Flexographic Printing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

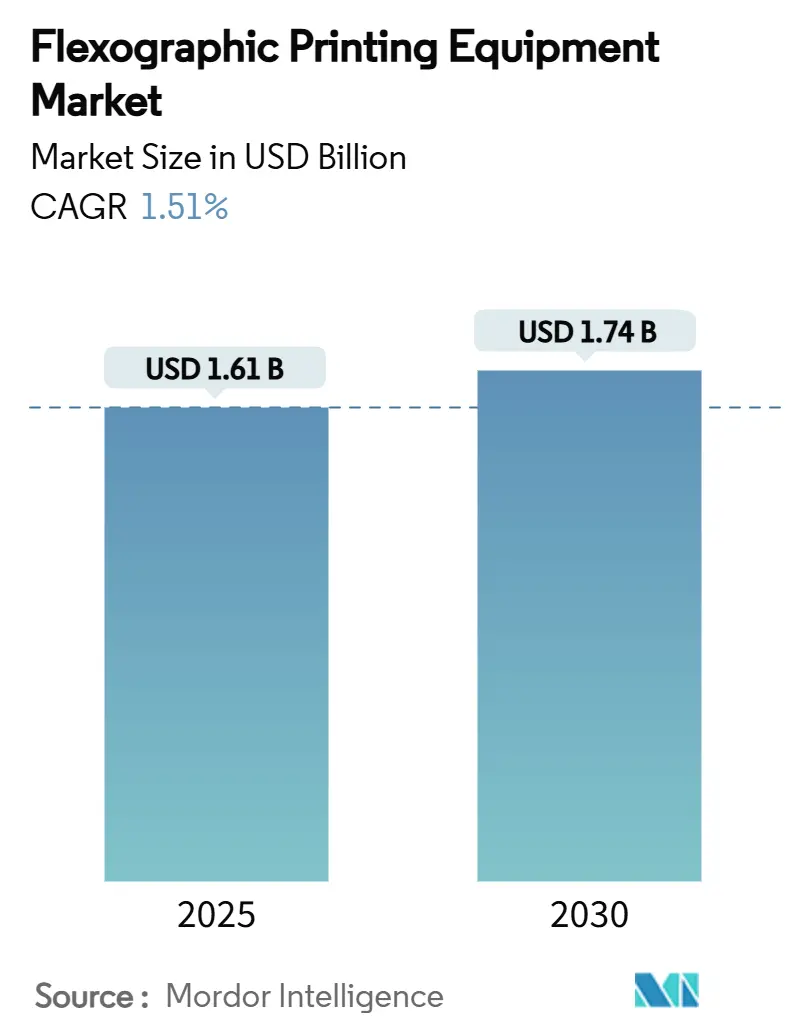

| Market Size (2025) | USD 1.61 Billion |

| Market Size (2030) | USD 1.74 Billion |

| Growth Rate (2025 - 2030) | 1.51% CAGR |

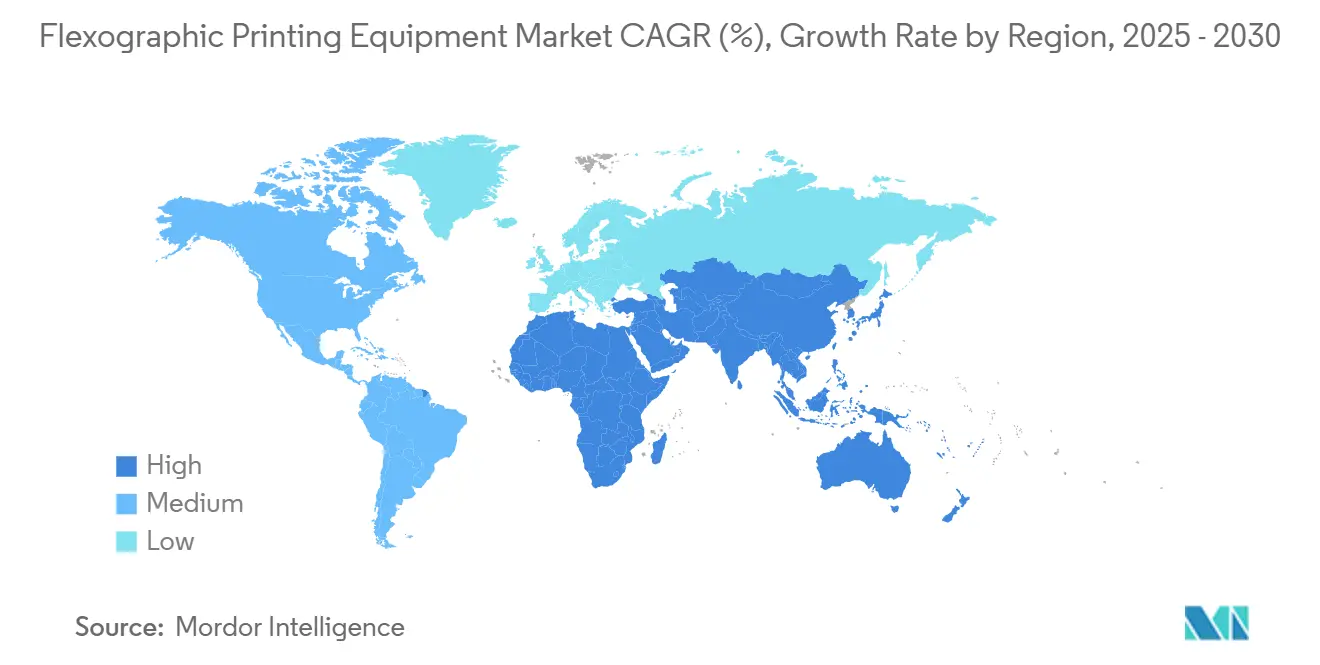

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flexographic Printing Equipment Market Analysis by Mordor Intelligence

The flexographic printing equipment market stands at USD 1.61 billion in 2025 and is projected to advance at a 1.51% CAGR, reaching USD 1.74 billion by 2030. Demand holds steady as converters balance technology upgrades with cost pressure from digital alternatives. Capital is flowing into workflow automation, AI-assisted press controls, and ink systems that curb energy use. Hybrid press platforms, which marry flexo’s low running cost with digital’s variable-data strengths, are redefining equipment investment criteria. Brand-owner sustainability pledges are redirecting R&D toward LED-UV curing, water-based chemistry, and lower waste rates, further shaping purchasing decisions throughout the flexographic printing equipment market.

Key Report Takeaways

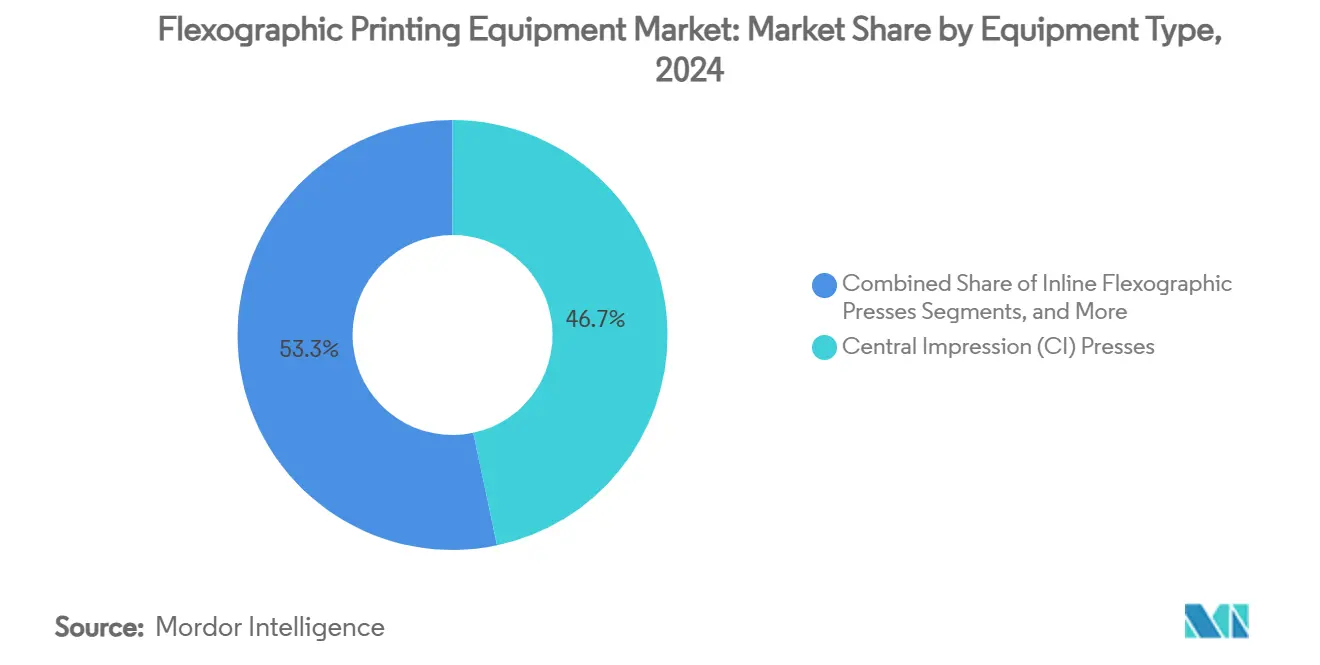

- By equipment type, Central Impression presses led with 46.68% of flexographic printing equipment market share in 2024.

- By substrate, flexible plastic films captured 53.8% of flexographic printing equipment market share in 2024.

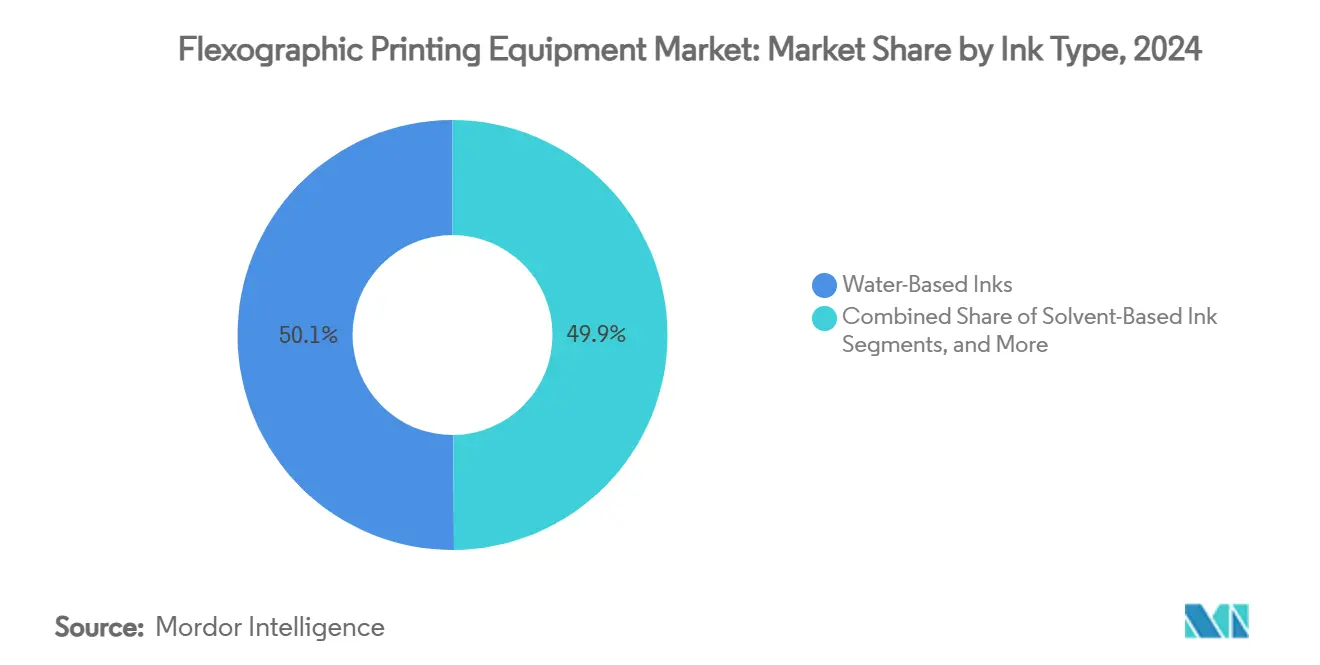

- By ink type, water-based inks accounted for 50.12% share of the flexographic printing equipment market size in 2024.

- By end-user, food and beverage packaging held 38% of the flexographic printing equipment market size in 2024.

- By geography, Asia-Pacific commanded 38.4% of flexographic printing equipment market share in 2024.

Global Flexographic Printing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward short-run, quick changeover package printing | +0.5% | Global, stronger in North America and Europe | Medium term (2-4 years) |

| Expansion of e-commerce and corrugated packaging demand | +0.4% | Global, highest in Asia-Pacific | Long term (≥4 years) |

| Adoption of eco-friendly, water-based and LED-UV inks | +0.3% | Europe and North America, rising in Asia-Pacific | Medium term (2-4 years) |

| Preference for inline digital embellishment and inspection for packaging OEE | +0.2% | North America and Europe | Short term (≤2 years) |

| Cost advantages of flexo vs. gravure for small- and mid-sized converters | +0.1% | Asia-Pacific and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Short-Run, Quick Changeover Package Printing

Shorter product life cycles and SKU growth are pushing converters to presses that swap jobs in minutes rather than hours. Bobst’s MASTER M6 demonstrates three-minute changeovers and automated plate mounting, cutting unproductive time nearly in half compared with 2023 installations. Windmöller & Hölscher’s ALPHAFLEX uses AI to pre-set tension and register, slashing waste during startup and handling the 43% rise in SKU counts recorded since 2024 [2]Windmöller & Hölscher, “70 years CI flexo printing – leading innovations,” wh.group. Workflow vendors are integrating prepress and MIS data so operators receive optimized plate layouts automatically, completing the end-to-end efficiency loop. As these capabilities penetrate mid-tier converters, the flexographic printing equipment market sees purchase decisions driven by changeover metrics rather than headline press speed.

Expansion of E-Commerce and Corrugated Packaging Demand

Online retail growth fuels corrugated box consumption, lifting demand for presses engineered for heavyweight liners and high-ink coverage. Heidelberg’s Boardmaster runs to 600 m/min yet maintains substrate tension critical for board caliper stability [1]Heidelberger Druckmaschinen, “Boardmaster – high volume packaging press,” heidelberg.com. Asia-Pacific converters expand fleets to serve parcel hubs springing up around urban centers in China and India, catalyzing new installations across the region. Corrugators now seek inline flexo-slotter-die-cut lines that print, crease, and fold in one pass, heightening equipment integration requirements. Sustainability goals add further momentum because corrugated fiber is widely recycled, aligning with circular economy mandates.

Adoption of Eco-Friendly, Water-Based and LED-UV Inks

Regulation tightening on VOC emissions accelerates the shift to water-based and LED-UV chemistries. Water-based formulas now dominate food packaging due to lower migration risks, while LED-UV uptake climbs on its 60% energy-saving advantage versus mercury UV systems. Fujifilm’s LuXtreme retrofit kit converts legacy dryers to LED-UV, stimulating aftermarket revenues and extending press lifecycles. Manufacturers redesign dryer architecture to accommodate higher air volumes required for water-based ink drying without sacrificing line speed. These innovations support both corporate carbon-reduction targets and lower total cost of ownership, influencing buying decisions across the flexographic printing equipment market.

Cost Advantages of Flexo vs. Gravure for Small- and Mid-Sized Converters

Plate cost declines and automated registration shrink flexo’s previous economic gap with gravure for runs once considered too short. Plate suppliers report 25% lower material and imaging costs since 2024. Entry-level modular presses allow converters in India and Brazil to start small and bolt on drying or inspection modules as volumes grow. Leasing and click-charge models appear, enabling capex-constrained firms to access the latest technology without balance-sheet strain, broadening the customer base of the flexographic printing equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital investment in CI flexo presses for SME converters | -0.3% | Global, highest in emerging markets | Medium term (2-4 years) |

| Rising competition from digital inkjet in short-run label printing | -0.2% | North America and Europe, rising in Asia-Pacific | Long term (≥4 years) |

| Skilled labor shortage for operating multi-color gearless flexo presses | -0.1% | Global, acute in North America and Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Capital Investment in CI Flexo Presses for SME Converters

An eight-color CI press starts near USD 1.2 million, putting ownership beyond many small converters, especially where financing is scarce. Vendors counter with compact footprints and lower energy loads, as seen in Uteco’s OnyxGO occupying under 50 sqm and consuming up to 50% less power. Flexible leasing deals and pay-per-impression contracts aim to democratize access. Yet perceived risk of debt deters some entrepreneurs, tempering the expansion of the flexographic printing equipment market in cash-tight regions.

Rising Competition from Digital Inkjet in Short-Run Label Printing

Inkjet presses eliminate plates and can print fewer than 10 000 labels economically, nibbling at flexo volumes. Equipment makers respond with hybrid architectures; Windmöller & Hölscher’s central-cylinder concept blends up to 7 inkjet heads with 4 flexo units, allowing converters to toggle processes mid-job. Integrated workflows dispatch art files to either analog or digital decks based on run length and color coverage, sustaining flexographic relevance yet intensifying the technology race.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Automation Redefines Press Architecture

Central Impression presses commanded 46.68% of flexographic printing equipment market share in 2024 due to precise register and high web speeds that meet flexible packaging needs. Their multi-motor gearless drives now include predictive maintenance analytics that trim unplanned downtime, enhancing ROI for converters focused on throughput. Inline presses are growing at a 1.5% CAGR through 2030 as their modular design supports coating, die-cutting, and lamination in one pass, ideal for value-added labels where run lengths vary widely.

Hybrid integration blurs boundaries: W&H’s digital-flexo prototype presented at drupa 2024 stacks inkjet of up to seven colors atop a central-cylinder frame, offering variable data without sacrificing flexo economics in long runs. Such systems shift capital allocation from separate machines to unified lines, enlarging the flexographic printing equipment market.

By Substrate: Corrugated Growth Outpaces Traditional Films

Flexible plastic films retained 53.8% share in 2024 on account of food, beverage, and consumer goods demand. Yet environmental scrutiny triggers R&D into PCR content and downgauging, driving converters to presses with advanced tension feedback to handle thinner films. Corrugated board, projected to climb 3% CAGR, receives investment in wide-format post-print flexo lines like Heidelberg’s Boardmaster, which balances speed with ink laydown uniformity critical for e-commerce graphics.

Paper and paperboard applications grow as brands swap plastic pouches for fiber-based wraps, helped by barrier coatings that survive humid supply chains. Press makers calibrate dryers and nip control for these substrates, stressing versatility in product brochures to enlarge their addressable slice of the flexographic printing equipment market size.

By Ink Type: LED-UV Acceleration Transforms Curing Technology

Water-based inks held 50.12% share in 2024, bolstered by migration regulations in Europe and North America. New resin systems boost rub resistance, letting water-based formulas encroach on jobs once reserved for solvent lines. LED-UV inks, the fastest growing at 2.2% CAGR, cut energy use 60% and extend lamp life tenfold.

Retrofit modules such as Fujifilm LuXtreme enable converters to shift legacy mercury systems to LED-UV, expanding aftermarket revenue. Solvent and traditional UV formulations persist in niche barriers where aggressive anchorage is vital. Dryer innovation around airflow modeling and instant-on lamp arrays positions ink choice as a core determinant of capital investment inside the flexographic printing equipment market.

By End-User Industry: Pharmaceuticals Drive Premium Equipment Demand

Food and beverage applications held 38% of the flexographic printing equipment market size in 2024, relying on flexo’s rapid throughput and low per-unit cost for high-volume SKUs. Brand owners’ recyclable mono-material goals trigger upgrades to presses with tighter solvent-capture and inline inspection to guarantee shelf appeal. Pharmaceuticals register the highest 3% CAGR as serialization mandates, micro-text, and low-migration ink rules demand premium gearsets. Inline vision systems paired with human-readable codes ensure compliance.

Cosmetics and personal care brands commission specialty varnish and tactile effect modules, cementing growth for presses offering multi-process capability. Industrial and household chemicals maintain steady usage, favoring durable plates and quick-wash anilox systems that accommodate abrasive pigment loads.

Geography Analysis

Asia-Pacific leads the flexographic printing equipment market with 38.4% share in 2024 and a 2.5% CAGR outlook. Chinese converters invest in gearless CI lines to meet premium graphics demanded by domestic brands, while India’s packaging surge lifts inline press installations targeted at regional FMCG players. Government incentives for energy-efficient machinery spur adoption of LED-UV dryers and waste-heat recovery, embedding sustainability in new plant designs.

North America focuses on hybrid platforms to offset labor shortages. Converters blend inkjet personalization with flexo laydown on a single frame, meeting rapid private-label turnaround cycles. Regulatory movement toward PFAS-free packaging drives migration to water-based systems, shaping purchasing specifications across the flexographic printing equipment market.

Europe emphasizes carbon reduction; OEMs tout lifecycle assessments and energy monitoring dashboards. Funding programs in Germany and the Nordics provide rebates for presses equipped with regenerative drives and solvent-capture, further accelerating upgrades. South America and the Middle East and Africa show rising but uneven demand, tied to local economic cycles. Brazil’s print groups upgrade to comply with multinational brand guidelines, while South African converters eye niche exports requiring ISO quality credentials.

Competitive Landscape

Roughly 40% of global revenue lay with Bobst Group, Windmöller & Hölscher, Koenig & Bauer, Uteco Converting, and PCMC in 2024. Leadership hinges on automation software as much as mechanical design. Bobst bundles IoT diagnostics allowing predictive part replacement. W&H markets central dashboards aggregating all press KPIs, letting teams compare OEE across plants. Koenig & Bauer courts mid-tier corrugated converters with press-wide motor coordination that limits board crush.

Acquisitions strengthen portfolios: Komori’s purchase of CPS Canadian Primoflex Systems in January 2025 extends its reach in North America and deepens sleeve-handling expertise. XSYS absorbed MacDermid Graphics Solutions, creating vertical integration in plates and processing. Emerging disruptors such as Durst Group champion digital-flexo hybrids, leveraging inkjet IP to win label converters migrating shorter runs. Software vendors like Esko integrate platemaking and color management modules, making workflow solutions a decisive differentiator in the flexographic printing equipment market.

Flexographic Printing Equipment Industry Leaders

Bobst Group SA

Windmöller & Hölscher KG

Uteco Converting S.p.A.

Koenig & Bauer AG (KBA-Flexotecnica)

Heidelberger Druckmaschinen AG (Gallus)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Provident merged with Precision Flexo and Gravure, expanding flexographic service capabilities across new regions.

- May 2025: INX International acquired Servicom and Galaxy Inks and Coatings, enlarging its Asia-Pacific presence.

- April 2025: Rotocon and HS Machinery formed a partnership to blend German engineering with Chinese cost structures, aiming at competitively priced equipment.

- March 2025: XSYS finalized its MacDermid Graphics Solutions acquisition, bolstering its plate portfolio.

- January 2025: Komori Corporation bought CPS Canadian Primoflex Systems, reinforcing North American market access.

Global Flexographic Printing Equipment Market Report Scope

| Central Impression (CI) Flexographic Presses |

| Inline Flexographic Presses |

| Stack Flexographic Presses |

| Narrow Web Presses |

| Flexible Plastic Films (PE, PP, PET) |

| Paper and Paperboard |

| Corrugated Board |

| Metallic Films and Foils |

| Other Specialty Substrates |

| Water-Based |

| Solvent-Based |

| UV-Curable |

| LED-UV |

| Food and Beverage |

| Pharmaceuticals and Healthcare |

| Personal Care and Cosmetics |

| Industrial and Household Goods |

| Logistics and Shipping Labels |

| Others (Tobacco, Electronics) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Equipment Type | Central Impression (CI) Flexographic Presses | |

| Inline Flexographic Presses | ||

| Stack Flexographic Presses | ||

| Narrow Web Presses | ||

| By Substrate | Flexible Plastic Films (PE, PP, PET) | |

| Paper and Paperboard | ||

| Corrugated Board | ||

| Metallic Films and Foils | ||

| Other Specialty Substrates | ||

| By Ink Type | Water-Based | |

| Solvent-Based | ||

| UV-Curable | ||

| LED-UV | ||

| By End-User Industry | Food and Beverage | |

| Pharmaceuticals and Healthcare | ||

| Personal Care and Cosmetics | ||

| Industrial and Household Goods | ||

| Logistics and Shipping Labels | ||

| Others (Tobacco, Electronics) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the flexographic printing equipment market?

The market is valued at USD 1.61 billion in 2025.

How fast is the flexographic printing equipment market expected to grow?

It is forecast to post a 1.51% CAGR, reaching USD 1.74 billion by 2030.

Which region leads the market?

Asia-Pacific accounts for 38.4% of global revenue and shows the highest 2.5% CAGR.

Which equipment type is growing quickest?

Inline flexographic presses grow at 1.5% CAGR owing to their modular, quick-change design.

Why are LED-UV inks gaining traction?

LED-UV inks cure instantly while cutting energy use by 60%, aligning with converter sustainability targets.

What restrains small converters from adopting CI presses?

Entry-level eight-color CI lines cost about USD 1.2 million, posing financing challenges for SMEs.

Page last updated on: