Canada Pet Nutraceuticals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

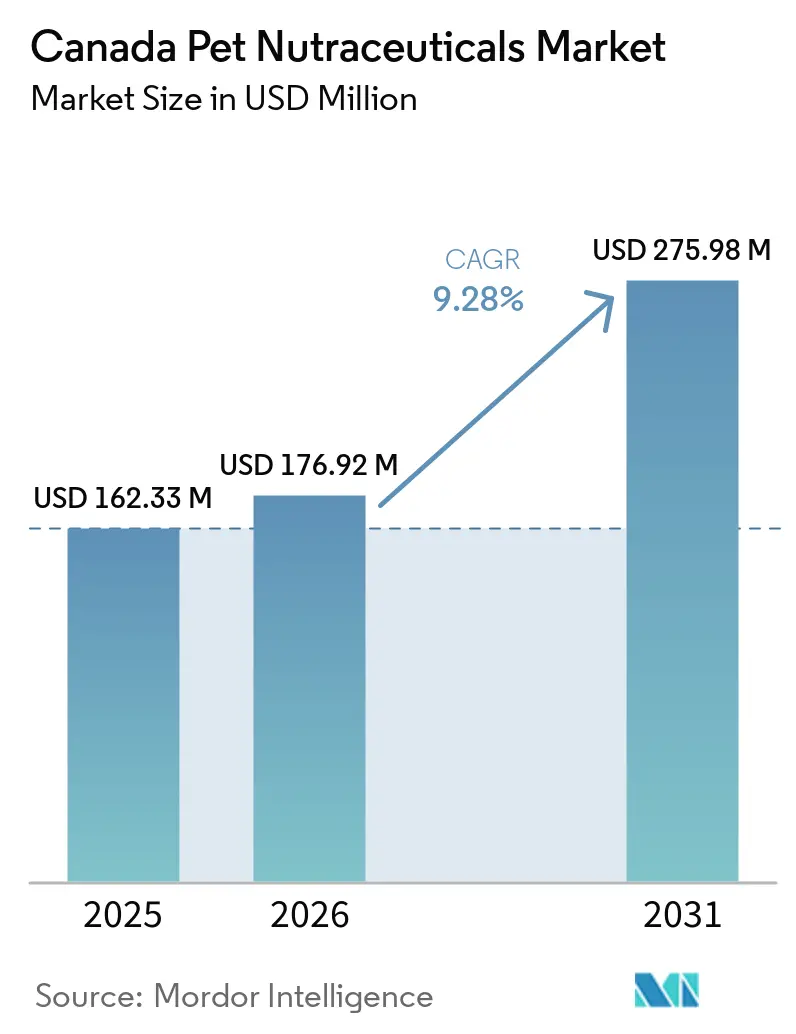

| Base Year Market Size (2025) | USD 162.33 Million |

| Market Size (2026) | USD 176.92 Million |

| Market Size (2031) | USD 275.98 Million |

| Growth Rate (2026 - 2031) | 9.28% CAGR |

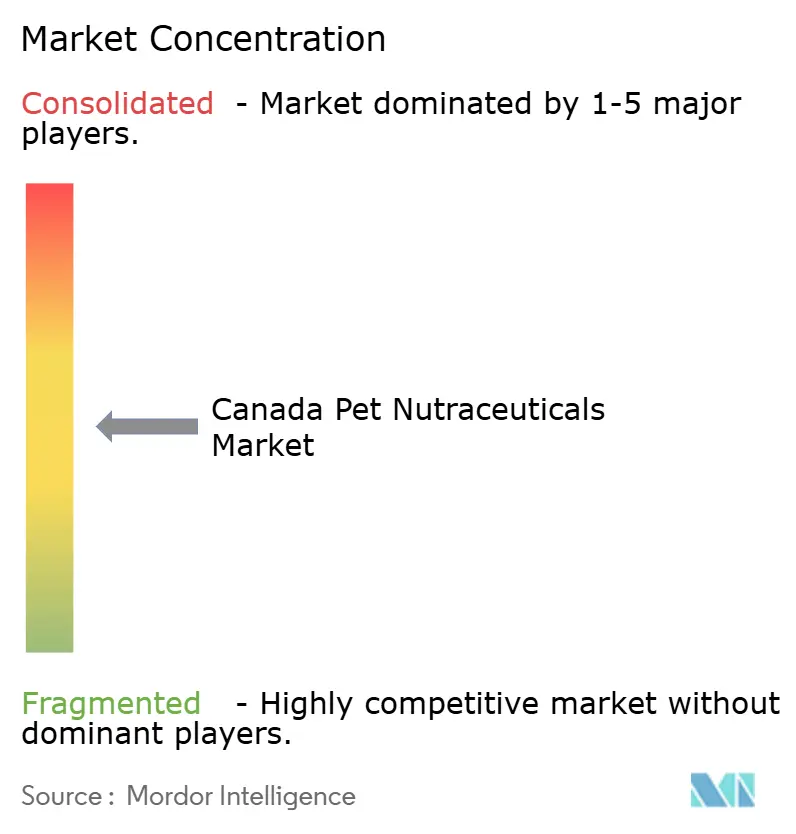

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Pet Nutraceuticals Market Analysis by Mordor Intelligence

The Canada pet nutraceuticals market was valued at USD 162.33 million in 2025 and is projected to grow from USD 176.92 million in 2026 to USD 275.98 million by 2031, registering a CAGR of 9.28% during the forecast period (2026-2031). The market is driven by factors such as increasing pet humanization, a growing emphasis on preventive healthcare, and the influence of veterinarians in promoting supplement adoption, particularly for applications such as joint health, digestive wellness, immunity, and healthy aging. Premiumization trends are fueling demand for scientifically formulated products that feature clinically supported ingredients, clean-label claims, and transparent sourcing. Additionally, e-commerce platforms and subscription-based purchasing models are enhancing product accessibility and encouraging repeat purchases. Dogs remain the dominant consumer segment due to higher healthcare spending, while demand for feline nutraceuticals is rising, supported by increasing cat ownership and growing health awareness among cat owners. Urban provinces such as Ontario, Quebec, and British Columbia contribute significantly to market demand, driven by higher disposable incomes and advanced pet care infrastructure.

Key Report Takeaways

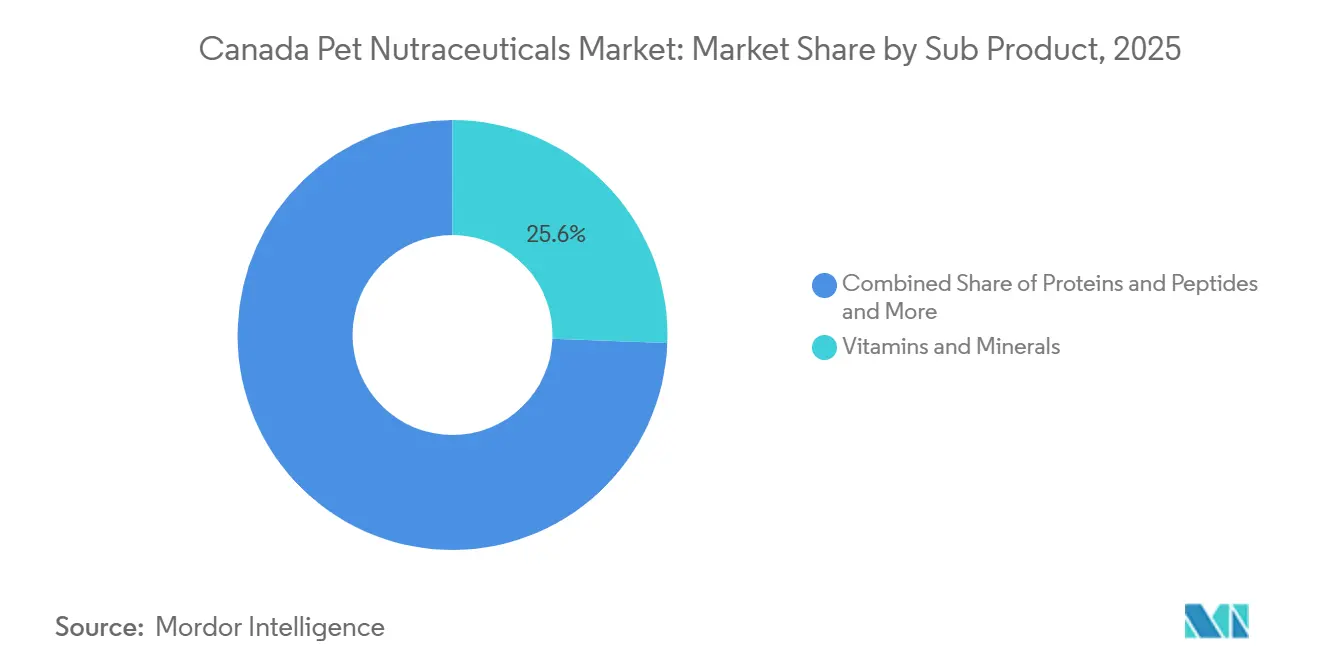

- By sub product, the Canada pet nutraceuticals market share for vitamins and minerals accounted for the largest 25.6% in 2025, and it is projected to expand at the fastest 9.8% CAGR from 2026 to 2031.

- By pets, dogs held the largest 45.0% share in 2025, while the Canada pet nutraceuticals market size for cats is forecast to grow at the fastest CAGR of 10.2% from 2026 to 2031.

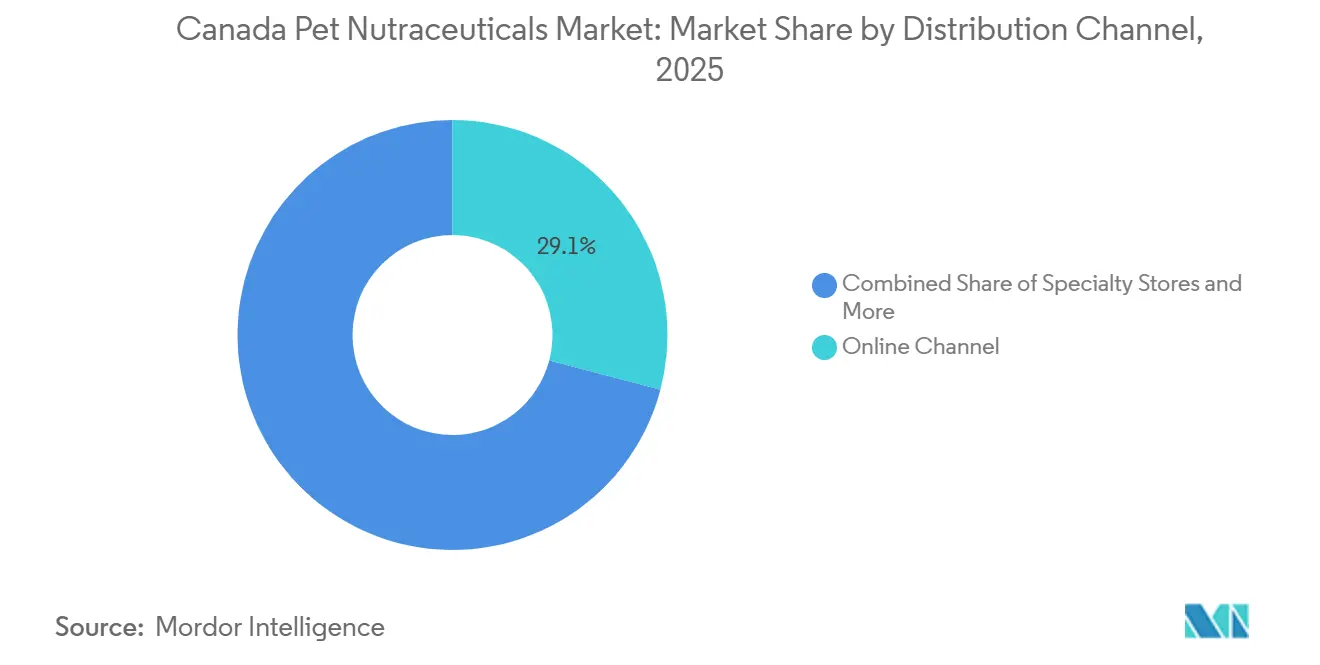

- By distribution channel, the online channel captured the largest share at 29.1% in 2025, while the online channel is projected to grow at the fastest CAGR of 10.1% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Pet Nutraceuticals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pet humanization and preventive health spending | +2.1% | National, concentrated in Toronto, Vancouver, Calgary, and Montreal metropolitan areas | Short term (≤ 2 years) |

| Aging pet population and chronic condition management | +1.6% | National, with early momentum in Ontario and British Columbia senior-pet households | Long term (≥ 4 years) |

| Veterinary endorsement of functional ingredients | +1.3% | National, strongest in clinic-dense urban centers in Ontario, Quebec, and British Columbia | Medium term (2-4 years) |

| E-commerce and subscription adoption for repeat purchase categories | +1.4% | National, strongest in metropolitan corridors with high broadband penetration | Short term (≤ 2 years) |

| Premiumization of health-positioned pet nutrition | +1.0% | National, with premium price elasticity concentrated in Ontario and British Columbia | Medium term (2-4 years) |

| Demand for local, clean-label, and traceable products | +0.8% | Quebec and British Columbia as early adopters, followed by Alberta and Ontario | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pet Humanization and Preventive Health Spending

The rising trend of pet humanization and an increasing focus on preventive healthcare, as pet owners are investing in wellness-oriented products to address potential health issues before they become severe. According to the 2024 Canadian Pet Population Survey, published in March 2025, dogs visited veterinarians an average of twice per year, while cats visited veterinarians once per year [1]Source: Canadian Animal Health Institute (CAHI), “Canadian Pet Population Survey Highlights the Importance of Access to Veterinary Care,” cahi-icsa.ca.. This data underscores the strong commitment of pet owners to routine healthcare and professional wellness advice. Frequent veterinary visits have contributed to the growing adoption of nutraceutical products, including probiotics, joint-support supplements, omega-3 formulations, and digestive health solutions, as pet owners prioritize their pets' long-term health and quality of life.

Aging Pet Population and Chronic Condition Management

The growing awareness of age-related health issues in companion animals and the increasing adoption of preventive wellness solutions for senior pets are driving the demand for pet nutraceutical products. Guidance from Veterinary Centers of America (VCA) Canada Animal Hospitals highlights that aging dogs and cats may face reduced nutrient absorption due to metabolic changes and weakened immune systems, making them more prone to infections. As a result, pet owners are incorporating nutraceutical products such as omega fatty acids, probiotics, digestive enzymes, glucosamine, coenzyme Q-10, and L-carnitine into their pets' daily care routines. These products promote healthy aging, mobility, digestive health, and overall quality of life, thereby contributing to the growth of the industry.

Veterinary Endorsement of Functional Ingredients

The market is witnessing growth due to increasing veterinarian confidence in products that adhere to established regulatory standards and ingredient transparency requirements. Health Canada's September 2024 guidance on List C Veterinary Health Products mandates that these products must include permitted active, homeopathic, or traditional medicine substances and comply with conditions regarding route of administration, species eligibility, labeling, and ingredient use. These regulations promote product consistency and quality while encouraging manufacturers to create evidence-based formulations. As veterinarians increasingly recommend supplements that meet these regulatory standards, consumer trust in functional ingredients is bolstered, driving market growth across Canada.

Premiumization of Health-Positioned Pet Nutrition

Increasing consumer willingness to invest in premium products that provide targeted health benefits and are backed by scientific research. For instance, Agriculture and Agri-Food Canada’s 2025 analysis of pet food trends highlights the rising prominence of functional claims, such as digestive health, joint and bone support, and probiotic benefits, in new dog and cat product launches in Canada[2]Source: Agriculture and Agri-Food Canada, “Sector Trend Analysis Pet Food Trends in Canada,” agriculture.canada.ca.. The emphasis on these health-focused claims indicates a broader shift toward premium nutrition solutions designed to address specific wellness needs rather than general supplementation. This trend is driving the adoption of higher-value products and prompting manufacturers to expand their portfolios with condition-specific nutraceutical offerings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium price sensitivity outside core urban households | -1.3% | Rural and suburban markets in Prairie provinces, Atlantic Canada, and non-metropolitan Quebec | Short term (≤ 2 years) |

| Limited clinical differentiation across many supplement claims | -1.0% | National, affecting mid-tier brands across all channels | Medium term (2-4 years) |

| Ingredient sourcing volatility for marine and specialty actives | -0.8% | National, with supply chain exposure in omega-3 and collagen peptide categories | Medium term (2-4 years) |

| Compliance risk around structure-function and therapeutic claims | -0.7% | National, most acute for small and mid-sized brands entering the veterinary channel | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Clinical Differentiation Across Many Supplement Claims

The lack of significant clinical differentiation among many pet nutraceutical formulations remains a challenge for industry growth. In Canada, pet supplements are primarily marketed as Veterinary Health Products (VHPs), a classification established by Health Canada for low-risk products aimed at maintaining or promoting animal health and welfare, rather than diagnosing, treating, curing, or preventing diseases. Consequently, products in categories such as joint health, digestive health, immune support, and healthy aging often feature similar wellness-oriented claims. This similarity makes it challenging for pet owners and veterinarians to evaluate products based on clinically validated efficacy. Furthermore, the absence of pharmaceutical-level efficacy requirements for many supplement categories undermines confidence in performance claims, complicates product comparisons, and hinders the adoption of premium nutraceutical formulations, thereby restricting industry growth.

Ingredient Sourcing Volatility for Marine and Specialty Actives

The Canada pet nutraceuticals market encounters challenges in sourcing marine- and animal-derived ingredients, which are commonly used in formulations for omega-3, collagen, and joint health. As per the Canadian Food Inspection Agency's April 2024 update on pet supplement import requirements, supplements containing animal-origin ingredients must include a zoosanitary certificate endorsed by an official veterinarian from the country of origin[3]Source: Canadian Food Inspection Agency (CFIA), “Changes to Import Requirements for Pet Supplements,” inspection.canada.ca. This regulation applies to various specialty ingredients, such as fish oils, collagen, and green-lipped mussel powder, thereby increasing regulatory oversight for imported raw materials. The additional compliance requirements complicate sourcing strategies and reduce supply flexibility for manufacturers, especially those reliant on internationally sourced specialty ingredients.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Product: Vitamins and Minerals Lead, Probiotics Gain Relevance

The Canada pet nutraceuticals market share for vitamins and minerals accounted for 25.6% in 2025, the largest share within the market. Vitamins and minerals maintain their leading position due to their ability to address a wide range of wellness needs across various pet life stages and health conditions. Their versatility enables their inclusion in formats such as soft chews, powders, liquids, tablets, and food toppers, contributing to broad consumer acceptance. Manufacturers continue to develop formulations targeting immune health, skin and coat care, bone strength, and healthy aging. Compatibility with routine feeding practices and preventive care strategies further drives sustained demand for these products within the companion animal nutrition market.

Vitamins and minerals are projected to grow at the fastest CAGR of 9.8% from 2026 to 2031. This growth is driven by an increasing preference for targeted micronutrient supplementation over general wellness blends. Pet owners are prioritizing products designed for specific outcomes, such as cognitive support, digestive health, mobility enhancement, and immune system resilience. Veterinary recommendations continue to endorse the use of condition-specific vitamin and mineral products as part of preventive care programs. Manufacturers are addressing this demand by improving ingredient quality, enhancing palatability, and offering convenient delivery formats, ensuring the segment remains competitive within the expanding pet nutraceutical market.

By Pets: Dogs Hold the Largest Base, Cats Expand Faster

Dogs held the largest 45.0% share in 2025. This dominance is attributed to higher owner engagement with preventive healthcare, wellness supplementation, and routine veterinary consultations. Key nutraceutical categories for dogs include joint health, digestive support, skin and coat wellness, and mobility-focused products. The segment benefits from a diverse range of product formats and formulations tailored to various breeds, sizes, and life stages. These factors position dogs as the primary focus for premium nutraceutical innovation and commercialization.

The Canada pet nutraceuticals market size for cats is projected to grow at the fastest CAGR of 10.2% from 2026 to 2031. Meanwhile, cat-focused nutraceutical products are gaining traction as manufacturers develop formulations that address feline-specific nutritional needs and behavioral traits. Increasing demand is observed for products targeting digestive wellness, immune function, urinary health, stress management, and healthy aging. Additionally, product developers are emphasizing palatable delivery systems to enhance compliance among cats. Growing awareness of feline health requirements, coupled with rising premium pet care spending, is driving broader adoption of specialized nutraceutical solutions and supporting faster growth in the cat segment.

By Distribution Channel: Online Leads Growth, Specialty Holds Premium Value

The online channel accounted for the largest share at 29.1% in 2025. Online platforms have gained prominence due to their convenience, product variety, subscription purchasing options, and direct access to consumer reviews. These digital channels enable pet owners to efficiently compare formulations, ingredient profiles, and health claims, which is less feasible in traditional retail settings. Additionally, the recurring nature of many nutraceutical products aligns well with autoship programs and replenishment models, fostering strong customer retention and driving the shift toward online purchasing across various pet health and wellness categories.

The online channel is projected to grow at the fastest CAGR, 10.1%, from 2026 to 2031. Specialty retailers, veterinary clinics, and direct-to-consumer channels remain critical for products requiring education, professional guidance, or condition-specific recommendations. These outlets enhance premium positioning by helping consumers understand ingredient benefits, usage protocols, and wellness objectives. Meanwhile, supermarkets and mass-market retailers cater to value-oriented buyers with accessible pricing and broad product availability. The coexistence of digital, specialty, and traditional retail formats allows manufacturers to meet diverse purchasing preferences and expand category penetration within the companion animal health market.

Geography Analysis

Ontario remains the most commercially significant province for pet nutraceutical demand, driven by its large urban population, extensive veterinary infrastructure, and high levels of premium pet care spending. The province benefits from a well-established network of veterinary clinics, specialty retailers, and e-commerce capabilities, ensuring broad access to health-focused pet products. Demand is particularly strong for supplements addressing joint mobility, digestive wellness, immunity, and healthy aging. Additionally, Ontario serves as a central hub for pet nutrition manufacturing and distribution, enabling brands to enhance product availability and foster stronger relationships with retailers and veterinary professionals across Canada.

Quebec remains a significant market for pet nutraceutical products, supported by its large companion animal population, established veterinary network, and increasing interest in premium pet wellness solutions. The province exhibits strong demand for products targeting digestive health, immunity, and healthy aging, particularly through specialty retail and veterinary channels. French-language packaging and labeling requirements encourage manufacturers to focus on localized product communication and regulatory compliance. These factors create favorable conditions for premium and condition-specific nutraceutical formulations, while also driving product innovation and distribution growth across the province.

Western Canada and Atlantic Canada continue to offer growth opportunities as pet ownership remains widespread beyond major metropolitan areas. According to Agriculture and Agri-Food Canada, the total pet population in Canada reached 29.7 million animals in 2024 and is projected to grow further, supporting sustained demand for pet wellness and nutrition products. The increasing reliance on e-commerce platforms is improving access to specialized nutraceutical formulations in smaller cities and rural communities, where specialty retail options are more limited. This expanded geographic reach is enabling manufacturers to increase market penetration and strengthen customer engagement across diverse regional consumer segments.

Competitive Landscape

The competitive environment in the Canada pet nutraceutical market is moderately consolidated, with key players including Nestlé S.A., Mars, Incorporated, Hill's Pet Nutrition, Inc. (Colgate-Palmolive Company), The J. M. Smucker Company, and Zoetis Inc. These companies compete alongside veterinary-focused specialists and ingredient suppliers by leveraging extensive product portfolios, established retailer relationships, and strong veterinarian engagement programs. Competitive differentiation increasingly focuses on ingredient transparency, condition-specific formulations, scientific validation, and premium positioning. Additionally, companies are investing in digital engagement strategies and direct-to-consumer channels to enhance customer retention and improve brand visibility. This combination of scale, innovation, and professional credibility continues to shape the competitive dynamics in this market.

Manufacturers are placing greater emphasis on specialized health areas such as joint mobility, digestive wellness, immune support, cognitive health, and healthy aging to achieve clearer product differentiation. Premium formulations incorporating probiotics, omega-3 fatty acids, postbiotics, and functional bioactive ingredients are gaining prominence as companies respond to evolving consumer expectations. Veterinary recommendations remain a significant competitive advantage, prompting suppliers to back product development with scientific evidence and professional education initiatives. Simultaneously, the expansion of online retail channels is enabling both established brands and emerging players to efficiently reach consumers across various regions.

Competitive activity is further supported by ongoing investments in pet nutrition and health infrastructure. In March 2026, Mars, Incorporated announced a CAD 180 million (USD 130 million) investment across four Ontario facilities. This includes a 12% production capacity expansion at its Royal Canin manufacturing site in Guelph, aimed at enhancing local production capabilities and supporting the development of premium pet nutrition products in Canada. This investment underscores the importance of manufacturing scale, supply chain resilience, and product availability as companies strive to strengthen their positions in the evolving pet wellness market.

Canada Pet Nutraceuticals Industry Leaders

Nestlé S.A.

Mars, Incorporated

Hill's Pet Nutrition, Inc. (Colgate-Palmolive Company)

The J. M. Smucker Company

Zoetis Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Mars, Incorporated invested CAD 180 million (USD 130 million) in four manufacturing facilities in Ontario. This investment included the expansion of its Royal Canin operations in Guelph, aimed at enhancing production capacity for premium pet nutrition products and supporting the availability of health-focused formulations in Canada.

- March 2026: Archer-Daniels-Midland Company introduced PRIOME Joint Health, a postbiotic ingredient designed for pet supplements aimed at improving joint health and mobility in dogs and cats. This launch enhances innovation in the healthy-aging pet nutraceuticals market across North America, including Canada.

- April 2025: The Canadian Food Inspection Agency (CFIA) established a certification agreement with New Zealand’s Ministry for Primary Industries. This agreement allows the import of eligible pet supplements into Canada, facilitating supply chain expansion for companies in the pet nutraceuticals market.

Canada Pet Nutraceuticals Market Report Scope

Pet nutraceuticals are functional nutritional products designed to enhance pet health beyond basic dietary needs. These include vitamins, probiotics, omega-3 fatty acids, and bioactive compounds that support immunity, digestion, joint health, skin condition, and overall well-being.

The Canada Pet Nutraceuticals Market Report is Segmented by Sub-Product (Milk Bioactives, Omega-3 Fatty Acids, Probiotics, Proteins and Peptides, Vitamins and Minerals, and More), by Pets (Cats, Dogs, and Other Pets), and by Distribution Channel (Convenience Stores, Online Channel, Specialty Stores, Supermarkets and Hypermarkets, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Milk Bioactives |

| Omega-3 Fatty Acids |

| Probiotics |

| Proteins and Peptides |

| Vitamins and Minerals |

| Other Nutraceuticals |

| Cats |

| Dogs |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| By Sub Product | Milk Bioactives |

| Omega-3 Fatty Acids | |

| Probiotics | |

| Proteins and Peptides | |

| Vitamins and Minerals | |

| Other Nutraceuticals | |

| By Pets | Cats |

| Dogs | |

| Other Pets | |

| By Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels |

Key Questions Answered in the Report

How large is the Canada pet nutraceuticals space in 2026?

Canada pet nutraceuticals market is valued at USD 176.92 million in 2026.

Which sub product leads demand in Canada?

Vitamins and minerals led with the largest 25.6% share in 2025 and are also projected to grow at the fastest 9.8% CAGR from 2026 to 2031.

Why is the online channel becoming so important for pet supplements in Canada?

Online channel sales held the largest 29.1% share in 2025 and are growing at 10.1% CAGR from 2026 to 2031 because subscriptions and repeat delivery fit daily supplement use well.

What are the main factors supporting future growth in this category?

Preventive health spending, an aging pet population, stronger veterinarian endorsement, and demand for cleaner and more traceable products are supporting continued expansion.

Page last updated on: