Omega-3 Pet Supplement Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.58 Billion |

| Market Size (2031) | USD 2.56 Billion |

| Growth Rate (2026 - 2031) | 10.10% CAGR |

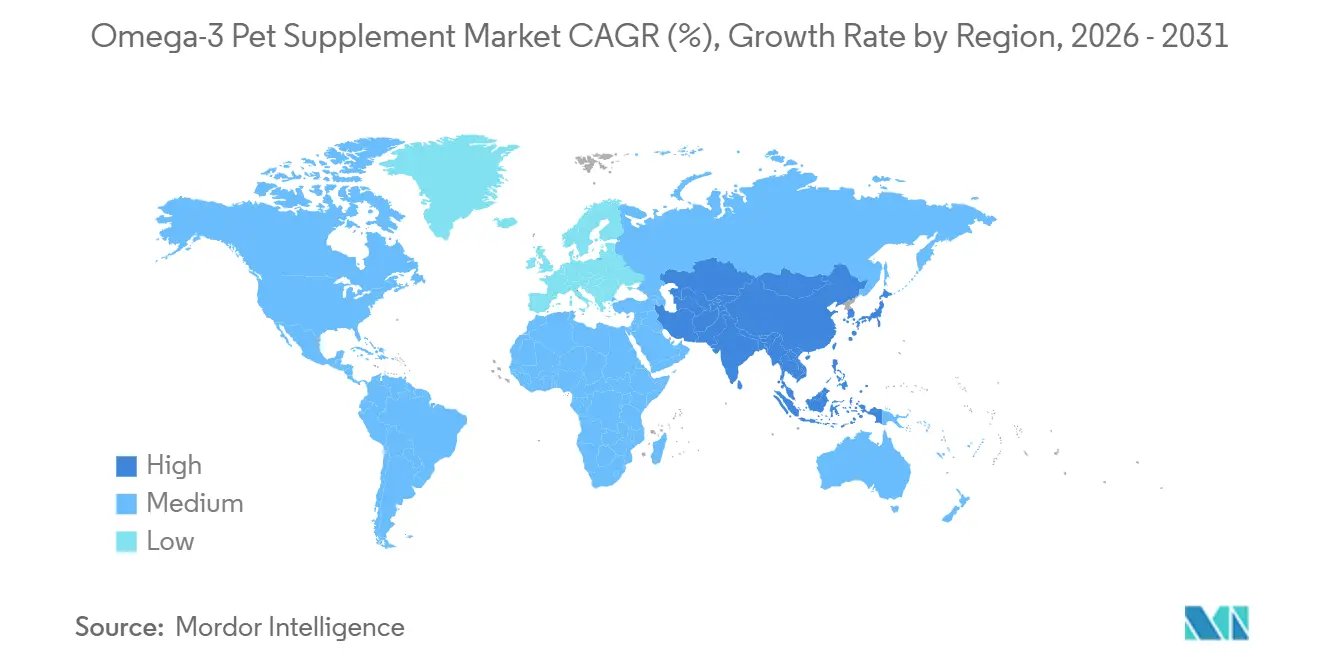

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

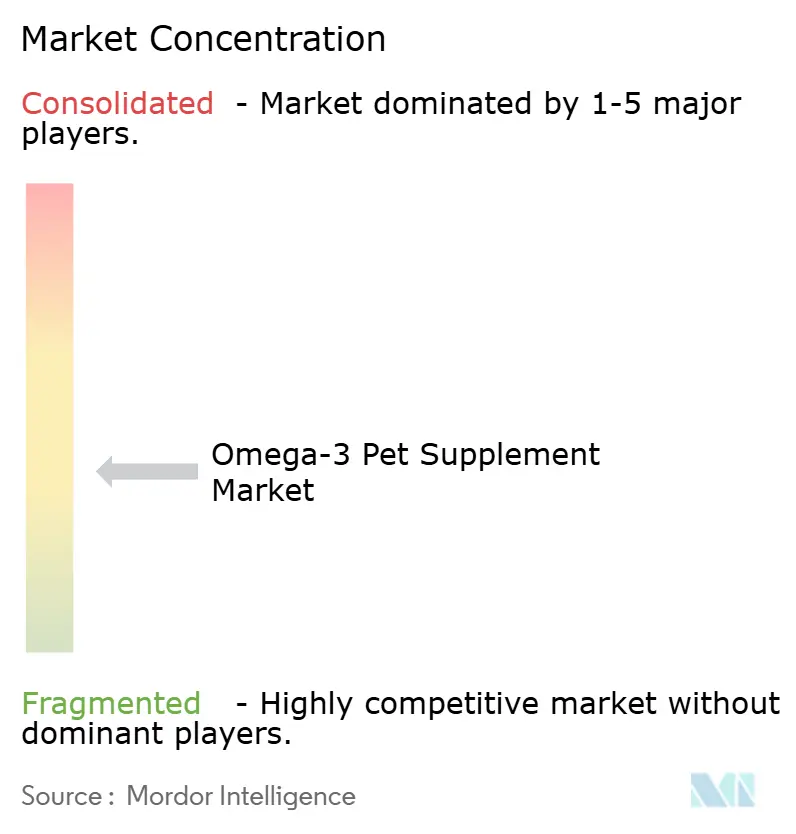

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Omega-3 Pet Supplement Market Analysis by Mordor Intelligence

The omega-3 pet supplement market size is projected to expand from USD 1.43 billion in 2025 and USD 1.58 billion in 2026 to USD 2.56 billion by 2031, registering a CAGR of 10.10% between 2026 and 2031. Rising acceptance of supplements as preventive care, growing clinical evidence of the efficacy of eicosapentaenoic acid and docosahexaenoic acid, and scalable algae fermentation that cushions supply shocks are shaping demand. Subscription-based e-commerce transforms one-time purchases into predictable revenue, while human-grade certification elevates quality expectations and margins. Regulatory updates in the United States and Europe clarify ingredient definitions and minimum inclusion levels, giving global brands a clearer route to market. Ingredient innovation, including phospholipid-bound and lysophosphatidylcholine-bound delivery systems, is improving bioavailability and palatability.

Key Report Takeaways

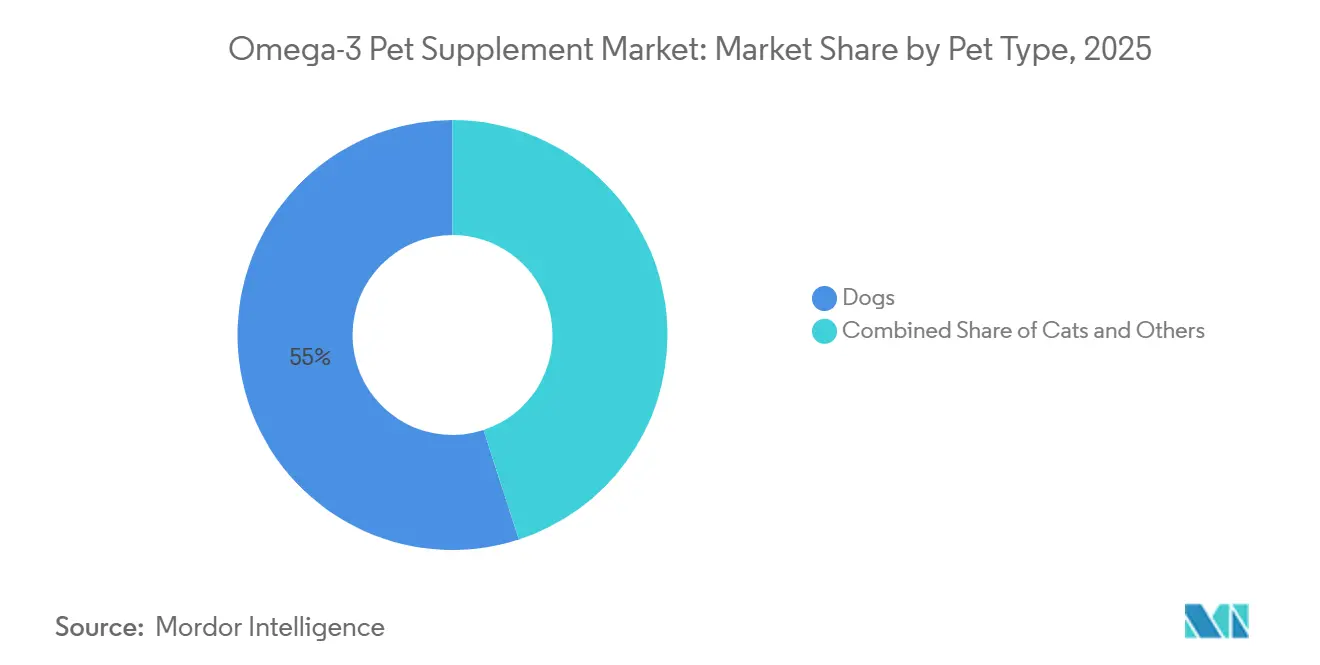

- By pet type, the omega-3 pet supplement market share for the dog segment led with 55% in 2025, while the cats segment is forecast to post the fastest 11.3% CAGR over 2026-2031.

- By product form, soft chews led with the largest share, accounting for 38% share in 2025, whereas capsules are forecast to post the fastest 10.6% CAGR through 2026-2031.

- By source, fish oil led with the largest share, accounting for 60% of the omega-3 pet supplement market size in 2025, yet algal oil is forecast to post the fastest 14.5% CAGR during 2026-2031.

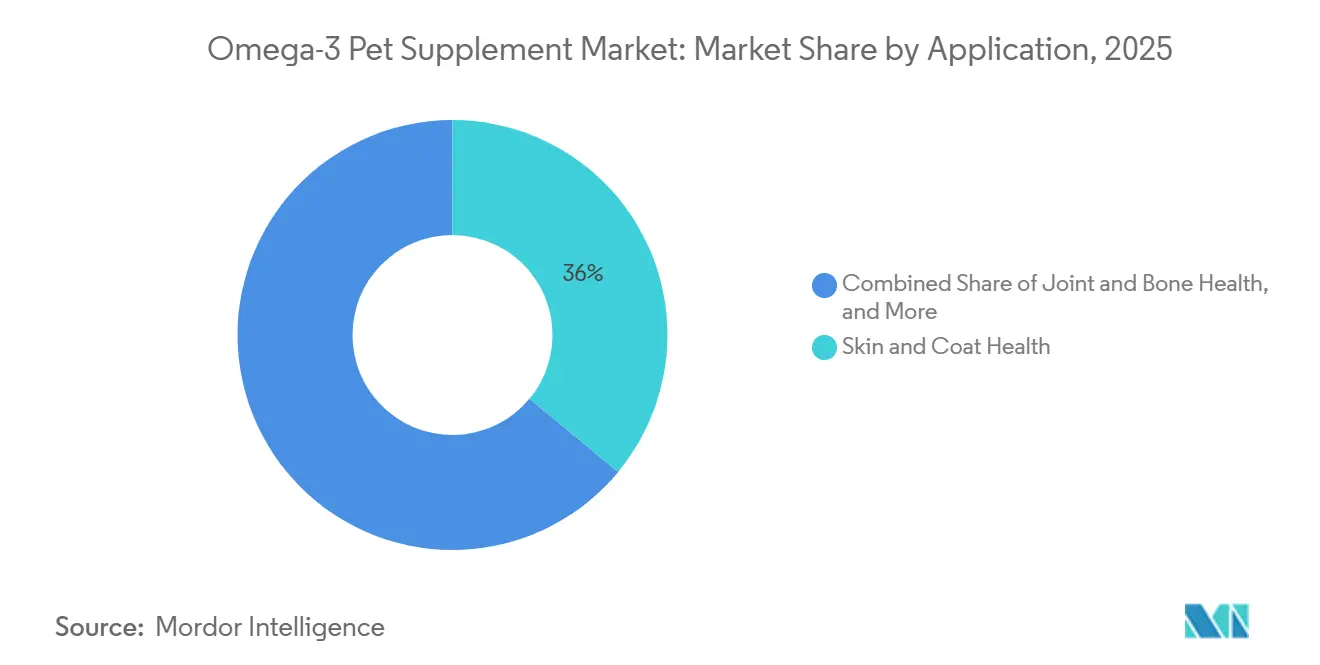

- By application, skin and coat health led with the largest share, accounting for 36% share of the market in 2025, whereas cognitive and vision support are forecast to post the fastest 12.2% CAGR to 2026-2031.

- By distribution channel, online retailers led with the largest share, accounting for 30% share in 2025, and they are forecast to grow at the fastest 16% CAGR through 2026-2031.

- By geography, North America accounted for the largest 38.5% market share in 2025, while Asia-Pacific region is projected to grow at the fastest CAGR of 10.7% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Omega-3 Pet Supplement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Human-grade ingredient demand in pet nutrition | +2.1% | Global with strength in North America and Western Europe | Medium term (2-4 years) |

| Clinical validation of Eicosapentaenoic Acid (EPA)/Docosahexaenoic Acid (DHA) for joint and cognitive health | +2.5% | Global veterinary communities | Long term (≥ 4 years) |

| Veterinary-led preventive-care programs | +1.8% | North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| E-commerce subscription models for functional treats | +2.0% | Global, with high uptake in North America | Short term (≤ 2 years) |

| Algae-derived omega-3 scalability lowering cost curve | +1.2% | Production is centered in North America and Europe | Long term (≥ 4 years) |

| Artificial Intelligence (AI)-driven personalized dosing and tele-vet platforms | +0.5% | North America and select Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Human-grade ingredient demand in pet nutrition

Pet owners increasingly expect pet supplements to adhere to the same manufacturing and safety standards as human food. The Association of American Feed Control Officials (AAFCO) specifies that products labeled as human grade must be manufactured, packed, and stored in compliance with regulations applicable to human edible foods. These standards enhance quality control, ingredient traceability, and manufacturing practices across the industry, enabling premium brands to differentiate their products and build consumer trust in fortified pet nutrition offerings. Manufacturers without these certifications are exiting or consolidating, as demonstrated by several contract manufacturing deals disclosed in 2025. Nordic Naturals extended its human omega-3 line to pets in 2025 and reached 10% share by highlighting identical sourcing and testing. Retailers are increasingly favoring pet supplement brands that carry the National Animal Supplement Council (NASC) Quality Seal, as it signifies adherence to established quality and safety standards while enhancing premium product positioning.

Clinical validation of Eicosapentaenoic Acid (EPA)/Docosahexaenoic Acid (DHA) for joint and cognitive health

A 2025 systematic review established specific dosing ranges for EPA and DHA in dermatology, osteoarthritis, cardiology, and cognition, transitioning from anecdotal use to evidence-based protocols. This clarity has increased veterinarian confidence and encouraged clinic recommendations, accounting for 28% of 2025 channel sales[1]Source: Lenox, C.E. et al., “Exploring the Efficacy and Optimal Dosages of Omega-3 Supplementation for Companion Animals,” cambridge.org.. The European Pet Food Industry Federation (FEDIAF) included minimum levels of EPA and DHA in its 2025 nutrient guidelines, emphasizing their significance in companion animal nutrition. Additionally, veterinary colleges are integrating omega-3 modules into nutrition curricula, expanding the future prescribing base. With the growing body of peer-reviewed data, product labels now frequently specify precise per-kilogram dosing to align with clinically supported ranges.

Veterinary-led Preventive Care Programs

Veterinary practices are bundling annual wellness exams, vaccinations, and targeted supplements into prepaid plans. The American Animal Hospital Association reaffirmed the need for nutrition assessment at every visit in its 2024 guidelines, legitimizing the sale of supplements in clinics[2]Source: American Animal Hospital Association, “Canine and Feline Nutrition Guidelines 2021,” aaha.org. Purina launched a skin health omega-3 line through clinics in 2025, using the veterinarian’s role as a trusted adviser. Wellness plans stabilize clinic revenue while improving compliance, and clinics benefit from dual margins on services and product sales. In response, brands are formulating professional-only versions with higher Eicosapentaenoic Acid (EPA) and Docosahexaenoic Acid (DHA) per serving to differentiate from retail packs.

Algae-Derived Omega-3 Scalability Lowering Cost Curve

Fermentation-based production decouples omega-3 supply from anchovy quotas. In April 2026, DSM-Firmenich added an Eicosapentaenoic Acid (EPA)-rich algae oil that mirrors fish oil ratios, unlocking joint health formulations. Aker BioMarine is developing Revervia algae oils alongside its krill portfolio to diversify feedstock. As new fermenters come online, the cost per kilogram of EPA and Docosahexaenoic Acid (DHA) is projected to match refined fish oil late this decade. Sustainability certification from the Marine Stewardship Council and Life Cycle Analysis scoring are appearing on labels, satisfying eco-conscious consumers. Lower input volatility and clearer traceability encourage multiyear supply contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Marine oil price volatility | -1.8% | Global with an acute effect on Peru-dependent supply chains | Short term (≤ 2 years) |

| Oxidative stability and shelf-life limits | -1.2% | Higher risk in the Middle East and Africa | Medium term (2-4 years) |

| Patchy regulatory alignment across regions | -0.9% | United States, European Union, and Asia-Pacific | Long term (≥ 4 years) |

| Palatability issues with high Eicosapentaenoic Acid (EPA) oils | -0.7% | Feline products globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Marine-Oil Price Volatility

Peru cut its 2026 anchovy quota by 36%, squeezing global fish oil availability and lifting refined concentrate prices to USD 3,800 per metric ton[3]Source: Peruvian Ministry of Production, “Anchovy Quota Reduction 2026,” gob.pe. Rabobank projected a 20,000 metric ton deficit in the same year as aquaculture demand surged. Manufacturers either stockpile inventory, accept margin erosion, or raise prices, risking a shift by consumers to cheaper plant blends that provide limited Eicosapentaenoic Acid (EPA) and Docosahexaenoic Acid (DHA). Volatility complicates long-term contracts and investor forecasts. Accelerated algae commercialization offers a hedge but remains constrained by capacity today.

Oxidative Stability and Shelf-Life Limits

Eicosapentaenoic Acid (EPA) and Docosahexaenoic Acid (DHA) oxidize when exposed to heat, oxygen, or light, producing rancid odors that deter pets. A 2025 study found several retail fish oil products exceeded peroxide limits months before expiry. Manufacturers invest in nitrogen flushing, antioxidant blends, and opaque packaging, adding 15% to 25% to the cost. Cold-chain logistics raise distributor expenses, especially in hot climates across the Middle East and Africa. Microencapsulation improves stability but currently inflates ingredient costs by up to 30%, limiting use to premium lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pet Type: Canine Leadership and Feline Upside

In 2025, dogs accounted for 55% of the omega-3 pet supplement market share, reflecting higher spend per animal and established veterinary joint-care protocols. Clinical evidence positions the Eicosapentaenoic Acid (EPA) and Docosahexaenoic Acid (DHA) as adjuncts in the management of osteoarthritis in large breeds, supporting dog owners' willingness to pay. Nutravet’s April 2025 Nutramega launch targets this demographic with an EPA-rich formula for mobility and dermatology. Cats are projected to expand at 11.3% CAGR through 2026-2031 as awareness of feline cognitive dysfunction syndrome rises. Capsule formats that owners puncture over wet food are gaining traction, easing historical palatability barriers.

Veterinarians possess decades of canine dosage data, fostering confident prescriptions that drive clinic sales. Feline research, while limited, is growing as universities run cognition studies funded by ingredient suppliers. Younger cat owners rely on social media advice, helping direct-to-consumer brands bypass clinic endorsement. Other pets, including horses and birds, form a niche that prizes omega-3 for joint comfort and feather quality, but volumes remain modest. Future growth hinges on labeling that specifies species-appropriate dosages and flavor masking that respects feline taste sensitivity.

By Product Form: Soft Chews Dominate while Capsules Accelerate

Soft chews accounted for 38% of sales in 2025, turning supplements into treat experiences that eliminate dosing battles. Zesty Paws doubled social media investment in 2025, using influencer content to normalize daily soft-chew routines. However, chew format limits fatty acid loading, prompting owners of large dogs to administer multiple pieces. Capsules will grow at a 10.6% CAGR, driven by microencapsulation, which enhances stability, and by algae oils, which enable smaller pill sizes. DSM-Firmenich’s Life’s Docosahexaenoic Acid (DHA) B54-0100, released in October 2024, extended shelf life beyond 24 months in sealed blister packs.

Liquids remain favored in clinics for precise titration, but oxidation risk and messy application hinder retail growth. Powders sprinkled on food serve multi-pet households looking for cost savings, although inconsistent mixing limits efficacy. Format preference often aligns with pet size. Small dogs and cats tend to prefer capsules and chews, while owners of giant breeds prefer liquids. As brands roll out multi-functional chews that combine omega-3 with probiotics or glucosamine, category boundaries blur. Certification by the National Animal Supplement Council is becoming mandatory across every format tier.

By Source: Fish Oil Strength and Algal Oil Upsurge

Fish oil accounted for 60% of the omega-3 pet supplement market size in 2025, on the back of mature supply chains and a price advantage. Supply pressure after Peru’s 2026 quota cut, though, has spotlighted sustainability risks. Algal oil will post the fastest 14.5% CAGR as industrial fermenters reach scale and cost parity. DSM-Firmenich’s April 2026 expansion added an Eicosapentaenoic Acid (EPA)-balanced algae option that solves prior DHA-only limitations. Krill oil holds a premium niche, prized for phospholipid absorption but constrained by Antarctic harvest caps.

Blended formulas mixing fish and algae hedge price and perception risks. Plant oils like flax contain alpha-linolenic acid but are inefficiently converted in dogs and cats, limiting their therapeutic use. Ingredient traceability labeling, including QR codes linking to fishery certificates, is becoming standard. As algae production migrates to Asia to serve local brands, regional supply chains will diversify. Cost convergence by 2029 could invert the historical hierarchy, shifting volume from marine to microbial sources.

By Application: Skin and Coat Health Largest and Cognitive and Vision Support Fastest

Skin and coat health commanded 36% share in 2025, benefiting from quick, visible improvements that encourage repurchase. Purina introduced a veterinary-exclusive omega-3 skin line in May 2025, cementing clinician trust. Joint and Bone Health sits in second place, underpinned by long-running osteoarthritis data. Cognitive and vision support is growing at a 12.2% CAGR as owners notice behavioral changes in aging pets and breeders feed Docosahexaenoic Acid (DHA) to puppies for developmental benefits. Cardio-renal support serves geriatric pets diagnosed with chronic diseases, representing a small but high-value niche.

Evidence-based dosing ranges published in June 2025 specify milligrams per kilogram for each condition, empowering veterinarians to write precise scripts. Ingredient firms now tailor delivery systems, such as lysophosphatidylcholine carriers, for brain applications. Marketing messaging is shifting from generic wellness to condition-specific outcomes, mirroring human nutraceutical segmentation. Regulatory bodies scrutinize disease claims, so brands use structure-function language, such as “supports cognitive function,” to remain compliant. Cross-application blends are emerging, but excessive label complexity risks confusing consumers.

By Distribution Channel: Online Subscriptions Transform Access

Online retailers accounted for 30% of 2025 revenue, with subscription models growing at a 16% CAGR from 2026 to 2031. Chewy’s autoship penetration demonstrated that pet owners accept automated refill of consumables. Veterinary clinics leverage prescriber authority and therapeutic positioning. Pet specialty stores, offering staff guidance and experiential services like grooming, cement loyalty. Supermarkets and hypermarkets remain minor outlets due to limited shelf space for specialized supplements.

Direct-to-consumer brands utilize first-party data to strategically launch complementary products. Clinics protect their market share by incorporating supplements into wellness plans and highlighting medical supervision. Specialty chains introduce loyalty programs that reward repeat supplement purchases with points, similar to airline rewards systems. Brick-and-mortar retailers implement endless-aisle kiosks to showcase online-exclusive products without bearing inventory risks. Channel convergence is increasingly observed among e-commerce platforms, as they integrate physical stores and digital channels to enhance customer experience.

Geography Analysis

North America remains the largest regional contributor, capturing 38.5% of global revenue in 2025. High veterinary visit frequency, widespread pet insurance reimbursement, and mature e-commerce infrastructure sustain its momentum. Asia-Pacific is the fastest region, projected to advance at a 10.7% CAGR over 2026-2031 as rising middle-class incomes and urbanization lift premium pet spending. Growing regulatory clarity and an expanding veterinary workforce further anchor long-term demand in both regions.

Europe follows with steady growth, driven by a strong veterinary culture and recent nutrient guidelines that standardize minimum levels of Eicosapentaenoic Acid (EPA) and Docosahexaenoic Acid (DHA) set by European Pet Food Industry Federation (FEDIAF). South America benefits from rapid urbanization and improving retail access, though price sensitivity tempers premium adoption. The Middle East and Africa are building momentum as distributors introduce shelf-stable soft-chew formats suited to hot climates. Each of these regions is diversifying supply sources, including algae-derived oils, to hedge marine price swings.

Across all regions, subscription e-commerce and veterinary wellness plans are deepening repeat purchase behavior. Ingredient suppliers are localizing fermentation plants, reducing transit times, and improving freshness, thereby boosting regional competitiveness. Regulatory bodies continue to harmonize labeling standards, reducing compliance hurdles for multinational brands. These converging factors suggest that every territory will widen its contribution to global revenue through 2031, reinforcing robust overall market expansion.

Competitive Landscape

The omega-3 pet supplement market is moderately fragmented, with the top five key players including Nutramax Laboratories, Nordic Naturals, Zesty Paws LLC, Grizzly Pet Products, LLC, and VetriScience Laboratories. Nutramax Laboratories anchors this leadership pack by distributing only through veterinary clinics, a strategy that commands premium pricing and cements medical credibility. Nordic Naturals matches human-grade sourcing and third-party testing across its pet line, which earns trust among specialty retailers and wellness-focused owners. Both companies invest in peer-reviewed research and quality-seal programs, making it costly for clinics and consumers to switch brands.

Zesty Paws LLC captures fast volume growth by pairing soft-chew formats with social-media subscriptions that harvest first-party data for quick formula tweaks. Grizzly Pet Products, LLC secures supply stability and cost control through vertical integration with salmon-oil fisheries, positioning itself as a reliable partner when marine oil prices swing. VetriScience Laboratories relies on decades of clinic relationships and consistent compliance with the National Animal Supplement Council to retain professional loyalty. Together, these three brands compete on flavor systems, delivery forms, and targeted condition claims such as skin, coat, and mobility support.

Looking forward, consolidation is likely as food conglomerates shop for functional portfolios and as raw-material suppliers move downstream to lock in retail visibility. Feline-specific palatable formats, algae-derived oils for environmentally minded shoppers, and cognitive support blends for senior dogs represent clear whitespace. Rising audit rigor from the National Animal Supplement Council and tougher retailer standards will lift entry barriers, favoring well-capitalized firms that can fund continuous testing. Personalized dosing algorithms and tele-veterinary platforms are anticipated to expand the total addressable market, offering major players new opportunities for premium growth.

Omega-3 Pet Supplement Industry Leaders

Nutramax Laboratories

Nordic Naturals

Zesty Paws LLC

Grizzly Pet Products, LLC

VetriScience Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: DSM-Firmenich expanded its Veramaris algae omega-3 line, adding an EPA-rich variant for pet applications. The new balanced profile strengthens supply security beyond marine sources and is likely to accelerate adoption among environmentally conscious owners, supporting long-term category expansion.

- May 2025: Nestlé Purina PetCare launched Purina Pro Plan Veterinary Supplements Skin Care, a clinic-exclusive omega-3 range. By anchoring the product inside veterinary channels, the brand reinforces professional trust and drives premium pricing, which lifts overall market value.

- April 2025: Nutravet introduced Nutramega, a blend of Eicosapentaenoic Acid (EPA) and Docosahexaenoic Acid (DHA) for canine joint and skin benefits. The targeted formulation widens therapeutic use cases and encourages repeat purchases in the aging dog segment, adding incremental volume to market growth.

Global Omega-3 Pet Supplement Market Report Scope

Omega-3 pet supplements are dietary additives, primarily derived from fish oil and rich in EPA and DHA, formulated to support immune function, skin health, joint health, and heart health in dogs and cats.

The Omega-3 pet supplement market is segmented by pet type into dogs, cats, and other pets; by product form into soft chews, liquids, capsules, and powders; by source into fish oil, algal oil, krill oil, and flaxseed; by application into skin health and coat health, joint and bone health, cognitive sand vision upport, cardiovascular and support, and general wellness; by distribution channel into veterinary clinics, pet specialty stores, supermarkets and hypermarkets, and online retailers; and by geography into North America, Europe, Asia-Pacific, South America, Middle East, and Africa. The market forecasts are provided in terms of value (USD).

| Dogs |

| Cats |

| Other Pets |

| Soft Chews |

| Liquid |

| Capsules |

| Powders |

| Fish Oil |

| Algal Oil |

| Krill Oil |

| Flaxseed |

| Skin and Coat Health |

| Joint and Bone Health |

| Cognitive and Vision Support |

| Cardiovascular and Renal Support |

| General Wellness |

| Veterinary Clinics |

| Pet Specialty Stores |

| Supermarkets and Hypermarkets |

| Online Retailers |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Pet Type | Dogs | |

| Cats | ||

| Other Pets | ||

| By Product Form | Soft Chews | |

| Liquid | ||

| Capsules | ||

| Powders | ||

| By Source | Fish Oil | |

| Algal Oil | ||

| Krill Oil | ||

| Flaxseed | ||

| By Application | Skin and Coat Health | |

| Joint and Bone Health | ||

| Cognitive and Vision Support | ||

| Cardiovascular and Renal Support | ||

| General Wellness | ||

| By Distribution Channel | Veterinary Clinics | |

| Pet Specialty Stores | ||

| Supermarkets and Hypermarkets | ||

| Online Retailers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the omega-3 pet supplement market be by 2031?

The omega-3 pet supplement market size is projected to reach USD 2.56 billion by 2031, growing at a 10.10% CAGR over 2026-2031.

Which pet type buys the most omega-3 supplements?

Dogs accounted for 55% of the omega-3 pet supplement market share in 2025, reflecting higher spend per animal and established veterinary protocols.

Which application will grow the fastest over 2026-2031?

Cognitive and vision support is forecast to post the fastest 12.2% CAGR as owners address aging-related behavioral issues.

What is the leading distribution channel today?

Online retailers accounted for 30% of 2025 sales and are expanding fastest, with a 16% CAGR through 2031, driven by autoship subscription models.

Page last updated on: