Vegan Cosmetics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

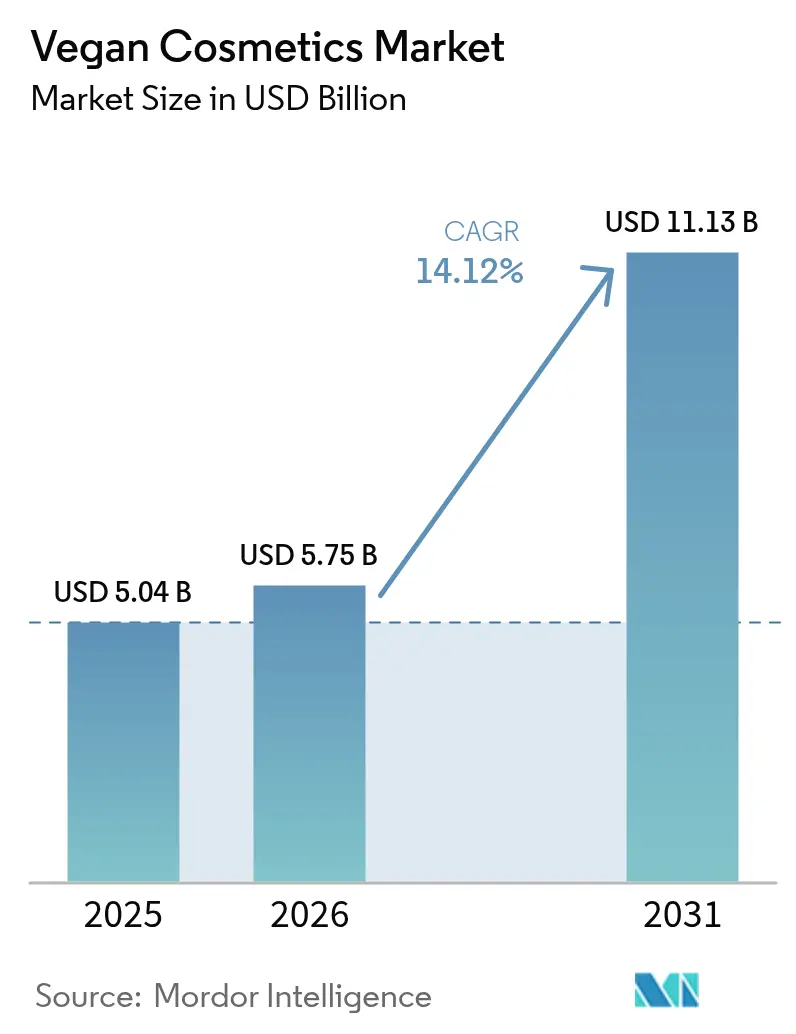

| Market Size (2026) | USD 5.75 Billion |

| Market Size (2031) | USD 11.13 Billion |

| Growth Rate (2026 - 2031) | 14.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vegan Cosmetics Market Analysis by Mordor Intelligence

The global vegan cosmetics market size in 2026 is estimated at USD 5.75 billion, growing from 2025 value of USD 5.04 billion with 2031 projections showing USD 11.13 billion, growing at 14.12% CAGR over 2026-2031. The market growth is driven by increasing consumer awareness of natural, chemical-free products and environmental sustainability. Vegan cosmetics exclude animal-derived ingredients, including beeswax, collagen, gelatin, milk, and others. Millennials and Gen Z consumers are the primary market drivers, showing a preference for products that avoid chemical-based ingredients and animal testing. In response, major cosmetic manufacturers are expanding their vegan product lines through new launches and acquisitions, while incorporating natural and organic ingredients to align with clean beauty preferences. The market is expected to maintain its growth trajectory, driven by increasing consumer awareness and favorable regulatory frameworks that support sustainable practices.

Key Report Takeaways

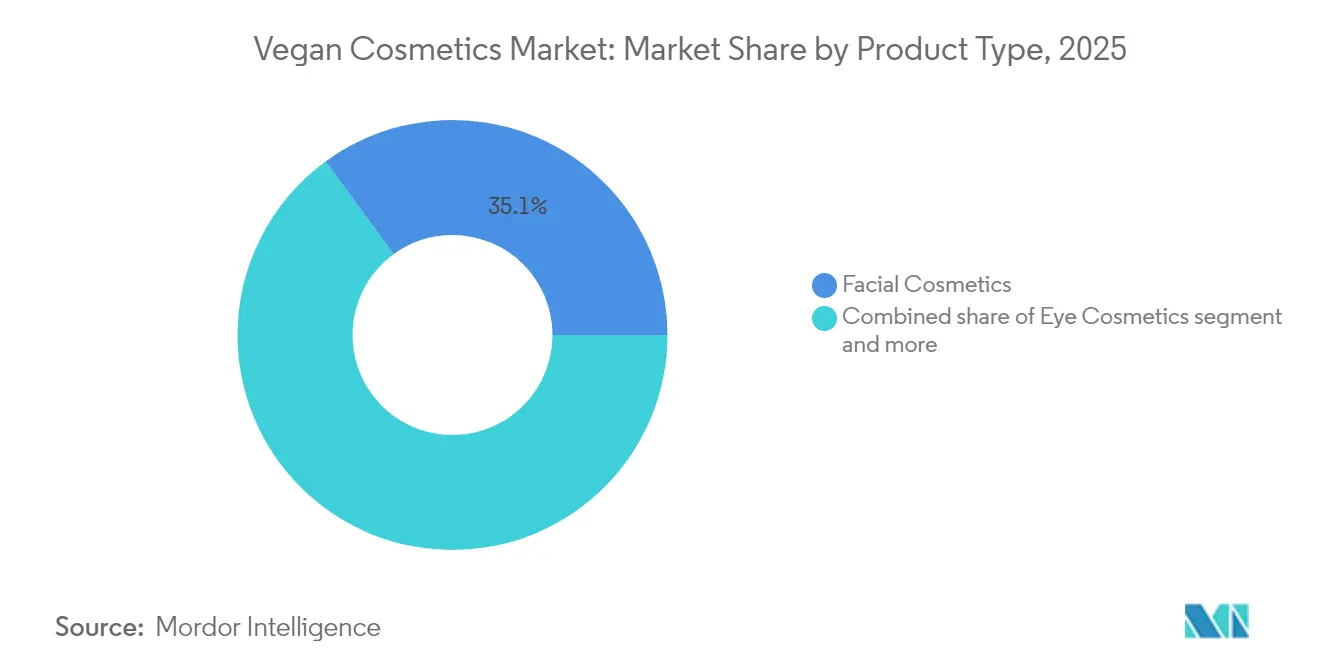

- By product type, facial cosmetics led with 35.05% of the vegan cosmetics market share in 2025; lip and nail make-up products are projected to expand at a 16.22% CAGR through 2031.

- By category, mass products held 55.10% of the vegan cosmetics market, while the premium products segment is poised for a 15.01% CAGR through 2031.

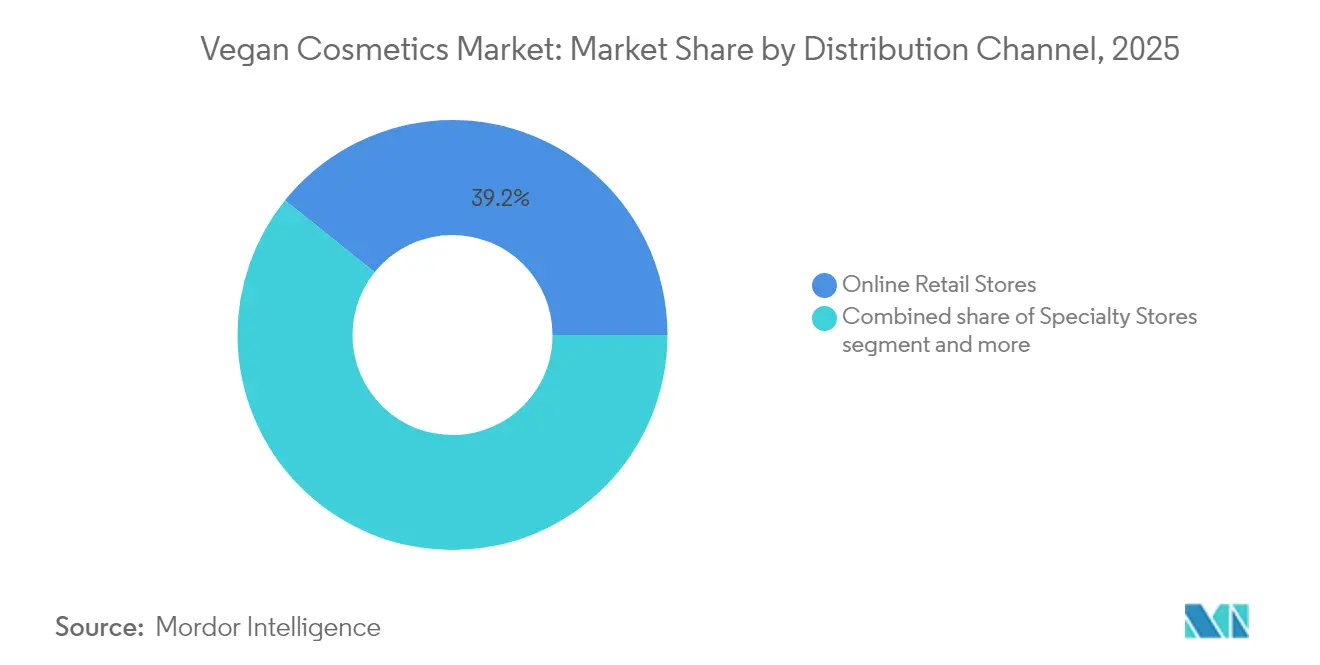

- By distribution channel, online retail stores commanded a 39.22% share of the vegan cosmetics market in 2025 and remain the fastest-growing segment at 17.45% CAGR through 2031.

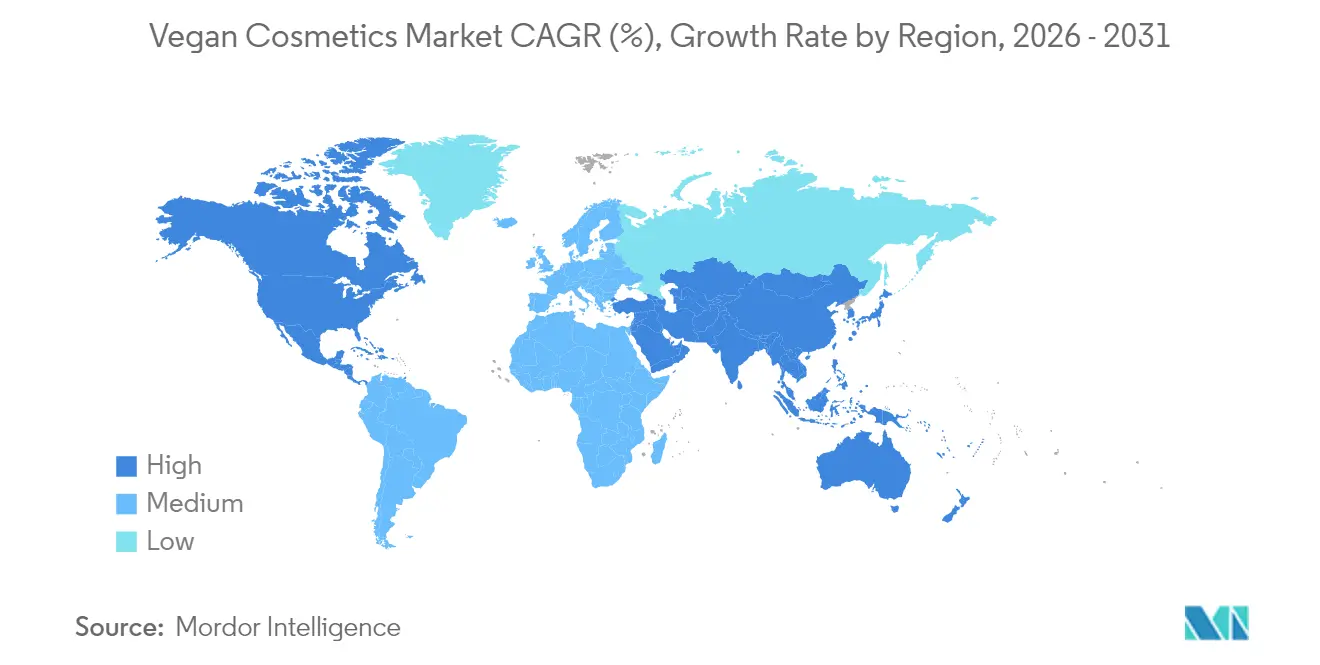

- By geography, Europe captured 41.10% of the market share in 2025, while Asia-Pacific is growing at a 21.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vegan Cosmetics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for cruelty-free products | +3.2% | Global, most pronounced in Europe and North America | Medium term (3-4 years) |

| Celebrity endorsements and influencer marketing power | +1.1% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Sustainability trends gaining traction | +2.5% | Global, with early Asia-Pacific/Western Europe | Long term (≥ 5 years) |

| Innovative botanical ingredients boost the market demand | +1.8% | Global, with Asia-Pacific and Europe leading | Medium term (3-4 years) |

| Rising consumer awareness of synthetic chemicals | +1.6% | Global, notably North America and Europe | Short term (≤ 2 years) |

| Increasing research and development investments for vegan alternatives | +1.3% | Global, innovation hubs (United States, Europe, Asia-Pacific) | Medium term (3-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Cruelty-Free Products

Consumer preferences in the vegan cosmetics market are evolving beyond ingredient selection to encompass the entire product development process. A Global Cosmetics Industry survey for 2025 indicates that 37% of consumers will prioritize "no animal testing" in their skincare product purchases, while 41% emphasize natural ingredients. In response to this consumer shift, major companies like Unilever are collaborating with European regulatory authorities to eliminate animal testing practices. The certification process for vegan cosmetics, managed by organizations such as BeVeg, implements rigorous verification procedures, including ingredient analysis, factory inspections, and testing validation. This market evolution is furthered by the use of ed by new product launches, such as singer SZA's Not Beauty vegan lip collection in April 2025, featuring three signature shades. The combination of increasing consumer demand, strict certification requirements, corporate commitments to sustainable practices, and celebrity-driven product launches continues to drive the expansion of the vegan cosmetics market.

Celebrity Endorsements and Influencer Marketing Power The Vegan Cosmetic Revolution

Celebrity-launched vegan cosmetics brands are transforming the market by accelerating consumer adoption and establishing a strong presence. The industry is witnessing an increase in consumer expectations for celebrities to demonstrate a genuine commitment to vegan principles, making transparent ingredient sourcing and formulation essential for maintaining brand credibility. Generation Z consumers have a significant influence on the vegan cosmetics market, as evidenced by their emphasis on peer recommendations and word-of-mouth validation. Moreover, a 2024 University of Portsmouth survey found that 60% of consumers trusted influencer recommendations, with nearly half of all purchasing decisions being influenced by these endorsements [1]Source: University of Portsmouth, “Influencer Impact on Consumer Skincare Choices,” port.ac.uk. Source: . The market continues to expand, driven by celebrity endorsements, the ethical product preferences of Generation Z, and growing environmental awareness among consumers.

Sustainability Trends Gaining Traction

Consumer expectations for vegan cosmetics have evolved beyond animal-free ingredients to encompass comprehensive sustainability practices. Companies are implementing environmental initiatives across their operations, as demonstrated by e.l.f. Cosmetics' Project Unicorn, which reduces packaging waste while maintaining vegan formulations. The market emphasizes sustainable packaging and responsible ingredient sourcing, reflecting the principles of a circular economy. This approach resonates particularly with younger consumers, who consistently opt for sustainable products and are willing to pay higher prices for environmentally responsible options. Recent market developments reflect this trend, as seen in October 2023, when Organic Harvest launched its 100% vegan organic makeup line featuring toxin-free and cruelty-free formulations. The combination of environmental awareness and demand for sustainable practices continues to drive market growth, benefiting companies that incorporate these values throughout their operations.

Innovative Botanical Ingredients Boost the Market Demand

Advances in botanical extraction and stabilization technologies are transforming the vegan cosmetics industry, enabling formulations that match the performance of conventional products. This technological progress is evident in developments such as Unilever's Hourglass brand, creating a vegan alternative to carmine red pigment, traditionally sourced from cochineal insects. The industry's collaborative approach is demonstrated by Unilever's decision to open-source this technology. Similarly, Givaudan Active Beauty's launch of the [N.A.S.]™ Vibrant Collection in October 2024 showcases the evolution of vegan botanical extracts, offering color stability and longevity in hybrid makeup products. The integration of biotechnology facilitates the production of nature-identical compounds, which provide consistent performance while avoiding the supply chain vulnerabilities typically associated with plant-derived ingredients. These technological capabilities, combined with increasing consumer demand for ethical and sustainable products, indicate strong growth potential for the vegan cosmetics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulations and compliance challenges | -1.9% | Europe, North America, Asia-Pacific | Short term (≤ 2 years) |

| High production costs limit market accessibility and growth | -2.3% | Global, more acute in emerging markets | Medium term (3-4 years) |

| Complex ingredient sourcing and supply chain management | -1.4% | Global, especially Asia-Pacific and Europe | Medium term (3-4 years) |

| Limited shelf life of natural ingredients | -1.0% | Global, with higher impact in tropical regions | Medium term (3-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulations and Compliance Challenges

The regulatory environment for vegan cosmetics presents market entry challenges, especially for small brands. Regional compliance requirements, such as the European Union's Regulation (EC) No 1223/2009, establish specific guidelines for cosmetic safety assessment, ingredient limitations, and labeling [2]Source: European Union, "Regulation 1223/2009: Regulatory Framework for Cosmetic Products in the European Union," Belab Services, belabservices.com. The absence of universal standards for "vegan" cosmetics results in market fragmentation, as brands must obtain multiple certifications for international distribution. The rise in misleading environmental claims has led to stricter requirements for transparency in sustainability reporting and marketing, which in turn affects market expansion. These complex and evolving regulations increase operational costs and delay product launches, discouraging new entrants from investing in the sector.

High Production Costs Limit Market Accessibility and Growth

The high costs associated with vegan cosmetics production restrict market growth. The sourcing of plant-based and cruelty-free ingredients is more expensive than conventional alternatives. Additionally, specialized manufacturing processes, rigorous quality control measures, and third-party certifications increase production expenses. These elevated costs are passed on to consumers through higher retail prices, making vegan cosmetics less accessible to price-sensitive consumers and limiting market penetration in developing regions. The limited availability of cost-effective raw materials further intensifies pricing challenges, while small and emerging brands struggle to achieve economies of scale, constraining their competitiveness in the global market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Facial Products Lead Innovation Wave

Facial cosmetics dominate the market, accounting for a 35.05% share in 2025, as consumers increasingly opt for vegan alternatives due to their skin health benefits. The segment maintains its leading position because consumers typically start their vegan beauty journey with facial products, which has led companies to focus their product development in this category. In March 2024, Ilia introduced the New Blurring Complexion Stick. This emphasis on facial products enables companies to showcase the effectiveness of their products and establish consumer confidence in vegan formulations.

The lip and nail makeup segments are projected to grow at a 16.22% CAGR from 2026 to 2031, driven by advancements in vegan pigment technology. The growing trend of clean beauty and natural ingredients has driven up consumer demand for vegan lip and nail products. These technological developments have improved performance qualities and widened the color selection of vegan lip and nail products, making them comparable to conventional cosmetic formulations.

By Category: Premium Segment Accelerates Despite Value Constraints

The mass segment dominates the vegan cosmetics market, accounting for a 55.10% share in 2025. This segment's accessibility enables broader market penetration beyond dedicated ethical consumers. The mass market effectively serves price-conscious consumers while maintaining vegan and cruelty-free certifications. Key brands in this segment include e.l.f. Cosmetics, including CoverGirl and Revolution Beauty, and others.

The premium segment is projected to grow at a CAGR of 15.01% during 2026-2031. This growth stems from consumer demand for advanced formulations and enhanced brand experiences. Premium segment customers exhibit higher basket values and more frequent multi-category purchasing patterns, leading to stronger customer lifetime value. In August 2024, Anastasia Beverly Hills introduced the Blurring Serum Blush, a hydrating liquid blush that provides a soft-matte, radiant, and blurred finish.

By Distribution Channel: Digital Commerce Reshapes Access

Online retail stores dominate the vegan cosmetics distribution landscape with a 39.22% market share in 2025 and are projected to grow at a CAGR of 17.45% through 2031. These platforms effectively showcase ingredient details and ethical certifications, which are essential for selecting vegan products. Digital marketplaces facilitate community interaction and customer reviews, particularly resonating with Generation Z consumers who prioritize peer recommendations and reviews. For instance, Korean vegan beauty brand Heimish enhanced its U.S. market reach through Amazon distribution.

Specialty stores maintain their significance by offering personalized assistance and expert recommendations, while supermarkets and hypermarkets provide widespread product availability. The distribution network is evolving into an omnichannel model, with companies integrating technology to deliver uniform educational content across digital and physical retail channels. Additionally, the growing influence of social media and e-commerce platforms is enhancing brand visibility and enabling direct consumer engagement, further strengthening the retail ecosystem.

Geography Analysis

Europe holds the largest regional market share at 41.10% in 2025, supported by strict regulations and high consumer awareness of ethical consumption. The European Union's Regulation establishes comprehensive standards for cosmetic safety assessment and prohibits animal testing, thereby creating a regulatory environment that is favorable to vegan formulations. Germany and the United Kingdom serve as innovation centers within the European market, where consumers demonstrate strong awareness of ingredient sourcing and sustainability metrics. Unilever PLC's commitment to eliminating animal testing in Europe further strengthens the region's market position.

Asia-Pacific exhibits the highest growth potential with a 21.05% CAGR from 2026-2031, driven by increasing disposable income, environmental awareness, and digital commerce adoption. Japan and Australia lead the regional adoption of vegan cosmetics, with Japanese consumers prioritizing the skin health benefits of plant-based formulations. In April 2024, a German beauty brand entered the Southeast Asian market by launching a new range of vegan makeup products.

North America maintains steady growth as a mature market, characterized by high consumer awareness and a strong direct-to-consumer brand ecosystem. The United States market benefits from an established vegan consumer base and advanced manufacturing capabilities. Gen Z consumers drive market expansion, with 61% prioritizing their appearance and spending an average of USD 84 on health and beauty products per quarter, according to a 2024 survey by the Global Cosmetics Industry . This demographic shift prompts established companies to develop vegan product lines and reformulate existing offerings.

Competitive Landscape

The vegan cosmetics market encompasses a fragmented, competitive landscape with conglomerates, established natural brands, and digital-first companies. Industry leaders like L'Oréal, Unilever, MuLondon, Coty Inc., and Beauty Without Cruelty are expanding their global presence through strategic acquisitions, brand development, and ingredient innovation. L'Oréal's 2024 Universal Registration Document highlights investments in in-vitro safety testing and green chemistry to eliminate animal-derived components, while Unilever has implemented science-based targets for ingredient transparency.

The market presents specific technical challenges, particularly in full-coverage color cosmetics, where manufacturers must balance the stability of opacifying pigments with ethical sourcing requirements. Companies that effectively address these technical requirements gain competitive advantages, especially in the professional makeup artist segment. Market leaders are implementing technological solutions, such as L'Oréal's Garnier Skin Coach, which utilizes AI diagnostics to enhance customer education and product accessibility.

Companies continue to expand their product portfolios through new launches and strategic acquisitions in emerging markets. For instance, in July 2023, TryHealthyLips.com introduced a vegan cosmetic line featuring five fruit-inspired colors with formulations containing shea butter and vitamin E. These developments demonstrate the industry's commitment to addressing evolving consumer needs and strengthening market positions through product innovation and market expansion.

Vegan Cosmetics Industry Leaders

-

MuLondon

-

Beauty Without Cruelty

-

Loreal SA

-

Cottage Holdco B.V. (Coty Company)

-

E.L.F. Cosmetics Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Marinela Makeup launched its vegan cosmetics line in the U.S. and Canada, employing a logistics-first production model that prioritizes ingredient freshness and minimizes waste. By emphasizing fresh-to-order batches and transparent sourcing, the company is drawing attention as a viable alternative to traditional beauty supply chains.

- March 2025: L'Oréal and Unilever jointly invested USD 34 Cr (approximately USD 4.1 million) in Arata, a Delhi NCR-based haircare brand. The investment in Arata, which specializes in natural formulations, indicates increased strategic interest in the expanding Asian vegan beauty market. This investment aligns with both companies' commitment to sustainable and natural beauty products, as they aim to strengthen their presence in the growing Asian cosmetics and personal care market.

- January 2024: Af94, About-Face, announced a new retail partnership with Ulta Beauty. Currently on ulta.com and in select Ulta Beauty stores across the United States, in mid-January, the made-to-play makeup brand and the beauty retailer Af94’s teen-approved, vegan multi-functional products, innovative formulas, and bold infusions of colour at an accessible price point of USD10 or less.

- February 2024: European color cosmetics manufacturer and supplier to many of the world’s biggest cosmetics brands, Schwan Cosmetics, launched the new Glowy Blur Stick at the skincare and makeup industry event MakeUp in LosAngeles. The vegan, lightweight serum-like formula is a blend of skincare ingredients, jojoba, and cocoa butter that help the product glide on the skin and blend in seamlessly.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the vegan cosmetics market as factory-made beauty and personal-care products whose ingredients, processing aids, and testing procedures exclude animals entirely; permitted inputs are plant, mineral, or certified synthetic. Mordor analysts size the market at manufacturer revenue level across skin care, hair care, color cosmetics, fragrance, and related sets sold into retail and professional channels worldwide.

Scope exclusion: products labeled "clean," "organic," or merely "cruelty-free" yet containing beeswax, lanolin, carmine, or any other animal-derived material are left outside this assessment.

Segmentation Overview

-

By Product Type

- Facial Cosmetics

- Eye Cosmetics

- Lip and Nail Make-up Products

-

By Category

- Premium Products

- Mass Products

-

By Distribution Channel

- Specialty Stores

- Supermarkets/Hypermarkets

- Online Retail Stores

- Other Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- France

- United Kingdom

- Spain

- Netherlands

- Italy

- Sweden

- Poland

- Belgium

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Indonesia

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Chile

- Colombia

- Peru

- Rest of South America

-

Middle East and Africa

- United Arab Emirates

- South Africa

- Nigeria

- Saudi Arabia

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and pulse surveys with raw-material suppliers, indie-brand founders, specialty-store buyers, certification auditors, and dermatologists across North America, Europe, Asia-Pacific, and Latin America enabled us to benchmark average selling prices, gauge reformulation costs, and understand certification lead times that secondary data alone could not reveal.

Desk Research

We began by compiling regulatory and trade statistics, such as EU Regulation 1223/2009 notifications, U.S. FDA Voluntary Cosmetic Registration data, and export records from UN Comtrade, alongside consumer attitude polls released by bodies like The Vegan Society and Cosmetics Europe. Our team then reviewed peer-reviewed journals on plant-based formulation science and open-access patent filings to map emerging actives and packaging shifts.

Company 10-Ks, investor decks, and industry press articles retrieved through Dow Jones Factiva, as well as financial snapshots from D&B Hoovers, helped estimate brand revenues and channel mixes, while regional insight was strengthened through associations such as Personal Care Products Council and Asia Cosmetics Association. The sources listed are illustrative; numerous additional documents were consulted to validate figures and close information gaps.

Market-Sizing & Forecasting

A top-down demand pool was built by linking per-capita beauty spend to vegan population penetration, then reconciling it with selective bottom-up checks such as sampled ASP x volume for leading SKUs and online channel take-rates. Core variables, number of certified vegan SKUs, specialty-store floor space, digital share of beauty sales, ingredient cost indices, and regional disposable income feed a multivariate regression that projects revenues to 2030. Where supplier roll-ups under- or over-shot the model, results were proportionally adjusted before finalization.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated anomaly scans, senior-analyst variance checks, and final lead-analyst sign-off. We refresh every twelve months and trigger mid-cycle updates if regulatory bans, major M&A, or raw-material shocks materially shift baseline assumptions.

Why Our Vegan Cosmetics Baseline Inspires Confidence

Published estimates differ because firms vary market scope, price levels, and refresh cadence. By focusing strictly on 100% vegan inputs and net manufacturer revenues, Mordor Intelligence delivers a narrower yet cleaner baseline that decision-makers can trace to explicit drivers.

Key gaps arise when others merge cruelty-free with non-vegan lines, layer retail mark-ups onto manufacturer totals, or project growth through straight-line extensions rather than variable-driven models; our analysts avoid those shortcuts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.04 B (2025) | Mordor Intelligence | - |

| USD 20.48 B (2025) | Global Consultancy A | Counts all cruelty-free cosmetics and uses retail values including channel margins |

| USD 19.50 B (2025) | Industry Association B | Broad personal-care scope and assumes uniform vegan uptake across categories |

| USD 18.25 B (2024) | Trade Journal C | Applies VAT-inclusive receipts and linear growth without driver calibration |

The comparison shows that, while others report larger totals, their wider scopes and looser assumptions inflate values. By anchoring figures to verifiable vegan-only revenues and dynamic variables, Mordor provides a balanced, transparent baseline that clients can rely on when sizing opportunities or benchmarking performance.

Key Questions Answered in the Report

What is the projected vegan cosmetics market size in 2031?

The market is expected to reach approximately USD 11.13 billion by 2031, nearly doubling from its 2026 level.

Which product segment currently commands the largest vegan cosmetics market share?

Facial cosmetics dominate the category, accounting for 35.05% of the total market share in 2025.

What regional market is growing fastest for vegan beauty products?

Asia-Pacific region demonstrates the highest growth rate at 21.05% CAGR, driven by increasing disposable income levels and the growing integration of vegan products with overall wellness trends.

Are premium vegan cosmetics outpacing mass-market alternatives?

The premium segment is widening its revenue contribution due to higher average basket sizes and consumer willingness to trade up for verifiable ethical benefits, with a CAGR of 15.01%.

Page last updated on: