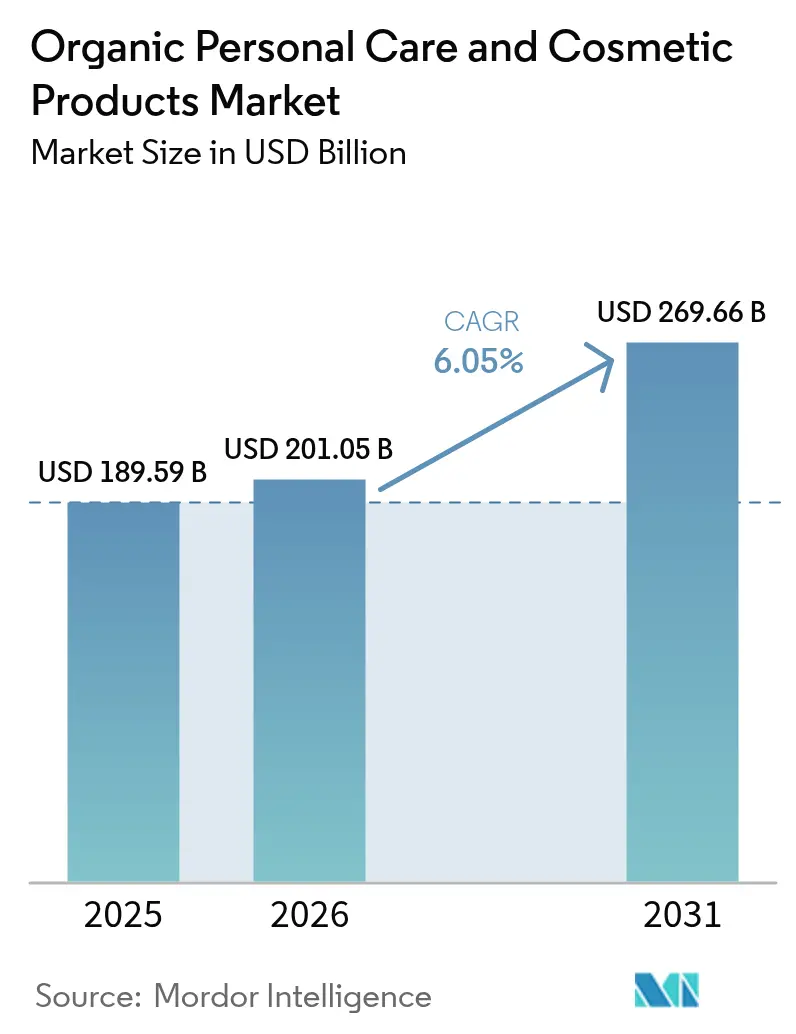

| Market Size (2026) | USD 201.05 Billion |

| Market Size (2031) | USD 269.66 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

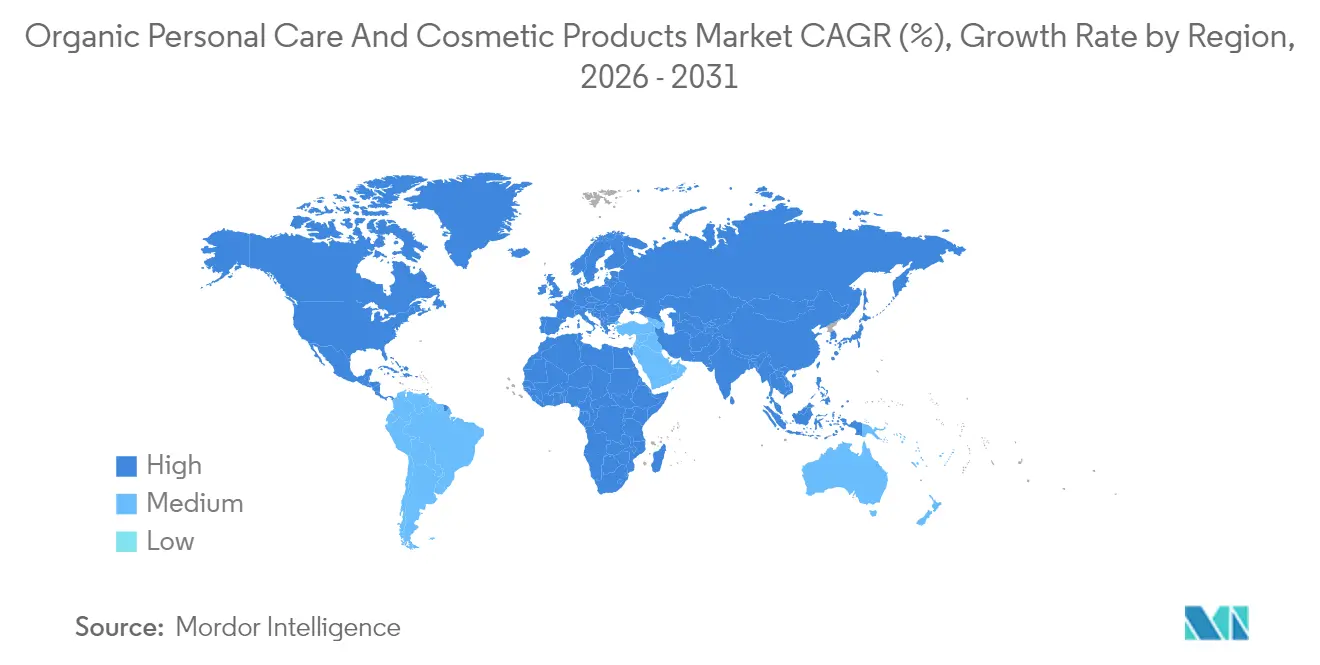

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

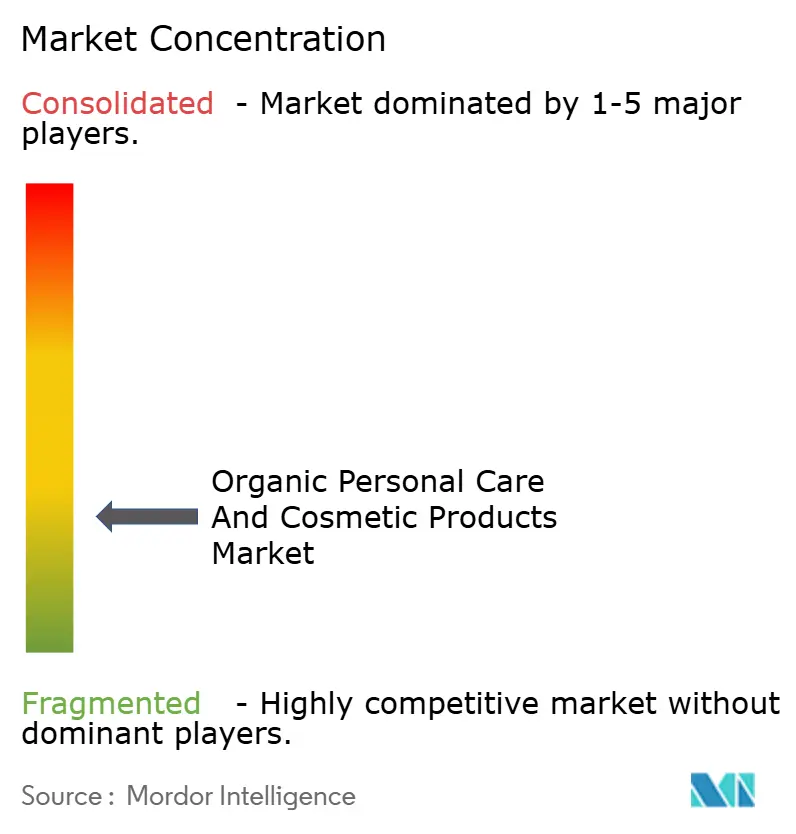

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Organic Personal Care And Cosmetic Products Market Analysis by Mordor Intelligence

The organic personal care and cosmetic products market size is expected to grow from USD 189.59 billion in 2025 to USD 201.05 billion in 2026 and is forecast to reach USD 269.66 billion by 2031 at 6.05% CAGR over 2026-2031. Purchasers gravitate toward formulations that are free from controversial synthetics, and regulators intensify disclosure rules that favor brands with verified organic sourcing. Asia-Pacific leads both scale and speed, helped by China’s 2025 rules that shorten approval times for natural ingredients and by India’s long-standing animal-testing ban. In mature regions, extra scrutiny on nanomaterials in the EU and state-level chemical bans in the United States open doors for compliant organic players while slowing conventional rivals. Digital channels raise transparency standards by letting firms show certification proofs and full ingredient lists, bolstering trust and conversion. The market’s low concentration score fosters steady entry by niche innovators that capitalize on sustainability gaps left by global incumbents.

Key Report Takeaways

- By product type, personal care products held 90.94% of the organic personal care and cosmetic products market share in 2025, while cosmetics and makeup products are projected to grow at a 6.62% CAGR from 2026 to 2031.

- By category, mass products accounted for 61.10% of the organic personal care and cosmetic products market size in 2025, whereas premium products are expected to expand at a 6.85% CAGR through 2031.

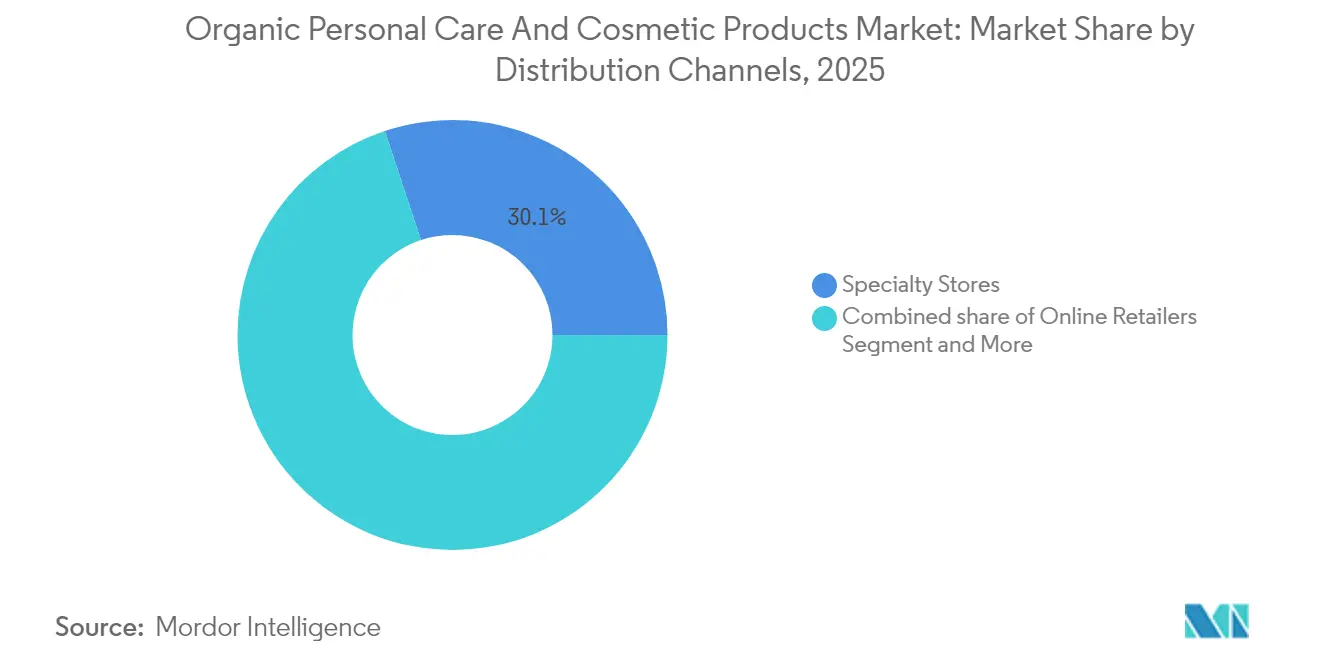

- By distribution channel, specialty stores led with 30.10% revenue share in 2025; online retail is forecast to register the highest 7.21% CAGR between 2026 and 2031.

- By geography, Asia-Pacific commanded 32.10% of the organic personal care and cosmetic products market in 2025 and is set to advance at a 7.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Organic Personal Care And Cosmetic Products Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inclination towards clean-label products | +1.2% | Global, with the strongest uptake in North America and Europe | Medium term (2-4 years) |

| Rising demand for herbal personal care products | +0.9% | Asia-Pacific core, spill-over to Middle East and Africa and Latin America | Long term (≥ 4 years) |

| Awareness of vegan and cruelty-free beauty products | +0.8% | Global, led by North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Growing concerns over the effects of synthetic products | +0.7% | Global, with accelerated adoption in developed markets | Medium term (2-4 years) |

| Supportive government regulations and certifications | +0.6% | North America and Europe primarily, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Environmental sustainability and ethical consumerism | +0.5% | Global, with premium market concentration in developed regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Inclination towards clean-label products

Consumer demand for transparency in beauty formulations has evolved beyond marketing preference to become a fundamental purchasing criterion, particularly among Millennial and Generation Z demographics who prioritize ingredient safety and environmental impact. The absence of government-defined "clean beauty" standards has created market opportunities for brands that proactively adopt stringent self-regulation, with retailers and influencers filling the definitional void through their criteria. This regulatory gap enables organic brands to establish competitive differentiation through third-party certifications like United States Department of Agriculture Organic, which requires 95% organic ingredients, and COSMOS certification, which sets standards for natural and organic cosmetics under the European Union Green Claims Directive, according to the Provenance Organization data[1]Provenance, “Understanding COSMOS and USDA Organic,” provenance.org. The clean label trend particularly benefits smaller organic brands that can achieve faster formulation pivots compared to multinational corporations constrained by legacy product portfolios and global regulatory compliance requirements.

Rising demand for herbal personal care products

European herbal medicinal products, operating under the EU Directive 2004/24/EC framework, this regulatory framework offers three distinct pathways for herbal products: full marketing authorization, Well-Established Use (WEU), and Traditional Herbal Medicinal Products (THMP). These pathways not only ensure compliance with safety and efficacy standards but also present beauty brands with a chance to capitalize on documented efficacy claims, thereby enhancing consumer trust and market penetration. The growing demand for herbal beauty formulations is driven by increasing consumer awareness of natural and sustainable products, coupled with the rising preference for plant-based ingredients in personal care. Notably, Germany stands out as the top importer of medicinal plants, suggesting a concentrated supply chain that could sway pricing and availability of herbal beauty formulations throughout the region. This concentration highlights the importance of supply chain management and strategic sourcing for beauty brands aiming to maintain competitive pricing and consistent product availability. Meanwhile, the integration of traditional medicine into contemporary beauty products has shifted from mere cultural inclination to a scientifically endorsed strategy.

Awareness of vegan and cruelty-free beauty products

The convergence of ethical consumption and regulatory enforcement has transformed vegan and cruelty-free positioning from niche marketing to mainstream expectation. The regulatory precedent influences global brand strategies, as companies developing for the Indian market must inherently adopt cruelty-free formulations, creating spillover effects for their international product lines. The vegan beauty segment benefits from technological advances in plant-based alternatives to traditional animal-derived ingredients like lanolin and carmine, with innovations in fermentation-derived actives enabling performance parity with conventional formulations. Consumer research indicates that younger demographics view cruelty-free certification as a baseline requirement rather than a premium feature, suggesting that brands without these credentials face increasing market access barriers rather than simply missing growth opportunities.

Supportive government regulations and certifications

Regulatory frameworks are increasingly favoring organic and natural formulations. This shift is driven by both positive incentives and restrictive measures targeting synthetic ingredients, creating a dual-pressure environment that accelerates the adoption of organic products. The EU's 2025 ban on certain nanomaterials and substances, including 4-Methylbenzylidene Camphor and Retinol, offers a compliance edge to brands already pivoting towards organic alternatives. This regulatory move aligns with the broader consumer demand for safer and environmentally friendly products, encouraging manufacturers to innovate and invest in organic formulations. Meanwhile, China's provisions in February 2025, which bolster cosmetic ingredient innovation, are fine-tuning technical requirements to favor natural ingredients. These provisions also advocate for the concurrent submission of new ingredients and products, streamlining the path to market for organic formulations. By reducing time-to-market, these measures provide a competitive advantage to companies focusing on natural and organic products, further driving growth in this segment.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong presence of counterfeit products | -0.8% | Global, with highest impact in Europe and emerging markets | Short term (≤ 2 years) |

| Higher cost of organic products | -0.6% | Global, with pronounced effects in price-sensitive markets | Medium term (2-4 years) |

| Limited awareness in developing countries | -0.4% | Emerging markets in Asia-Pacific, Middle East and Africa, and Latin America | Long term (≥ 4 years) |

| Challenges in raw material sourcing | -0.3% | Global, with supply chain concentration in specific regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong presence of counterfeit products

Counterfeit organic beauty products undermine market development by eroding consumer trust and creating unfair price competition, with the Europe Union cosmetics market losing approximately USD 3.51 billion annually to fraudulent products, representing 4.8% of legitimate sales and nearly 32,000 lost jobs, according to EUPIO data[2]EUIPO, “The Economic Cost of IPR Infringement in the Cosmetics Sector,” euipo.europa.eu. The French cosmetics industry suffers the highest impact in annual lost sales, indicating that premium organic brands face disproportionate counterfeiting risks due to their higher margins and brand equity. Counterfeit organic products often contain prohibited synthetic ingredients while claiming natural credentials, creating safety risks that damage the entire organic category's reputation when adverse events occur. The complexity of organic supply chains, particularly for exotic botanical ingredients, creates authentication challenges that counterfeiters exploit through sophisticated packaging and documentation fraud.

Higher cost of organic products

Premium pricing for organic beauty products stems from higher raw material costs, complex certification processes, and smaller production scales, creating market access barriers, particularly in price-sensitive segments and developing economies. Organic ingredient sourcing requires adherence to strict agricultural standards, third-party certification, and often involves smaller suppliers with limited economies of scale, resulting in ingredient costs that can be higher than conventional alternatives. The certification process itself adds costs through required documentation, testing, and ongoing compliance monitoring, with USDA Organic certification requiring annual inspections and detailed record-keeping that smaller brands may struggle to afford. Mass market penetration remains limited as organic brands compete against established conventional products with decades of manufacturing optimization and supply chain efficiency, creating a premium positioning that may limit broader market adoption despite growing consumer interest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Product Type: Personal Care Dominates While Cosmetics Accelerate

Personal care dominates with a 90.94% market share in 2025, reflecting its established position in the natural and organic beauty market. The cosmetics segment is growing at a 6.62% CAGR, as consumers increasingly integrate skin care elements into their makeup routines, seeking products that offer both cosmetic and therapeutic benefits. Sky Organics' April 2025 launch of certified organic hair oil and butter demonstrates the ongoing innovation in hair care, where brands combine traditional oil-based formulations with silicone-free alternatives to meet clean-label demands while maintaining product performance. Hair care leads personal care growth through innovations in sulfate-free shampoos and plant-based conditioning agents, while skin care leverages botanical actives and fermentation-derived ingredients that deliver clinical-grade results without synthetic additives.

The cosmetics segment's accelerated growth stems from technological breakthroughs in natural colorants and sustainable packaging that enable performance parity with conventional makeup products. Oral care represents an emerging opportunity within personal care, driven by consumer awareness of ingredient absorption through oral tissues and regulatory pressure on fluoride alternatives. Men's grooming products experience notable expansion as male consumers increasingly prioritize ingredient transparency and environmental responsibility in their personal care routines. Bath and shower products benefit from the premiumization trend, where consumers view organic formulations as spa-like experiences that justify higher price points compared to conventional alternatives.

By Category: Premium Segment Accelerates Despite Mass Market Dominance

Mass products maintain 61.10% market share in 2025, yet premium products achieve faster growth at 6.85% CAGR through 2031, indicating a market bifurcation where organic brands can succeed through either accessibility or exclusivity strategies. This growth differential reflects premium brands' ability to command higher margins while investing in advanced organic formulations, sustainable packaging, and direct-to-consumer marketing that builds brand loyalty among environmentally conscious consumers. Mass market organic products face intense price competition and must achieve economies of scale through simplified formulations and efficient distribution partnerships with major retailers.

Premium organic brands leverage their higher price points to invest in cutting-edge natural ingredients like adaptogenic botanicals, marine-derived actives, and biotechnology-produced compounds that deliver superior performance compared to basic organic formulations. The premium segment also benefits from regulatory advantages, as luxury consumers often prioritize safety and environmental credentials over price considerations, making them early adopters of products that exceed regulatory requirements. Mass market success requires different strategies, including partnerships with established retailers, simplified ingredient profiles that reduce costs, and marketing focused on essential benefits rather than exotic ingredients. The category dynamics suggest that organic brands must choose clear positioning strategies rather than attempting to serve both segments simultaneously.

By Distribution Channel: Digital Transformation Reshapes Retail Landscape

Specialty stores maintain 30.10% market share in 2025, providing essential credibility and education for organic beauty products, while online retail channels achieve the fastest growth at 7.21% CAGR through 2031, reflecting fundamental shifts in consumer shopping behavior and brand communication strategies. This channel evolution enables organic brands to bypass traditional retail gatekeepers and communicate their sustainability credentials directly to consumers through detailed product information, ingredient transparency, and brand storytelling that specialty stores cannot match at scale. Supermarkets and hypermarkets serve as crucial accessibility channels for mass market organic products, though their growth lags behind digital channels due to limited shelf space and price-focused consumer behavior.

Online retail's growth acceleration stems from its ability to serve niche organic brands that cannot achieve sufficient scale for traditional retail distribution, while also enabling established brands to test new products and gather consumer feedback without major retail commitments. The digital channel particularly benefits organic brands through subscription models, personalized recommendations based on ingredient preferences, and direct customer relationships that reduce dependence on retail intermediaries. Other channels, including direct-to-consumer showrooms and pop-up retail experiences, represent emerging opportunities for organic brands to create immersive brand experiences that justify premium pricing and build customer loyalty beyond traditional transactional relationships.

Geography Analysis

Asia-Pacific dominates with 32.10% market share in 2025 while simultaneously achieving the fastest regional growth at 7.55% CAGR through 2031, driven by regulatory innovations like China's February 2025 provisions supporting cosmetic ingredient innovation and India's established ban on animal testing that creates competitive advantages for organic brands. China's streamlined approval processes for natural ingredients, combined with simultaneous submission protocols for new ingredients and products, reduce time-to-market for organic formulations while maintaining safety standards. Japan and Australia contribute to regional growth through premium organic positioning and strict quality standards that align with consumer preferences for authentic, high-performance natural products.

Europe represents a mature yet evolving market where regulatory frameworks like the EU Green Claims Directive and COSMOS certification create competitive advantages for compliant organic brands while establishing barriers for conventional players lacking sustainability credentials. The region's focus on environmental sustainability, evidenced by France's ban on 'biodegradable' claims without substantiation and the EU's prohibition of specific nanomaterials from 2025, positions organic brands as regulatory-compliant alternatives to conventional formulations. Germany leads European demand for natural ingredients, particularly medicinal plants, while the UK, France, Italy, and Spain drive premium organic adoption through sophisticated consumer bases that prioritize ingredient transparency and environmental responsibility.

North America experiences steady growth driven by state-level regulations that create compliance advantages for organic brands, including Washington State's Toxic-Free Cosmetics Act, effective January 2025 and similar legislation in California, Colorado, and Minnesota banning PFAS and other synthetic chemicals in cosmetics. The United States leads regional adoption through consumer awareness campaigns and regulatory uncertainty around MoCRA implementation that benefits brands already formulating without controversial ingredients. Canada and Mexico contribute through cross-border trade facilitation and growing consumer sophistication regarding ingredient safety and environmental impact. South America, Middle East and Africa represent emerging opportunities where organic brands can establish early market positions as consumer awareness and regulatory frameworks develop, particularly in Brazil's established natural beauty culture and South Africa's indigenous botanical heritage.

Competitive Landscape

The organic beauty and personal care products market exhibits fragmented, creating opportunities for both established multinational corporations and specialized organic brands to compete through differentiated strategies rather than scale advantages alone. This fragmentation enables innovation-focused companies to achieve market success through superior formulations, sustainability credentials, and direct-to-consumer relationships, while established players leverage distribution networks and marketing resources to expand organic product lines. Strategic patterns reveal a bifurcation between companies pursuing organic acquisition strategies, like Weleda AG, continued expansion of natural brands, and those developing organic capabilities internally through dedicated R and D investments and supply chain partnerships.

Major players in the market include The Estée Lauder Companies Inc., The Hain Celestial Group Inc., Honasa Consumer Ltd., Natura and Co., and Eminence Organic Skin Care, among others. These players are expanding their market presence with the help of various strategies such as product launches, expansions, partnerships, and acquisitions. For instance, in June 2024, Sophyto launched a professional organic skincare range in the United Kingdom. The products include masks, moisturizers, and others.

White-space opportunities exist in developing markets where organic awareness remains limited, premium organic segments require advanced natural technologies, and regulatory-compliant formulations that anticipate future restrictions on synthetic ingredients. Emerging disruptors focus on biotechnology-derived ingredients, circular economy packaging solutions, and direct-to-consumer models that bypass traditional retail intermediaries while building authentic brand relationships with environmentally conscious consumers.

Organic Personal Care And Cosmetic Products Industry Leaders

The Estee Lauder Companies Inc.

The Hain Celestial Group Inc.

Natura & Co Holding SA

Honasa Consumer Ltd.

Eminence Organic Skin Care

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Organic skincare brand, Kora Organics, relaunched its products in India in partnership with Beautindia. The company offers a wide range of products, like Turmeric Glow Foaming Cleanser, Kakadu Plum Vitamin C Serum, Noni Glow Face Oil, Turmeric Brightening and Exfoliating Scrub + Mask, Active Algae Calming Cleansing Balm, and Milky Mushroom Gentle Cleansing Oil. The products are available on the Naykaa website.

- April 2025: Evolve Organic Beauty introduced commercial refill products in sustainable fiber bottles manufactured from PEFC-accredited and FSC-certified wood pulp. The company's packaging solution represents a significant advancement in sustainable packaging technology. These bottles are recyclable with standard household paper and cardboard waste, offering consumers an environmentally responsible option for their beauty products.

- September 2024: Indus Valley Organics launched a range of ready-to-use herbal hair care pastes. The hair care pastes are available in different formats. The products are available through various websites such as Amazon, Flipkart, Naykaa, Myntra, and others.

- May 2024: Eminence Organic Skin Care introduced a new skincare line featuring charcoal and black seed extract for skin purification. The product range includes a face oil, face mask, and gel. The formulation combines natural ingredients to cleanse and detoxify the skin while maintaining its moisture balance. These products aim to address various skin concerns, including excess oil, impurities, and uneven texture.

Global Organic Personal Care And Cosmetic Products Market Report Scope

The global organic personal care and cosmetic products market is segmented by product type, by category, by distribution channel, and by geography. By product type, the market studied is segmented into personal care products and cosmetic products. The personal care products segment is further segmented into hair care products, skincare products, bath and shower products, oral care products, men's grooming products, and deodorants and antiperspirants. Similarly, the cosmetic products segment is also further sub-segmented into facial cosmetics, eye cosmetic products, and lip and nail make-up products. The market is segmented by category into mass and premium products. By distribution channel, the market studied is segmented into specialist retail stores, supermarkets/hypermarkets, convenience stores, pharmacies/drug stores, online retail channel, and other distribution channels. The market is segmented by geography into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Personal Care Products | Hair Care | Shampoo |

| Conditioner | ||

| Hair Colourant | ||

| Hair Styling Products | ||

| Others | ||

| Skin Care | Facial Care Products | |

| Body Care Products | ||

| Lip and Nail Care Products | ||

| Bath and Shower | Shower Gels | |

| Soaps | ||

| Others | ||

| Oral Care | Toothbrush | |

| Toothpaste | ||

| Mouthwashes and Rinses | ||

| Others | ||

| Men’s Grooming Products | ||

| Deodorants and Antiperspirants | ||

| Perfumes and Fragrances | ||

| Cosmetics/Make-up Products | Facial Cosmetics | |

| Eye Cosmetics | ||

| Lip and Nail Make-up Products | ||

| Premium Products |

| Mass Products |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Personal Care Products | Hair Care | Shampoo |

| Conditioner | |||

| Hair Colourant | |||

| Hair Styling Products | |||

| Others | |||

| Skin Care | Facial Care Products | ||

| Body Care Products | |||

| Lip and Nail Care Products | |||

| Bath and Shower | Shower Gels | ||

| Soaps | |||

| Others | |||

| Oral Care | Toothbrush | ||

| Toothpaste | |||

| Mouthwashes and Rinses | |||

| Others | |||

| Men’s Grooming Products | |||

| Deodorants and Antiperspirants | |||

| Perfumes and Fragrances | |||

| Cosmetics/Make-up Products | Facial Cosmetics | ||

| Eye Cosmetics | |||

| Lip and Nail Make-up Products | |||

| By Category | Premium Products | ||

| Mass Products | |||

| By Distribution Channel | Specialty Stores | ||

| Supermarkets/Hypermarkets | |||

| Online Retail Stores | |||

| Other Channels | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Netherlands | |||

| Poland | |||

| Belgium | |||

| Sweden | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Indonesia | |||

| South Korea | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Chile | |||

| Peru | |||

| Rest of South America | |||

| Middle East and Africa | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

What is the current value of the organic beauty and personal care products market?

The market stands at USD 201.05 billion in 2026.

Which region leads the organic beauty and personal care products market?

Asia-Pacific leads with 32.10% revenue share and is on track for a 7.55% CAGR.

Which product segment grows the fastest?

Cosmetics and makeup products post the quickest pace at a 6.62% CAGR through 2031.

How do online channels influence market growth?

Online retail is forecast to record a 7.21% CAGR by enabling direct storytelling and certification proof.

Page last updated on: