Organic Coffee Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 8.73 Billion |

| Market Size (2031) | USD 14.12 Billion |

| Growth Rate (2026 - 2031) | 10.09% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

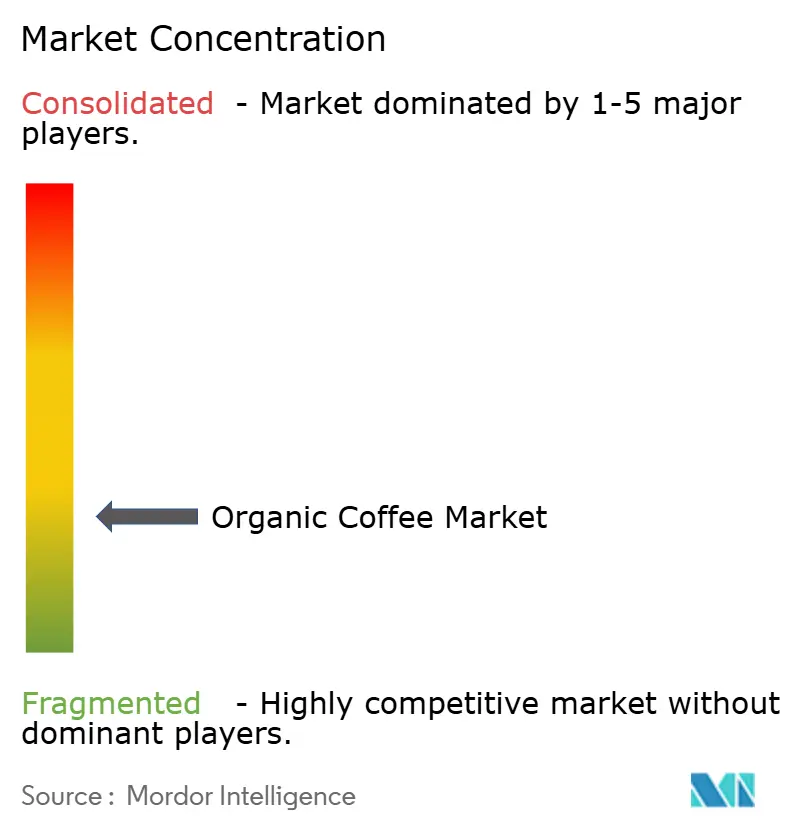

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Organic Coffee Market Analysis by Mordor Intelligence

The organic coffee market size is projected to expand from USD 8.1 billion in 2025 and USD 8.73 billion in 2026 to USD 14.12 billion by 2031, registering a CAGR of 10.09% between 2026 to 2031. Driven by robust consumer demand for certified-sustainable beverages, tightening environmental regulations like the EU Deforestation Regulation, and a rising health consciousness, households in both developed and emerging economies are increasingly adopting these products. Europe, led by Germany and the Netherlands as re-export hubs, continues to dominate in terms of revenue. Meanwhile, the Asia-Pacific region is witnessing a surge in new café openings, particularly in China and India. While on-trade venues remain the primary drivers of value creation, direct-to-consumer subscriptions and online grocery platforms are swiftly expanding off-trade reach and altering gross-margin dynamics. Arabica beans remain the cornerstone of specialty offerings. However, a notable shift is emerging: with accelerating investments in organic Robusta certifications in Vietnam and Indonesia, there's a pivot towards espresso blends. These blends, preferred in Southern Europe and East Asia for their ability to pair with milk and sugar, signal a changing trend in the market.

Key Report Takeaways

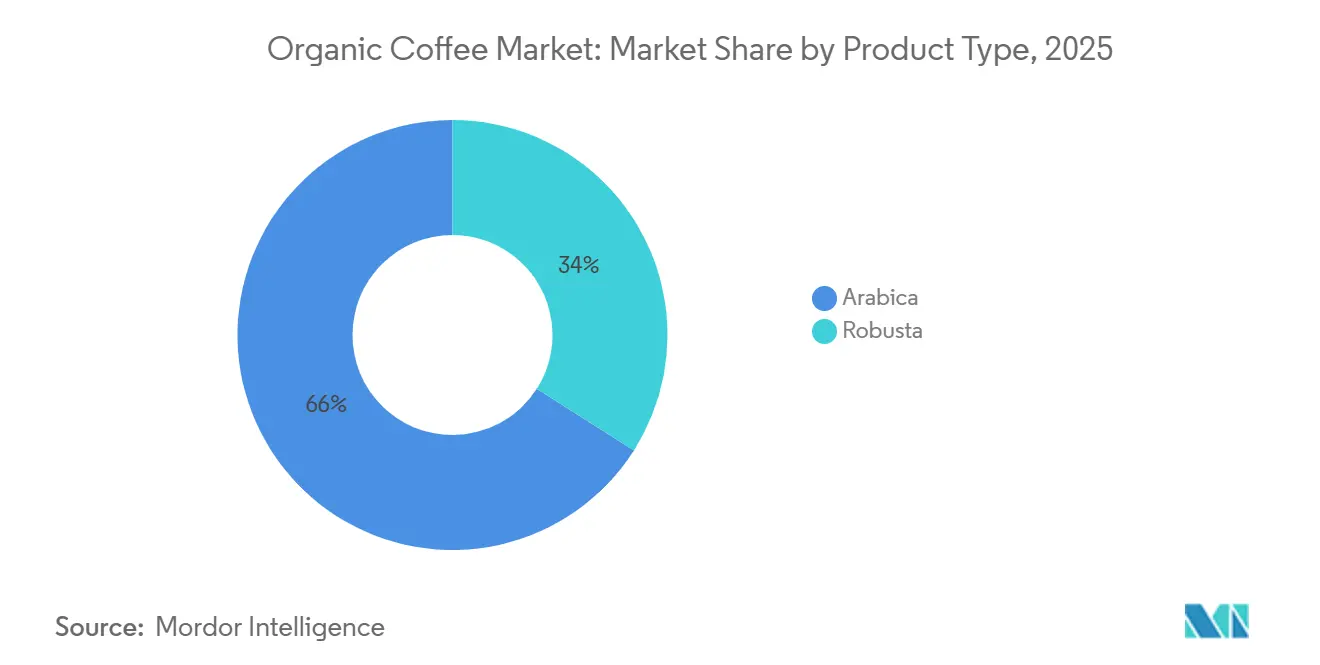

- By origin, Arabica beans led with 65.98% of the organic coffee market share in 2025, and Robusta is forecast to expand at a 10.87% CAGR through 2031.

- By product form, ground coffee accounted for 34.87% of 2025 revenue, whereas pods and capsules are projected to grow at an 11.24% CAGR to 2031.

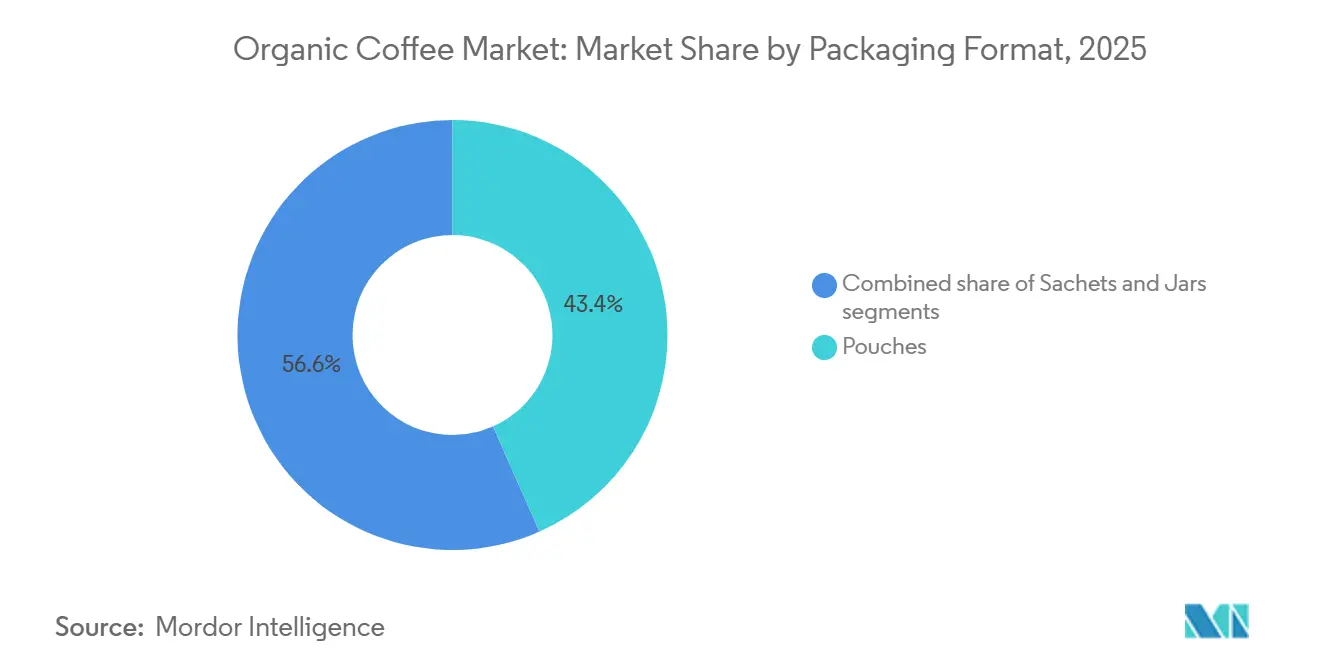

- By packaging, pouches captured 43.37% of 2025 sales, yet jars are set to rise at a 12.56% CAGR through 2031.

- By channel, on-trade outlets generated 76.83% of 2025 revenue, although off-trade is advancing at a 7.98% CAGR.

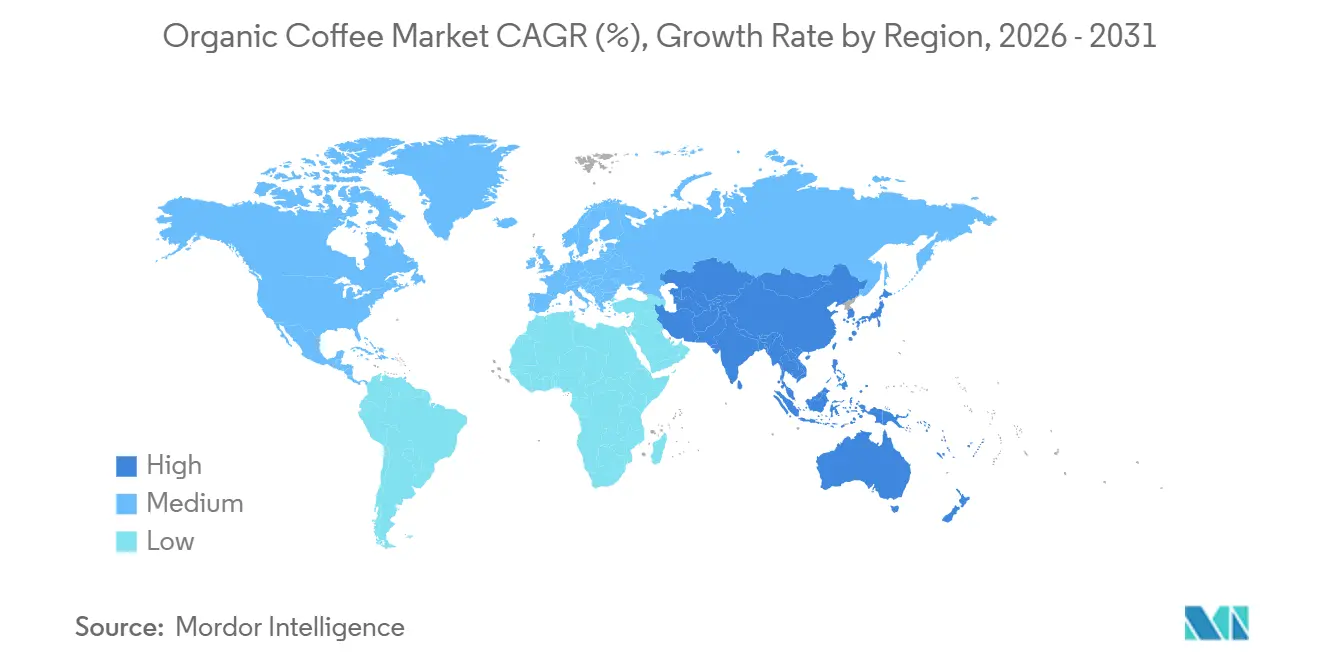

- By region, Europe held 34.90% of 2025 turnover; Asia–Pacific is the fastest-growing territory, advancing at a 9.62% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Organic Coffee Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium-pricing acceptance in developed economies | +1.8% | North America, Western Europe, Australia | Medium term (2-4 years) |

| Government incentives expanding organic cultivation | +1.5% | Brazil, Colombia, Peru, Central America | Long term (≥ 4 years) |

| Growth of single-serve organic coffee formats | +1.9% | Global, led by the United States and the European Union | Short term (≤ 2 years) |

| Clean-label café menu adoption | +1.2% | Urban centers worldwide | Medium term (2-4 years) |

| Low-acid SKUs boosting specialty-retail demand | +0.9% | North America, Northern Europe | Short term (≤ 2 years) |

| On-trade outlets switching to 100% organic beans | +1.1% | Europe, North America, urban Asia–Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premium-pricing acceptance in developed economies

In 2025, consumers in the U.S., Canada, Germany, and France accepted 25-40% price premiums on organic products. According to the Center for the Promotion of Imports, 19% of German consumers in 2024 were willing to pay premium prices for organic-certified coffee, indicating a direct correlation between ethical sourcing and purchasing behavior [1]Source: Center for the Promotion of Imports, “The German market potential for coffee,” cbi.eu. This trend was bolstered by transparent supply-chain narratives and QR-code traceability initiatives introduced by Starbucks and Nestlé. Nestlé's organic Nespresso line achieved an 18% increase in average selling prices, yet maintained repeat purchases. This indicates a shift: consumers are now more inclined to pay for verification rather than viewing it as a niche rarity. Blockchain initiatives in 2,400 U.S. stores led to double-digit increases in organic attachment rates, underscoring the effectiveness of in-store digital prompts in converting certification stories into sales. Australia saw a similar pattern, with the Australian Bureau of Statistics noting a 22% rise in organic coffee retail turnover, driven by millennials' preference for Fair Trade and Rainforest Alliance certifications. Given the consistent price resilience, the narrowing price gap between organic and conventional roasts suggests a broader market potential for organic coffee in the coming years.

Government incentives expanding organic coffee cultivation

Brazil allocated BRL 500 million (USD 100 million) in subsidies to transform 50,000 hectares of conventional coffee into organic by 2028. This initiative, primarily in Minas Gerais and Espírito Santo, covers 70% of certification fees and mitigates transition risks for smallholders. In 2024, the Asian Development Bank extended a USD 100 million loan to ECOM Agroindustrial Corporation. This funding aims to cultivate climate-resilient coffee value chains in India, Indonesia, Papua New Guinea, and Vietnam, benefiting over 62,000 smallholder farmers[2]Source: Asian Development Bank, “ADB Provides USD 100 Million Loan to Boost Climate-Resilient Coffee,” adb.org. Colombia and Peru implemented concurrent technical-assistance programs and expanded their inspector workforce, effectively halving accreditation lead times. These governmental initiatives are steering farmers towards formal organic certification, stabilizing supply curves in origin countries, and reducing the premium multinationals previously paid for certified beans. With a more abundant supply, vertically integrated roasters like JDE Peet’s, which secure multiyear supply contracts, can expect improved margin predictability. Additionally, a broader grower pipeline allows smaller craft roasters to access micro-lots, bypassing the large-lot minimums that typically advantage established players.

Growth of single-serve organic coffee formats

As lineups compatible with Keurig and Nespresso platforms enter mass distribution, pods and capsules are set to grow through 2031. Within just six months, Keurig Dr Pepper’s 12-SKU compostable range captured a 6% share of the U.S. single-serve organic segment, underscoring a strong demand for convenience alongside eco-friendly disposal options. Lavazza bolstered its aluminum capsule-recycling initiative in Italy and Spain by introducing over 1,200 municipal drop-off points, highlighting that a robust circular-economy infrastructure can mitigate consumer concerns about waste. In 2025, patent activity surrounding oxygen-barrier biopolymers surged by a third, signaling a competitive technological race within the industry to replicate aluminum-pod shelf life while ensuring compostability. The allure of convenience remains strong, even among eco-conscious consumers, suggesting that the industry will lean towards gradual material innovations instead of a complete shift back to bulk formats.

Clean-label café menu adoption

Municipal bans on single-use plastics, coupled with heightened consumer scrutiny over ingredient origins, are driving a shift towards clean-label menus in both independent cafés and global chains. Starbucks has committed to sourcing 20% of its total coffee volume from organic origins by 2027. In a move towards transparency, the coffee giant began highlighting cooperative names on its European menu boards in late 2025. The clean-label initiative, as exemplified by Starbucks, emphasizes both ingredient transparency and ethical sourcing. Starbucks proudly sources 99% of its coffee through its Coffee and Farmer Equity Practices[3]Source: Starbucks Corporation, “Global Environmental and Social Impact Report 2025,” starbucks.com. In January 2026, Blue Bottle Coffee made a significant shift, transitioning its entire U.S. offerings to organic beans. This decision was backed by survey data indicating that 68% of its patrons associate organic certification with superior taste and ethical practices. The trend isn't limited to coffee; vendors of oat and almond milk are now required to present organic certificates to stay on approved supplier lists. Urban centers like Shanghai and Seoul witnessed a 30% surge in organic brew sales during 2025, underscoring the amplified reputational benefits of clean-label commitments in densely populated areas. These industry shifts are not just about meeting consumer demands; they're also about locking in future demand. As a result, exporters are now standardizing organic and traceability protocols to align with the rigorous requirements of multinational audits.

Restraints Impact Analysis of Organic Coffee Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Organic-grade fertilizer scarcity in Central America | -1.4% | Guatemala, Honduras, Nicaragua, Costa Rica | Short term (≤ 2 years) |

| Heightened consumer concern over caffeine intake | -0.8% | North America, Northern Europe | Medium term (2-4 years) |

| Substitution from functional RTD beverages | -0.6% | Global, led by U.S. and urban Asia | Short term (≤ 2 years) |

| Higher price volatility vs. conventional coffee | -0.7% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Organic-grade fertilizer scarcity in Central America

In 2025, Guatemala, Honduras, and Nicaragua faced significant shortages of USDA-compliant compost, as the growth in organic acreage outstripped the region's composting capabilities. Despite Guatemala boosting its organic fertilizer imports by 45% year-over-year, the supply still fell short, meeting only 62% of local demand. This shortfall compelled local growers to stretch application intervals and settle for diminished yields. In Honduras, organic yields per hectare dropped by 12% in 2025 compared to 2024, a decline directly linked to delays in nutrient delivery during the crucial flowering stage. Meanwhile, the Costa Rican government, in a bid to bolster its biochar plants, aimed to add 15,000 metric tons of capacity by 2027. However, this intervention comes too late to avert immediate output declines. These ongoing nutrient bottlenecks threaten to trigger regional supply shocks, potentially widening the price gap between organic beans from Central and South America.

Heightened consumer concern over caffeine intake

Shoppers in North America and Northern Europe are cutting back on caffeine, particularly in the evenings, leading to a rise in the popularity of half-caf blends and herbal substitutes. Data from a 2025 survey by Canada's Heart & Stroke Foundation showed a notable increase: 37% of adults now limit their caffeine intake to one cup daily, a jump from 28% in 2023. This shift reflects growing health awareness and concerns about the potential negative effects of excessive caffeine consumption, such as sleep disturbances and increased heart rate. In response, specialty roasters are turning to naturally low-caffeine Arabica varieties like Laurina and Aramosa. However, these varieties face challenges due to their limited agronomic yield, which restricts large-scale production and availability. Retailers are broadening their offerings of organic decaf options. Yet, the solvent-free Swiss Water processing method, which inflates green-bean costs by 20-25%, tightens margins unless consumers are willing to pay a premium. If this trend solidifies, it may limit the growth potential for regular organic SKUs in established markets, as consumer preferences shift toward healthier and lower-caffeine alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Organic Coffee Market Segment Analysis

By Origin:

Robusta Gains Ground on Espresso DemandBy 2025, Arabica is set to command a dominant 65.98% share of the global organic coffee market. Its supremacy is bolstered by premium offerings from high-altitude regions like Colombia and Ethiopia, known for their unique flavor profiles and assured traceability. Even with challenges like saturated cultivated acreage and rising climate threats, these regions consistently fetch premiums, ensuring specialty roasters remain profitable. Initiatives like blockchain traceability pilots, especially Colombia’s collaboration with IBM Food Trust, bolster buyer trust. Additionally, agronomy training programs backed by Latin American governments are refining cupping scores, solidifying Arabica’s status at the pinnacle of the premium organic market.

In contrast, Robusta is emerging as the organic coffee market's fastest-growing segment, with projections of a 10.87% CAGR through 2031. This surge is largely driven by intensified certification efforts from producers in Vietnam and Indonesia. European roasters are now tweaking their espresso blends, incorporating organic Robusta for its cost-effectiveness and richer crema. In 2025, with backing from Rainforest Alliance, Indonesia's Sulawesi and Sumatra regions expanded their certified Robusta acreage by 8,500 hectares. This swift certification expansion is paving the way for budget-friendly organic instant coffee, catering to Eastern Europe and Southeast Asia, where consumers prioritize value over single-origin tales. Such developments position Robusta as a crucial growth catalyst, diversifying the supply landscape while complementing Arabica's premium emphasis

By Product Form:

Pods and Capsules Reshape Household ConsumptionIn 2025, ground coffee dominated the organic coffee market, accounting for 34.87% of its total value. Its widespread appeal stems from its adaptability to various brewing devices and a strong consumer affinity for traditional preparation methods. While ground coffee's growth rate of 8% lags behind the surge of single-serve options, it remains a cornerstone for both retail and out-of-home sales worldwide. Whole-bean formats, commanding a 28% share, bolster their premium status, appealing to third-wave cafés and aficionados who relish grinding fresh beans at home. Yet, in North America, growth has slowed as the adoption of espresso machines stabilized, coinciding with the settling of hybrid work trends.

Pods and capsules have emerged as the quickest-growing segment, boasting an impressive 11.24% CAGR through 2031, driven by consumer demands for convenience and sustainability. The swift rise of compostable and bio-based capsule materials, like BASF’s polylactic-acid format, which is certified for industrial composting, has alleviated environmental worries without compromising on performance or shelf life. As more households embrace organic coffee, the audience is expanding from niche specialty drinkers to families in search of hassle-free brewing. Instant organic coffee is also riding this wave of convenience, especially in the Asia–Pacific region, where innovative freeze-dried products propelled South Korean sales by 34% in 2025. This collective momentum in single-serve formats is not only shifting value distribution within the category but also spurring innovation among suppliers.

By Packaging Format:

Jars Capture Premiumization WavePouches led the organic coffee packaging scene in 2025, capturing 43.37% of total sales. Their lightweight nature, resealability, and cost-effective shipping make them especially appealing for e-commerce, where breakage is a concern. Even with intensifying competition, pouches retain their top spot, bolstered by sustainable options and hybrid designs that enhance shelf appeal. In markets prioritizing efficiency, exporters and major retailers alike favor these flexible formats. Ongoing advancements in recyclable and mono-material films further solidify pouches' status, even amidst a trend towards premiumization.

Jars are the packaging format on the rise, boasting a 12.56% CAGR as consumers increasingly associate glass with artisanal quality and reusability. Brand initiatives have fueled this momentum, exemplified by JDE Peet’s 2025 glass-jar debut, which captured 9% of the U.S. premium organic market in just four months, all while commanding an 18% price premium. Starbucks’ jar-return initiative highlighted the model's loyalty potential, achieving a notable 22% repeat purchase rate with a USD 2 refill incentive. In Germany, sales of embossed glass jars jumped 41% year on year, driven by small roasters aiming for a unique shelf presence. This uptick underscores how aesthetic allure and circular packaging efforts are transforming jars from a niche choice to a key growth driver.

By Distribution Channel:

Off-Trade Gains on Direct-to-Consumer ModelsIn 2025, on-trade channels dominated the organic coffee market, capturing 76.83% of total sales. This stronghold is bolstered by entrenched café cultures in countries like Italy and Japan, where traditions such as espresso bars and kissaten play pivotal roles in daily consumption. Demand is further amplified by hotels, restaurants, and specialty cafés, all of which feature premium organic beverages on their menus. While convenience stores have limited space and often prioritize functional ready-to-drink options, they struggle to accommodate high-priced organic formats. Consequently, despite evolving consumer habits, on-trade channels remain central to organic coffee consumption.

Off-trade channels are emerging as the fastest-growing segment, boasting a 7.98% CAGR, fueled by the rapid ascent of online grocery shopping, home delivery, and subscription services. In 2025, U.S. e-commerce sales of organic coffee surged by 16%, with Shopify-backed storefronts enabling small roasters to achieve impressive 60–70% gross margins through direct shipments to households. Supermarkets played a pivotal role in enhancing category visibility, with notable expansions in organic shelf space at Whole Foods by 12% and Carrefour by 9%. Subscription platforms showcased their prowess by keeping churn rates below 4% monthly, thanks to curated rotating micro-lots and compelling storytelling content that fostered customer loyalty. This broader diversification across both retail and digital avenues not only helps brands tap into new consumer occasions but also acts as a buffer against the volatility of on-trade channels.

Geography Analysis

Europe Organic Coffee Market

In 2025, Europe accounted for 34.90% of global revenue, largely due to Germany and the Netherlands acting as re-export hubs, channeling beans from Latin America and Africa to the wider EU. Germany and the Netherlands leveraged their advanced logistics infrastructure and strategic geographic positioning to dominate re-export activities. Specialty cafés in the UK and France expanded their menus to include innovative offerings such as single-origin brews and plant-based milk options, catering to evolving consumer preferences. Meanwhile, Italy, drawing on its espresso legacy, popularized organic blends in independent bars, further solidifying its reputation as a coffee culture leader. Compliance lapses with the EUDR caused spot-price fluctuations, momentarily tightening supply. This led to a high-single-digit increase in café menu prices but also heightened consumer awareness regarding traceability, encouraging more informed purchasing decisions.

APAC Organic Coffee Market

Asia-Pacific is on a growth trajectory, boasting a 9.62% CAGR. This surge is bolstered by China, which introduced over 1,200 specialty cafés in Shanghai in 2025, reflecting the growing urban demand for premium coffee experiences. India’s modern trade shelf resets expanded organic SKUs by 28%, driven by increasing health consciousness and the rising availability of organic products in urban retail outlets. Japan saw a 14% rise in imports, driven by third-wave roasters in Tokyo and Osaka, who prioritized single-origin transparency to meet the demands of discerning coffee enthusiasts. In South Korea, the instant organic segment thrived due to its convenience appeal, particularly among busy urban professionals. Meanwhile, Australia experienced a 22% retail growth, fueled by millennials' preference for Fair Trade-verified products, as sustainability and ethical sourcing became key purchasing factors.

The Americas and MEA Organic Coffee Market

North America commanded a 28% share in 2025, with the U.S. accounting for a dominant 82% of the region's turnover. Retail giants like Whole Foods, Costco, and Trader Joe’s bolstered consumer choices by introducing direct-trade lines from Central America, which emphasized ethical sourcing and quality. A significant milestone was reached in Q3 2025 when online sales surpassed foodservice for the first time, enhancing price transparency and driving subscription growth. This shift was fueled by the convenience of e-commerce platforms and the growing popularity of subscription models offering curated coffee selections. South America, with a 12% share of global sales, witnessed a shift: domestic consumption in Brazil and Colombia now matches export growth, as the middle class increasingly opts for organic labels. This trend reflects a broader shift in consumer behavior, with local shoppers prioritizing quality and sustainability. The Middle East and Africa, though representing only 8% of the total, showcase vigorous growth in the UAE and South Africa, highlighted by a surge in re-export and private-label initiatives. These regions benefited from increasing investments in coffee processing facilities and the rising popularity of private-label brands among cost-conscious consumers.

Competitive Landscape

The organic coffee market is moderately concentrated. Global giants like Nestlé, JDE Peet’s, and Starbucks share the stage with regional craft players and vertically integrated cooperatives. Nestlé's acquisition of Blue Bottle's sourcing network reduced its dependence on commodity exchanges, yielding a 15% savings in procurement costs projected through 2028. This strategic move not only enhances cost efficiency but also strengthens control over supply chain operations, ensuring consistent quality and sustainability. Operational since December 2025, JDE Peet's EUR 45 million wet-mill in Guatemala offers oversight from bean to bag, cutting shipment lead times to Europe from three weeks to just five days. This facility enables the company to streamline its production process, improve product freshness, and respond more quickly to market demands. In a move emphasizing transparency, Starbucks and IBM introduced blockchain technology in 3,200 European outlets, allowing consumers to scan and access farm data. This initiative positions transparency as a key differentiator, fostering consumer trust and loyalty.

Technology start-ups are heightening the competition: Driftaway Coffee, utilizing IBM Food Trust, highlights roast dates and farmer profiles, prioritizing subscription freshness over traditional branding. This approach appeals to a growing segment of consumers who value freshness and traceability over legacy brand recognition. Smaller roasters, through accelerated patents on nitrogen-flushing for compostable pods, now match the shelf life of aluminum capsules, diminishing the advantages held by larger incumbents. This technological advancement levels the playing field, enabling smaller players to compete effectively in terms of product longevity. Retail prices are under pressure as supermarket private labels captured 18% of organic unit sales in 2025, up from 14% in 2024. This surge has pushed branded players to bolster investments in digital loyalty programs, exclusive micro-lots, and café events. These strategies aim to enhance customer engagement and differentiate branded products in an increasingly competitive market.

In the Asia-Pacific region, a lack of supply-chain transparency has allowed niche players to flourish by establishing direct-trade agreements, bypassing European importers. However, these players struggle with brand building due to limited scale, which restricts their ability to expand market presence and compete with larger players. Central American cooperatives are increasingly collaborating with ESG funds for organic transitions, securing advance purchase contracts that guarantee minimum price floors. These partnerships provide financial stability for cooperatives, enabling them to invest in sustainable farming practices and meet the growing demand for organic coffee. In summary, the industry's strategic focus is on vertical integration, traceability technology, and premium segmentation to maintain pricing power amidst growing private-label competition. These strategies are critical for navigating the evolving market dynamics and sustaining long-term growth.

Organic Coffee Industry Leaders

JDE Peet’s N.V.

Nestlé S.A.

Keurig Dr Pepper Inc.

Starbucks Corporation

Luigi Lavazza S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Organic Coffee Market Companies Covered in this Report

- JDE Peet's N.V.

- Nestle S.A.

- Keurig Dr Pepper Inc.

- Starbucks Corporation

- Luigi Lavazza S.p.A.

- Kicking Horse Coffee Co.

- Ecotone

- Tru Bru Coffee

- Burke Brands (Don Pablo)

- Rogers Family Co. (Organic Coffee Co.)

- Death Wish Coffee Co.

- Jim's Organic Coffee

- Dean's Beans Organic Coffee Co.

- Volcanica Coffee

- Camano Island Coffee Roasters

- Ethical Bean Coffee

- Fresh Roasted Coffee LLC

- West Berkshire Roastery

- Balance Coffee LTD.

- Cafe direct Group (Grumpy Mule)

Recent Industry Developments in Organic Coffee Market

- February 2026: Beach City Coffee has introduced its Fair Trade Organic whole bean coffee in over 350 Kroger locations nationwide, encompassing Ralphs and other Kroger banners. This expansion not only broadens the brand's retail presence but also makes ethically sourced, certified organic beans accessible to mainstream grocery shoppers.

- April 2025: In a strategic move, Four Sigmatic teamed up with Sony Pictures Consumer Products to unveil a special coffee blend, coinciding with the debut of HBO's "The Last of Us." Dubbed "The Last of Us High Caffeine Organic Ground Coffee," the blend featured organic Arabica dark roast beans, infused with cordyceps, lion's mane mushrooms, vitamin B12, and a natural coffee extract.

- February 2025: Artigiano, a coffee roaster and café chain based in Vancouver, has acquired Salt Spring Coffee, known for its focus on organic and sustainable coffee production. With this acquisition, Artigiano not only becomes Canada's second-largest organic-certified coffee roaster but also stands out as the sole supplier of Regenerative Organic Certified® beans. This move capitalizes on Salt Spring's strong reputation in ethical sourcing and commitment to environmental practices.

- February 2024: Nespresso Professional has broadened its Origins Organic lineup by introducing the Brazil Organic capsule. This new addition joins the ranks of its already available Peru, Congo, and Colombia variants. Sourced from Brazil's Cerrado Mineiro, Minas Gerais, and São Paulo regions, this single-origin Arabica blend boasts sweet toasted cereal and caramel notes, with subtle undertones of wood, nut, and spice. These beans were cultivated under Nespresso's AAA Sustainable Quality Program, which champions organic and regenerative farming practices. The program places a strong emphasis on soil health, composting, biocontrol methods, and minimizing chemical usage.

Global Organic Coffee Market Report Scope

The global organic coffee market is segmented as light, medium, and dark, based on the roast type. Based on origin, the organic coffee market is classified into Arabica and Robusta types. The market is also classified based on the distribution channel into supermarkets and hypermarkets, independent retailers, convenience stores, specialty stores, and others. Lastly, the organic market has been segmented by geography.

Segmentation Overview

| Arabica |

| Robusta |

| Whole Bean |

| Ground |

| Instant |

| Pods/Capsules |

| Sachets |

| Pouches |

| Jars |

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail | |

| Other Off-Trade Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Nigeria | |

| Saudi Arabia | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Origin | Arabica | |

| Robusta | ||

| By Product Form | Whole Bean | |

| Ground | ||

| Instant | ||

| Pods/Capsules | ||

| By Packaging Format | Sachets | |

| Pouches | ||

| Jars | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail | ||

| Other Off-Trade Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Nigeria | ||

| Saudi Arabia | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast size of the organic coffee market by 2031?

The organic coffee market size is expected to reach USD 14.12 billion by 2031, expanding at a 10.09% CAGR from 2026 to 2031.

Which origin currently leads volume sales?

Arabica retains volume leadership at 65.98% of 2025 shipments, although Robusta is the faster-growing origin.

How fast are pods and capsules growing?

Single-serve pods and capsules are advancing at an 11.24% CAGR through 2031, the quickest pace among all product forms.

Which region shows the highest growth momentum?

Asia–Pacific is the fastest-growing geography, recording a 9.62% CAGR through 2031 on rapid café expansion in China and India.

Page last updated on: