Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 20.94 Billion |

| Market Size (2031) | USD 27.71 Billion |

| Growth Rate (2026 - 2031) | 5.76% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flexographic Printing Market Analysis by Mordor Intelligence

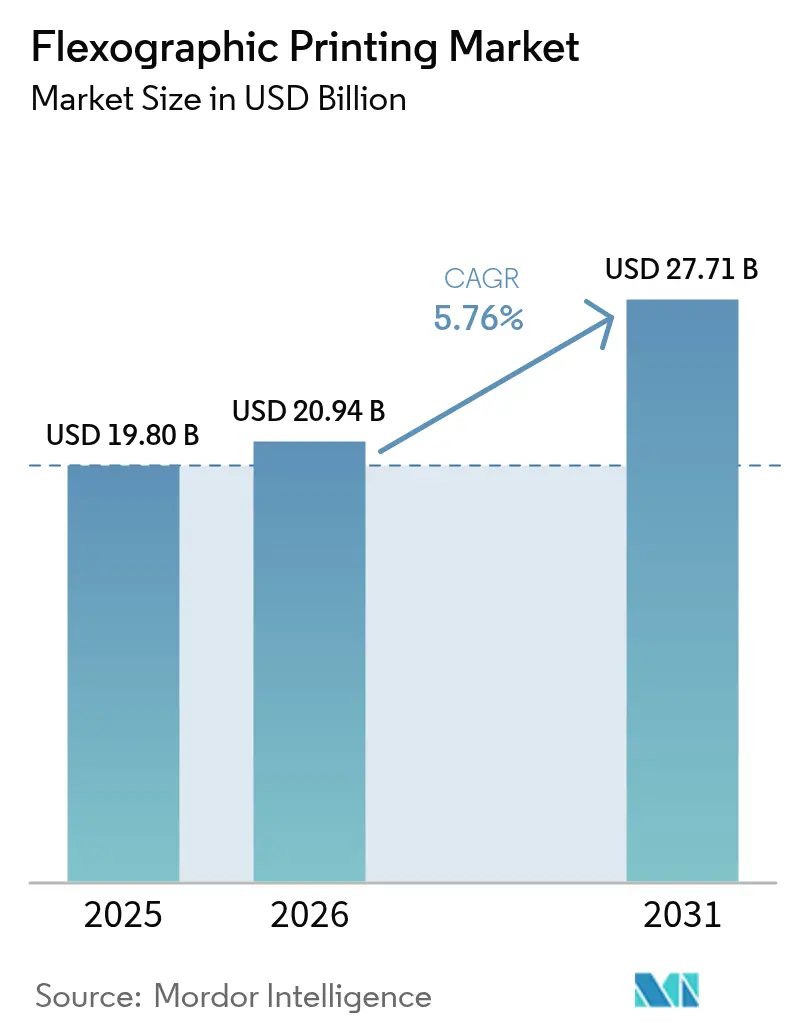

The flexographic printing market size was valued at USD 19.80 billion in 2025 and estimated to grow from USD 20.94 billion in 2026 to reach USD 27.71 billion by 2031, at a CAGR of 5.76% during the forecast period (2026-2031). Rising e-commerce volumes, stringent food-contact regulations, and continuous improvements in AI-enabled press automation are expected to uphold this momentum in the flexographic printing market. Equipment vendors are optimizing narrow-web and digital-hybrid presses to serve brands that juggle shorter SKU life cycles, while converters intensify water-based ink adoption to comply with global VOC thresholds. Growing demand for sustainable corrugated logistics, together with investments in rapid plate-mounting and inspection systems, keeps the flexographic printing market well placed against competing lithography and gravure methods. Asia-Pacific’s manufacturing capacity, paired with government incentives for circular packaging, further cements the region’s leadership role in the flexographic printing market.

Key Report Takeaways

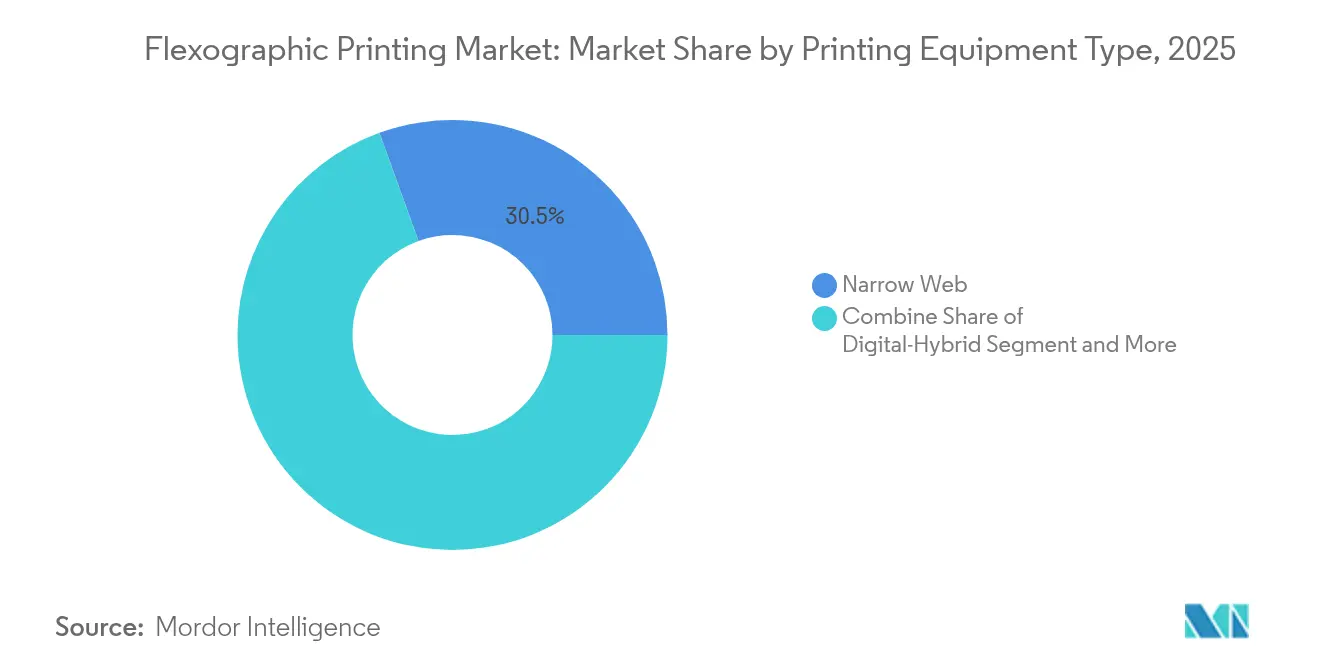

- By printing equipment, narrow-web presses led with 30.52% revenue share in 2025, while digital-hybrid systems are projected to advance at 9.09% CAGR.

- By ink type, water-based formulations accounted for 40.42% of the flexographic printing market size in 2025; UV-curable inks are set to expand at 8.28% CAGR.

- By substrate type, paper and paperboard led with 45.10% revenue share in 2025, while flexible plastic films are projected to advance at 7.86% CAGR.

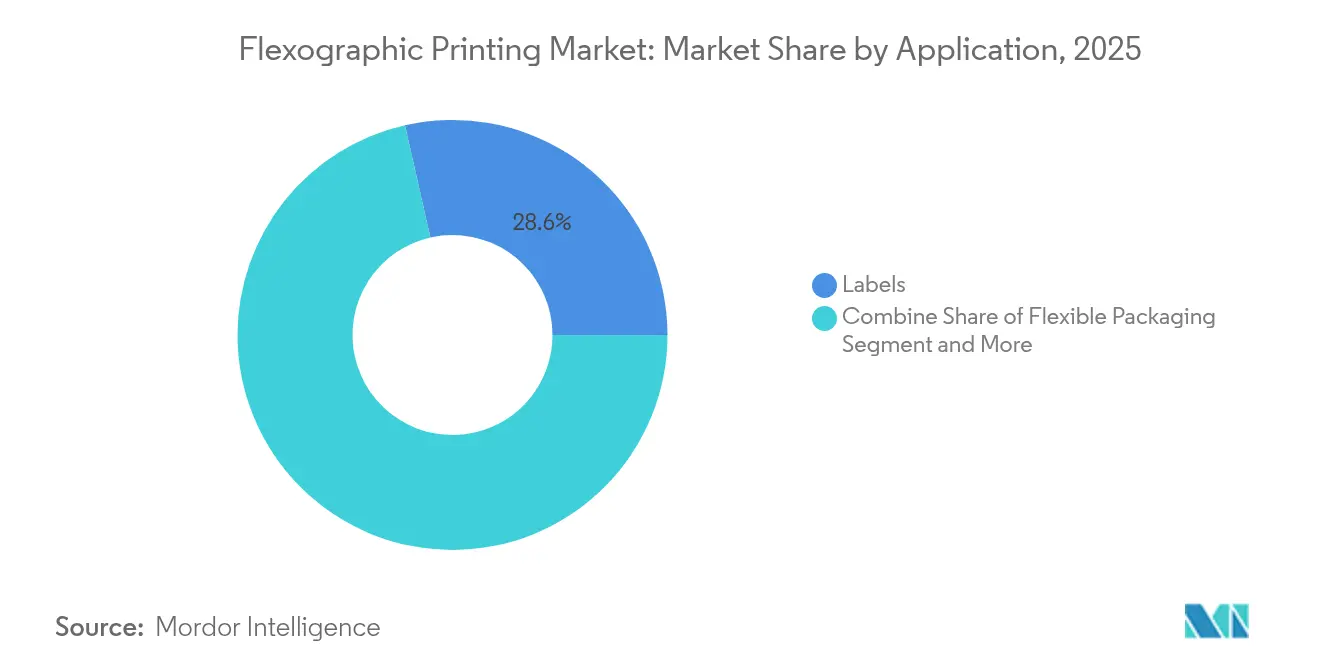

- By application, flexible packaging is projected to climb at 8.05% CAGR to 2031, overtaking labels, which retained 28.55% revenue share in 2025.

- By end-user industry, healthcare and pharmaceuticals are anticipated to record the fastest 9.05% CAGR, even as food and beverage held 34.10% share of the flexographic printing market size in 2025.

- By geography, Asia-Pacific commanded 38.05% of flexographic printing market share in 2025, and the region is forecast to grow at 9.06% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Flexographic Printing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Brand-owner demand for shorter SKU cycles | +1.2% | Global; North America and EU most active | Medium term (2-4 years) |

| Cost-effective long-run package printing | +0.9% | Asia-Pacific core; spill-over into MEA | Long term (≥ 4 years) |

| Water-based ink adoption for food compliance | +1.1% | Global; led by North America and EU regulations | Short term (≤ 2 years) |

| Sustainable corrugated logistics | +0.8% | Global; earliest traction in Europe and North America | Medium term (2-4 years) |

| AI-driven press automation | +1.0% | Asia-Pacific and North America, expanding across the EU | Long term (≥ 4 years) |

| E-commerce multi-wall mailers | +0.7% | Global; concentrated in urban fulfillment hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Brand-owner Demand for Shorter SKU Cycles

Consumer preferences now turn over faster than ever, pushing brand managers to refresh packaging artwork frequently. Converters respond by leaning on narrow-web presses that complete plate changes in minutes, curbing downtime and material waste. Solutions such as the Onyx GO deliver active register control that lowers setup scrap by 30%. [1]Uteco Converting S.p.a., “Onyx GO,” uteco.comShorter runs also let retailers pilot seasonal editions without carrying surplus inventory, reducing the working-capital burden throughout the flexographic printing market. In parallel, cloud-based workflow software accelerates artwork approvals, ensuring that new designs progress from concept to shelf within weeks.

Cost-Effective Long-Run Package Printing

Where volumes exceed millions of impressions, flexography still offers the lowest unit cost. Photopolymer plates last hundreds of thousands of cycles, while energy-efficient dryers reduce operating expenses. DuPont’s Orion case illustrates 30% solvent savings after migrating from gravure to flexo, along with safer shop-floor conditions. [2]DuPont, “Orion adopts advanced flexography,” dupont.comSuch economics keep legacy consumer-goods lines anchored in the flexographic printing market, preserving press utilization and spare-parts sales for OEMs. Asian converters, often running three shifts, maximize these cost advantages to meet export-driven demand.

Water-Based Ink Adoption for Food Contact Compliance

Regulators on both sides of the Atlantic cap solvent residues in primary packaging, steering printers toward water-based or low-migration UV sets. These formulations eliminate hazardous VOCs and demonstrate strong adhesion on paper as well as treated films. TROY Group’s UV/LED low-migration inks meet FDA 21 CFR §175.300 limits while cutting curing energy by up to 60%. [3]TROY Group, “Inks for Food Packaging,” troygroup.com Early adopters enjoy premium supplier status with multinational food producers, and that differentiation supports price realization in the flexographic printing market.

Shift Toward Sustainable Corrugated Logistics

E-retail generates parcel volumes that favor shock-resistant, easily recycled corrugated boxes. Flexo presses equipped with anilox rolls optimized for high-porosity liners deliver bold graphics without crushing micro-flutes. The EU Circular Economy Action Plan accelerates this shift by stipulating recycled-content thresholds. Logistics firms also cite reduced pallet weight, shrinking emissions throughout the supply chain. Converters able to certify paper provenance under FSC or PEFC gain access to retailer “green-label” programs, lifting overall demand in the flexographic printing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital inkjet cannibalisation in short runs | -0.8% | Global; most acute in highly automated economies | Short term (≤ 2 years) |

| Volatile photopolymer plate prices | -0.6% | Global; supply chain concentrated in Asia | Medium term (2-4 years) |

| Solvent-based VOC regulations tightening | -0.7% | North America and EU, gradually affecting APAC | Medium term (2-4 years) |

| Skilled press-operator shortage | -0.5% | Global; widest gap in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital Inkjet Cannibalisation in Short Runs

Advances in piezo-electric heads and aqueous dispersion inks enable variable data and near-offset image quality at competitive click rates. Pharmaceutical packagers integrate digital lines with ERP software to produce country-specific leaflets on demand, cutting inventory to zero. In response, the flexographic printing market is pivoting to hybrid presses that merge in-line inkjet stations with conventional units, preserving established finishing workflows while adding serialization capability.

Volatile Photopolymer Plate Prices

Elastomer and resin feedstocks remain exposed to petrochemical swings and geopolitical uncertainty. Spot surcharges reached double-digit percentages in late 2024, eroding gross margins for converters locked into annual supply contracts. Liquid plate technology, pioneered by MacDermid, promises lower raw-material intensity and localized production, though adoption still sits below 5% of all new plate volumes. Stable plate pricing is critical for job costing accuracy, and volatility continues to temper expansion plans in the flexographic printing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Printing Equipment Type: Digital-Hybrid Drives Innovation

Digital-hybrid presses lifted their share of new installations as converters sought one line that could alternate between mass-production mode and personalized batches. Although narrow-web machines secured 30.52% of revenue in 2025, the hybrid cohort is on course for 9.09% CAGR, well above the overall flexographic printing market. Typical configurations combine 10-color flexo decks for brand colors with CMYK inkjet bars placed just before the rewinder. Such set-ups reduce job changeover time to under five minutes, keeping lines profitable even when average order quantities fall below 5,000 linear m. Medium-web lines remain favored in tissue overwraps and snack wrappers, while wide-web CI flexo retains dominance in stand-up pouches. Sheet-fed presses serve folding cartons that require precise die-cutting stations downstream.

Converters equipping themselves with modular platforms can later bolt on corona treaters, chill rolls, or second inkjet bars as client mixes evolve. The SapphireLUCE exemplifies this modular path, pairing 1200 × 1200 DPI resolution with speeds of 150 mpm. Service-level agreements often bundle predictive-maintenance analytics, shrinking unplanned downtime below 2% of available hours. These feature sets sustain pricing power for OEMs, even as the broader flexographic printing market experiences competitive pressure from refurbished presses in emerging economies.

By Ink Type: UV-Curable Gains Despite Water-Based Dominance

Water-based systems commanded 40.42% revenue in 2025 thanks to low odour and direct-food-contact approval in most jurisdictions. They form the baseline chemistry for corrugated boxes, folding cartons, and paper wraps. UV-curable inks, however, are projected to register 8.28% CAGR through 2031 because they support higher line speeds and excellent scratch resistance on non-porous films. Energy-curable solutions require compact LED lamps that draw 65% less power than mercury arc units, reducing plant electricity bills. Solvent variants, constrained by tightening VOC caps under the US EPA Part 59 ruling, continue to cede share. Electron-beam curables remain a niche at under 2% penetration but show promise in dairy lidding and aseptic cartons.

Ink suppliers differentiate through pigment dispersion stability, rheology control, and low-migration additive packages. INX International’s GelFlex EB ink removes lamination in certain snack applications, dropping gauge weight and cutting foil usage. Such innovations echo the broader sustainability narrative resonating throughout the flexographic printing market.

By Substrate Type: Flexible Films Challenge Paper Dominance

Paper and paperboard still represented 45.10% of print surface area in 2025, propelled by surge demand for e-commerce shippers. By contrast, multi-layer PE, PP, and PET films are forecast to advance at 7.86% CAGR, outpacing earlier projections due to expanded grocery delivery. Metallised foils safeguard aroma and light-sensitive foods, maintaining relevance despite recyclability debates. High-barrier films treated with plasma enable mono-material pouches, opening a new sustainability pathway that keeps plastics competitive.

Brand owners now pilot chemically recycled feedstock, allowing drop-in grades that meet soon-to-mature recycled-content mandates. National Flexible’s protein-bar wrapper using 70% recycled PET underscores this commercial reality. Such case studies highlight how substrate evolution directly shapes capex plans in the flexographic printing market.

By Application: Flexible Packaging Outpaces Traditional Segments

Label lines generated 28.55% of revenue in 2025, but flexible packaging is on track for 8.05% CAGR as omni-channel retail demands robust mailer protection. Corrugated shippers retain core logistics applications yet transition toward premium inside-print graphics for improved unboxing experiences. Folding cartons, challenged by substrate substitutions, maintain share where structural rigidity is essential. Print media continues its secular contraction as brand owners redirect budgets to digital channels.

Converters serving fresh produce tap variable-data flexo to print traceability QR codes each shift. Emerald Packaging deploys this model across 2 billion pouches annually, reflecting a broader pivot toward on-pack engagement. These use cases expand value capture within the flexographic printing market beyond traditional food branding.

By End-User Industry: Healthcare Drives Premium Growth

Food and beverage producers consumed 34.10% of total press output in 2025, riding consistent staple-goods demand. Healthcare and pharmaceuticals, however, will log the highest 9.05% CAGR as serialization rules spread worldwide. OTC drugs and medical-device labels require micro-text, high-contrast barcodes, and tamper-evident varnishes, functions well supported by high-line-screen anilox rolls. Personal care brands prioritize metallic effects and natural-fiber substrates, delivering steady premium volumes. Industrial firms, such as chemical drum suppliers, value UV-resistant inks that survive outdoor storage.

WestRock integrates blister-card and leaflet production under ISO 13485 protocols, offering turnkey solutions that simplify vendor qualification for drug companies. Such specialist capability underpins margin resilience in the flexographic printing market’s healthcare vertical.

Geography Analysis

Asia-Pacific generated the largest revenue slice at 38.05% in 2025 and is projected to compound at 9.06% CAGR to 2031. China supplies substrates, inks, and machinery, enabling integrated cost synergies, while India posts double-digit e-commerce parcel growth that fuels domestic packaging demand. Japan and South Korea emphasize automation, pioneering press lines equipped with cobot-assisted roll changes. Government recycling targets across ASEAN incentivize water-based inks and mono-material pouch designs, broadening addressable opportunities throughout the flexographic printing market.

North America remains the technology pioneer, hosting pilot runs for AI-driven inspection cameras and cloud-connected viscosity controllers. Brand owners reward converters that demonstrate FDA-compliant low-migration workflows, sustaining high value-added print per square meter. Labor shortages persist, prompting initiatives like Ricoh’s Advanced Career Education program that trains operators in press-side data analytics. Nearshoring trends reroute consumer-goods manufacturing from Asia to Mexico, spurring fresh investments in CI flexo lines within North America.

Europe maintains keen regulatory oversight, compelling swift adoption of plant-based photoinitiators and mineral-oil-free ink sets under the Zero Pollution framework. Germany anchors engineering excellence, France accelerates bio-plastic packaging, and Italy scales narrow-web competence hubs such as Bobst’s 1,200 sqm Florence center. Eastern European converters leverage favorable wage structures to absorb overflow orders, reinforcing the region’s diverse role in the flexographic printing market.

Regulatory Landscape

Packaging sustainability and food-contact requirements are increasingly shaping flexographic ink, substrate, and workflow choices, particularly for flexible packaging and paper-based formats. In the EU, the Packaging and Packaging Waste Regulation, Regulation (EU) 2025/40, entered into force on 11 February 2025 and introduces packaging sustainability and labeling requirements that generally apply from 12 August 2026. This is reinforcing converter demand for low-migration chemistries and packaging designs compatible with recycling streams.

Technical standards are also tightening design-for-recycling constraints on print layers. CEN published EN 18120-7:2026 in April 2026 with design-for-recycling guidelines for PE and PP flexible packaging, including guidance relevant to printing inks and their compatibility with recycling processes. In the United States, the FDA determined on 6 January 2025 that 35 PFAS-related food contact notifications for grease-proofing paper and paperboard packaging were no longer effective, with a final compliance date of 30 June 2025. This is accelerating substitution toward PFAS-free barrier and ink systems for food-contact packaging.

Competitive Landscape

The global flexographic printing market is moderately concentrated, with the top five press and pre-press suppliers combining to cover between 35% and 45% of annual equipment billings. Bobst, Heidelberger Druckmaschinen, Mark Andy, Koenig & Bauer, and SOMA sustain differentiation through integrated workflow software, remote diagnostics, and flexible service contracts. Each has introduced AI modules that dynamically adjust ink keys and tension settings, reducing waste by up to 20%. XSYS’s acquisition of MacDermid Graphics Solutions expanded vertical integration into photopolymer plates, fortifying supply stability for large converter groups.

New entrants focus on single-pass inkjet architectures or regionalized service models that promise faster spare-parts delivery. However, buyers still value proven color-management libraries and long-life mechanical frames. SOMA’s Optima press uses machine-learning vision to flag print variations in milliseconds, highlighting how incumbents fuse software with hardware to defend share. Across the flexographic printing market, price competition intensifies in mid-tier CI presses, yet premium hybrid lines preserve double-digit margins.

Strategic alliances also shape competition. Bobst collaborates with apex roller specialists to optimize cell geometry, while ink vendors partner with OEMs to certify low-migration recipes ahead of legislation. Consolidation is set to continue as suppliers seek scale to fund R&D and meet end-user sustainability scorecards. The resulting ecosystem favors participants that can deliver cradle-to-cradle solutions, spanning plate imaging, anilox cleaning, and digital twin simulations.

Flexographic Printing Industry Leaders

Bobst Group SA

OMET S.r.l

Comexi Group

Mark Andy Inc.

Edale Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory-driven recyclability requirements and brand-owner sustainability scorecards are expanding whitespace for de-inkable and recycling-compatible ink systems, along with process upgrades in plate-making and press automation. Market actions provide evidence in this direction: Siegwerk received RecyClass Technology Approval in March 2026 for its UR 62 flexographic ink to support recyclable PE and PP structures, and Actega and Living Ink Technologies launched ACTExact UV Black Algae Ink in March 2026 as a carbon-negative pigment option designed for compatibility with conventional UV flexographic systems. Together, these developments expand the addressable space for ink suppliers and converters to qualify low-migration, recyclable structures on both virgin and higher-PCR substrates while sustaining print performance.

On the converter side, capacity and capability investments point to near-term opportunities in higher-value flexible packaging and labels, particularly where modern CI flexo and multi-station lines improve consistency and uptime. Amcor announced a multi-million-euro investment in April 2026 in a new flexographic printing line at Hardenberg, the Netherlands, with commissioning scheduled for summer 2026. Tecnopack Univel also commissioned a Bobst VISION CI press at Mortara in May 2026 to expand capacity. On productivity and energy efficiency, DuPont Cyrel FAST received GreenCircle certification in April 2026 for reducing energy consumption versus solvent-based plate-making, supporting growing demand for audited efficiency improvements that help converters meet customer and regulatory requirements while reducing operating costs.

Recent Industry Developments

- June 2026: Bobst launched a redesigned MASTERFOLD folder-gluer range built on a fully redesigned platform for corrugated converting. The update improves end-to-end packaging line integration where flexo-printed corrugated jobs require higher throughput, automation, and compliance with evolving European requirements.

- December 2025: Edale announced a press portfolio refresh aligned with Canon, introducing the LabelLine (FL4e, FL4p) and CartonLine (FL6p, FL7p) series. The expansion broadens the set of modular flexo press options for converters serving both label and carton applications, supporting faster configuration matching to shorter SKU cycles.

- September 2024: Mark Andy highlighted next-generation flexographic solutions at Labelexpo with reported customer uptake. The focus on newer platforms and workflows reflected converter demand for productivity features and quality control that reduce setup waste and improve consistency across frequent changeovers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of flexographic printing services delivered using flexo presses to print on packaging and label substrates, where revenues are counted from the printing activity and its directly linked work (prepress setup and finishing as billed).

Scope exclusions: We exclude standalone sales of printing presses, inks, plates, and unrelated commercial print processes where flexo is not the printing method used.

Segmentation Overview

- By Printing Equipment Type

- Narrow Web

- Medium Web

- Wide Web

- Sheet-Fed

- Digital-Hybrid

- By Ink Type

- Water-Based

- Solvent-Based

- UV-Curable

- Electron-Beam

- By Substrate Type

- Paper and Paperboard

- Flexible Plastic Films

- Metallic Foil

- Other Substrate Type

- By Application

- Corrugated Boxes

- Folding Carton

- Flexible Packaging

- Labels

- Print Media

- Other Application

- By End-user Industry

- Food and Beverage

- Healthcare and Pharmaceuticals

- Personal Care and Cosmetics

- Industrial

- Other End-user Industry

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public packaging and print industry signals to set realistic volume and pricing guardrails. Useful inputs came from sources such as the US Census Bureau manufacturing and trade series, Eurostat industrial production releases, UN Comtrade for packaging material trade flows, and US EPA publications on VOC and solvent handling that affect ink choices and compliance costs.

We also reviewed equipment and converter disclosures in annual reports, investor presentations, and reputable trade press so the model reflects how capacity, utilization, and customer mix are changing. Patent databases were referenced to understand the pace of press, plate, and curing innovation without overstating adoption. A company financials and intelligence subscription and a news and financials subscription were used selectively to normalize revenue splits and track plant expansions. The sources listed here are illustrative only, and many other public documents were used to collect data, cross-check assumptions, and clarify gaps.

Primary Interviews and Surveys

Primary inputs were collected from conversations and structured questionnaires with print service providers, packaging converters, material suppliers, and a few downstream buyers that specify print requirements. Since this is a global market, views were balanced across APAC, EMEA, and the Americas to confirm utilization trends, typical run lengths, pricing moves, and where flexo is gaining or losing share versus adjacent printing methods.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 14% | APAC: 47% |

| Mid tier: 50% | Functional/Unit leaders: 41% | EMEA: 30% |

| Smaller Players: 16% | Managers: 45% | Americas: 23% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where packaging print demand is reconstructed from packaging output and trade indicators, and then filtered through flexo penetration by substrate and application before value is applied. The key inputs we leaned on include flexible packaging and corrugated output trends, label demand linked to FMCG volumes, average press utilization ranges, typical job mix shifts toward shorter runs, and ink system migration toward water-based options where regulations and brand requirements push change.

After the top-down totals were created, they were checked against selective bottom-up approximations, including sampled converter revenue ranges, channel checks on printed square meter throughput, and simple ASP by volume sanity checks for labels and flexible packaging. Where coverage gaps showed up in smaller geographies, assumptions were bridged using proxy indicators such as packaging production growth, import dependence, and installed converting capacity. Forecasts were produced using scenario analysis supported by a light multivariate regression on packaging output, consumer staples demand, and trade flows, and then adjusted using what interviewees expect for pricing and utilization over the next few years.

Data Validation & Update Cycle

Outputs were validated by comparing implied print volumes and revenue per unit against independent signals such as packaging production series, converter margin patterns, and reported capacity additions. When large variances appeared, the assumptions were revisited, and respondents were re-contacted to confirm whether the change came from pricing, mix, or utilization rather than a modeling error.

Before sign-off, the model goes through multi-step analyst review where regional splits, growth rates, and currency conversions are checked for consistency. The study is refreshed annually, and interim updates are made when major events occur, such as regulatory shifts, large capacity expansions, or sudden raw material cost moves that affect print pricing. Right before delivery, a final review pass is done so clients receive the most current view available.

Mordor Intelligence's Flexographic Printing Market Size Measured Against Other Published Estimates

Published values for flexographic printing rarely align perfectly because the scope and the revenue point being counted can shift from one publisher to another. Differences also come from the choice of base year, the way currencies are converted, and how much primary validation is used to confirm utilization and pricing assumptions.

In practice, the biggest gaps show up when one estimate counts only printed packaging output while another rolls in equipment, consumables, or broader printing categories under the same label. Some sources also lean on a single base year and apply a flat CAGR, even though mix shifts (labels versus corrugated), ink system changes, and utilization cycles can move the value line in uneven steps.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 20.94 B (2026) | |

| Industry Research House A | USD 9.17 B (2024) | Uses an earlier base year and appears to apply a narrower value definition that leans toward select application segments, which can reduce the counted revenue pool versus a full flexo services view. |

| Publisher B | USD 9.10 B (2024) | Builds the estimate around a segmented taxonomy by ink and substrate with a 2024 base, and the total can differ if parts of converter services, prepress, or finishing are not consistently captured across regions. |

The spread in the table is mainly explained by the year used and what is treated as in-scope flexo revenue, along with how aggressively pricing and utilization are refreshed during validation, which is why the service-led definition and the 2026 anchoring were kept explicit before the name is even mentioned, Mordor Intelligence.

Key Questions Answered in the Report

What is the current value of the flexographic printing market?

The flexographic printing market size reached USD 20.94 billion in 2026.

How fast is the flexographic printing market expected to grow?

The market is forecast to post a 5.76% CAGR between 2026 and 2031.

Which region leads the flexographic printing market?

Asia-Pacific holds 38.05% revenue share and will pace growth at 9.06% CAGR through 2031.

What equipment segment is expanding the quickest?

Digital-hybrid presses are projected to rise at 9.09% CAGR owing to their ability to handle both long and short runs efficiently.

Why are water-based inks so prominent in flexographic printing?

They meet tightening food-contact and VOC regulations while supporting sustainable packaging goals, securing 40.42% market share in 2025.

Which end-user vertical is projected to grow the fastest?

Healthcare and pharmaceuticals will expand at 9.05% CAGR as serialization mandates spread worldwide.

Page last updated on: