Cider Market Size and Share

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

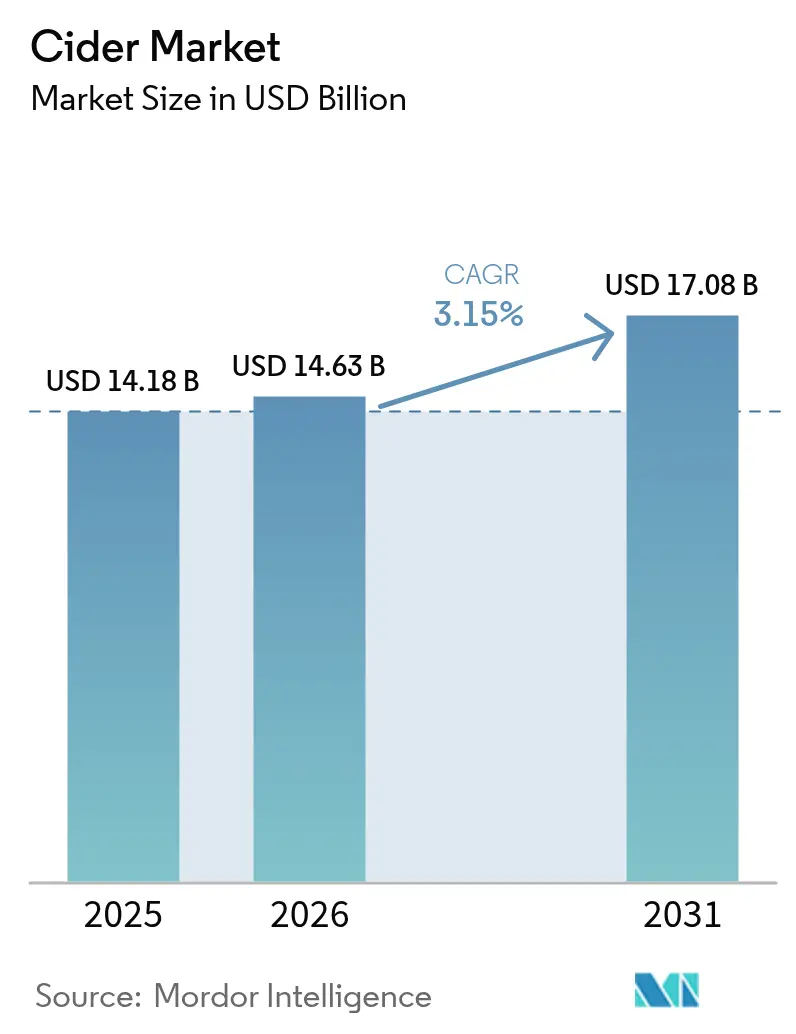

| Market Size (2026) | USD 14.63 Billion |

| Market Size (2031) | USD 17.08 Billion |

| Growth Rate (2026 - 2031) | 3.15% CAGR |

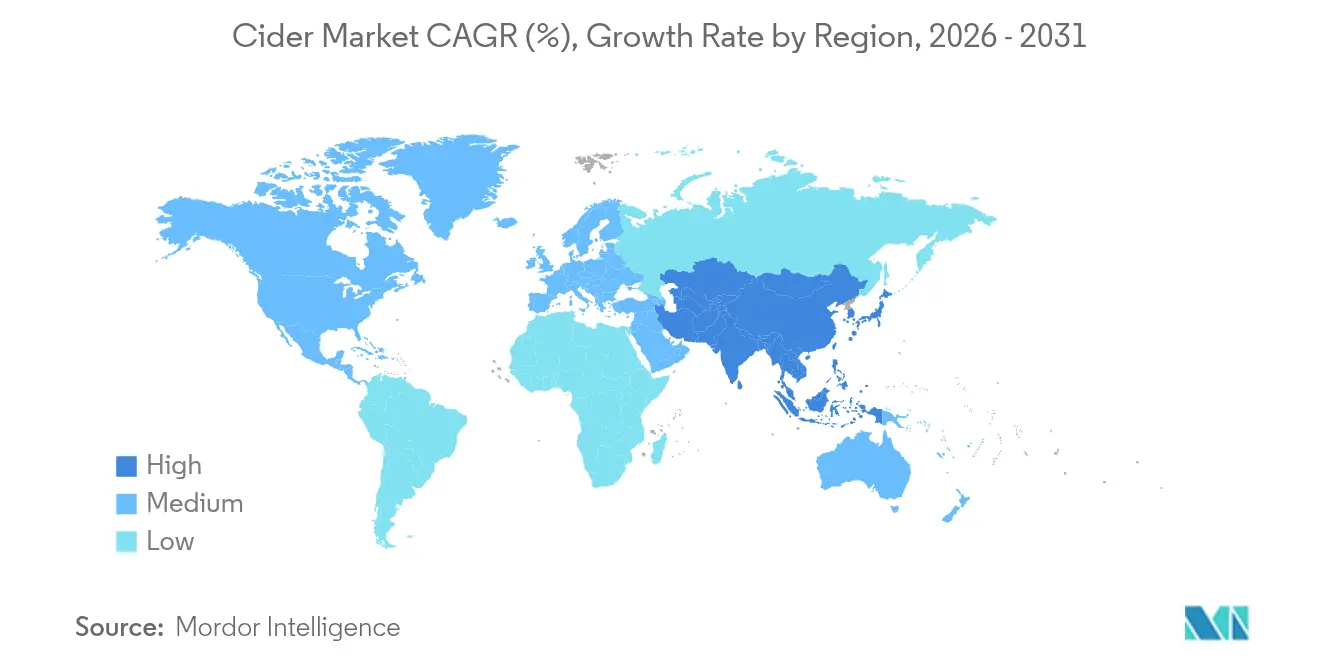

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

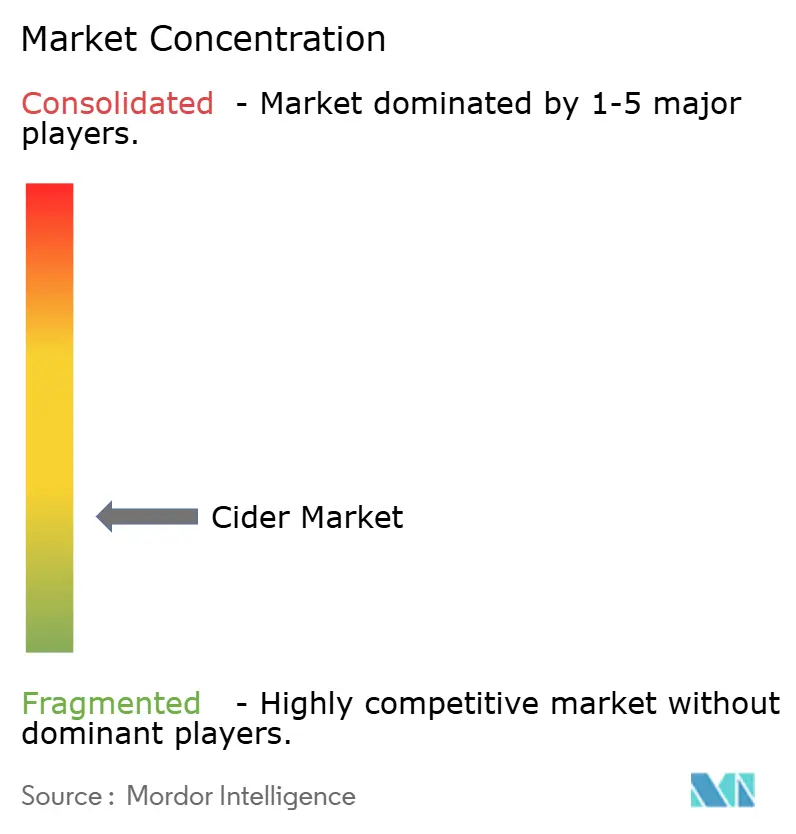

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cider Market Analysis by Mordor Intelligence

cider market size in 2026 is estimated at USD 14.63 billion, growing from 2025 value of USD 14.18 billion with 2031 projections showing USD 17.08 billion, growing at 3.15% CAGR over 2026-2031. The cider market is witnessing significant growth as younger consumers in urbanizing economies increasingly recognize cider as a lighter, fruit-forward alternative to beer. This growth is further supported by the category's maturation in legacy regions. The premium segment of the market strategically leverages its craft-oriented positioning, integrates functional ingredients, and emphasizes sustainability-focused messaging. These approaches collectively enhance brand loyalty, foster consumer engagement, and enable higher price realization. Despite the proliferation of competing ready-to-drink segments, the market continues to benefit from health-conscious moderation trends and cider's natural gluten-free attributes, which sustain steady demand. Additionally, innovations in packaging, particularly the shift toward cans, are driving new consumption occasions while addressing environmental sustainability concerns. These factors are becoming increasingly critical in shaping consumer purchasing behavior and influencing global cider market dynamics.

Key Report Takeaways

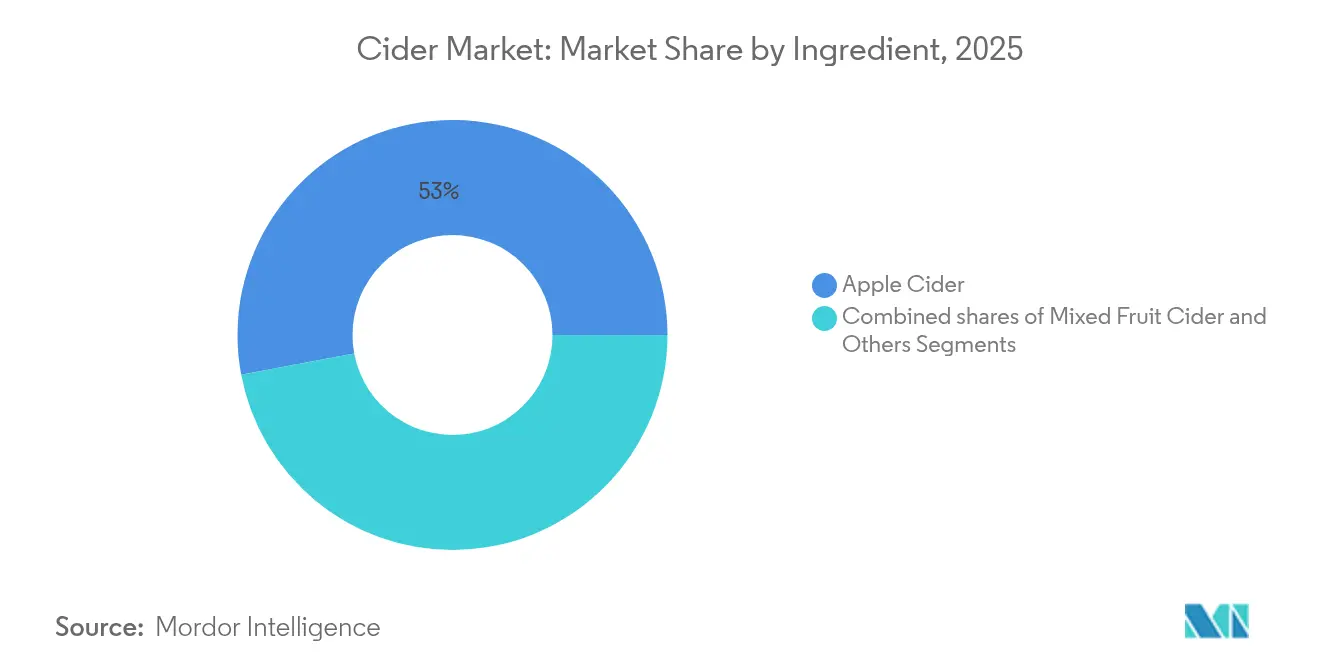

- By ingredient, apple cider led with 52.96% share of the cider market in 2025, while mixed fruit variants are projected to advance at a 3.42% CAGR through 2031.

- By alcohol content, the low-alcohol segment accounted for a 78.12% share of the cider market in 2025 and is expected to grow at a 3.65% CAGR to 2031.

- By packaging format, bottles retained 60.02% revenue share in 2025, whereas cans are forecast to expand at a 3.87% CAGR.

- By category, the mass segment held 72.02% market share in 2025, yet premium products are poised for 4.08% CAGR growth.

- By distribution channel, off-trade accounted for 65.01% market share in 2025; on-trade is set to rise at a 3.22% CAGR.

- By geography, Europe dominated with 43.05% revenue share in 2025, but Asia-Pacific is projected to achieve the fastest 4.48% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cider Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing demand for low-alcohol and health-conscious drinks | +0.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Innovation in flavors and seasonal offerings | +0.6% | Core in North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Growth of craft and artisanal alcohol movements | +0.5% | North America and Europe, emerging in Australia | Medium term (2-4 years) |

| Increased popularity of gluten-free and alternative alcohols | +0.4% | Global, led by developed markets | Long term (≥ 4 years) |

| Expansion of on-trade and social drinking culture | +0.3% | Asia-Pacific core, recovering in Europe and North America | Short term (≤ 2 years) |

| Product innovation with functional ingredients | +0.2% | North America and Europe early adoption, global rollout | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing demand for low-alcohol and health-conscious drinks

Shifting consumer preferences toward low-alcohol and health-conscious beverages are emerging as a significant growth driver in the hard cider market. The low-alcohol segment has gained a dominant position, supported by the rising influence of wellness campaigns that advocate for moderation in alcohol consumption. To meet this demand, producers are employing advanced production techniques, such as controlled fermentation and reverse osmosis, which effectively reduce ethanol content while preserving the beverage's flavor profile. This technological innovation has enabled the low-alcohol segment to achieve higher growth rates compared to traditional higher-ABV styles. Additionally, the integration of functional enhancements, including probiotic cultures and adaptogenic botanicals, is strengthening cider's appeal as a wellness-oriented beverage. These shifting consumer trends are creating lucrative opportunities for the development of premium low-ABV product lines and are expanding the occasions for cider consumption.

Innovation in flavors and seasonal offerings

In the intensely competitive hard cider market, smaller brands are strategically differentiating themselves by focusing on seasonal and fruit-forward recipes to attract and retain consumer interest. In the United States, the market experiences two prominent demand surges: one during summer social gatherings and the other during autumn harvest celebrations. Younger adult consumers, who prioritize unique experiences and prefer beverages with reduced bitterness, are increasingly gravitating toward innovative offerings such as barrel-aged ciders, wild-yeast fermentation techniques, and tropical fruit flavor integrations. These strategies not only enable brands to command premium pricing but also reposition cider as a versatile and contemporary beverage, effectively expanding its consumer base and moving beyond its traditional association with autumn in the global cider market. Furthermore, companies are intensifying their focus on product innovation and the introduction of flavored ciders. For instance, in October 2024, Farmland, in partnership with Minneapolis' Number 12 Cider, introduced a Maple Bacon-flavored Cider, strategically timed to align with the fall season and cater to evolving consumer preferences.

Growth of craft and artisanal alcohol movements

Consumers prioritizing authenticity are increasingly influenced by regional appellations and orchard-to-glass narratives. As of 2024, Australia has emerged as a significant player in the craft cider industry, with over 110 cider producers[1]Source: Cider Australia, “Submission to Standing Committee on Agriculture,” cideraustralia.org.au. This rapid expansion not only enhances local pride but also drives growth in the tourism sector. However, while this growth presents significant opportunities, it also introduces market fragmentation. Small-scale producers are capitalizing on their ability to source locally and utilize traditional production methods to distinguish themselves from mass-market competitors. By employing marketing strategies that emphasize the unique terroir of their regions, these producers are successfully positioning their products as premium offerings. The industry's focus on sustainability extends beyond production processes to include raw material sourcing. A current challenge is the limited availability of specialty cider apple varieties, which forces many producers to rely on lower-quality dessert apples or culls. This supply constraint creates opportunities for vertical integration, particularly for producers willing to invest in orchards dedicated to cider-specific apple cultivation. Furthermore, the integration of local branding with agritourism initiatives strengthens consumer engagement while contributing to rural economic development. This approach is especially beneficial in regions with a historical association with apple farming, where it supports traditional agricultural practices and fosters economic sustainability, reinforcing authenticity within the cider industry.

Increased popularity of gluten-free and alternative alcohols

The cider market is experiencing growth, driven by the increasing demand for gluten-free and alternative alcoholic beverages. Cider's gluten-free attribute provides a competitive advantage over traditional barley-based alcoholic drinks, appealing to the expanding base of health-conscious and food-sensitive consumers. Furthermore, the presence of apple-derived polyphenols, valued for their antioxidant properties, differentiates cider from high-sugar malt beverages. This differentiation enhances its positioning in health-focused retail channels and strengthens cider market positioning. Facilitates its entry into emerging non-traditional outlets, such as wellness cafés, aligning with the evolving consumer preference for healthier and innovative beverage options. In response to this trend, manufacturers are emphasizing product innovation. For instance, in February 2025, AVID Cider introduced its passion fruit tangerine hard cider, highlighting that all AVID ciders are gluten-free and made entirely from 100% fruit.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Limited penetration in traditional markets | -0.4% | Asia-Pacific and Middle East | Medium term (2-4 years) |

| Fluctuating Raw Material Prices | -0.3% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| High competition from RTD and flavored drinks | -0.5% | North America and Europe | Short term (≤ 2 years) |

| Stringent government regulations | -0.2% | Global, jurisdiction specific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited penetration in traditional markets

Limited penetration in traditional markets poses a significant challenge to the growth of the cider market, particularly in regions such as Asia and the Middle East. Cultural preferences and stringent licensing regulations continue to act as substantial barriers, restricting the category's expansion. In 2024, India implemented formal cider standards, which introduced additional complexities, including labeling requirements and excise compliance, further complicating market entry. Moreover, the dependence on three-tier distribution systems inflates operational costs and extends the payback period for new brands, discouraging investment unless high volumes can be achieved. Despite these challenges, the cider market holds growth potential, driven by favorable demographic shifts and rising disposable incomes. This potential could be unlocked further with the relaxation of import duties and the scaling up of local bottling operations across the global cider market.

High competition from RTD and flavored drinks

The cider market is encountering significant challenges due to the rising competition from ready-to-drink (RTD) beverages and flavored drinks. As of 2024, the Japan Soft Drink Association reported that carbonated drinks accounted for an 18.6% market share in Japan[2]Source: Japan Soft Drink Association, "Japan soft drink statistics 2025', www.j4ce.env.go.jp. These competing products are gaining a competitive edge by dominating retail shelf space with strong value propositions, such as zero sugar content and functional health benefits. To address this intensifying competition, cider brands operating within the Beyond-Beer segment are increasingly focusing on developing innovative flavors and implementing robust branding strategies. The traditional reliance on price differentiation is no longer sufficient to sustain market positioning. This competitive overlap is particularly pronounced among Gen Z consumers, who exhibit a strong preference for portable products and a wide variety of options. Companies that fail to adapt promptly to these shifting consumer demands and competitive pressures are at risk of losing market share in this rapidly evolving and highly dynamic market landscape.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient: Balancing Apple Heritage and Fruit Innovation

According to the cider market analysis, Apple Cider commands a dominant 52.96% market share in 2025, underscoring a strong consumer preference for traditional flavors and the expertise of leading manufacturers. Yet, it's the fruit-flavored variants that are surging ahead, boasting a robust 3.42% CAGR growth rate projected through 2031. This trend hints at a market shift towards flavor diversification and premium positioning. Meanwhile, Mixed Fruit Cider finds its niche, blending the familiar apple base with complementary fruits, catering to both traditionalists and the adventurous. Ingredient choices spotlight a strategic tug-of-war: producers grapple with upholding heritage authenticity while also venturing into modern flavor innovations, all in a bid to expand their market reach without compromising brand equity.

Specialty cider apple varieties remain in limited supply across major production regions, creating challenges for manufacturers. As a result, many producers are compelled to utilize dessert apple culls or juice concentrates instead of purpose-grown cider apples. Furthermore, fluctuations in apple pricing significantly impact production costs. Juice stock prices vary widely, ranging from USD 6.00 to USD 18.00 per hundredweight depending on the variety and quality. Meanwhile, juice apples sourced from Washington state command a premium price, ranging between USD 100.00 and USD 130.00 per ton, reflecting their higher demand and quality standards. Apple cider, though still leading in volume, is experiencing a slowdown in growth, attributed to market saturation and a limited flavor variety. Fruit-flavored ciders, with their sweeter and more approachable taste, align seamlessly with the trends of low-alcohol and gluten-free beverages, making them ideal for ready-to-drink formats.

By Alcohol Content: Low-ABV Formats Anchor Mindful Consumption

The Low Alcohol segment commands 78.12% market share in 2025 while simultaneously achieving the fastest growth at 3.65% CAGR, indicating both category dominance and internal expansion dynamics. This performance reflects strategic innovation by producers, who are developing advanced low-alcohol variants that deliver complex flavors while aligning with the preferences of health-conscious consumers. On the other hand, High Alcohol cider variants target niche markets that value stronger flavor profiles and traditional fermentation methods. However, these variants face challenges from increasing moderation trends and stricter regulatory measures. This segmentation aligns with the alcoholic beverage industry's broader shift toward mindful consumption, where lower alcohol content supports social drinking occasions without compromising on taste.

Regulatory developments increasingly support the low-alcohol category. The World Health Organization's SAFER initiative aims to reduce harmful alcohol use by 10% by 2025. Similarly, Canada's updated alcohol consumption guidelines advocate zero alcohol as the only risk-free option, creating favorable policy conditions for low-alcohol alternatives in North America. Production methods for low-alcohol cider, such as controlled fermentation, reverse osmosis for alcohol removal, and blending techniques, ensure the retention of organoleptic properties while reducing alcohol content. Although these processes require significant technical investment, they enable premium positioning within the health-conscious consumer segment.

By Packaging Format: Environmental Metrics Favor Aluminum

In 2025, bottles hold a 60.02% market share, highlighting consumer preference for traditional packaging and premium product positioning. Conversely, cans are experiencing faster growth, with a 3.87% CAGR, driven by sustainability benefits and convenience. Aluminum cans, offering superior and indefinite recyclability, appeal to environmentally conscious consumers. This shift in packaging formats reflects broader trends in the beverage industry. The increasing adoption of canned wine demonstrates growing consumer acceptance of alternative packaging for premium alcoholic beverages. While glass bottles excel in preserving flavor and maintaining a premium image, they face challenges such as higher shipping weight, breakage risks, and environmental concerns.

Packaging innovation now extends beyond material selection to address portion control and convenience, aligning with trends in moderation and social consumption. Smaller serving sizes cater to health-conscious consumers, while resealable packaging supports multi-occasion consumption. Advanced can coating technologies, such as Sherwin-Williams' valPure V70 non-BPA epoxy, ensure product integrity while meeting safety standards. Packaging format choices are increasingly influencing distribution channel strategies. Canned products are better suited for convenience retail and outdoor consumption, while bottled variants retain an edge in premium on-premise establishments. With 85% of consumers considering environmental factors in purchasing decisions, recyclable packaging formats gain a competitive advantage in the global cider market through sustainability positioning.

By Category: Premium Momentum Challenges Mass Majority

Mass market cider maintains 72.02% market share in 2025, reflecting price-sensitive consumer behavior and established distribution relationships with major retailers. Meanwhile, the premium category's 4.08% CAGR indicates a shift in consumer demand toward higher-quality products, craftsmanship, and unique flavor profiles that justify premium pricing. Market segmentation highlights a clear divide: mass producers focus on competitive pricing and broad availability, while premium brands differentiate through artisanal production techniques, local sourcing, and innovative flavor offerings. This market dynamic presents strategic opportunities for mid-tier brands to position themselves by balancing affordability with a perception of quality.

Premiumization trends are driven by consumers' willingness to pay for products with sustainable attributes. Local sourcing and terroir-focused marketing strengthen premium positioning, particularly in regions with a strong apple-growing heritage and established craft beverage industries. However, the premium segment faces challenges such as limited distribution networks and the need to educate consumers, as cider lacks the well-defined quality hierarchies present in wine and spirits. Innovations in the premium cider segment, including barrel aging, wild yeast fermentation, and single-variety apple offerings, provide avenues for differentiation. The evolution of the cider category aligns with broader craft beverage trends, where smaller producers leverage authenticity and craftsmanship to compete effectively with larger manufacturers, despite resource constraints.

By Distribution Channel: Digital Savvy Complements On-Trade Revival

Off-Trade continued to lead with 65.01% of hard cider market size in 2025 as grocery and convenience retail remained convenient pandemic habits. On-Trade channels are experiencing a faster growth rate of 3.22% CAGR, supported by the recovery of social drinking occasions. Supermarkets and hypermarkets within the off-trade segment leverage cider's positioning as a grocery product rather than a niche alcoholic beverage, enhancing consumer accessibility and encouraging impulse purchases. Specialty stores focus on premium and craft cider offerings, providing curated experiences and education that drive higher-margin sales. Online retail platforms cater to convenience-oriented consumers and enable direct-to-consumer sales, bypassing traditional distribution challenges.

The evolution of distribution channels reflects broader changes in the alcoholic beverage industry, with digital platforms increasingly influencing purchasing decisions, even for products ultimately acquired through traditional outlets. The on-trade segment benefits from cider's alignment with social consumption trends and seasonal marketing strategies that capitalize on outdoor dining and festival opportunities. Variations in direct-to-consumer shipping regulations across states create compliance complexities but also allow premium producers to directly engage with consumers and secure higher profit margins. The U.S. three-tier distribution system poses barriers for smaller producers, favoring established brands with strong distributor relationships. E-commerce, which saw significant growth during the pandemic, continues to expand, with digital platforms playing a critical role in brand discovery and consumer education, even when final purchases occur through traditional retail channels, boosting cider market sales visibility.

Geography Analysis

In 2025, the global cider market, Europe maintained its dominant position with a 43.05% market share, driven by the well-established cider traditions in key markets such as the United Kingdom, Spain, and Ireland. However, the region's high excise tax regimes continue to pose challenges for small-scale producers, limiting their ability to expand. Despite these constraints, major industry players like Heineken are leveraging innovation to sustain growth. For instance, Heineken’s Inch’s series aligns with evolving consumer preferences by incorporating sustainability narratives, thereby strengthening its market presence.

The Asia-Pacific region is positioned as the fastest-growing geography, recording a robust compound annual growth rate (CAGR) of 4.48%. Mainland China, with its emerging consumer base, is demonstrating a strong appetite for diverse and innovative flavor profiles, creating significant opportunities for market expansion. In India, recent regulatory developments that differentiate between soft and hard cider have created a more structured market environment. This regulatory clarity is enabling new entrants to follow the path of early movers like Thirsty Fox, which has successfully capitalized on this evolving landscape.

North America plays a pivotal role in driving the global cider market. In the U.S., consolidation of distribution channels is pushing smaller producers to focus on taproom sales and agritourism. Treasury Department-led competition studies are advocating franchise law reforms, which could reshape the competitive landscape. In Canada, producers benefit from abundant dessert-grade apples and favorable excise tax policies on lower-alcohol fruit wines, enhancing cost competitiveness. In Mexico, the United States-Mexico-Canada Agreement (USMCA) offers growth opportunities, but high slotting fees from dominant chain retailers remain a barrier for smaller players. In South America, rising demand for premium beverages and the growth of local craft cider are driving the market, though economic instability and weak distribution networks limit expansion. In the Middle East and Africa, the market is nascent but supported by a growing expatriate population and evolving preferences. However, strict regulations and cultural restrictions on alcohol sales continue to cap growth.

Competitive Landscape

The cider market landscape is characterized by a fragmented structure, driven by the presence of numerous regional and global players. Major players, including Heineken N.V., Carlsberg Group, C and C Group Plc, Anheuser-Busch InBev, and Molson Coors Beverage Co., are focusing on product innovation and expanding their portfolios to bolster their market positions and seize a larger share of the market. These companies are leveraging strategies such as introducing new flavors, targeting niche consumer segments, and investing in marketing campaigns to enhance brand visibility. Additionally, they are exploring sustainable production practices and premium product offerings to align with evolving consumer preferences and strengthen their competitive edge.

Cider market dynamics favor regional leaders over global dominance. Heineken's extensive cider portfolio capitalizes on scale efficiencies, achieving 2% organic growth in 2024 to reach 8 million hectoliters. The Savanna brand has shown strong performance in South Africa, driven by innovations such as premium whisky-flavored variants. Strategic initiatives focus on local sourcing, craft-oriented positioning, and seasonal marketing to differentiate cider offerings from mass-market beer and wine alternatives.

Growth opportunities are emerging in areas such as functional ingredient integration, sustainable packaging solutions, and penetration into emerging markets where regulatory environments are more favorable to new entrants compared to established alcohol categories. Technology adoption within the sector emphasizes fermentation control, quality assurance, and supply chain optimization, with producers combining traditional methods with modern quality control systems. Smaller producers are leveraging direct-to-consumer channels and agritourism to gain a competitive edge, while larger players utilize extensive distribution networks and marketing capabilities to maintain their market presence.

Cider Industry Leaders

-

Heineken N.V.

-

Anheuser-Busch InBev

-

Molson Coors Beverage Co.

-

Carlsberg Group

-

C and C Group Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Blake's Hard Cider partnered with Carhartt to launch American Apple initiative supporting farmers and combating food waste, reflecting growing industry focus on sustainability and community engagement.

- March 2025: Heineken UK has unveiled two fresh variants under its Inch's cider brand. The new offerings include Inch's Clou (dyABV 4.0%) and Inch's 0.0, marking the debut of the first dealcoholised cider in the UK market. These new SKUs are now available at convenience stores, wholesalers, and supermarkets.

- October 2024: AleSmith Brewing Company has expanded its year-round product portfolio with the launch of its premium Hard Cider. Demonstrating its dedication to quality and innovation, the company introduced its Traditional Dry Apple Cider, crafted using fresh-pressed apples sourced from the West Coast.

- May 2024: Budweiser Brewing Group (BBG) has unveiled Brutal Fruit Cider, targeting women and younger adult drinkers. The premium cider is now offered in 4x330ml can multipacks and 500ml bottles.

Global Cider Market Report Scope

The Global Cider Market is segmented, based on product type, distribution channel, and geography. On the basis of product type, the cider market has been segmented into flavored and plain cider. By distribution channel, the market has been segmented into specialty stores, supermarkets/hypermarkets, and others. By geography, the cider market has been classified by North America, Europe, Asia-Pacific, South America, and Middle East & Africa. The report analyzes the recent trends, drivers, and challenges affecting the market. Additionally, various factors that are instrumental in changing the market scenario are identified, along with prospective opportunities and key trends that can influence the market.

| Apple Cider |

| Mixed Fruit Cider |

| Others |

| Low Alcohol |

| High Alcohol |

| Bottles |

| Cans |

| Mass |

| Premium |

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Stores | |

| Others Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Ingredient | Apple Cider | |

| Mixed Fruit Cider | ||

| Others | ||

| By Alcohol Content | Low Alcohol | |

| High Alcohol | ||

| By Packaging Format | Bottles | |

| Cans | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Others Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the hard cider market?

The global market stands at USD 14.63 billion in 2026 and is forecast to reach USD 17.08 billion by 2031.

Which region is growing fastest?

Asia-Pacific leads growth with a projected 4.48% CAGR through 2031, driven by rising demand in China and Australia.

Why is low-alcohol cider gaining traction?

Wellness trends and moderation campaigns have pushed the low-alcohol segment to 78.12% share while still expanding at 3.65% CAGR.

How are packaging preferences shifting?

Glass bottles retain 60.02% share, yet aluminum cans are growing quicker at 3.87% CAGR thanks to recyclability and lighter weight.

What is driving premiumization in the category?

Consumers are paying more for organic, single-variety, and barrel-aged ciders, propelling premium products at a 4.08% CAGR.

Page last updated on: