Offset Printing Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

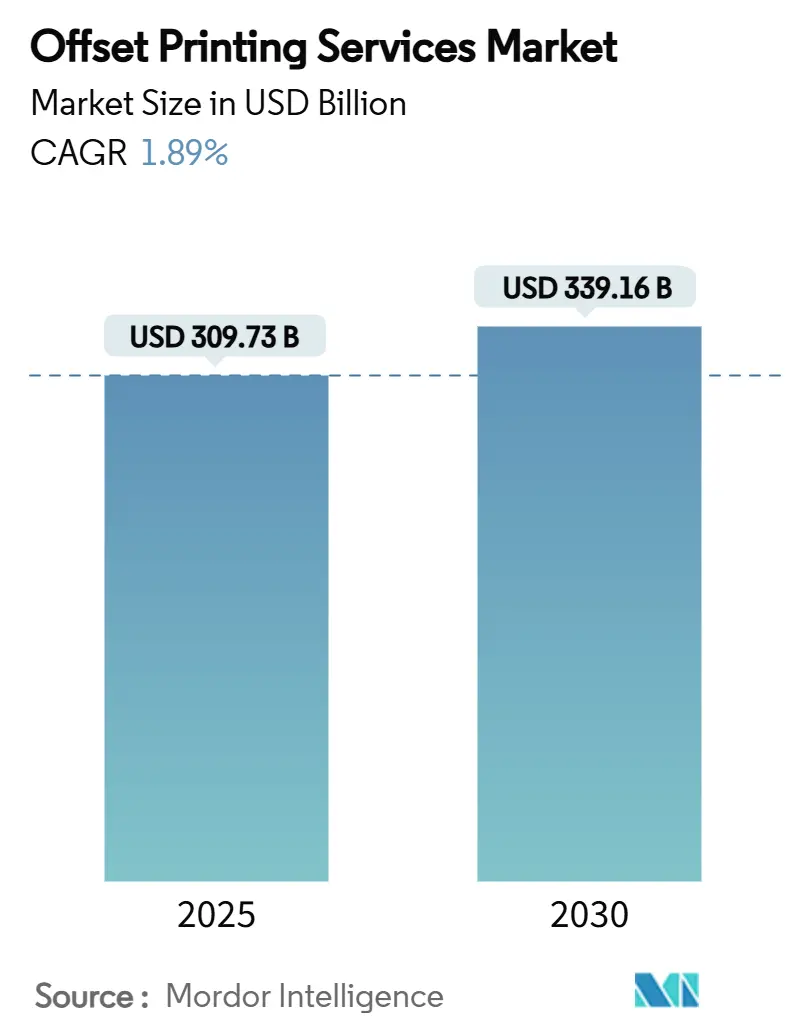

| Market Size (2025) | USD 309.73 Billion |

| Market Size (2030) | USD 339.16 Billion |

| Growth Rate (2025 - 2030) | 1.89% CAGR |

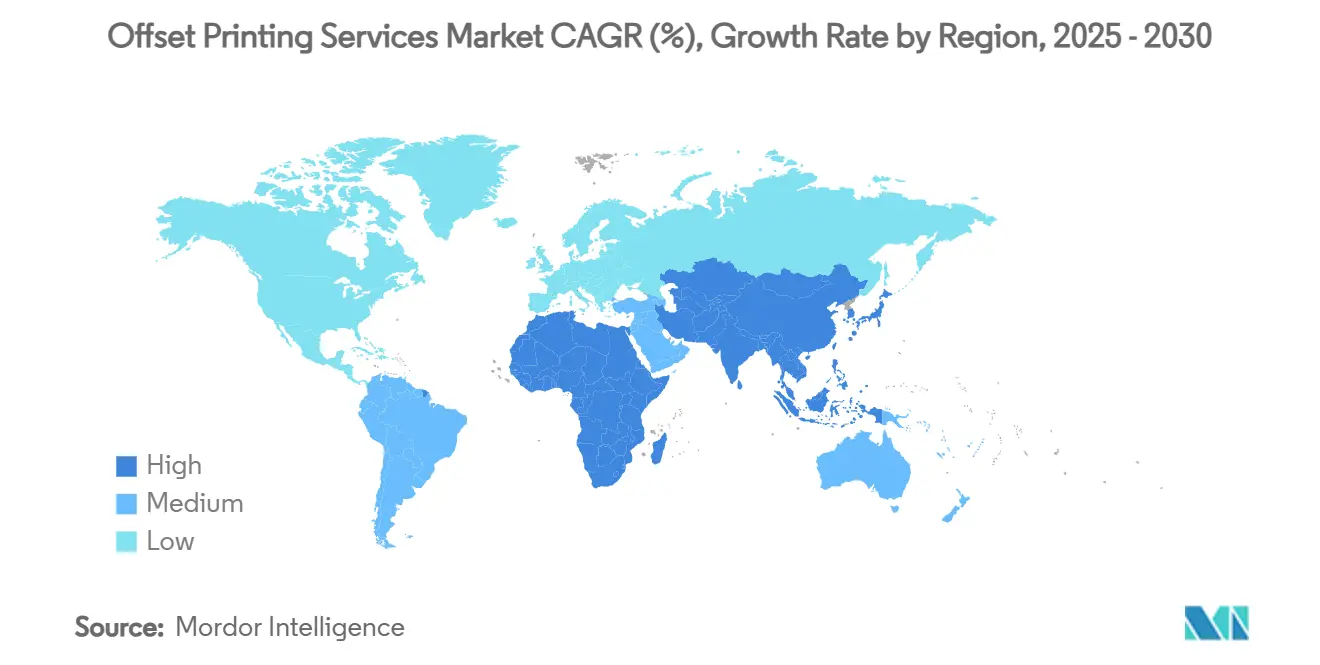

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

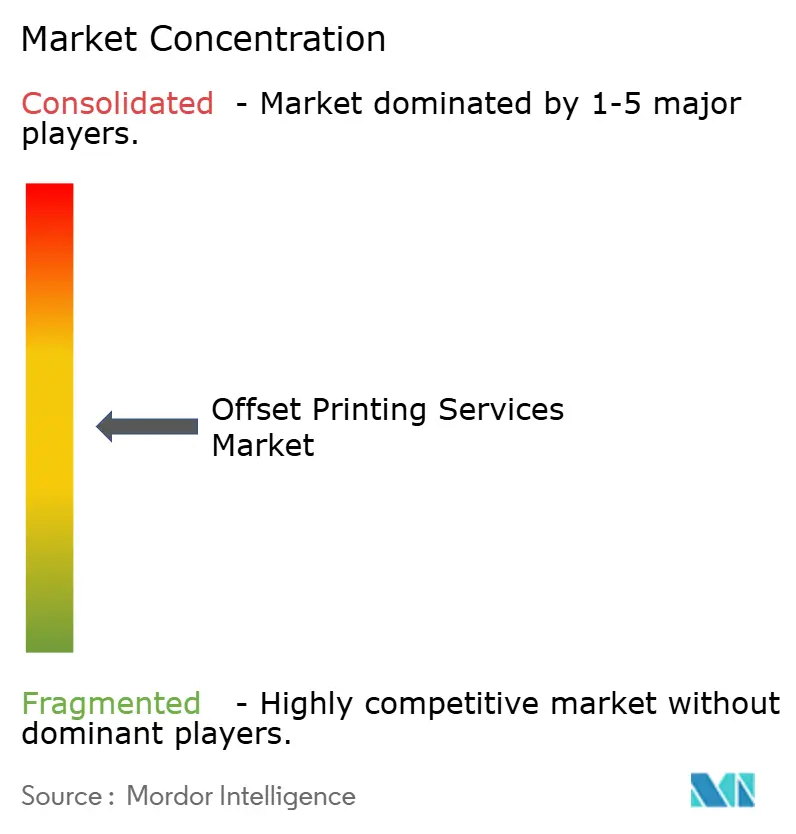

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Offset Printing Services Market Analysis by Mordor Intelligence

The offset printing services market size stands at USD 309.73 billion in 2025 and is forecast to reach USD 339.16 billion by 2030 on a steady 1.83% CAGR. This trajectory reflects a mature sector that continues to modernize as digital communication saturates and sustainability standards tighten. Persistent demand for high-quality, tactile print in books, packaging, labels, and security documents underpins a resilient outlook even as customers adopt multichannel strategies. Print service providers now combine workflow automation with lean production to protect margins from volatile aluminum plate costs and energy price swings. Late-stage consolidation among equipment makers and service firms further stabilizes industry structure while innovations such as carbon-neutral press retrofits create fresh revenue streams. Asia-Pacific remains the volume engine, but the Middle East and Africa are gaining ground on the back of economic diversification and retail formalization.

Key Report Takeaways

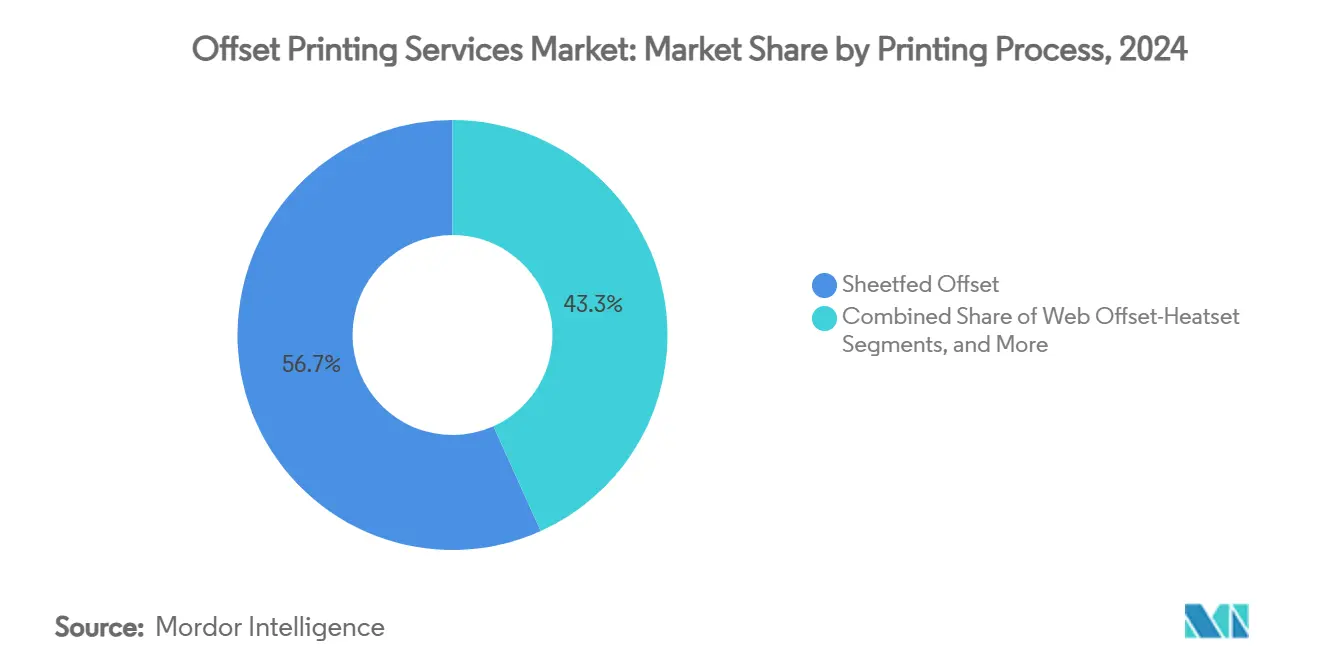

- By printing process, the offset printing services market for Others (waterless and UV) segment is projeted to grow at a 2.89% between 2025-2030.

- By application, Books captured 36.47% share of the offset printing services market in 2024.

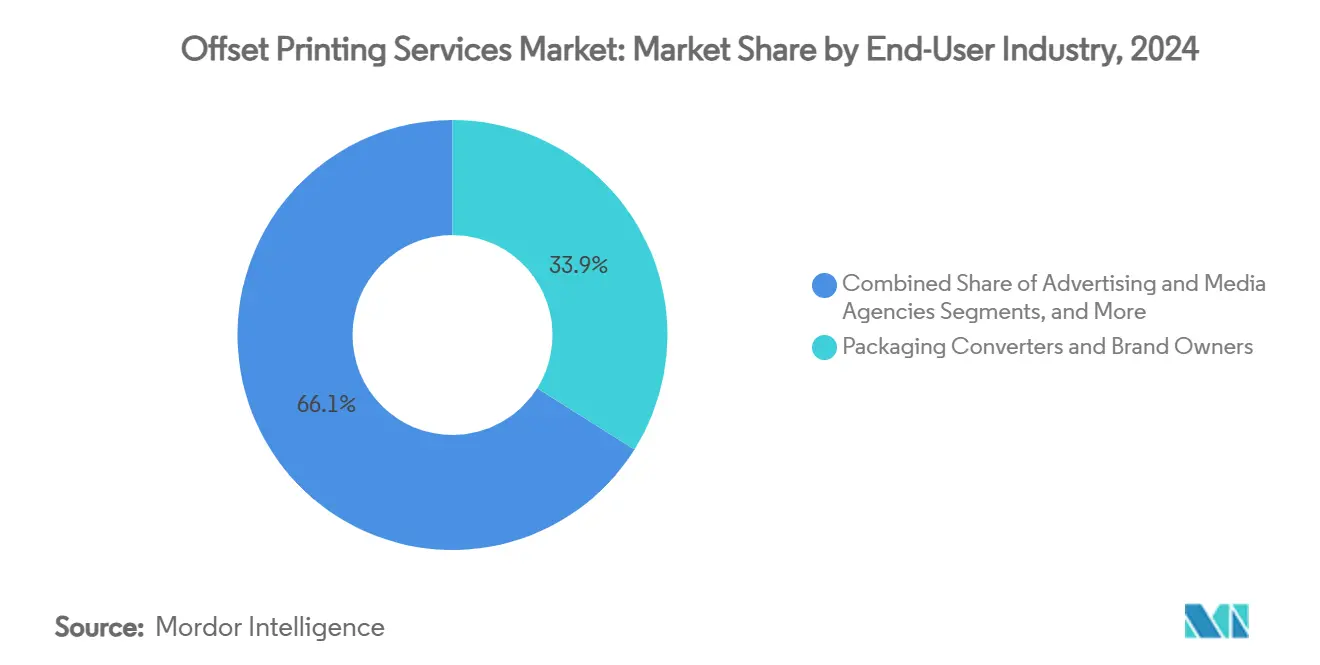

- By end-user industry, Packaging Converters and Brand Owners captured 33.94% share of the offset printing services market in 2024.

- By service stage, Printing/Press captured 63.38% share of the offset printing services market in 2024.

- By geography, offset printing services market for Middle East and Africa region is projeted to grow at a 3.31% between 2025-2030.

Global Offset Printing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Resurgence of direct-mail marketing amid digital fatigue | 0.5% | North America and EU, spill-over to APAC | Medium term (2-4 years) |

| Growth in short-run packaging and labels for e-commerce brands | 0.3% | Global, concentrated in APAC and North America | Short term (≤ 2 years) |

| Developing-world newspaper and textbook demand | 0.2% | APAC core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Cost-effective high-quality print for on-demand books | 0.2% | Global, early gains in North America and EU | Medium term (2-4 years) |

| OEM retrofits enabling carbon-neutral offset presses | 0.1% | EU and North America, expanding to APAC | Long term (≥ 4 years) |

| Corporate net-zero mandates favoring vegetable-oil inks | 0.1% | Global, led by EU regulatory framework | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Resurgence of Direct-Mail Marketing Amid Digital Fatigue

Brands facing online ad saturation increasingly turn to physical mailers that deliver stronger recall and engagement. The U.S. Postal Service extended growth incentives for Marketing Mail into 2025, lowering rate pressure for high-volume campaigns.[1]U.S. Postal Service, “Final Rule – Domestic Mailing Services,” usps.comOffset presses excel in color accuracy and substrate flexibility, giving mail houses the tactile edge now prized by premium consumer segments. Hybrid print-mobile formats such as QR-activated catalogs amplify response tracking while preserving the sensory appeal of paper. Printers able to align postal optimization with lean press setups win share as marketers demand both cost discipline and impact.

Growth in Short-Run Packaging and Labels for E-Commerce Brands

Online retailers pursuing memorable unboxing experiences favor high-quality litho-laminated cartons and sleeve labels produced in runs of a few thousand. Heidelberger Druckmaschinen notes that paper-based packaging demand has climbed more than 60% since 2014, with its digital-print-ready press portfolio expected to swell to EUR 7.5 billion by 2029.[2]Heidelberger Druckmaschinen AG, “China Print 2025 Press Release,” heidelberg.com Offset delivers the premium coating and embossing options that fast-moving consumer goods owners use to signal sustainability credentials and justify price premiums. Variable data capabilities extend personalization without sacrificing the crisp halftone reproduction that distinguishes lithography from inkjet alternatives.

Developing-World Newspaper and Textbook Demand

Textbook procurement programs remain critical in emerging economies where digital devices and bandwidth are still scarce. The World Bank stresses that print textbooks continue to deliver the highest learning gains per dollar in low-resource settings. Governments in Asia-Pacific and parts of Africa secure domestic printers through local-content policies, insulating offset volumes from Western market declines. Regional newspapers also sustain coldset runs as daily readership habits endure in rural communities with limited online access.

Cost-Effective High-Quality Print for On-Demand Books

As physical books regain favor among readers fatigued by screens, publishers are re-evaluating inventory-light models. Offset becomes the cost winner beyond roughly 500 copies, offering durable bindings and rich blacks valued by authors and art houses alike. Workflow software now links digital order intake directly to automated plate imaging, cutting makeready waste, and aligning offset economics with print-on-demand timelines. Specialty papers, foil stamping, and lay-flat formats reinforce the premium aura that digital toner presses struggle to match.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift of ad spend to digital channels | -0.4% | Global, most pronounced in North America and EU | Short term (≤ 2 years) |

| Accelerating adoption of production inkjet presses | -0.2% | Global, led by North America and EU | Medium term (2-4 years) |

| Postal-rate inflation eroding catalogue economics | -0.1% | North America primarily, spreading to other regions | Short term (≤ 2 years) |

| Volatility in aluminium plate supply | -0.1% | Global, supply chain concentrated in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift of Ad Spend to Digital Channels

Advertisers continue reallocating budgets toward data-rich online platforms, shrinking demand for catalogs and magazines. Donnelley Financial reports that software now contributes 34% of total revenue as it pivots from traditional print workflows.[3]Donnelley Financial Solutions, “Form 10-K 2024,” dfinsolutions.comWhile luxury and nonprofit segments still champion direct mail, the broader mix shift compresses litho volumes and places a premium on measurable return. Printers combat the squeeze by bundling analytics dashboards with print campaigns and emphasizing print’s higher dwell time among affluent cohorts.

Accelerating Adoption of Production Inkjet Presses

Continuous-feed inkjet lines break steadily into mid-run territory once dominated by offset. Partnerships such as Heidelberg-Canon accelerate crossover speeds, and cost curves keep falling. Although offset retains an edge in dense solids, metallic inks, and textured substrates, buyers now evaluate hybrid fleets that pair inkjet flexibility with offset finishing. Service providers must justify new plate investments through superior uptime, color consistency, and carbon reporting to fend off inkjet encroachment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Printing Process: Sheetfed Offset Dominance Amid Sustainability Shift

Sheetfed Offset generated 56.73% of 2024 revenue, illustrating how its adaptability meets commercial printing, folding carton, and rigid box applications. Efficiency gains in plate imaging and ink metering have trimmed makeready waste, sustaining profitability even as run lengths shorten. The offset printing services market size for sheetfed presses is forecast to expand modestly as converters chase premium print effects that justify higher average selling prices. Waterless and UV offset systems, grouped under the Others category, are pacing ahead with a 2.89% CAGR thanks to mineral-oil ink restrictions and VOC thresholds enacted across the EU.[4]European Printing Ink Association, “Mineral Oil Regulation Update 2025,” eupia.org Their chemistry-free plates slash energy use and enable thinner substrates, aligning with corporate ESG scorecards. Consequently, demand for retrofits that convert legacy sheetfed lines into LED-UV configurations is rising among mid-tier printers seeking differentiation without new-build capex.

Heatset and coldset web offset formats face volume attrition in magazine and newspaper niches, yet they remain irreplaceable for high-pagination, light-weight paper products. Publishers optimize plant footprints by deploying modular presses that toggle between heatset and coldset modes, eking productivity gains from mature assets. Coldset installations in particular hold up in South Asian markets where daily circulation remains culturally entrenched, preserving a predictable if subdued revenue stream for press vendors and plate suppliers.

By Application: Books Leadership Challenged by Packaging Growth

Books accounted for 36.47% of 2024 revenue as academic publishers replenished stockpiles to meet in-person teaching rebounds. The offset printing services market size attributable to books is projected to advance steadily, underpinned by government textbook tenders in India, Indonesia, and Nigeria. Yet the fastest expansion lies in Packaging and Labels, on course for a 3.04% CAGR through 2030. Folding cartons, sleeve labels, and litho-laminated corrugate capitalize on e-commerce’s need for protective and brand-rich outer layers, driving incremental plate volumes.

Magazines and newspapers remain in structural decline across advanced economies but pivot toward collectible editions and niche titles with higher cover prices. Marketing collateral shows mixed fortunes: direct mail rides a renaissance, whereas tri-fold brochures give way to QR-linked microsites. Security and transactional print stays resilient because governments and banks still require anti-counterfeit features, micro-text, and magnetic inks best achieved on offset lines.

By End-User Industry: Packaging Converters Lead Amid E-Commerce Surge

Packaging Converters and Brand Owners contributed 33.94% of the 2024 turnover, leveraging offset to deliver vivid graphics on recycled boards and bio-based liners. Their fortunes track closely with fast-moving consumer goods spending and private-label rollouts in grocery chains. Retail and E-commerce form the growth hotspot at a 3.13% CAGR as direct-to-consumer brands commission shorter, design-driven print runs to stand out on social feeds.

Publishing Houses continue to procure offset for first-edition hardbacks and academic journals where the margin per unit supports higher finishing costs. Advertising and Media Agencies now package multichannel campaigns that knit variable-data mailers with geotargeted digital ads, demanding cross-platform color matching. Educational Institutions underpin stable textbook offtake, their budgets tied to public funding cycles, and literacy drives supported by philanthropic programs.

By Service Stage: Press Operations Dominance with Logistics Growth

Printing/Press Operations occupied 63.38% of 2024 revenue, the heart of capital-intensive lithographic activity. Plate imaging automation and predictive maintenance analytics trimmed downtime, reinforcing offset’s cost leadership over long and mid-length runs. Logistics and Fulfilment, though smaller today, is projected to rise 3.26% annually as customers prefer single-vendor solutions that handle print, pick-pack, and last-mile delivery.

Pre-Press workflows integrate cloud-based proofing tools that reduce client approval cycles from days to hours, while Post-Press/Finishing upgrades die-cutting, spot UV, and foil create tactile differentiation that digital competitors struggle to emulate. High-performing firms leverage data from all three stages to benchmark spoilage and energy intensity, winning procurement scorecards that rank sustainability alongside total cost of ownership.

Geography Analysis

Asia-Pacific held 38.52% of global revenue in 2024, reflecting entrenched manufacturing bases in China, India, and Vietnam, where labor skill and raw material proximity combine for favorable unit economics. Government campaigns to raise literacy rates translate into sustained textbook print demand, while export-oriented packaging converters deliver premium folding cartons for global electronics and cosmetics brands. Significantly, the offset printing services market share in the region benefits from integrated paper-mill-to-print-shop clusters that compress lead times and shave logistics overhead.

Europe and North America remain technologically advanced, channeling capital into LED-UV retrofits, alcohol-free dampening systems, and carbon accounting platforms. Although overall tonnage declines, print runs for direct mail and specialty catalogs stabilize as retailers use high-quality imagery to complement online merchandising. Strict chemical regulations, such as France’s mineral-oil ban effective January 2025, accelerate the adoption of vegetable-oil and waterless inks, prompting service providers to certify supply chains under ISO 22067 sustainability standards.

The Middle East and Africa posts the fastest CAGR at 3.31% through 2030, buoyed by diversification programs in the Gulf and rising consumer packaged goods penetration across sub-Saharan Africa. New free-zone industrial parks in Saudi Arabia and the UAE attract press installations that serve regional food and pharma brands seeking shorter supply chains. Print shops in Kenya and Nigeria expand coldset capacity for election ballots and community newspapers, sectors where digital migration lags due to infrastructure gaps. Latin America delivers moderate expansion tied to retail recovery and educational spending, with Mexico and Brazil upgrading to hybrid offset-digital lines for bilingual packaging.

Competitive Landscape

Moderate concentration characterizes the offset printing services market. Heidelberger Druckmaschinen, Komori, and Manroland dominate press manufacturing, but the service layer comprises thousands of regional printers with sub-USD 50 million revenue. Heidelberg’s 41% share of installed sheetfed presses gives it a strategic foothold in aftermarket consumables and predictive maintenance contracts. TC Transcontinental exemplifies vertical integration, combining retail marketing, print, flexible packaging, and book manufacturing to secure stable earnings streams.[5]TC Transcontinental, “Q2 2025 Results,” tc.tc

Strategic moves in 2024–2025 include Heidelberg’s commitment to generate EUR 300 million in new packaging-related sales by 2029 and Sakata Inx’s rollout of bio-based Botanical Ink aimed at VOC-sensitive markets. Komori invests in anti-counterfeit press modules for banknote and passport issuance, reinforcing a high-margin niche shielded from digital disruption. On the buyer side, multinational CPG firms issue carbon-neutral procurement mandates that favor printers offering cradle-to-gate emissions reporting. Supply chain volatility, especially a 19% year-over-year rise in aluminum plate prices reported by the U.S. Geological Survey, pressures input costs and accelerates plate recycling initiatives.

M&A remains selective: regional printers acquire logistics startups to build omnichannel fulfilment, while equipment vendors pursue software firms to bundle color management and MIS platforms with hardware. The competitive rubric now rewards lean inventory, sustainable chemistry, and data-rich job tracking over raw press capacity. Niche specialists—security printing, pharmaceutical leaflets, high-touch art books—maintain pricing power by offering capabilities that rivals cannot replicate without large capital outlays.

Offset Printing Services Industry Leaders

R.R. Donnelley & Sons Company

Toppan Holdings Inc.

Dai Nippon Printing Co. Ltd.

Cimpress plc

Quad Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Heidelberger Druckmaschinen AG outlined a growth plan targeting over EUR 300 million in additional sales by 2028/2029, driven by packaging and digital press expansion.

- August 2024: Sakata Inx released its Integrated Report 2024, prioritizing eco-friendly Botanical Ink and aiming for 180 billion yen operating profit by 2026.

- July 2024: The U.S. Postal Service instituted revised mailing standards and marketing mail incentives effective July 2024, supporting print-driven campaigns.

- June 2024: Nippon Paper Industries unveiled its Medium-Term Business Plan 2025, committing to a 54% GHG emission cut by 2030 versus FY 2013.

- May 2024: Stellantis detailed a net-zero carbon pledge by 2038 and projected EUR 300 billion in 2030 net revenues, signaling stricter supplier sustainability criteria.

- February 2024: Cascades Inc. posted USD 4,638 million in 2023 sales, 48% EBITDA growth, and noted that recycled fibers power 85% of capacity.

Global Offset Printing Services Market Report Scope

| Sheetfed Offset |

| Web Offset-Heatset |

| Web Offset-Coldset |

| Others (Waterless, UV) |

| Books |

| Magazines and Newspapers |

| Marketing Collateral (Brochures, Catalogues, Direct Mail) |

| Packaging and Labels |

| Others (Security, Transactional) |

| Publishing Houses |

| Advertising and Media Agencies |

| Packaging Converters and Brand Owners |

| Retail and E-commerce |

| Education Institutions |

| Pre-Press |

| Printing/Press |

| Post-Press/Finishing |

| Logistics and Fulfilment |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Printing Process | Sheetfed Offset | ||

| Web Offset-Heatset | |||

| Web Offset-Coldset | |||

| Others (Waterless, UV) | |||

| By Application | Books | ||

| Magazines and Newspapers | |||

| Marketing Collateral (Brochures, Catalogues, Direct Mail) | |||

| Packaging and Labels | |||

| Others (Security, Transactional) | |||

| By End-user Industry | Publishing Houses | ||

| Advertising and Media Agencies | |||

| Packaging Converters and Brand Owners | |||

| Retail and E-commerce | |||

| Education Institutions | |||

| By Service Stage | Pre-Press | ||

| Printing/Press | |||

| Post-Press/Finishing | |||

| Logistics and Fulfilment | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the offset printing services market?

The offset printing services market size is valued at USD 309.73 billion in 2025.

How fast is the offset printing services market expected to grow?

Revenue is projected to reach USD 339.16 billion by 2030, registering a 1.83% CAGR.

Which printing process holds the largest market share?

Sheetfed Offset led with 56.73% of revenue in 2024, ahead of web offset and other specialized processes.

Which application segment is growing the fastest?

Packaging and Labels is forecast to expand at a 3.04% CAGR through 2030 due to e-commerce and sustainability trends.

Which region will witness the quickest growth?

The Middle East and Africa is expected to post the highest regional CAGR at 3.31% over the forecast period.

What sustainability measures are influencing the industry?

Adoption of vegetable-oil inks, LED-UV curing and carbon-neutral press retrofits are key initiatives driven by corporate net-zero mandates and new EU chemical regulations.

Page last updated on: