Facial Care Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

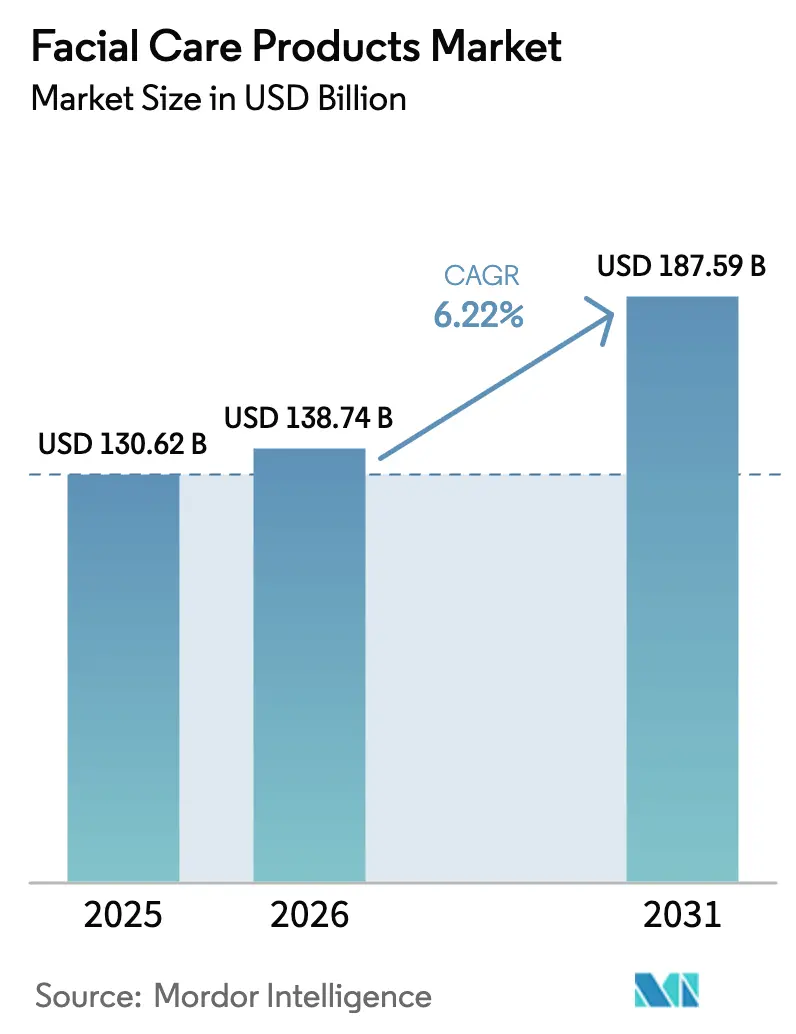

| Market Size (2026) | USD 138.74 Billion |

| Market Size (2031) | USD 187.59 Billion |

| Growth Rate (2026 - 2031) | 6.22% CAGR |

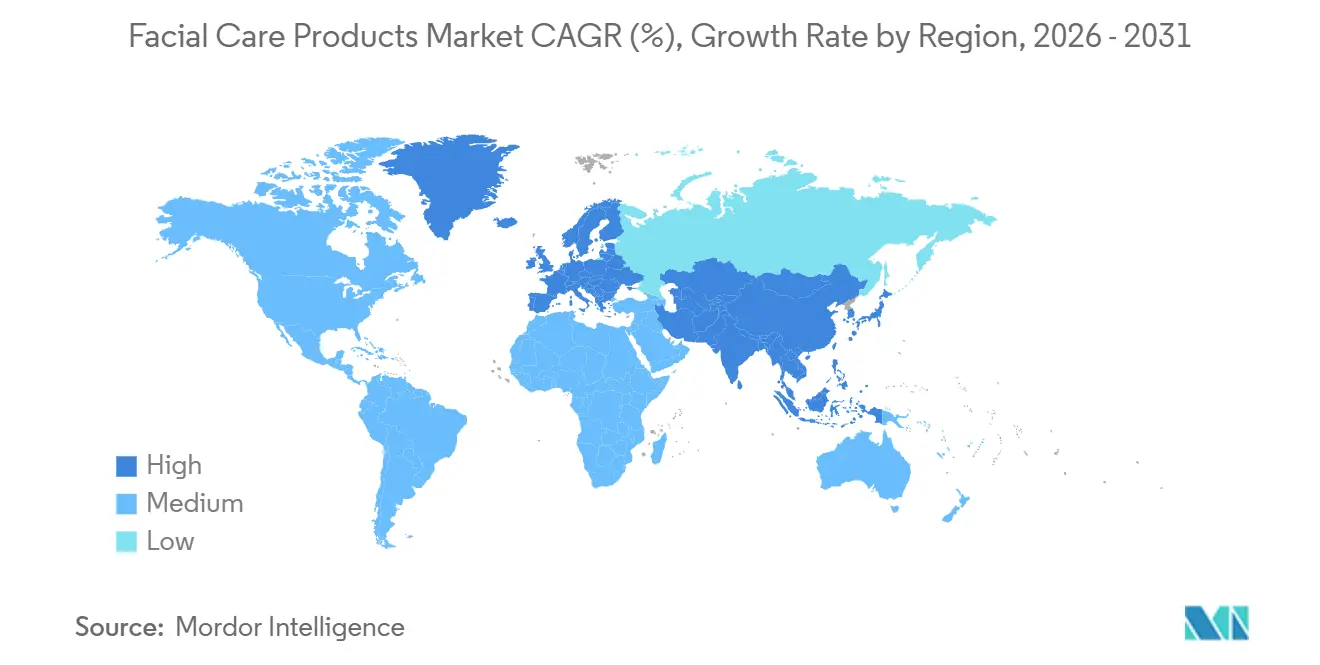

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

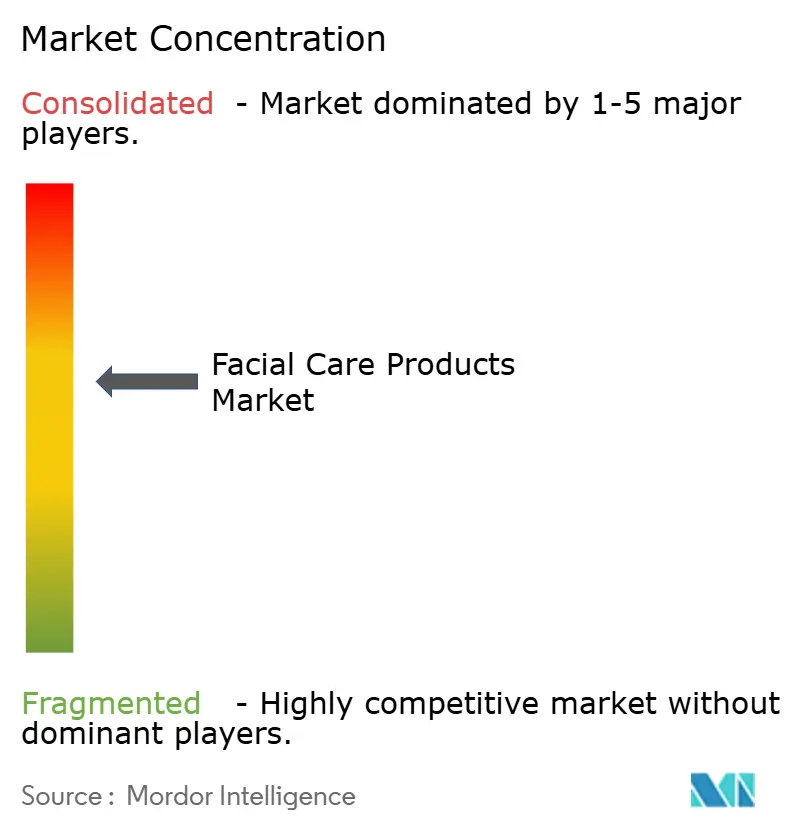

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Facial Care Products Market Analysis by Mordor Intelligence

The facial care market size was valued at USD 130.62 billion in 2025 and estimated to grow from USD 138.74 billion in 2026 to reach USD 187.59 billion by 2031, at a CAGR of 6.22% during the forecast period (2026-2031). Current momentum stems from a consumer shift toward preventive skin health, stringent scrutiny of ingredient transparency, and rapid product innovation. Asia-Pacific continues to anchor growth as localized C-beauty formulations and K-beauty exports scale, while South America records the fastest expansion on the back of botanical-based offerings and rising disposable income. Premiumization, propelled by masstige strategies, compresses the distance between price and science-backed efficacy. Online social commerce redraws distribution economics, and biotechnology reshapes the supply chain for actives and emollients.

Key Report Takeaways

- By product type, moisturizers and creams led with 58.45% revenue share of the facial care market in 2025, whereas toners are set to expand at a 6.78% CAGR through 2031.

- By formulation, conventional formulations retained 68.24% of the facial care market share in 2025, yet natural and organic variants will grow at a 6.89% CAGR, outpacing the headline rate.

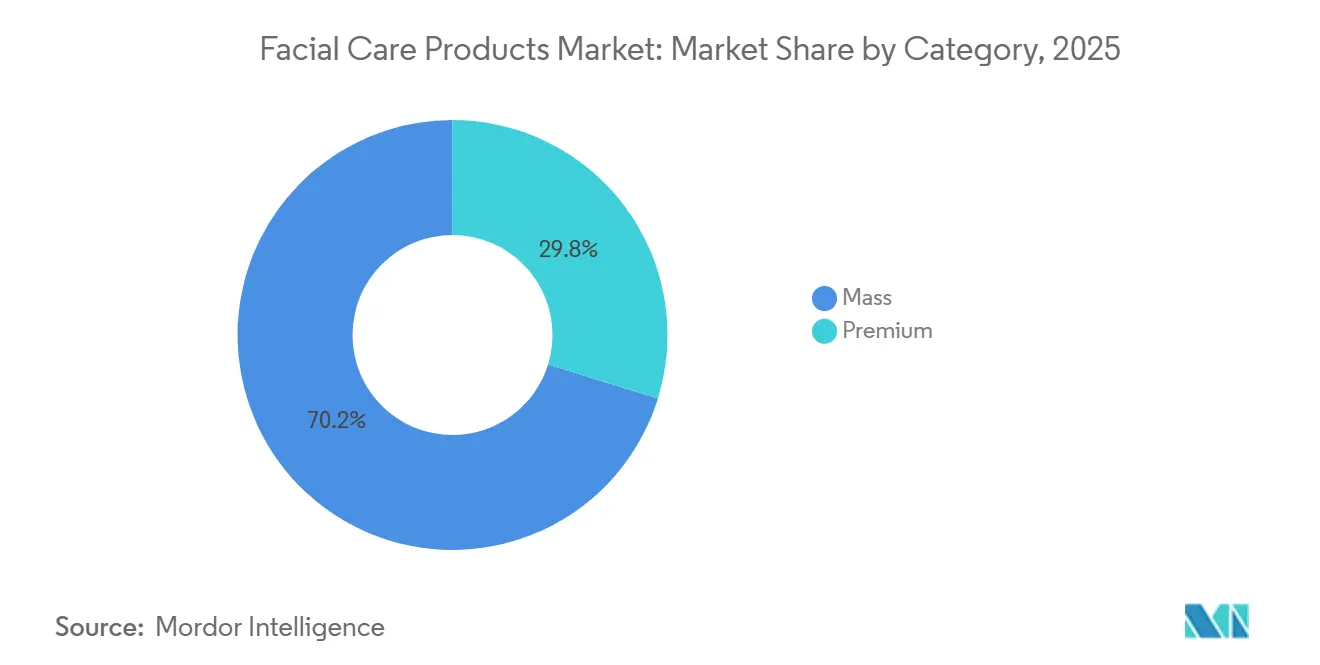

- By category, mass offerings accounted for 70.22% of the facial care market size in 2025, and premium offerings are forecast to rise at a 7.36% CAGR, outstripping the mass segment.

- By distribution channel, online retail stores are projected to grow at a 7.53% CAGR to 2031, eroding the 48.21% share held by beauty and health stores in 2025.

- By geography, Asia-Pacific captured 47.21% of 2025 revenue; South America is projected to advance at an 8.03% CAGR, the fastest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Facial Care Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer inclination towards organic and natural products | +1.2% | Global, with strongest adoption in North America and Europe | Medium term (2-4 years) |

| Influence of social media and celebrity endorsement | +0.8% | Global, particularly strong in Asia-Pacific and North America | Short term (≤ 2 years) |

| Technological innovations in product formulations | +0.6% | Global, led by North America and Europe research and development centers | Long term (≥ 4 years) |

| Increasing demand for anti-aging products | +0.5% | Global, with highest impact in developed markets | Medium term (2-4 years) |

| Growing demand for multifunctional facial care products | +0.7% | Global, with early adoption in urban centers | Medium term (2-4 years) |

| Growing awareness regarding skin-related issues | +0.4% | Global, accelerated by health campaigns | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consumer inclination towards organic and natural products

The shift toward organic and natural facial care products represents a fundamental transformation in consumer behavior, driven by heightened awareness of ingredient safety and environmental sustainability. This trend extends beyond food to personal care, where consumers increasingly scrutinize ingredient lists and seek products free from synthetic chemicals. The California Department of Public Health's Cosmetic Safety Program mandates that products labeled as organic must contain at least 70% organic content, establishing regulatory frameworks that support market transparency[1]Source: California Department of Public Health, "Cosmetic Safety Program", cdph.ca.gov. The convergence of health consciousness and environmental stewardship creates a powerful market force that transcends traditional demographic boundaries. These efforts are also enhancing brand reputation and fostering long-term customer loyalty among environmentally conscious consumers. For instance, in October 2023, Kimirica Organic launched its first plant-based Hydrating + Brightening Face Cream for dull and dehydrated skin. The product offers hydration and brightening.

Influence of social media and celebrity endorsement

Social media platforms have fundamentally altered how consumers discover, evaluate, and purchase facial care products, creating unprecedented influence over market dynamics. The Federal Trade Commission's examination of social media data from 2024 practices reveals that platforms collect extensive demographic information, user metrics, and shopping behaviors, enabling highly targeted advertising that drives consumer purchasing decisions. Research on behavioral advertising demonstrates that targeted advertisements increase purchase intentions compared to random products, though they often present offerings from smaller, less familiar vendors. This dynamic creates opportunities for emerging brands to gain market share through strategic social media positioning, while established companies must adapt their marketing strategies to maintain relevance. Celebrity equity deepened when Coty increased its stake in Kylie Cosmetics, proving that creator-led labels can command enterprise-level valuations. Brand value is thus migrating from traditional advertising to direct community engagement.

Technological innovations in product formulations

Formulation science is moving from empirical chemistry to molecular dermatology. Peptide complexes, such as Matrixyl and Argireline, retail for under USD 30 per unit through The Ordinary, demonstrating that clinical-grade actives can penetrate mass channels. Retinoid alternatives like bakuchiol deliver collagen stimulation with limited irritation according to peer-reviewed trials. Barrier repair follows the 3-1-1 lipid ratio, a model commercialized by CeraVe with dermatologist backing. The integration of research findings enables manufacturers to create more sophisticated skincare solutions. As a result, manufacturers are launching new product formulations in the market. For instance, in February 2025, the Nivea brand launched an advanced skincare segment with the launch of the Luminous Even Glow Range. The range includes a serum, night cream, day cream, and face wash. It features Thiamidol along with Salicylic Acid, Green Tea, and Hyaluronic Acid to help improve skin tone, hydration, and clarity. Advanced formulations allow companies to combine multiple skincare benefits in a single product, meeting consumer preferences for simplified routines.

Increasing demand for anti-aging products

Demographic shifts toward an aging population create sustained demand for anti-aging facial care products, supported by increased healthcare spending and longevity trends. The United States Census data projects that by 2030, 20% of the United States population will be aged 65 or older, with older adults outnumbering children under 18 by 2034. Anti-aging products benefit from scientific validation and clinical efficacy claims, differentiating them from general skincare offerings. Premium price tolerance rises when clinical data backs technology claims. The intersection of aging demographics with increased beauty consciousness among individuals creates a robust market foundation that extends beyond traditional cosmetic applications to include preventive skincare and dermatologically recommended treatments. In response, the Purple Pompa brand introduced an innovative skincare range in August 2024, focused on achieving age balance. The anti-aging products include creams, toners, and moisturizers. In addition, partnerships between cosmetic brands and dermatology clinics are expanding access to medically backed skincare, further driving consumer trust and adoption of anti-aging facial care solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of counterfeit products | -0.3% | Global, with highest impact in emerging markets | Short term (≤ 2 years) |

| Health concerns over chemical ingredients | -0.2% | Global, particularly in regulated markets | Medium term (2-4 years) |

| Growing adoption of at-home skin treatment services | -0.4% | Developed markets, urban centers | Medium term (2-4 years) |

| Fluctuating raw material prices | -0.3% | Global, with supply chain dependencies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of counterfeit products

The counterfeit facial care products market threatens legitimate manufacturers and consumer safety, as government data indicates extensive illicit trade networks. These counterfeit products contain harmful ingredients and are manufactured in poor conditions, creating health risks and reducing consumer trust. The Department of Homeland Security reports that e-commerce growth has facilitated counterfeit product distribution, necessitating increased import monitoring and online platform oversight. The rapid expansion of online marketplaces has made it increasingly difficult for authorities to track and prevent the sale of counterfeit products. U.S. Customs seized USD 3.4 billion in counterfeit items in 2023, while EU authorities intercepted 86 million units, with cosmetics prominent in both tallies. Fake products can replicate authentic packaging and even batch codes, eroding brand equity when adverse reactions occur. LVMH addresses authenticity with Aura, a blockchain that tracks each unit from factory to point of sale.

Growing adoption of at-home skin treatment services

The growth of at-home skincare treatments and telehealth services affects traditional facial care product sales by providing alternative skin health management options. The Bureau of Labor Statistics forecasts 10% employment growth for skincare specialists from 2023 to 2033, due to increased consumer demand for professional treatments and mobile facial services. At-home devices covering LED therapy, micro-current, and ultrasonic infusion are forecast to rise by 2033, reducing spa visitation frequency. Professional operators now bundle in-clinic treatments with device-enabled upkeep programs. Brands supplying both service protocols and retail devices secure recurring revenue streams. The combination of professional expertise and convenient delivery methods competes with traditional facial care products. The availability of at-home treatment devices and professional-grade formulations reduces the distinction between consumer and professional markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Toners Drive Multi-Step Adoption

Moisturizers and creams dominated 2025 revenue with 58.45%, reflecting their central role in maintaining the skin barrier. Toners will post a 6.78% CAGR through 2031, the highest within the facial care market, as multi-layer hydration routines originating in Korea become mainstream. The 7-skin method popularized the idea that toners can function as treatment vehicles rich in fermented filtrates, propelling sales of essence-toner hybrids. Exfoliating toners containing polyhydroxy acids expand addressability to sensitive-skin users. Cleansers undergo premiumization via oil-to-milk textures that avoid barrier disruption, while masks move from occasional indulgence to nightly sleep packs. Other formats, such as serums, benefit from targeted active delivery, commanding premium pricing.

The Bureau of Labor Statistics reports that personal care products experienced 1.0% price increases in March 2025, indicating inflationary pressures that may shift consumer preferences toward value-oriented formulations within each category[2]Source: Bureau of Labor Statistics, "Consumer Price Index March 2025", bls.gov. Product type segmentation increasingly blurs as manufacturers develop hybrid formulations that combine cleansing, treatment, and moisturizing benefits in single products. This trend toward multifunctional products reflects consumer demand for simplified skincare routines without compromising skincare efficacy, creating opportunities for innovation across traditional category boundaries.

By Formulation: Biotech Blurs Conventional–Natural Divide

Conventional products held a 68.24% share in 2025, yet natural and organic options will grow at a 6.89% CAGR. COSMOS sets a 95% natural origin threshold and bans GMOs and parabens, providing a harmonized framework for cross-border trade. Precision fermentation now yields hyaluronic acid and squalane at scale, enabling “naturally identical” positioning and lowering environmental impact. This market segmentation aligns with broader consumer trends, where health awareness, taste preferences, and environmental concerns drive organic product purchases across categories. To capitalize on this growing interest, manufacturers are revamping and expanding their product offerings by introducing a wide range of organic facial care products that contain plant-based, clean-label ingredients, with claims such as ‘organic’, ‘natural’, ‘chemical-free’, and ‘cruelty-free’.

The United States Food and Drug Administration's Modernization of Cosmetics Regulation Act strengthens ingredient oversight by requiring manufacturers to validate safety claims and maintain comprehensive records. This regulatory framework benefits natural ingredient suppliers with transparent sourcing and processing documentation, while creating additional compliance requirements for conventional formulations using synthetic compounds. The ingredient composition influences product positioning, as natural and organic products generate higher margins despite elevated production costs. Synthetic ingredients still offer cost and stability advantages. Phenoxyethanol remains a reliable preservative, and silicones give the desired slip. However, EU restrictions on microplastics and certain UV filters force even conventional brands to reformulate.

By Category: Masstige Collapses Price–Quality Perception

Mass products accounted for 70.22% of 2025 revenue, yet premium offerings will grow at a 7.36% CAGR. The Ordinary proved that transparent, high-concentration actives can retail below USD 10 without undermining credibility. CeraVe leverages dermatologist endorsements to straddle mass and prestige positioning. Premium brands respond by emphasizing patented technology and sensorial packaging. Estée Lauder prices Advanced Night Repair above USD 100 per ounce, substantiating the premium through Chronolux Power Signal research. This trend correlates with rising disposable incomes and growing health awareness among consumers. Additionally, the accessibility of premium products through e-commerce and specialty retailers is narrowing the gap between mass and premium facial care product offerings.

According to the Bureau of Labor Statistics, consumer spending on personal care products and services increased by 9.7% in 2023, indicating strong market demand across both segments[3]Source: Bureau of Labor Statistics, "Consumer Expenditures 2023", bls.gov. Premium products gain momentum through advanced formulation technologies, supported by federal initiatives that enable the commercialization of innovative skincare solutions. Market success across both mass and premium segments increasingly relies on clinical evidence, ingredient disclosure, and eco-friendly packaging to meet consumer demands for transparency and environmental responsibility. Brands that align with wellness trends and offer multifunctional benefits are particularly well-positioned to capture evolving consumer preferences. Mid-tier labels risk squeeze as consumers polarize between affordable efficacy and experiential luxury. Strategies include vertical integration to lower the cost of goods or acquisition by conglomerates.

By Distribution Channel: Social Commerce Rewrites Retail

Beauty and health stores captured 48.21% revenue in 2025 thanks to experiential discovery, yet online retail will expand at a 7.53% CAGR to 2031. TikTok Shop converted short-form video engagement into USD 2.5 billion sales within its first year, showing how entertainment integrates with checkout. Instagram Shopping exposes 130 million users to product tags each month. Sephora and Ulta embed virtual try-on tools and buy-online-pick-up-in-store services to maintain relevance. Supermarkets and hypermarkets serve as convenient access points for regular purchases, while pharmacies and drug stores capitalize on their health-oriented positioning and professional guidance. Alternative distribution channels, such as subscription services, provide new routes to market outside traditional retail networks.

Distribution channels continue to adapt to retail trends that emphasize omnichannel experiences, where consumers conduct online research and make purchases across various platforms. The expansion of online retail creates market entry opportunities for new brands while prompting traditional retailers to strengthen their market position through customized services and unique product offerings. Moreover, the rise of social commerce and influencer-driven marketing is blurring the lines between content and commerce, enabling direct-to-consumer engagement and boosting conversion rates. Supermarkets lose share as shoppers research ingredients before purchase. Direct-to-consumer sites capture full margin and first-party data. Salons and spas offset slower service traffic by retailing professional-grade products, blending treatment and take-home regimens.

Geography Analysis

Asia-Pacific generated 47.21% of 2025 revenue for the facial care market. Local brands fuse traditional medicine ingredients with modern textures, resonating with cultural identity. K-beauty exports reached USD 13.2 billion in 2023, with a national goal of USD 20 billion by 2030. Japan focuses on barrier science and UV protection, reflecting consumer preference for concise routines. ASEAN growth accelerates as mobile commerce penetrates secondary cities. The region's market position stems from robust manufacturing capabilities and domestic consumption patterns, with South Korea and Japan driving product innovation and beauty technology development. China's growing middle class provides significant market opportunities, while Southeast Asian markets show increased sophistication in product preferences and premium skincare adoption.

South America is forecast to expand at an 8.03% CAGR through 2031, the fastest regional pace in the facial care market. The region's expansion results from growing middle-class populations and shifting preferences toward premium personal care products. Brazil dominates regional demand with its large population and established beauty culture. The region leverages established supply chains for natural ingredients and manufacturing infrastructure that supports local market demand. Brazil ranks fourth globally in beauty spending led by Natura and O Boticário. Indigenous Amazonian oils and butters give local brands a clean-beauty narrative. ANVISA maintains EU-comparable safety protocols, supporting export ambitions.

North America maintains a mature market characterized by consumer preferences for scientifically validated products and strong brand loyalty toward companies with established research capabilities. Europe focuses on sustainability and ingredient transparency, generating demand for natural and organic formulations that meet environmental regulations and consumer expectations. The region's aging population sustains anti-aging product demand, while younger consumers drive growth in multifunctional and technology-enhanced products. The Middle East and Africa offer growth opportunities due to young populations and increasing urbanization, though market development varies by country based on economic conditions and regulations. India’s Ayurvedic subcategory gains traction, though oversight remains separate from conventional cosmetic regulation under the Ministry of Ayush.

Competitive Landscape

The facial care products market demonstrates moderate concentration, which enables both established companies and new entrants to capture market share through distinct strategies. Major players in the market include The Estée Lauder Companies Inc., L'Oréal SA, Shiseido Company Limited, Unilever PLC, and The Procter and Gamble Company, among others. Large multinational corporations maintain their market positions through scale advantages, robust distribution networks, and substantial research capabilities. Smaller companies compete effectively by focusing on niche segments, implementing direct-to-consumer business models, and developing specialized formulations for specific consumer requirements.

Companies in the market prioritize natural and organic product development, digital marketing initiatives, and integrated distribution strategies that serve customers across various channels. The industry's technological advancement centers on personalization systems, AR-based product testing, and consumer data analytics to improve customer relationships and loyalty. Key growth opportunities exist in sustainable packaging development, men's facial care segments, and age-targeted formulations. However, the market faces significant challenges from counterfeit products, emphasizing the need for product authentication systems and secure distribution methods.

New market entrants include biotech firms developing innovative ingredients, personalized subscription services, and digital platforms combining professional skincare advice with product suggestions. Success in the market increasingly depends on companies' ability to balance scientific validity with strong brand relationships, establishing lasting competitive advantages in this expanding market. The market is increasingly rewarding for companies successfully combining scientific credibility with brand connections, creating sustainable differentiation in an increasingly crowded marketplace.

Facial Care Products Industry Leaders

-

The Estée Lauder Companies Inc.

-

L'Oréal SA

-

Shiseido Company Limited

-

The Procter and Gamble Company

-

Unilever PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Vedic Pride introduced its Face Cleanser, claiming to combine Ayurvedic principles with stem cell technology and nanotechnology. The cleanser uses plant-based stem cells to support skin regeneration and repair while maintaining its cleansing properties.

- October 2024: Bayer's Consumer Health Division introduced Bepanthen, a global skincare brand, to the Indian market. The Bepanthen product line in India includes moisturizers and cleansers for face and body, specifically formulated for dry, irritated, and sensitive skin. The products contain pro-Vitamin B5 and prebiotics and are free from fragrances and parabens.

- April 2024: Sisley Paris, a renowned beauty brand, unveiled Neuraé. This new skincare line claims to focus on neuroscience and emphasizes the link between the skin and emotions. Drawing inspiration from neuroscientific research, Neuraé mentions offering innovative and effective solutions targeting issues like dullness, fatigue, and tension in the skin, all of which can signal premature aging.

- March 2024: Clinique made its debut in the United States Amazon Premium Beauty store, enhancing access to its clinically validated skincare and makeup solutions, and dermatological insights.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study frames the facial care products market as the sale-through value of cleansers, toners, serums, moisturizers, masks, exfoliants, and allied leave-on or wash-off formulations created specifically for facial skin. Products for body care, devices, ingestible supplements, and professional in-clinic services sit outside this boundary.

Scope exclusion: hand, body, and device-based skin treatments do not enter the model.

Segmentation Overview

-

Product Type

- Cleansers

- Masks

- Moisturizers and Creams

- Toner

- Other Product Types

-

Formulation

- Conventional

- Natural/Organic

-

Category

- Mass

- Premium

-

Distribution Channel

- Supermarkets/Hypermarkets

- Beauty and Health Stores

- Online Retail Stores

- Others Distribution Channel

-

Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed formulators, dermatologists, category buyers at pharmacy chains, and digital-first beauty founders across Asia-Pacific, North America, and Europe. These discussions clarified average selling prices, refill uptake, and the pace at which premium SKUs are cannibalizing mass lines, allowing us to tighten elasticity assumptions before final triangulation.

Desk Research

We began by gathering trade statistics from sources such as UN Comtrade for finished-product exports, Euromonitor International for retail channel splits, and consumer expenditure tables from the World Bank that signal wallet share shifts. Ingredient usage volumes from the Personal Care Products Council, quarterly financials in 10-K filings, and patent trends captured via Questel helped us spot innovation cycles. Subscription databases like D&B Hoovers delivered brand-level revenue that anchors company shares. This list is illustrative; many more open and paid sources informed the desk-review grid.

The material above gave us baseline volumes, category weights, and regional demand curves, yet pricing dynamics and future launch pipelines remained hazy until corroborated with field input.

Market-Sizing & Forecasting

We employed a top-down build that reconstructs demand from household spending on personal care, facial-care penetration rates, and average annual usage per capita. Outputs are pressure-tested with selective bottom-up checks (brand roll-ups and sampled ASP × units) so totals converge. Key variables include urban female labor-force participation, online beauty channel share, natural-ingredient claim prevalence, promotional density during festival months, and SPF/moisturizing dual-claim launches. A multivariate regression, supplemented by ARIMA for short-term shocks, extends these inputs through 2030. Gaps in brand-level splits are bridged using weighted averages from closest public peers.

Data Validation & Update Cycle

Every quarter, Mordor analysts benchmark fresh sell-out receipts, ingredient cost swings, and currency moves against the model. Variances above set thresholds trigger re-checks with external experts before sign-off. Reports refresh annually, and clients receive an interim revision whenever material regulatory or M&A events surface.

Why Mordor's Facial Care Products Baseline Commands Dependability

Published estimates often differ because firms select dissimilar product mixes, price points, and refresh cadences.

Key gap drivers include narrower SKU baskets, single-region focus, or unvetted ASP escalators applied by some publishers versus the disciplined scope and live-pricing loops we maintain.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 130.87 B (2025) | Mordor Intelligence | |

| USD 116.03 B (2024) | Global Consultancy A | Excludes premium serums and uses 2024 base without currency normalization |

| USD 160.30 B (2025) | Regional Consultancy B | Adds body lotions and includes professional spa facials under retail umbrella |

| USD 107.69 B (2025) | Industry Association C | Omits online-only indie labels, leading to understated retail value |

The comparison shows that while other studies swing wide due to scope or pricing gaps, Mordor Intelligence grounds its baseline in transparent product limits, multi-source price audits, and a repeatable update cadence, giving decision-makers a balanced figure they can trust.

Key Questions Answered in the Report

How large is the facial care market in 2026?

The facial care market size stands at USD 138.74 billion in 2026 with a 6.22% CAGR outlook to 2031.

Which region records the fastest facial care growth?

South America leads with an 8.03% CAGR forecast, propelled by Brazil’s robust beauty spending and botanical formulations.

Which product segment is growing the quickest?

Toners post the fastest growth at a 6.78% CAGR as multi-step hydration routines gain global acceptance.

How are online channels impacting facial care sales?

Online retail, powered by social commerce on platforms like TikTok Shop, is projected to expand at 7.53% CAGR and capture share from beauty specialty stores.

Page last updated on: