Printed Flexible Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

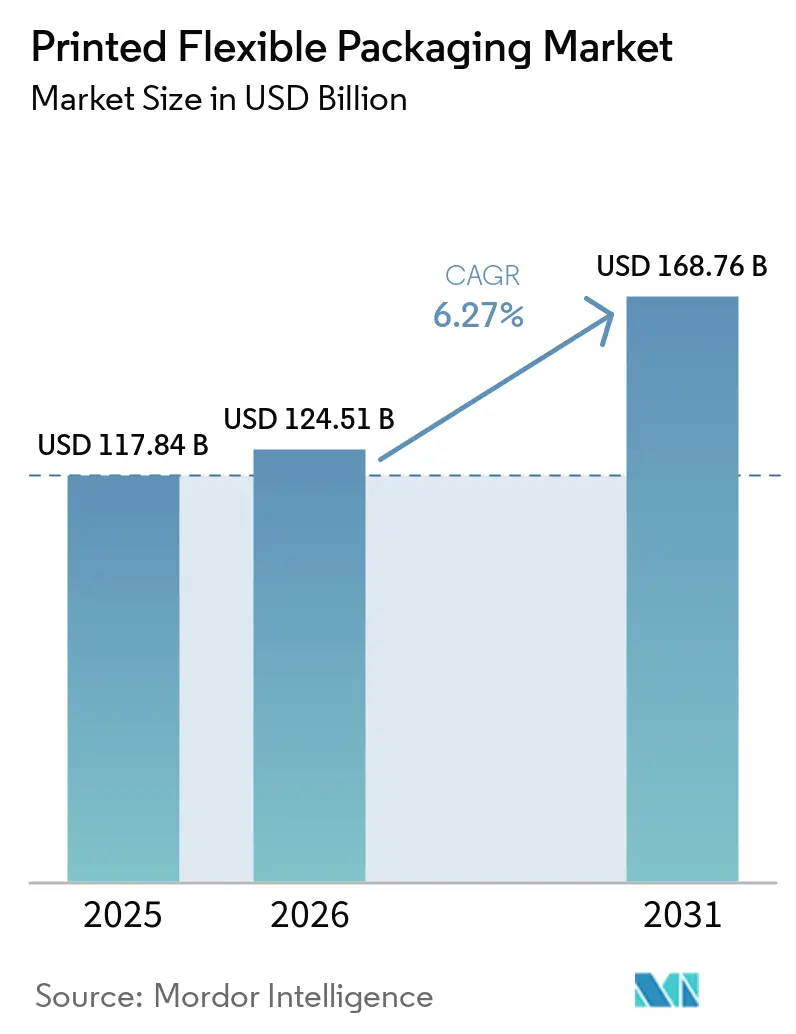

| Market Size (2026) | USD 124.51 Billion |

| Market Size (2031) | USD 168.76 Billion |

| Growth Rate (2026 - 2031) | 6.27% CAGR |

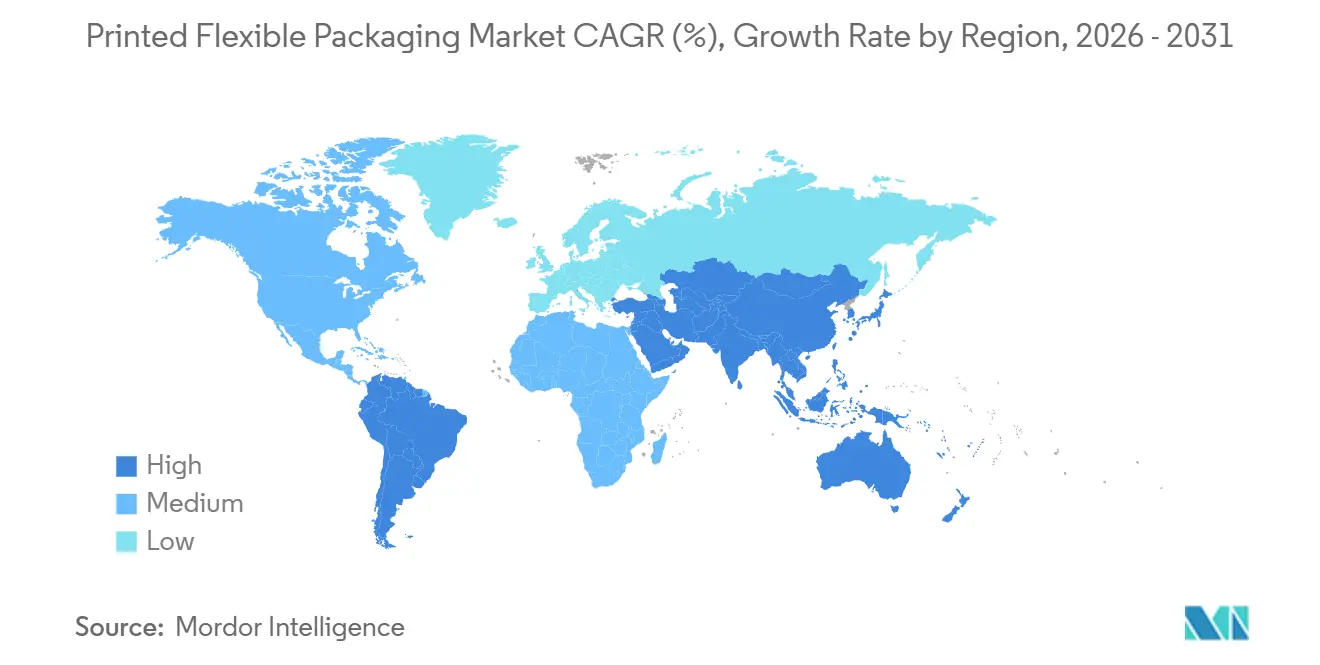

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Printed Flexible Packaging Market Analysis by Mordor Intelligence

The printed flexible packaging market size is projected to expand from USD 117.84 billion in 2025 and USD 124.51 billion in 2026 to USD 168.76 billion by 2031, registering a CAGR of 6.27% between 2026 and 2031. Growth is being supported by stronger brand spending on pack appearance, wider adoption of recyclable structures, and higher demand for packaged goods across emerging economies. The printed flexible packaging market is also benefiting from the shift toward shorter product cycles, local pack versions, and promotional runs that need faster print response from converters. Healthcare demand is driving support at the higher-value end because serialization, traceability, and clean-substrate requirements are becoming stricter across regulated packaging applications. Food and beverage continues to provide the largest volume base in the printed flexible packaging market, while better margins are appearing in premium structures that combine print quality, barrier performance, and sustainability claims. Competition is becoming tighter as larger converters add capacity, pursue acquisitions, and invest in mono-material films and advanced print lines, while resin, foil, and ink cost swings continue to pressure profitability.

Key Report Takeaways

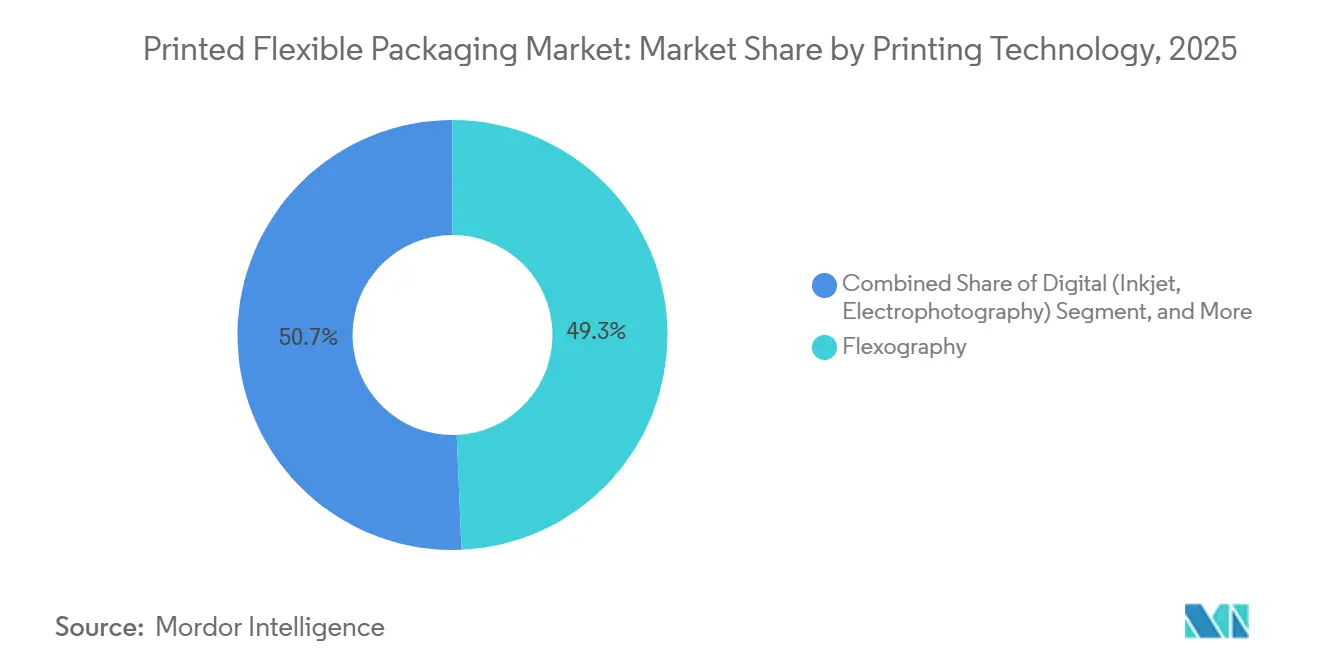

- By printing technology, flexography captured 49.34% share of the printed flexible packaging market in 2025.

- By packaging type, the printed flexible packaging market for the pouches segment is projected to grow at a 7.43% CAGR between 2026 and 2031.

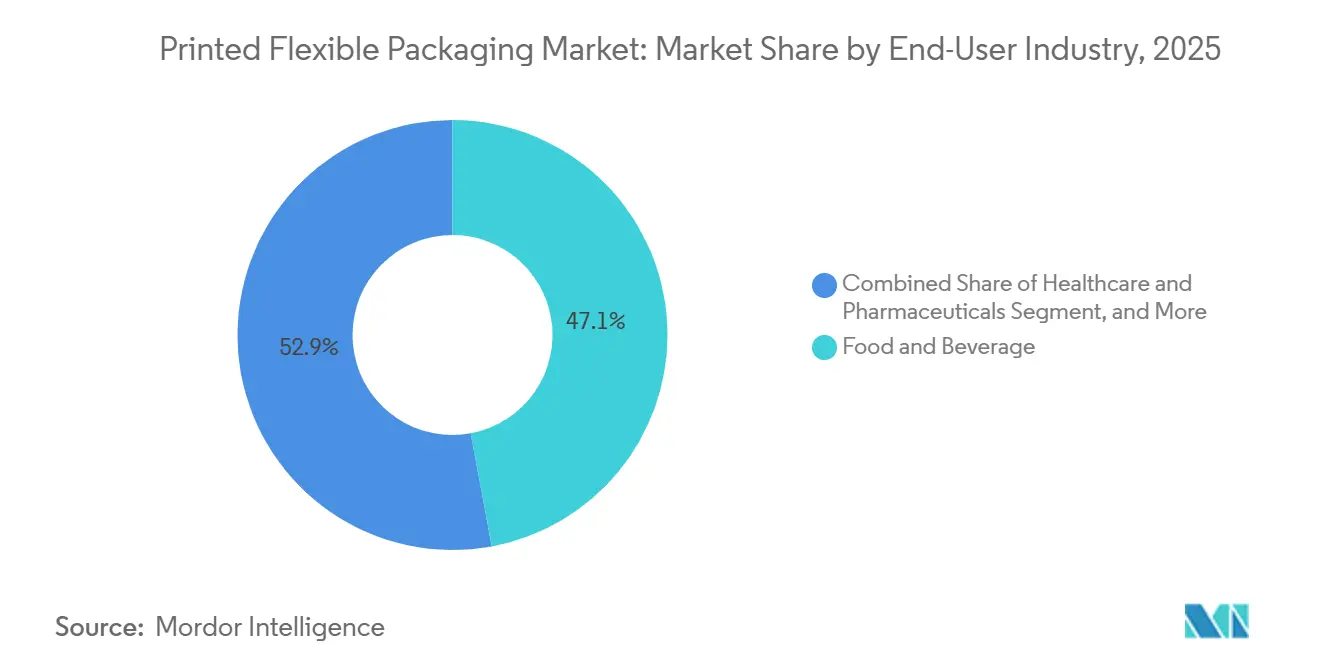

- By end-user industry, food and beverage captured 47.08% share of the printed flexible packaging market in 2025.

- By substrate, the printed flexible packaging market for the paper-based materials segment is projected to grow at a 7.03% CAGR between 2026 and 2031.

- By geography, Asia-Pacific captured 37.89% share of the printed flexible packaging market in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Printed Flexible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Shelf-Ready Retail Packaging | +1.2% | North America and Europe, with spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Faster Adoption of High-Barrier Mono-Material Structures | +1.4% | Europe core, spill-over to Asia-Pacific and North America | Medium term (2-4 years) |

| Growth in Short-Run Digital and Versioned Printing | +0.9% | Global, with early gains in Asia-Pacific and North America | Short term (≤ 2 years) |

| Expansion of Packaged Food and Convenience Consumption | +0.8% | Asia-Pacific, Middle East and Africa | Long term (≥ 4 years) |

| Shift Toward Lightweight and Material-Efficient Packs | +0.7% | Global | Medium term (2-4 years) |

| Sustainability-Led Conversion from Rigid to Flexible Formats | +0.6% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Shelf-Ready Retail Packaging

Shelf-ready formats are becoming a stronger demand driver in the printed flexible packaging market, as retailers seek packs that move from transit to display with less handling. That change gives printed graphics a more central role because converters are expected to deliver visual impact, legibility, and operational consistency on the same structure. Large grocery chains in Europe have continued to standardize on display-ready specifications, which has increased the need for high-quality print directly on flexible substrates rather than on separate labels. It also shortens the time between artwork approval and store placement, favoring suppliers that can manage faster, more frequent production cycles in the printed flexible packaging market. As more brand owners run seasonal, promotional, and regional pack changes, converters with flexographic and digital capability are better placed to retain repeat work and protect pricing.

Faster Adoption of High-Barrier Mono-Material Structures

The printed flexible packaging market is moving more quickly toward high-barrier mono-material structures because recyclability targets now affect both material choice and print chemistry. In September 2025, Siegwerk, Borouge, and TPN Food Packaging commercialized a fully de-inkable mono-PE stand-up pouch with an oxygen transmission rate below 1 cc/m²/day, demonstrating that recyclable designs can now deliver barrier performance previously associated with more complex laminates. BOBST also reported that its oneBARRIER PrimeCycle mono-PE structure had a lower environmental impact than foil-based alternatives across all assessed categories, which strengthens the commercial case for converters investing in recyclable film solutions.[1]BOBST, “Life Cycle Assessment Confirms BOBST oneBARRIER as Superior Packaging Choice,” BOBST, bobst.com The EU packaging and packaging waste rules are reinforcing this shift by requiring packaging to be designed for recyclability at scale. As a result, the printed flexible packaging market is seeing capital move toward print-compatible mono-material films, de-inking coatings, and surface treatments that preserve both appearance and recyclability.

Growth In Short-Run Digital and Versioned Printing

Short-run, versioned work is expanding in the printed flexible packaging market because brand owners now need faster replenishment, lower minimum order sizes, and greater pack variation across channels and regions. Digital printing meets that need by reducing the time lost to plate preparation and making small and mid-sized orders easier to execute without the same setup burden as analog processes. In April 2026, Amcor advanced a collaboration with Metsä Group and G. Mondini to commercialize a fiber-based packaging solution using direct digital printing, demonstrating that digital decoration is moving into broader commercial use rather than remaining in isolated pilot work. This shift is changing procurement in the printed flexible packaging market because brand owners are leaning toward suppliers that can handle both long analog runs and short digital runs within a single operating platform. The result is a clearer divide between converters with flexible production models and those still built around a single run-length model.

Expansion of Packaged Food and Convenience Consumption

The printed flexible packaging market continues to gain support from rising demand for packaged food and convenience products, as food remains the highest-volume application for printed flexible structures. The Flexible Packaging Association reported that the US flexible packaging sector generated USD 42.6 billion in sales in 2024, with food and beverage remaining the dominant end use, confirming the depth of the base demand supporting converter utilization. Demand is widening across pouches, sachets, and rollstock as urban retail growth and faster daily consumption patterns increase the need for portable, portioned formats. This is especially important in Asia-Pacific and the Middle East and Africa, where modern retail expansion and higher processed food use are creating long-term volume support for the printed flexible packaging market. At the same time, premium food categories in mature markets are creating room for better print quality, shorter runs, and more frequent design refreshes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Resin, Film, and Ink Input Costs | -1.1% | Global | Short term (≤ 2 years) |

| Recycling Complexity of Multilayer Laminate Structures | -0.8% | Europe and North America | Medium term (2-4 years) |

| Capital Intensive Migration to Advanced Printing Lines | -0.5% | South America, the Middle East and Africa, emerging markets | Long term (≥ 4 years) |

| Food Contact and Extended Producer Responsibility Compliance Burden | -0.4% | Europe and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Resin, Film, and Ink Input Costs

Input cost swings remain one of the clearest constraints on the printed flexible packaging market because converters are heavily exposed to resin, film, foil, and ink pricing. Polyethylene and polypropylene costs remain sensitive to feedstock and energy prices, and that exposure is stronger in regions that depend on imported polymer supply. Ink systems are also under pressure because converters must balance performance, compliance, and availability simultaneously. Siegwerk introduced an NC-free ink color system for surface printing on polyolefin-based structures, and that move showed how compliance-driven reformulation is also becoming part of input cost management in the printed flexible packaging market. Converters that delay material and ink changes face a more difficult position because they may face both cost volatility and recyclability risk simultaneously.

Recycling Complexity of Multilayer Laminate Structures

The printed flexible packaging market still relies heavily on multilayer laminates because they deliver barrier, strength, and process performance that many applications have needed for years. That same structure mix is now a restraint because layers built from different materials are much harder to recover through standard recycling systems. The EU packaging and packaging waste framework is making this issue more urgent because packaging design is being pushed toward recyclable solutions that can work at scale across the region. BOBST reported that mono-material, high-barrier alternatives can reduce environmental impact while maintaining functionality, indicating the technical gap is narrowing, even though conversion is still not simple for every application. Converters in the printed flexible packaging market that build print, coating, and lamination capability around mono-material webs are likely to face lower long-term compliance friction than those that stay centered on legacy laminate structures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Printing Technology: Flexography Holds Scale as Digital Resets Economics

Flexography held 49.34% of the printed flexible packaging market in 2025, which kept it in the lead across long-run applications in food, personal care, and home care. Its position remained strong because converters continued to rely on favorable cost-per-meter economics, broad substrate compatibility, and steady improvements in print quality. Post-2020 progress in line-screen capability, expanded color systems, and faster plate change methods reduced the older quality gap that had once separated flexography more clearly from gravure. In April 2026, Amcor committed a multi-million-euro investment in a new flexographic printing line at Hardenberg in the Netherlands, adding capacity for up to 6,000 metric tonnes per year, which showed continued confidence in large-scale flexographic output.

Digital printing is projected to expand at an 11.71% CAGR through 2031, which makes it the fastest-growing process in the printed flexible packaging market size among printing technologies. The main reason is that digital systems are better suited to short runs, versioned packs, and jobs that need variable content or faster turnaround. That is changing supplier selection in the printed flexible packaging market because more buyers now want a converter that can manage both large-volume analog work and quick-turn digital work from the same platform. Rotogravure still retains a strong position in premium applications that demand very stable ink laydown and very high line speeds, especially where visual consistency remains critical over long runs. Other technologies, including hybrid and specialty systems, continue to serve narrower needs such as security print effects or tactile finishes, but they do not challenge the scale held by flexography and the growth pace now seen in digital.

By Packaging Type: Pouches Anchor Volume While Rollstock Sustains Converting Infrastructure

Pouches accounted for 35.98% of the printed flexible packaging market in 2025, reflecting their widespread use across food, healthcare, and personal care products. Stand-up, flat, and spouted pouch designs continue to attract demand because they combine strong shelf visibility with lower material use and good handling convenience. The stand-up pouch has become a common upgrade route for brands moving away from glass, rigid plastic, or older pack types that carry higher weight or less flexible design space. In September 2025, Siegwerk, Borouge, and TPN Food Packaging introduced a recyclable high-barrier mono-material stand-up pouch, showing that pouch growth in the printed flexible packaging market is now tied to both convenience and improved recyclability.

Rollstock and films remain central to the printed flexible packaging market because they support high-volume form-fill-seal operations and provide the production base that keeps many converter networks efficient. While the value per unit is lower than in several pre-made formats, rollstock provides converters with steady volume and longer runs that help fund investment in digital presses, coatings, and recycle-ready laminates. Bags and sacks still serve bulk industrial and agricultural use where print requirements are simpler but shipment volumes are large. Labels and shrink sleeves stay important as a graphics-led niche, and CCL Industries expanded that area in June 2026 through its acquisition of Sleever International, strengthening its flexible film and sleeve position across consumer goods and healthcare uses in global packaging. This leaves converters with a clear balancing act in the printed flexible packaging market because pouch-making growth attracts capital, while rollstock remains the format that often supports plant-level utilization and cash generation.

By End-User Industry: Food Anchors Volume as Healthcare Drives Value Premium

Food and beverage accounted for 47.08% of the printed flexible packaging market in 2025, making it the largest end-user group. The segment stayed ahead because flexible printed formats are widely used in snacks, confectionery, dairy, chilled foods, and beverage applications, where both barrier and branding are important. The Flexible Packaging Association continued to identify food and beverage as the dominant use case in the United States, supporting the view that food remains the main demand base for the printed flexible packaging market across regions.[2]Flexible Packaging Association, “2025 State of the U.S. Flexible Packaging Industry Report,” Flexible Packaging Association, flexpack.org Growth also reflects the spread of single-serve, portable, and meal-oriented packs, especially in urban channels where convenience carries more weight in purchase decisions. Within food, the gap between private-label needs and branded promotional needs is becoming more visible, as one side still favors low-cost, long-run printing while the other increasingly wants shorter, higher-change print programs.

Healthcare and pharmaceuticals are projected to grow at a 7.58% CAGR through 2031, making it the fastest-rising end-user group in the printed flexible packaging market. This segment is gaining momentum as track-and-trace rules, product security requirements, and substrate purity standards are increasing the value of accurate printed content on regulated packs. The Drug Supply Chain Security Act continues to reinforce the need for machine-readable codes and tighter product identification, which raises the importance of print precision and data handling in pharmaceutical packaging. That requirement supports higher-value work because coding, numbering, and other compliance elements are increasingly built into the print process rather than added later as a separate step. Personal care, home care, and industrial end uses still add breadth to the printed flexible packaging market, but healthcare is where converters are more likely to see stronger pricing for technical capability and documentation discipline.

By Substrate: Plastics Sustain Share While Paper Commands the Fastest Growth

Plastics held 46.23% of the printed flexible packaging market in 2025, giving them the leading position among substrate groups. Their scale remains hard to displace because polyethylene, polypropylene, PET, and related films still offer the best mix of barrier performance, printability, line compatibility, and cost at commercial volumes. Even so, the composition of plastic use is changing as converters and brand owners move away from more complex multi-layer combinations toward mono-PE and mono-PP designs better aligned with recycling goals. In March 2026, Amcor invested in a new line in Lugo di Vicenza, Italy, focused on high-barrier, recycle-ready films, including a mono-material retort solution, demonstrating how large suppliers are trying to keep plastics relevant through redesign rather than resistance to change.

Paper and paper-based substrates are projected to expand at a 7.03% CAGR through 2031, marking the fastest growth among major substrate options in the printed flexible packaging market. This rise reflects stronger fiber-based packaging programs from brand owners and a consumer view that paper is easier to understand and accept from a recycling standpoint. Paper is still constrained by the need to match barrier, grease resistance, moisture control, and shelf-life needs that plastic and foil structures have long delivered more easily. Even with those limits, the printed flexible packaging market is giving paper a larger role because converters are developing barrier-coated solutions that can address a wider range of food and home care uses. At the same time, aluminum foil and metallized structures remain necessary in certain high-barrier applications, although the shift toward recyclable mono-material alternatives is placing more pressure on those legacy constructions over time.

Geography Analysis

Asia-Pacific accounted for 37.89% of the printed flexible packaging market share in 2025, making it the largest regional market. The region benefits from China’s large converting base, India’s expanding food processing activity, and Japan’s strong demand for premium and tightly specified packaging applications. China remains important because fast production response and localized pack design are increasingly valued across e-commerce, food, and consumer goods channels. India continues to add volume through pouch, laminate, and rollstock demand as packaged food and fast-moving consumer goods distribution deepen across urban and semi-urban markets. Japan supports the higher-value side of the printed flexible packaging market because pharmaceutical and premium food categories continue to require strong print quality, compliance, and consistency.

Europe remained the second-largest region in the printed flexible packaging market, and it continues to be shaped by strict sustainability rules and demanding print standards. The EU Packaging and Packaging Waste Regulation is a major driver of converter investment, pushing the region away from non-recyclable multilayer structures toward mono-material films with functional coatings.[3]European Commission, “Packaging and Packaging Waste,” European Commission, europa.eu Germany and Italy remain important production centers, while Poland continues to attract activity as a competitive manufacturing base for flexible packaging conversion. North America keeps a strong position in the printed flexible packaging market because healthcare packaging, promotional brand runs, and specialty film applications continue to support investment in advanced print and material capability.

The Middle East and Africa is projected to expand at a 7.04% CAGR through 2031, which makes it the fastest-growing regional block in the printed flexible packaging market. Saudi Arabia is directing more attention toward downstream manufacturing, and that is improving the local base for flexible pack production in food, dairy, snacks, and personal care. Turkey is strengthening its role as a supply and trade link into North Africa, especially in rollstock and pre-made pouch movement. South Africa and Nigeria remain the main Sub-Saharan demand anchors, while South America is growing at a slower pace as Brazil continues to modernize food packaging formats and add more digitally printed applications in consumer and e-commerce channels.

Competitive Landscape

The printed flexible packaging market is moderately fragmented, with a limited group of global converters competing alongside a much broader field of regional and specialty suppliers. Amcor plc, Mondi plc, Constantia Flexibles, and Huhtamaki Oyj remain among the most visible large-scale names because they combine material development, converting scale, and multinational customer relationships. The Amcor and Berry Global combination, completed in April 2025, created a much larger packaging platform with broad reach across consumer, healthcare, and film applications, increasing the scale pressure felt across the printed flexible packaging market. In March 2026, TC Transcontinental completed the sale of its packaging business to ProAmpac for CAD 2.1 billion (USD 1.53 billion), further consolidating North American printed flexible packaging and widening ProAmpac’s operating footprint. These moves show that scale, financing capacity, and the ability to invest across print and substrate technology are becoming more important competitive tools.

Competition in the printed flexible packaging market is now centering on 3 practical areas: recyclable mono-material capability, digital print integration, and the ability to meet regulated packaging requirements. Amcor’s March 2026 investment in Italy strengthened its position in recycle-ready high-barrier films, which showed how major companies are aligning film design and print compatibility in one platform. Siegwerk’s 2025 work with Borouge and TPN Food Packaging showed another path to differentiation because de-inkable high-barrier mono-material pouches can give converters a better position when brand owners want both shelf performance and recyclability.[4]Siegwerk, “Borouge, Siegwerk, and TPN Food Packaging Launch Fully Recyclable Mono-Material Packaging Solution,” Siegwerk, siegwerk.com Amcor’s April 2026 collaboration with Metsä Group and G. Mondini also showed that direct digital printing is becoming part of broader commercialization strategy rather than a limited niche feature.

The printed flexible packaging market still leaves room for regional and specialist converters because many customers need short runs, local service, or narrow technical expertise rather than only scale. Printpack’s 2025 performance at the Flexible Packaging Association Achievement Awards showed that product development, sustainability work, and shelf impact remain meaningful points of distinction below the very largest global players. Coveris also expanded capability through a EUR 9.5 million (USD 10.45 million) investment at its Halle facility in Germany, reinforcing the idea that targeted site upgrades remain an active competitive lever in the printed flexible packaging market. Overall, the competitive picture is becoming firmer at the top, but the market is still broad enough that mid-sized specialists can remain relevant when they offer clear technical or regional advantages.

Printed Flexible Packaging Industry Leaders

Amcor plc

Huhtamaki Oyj

Constantia Flexibles Group GmbH

Sealed Air Corporation

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Amcor advanced its collaboration with Metsä Group and G. Mondini to commercialize a fiber-based packaging solution featuring G. Mondini's direct digital printing for fiber trays, enabling brand differentiation while preserving natural appearance.

- April 2026: Sealed Air Corporation completed its acquisition by funds affiliated with CD&R at a USD 10.3 billion enterprise value, transitioning to private ownership. CD&R committed to supporting Sealed Air's continued investment in its food and protective packaging platforms.

- March 2026: Amcor invested in a new production line at its Lugo di Vicenza, Italy site dedicated to high-barrier recycle-ready films, including AmLite HeatFlex for retort-compatible mono-material lidding and pouches serving food, beverage, and healthcare applications.

- March 2026: TC Transcontinental Inc. completed the sale of its Packaging Sector to ProAmpac Holdings Inc. for CAD 2.1 billion (USD 1.53 billion), making ProAmpac one of North America's largest printed flexible packaging converters with approximately 3,600 additional employees.

Global Printed Flexible Packaging Market Report Scope

The Printed Flexible Packaging Market refers to the segment of the flexible packaging industry that incorporates printed designs, branding, and information directly onto packaging materials. This type of packaging is widely used across various industries, including food and beverages, pharmaceuticals, and personal care, due to its ability to enhance product appeal and provide essential information to consumers.

Printed Flexible Packaging Market Report is Segmented by Printing Technology [Flexography, Rotogravure, Digital (Inkjet, Electrophotography), and Other Printing Technologies], Packaging Type [Pouches (Stand-up, Flat, Spouted), Rollstock and Films, Bags and Sacks, Labels and Shrink Sleeves, and Other Packaging Types], End-User Industry (Food and Beverage, Healthcare and Pharmaceuticals, Personal Care and Cosmetics, Home Care and Industrial, and Other End-User Industries), Substrate [Plastics (PE, PP, PET, Others), Paper and Paper-based, Aluminum Foil and Metallised Films, and Other Substrate Types], and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Flexography |

| Rotogravure |

| Digital (Inkjet, Electrophotography) |

| Other Printing Technologies |

| Pouches (Stand-up, Flat, Spouted) |

| Rollstock and Films |

| Bags and Sacks |

| Labels and Shrink Sleeves |

| Other Packaging Types |

| Food and Beverage |

| Healthcare and Pharmaceuticals |

| Personal Care and Cosmetics |

| Home Care and Industrial |

| Other End-User Industries |

| Plastics (PE, PP, PET, Others) |

| Paper and Paper-based |

| Aluminum Foil and Metallised Films |

| Other Substrate Types |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Thailand | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Printing Technology | Flexography | ||

| Rotogravure | |||

| Digital (Inkjet, Electrophotography) | |||

| Other Printing Technologies | |||

| By Packaging Type | Pouches (Stand-up, Flat, Spouted) | ||

| Rollstock and Films | |||

| Bags and Sacks | |||

| Labels and Shrink Sleeves | |||

| Other Packaging Types | |||

| By End-User Industry | Food and Beverage | ||

| Healthcare and Pharmaceuticals | |||

| Personal Care and Cosmetics | |||

| Home Care and Industrial | |||

| Other End-User Industries | |||

| By Substrate | Plastics (PE, PP, PET, Others) | ||

| Paper and Paper-based | |||

| Aluminum Foil and Metallised Films | |||

| Other Substrate Types | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Thailand | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast size of the printed flexible packaging space?

The printed flexible packaging market was valued at USD 117.84 billion in 2025, stands at USD 124.51 billion in 2026, and is forecast to reach USD 168.76 billion by 2031 at a 6.27% CAGR.

Which printing technology is growing the fastest in printed flexible packaging?

Digital printing is projected to expand at an 11.71% CAGR through 2031 because brand owners increasingly need shorter runs, versioned packs, and faster turnaround.

Which packaging format leads demand in printed flexible packaging?

Pouches led with a 35.98% share in 2025 because they combine shelf visibility, convenience, and broad use across food, healthcare, and personal care.

Why is healthcare becoming more important for printed flexible packaging suppliers?

Healthcare and pharmaceuticals is projected to grow at a 7.58% CAGR through 2031 as serialization, coding, and compliance requirements raise the value of precise printed content.

Which substrate is growing the fastest in printed flexible packaging?

Paper and paper-based substrates are projected to expand at a 7.03% CAGR through 2031, even though plastics still held the largest share at 46.23% in 2025.

Which region offers the strongest growth outlook for printed flexible packaging?

The Middle East and Africa is forecast to grow at a 7.04% CAGR through 2031, while Asia-Pacific remained the largest regional market with a 37.89% share in 2025.

Page last updated on: