Europe E-Commerce Apparel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

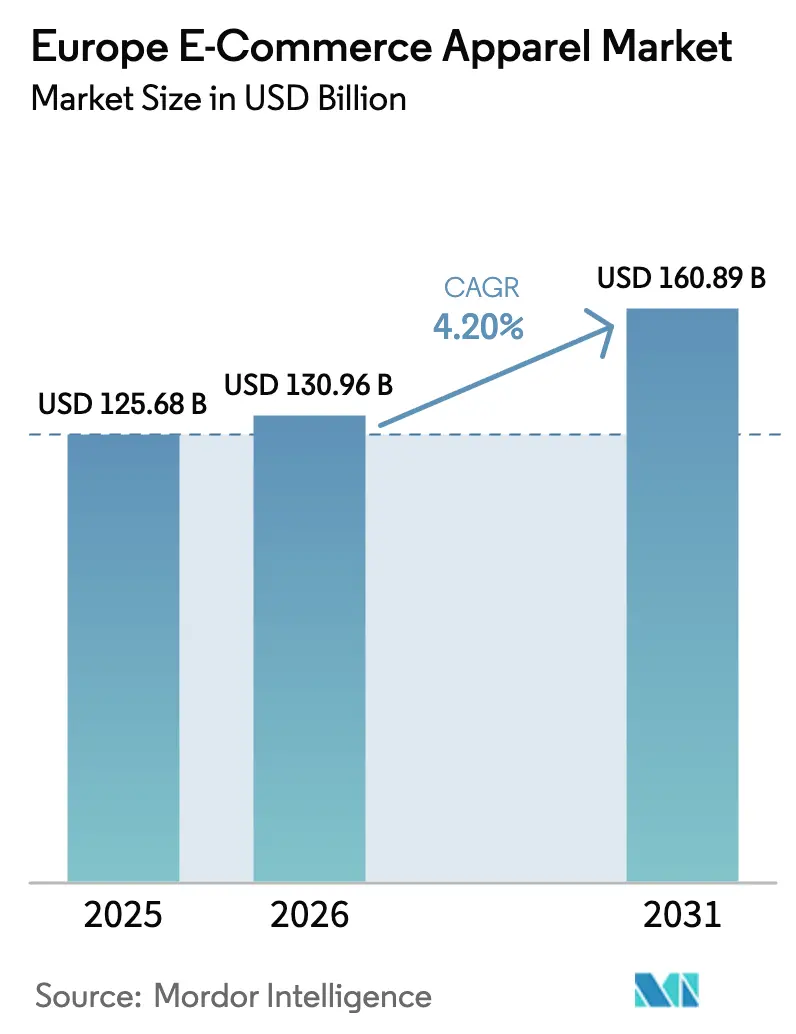

| Base Year Market Size (2025) | USD 125.68 Billion |

| Market Size (2026) | USD 130.96 Billion |

| Market Size (2031) | USD 160.89 Billion |

| Growth Rate (2026 - 2031) | 4.20% CAGR |

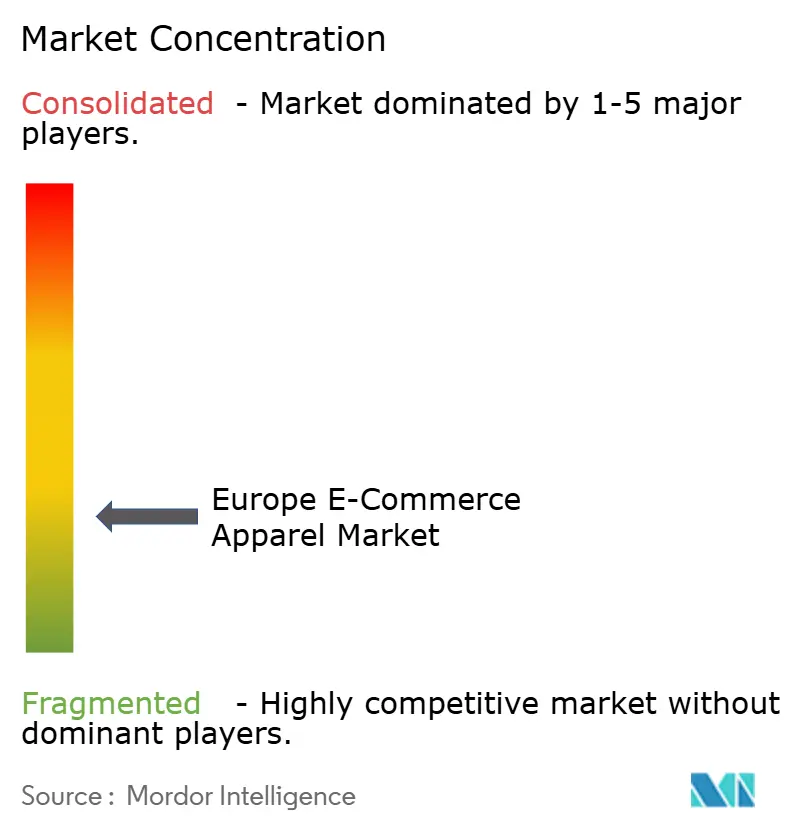

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe E-Commerce Apparel Market Analysis by Mordor Intelligence

The Europe e-commerce apparel market size in 2026 is estimated at USD 130.96 billion, growing from 2025 value of USD 125.68 billion with 2031 projections showing USD 160.89 billion, growing at 4.2% CAGR over 2026-2031. This market plays a pivotal role in the broader European e-commerce ecosystem, reflecting the increasing consumer inclination toward online platforms for apparel purchases. The growth is driven by a combination of factors, including evolving consumer preferences, advancements in technology, and the widespread adoption of digital shopping channels. Retailers are increasingly prioritizing digital transformation and implementing omnichannel strategies to cater to the dynamic demands of consumers, creating a seamless integration between online and offline shopping experiences. As innovation and adaptability continue to shape the market landscape, the Europe e-commerce apparel market is poised for sustained expansion, underpinned by the ongoing evolution of consumer behavior and the growing importance of digital platforms in the retail sector.

Key Report Takeaways

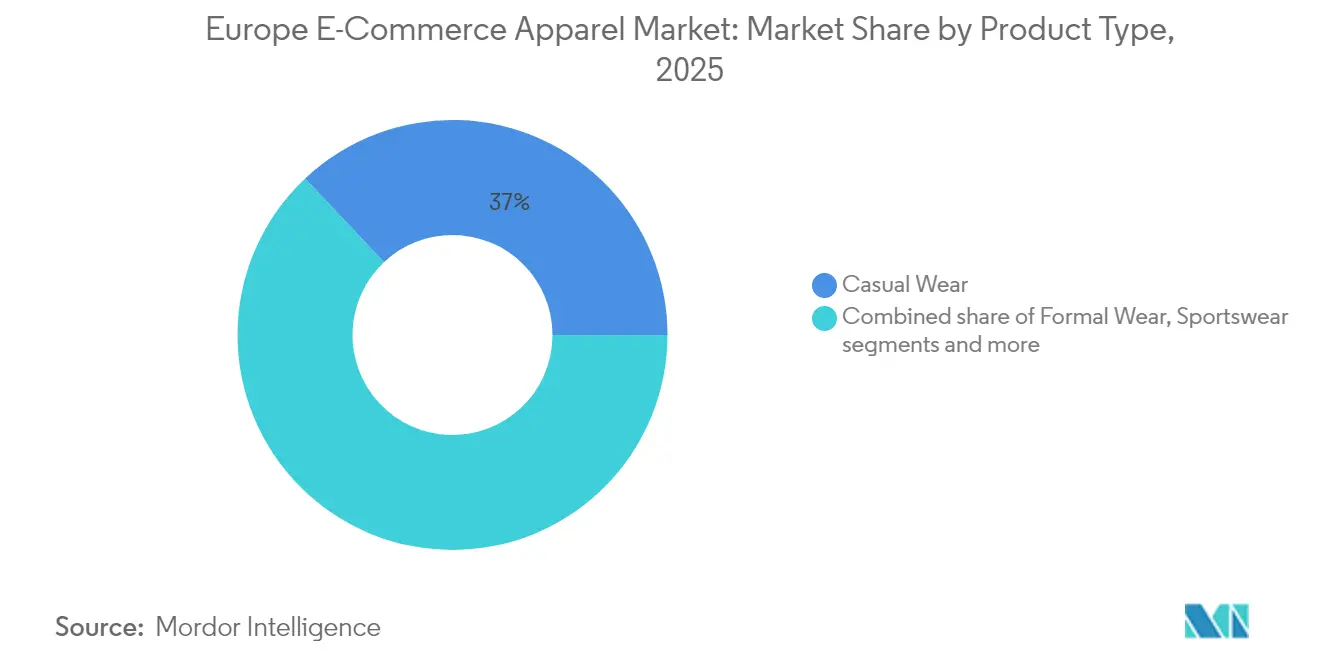

- By product type, casual wear held 37.02% of Europe e-commerce apparel market share in 2025, while sportswear is poised to post the fastest 4.57% CAGR through 2031.

- By end user, women led with a 44.18% share in 2025; children’s apparel is projected to expand at a 4.89% CAGR between 2026 and 2031.

- By fabric material, cotton captured 39.92% share of the Europe e-commerce apparel market size in 2025, whereas polyester is forecast to register a 5.14% CAGR to 2031.

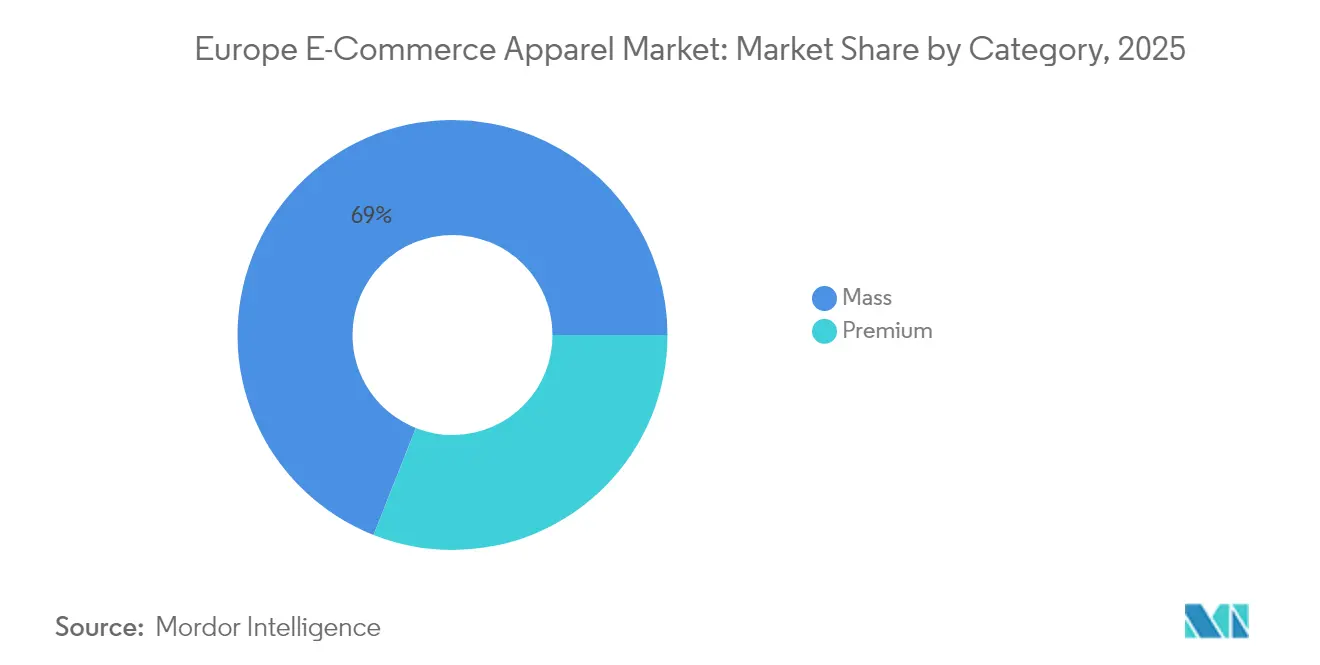

- By category, mass-market labels commanded 69.02% share in 2025; the premium tier is on track for a 5.43% CAGR through 2031.

- By platform type, third-party marketplaces accounted for 80.88% share in 2025 and are forecast to grow at a 5.86% CAGR to 2031.

- By geography, the United Kingdom contributed 17.64% of 2025 revenue; Spain is anticipated to log the quickest 6.11% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe E-Commerce Apparel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Promotion and Discounts Enticing Consumer to Make Purchase | +3.0% | Pan-European, with higher impact in Southern Europe | Short term (≤ 2 years) |

| Personalized Shopping Experience Enabled by Technology | +2.6% | Northern & Western Europe, UK, Germany, Netherlands | Medium term (2-4 years) |

| Direct-to-Consumer (DTC) Brand Growth | +3.8% | UK, Germany, France, Netherlands | Long term (≥ 4 years) |

| Influence of Social Media Platforms and Celebrity Endorsements | +2.1% | Pan-European, with higher impact among younger demographics | Medium term (2-4 years) |

| Flexible and Diverse Payment Options | +3.4% | Western Europe, UK, Germany, France | Medium term (2-4 years) |

| Rising Demand for Sustainable and Ethical Fashion | +3.0% | Northern Europe, Germany, France, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Promotion and Discounts Enticing Consumer to Make Purchase

Promotions and discounts drive consumer purchasing decisions in the E-Commerce apparel market. These strategies influence buying behavior through multiple factors: creating urgency, providing value, and reducing purchase costs in a competitive market. Common promotional tactics include time-limited discounts, flash sales, and exclusive offers, which encourage immediate purchases. Additionally, loyalty programs and personalized promotions help build customer retention. The integration of omnichannel marketing and social commerce has enhanced promotional effectiveness, enabling brands to deliver targeted offers across platforms using customer data analytics. Social media platforms like TikTok and Instagram have become key promotional channels, with brands such as Zara and H&M implementing shoppable video content that connects users to exclusive online discounts.

Personalized Shopping Experience Enabled by Technology

The Europe e-commerce apparel industry's shift toward personalized shopping experiences is driven by technological advancements and evolving consumer preferences. Consumers seek convenience, relevance, and brand connection, prompting retailers to implement artificial intelligence, machine learning, and data analytics solutions. These technologies analyze customer data, including browsing patterns, purchase records, preferences, and social media interactions, to create personalized product recommendations and targeted promotions. Virtual fitting rooms and augmented reality solutions help customers visualize clothing fit and appearance before purchase, which helps reduce return rates. AI-powered chatbots provide immediate, personalized customer support throughout the shopping process. According to Eurostat, in 2024, 13.5% of enterprises in the European Union implemented artificial intelligence technologies in their operations, with retail emerging as a primary adopter [1]Source: Eurostat, "Usage of AI technologies increasing in EU enterprises", ec.europa.eu.

Direct-to-Consumer (DTC) Brand Growth

Apparel brands adopting a direct-to-consumer (DTC) approach benefit from controlling branding, pricing, and customer experience, enabling consistent narratives that appeal to transparency-focused consumers. The DTC model provides access to customer data for personalized marketing and product recommendations. Eliminating intermediaries boosts profit margins and operational efficiency, allowing competitive pricing and investment in product development and customer service. Digital-first operations and social media presence help brands quickly adapt to preferences, launch products, and target niche segments. Advanced e-commerce platforms and logistics partnerships optimize order fulfillment and enhance customer experience. Traditional companies are adapting, with Adidas aiming for 50% of revenue from DTC sales by 2025. Technology, direct data access, and strong customer relationships drive DTC apparel brand growth across the region.

Influence of Social Media Platforms and Celebrity Endorsements

Social media platforms and celebrity endorsements shape fashion and apparel purchasing decisions, particularly among younger consumers seeking authenticity and trend accessibility. Social media has transformed from a communication tool into a marketplace that enables product discovery and direct purchasing. Platforms like Instagram, TikTok, Facebook, and Pinterest serve as digital fashion showcases where users trust recommendations from influencers and peer consumers more than traditional advertising. Integrated shopping features, such as in-app purchases and product tags, simplify the purchasing process. Celebrity endorsements and influencer collaborations help brands build trust and appeal while meeting consumer expectations for transparency. Social commerce effectiveness increases through user-generated content, live shopping events, and personalized recommendations. Facebook recorded 408 million monthly active users (MAUs) in Europe during the fourth quarter of 2023 [2]Source: Meta Platforms, "Meta Earnings Presentation Q4 2023", www.meta.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of Counterfeit Products | -2.6% | Pan-European, with higher impact in Southern and Eastern Europe | Medium term (2-4 years) |

| Competition from Brick-and-Mortar Stores and Alternative Retail Channels | -1.7% | Western Europe, Urban Centers | Medium term (2-4 years) |

| Logistical Challenges in Fulfillment and Delivery | -2.1% | Eastern Europe, Rural Areas, Cross-Border Markets | Short term (≤ 2 years) |

| Size, Fit, and Product Assessment Challenges | -1.8% | Pan-European, with higher impact in cross-border purchases | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Availability of Counterfeit Products

The proliferation of counterfeit products poses a significant challenge to the European e-commerce apparel market, eroding consumer trust and brand equity while creating unfair competitive dynamics. According to the European Union Intellectual Property Office (EUIPO), counterfeit goods cost the clothing, cosmetics, and toy industries EUR 16 billion in sales and nearly 200,000 jobs annually [3]Source: European Union Intellectual Property Office (EUIPO), "Counterfeit goods cost EU industries billions of euros and thousands of jobs annually", www.euipo.europa.eu/en. The digital nature of e-commerce has inadvertently facilitated this problem, with counterfeiters using third-party marketplaces and social media platforms to reach consumers directly, often utilizing authentic product images and descriptions to create misleading listings. The industry's response has evolved from basic authentication tags to blockchain-based verification systems that provide proof of authenticity throughout the supply chain. Companies are implementing comprehensive anti-counterfeiting strategies that combine technological solutions with consumer education initiatives. This issue particularly affects premium and luxury segments, where brand equity directly influences value proposition and pricing power.

Competition from Brick-and-Mortar Stores and Alternative Retail Channels

Competition from brick-and-mortar stores and alternative retail channels restrains the growth of E-commerce apparel sales. Physical stores provide advantages that e-commerce platforms cannot fully replicate, including the ability to touch and try on clothing, receive immediate personalized service, and purchase items instantly. The in-store shopping experience creates emotional connections and brand loyalty through tactile and experiential elements that e-commerce platforms find challenging to match. Consumers value the ability to assess fit and quality firsthand, resulting in lower return rates and higher satisfaction levels in physical stores. Alternative retail channels, including pop-up shops, department store concessions, and omnichannel models, offer consumers flexible shopping options and increase competition for online-only retailers. Major retailers utilize their store networks to provide services such as Buy Online, Pick Up In Store (BOPIS), combining convenience with immediate product availability. Consumers increasingly prefer retailers offering seamless integration between online and offline channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Casual Wear Dominates Amid Lifestyle Shifts

The casual wear segment holds a 37.02% share of the European e-commerce apparel market in 2025, driven by consumers' increasing preference for comfortable and versatile clothing. This trend is supported by the growth in remote work, with 8.9% of employed people in the European Union working from home in 2023, according to Eurostat. The segment shows particular strength in Northern European countries, including Germany and the Netherlands, where practical clothing aligns with local preferences. The sportswear segment is expected to grow at a CAGR of 4.57% from 2026 to 2031, supported by athleisure trends and increased health awareness. The Formal Wear segment has adapted by incorporating more comfortable designs that work in both professional and casual settings.

The nightwear category shows growth due to increased consumer interest in sleep quality and wellness, with premium sleep brands gaining market share. Across all segments, manufacturers are incorporating technical fabrics with moisture-wicking, temperature-regulating, and odor-resistant properties to differentiate their products. Product strategies focus on versatility and year-round appeal, moving away from strict seasonal collections toward more sustainable inventory management. This trend is reflected in the popularity of modular clothing systems that adapt to various situations and weather conditions, appealing to consumers seeking maximum value from their clothing purchases.

By End User: Women's Segment Leads While Children's Category Accelerates

The women's segment holds a dominant 44.18% market share in 2025, attributed to higher purchase frequency and broader product category selection compared to other segments. This dominance is strongest in Southern European markets, particularly Italy and Spain, where fashion plays a significant role in cultural identity. Major retailers have successfully implemented AI-powered size recommendation tools in the women's segment to resolve the persistent issue of size inconsistency across brands. The children's wear segment is expected to achieve the highest growth rate at 4.89% CAGR from 2026 to 2031, as parents prioritize quality and sustainable clothing options despite Europe's declining birth rates.

The men's segment is undergoing significant changes, focusing on style education and curation services to overcome traditional barriers in fashion engagement. Retailers are implementing data-driven personalization to streamline the shopping experience for male consumers through guided navigation that reduces choice complexity while maintaining style options. Across all segments, demand for inclusive sizing continues to increase, prompting brands to expand their size ranges. This inclusivity trend extends to age-appropriate styling, particularly targeting Europe's growing 50+ demographic, which represents a significant portion of discretionary spending power.

By Fabric Material: Cotton Maintains Leadership as Polyester Gains Momentum

In 2025, cotton retains a commanding 39.92% market share, leveraging its natural appeal, breathability, and perceived sustainability advantages over synthetic alternatives. This fabric demonstrates exceptional performance in the premium and sustainable fashion segments, where brands prioritize natural materials to enhance their positioning and value proposition. European consumers exhibit a marked preference for high-quality, long-staple cotton, valued for its superior durability and comfort.

Polyester is projected to grow at a 5.14% CAGR from 2026 to 2031, supported by technological advancements and the rise of recycled polyester from post-consumer plastic waste. Brands like Hennes & Mauritz AB aim for 100% recycled or sustainably sourced materials by 2030, with a 30% interim target by 2025. Nylon remains vital in performance apparel, especially sportswear and outerwear, due to its durability and water resistance, with production shifting to bio-based sources. Denim retains a significant market share, with European consumers loyal to this versatile fabric. Sustainable innovations, such as water-saving dyeing processes, are transforming the denim segment.

By Category: Mass Market Dominates While Premium Segment Accelerates

In 2025, the mass category dominates the European e-commerce apparel market, holding a substantial 69.02% share. This dominance underscores the segment's broad appeal and value proposition, especially in today's price-sensitive consumer landscape. Fast-fashion business models, adept at translating runway trends to market in as little as two weeks, fuel the segment's strength. This agility fosters a constant influx of new offerings, enticing frequent site visits and purchases. Leading mass-market retailers are harnessing AI-driven trend forecasting, pinpointing emerging styles ahead of mainstream recognition.

Meanwhile, the premium segment, though smaller, is set to outpace with a projected 5.43% CAGR growth from 2026 to 2031. This surge is attributed to a rising consumer inclination towards quality and the enhanced accessibility of luxury goods via digital platforms. Digital channels are reshaping the Premium segment, demystifying luxury and making it more approachable. As a result, the premium customer base has broadened, encompassing not just traditional luxury buyers but also those who occasionally splurge on select investment pieces. This blending of markets is giving rise to a new "masstige" segment, merging premium quality with mass-market reach.

By Platform Type: Third-Party Marketplaces Lead Digital Commerce Revolution

In 2025, European e-commerce apparel market sees third-party marketplaces commanding a dominant 80.88% share. Leveraging extensive assortments, transparent pricing, and established consumer trust, these platforms lead in digital fashion spending. They reap significant benefits from robust network effects: each added seller broadens consumer choice, and every new consumer amplifies the platform's allure to brands eyeing digital distribution. Projections suggest this segment will maintain its lead, boasting a 5.86% CAGR from 2026 to 2031, outpacing all other platform types. Notably, marketplaces like Zalando have transitioned from mere transaction hubs to holistic fashion ecosystems, introducing value-added services such as styling advice, outfit recommendations, and loyalty programs to bolster customer retention.

Company-owned platforms, although smaller in scale, represent a strategically significant segment of the market. These platforms enable brands to establish direct relationships with consumers and maintain complete control over the shopping experience. By leveraging first-party data, they deliver highly personalized shopping experiences that enhance both conversion rates and customer loyalty. The most advanced company-owned platforms are adopting "headless commerce" architectures, which decouple front-end user experiences from back-end systems. This approach facilitates rapid experimentation and optimization across multiple customer touchpoints.

Geography Analysis

In 2025, the United Kingdom solidifies its status as the dominant player in Europe's e-commerce apparel market, commanding a 17.64% share. This achievement is largely attributed to the United Kingdom's robust digital infrastructure and the populace's strong trust in online shopping. Historically, the United Kingdom has been at the forefront of e-commerce adoption. This digital prowess has spurred innovative retail strategies, with United Kingdom retailers leading the charge in offering services such as same-day delivery in bustling urban locales and AI-driven styling suggestions, elevating the online shopping journey.

Spain is rapidly emerging as the fastest-growing market, with a projected CAGR of 6.11% from 2026 to 2031. This growth is driven by swift digital adoption and an influx of cutting-edge fashion retailers. By 2023, over 95.4% of Spaniards were online, according to the International Telecommunication Union (ITU). Inditex, a major player in this arena, has leveraged its Spanish heritage to pilot and refine digital innovations, introducing them globally and nurturing a sophisticated digital fashion ecosystem in Spain. Germany also emerges as a key market, blending its strong purchasing power with a tech-savvy population, resulting in significant online fashion spending. France and Italy, while both major players, each bring unique flavors to the online fashion arena. France is at the forefront of sustainable fashion, enacting stringent measures like banning the destruction of unsold garments and championing a circular economy, underscored by a EUR 1 billion commitment to garment recycling. The Netherlands is carving out a niche as a distribution epicenter, bolstered by its sustainability efforts. In contrast, Poland is witnessing a surge in imports, especially from developing nations. Even smaller markets like Belgium and Sweden are making their mark on the diverse European tapestry, each showcasing distinct consumer tastes and varying rates of digital adoption, prompting retailers to tailor their strategies for broader European appeal.

Competitive Landscape

The European e-commerce apparel market presents a fragmented competitive landscape, allowing specialized players to carve out market share by offering unique value propositions. Key players in this arena include Burberry Group plc, Hennes & Mauritz AB, Adidas AG, and Puma SE. Meanwhile, the European Commission's Digital Markets Act aims to level the playing field, ensuring fair competition among major platforms and empowering smaller entities to thrive.

Regulatory shifts are molding the competitive terrain. For instance, the European Commission's Digital Services Act mandates platforms to adopt stricter transparency and content moderation protocols, impacting how brands manage customer engagement and product visibility. Furthermore, there's a notable gap in certain market segments. Areas like sustainable fashion and inclusive sizing, highlighted by the European Environment Agency and the European Disability Forum as having significant unmet consumer demands, present lucrative opportunities for agile entrants and niche brands.

Innovation continues to gain momentum. According to the European Patent Office, patent filings related to fashion technologies are on the rise, spanning virtual try-on systems, 3D knitting, and bio-based textiles. These developments reflect the sector’s rapid digital transformation and growing consumer demand for personalization and sustainability. Additionally, open banking regulations led by the European Banking Authority are facilitating the emergence of integrated fintech tools, such as “buy now, pay later” and real-time installment payments, giving forward-thinking fashion retailers a competitive edge in converting and retaining online shoppers.

Europe E-Commerce Apparel Industry Leaders

-

Burberry Group plc

-

Hennes & Mauritz AB

-

Adidas AG

-

Puma SE

-

Kering S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Tesco launched its F&F clothing range online to meet growing customer demand and improve shopping convenience. The online platform offers women's, men's, and children's clothing, footwear, and accessories, including the F&F Edit, Sports, and F&F Active Athleisure collections.

- April 2025: Dressmann, a chain of men's clothing stores, expanded its online operations to Denmark, Austria, and Germany. This expansion marks the beginning of the company's European market strategy.

- August 2024: Authentic Brands Group partnered with United Legwear & Apparel Co. to manage Ted Baker's e-commerce operations in the United Kingdom and Europe. The collaboration aims to restore the brand's digital presence for its customers.

- May 2024: MUJI, a Japanese fashion and lifestyle brand, expanded its European operations by launching online storefronts on the BigCommerce platform. The implementation enables MUJI to use BigCommerce's open SaaS and composable ecommerce platform for its B2C and B2B operations.

Europe E-Commerce Apparel Market Report Scope

E-commerce apparel includes the buying and selling of fashion and apparel products online, specifically through e-commerce platforms.

The Europe e-commerce apparel market is segmented by product type, end-user, platform type, and geography. Based on product type, the market is segmented into formal wear, casual wear, sportswear, nightwear, and other types. Based on end users, the market is segmented into men, women, and kids/children. Based on platform type, the market is segmented into third-party retailers and the company's own website. The study also analyzes major geography, such as Germany, the United Kingdom, France, Italy, Spain, Russia, and Rest of Europe.

The market sizing has been done in value terms in USD for all the abovementioned segments.

| Formal Wear |

| Casual Wear |

| Sportswear |

| Nightwear |

| Intimate and Loungewear |

| Other Product Tyoes |

| Men |

| Women |

| Children |

| Cotton |

| Polyester |

| Nylon |

| Denim |

| Other Fabric Types |

| Mass |

| Premium |

| Third-Party Marketplace |

| Company-owned Platform |

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Formal Wear |

| Casual Wear | |

| Sportswear | |

| Nightwear | |

| Intimate and Loungewear | |

| Other Product Tyoes | |

| By End User | Men |

| Women | |

| Children | |

| By Fabric Material | Cotton |

| Polyester | |

| Nylon | |

| Denim | |

| Other Fabric Types | |

| By Category | Mass |

| Premium | |

| By Platform Type | Third-Party Marketplace |

| Company-owned Platform | |

| By Country | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe E-commerce apparel market?

The market is valued at USD 130.96 billion in 2026 and is projected to reach USD 160.89 billion by 2031.

Which product segment leads Europe online apparel sales?

Casual wear is the largest category, holding 37.02% of 2025 revenue.

Why are third-party marketplaces so dominant in Europe?

They provide vast assortments, transparent pricing, and strong buyer protection, securing 80.88% share in 2025 and maintaining scale advantages under the Digital Markets Act.

Which country offers the fastest growth opportunity?

Spain is forecast to expand at a 6.11% CAGR between 2026 and 2031 owing to near-universal internet access and targeted digital-skills programmes.

Page last updated on: