Online Apparel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 438.16 Billion |

| Market Size (2031) | USD 544.72 Billion |

| Growth Rate (2026 - 2031) | 4.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Online Apparel Market Analysis by Mordor Intelligence

The online apparel market size is projected to expand from USD 420.7 billion in 2025 and USD 438.2 billion in 2026 to USD 544.7 billion by 2031, registering a CAGR of 4.5% between 2026 and 2031. This growth rate points to a market that is still adding value, but is now moving through a more mature digital phase in North America and Europe. At the same time, the online apparel market continues to gain support from first-time and repeat digital shoppers in South and Southeast Asia, where mobile-led buying keeps widening the addressable base. Social content, app-based browsing, and faster checkout paths are tightening the distance between inspiration and purchase, which is raising the value of responsive merchandising and flexible inventory in the online apparel market. Brands are also putting more capital into owned digital systems to recover margin and collect first-party customer data, a shift visible in Inditex’s FY2025 online performance and its 2026 investment plan for technology and platform improvement. The online apparel market remains fragmented, so companies that can manage pricing, returns, data, and operating complexity at the same time are better placed to gain share through 2031.

Key Report Takeaways

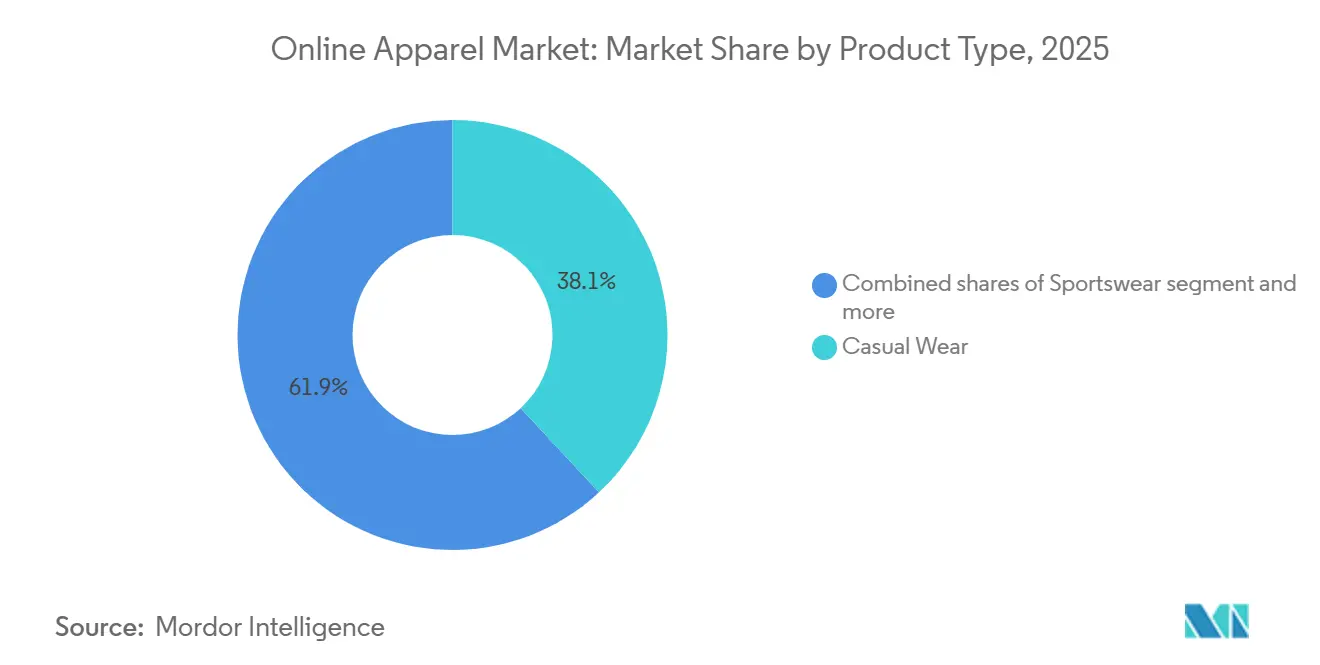

- By product type, casual wear led with 38.06% revenue share in 2025, while sportswear is forecast to expand at a 6.35% CAGR through 2031.

- By end-user, women held 52.33% of revenue in 2025, while children recorded the highest projected CAGR at 5.62% through 2031.

- By fabric material, cotton accounted for 42.38% of revenue in 2025, while nylon is advancing at a 5.38% CAGR through 2031.

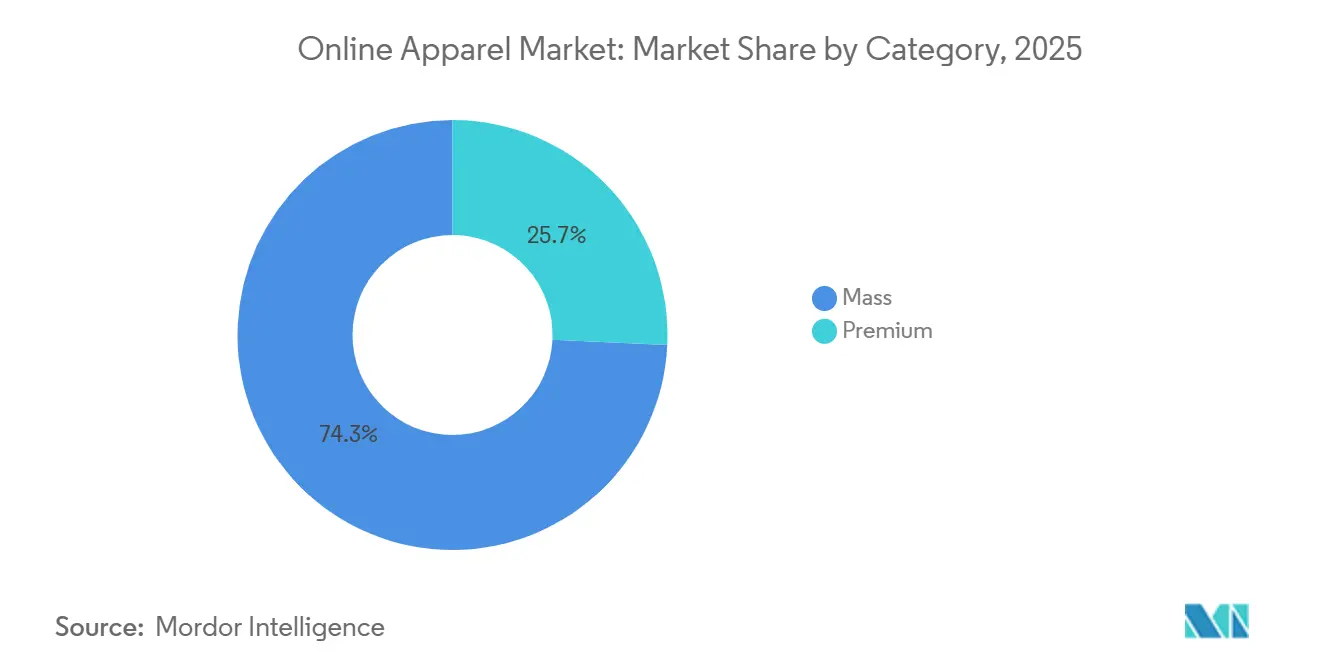

- By category, mass held 74.26% revenue share in 2025, while premium is projected to grow at a 5.81% CAGR through 2031.

- By distribution channel, third-party retailer platforms held 67.88% revenue share in 2025, while company-owned platforms are forecast to expand at a 7.25% CAGR through 2031.

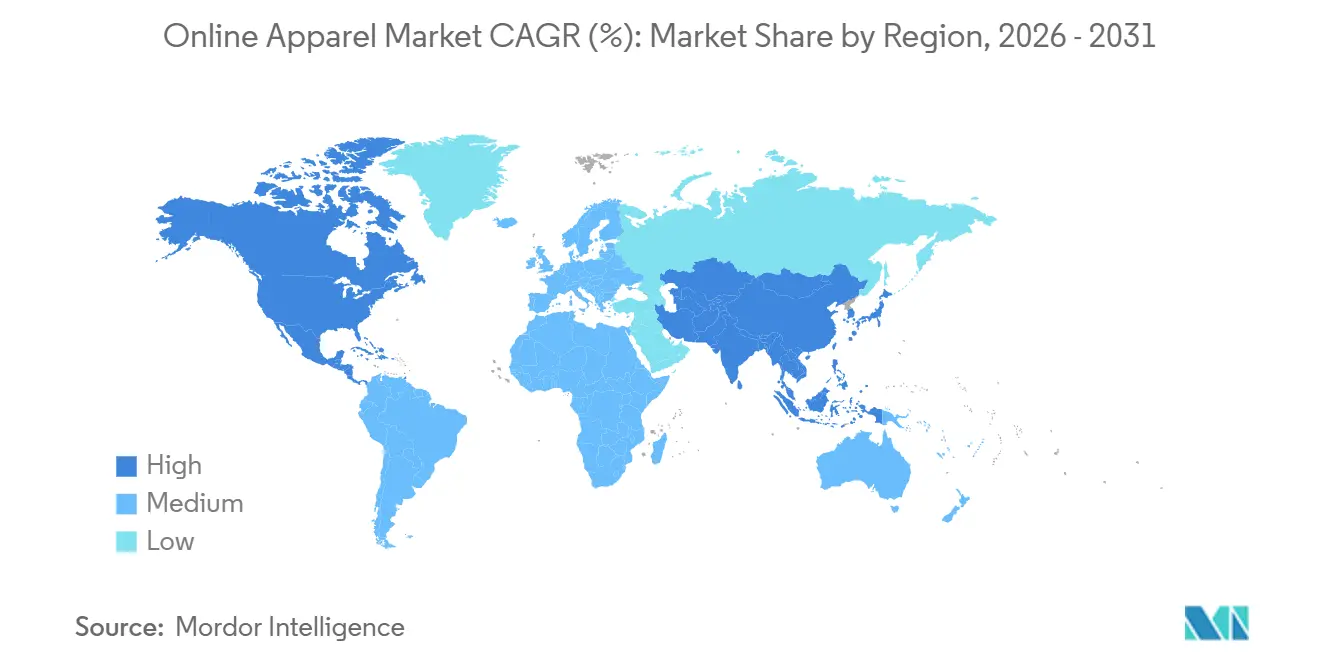

- By geography, Asia-Pacific led with 34.81% revenue share in 2025 and is also the fastest-growing regional cluster with a 6.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Online Apparel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Influence of Social Media Fashion Trends | +1.0% | Global, highest in Asia-Pacific and North America | Short term (≤ 2 years) |

| Expansion of Mobile Commerce and Shopping Apps | +0.9% | Global, highest in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Frequent Discounts and Promotional Pricing Strategies | +0.6% | Global, strongest in mass segments | Short term (≤ 2 years) |

| Easy Product Comparison Across Multiple Brands | +0.4% | North America and Europe, growing in Asia-Pacific | Medium term (2-4 years) |

| Convenient Return and Exchange Policies Boosting Purchases | +0.5% | North America and Europe | Medium term (2-4 years) |

| Increasing Adoption of Omnichannel Retail Models | +0.7% | North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Influence of Social Media Fashion Trends

Social platforms now shape a large part of how consumers discover clothing, compare looks, and complete purchases in the online apparel market. The shift matters because the same channel can now handle inspiration, recommendation, and checkout without forcing shoppers to move across several sites. That shortens the buying cycle and makes creator partnerships more important for brands that need quick visibility in crowded fashion categories. It also puts pressure on merchandising teams, because trend cycles now move faster and leave less time for seasonal planning in the online apparel market. Brands with flexible sourcing and faster content refresh rates are in a better position to turn rising attention into conversion. Brands that still depend on slower planning calendars face a clear disadvantage when social-led demand shifts within days.

Expansion of Mobile Commerce and Shopping Apps

Mobile devices are now central to browsing and purchasing behavior in the online apparel market, especially where younger shoppers spend more time inside brand apps, marketplace apps, and short-video feeds. This shift favors interfaces that reduce friction, store payment details, and keep product discovery active through push notifications and personalized feeds. It also raises the importance of app retention, because the winning platform is often the one that stays on the customer’s home screen rather than the one that ranks highest in search. Japan offers a clear signal of this transition, as apparel e-commerce penetration reached 23.38% in 2024, almost double the 2019 level [1]Source: METI Ministry of Economy, Trade and Industry, "Apparel E-Commerce", meti.go.jp . That pattern shows how even developed digital markets still have room for deeper online penetration when user habits shift toward app-led buying. In the online apparel market, stronger mobile engagement also helps brands test faster launches, dynamic pricing, and more precise product recommendations.

Frequent Discounts and Promotional Pricing Strategies

Promotional pricing has become a structural part of the online apparel market, especially because the mass category represented 74.26% of revenue in 2025 and keeps price sensitivity high. Discounts remain effective because consumers can compare alternatives quickly and move between brands with very little effort. This makes price events useful for volume generation, but it also creates steady pressure on margin quality when promotions become too frequent. Adidas’ 2025 annual report made that tradeoff clear, as the company pointed to the need to reduce promotional intensity and improve pricing discipline while continuing to expand digital demand. In practice, that means the best operators in the online apparel market will be the ones that use promotions selectively rather than as a permanent demand substitute. Brands with first-party data from owned channels are better placed to personalize offers and protect margin than brands that depend fully on third-party platforms.

Increasing Adoption of Omnichannel Retail Models

Omnichannel retail has become more important in the online apparel market because shoppers increasingly expect smooth movement between stores, apps, websites, delivery, and returns. That expectation improves the value of unified inventory visibility, shared customer profiles, and consistent promotions across channels. It also strengthens the role of physical locations, because stores can support pickup, exchange, and last-mile fulfillment rather than acting only as selling points. Inditex showed the scale of this model in FY2025, when online sales reached EUR 10.7 billion, and the group then directed EUR 2.3 billion of 2026 capital expenditure toward technology and online platform improvement. In the online apparel market, omnichannel strength is now closely tied to data quality because integrated systems make personalization and demand planning more reliable. The longer-term benefit is stronger loyalty, since shoppers are less likely to leave a brand when digital and physical touchpoints work as one system.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit Apparel Products Reducing Consumer Trust | -0.6% | Global, peak impact in North America and Europe | Short term (≤ 2 years) |

| Size And Fit Uncertainties In Online Purchases | -0.5% | Global, highest in North America and Europe | Medium term (2-4 years) |

| Data Privacy and Cybersecurity Concerns Among Shoppers | -0.4% | Global, highest in North America and Europe | Long term (≥ 4 years) |

| Growing Concerns Over Sustainability And Packaging Waste | -0.3% | Europe, North America, and consumer-driven parts of Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit Apparel Products Reducing Consumer Trust

Counterfeit exposure continues to weaken trust in the online apparel market because shoppers often discover fake products inside the same digital environments where legitimate brands are trying to build demand. A 2025 counterfeit-focused session hosted by the American Apparel & Footwear Association showed that 61% of buyers of fake goods did so unintentionally, and 52% of those unintentional purchases were fake fashion items [2]Source: American Apparel & Footwear Association, "Webinar: Where & How Counterfeiters Target Fashion Shoppers in 2025", americanimageawards.org. Pew Research Center also found that 17% of U.S. adults bought a counterfeit product online and were not refunded, while 85% saw online shopping scams as a significant problem. The damage extends beyond a single order because a poor counterfeit experience can lower repeat buying and reduce trust in the broader online apparel market. The European Union Intellectual Property Office also identified clothing as one of the most frequently seized counterfeit categories in global fake trade flows [3]Source: European Union, "Mapping Global Trade in Fakes 2025", europa.eu. Brands and platforms that invest more heavily in seller verification, monitoring, and fast takedowns will be better able to protect conversion and repeat purchase rates.

Size and Fit Uncertainties in Online Purchases

Fit remains one of the clearest sources of friction in the online apparel market because the customer cannot test shape, stretch, drape, or comfort before payment. That problem is costly because returns in apparel are already high, and each return adds reverse logistics cost, markdown risk, and customer service effort. The National Retail Federation stated that total U.S. retail returns are expected to reach USD 849.9 billion in 2025, with apparel and footwear posting return rates above 30%, the highest among major categories. In the online apparel market, repeated fit failures can also reduce customer confidence and make shoppers delay purchases or shift toward easier-to-fit products. This is why virtual fitting, size guidance, and clearer product information are moving from optional features to core conversion tools. The brands that reduce fit uncertainty more effectively are likely to protect margin, lower return rates, and retain customers longer.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Casual Wear Anchors Volume, Sportswear Claims the Growth Premium

Casual wear held 38.06% of the online apparel market share in 2025, which kept it firmly ahead of all other product groups in current revenue terms. That lead came from its broad use case, because casual clothing fits remote work, hybrid routines, travel, and everyday wear without requiring high wardrobe specialization. It also benefits from deeper SKU breadth, more frequent replenishment, and a lower decision threshold for many repeat buyers. In the online apparel market, casual wear works especially well with search, filtering, and recommendation tools because consumers often browse by style, price, and color rather than by a formal occasion. The size of this segment gives it a stabilizing effect on overall revenue, even when fashion cycles shift quickly.

Sportswear is forecast to grow at a 6.35% CAGR from 2026 to 2031, which places it ahead of the overall growth pace of the online apparel market. That premium is supported by rising overlap between performance wear and everyday style, which keeps the category relevant beyond gym or training use. Mordor Intelligence also noted that the broader sports apparel space is expected to grow strongly through 2031, with online channels showing particularly strong traction among digital-first consumers. Formal wear is recovering more gradually, because event-led demand tends to be less frequent and more fit-sensitive. Nightwear, loungewear, and intimate apparel remain important because they attract repeat buying and can be easier to standardize in digital selling. Across the online apparel market, brands with a balanced mix of casual, sports, and replenishment-driven items are likely to manage volatility better than brands that depend heavily on occasion-led demand.

By End-User: Women Lead Revenue, Children Drive the Forward Momentum

Women held 52.33% of revenue in 2025, which made this the largest end-user group in the online apparel market by a wide margin. That scale reflects wider assortment depth, higher browsing frequency, and stronger engagement across value, premium, and trend-driven categories. Women’s apparel also benefits from more varied purchase missions, including workwear, casualwear, occasionwear, intimate apparel, and athleisure. In the online apparel market, this range creates more search and recommendation opportunities, which support basket building and repeat visits. It also gives platforms and brands a broader base for promotions, loyalty programs, and creator-led campaigns.

Children’s apparel is forecast to expand at a 5.62% CAGR through 2031, which gives it the strongest growth outlook within end-user segmentation. The demand pattern is supported by recurring replacement cycles, because children outgrow sizes quickly and require more frequent wardrobe updates than adults. Mordor Intelligence also highlighted that the children’s wear segment is expected to post strong growth through 2031, supported by rising online adoption and digital tools that can ease fit-related hesitation. Men’s apparel continues to advance steadily, with online adoption helped by growing interest in athleisure, basics, and easier replenishment purchases. Across the online apparel market, the end-user mix increasingly rewards brands that can combine convenience with strong size guidance and quick product discovery.

By Fabric Material: Cotton Holds Volume Dominance, Nylon Leads Performance-Driven Growth

Cotton held 42.38% of revenue in 2025, which kept it the largest fabric group in the online apparel market by current value. Its lead came from familiarity, comfort, broad price accessibility, and its use across casualwear, basics, intimate apparel, and children’s clothing. Cotton also supports wide assortment planning, because brands can apply it across multiple silhouettes and seasons without forcing a narrow product identity. In the online apparel market, that versatility matters because consumers often search across categories rather than shopping only for one fabric type. The result is a material base that helps stabilize volume across both mass and premium ranges.

Nylon is projected to grow at a 5.38% CAGR through 2031, which places it ahead of the overall growth pace of the online apparel market. This reflects its close link to sportswear, swimwear, and technical categories, where moisture control, stretch support, and durability carry more weight in the buying decision. As performance-driven categories gain more digital visibility, nylon benefits from the same shift toward comfort and utility that is lifting activewear demand. Polyester and denim remain important in the broader mix, with polyester valued for efficiency and denim supported by its lasting place in casual wardrobes. Recycled nylon variants are also gaining more commercial attention as brands try to connect product performance with stronger environmental positioning.

By Category: Mass Market Owns the Volume, Premium Segment Captures Value Growth

The mass segment accounted for 74.26% share of the online apparel market size in 2025, which confirms that value-oriented demand remains the dominant force in current online spending. This scale reflects broad consumer price sensitivity, strong marketplace traffic, and the appeal of frequent assortment refreshes at accessible price points. It also explains why discounting remains so influential in the online apparel market, since high-volume digital traffic often responds quickly to visible price changes. The mass segment benefits from reach, but it also faces the strongest margin pressure because many sellers compete on speed and price at the same time. That makes operating discipline just as important as customer acquisition.

The premium segment is forecast to grow at a 5.81% CAGR through 2031, which places it above the overall growth rate of the online apparel market. This growth comes from rising digital comfort among aspirational consumers, stronger brand-direct experiences, and improved product presentation online. Premium brands are also benefiting from digital tools that help explain quality, fit, and styling more clearly, which reduces the gap between physical and online selling. At the same time, the line between mass and premium is becoming less rigid as value players use collaborations and limited drops, while premium brands selectively use digital promotions to widen reach. The brands best positioned here are the ones that can protect brand perception while still staying visible and easy to shop online.

By Distribution Channel: Third-Party Platforms Command the Present, DTC Owns the Future

Third-party retailer platforms held 67.88% of revenue in 2025, which kept them as the largest route to purchase in the online apparel market. Their lead comes from assortment scale, trusted search behavior, integrated logistics, and the convenience of comparing many brands in one place. These platforms also lower discovery friction, especially for consumers who start with price, reviews, or marketplace familiarity rather than with a specific brand. In the online apparel market, this creates a strong current advantage for marketplaces and multi-brand platforms that can capture broad browsing traffic. The channel is therefore likely to remain important even as brand-owned digital stores gain ground.

Company-owned platforms are forecast to grow at a 7.25% CAGR through 2031, making them the fastest-growing slice of the online apparel market size over the forecast period. Their advantage goes beyond margin because they give brands direct access to customer behavior, stronger control over merchandising, and more room for loyalty and subscription design. Inditex’s 2026 investment plan and its FY2025 online performance show how major apparel groups are still building this capability aggressively. Japan’s apparel e-commerce penetration also points to deeper room for digital channel expansion as brand and platform ecosystems continue to mature. Over time, the online apparel market is likely to reward brands that can balance the reach of third-party platforms with the data and brand control of owned channels.

Geography Analysis

Asia-Pacific accounted for 34.81% share of the online apparel market size in 2025, and it is projected to grow at a 6.31% CAGR through 2031, which makes it both the largest and fastest-growing regional block. China remains the anchor within this region because of its deep platform ecosystem, high comfort with digital fashion buying, and the growing role of content-led commerce. India adds another layer of expansion potential because digital retail penetration is still lower than in China, which leaves more room for first-time online apparel adoption. Southeast Asia also supports regional growth, with fashion demand tied closely to mobile usage, flash sales, and influencer-driven discovery. Japan shows that even mature regional markets still have runway, as apparel e-commerce penetration reached 23.38% in 2024.

North America and Europe formed the second and third largest regional clusters in 2025, and both parts of the online apparel market are marked by strong digital infrastructure and a more mature buying base. These markets still deliver large revenue pools, but growth is more measured because digital shopping habits are already well established. Competition in these regions is intense, especially where discounting, fast delivery expectations, and easy returns have become standard customer assumptions. Europe also faces added operating pressure from tighter packaging and compliance requirements, which can raise cost for cross-border fashion sellers that depend on high shipment volume. In practical terms, this means the online apparel market in North America and Europe is less about first-time digital migration and more about retention, efficiency, and share shifts between platforms and brands.

South America and MEA are smaller in current value, but they offer more open runway for platform expansion and mobile-led wallet growth in the online apparel market. These regions benefit from a younger digital user base in many countries, and that often makes app-first discovery especially important for apparel. In MEA, fashion and apparel represented 25.96% of B2C e-commerce product revenue in 2025, which shows how central this category already is to regional online demand. South America and MEA also give regional and local brands room to compete with global players through localized content, payment flexibility, and faster adaptation to local style cues. That makes both regions important long-term opportunity zones for the online apparel market, even if their present scale still trails the larger established regions.

Competitive Landscape

The online apparel market remains fragmented, and competition is shaped more by execution speed, assortment control, and customer data than by simple corporate size. No single company defines the category across all regions, which leaves room for different models to win in different price tiers and channel formats. One group of competitors is built around very fast trend response, low prices, and short product cycles. Another group relies on vertically integrated operations, stronger brand control, and tighter links between physical retail and digital selling. This split explains why the online apparel market supports both marketplace-oriented scale players and brand-led omnichannel groups at the same time.

Inditex remains a strong example of the integrated model, as FY2025 online sales reached EUR 10.7 billion and the company directed EUR 2.3 billion of 2026 capex toward technology and platform improvement. The December 2025 launch of Zara Try-On also showed how leading brands are using digital tools to reduce fit friction and keep traffic inside owned channels. Adidas is following a related path, with its 2025 annual report highlighting 15% DTC e-commerce growth and a stronger focus on better pricing discipline, inventory planning, and AI-supported execution. Nike offers a useful counterpoint, because NIKE Brand Digital revenue declined 9% in fiscal Q3 2026, which underlined the risk of relying too heavily on one channel mix. Taken together, these moves show that leadership in the online apparel market now depends on balancing reach, brand control, and channel health.

The next phase of competition is likely to bring more portfolio reshaping and capability-led deals rather than simple scale buying. eBay’s announced acquisition of Depop in February 2026 showed how major digital players are using fashion resale and younger user communities to deepen engagement. G-III Apparel Group’s May 2026 agreement with WHP Global around Marc Jacobs also reflected the same search for stronger brand control and long-term operating leverage. OTB’s June 2026 acquisition of Viktor&Rolf and Kering’s June 2026 partnership with ICCF further showed that portfolio design remains active in premium fashion as companies look to widen reach and deepen brand positioning. For the online apparel market, this means competitive pressure will keep rising not only from product and price, but also from ownership of technology, customer data, and distinctive brand assets.

Online Apparel Industry Leaders

-

Nike, Inc.

-

Adidas AG

-

Puma SE

-

Lululemon Athletica Inc.

-

PVH Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: G-III Apparel Group signed a definitive agreement with WHP Global to form a 50/50 joint venture owning Marc Jacobs' intellectual property, with G-III acquiring the global operating business and WHP managing licensing operations, a deal that restructures the brand's go-to-market model for long-term scale.

- June 2026: OTB Group completed the acquisition of 100% of Viktor&Rolf, adding the Haute Couture Maison to a portfolio that includes Diesel, Jil Sander, Maison Margiela, and Marni, broadening its premium digital and wholesale fashion reach.

- December 2025: Inditex launched Zara Try-On, an AI-based virtual fitting system available in 43 markets, generating over 7 million user sessions within weeks and representing a scalable attempt to reduce fit-driven returns

Global Online Apparel Market Report Scope

The market includes the online purchase of apparel across various categories, such as casual wear, formal wear, sportswear, and other products sold as part of apparel offerings. The Online Apparel Market Report is Segmented by Product Type (Formal Wear, Casual Wear, Sportswear, and More), End-User (Men, Women, and More), Fabric Material (Cotton, Polyester, and More), Category (Mass and Premium), Distribution Channel (Third-Party Retailer Platform and Company-Owned Platform), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Formal Wear |

| Casual Wear |

| Sportswear |

| Nightwear/Loungewear |

| Intimate |

| Other Product Types |

| Men |

| Women |

| Children |

| Cotton |

| Polyester |

| Nylon |

| Denim |

| Other Fabric Types |

| Mass |

| Premium |

| Third-Party Retailer Platform |

| Company-Owned Platform |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Formal Wear | |

| Casual Wear | ||

| Sportswear | ||

| Nightwear/Loungewear | ||

| Intimate | ||

| Other Product Types | ||

| End-User | Men | |

| Women | ||

| Children | ||

| Fabric Material | Cotton | |

| Polyester | ||

| Nylon | ||

| Denim | ||

| Other Fabric Types | ||

| Category | Mass | |

| Premium | ||

| Distribution Channel | Third-Party Retailer Platform | |

| Company-Owned Platform | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current outlook for online apparel through 2031?

The online apparel market is projected to rise from USD 438.2 billion in 2026 to USD 544.7 billion by 2031 at a 4.5% CAGR, showing steady rather than explosive growth.

Which product group is driving the most revenue online?

Casual wear led the online apparel market in 2025 with a 38.06% revenue share because it fits everyday use, hybrid work, and frequent replenishment.

Which segment is growing the fastest by channel?

Company-owned platforms are forecast to grow at a 7.25% CAGR through 2031 as brands invest more in first-party data, loyalty, and direct digital control.

Which end-user group is creating the strongest growth momentum?

Children’s apparel is the fastest-growing end-user segment at a 5.62% CAGR through 2031, supported by regular replacement demand and rising online comfort among parents.

Page last updated on: