Mexico Pet Nutraceuticals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

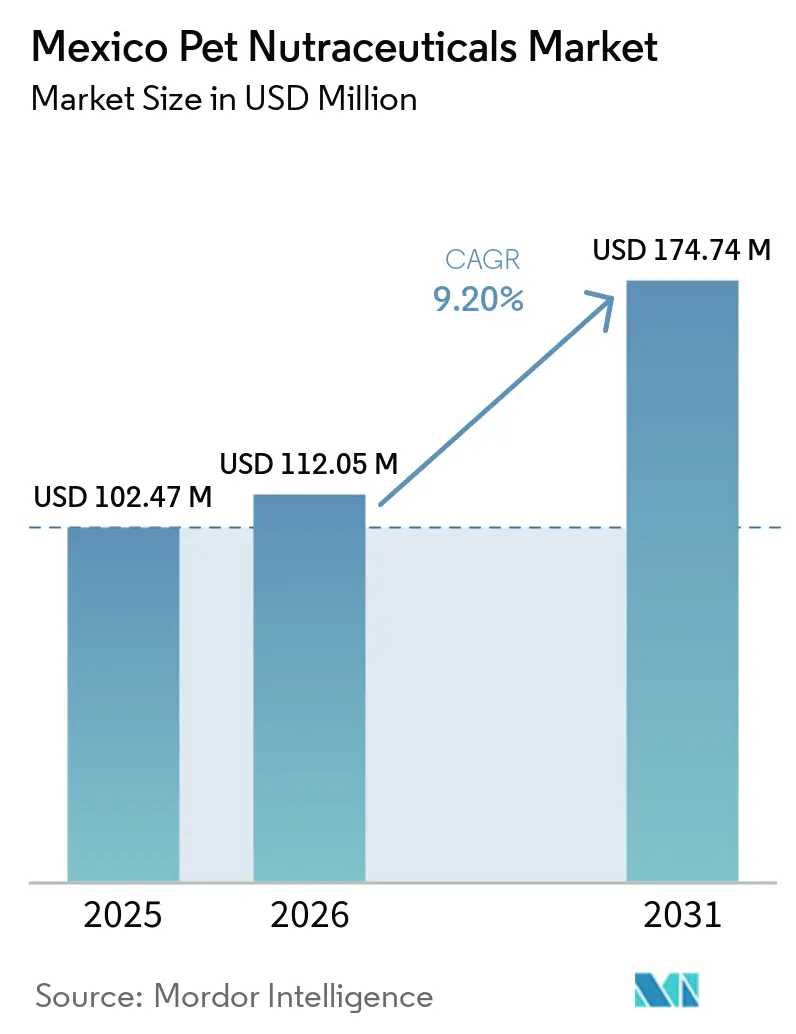

| Base Year Market Size (2025) | USD 102.47 Million |

| Market Size (2026) | USD 112.05 Million |

| Market Size (2031) | USD 174.74 Million |

| Growth Rate (2026 - 2031) | 9.20% CAGR |

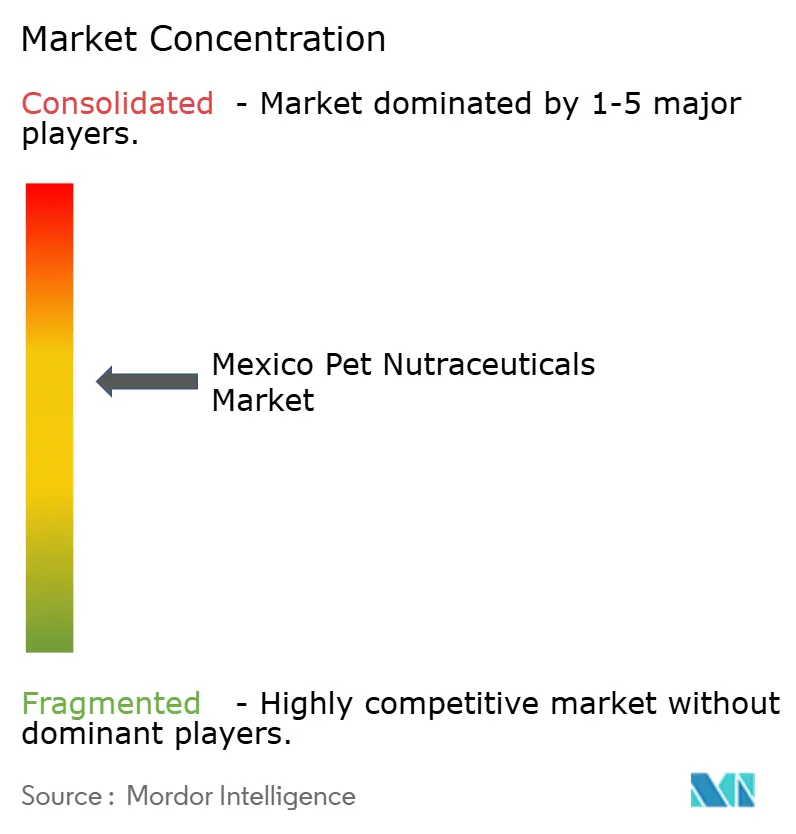

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Pet Nutraceuticals Market Analysis by Mordor Intelligence

The Mexico pet nutraceuticals market size is projected to expand from USD 102.47 million in 2025 and USD 112.05 million in 2026 to USD 174.74 million by 2031, registering a CAGR of 9.2% between 2026 and 2031. The Mexico pet nutraceuticals market is moving from routine feeding toward preventive care, as more owners look for products that support digestion, immunity, joint health, and healthy aging. Demand is supported by stronger interest in functional ingredients, with Mexican pet owners willing to pay more for formulas containing such ingredients and having bought microbiome-supporting products at least once. Veterinary guidance is also strengthening repeat demand because products with clearer health positioning are easier to recommend and easier for consumers to understand over time. Digital retail and recurring purchase models are widening access to specialized products, helping the Mexico pet nutraceuticals market expand beyond specialty pet stores into a broader buying base. At the same time, new production capacity from Symrise AG in Querétaro, together with premix supply support for Mexico from DSM-Firmenich AG and a larger manufacturing base from Mars, Incorporated, is easing supply constraints, even though imported specialty inputs still keep cost pressure in place.

Key Report Takeaways

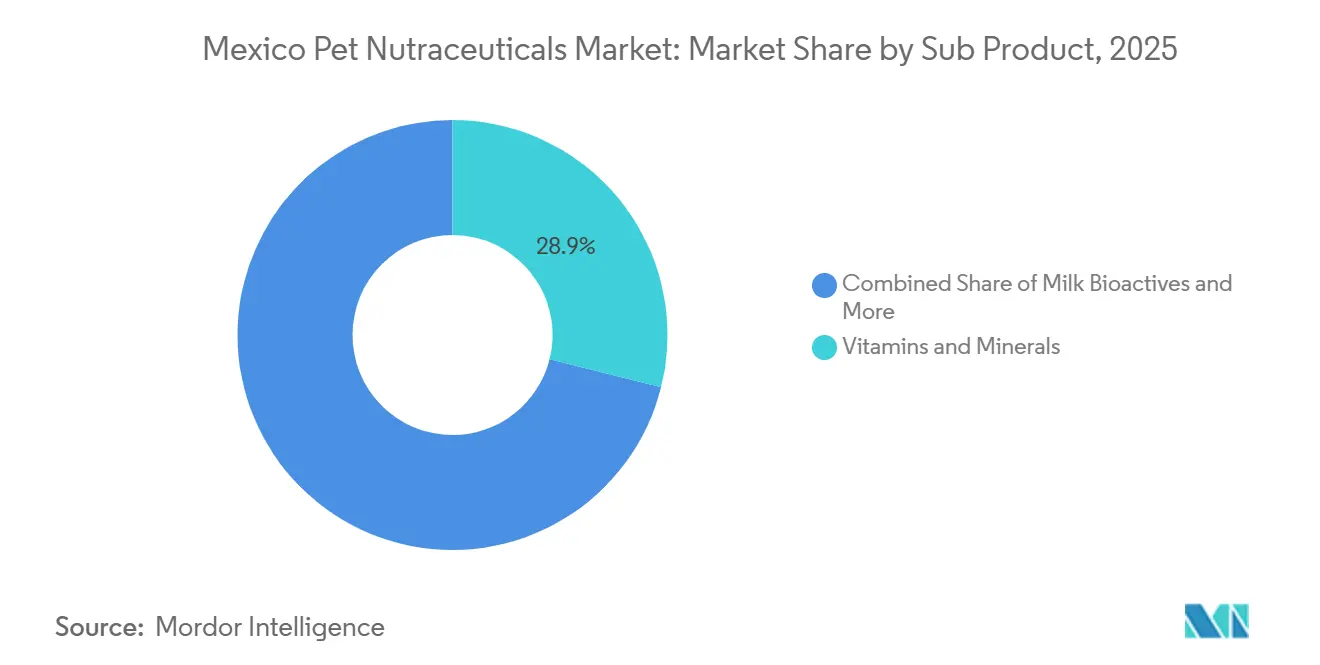

- By sub-product, vitamins and minerals held the largest share at 28.9% in 2025, and are the fastest-growing segment, with a projected CAGR of 9.7% through 2031.

- By pet type, dogs held 86% of the Mexico pet nutraceuticals market share in 2025, and the Mexico pet nutraceuticals market size for dogs is projected to expand at a 9.3% CAGR through 2031.

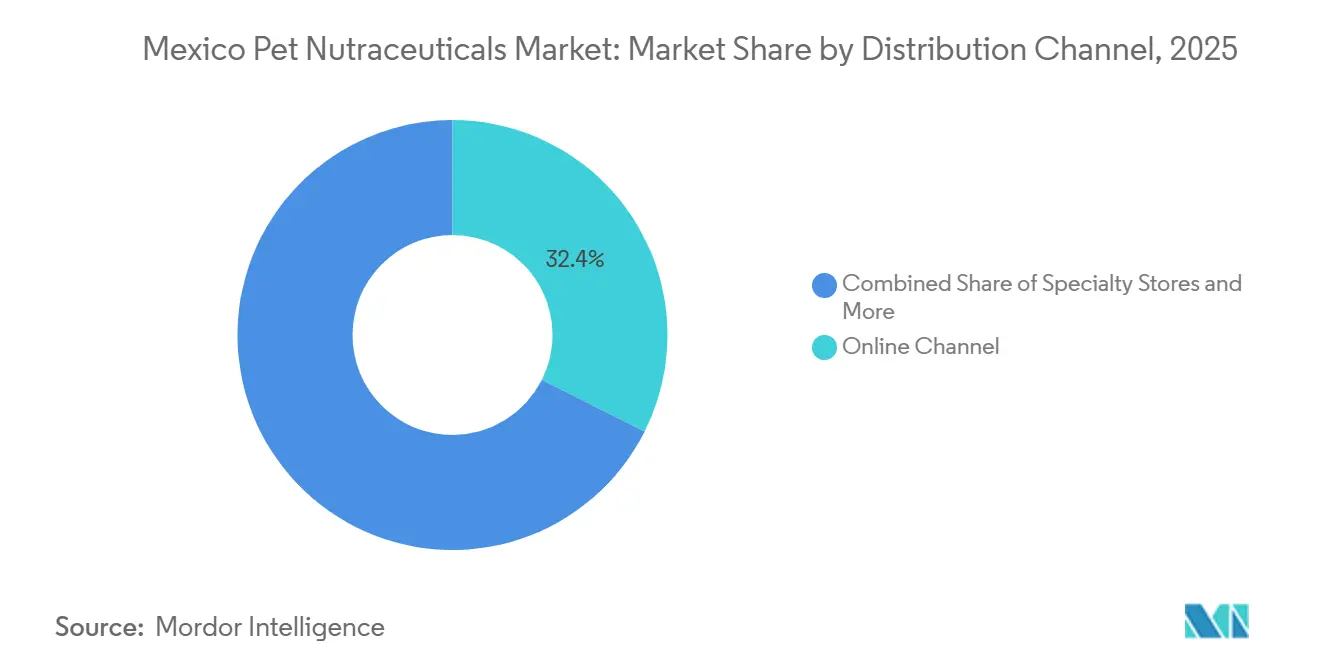

- By distribution channel, the online channel held the largest share at 32.4% in 2025, and the Mexico pet nutraceuticals market share for this channel is projected to expand at a 10.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Pet Nutraceuticals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pet humanization and premium health spending | +2.5% | Urban Mexico, especially Mexico City, Guadalajara, and Monterrey, with widening suburban spillover | Short term (≤ 2 years) |

| Veterinarian recommendation of functional formulas | +1.5% | National, strongest in tier-1 cities with established clinic networks | Medium term (2-4 years) |

| E-commerce reach for specialty pet wellness products | +1.8% | National, with early gains in Mexico City, Monterrey, and Guadalajara | Short term (≤ 2 years) |

| Subscription and refill models for preventive care | +0.9% | Urban Mexico among digitally active pet owner groups | Medium term (2-4 years) |

| Underused clinical nutrition positioning for senior pets | +0.8% | National, with stronger uptake in higher-income urban households | Long term (≥ 4 years) |

| Domestic manufacturing and formulation localization | +0.7% | National, especially Querétaro, Guanajuato, and Morelos production corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pet Humanization and Premium Health Spending

Market is gaining from a stronger shift in owner behavior, where pets are increasingly treated as long-term health dependents rather than basic household animals. That change matters because it raises demand for products that promise day-to-day wellness support instead of one-time corrective use. Archer Daniels Midland Company reported that 77% of Mexican pet owners were willing to pay more for formulas with functional ingredients, which shows clear readiness for premium positioning in this category[1]Source: Archer Daniels Midland Company, “Pet Nutrition Insights Report 2026,” adm.com. The same pattern also supports greater interest in labels, ingredient claims, and targeted benefit language, helping higher-value nutraceutical products stand apart from standard foods. Over time, that behavior supports better shelf economics for clinically positioned products and gives manufacturers more room to build segmented portfolios instead of relying on one broad wellness formula. It also keeps the Mexico pet nutraceuticals market closely tied to the wider premiumization trend already visible across pet care spending.

Veterinarian Recommendation of Functional Formulas

The market is also being shaped by veterinarian guidance, because pet owners often look for reassurance before paying more for a preventive product. This makes clinical recommendation a stronger sales trigger in nutraceuticals than in standard pet food, where brand familiarity often carries more weight. Products that address digestion, joint support, skin health, and immunity are better placed when a veterinarian can explain the benefit in practical terms. That in turn raises repeat purchase rates because the consumer has a clearer reason to stay with the same product over time. It also creates a harder path for low-cost products that do not carry the same scientific or functional positioning. As veterinary access continues to improve in larger cities and nearby urban centers, the Mexico pet nutraceuticals market should see stronger conversion from trial into regular use.

E-Commerce Reach for Specialty Pet Wellness Products

The Mexico pet nutraceuticals market has widened through e-commerce because digital channels remove many of the location limits that once held premium specialty products inside a few large cities. Online platforms make it easier for consumers to compare ingredients, read usage guidance, and buy targeted formats that may not be stocked in every physical outlet. This matters especially in nutraceuticals, where education is part of the sale and where product pages can explain digestive, mobility, or microbiome benefits more clearly than shelf packs. Digital channels also help brands introduce new formats faster because they can test bundles, dosage forms, and promotional offers without waiting for broad store placement. For consumers, that lowers the barrier to first purchase and improves access to repeat supply. As a result, the Mexico pet nutraceuticals market is increasingly supported by discovery and conversion that happen online before the product becomes a routine purchase offline.

Subscription and Refill Models for Preventive Care

It is also benefiting from subscription and refill models because preventive products work best when they are used consistently over time. A recurring order model fits that need by reducing the risk that owners stop using a product simply because they forget to repurchase it. This is especially important for joint support, digestive support, and daily vitamin products, where the value is built through routine use rather than immediate effect. Subscription programs also help brands smooth demand, improve customer retention, and build direct relationships with buyers who may later trade up into more specialized formulas. For consumers, these models turn pet wellness into a managed monthly habit rather than a sporadic discretionary purchase. That makes the Mexico pet nutraceuticals market more stable and more predictable as digital penetration keeps improving.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price sensitivity versus basic pet food | -1.8% | National, more acute in rural areas and lower-income urban households | Short term (≤ 2 years) |

| Claim substantiation and label compliance costs | -0.9% | National, with compliance influence on imported and domestic brands | Medium term (2-4 years) |

| Import dependence for specialty functional inputs | -1.2% | National supply chain, with highest exposure in colostrum and encapsulated omega-3 categories | Medium term (2-4 years) |

| Rural awareness gap for advanced nutraceuticals | -0.8% | Rural Mexico and municipalities with limited veterinary infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity Versus Basic Pet Food

Market still faces a clear affordability barrier because nutraceuticals compete not only with other premium products, but also with the much lower cost of basic pet food. That gap matters most in households where spending decisions are still centered on core nutrition rather than added functional benefits. Premium formulas with specialized proteins, probiotics, omega-3 concentrates, or advanced bioactives naturally carry a higher retail price, and that reduces the size of the addressable market. This creates a split between consumers who are trading up into preventive care and those who remain focused on entry-level feeding. The result is a thinner middle tier, where many households see value in wellness support but do not buy consistently at current price points. Until more affordable functional options are widely available, the Mexico pet nutraceuticals market will continue to grow unevenly across income groups.

Claim Substantiation and Label Compliance Costs

The Mexico pet nutraceuticals market also faces pressure from the cost of supporting claims, especially for products that sit close to the boundary between food support and therapeutic language. Brands must be careful in how they present digestive, immune, joint, or cognitive benefits because poorly supported claims can slow launches or limit how products are marketed. This raises development costs and stretches timelines, particularly for small and mid-sized companies without broad regulatory teams. Larger companies are better placed to absorb the documentation burden because they already manage multiple products, markets, and supplier records. That creates an uneven playing field in which innovation may exist, but not every player can bring it to shelf at the same pace. Over time, these compliance demands can shift the Mexico pet nutraceuticals market toward companies with stronger technical resources and deeper operating scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Product: Vitamins and Minerals Lead and Record the Fastest Growth Among All Segments

Vitamins and minerals accounted for the largest share, at 28.9%, of the Mexico pet nutraceuticals market in 2025. This segment is also projected to be the fastest-growing. This unique combination of being both the largest and fastest-growing segment highlights the versatility of micronutrient products. These products are widely applicable for supporting immunity, bone health, coat quality, and early cognitive development without requiring a condition-specific diagnosis. In the Mexico pet nutraceuticals market, this flexibility ensures the segment's relevance across various life stages and appeals to both veterinary recommendations and self-directed purchases by pet owners. Additionally, the category maintains strong visibility across multiple distribution channels due to its straightforward and easily communicated value proposition.

The Mexico pet nutraceuticals market size for vitamins and minerals is projected to expand at a 9.7% CAGR through 2031, making it the fastest sub-product group in the current outlook. This growth is tied to broader ingredient awareness and to a shift away from single-purpose products toward daily support formulas that can address several needs at once. It also aligns with the rising care needs of aging animals, for which vitamin and mineral support can be tailored to mobility, immune function, and healthy aging. Archer Daniels Midland Company reinforced this approach in March 2026 with PRIOME Joint Health, a postbiotic ingredient designed to support cartilage function, collagen production, muscle maintenance, gut barrier function, and healthy weight management in pets, aligning with the growing demand in the Mexico Pet Nutraceuticals Market. For the Mexico pet nutraceuticals industry, this means the fastest growth is likely to come from broader daily-use formulas rather than from a simple extension of legacy colostrum products.

By Pets: Dogs Hold The Largest Position And Remain The Fastest-Growing

Dogs held the largest market share at 86% in 2025, which gives the Mexico pet nutraceuticals market a clear canine base in both product design and commercial focus. That lead is reinforced by the wider range of validated use cases already available for dogs, including joint support, digestive support, skin support, and cognitive care. Dogs also benefit from stronger consumer familiarity with supplementation, since many owners already associate canine aging and mobility with routine wellness products. This makes the segment easier to scale for both established brands and new entrants. Because of that mix of scale, familiarity, and clearer benefit communication, dogs remain the main demand anchor across the Mexico pet nutraceuticals market.

The Mexico pet nutraceuticals market for dogs is projected to expand at a 9.3% CAGR through 2031, indicating that the largest segment is also the fastest-growing. The pace is supported by the rising share of older dogs. That age profile raises demand for targeted support in mobility, muscle maintenance, digestion, and day-to-day comfort. Cats remain smaller in current value terms, but they are gaining attention as brands move away from treating feline care as an extension of canine formulas. Other Pets still represent a small base, yet urban pet diversification could gradually bring more specialized formulations into that category as the Mexico pet nutraceuticals industry broadens.

By Distribution Channel: Online Channel Leads Current Sales And Future Expansion

The online channel held the largest market share at 32.4% in 2025, underscoring how strongly the buying cycle has shifted toward digital discovery and convenience. Online platforms are especially useful for nutraceuticals, as consumers often want to compare claims, ingredients, dosage forms, and reviews before buying. That gives digital sellers an advantage over outlets with tight shelf space and limited product education. It also lets brands introduce narrower, higher-value formats that might not secure immediate placement in a broad physical network. As a result, the online route has become a major access point for both first-time and repeat buyers across the Mexico pet nutraceuticals market.

The Mexico pet nutraceuticals market size for the online channel is projected to expand at a 10.2% CAGR through 2031, keeping digital retail in the fastest-growing position throughout the forecast period. The channel gains from convenience, a broader assortment, and the ability to support recurring orders, which matters for preventive products used over many weeks or months. Specialty stores still retain value because they offer advice and a curated product mix, while supermarkets and hypermarkets remain useful for replenishment purchases made during regular shopping trips. Convenience stores currently play a limited role because their pet wellness assortment is narrow and often centered on basic products. Over time, the Mexico pet nutraceuticals market is likely to keep its omnichannel shape, but online retail should remain the strongest growth engine because it combines access, education, and repeat ordering more effectively than the other channels.

Geography Analysis

Mexico held the largest single-country share within the regional landscape in 2025, which keeps the Mexico pet nutraceuticals market at the center of regional pet wellness demand. This position is supported by large urban consumption clusters in Mexico City, Monterrey, Guadalajara, and Querétaro, where premium pet care adoption is stronger, and product availability is wider. In 2025, local production is also becoming more important, with Mars, Incorporated describing the Querétaro plant as its largest pet food plant globally after the recent expansion to 14 production lines[2]Source: Mars, Incorporated, “Mars México: Tres Décadas Transformando el Cuidado de las Mascotas,” mars.com. In February 2026, Symrise AG expanded its domestic operations in Mexico by opening its Querétaro facility to support local pet food customers and address the growing demand in the Mexico pet nutraceuticals market[3]Source: Symrise AG, “Symrise Pet Food Inaugurates a New Facility in Querétaro, Mexico,” Symrise AG, petfood.symrise.com.

Urban centers represented the largest share of current demand in the Mexico pet nutraceuticals market because they combine higher spending power, better veterinary access, and stronger digital adoption. Mexico City, Monterrey, and Guadalajara remain the clearest premium demand centers because consumers there are more exposed to specialized pet retail and functional nutrition messaging. Second-tier cities such as Puebla, Tijuana, and León are still developing, and many households there are moving through earlier stages of premium pet care adoption. Rural markets face a slower uptake path because owner education is thinner, veterinary support is less available, and nutraceutical benefits are less familiar in everyday purchase decisions. That means national growth is not evenly distributed, and much of the Mexico pet nutraceuticals market still depends on urban concentration for present-day scale.

Mexico also stands out as one of the fastest-developing supply bases serving the Mexico pet nutraceuticals market, which gives it a stronger role than demand alone would suggest. DSM-Firmenich AG stated that its Tonganoxie premix facility was designed to serve Mexico, which confirms the country’s importance in wider pet nutrition supply planning across North America. That kind of upstream support matters because it improves access to vitamins, omega-3 systems, carotenoids, microbiome solutions, and other functional premix inputs. Companies that localize formulation and distribution earlier should have an advantage, since regulatory clearance, supplier relationships, and veterinarian-led market access all take time to build.

Competitive Landscape

The Mexico pet nutraceuticals market remains moderately concentrated, with large multinational companies using their scale in pet nutrition to expand into higher-value wellness and supplement formats.Personalization technology is emerging as a significant competitive advantage in the Mexico pet nutraceuticals market, with early adopters gaining a lead before broader market awareness develops. In Mexico, 78% of pet owners express interest in personalized nutrition, while only 30% are familiar with it, highlighting a substantial conversion gap.

Digital-native platforms are deploying data-driven recommendation engines and subscription models, converting one-time buyers into habitual users, at a pace that legacy physical-retail incumbents cannot replicate through product range alone. Ingredient-layer companies are reinforcing this dynamic by developing proprietary postbiotic and bioactive peptide platforms that give finished-product manufacturers exclusive functional differentiation, embedding switching costs before competitive imitation cycles begin. DSM-Firmenich AG is competing in the premix layer with automated, traceable, and customizable supply for pet food manufacturers serving Mexico. Together, these moves show that finished brands, veterinary players, and ingredient suppliers are all trying to secure a stronger place in the same value chain.

White space remains strongest in affordable senior pet support, more purpose-built feline formulations, and subscription-led preventive care for digitally connected households. Companies without local manufacturing support or a clear veterinary route to market are likely to face a tougher path because costs are higher and product trust is harder to build. This means the Mexico pet nutraceuticals market is competitive, but it is not dominated by one supplier with overwhelming control across products, channels, and formulation depth. Instead, advantage comes from how well a company links science-backed ingredients, local supply capability, and repeat consumer access.

Mexico Pet Nutraceuticals Industry Leaders

Mars, Incorporated

Nestle S.A. (Purina)

Virbac SA

Zoetis Inc.

Kemin Industries, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Archer Daniels Midland Company expanded its PRIOME postbiotics portfolio by introducing Joint Health, a formulation based on heat-treated Lacticaseibacillus rhamnosus NCIMB 30446. This product is designed to support cartilage function, collagen production, muscle maintenance, gut barrier function, and healthy weight management, which are key considerations in the Mexico pet nutraceuticals market.

- August 2025: Mexico's Federal Commission for the Protection against Sanitary Risks has issued a regulatory agreement simplifying import processes for food and supplements. By reducing administrative barriers, this may accelerate the availability of functional ingredients in the pet nutraceuticals market.

- March 2025: Mars, Incorporated expands Querétaro facility to become largest pet food production site. The expansion has established the Querétaro site as Mars's largest pet food production facility globally, featuring 14 operational production lines. This facility serves as a key export hub for South America, enhancing Mexico's role within the global Mars Petcare supply chain.

Mexico Pet Nutraceuticals Market Report Scope

Pet nutraceuticals are functional nutritional products formulated for pets that provide health benefits beyond basic nutrition, supporting specific functions such as joint health, digestion, immunity, skin and coat condition, and overall wellness. They typically include omega-3 fatty acids, probiotics, vitamins, minerals, proteins, peptides, and bioactive compounds.

The Mexico Pet Nutraceuticals Market Report is Segmented by Sub Product (Milk Bioactives, Omega-3 Fatty Acids, Probiotics, Proteins and Peptides, Vitamins and Minerals, and Other Nutraceuticals), by Pets (Cats, Dogs, and Other Pets), and by Distribution Channel (Convenience Stores, Online Channel, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Milk Bioactives |

| Omega-3 Fatty Acids |

| Probiotics |

| Proteins and Peptides |

| Vitamins and Minerals |

| Other Nutraceuticals |

| Cats |

| Dogs |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| Sub Product | Milk Bioactives |

| Omega-3 Fatty Acids | |

| Probiotics | |

| Proteins and Peptides | |

| Vitamins and Minerals | |

| Other Nutraceuticals | |

| Pets | Cats |

| Dogs | |

| Other Pets | |

| Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels |

Key Questions Answered in the Report

What is the current size of Mexico pet nutraceuticals demand?

The category is projected at USD 112.05 million in 2026 and is projected to reach USD 174.74 million by 2031, growing at a 9.2% CAGR.

Which sub product category leads in Mexico?

Vitamins and minerals were the largest segment in 2025 with a 28.9% share and are also projected to grow the fastest at 9.7% through 2031.

Why are dogs the main demand driver in this space?

Dogs held 86% of value in 2025 and are also projected to grow the fastest at 9.3% CAGR, which reflects their central role in current supplement use.

Which sales channel is expanding fastest for pet supplements in Mexico?

The online channel led with 32.4% share in 2025 and is projected to grow at 10.2% CAGR, helped by better product discovery and repeat ordering.

What is pushing growth in functional pet nutrition products?

Preventive care, premium ingredient demand, stronger veterinarian influence, and better digital access are the main factors supporting category expansion.

What is the biggest barrier to wider adoption?

Price sensitivity remains the main barrier because advanced formulas still cost much more than basic pet food, especially outside higher-income urban households.

Page last updated on: