E-commerce Apparel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

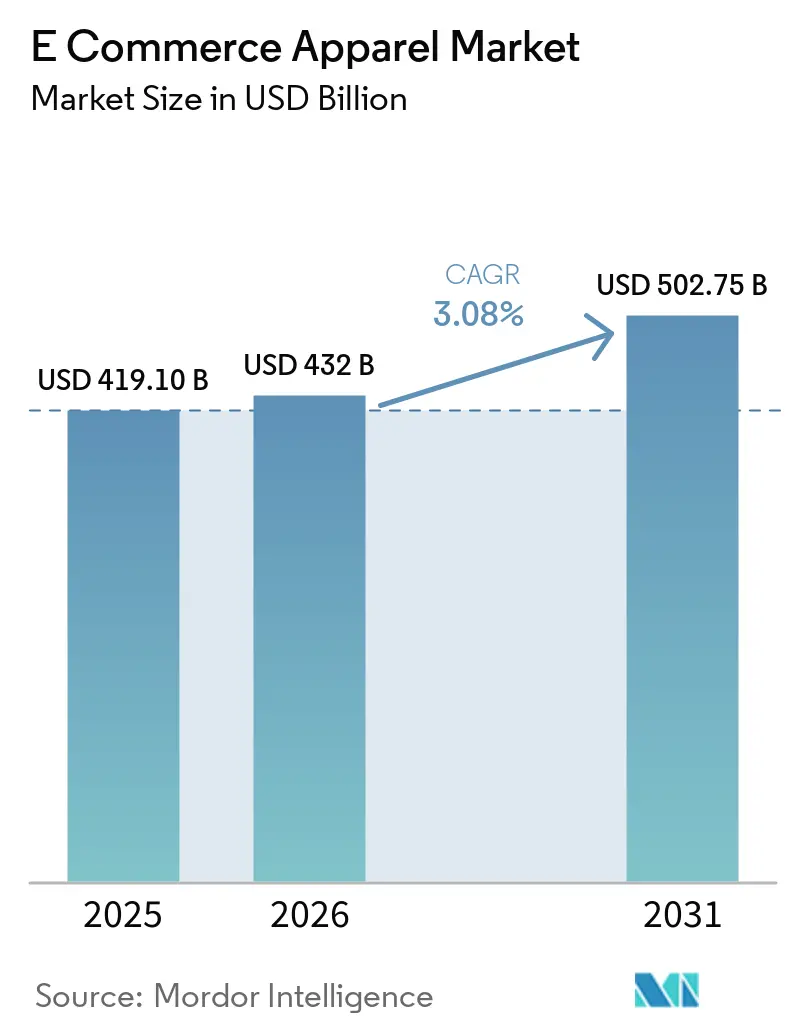

| Market Size (2026) | USD 432 Billion |

| Market Size (2031) | USD 502.75 Billion |

| Growth Rate (2026 - 2031) | 3.08% CAGR |

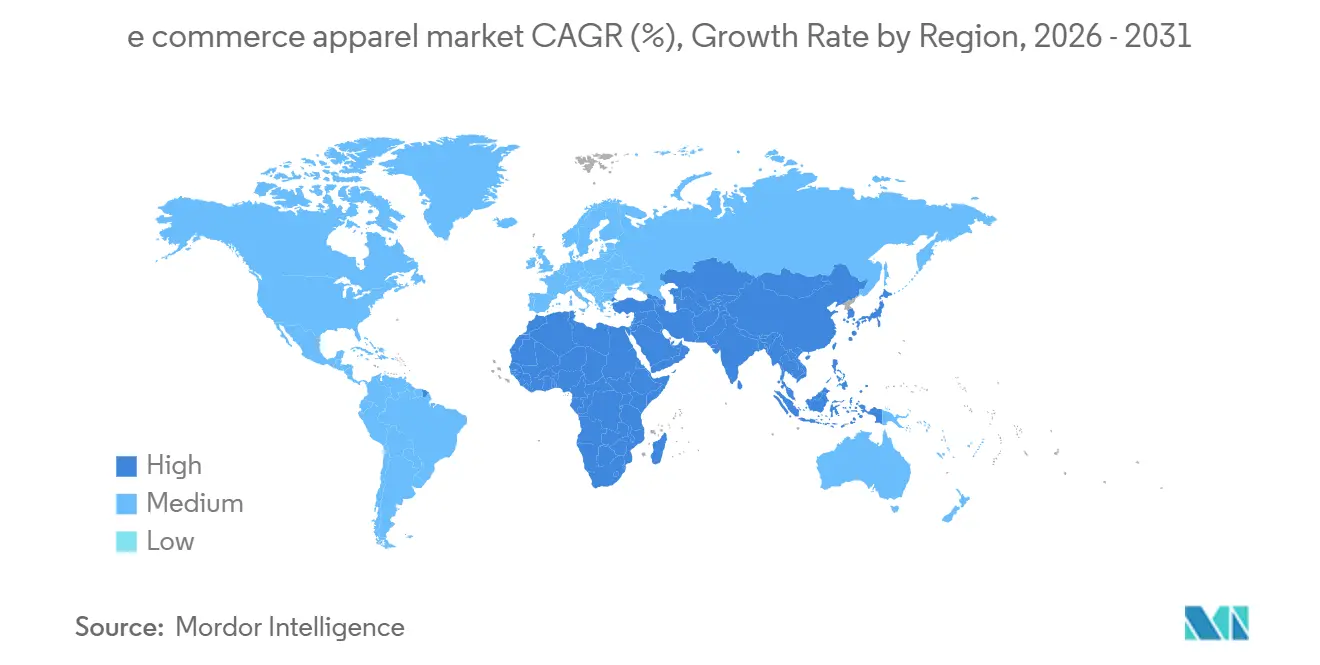

| Fastest Growing Market | South America |

| Largest Market | Asia-Pacific |

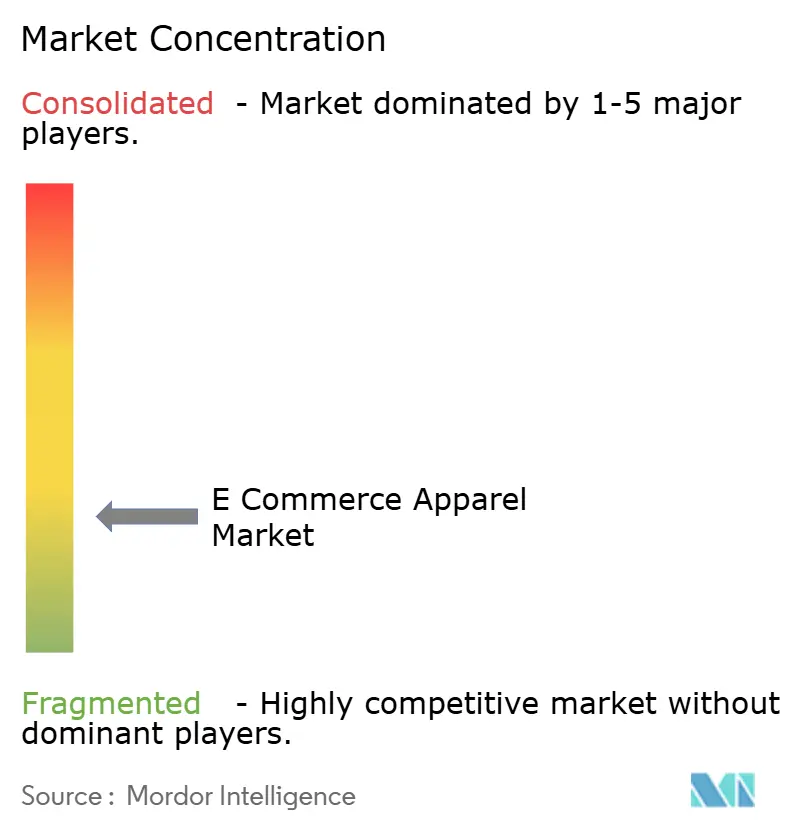

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

E-commerce Apparel Market Analysis by Mordor Intelligence

The E-commerce Apparel Market is projected to grow from USD 419.10 billion in 2025 to USD 432 billion in 2026, with an anticipated value of USD 502.75 billion by 2031, registering a CAGR of 3.08% during the period 2026–2031. This growth is attributed to the increasing adoption of digital shopping platforms, greater accessibility to smartphones and the internet, and a rising consumer preference for convenient and personalized online shopping experiences. Advancements in digital technologies, such as artificial intelligence-based recommendations, virtual try-on solutions, interactive product visualization, and data-driven personalization, are further enhancing customer engagement and boosting confidence in online purchases.

Key Report Takeaways

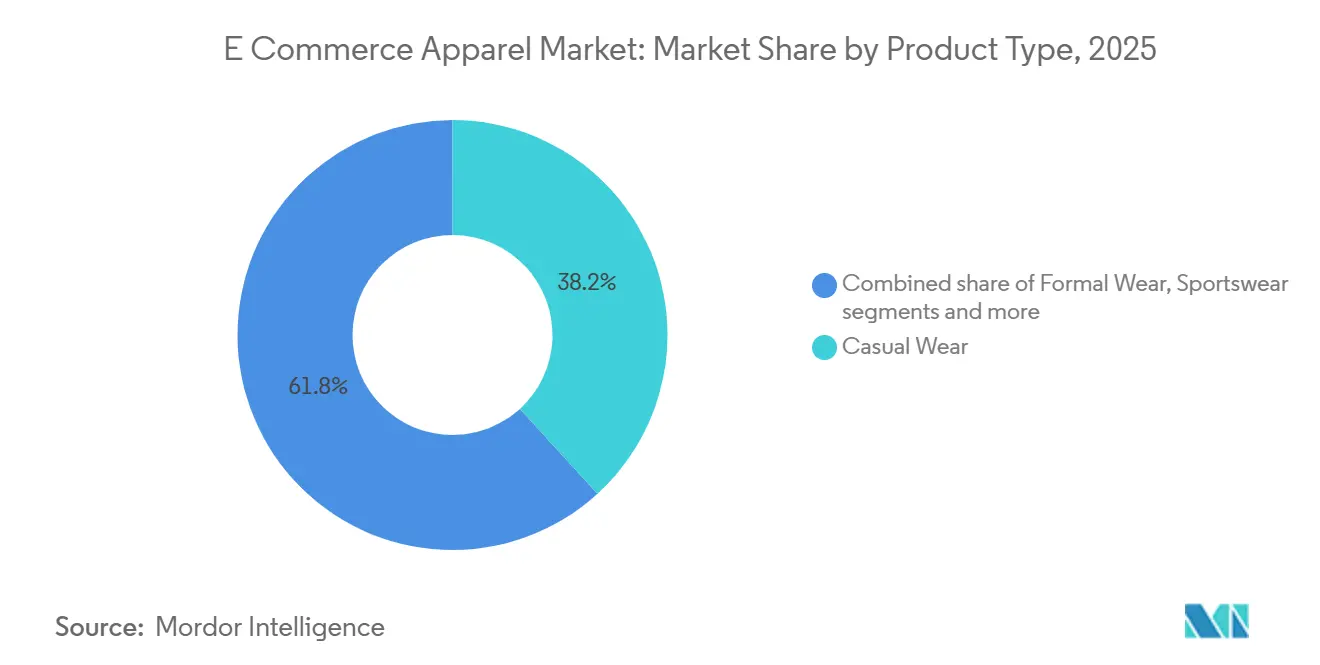

- By product type, casual wear led with 38.23% revenue share in 2025, while sportswear is forecast to expand at 4.11% CAGR through 2031.

- By end user, women held 54.53% share in 2025, while children recorded the highest projected CAGR at 3.59% through 2031.

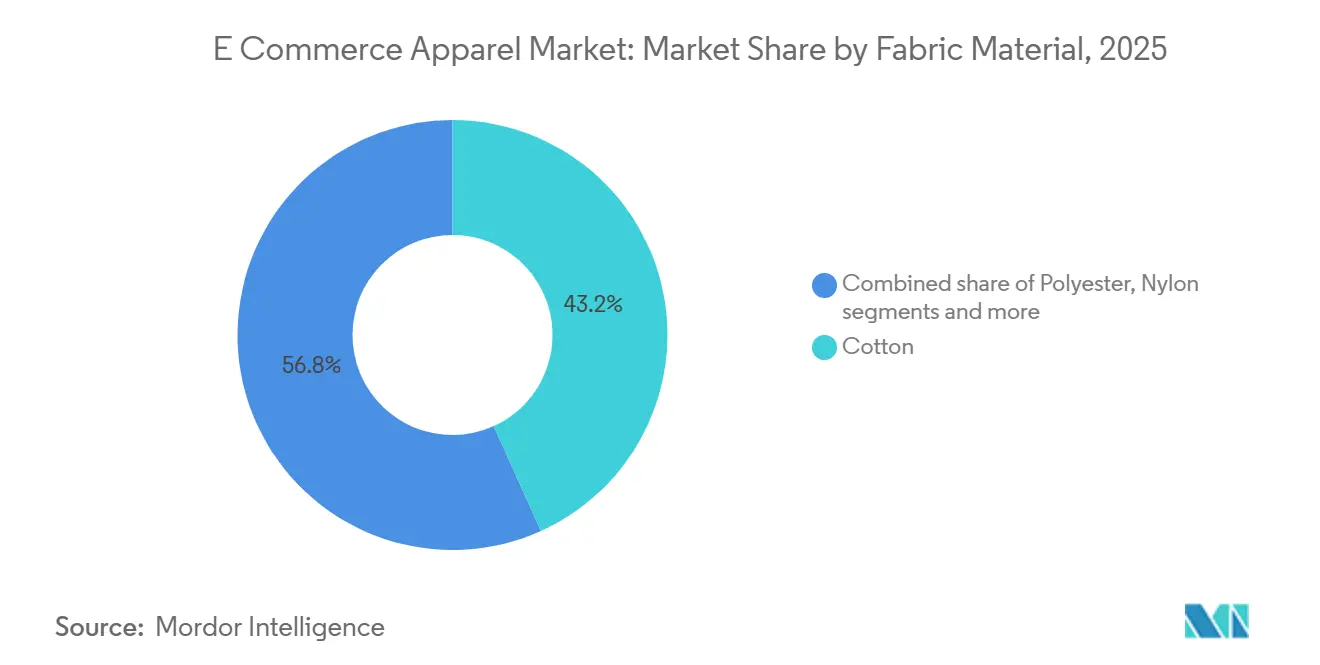

- By fabric material, cotton accounted for 43.24% share in 2025, while polyester is advancing at 4.35% CAGR through 2031.

- By category, mass apparel commanded 86.55% share in 2025, while premium is set to grow at 4.97% CAGR through 2031.

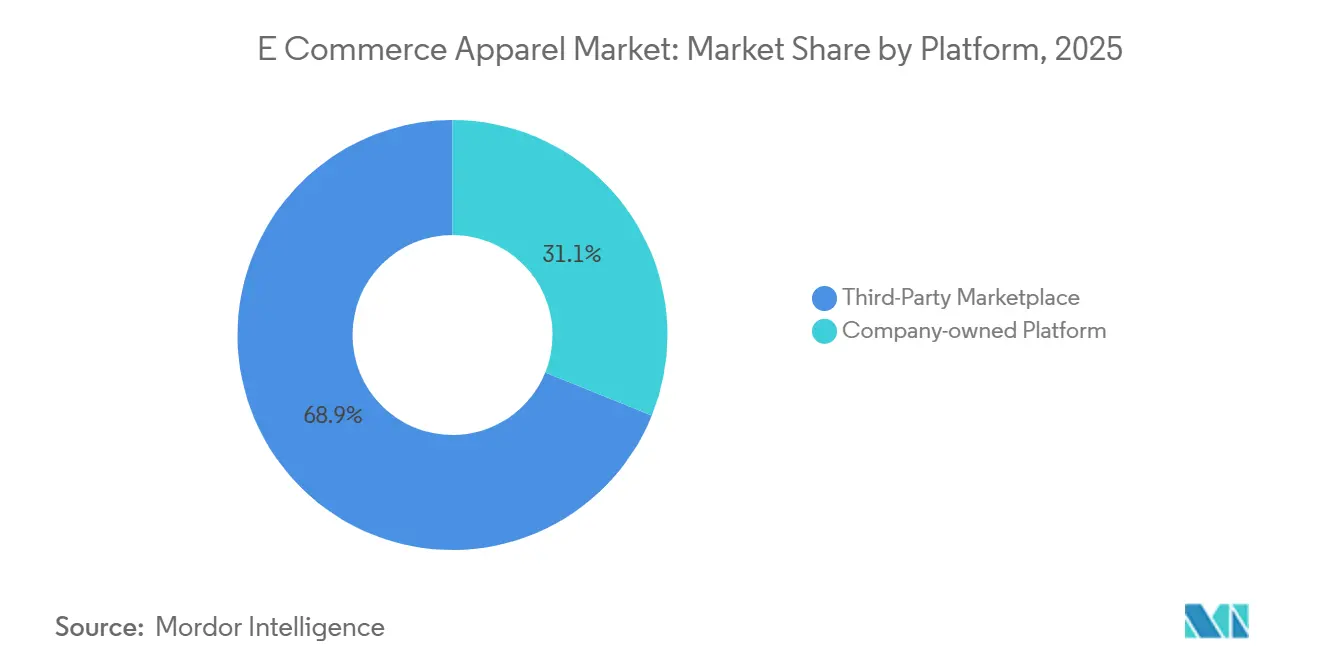

- By platform type, third-party marketplaces held 68.89% share in 2025, while company-owned platforms are projected to expand at 5.05% CAGR through 2031.

- By geography, Asia-Pacific accounted for 37.55% share in 2025, while South America is forecast to grow at 5.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global E-commerce Apparel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising internet and smartphone penetration | +0.7% | Global; concentrated gains in India, Southeast Asia, and Sub-Saharan Africa | Medium term (2–4 years) |

| Increasing adoption of digital payment solutions | +0.5% | Global; North America and Europe near term; Asia-Pacific and South America medium term | Short term (≤ 2 years) |

| Growth of virtual try-on and augmented reality (AR) technologies | +0.4% | North America, Europe, Asia-Pacific core (Japan, South Korea, China) | Medium term (2–4 years) |

| Influence of social media platforms and celebrity endorsements | +0.6% | Global; highest impact in Asia-Pacific and South America | Short term (≤ 2 years) |

| Demand for fast fashion and frequent style updates | +0.5% | Global; concentrated in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Direct-to-consumer (DTC) brand growth | +0.3% | North America, Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising internet and smartphone penetration

Increasing internet and smartphone penetration is enhancing digital connectivity, enabling more consumers to access online shopping platforms with ease. The widespread use of smartphones has significantly influenced apparel purchasing behavior by allowing users to browse fashion collections, compare products, receive personalized recommendations, and complete transactions through mobile applications and websites at any time. According to the International Telecommunication Union (ITU), in 2025, 82% of individuals aged 10 years or older globally owned a mobile phone [1]Source: International Telecommunication Union (ITU), "Mobile phone ownership", itu.int. Universal ownership, defined as a penetration rate exceeding 95%, highlights the growing accessibility of digital devices worldwide. The expanding base of smartphone users is driving the adoption of mobile commerce, allowing apparel retailers to reach a broader audience through digital marketing, social commerce, and app-based shopping platforms.

Increasing adoption of digital payment solutions

The growing adoption of digital payment solutions is driving the expansion of the E-commerce Apparel Market by enabling faster, safer, and more convenient online shopping experiences. The development of payment technologies, such as digital wallets, credit and debit cards, instant payment systems, and buy-now-pay-later (BNPL) services, has streamlined online transactions and enhanced consumer trust in purchasing apparel through digital platforms. According to the Bank for International Settlements (BIS), global cashless transactions reached 1,976.8 billion, underscoring the shift toward digital and contactless payment methods. The increasing availability of secure payment gateways, one-click checkout options, fraud protection systems, and flexible payment alternatives is reducing transaction barriers and boosting purchase completion rates.

Growth of virtual try-on and augmented reality (AR) technologies

The adoption of virtual try-on and augmented reality (AR) technologies is significantly influencing the E-commerce Apparel Market by improving the online shopping experience and addressing uncertainties associated with purchasing apparel digitally. As consumers are unable to physically try on clothing when shopping online, AR-powered solutions allow them to better visualize garment fit, size, appearance, and styling, thereby enhancing confidence in their purchase decisions. Tools such as virtual fitting rooms, AI-driven body measurement systems, and interactive product visualization features are narrowing the gap between physical and online retail experiences. These technologies also enhance customer engagement by providing personalized recommendations and immersive shopping experiences tailored to individual preferences. Furthermore, the integration of AR tools enables apparel retailers to address size-related challenges, reduce product return rates, and enhance overall customer satisfaction.

Influence of social media platforms and celebrity endorsements

Social media platforms and celebrity endorsements are playing a significant role in driving the growth of the E-commerce Apparel Market by transforming how consumers discover, evaluate, and purchase fashion products. These platforms have become key digital hubs for fashion discovery, where trends are quickly established and shared through influencers, celebrities, creators, and user-generated content. Celebrity collaborations, influencer recommendations, and promotional campaigns enhance product visibility, build brand awareness, and encourage consumers to explore new apparel collections online. Additionally, the integration of shopping features within social media applications, such as direct product links, live shopping events, and interactive advertisements, has streamlined the purchasing process, enabling consumers to transition seamlessly from inspiration to checkout.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Size and fit uncertainty among consumers | -0.3% | Global | Short term (≤ 2 years) |

| High product return and exchange challenges | -0.4% | North America, Europe | Short term (≤ 2 years) |

| Concerns regarding product quality and authenticity | -0.2% | Global; highest in Asia-Pacific and Middle East | Medium term (2–4 years) |

| Data privacy and cybersecurity concerns | -0.2% | Global; regulatory pressure concentrated in North America and Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Size and fit uncertainty among consumers

Size and fit uncertainty remains a significant challenge for the E-commerce Apparel Market. The inability of consumers to physically try on products before purchase often leads to hesitation and diminished confidence. Factors such as varying sizing standards across brands, differences in body shapes, and inconsistencies in garment measurements make it difficult for shoppers to choose the correct fit online. This issue contributes to higher rates of product returns, exchanges, and customer dissatisfaction, thereby increasing operational complexities for apparel retailers. Furthermore, concerns about fabric feel, comfort, and discrepancies between the actual product and its online representation also impact purchasing decisions. Frequent returns due to sizing issues add to costs related to reverse logistics, inventory management, and product handling.

High product return and exchange challenges

High product return and exchange rates pose a significant challenge for the E-commerce Apparel Market, increasing operational complexity and reducing retailer profitability. Online apparel purchases often face higher return rates due to factors such as incorrect sizing, fit mismatches, discrepancies between product images and actual items, unmet fabric expectations, and shifting consumer preferences. Managing frequent returns necessitates additional investments in reverse logistics, quality inspections, repackaging, inventory management, and customer service, placing strain on business operations. Excessive returns can also disrupt inventory planning and delay the resale of returned items, negatively affecting supply chain efficiency. Furthermore, complicated return processes or delayed refunds may lower customer satisfaction and deter repeat purchases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Casual Wear Commands While Sportswear Accelerates

Casual wear accounted for a 38.23% share of the product-type market in 2025, driven by increasing consumer preference for comfortable, versatile, and everyday apparel that aligns with evolving fashion and lifestyle trends. The shift toward relaxed dressing styles has fueled demand for clothing that combines functionality with aesthetic appeal, making casual apparel a popular choice for daily use, social activities, leisure, and flexible working environments. The convenience of online platforms has further supported adoption by offering consumers access to a wide range of styles, fits, colors, and designs, enabling easy comparison and personalized shopping experiences. Additionally, growing exposure to digital fashion trends, social media-driven styling inspiration, and frequent changes in consumer preferences have encouraged regular apparel purchases and faster wardrobe refresh cycles.

Sportswear is the fastest-growing product type, with a CAGR of 4.11% projected for 2026–2031. This growth is driven by the increasing integration of fitness, wellness, and active lifestyles into consumers’ daily routines. Rising participation in sports, exercise, and recreational activities has significantly increased demand for performance-oriented and comfortable apparel suitable for both athletic and everyday use. According to the Bureau of Labor Statistics, in 2024, approximately 94.2% of men in the United States engaged in sports and leisure activities, reflecting a strong consumer inclination toward active lifestyles and supporting greater adoption of sportswear [2]Source: Bureau of Labor Statistics, "Average share of population engaged in sports and leisure activities per day in the United States", bls.gov. Furthermore, the growing popularity of athleisure trends, where consumers seek clothing that combines functionality, comfort, and style, has expanded sportswear usage beyond traditional fitness purposes.

By End User: Children's Segment Emerges as the Fastest-Growing Cohort

In 2025, women accounted for 54.53% of the end-user market, driven by increased engagement with online fashion platforms and strong demand for a wide variety of apparel styles catering to different occasions and preferences. The growing adoption of digital shopping channels has provided consumers with access to extensive collections, including everyday clothing, professional attire, occasion wear, and trend-focused fashion, fostering frequent purchasing behavior. Social media influence, digital fashion content, celebrity trends, and personalized styling recommendations have further supported fashion discovery and boosted online apparel purchases. Additionally, features such as broader product selections, inclusive sizing, customized recommendations, customer reviews, and convenient return policies have enhanced shopping confidence and encouraged online adoption.

The children's segment is expected to be the fastest-growing end-user category, with a projected CAGR of 3.59% during 2026–2031. This growth is attributed to the rising demand for convenient access to a wide range of children’s apparel through digital shopping platforms. Frequent changes in children’s clothing needs due to growth, seasonal requirements, and evolving style preferences are driving increased apparel purchases via online channels. The availability of diverse collections, including everyday wear, occasion wear, school-related clothing, and activity-specific apparel, enables consumers to find suitable products for various age groups and needs. Enhanced online shopping features, such as size guides, product recommendations, customer reviews, easy comparison tools, and simplified return processes, are further boosting consumer confidence in purchasing children’s apparel online.

By Fabric Material: Cotton Retains Scale as Polyester Disrupts Performance Categories

Cotton accounted for a 43.24% share of fabric-type revenues in 2025, driven by its widespread preference as a comfortable, breathable, and versatile material in online apparel purchases. Consumers favor cotton-based clothing due to its softness, durability, skin-friendly properties, and suitability for everyday use, making it one of the most preferred fabrics across various apparel categories. The increasing demand for comfort-oriented fashion has further boosted cotton adoption, as shoppers seek clothing that offers ease of movement and long-lasting wear. Online platforms have facilitated access to a wide variety of cotton apparel designs, styles, and fits, enabling consumers to compare products and make selections based on fabric quality, reviews, and personal preferences. Additionally, rising awareness of natural fibers and growing interest in sustainable and responsibly sourced materials have enhanced the appeal of cotton-based garments.

Polyester is the fastest-growing fabric segment, with a CAGR of 4.35% projected for 2026–2031, driven by increasing consumer preference for lightweight, durable, and easy-care apparel available through online platforms. The fabric’s key attributes, including wrinkle resistance, quick drying, color retention, stretch compatibility, and long-lasting performance, have contributed to its growing adoption among consumers seeking functional and convenient clothing options. The rising demand for versatile apparel suitable for daily wear, fitness activities, travel, and active lifestyles is further accelerating the use of polyester-based garments. Advancements in fabric engineering have enhanced polyester’s comfort, breathability, moisture-wicking capabilities, and overall texture, broadening its acceptance across a wider range of fashion categories. The development of recycled polyester and sustainable textile innovations is also driving growth by addressing consumer preferences for environmentally responsible apparel choices.

By Category: Mass Apparel Anchors Volume as Premium Outpaces Market Growth

Mass apparel is projected to hold a dominant 86.55% share of the category market in 2025, driven by strong consumer demand for affordable, accessible, and trend-responsive clothing available through online shopping platforms. The wide availability of diverse styles, designs, sizes, and everyday fashion options has made mass apparel appealing to consumers seeking variety and convenience. Frequent product launches, rapid fashion cycles, and the ease of discovering new trends online have contributed to higher purchasing frequency and sustained demand. E-commerce platforms further support this growth by offering extensive product catalogs, personalized recommendations, customer reviews, comparison tools, and simplified shopping experiences, enhancing consumer engagement.

The premium segment, while accounting for a smaller share of absolute revenue, is expected to grow at the fastest category CAGR of 4.97% through 2031. This growth is driven by increasing consumer preference for high-quality, exclusive, and value-added apparel available through digital platforms. Greater awareness of superior fabrics, enhanced durability, unique designs, and craftsmanship is encouraging a shift toward premium clothing that offers better style and long-term value. The expansion of online fashion platforms has improved access to premium collections by providing detailed product information, personalized recommendations, virtual styling features, and seamless shopping experiences. Additionally, the demand for sustainable materials, limited collections, customized products, and innovative designs is further boosting the appeal of premium fashion.

By Platform Type: Marketplaces Dominate but Brand Channels Accelerate

Third-party marketplaces accounted for a 68.89% share of platform revenues in 2025, driven by their ability to provide consumers with extensive product variety, competitive options, and a convenient one-stop online shopping experience. These platforms offer access to a broad range of apparel categories, styles, sizes, and brands within a single digital environment, enabling shoppers to compare products, prices, reviews, and delivery options with ease before making a purchase. Key features such as personalized recommendations, advanced search filters, secure payment systems, customer ratings, and simplified return processes have enhanced consumer confidence and fostered repeat purchases. Additionally, third-party marketplaces support sellers by offering established digital infrastructure, logistics solutions, marketing tools, and broader customer reach, enabling apparel businesses to expand their online presence effectively.

Company-owned platforms are expected to be the fastest-growing channel, with a projected CAGR of 5.05% during 2026–2031. This growth is driven by the increasing focus of apparel businesses on building direct digital relationships with consumers and delivering personalized shopping experiences. These platforms provide greater control over product presentation, customer engagement, pricing strategies, and brand identity, creating a more tailored and consistent online shopping journey. The integration of advanced digital tools, such as AI-powered recommendations, virtual try-on features, loyalty programs, and personalized promotions, is enhancing customer retention and encouraging repeat purchases. Furthermore, consumers are increasingly turning to official online stores and mobile applications to access exclusive collections, early product launches, customized products, and authentic merchandise.

Geography Analysis

Asia-Pacific accounted for a 37.55% share of global e-commerce apparel revenues in 2025, driven by the rapid growth of digital shopping ecosystems, high mobile commerce adoption, and increasing consumer engagement with online fashion platforms. This strong market position is supported by widespread internet accessibility, advanced digital payment systems, and a growing preference for convenient apparel shopping experiences. According to the State Council of the People’s Republic of China, China had 1.12 billion internet users by the end of 2025, underscoring the significant digital consumer base fueling online retail growth [3]Source: State Council of the People’s Republic of China, "China's internet user base hits 1.125 billion as AI adoption surges", gov.cn. The availability of diverse fashion collections, integration of social commerce, influencer-driven product discovery, and technology-enabled shopping features such as personalized recommendations and livestream shopping further reinforce Asia-Pacific’s leadership in the E-commerce Apparel Market.

South America is projected to be the fastest-growing region, with a CAGR of 5.11% during 2026–2031. This growth is supported by increasing digital adoption, expanding online retail infrastructure, and a rising consumer preference for convenient apparel purchasing channels. Enhancements in mobile shopping platforms, secure payment systems, logistics capabilities, and delivery networks are improving accessibility and encouraging more consumers to transition to online fashion purchases. The growing influence of social media, digital promotions, and trend-driven fashion consumption is further accelerating the adoption of e-commerce apparel platforms, positioning South America as the fastest-expanding regional market during the forecast period.

North America and Europe represent mature yet strategically significant markets, where growth is increasingly driven by AI-powered personalization, omnichannel retail strategies, and premium digital shopping experiences. Advanced technologies such as virtual fitting solutions, predictive recommendations, and data-driven customer engagement tools are enhancing online apparel conversion rates and fostering consumer loyalty. The Middle East and Africa (MEA) region is gaining traction through rising digital transformation, increasing mobile commerce adoption, improved logistics infrastructure, and the growing presence of online fashion platforms. Enhanced payment solutions, broader apparel accessibility, and evolving consumer preferences for digital-first shopping experiences are expected to support the continued growth of e-commerce apparel in these emerging markets.

Competitive Landscape

The global E-commerce Apparel Market is fragmented, with numerous global fashion brands, digital retailers, and specialized apparel companies competing through product innovation, digital transformation, and enhanced customer experiences. Key players in the market include Nike, Inc., Adidas AG, H & M Hennes & Mauritz AB, Lululemon Athletica Inc., and PVH Corp. Competition increasingly focuses on strengthening online channels, improving digital engagement, and expanding direct-to-consumer capabilities to align with evolving consumer shopping behaviors.

Market strategies emphasize technology integration, AI deployment, and online platform enhancement. Companies are prioritizing personalized and seamless shopping experiences by adopting AI-powered recommendations, virtual fitting technologies, data analytics, automated inventory systems, and mobile-first platforms. Investments in omnichannel ecosystems, loyalty programs, and digital supply chain capabilities further enable companies to differentiate themselves in a competitive market.

Additionally, companies are concentrating on sustainable fashion initiatives, faster product availability, exclusive online collections, and improved fulfillment services to enhance their market positions. Rising consumer demand for convenience, personalization, and responsible fashion is driving brands to adopt innovative materials, transparent sourcing practices, and efficient delivery solutions. As competition intensifies, continuous digital innovation, strong brand engagement, and enhanced online shopping experiences remain critical factors shaping the competitive dynamics of the global E-commerce Apparel Market.

E-commerce Apparel Industry Leaders

-

Nike, Inc.

-

Adidas AG

-

H & M Hennes & Mauritz AB

-

Lululemon Athletica Inc.

-

PVH Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Lululemon launched its e-commerce platform in Mexico to expand its integrated retail and digital presence, as well as its omnichannel capabilities in the market. The new e-commerce site aims to improve the customer experience.

- April 2025: Guess has launched its first dedicated e-commerce platform in India, expanding its digital retail presence in the country. The new website offers a range of men's and women's apparel, accessories, handbags, children's wear, and luggage.

- April 2025: Saks Fifth Avenue and Amazon Fashion have collaborated to introduce "Saks on Amazon," a new shopping experience within Luxury Stores at Amazon. This platform offers a curated selection of luxury merchandise from Saks Fifth Avenue, featuring women’s and men’s ready-to-wear collections.

Global E-commerce Apparel Market Report Scope

E-commerce apparel includes the buying and selling of fashion and apparel products online, specifically through e-commerce platforms. The E-commerce Apparel Market is segmented by product type, end user, fabric material, category, platform type, and geography. Based on product type, the market is segmented into formal wear, casual wear, sportswear, nightwear, intimate and loungewear, and other product types. Based on end user, the market is segmented into men, women, and children. Based on fabric material, the market is segmented into cotton, polyester, nylon, denim, and other fabric materials. Based on category, the market is segmented into mass and premium. Based on platform type, the market is segmented into third-party marketplace and company-owned platform. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Formal Wear |

| Casual Wear |

| Sportswear |

| Nightwear |

| Intimate and Loungewear |

| Other Product Types |

| Men |

| Women |

| Children |

| Cotton |

| Polyester |

| Nylon |

| Denim |

| Other Fabric Types |

| Mass |

| Premium |

| Third-Party Marketplace |

| Company-owned Platform |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Formal Wear | |

| Casual Wear | ||

| Sportswear | ||

| Nightwear | ||

| Intimate and Loungewear | ||

| Other Product Types | ||

| By End User | Men | |

| Women | ||

| Children | ||

| By Fabric Material | Cotton | |

| Polyester | ||

| Nylon | ||

| Denim | ||

| Other Fabric Types | ||

| By Category | Mass | |

| Premium | ||

| By Platform Type | Third-Party Marketplace | |

| Company-owned Platform | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of e-commerce apparel by 2031?

The E-commerce Apparel Market is forecast to reach USD 502.8 billion by 2031, up from USD 432 billion in 2026, at a CAGR of 3.1%.

Which region leads online apparel sales today?

Asia-Pacific led in 2025 with 37.6% of global revenue, supported by China’s large platform ecosystem and broad mobile-first buying behavior.

Which region is growing the fastest through 2031?

South America is projected to grow the fastest at a 5.1% CAGR, with Brazil remaining the main regional anchor.

Which product type is the largest and which is growing the fastest?

Casual wear was the largest segment in 2025 with 38.2% share, while sportswear is expected to grow the fastest at 4.1% CAGR through 2031.

Page last updated on: