Almond Ingredients Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

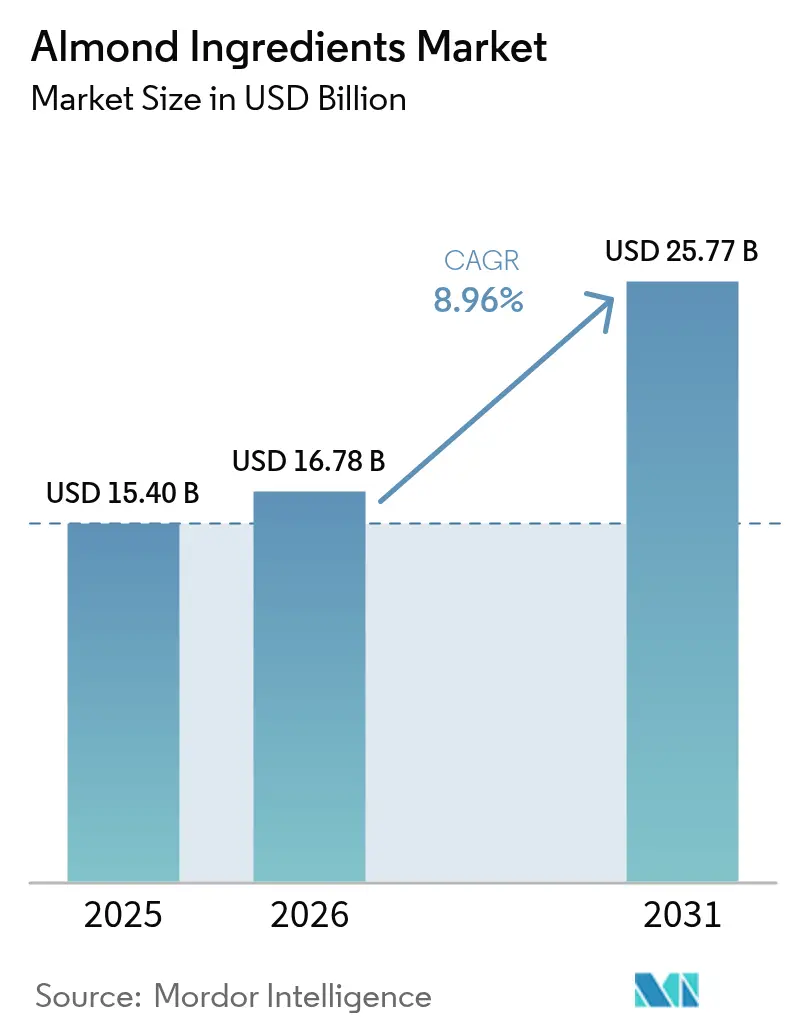

| Market Size (2026) | USD 16.78 Billion |

| Market Size (2031) | USD 25.77 Billion |

| Growth Rate (2026 - 2031) | 8.96% CAGR |

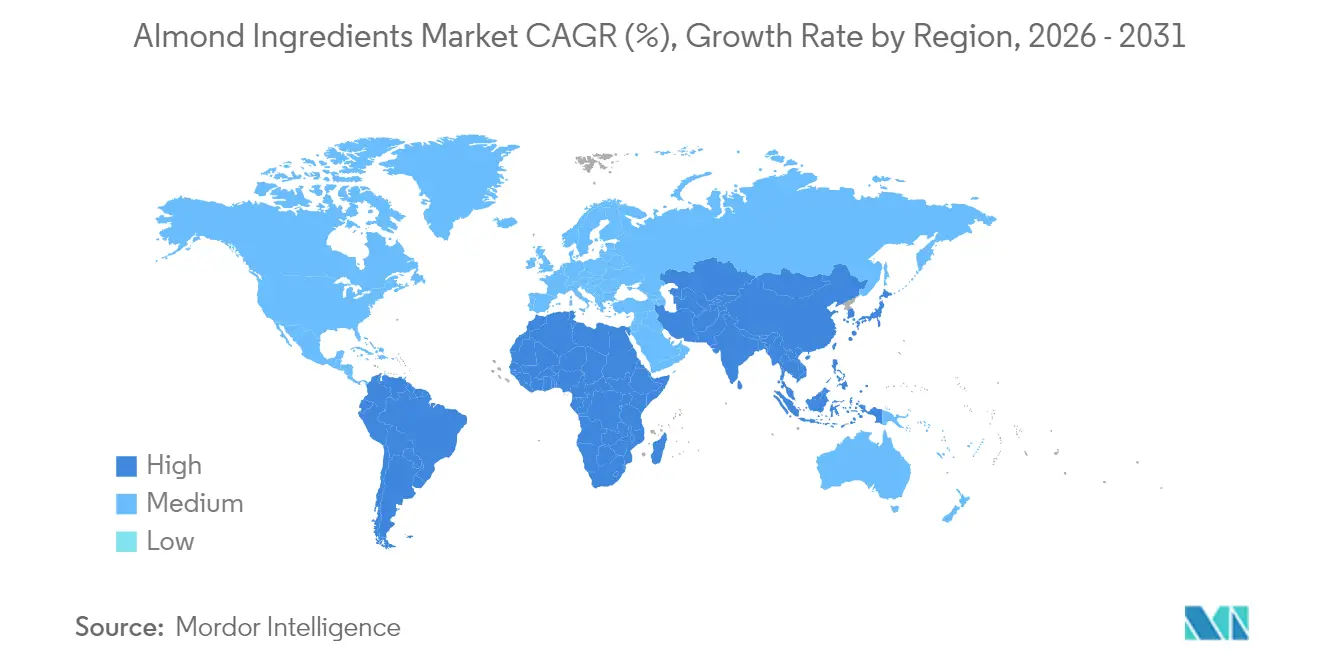

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

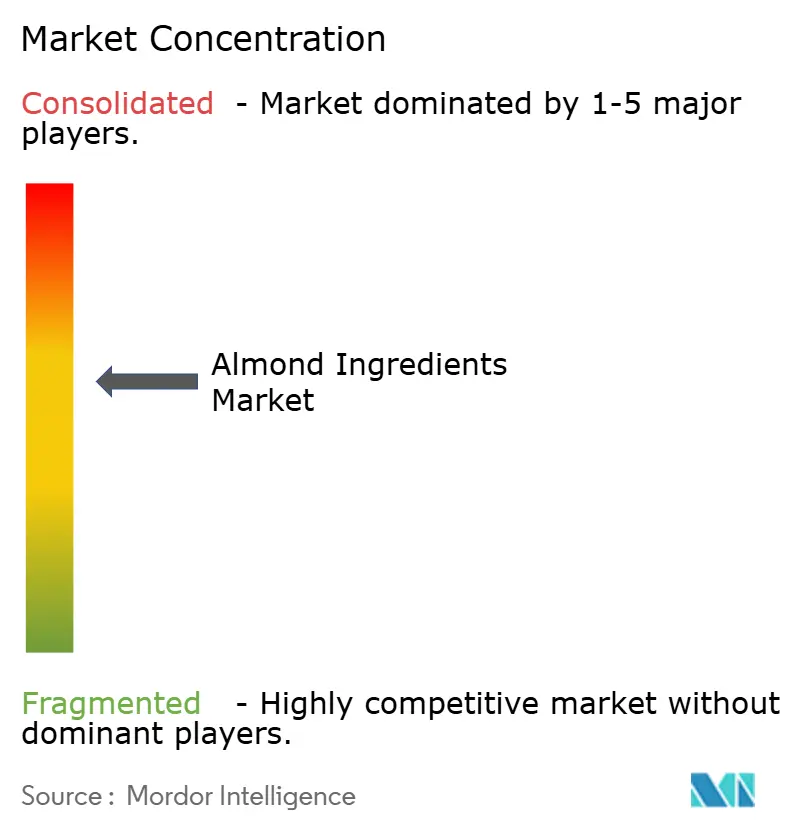

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Almond Ingredients Market Analysis by Mordor Intelligence

The almond ingredients market size in 2026 is estimated at USD 16.78 billion, growing from 2025 value of USD 15.4 billion with 2031 projections showing USD 25.77 billion, growing at 8.96% CAGR over 2026-2031. This growth underscores the almond's evolution from a mere commodity to a versatile ingredient, catering to the surging demand for plant-based products, premium snacking, and clean-label formulations. Technological advancements in extraction, irrigation, and by-product valorization are not only driving down unit costs but also paving the way for novel applications, particularly in cosmetics and functional foods. Additionally, as almond protein offers a mild taste, good solubility, and compatibility with diverse applications like protein bars, dairy alternatives (e.g., almond milk yogurt), shakes, and even bakery products, manufacturers are focused on considering almond ingredients to innovate their products. In the nutraceutical space, it adds muscle-supporting amino acids and is perceived as more “natural” than isolates from pea or rice. In line with this, manufacturers are also innovating almond ingredients with multiple application capabilities, driving the market's growth. For instance, in late 2024, Almonesia expanded beyond nuts and launched instant almond milk powder for both beverages and baking, with further plans to introduce almond-based jams and nut milks under its John Farmer label, leveraging almonds as versatile, natural bases.

Key Report Takeaways

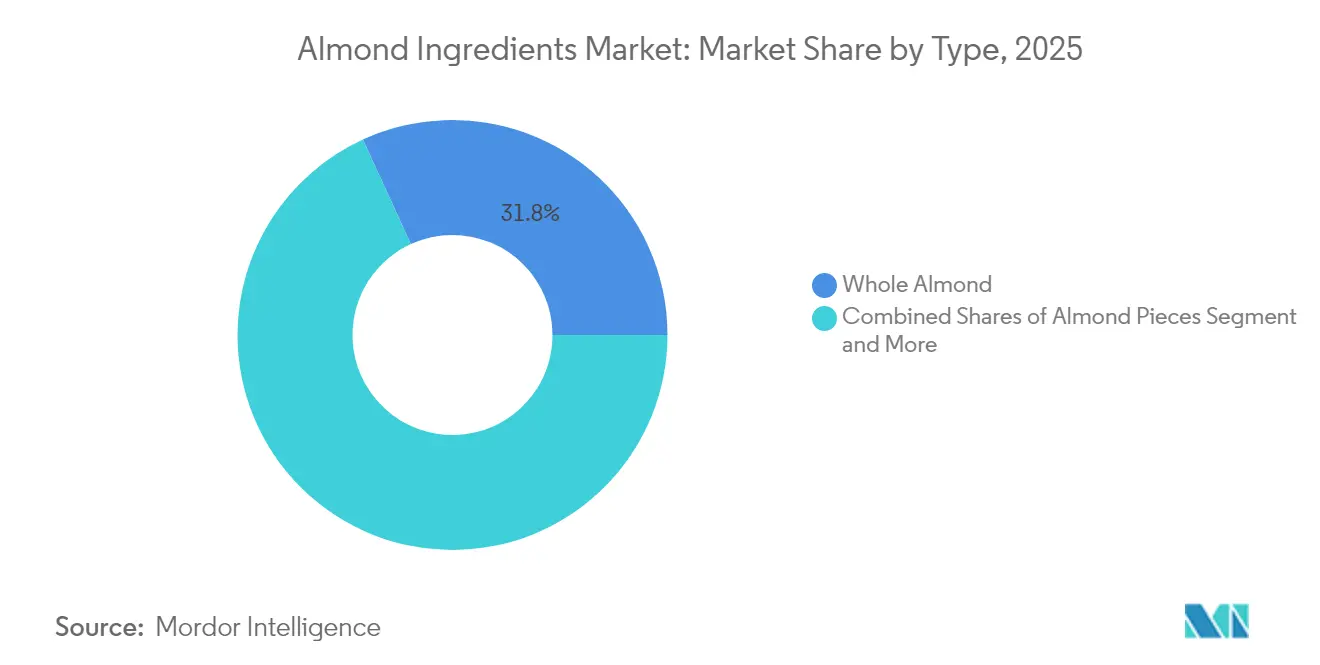

- By product type, Whole Almonds led with 31.84% of Almond market share in 2025, while Almond Oil recorded the fastest 10.78% CAGR forecast through 2031.

- By application, Food and Beverage commanded 70.12% revenue in 2025; Personal Care and Cosmetics is projected to expand at a 10.12% CAGR to 2031.

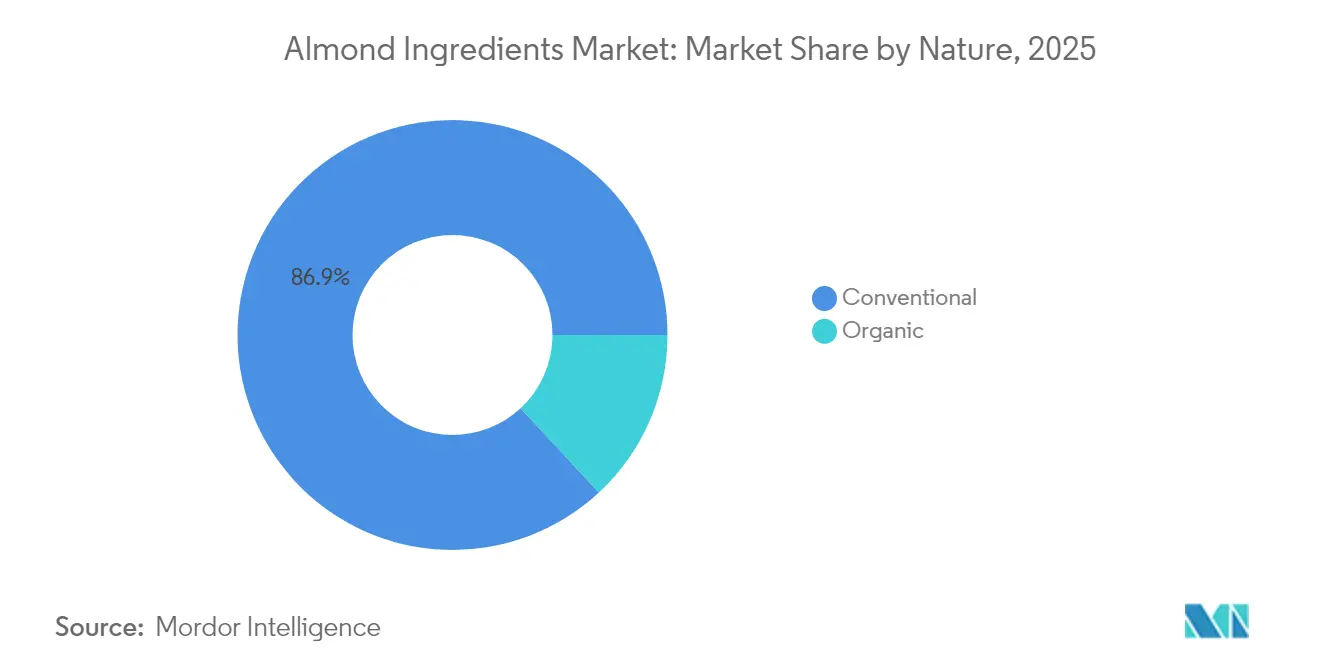

- By nature, Conventional products held 86.92% of the Almond market size in 2025, whereas Organic variants are set to grow at 9.95% CAGR between 2026 and 2031.

- By geography, Europe captured 34.12% revenue share in 2025; Asia-Pacific is the fastest region with a 10.41% CAGR expected through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Almond Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for plant-based food | +2.1% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Growth of convenient, on-the-go healthy snacking | +1.8% | Global, led by Asia-Pacific urban centers | Short term (≤ 2 years) |

| Growing consumer preference for clean label and gluten-free ingredients | +1.5% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Expansion of lactose-free and vegan dairy alternatives | +1.9% | Global, strongest in developed markets | Short term (≤ 2 years) |

| Increasing use in fortified and functional food products | +1.2% | North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Innovations in food processing and applications | +0.8% | Global, technology-driven markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for plant-based food

Almond protein’s complete amino-acid profile and neutral taste allow high inclusion levels in dairy substitutes, meat analogs, and protein bars, and partially defatted almond flour is now approved for up to 80% use in nutritional formulations, according to the FDA. Manufacturers are emphasizing their clean-label positioning and achieving better sensory scores when compared to soy and pea proteins. For example, Anthony markets an almond protein powder, touting it as being crafted from just one ingredient: California-grown almonds. This product is gluten-free, non-GMO, vegan, and devoid of fillers, artificial flavors, or additives. In a similar vein, Blue Diamond Growers, alongside other processors, is ramping up new protein extraction lines, fueling double-digit growth in plant-based categories. This surge in demand has led to heightened procurement activities, prompting orchard expansions beyond U.S. borders to ensure a diversified supply.

Growth of convenient, on-the-go healthy snacking

Urban consumers are increasingly favoring portable, nutrient-dense snacks, leading to a surge in the popularity of value-added almond products like energy bites, protein clusters, and spice-coated kernels. This trend is underscored by rising almond consumption. Data from the US Department of Agriculture reveals that in 2023/2024, per capita almond consumption in the U.S. reached nearly 2.3 pounds, marking the highest level in a decade[1]US Department of Agriculture," Per capita almond consumption in the United States", www.ers.usda.gov. Additionally, processors are reaping benefits from broader premium price ranges and heightened retailer acceptance of single-serve packs, especially those that prominently highlight health benefits, fueling the market's expansion. In line with this growing demand for almond-based foods and snacks, players are focused on expanding their almond ingredient lines to cater to the growing demand. For instance, in 2025, Almendras de Andalucía showcased a defatted almond powder, which is a high-protein ingredient suitable for fortified foods and health products.

Growing consumer preference for clean label and gluten-free ingredients

Almond flour, a gluten-free alternative, is increasingly replacing wheat flour in bakery and confectionery products, boosting protein content without the need for artificial stabilizers. While mandatory allergen disclosures for tree nuts enhance transparency, they also position almonds as a favored natural ingredient among health-conscious consumers. The rising demand for clean-label, organic, and natural foods is opening doors for manufacturers to introduce products boasting such claims. For example, data from the Bundesanstalt für Landwirtschaft und Ernährung (BMEL) indicates that by June 2024, 7,125 companies were active in producing or selling organic-labeled products in Germany[2]Bundesanstalt für Landwirtschaft und Ernährung," Development of product advertisements for the use of the organic seal, www.oekolandbau.de. Furthermore, formulators are turning to almond-based binders and emulsifiers to eliminate synthetic additives and streamline ingredient lists. A case in point: in 2024, Elmhurst utilized its HydroRelease method to cold-mill whole almonds, creating a non-dairy “milk” devoid of gums, stabilizers, or synthetic emulsifiers, and instead, relying on almond proteins and fibers for emulsion and texture.

Innovations in food processing and applications

Advanced techniques, including cold-press milling, protein fractionation, and hydrolysis, are transforming almonds into natural emulsifiers, binders, and texturizers. This shift allows formulators to move away from synthetic additives like gums, starches, and mono- and diglycerides. As a result, almonds now offer enhanced emulsification, moisture retention, and oxidative stability for diverse applications, spanning from plant-based milks and bakery fillings to dressings and snacks. Furthermore, investments in AI-driven shelling lines and facilities that convert by-products into energy not only reduce waste and carbon footprints but also align with retailer sustainability goals. Ongoing advancements in flavor encapsulation are broadening almond applications in ready-to-drink beverages and shelf-stable sauces, fueling market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of lower-priced nut and seed substitutes | -1.1% | Global, most severe in price-sensitive emerging markets | Medium term (2-4 years) |

| High price volatility of raw almonds | -1.4% | Global, most severe in price-sensitive markets | Short term (≤ 2 years) |

| Allergen concerns regarding almonds | -0.9% | Global, strictest in developed markets | Medium term (2-4 years) |

| Water-intensive cultivation | -0.7% | California, Mediterranean regions, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Availability of lower-priced nut and seed substitutes

Lower-priced substitutes like peanuts, sunflower seeds, and soy nuts are significantly restraining the almond ingredients market. These alternatives provide cost-sensitive food manufacturers and consumers with affordable options that don't drastically compromise on nutritional value or functionality. Often, these substitutes come with reduced raw material costs and exhibit less price volatility. This makes them particularly appealing for large-scale food production, especially in emerging markets with heightened price sensitivity. For example, StatCan reported that in August 2024, the average retail price for peanut butter in Canada was CAD 5.97 per kilogram, down from CAD 6.09 the previous year. Furthermore, some of these substitutes can replicate the texture and binding properties of almonds in specific applications. This allows formulators to uphold product quality while being mindful of ingredient budgets. Such competitive pressures are curtailing the growth of the almond ingredient market.

High price volatility of raw almonds

Weather conditions, particularly droughts in key regions like California, along with fluctuating water availability, trade policies, and global supply-demand imbalances, heavily influence almond prices. These unpredictable swings in costs challenge food manufacturers in budgeting and maintaining consistent pricing for almond-based products. As a result, many manufacturers either reformulate with more stable alternatives or significantly reduce their almond usage. For instance, the Australian Almonds Organization reported a production drop in 2023, with Australia yielding 110.71 thousand metric tons of almonds, down from 140.96 thousand metric tons the previous year. Additionally, rising input costs are squeezing margins for both producers and processors of almond ingredients. This financial pressure could stifle innovation and expansion within the category. Such volatility not only hampers long-term strategic planning for brands but also jeopardizes supply chain stability, ultimately stunting broader market growth and adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Whole Almonds hold scale while oil captures growth

In 2025, Whole Almonds captured a 31.84% share of the almond market, buoyed by their popularity in traditional snacking and as inclusions in baked goods. Meanwhile, Almond Oil emerged as the fastest-growing product, boasting an impressive 10.78% CAGR projected through 2031. This surge is largely attributed to beauty formulators' increasing preference for plant-based emollients, especially those rich in vitamin E and phytosterols. Innovations in roasting and flavoring not only enhance the sensory appeal of almonds but also extend their shelf life, justifying premium price points. In the Asia-Pacific region, rising disposable incomes are driving volume expansion, while European markets are honing in on provenance cues and crafting lower-salt recipes to align with public health objectives. Manufacturers are channeling investments into refining roasting techniques and adopting vacuum-filled packaging, ensuring that crunch and flavor integrity are preserved throughout extended distribution chains. A case in point: Treehouse California Almonds provides bulk offerings of natural, blanched, and roasted whole almonds, available in vacuum-packed 50 lb boxes and 25 lb options—catering perfectly to food manufacturers prioritizing longevity and consistent quality.

Utilizing aqueous extraction lines, producers are minimizing solvent residues, paving the way for cosmetic-grade certifications. These certifications can command prices 3-4 times higher than their edible oil counterparts. The culinary world is also embracing almond oil, drawn by its stable smoke-point and the growing consumer inclination towards premium, mono-unsaturated fats. Almond derivatives like Pieces, Flour, Milk, Paste, and Extract are carving out niche yet lucrative markets. These segments find their sweet spot at the intersection of gluten-free baking, dairy alternatives, and natural flavoring. Each sub-segment capitalizes on almonds' nutritional reputation, fine-tuning aspects like particle size, fat content, and flavor intensity to cater to specific end-use requirements.

By Application: Food and Beverage dominate as beauty surges

In 2025, the Food and Beverage sector dominated revenues, accounting for 70.12%. Key drivers included bakery inclusions, dairy substitutes, confectionery centers, and premium snack mixes. Meanwhile, the Personal Care and Cosmetics sector is projected to grow at a robust 10.12% CAGR. Almonds, celebrated for their natural richness in protein, fiber, healthy fats, and especially vitamin E, have become a go-to choice for health-conscious consumers. Their adaptability means almond derivatives—like almond flour, milk, butter, and protein powder—find applications in dairy alternatives, baked goods, snacks, and nutritional supplements. This versatility is a significant driver of their growth. Moreover, the surging popularity of gluten-free, keto, vegan, and paleo diets has amplified the demand for almond-based products, as they seamlessly cater to diverse dietary preferences while delivering exceptional taste and texture. Manufacturers are also reaping the benefits of almond ingredients' functional attributes—emulsification, binding, and moisture retention—which enhance product quality without resorting to synthetic additives, bolstering the segment’s expansion.

Formulators in the Personal Care and Cosmetics sector appreciate almond ingredients for their subtle scent, quick skin absorption, and vitamin E richness. These attributes make them prime candidates for anti-aging and baby-care product lines. The segment is further buoyed by the rising clean-beauty movement, which prioritizes traceable, plant-based ingredients over traditional mineral oils and silicones. Highlighting the sector's vitality, U.S. health and personal care store sales reached approximately USD 444.94 billion in 2024, a notable increase from the prior year's USD 435.71 billion, as reported by the US Census Bureau. Additionally, there's a burgeoning trend in functional beverages, sports supplements, and nutraceutical gummies, where almond protein isolates and fiber fractions are adeptly meeting both texture and nutritional goals.

By Nature: Conventional scale meets organic premium

In 2025, conventional almond varieties dominated the almond market, accounting for 86.92% of the market size. This dominance is attributed to established supply chains and competitive pricing in mainstream channels. Meanwhile, organic almonds are on an upward trajectory, projected to grow at a 9.95% CAGR until 2031. This surge is driven by consumers' preference for pesticide-free production, often willing to pay a premium of 40-60% over their conventional counterparts. In the food sector, products derived from conventional almonds, such as almond flour, milk, butter, and protein, are gaining traction. These nutrient-rich, plant-based alternatives not only bolster clean-label, gluten-free, and vegan claims but also enhance taste, texture, and shelf stability. As a result, they're becoming staples in snacks, baked goods, and dairy alternatives, fueling the segment's expansion.

Organic almonds, cultivated without synthetic pesticides, fertilizers, or GMOs, resonate with the global shift towards health-conscious and eco-friendly choices. In the food and beverage realm, organic variants of almond flour, milk, butter, and protein are increasingly featured in products emphasizing organic, vegan, gluten-free, and non-GMO labels. These labels are becoming pivotal in shaping consumer purchasing choices. Highlighting this trend, data from Bund Ökologische Lebensmittelwirtschaft (BÖLW) reveals that organic food revenues in Germany neared EUR 17 billion in 2024. Furthermore, these organic ingredients not only bolster clean-label formulations but are also viewed as safer and more premium, further propelling the segment's growth.

Geography Analysis

In 2025, Europe commanded the almond market, accounting for 34.12% of the revenue. This dominance is bolstered by the continent's established consumption habits, Mediterranean culinary traditions, and EU regulations that prioritize clean-label and organic products. European consumers, known for their health-conscious choices, are gravitating towards plant-based, clean-label, organic, and functional foods. This trend dovetails seamlessly with products derived from almonds, including almond milk, flour, butter, and protein. Furthermore, Europe's growing almond production capacity is fueling the market's expansion, reducing the region's dependence on imports. For instance, the USDA Foreign Agricultural Service reported that in 2023-24, Europe emerged as the second-largest almond producer, churning out approximately 147.7 thousand metric tons.

Asia-Pacific is on a rapid ascent, boasting a 10.41% CAGR projected through 2031, largely propelled by China's nut intake, which has seen a twofold increase. Nations such as China, India, Japan, South Korea, and Australia are showing a heightened appetite for nutritious, premium, and functional foods. This shift has catalyzed the integration of almond-based ingredients across various sectors, from plant-based beverages and snacks to bakery items and dairy alternatives. Additionally, the region's burgeoning cosmetics and personal care sectors are tapping into almond oil and extracts, lauding their moisturizing and anti-aging benefits, thus amplifying the demand across multiple industries.

North America, with California at its helm, stands as a powerhouse in global almond output and processing. While domestic consumption remains stable, the region's growth hinges on premiumization and innovative functionalities in products. Both Canada and Mexico are witnessing a gradual shift, with health considerations steering preferences towards unsalted and roasted-no-oil almond varieties. Despite facing challenges like rising water costs and pollination fees, which highlight the significance of initiatives such as the KIND Almond Acres Initiative, growers maintain a competitive edge in exports. Meanwhile, South America is diversifying the landscape, thanks to Chile's expanding orchards and advantageous trade agreements with China. In contrast, the Middle East and Africa markets, while presenting long-term promise, are reliant on factors like increasing disposable incomes and enhanced logistics.

Competitive Landscape

The Almond market sees moderate concentration, with major processors like Blue Diamond Growers, Olam Food Ingredients, and Royal Nut Company leading the way. By vertically integrating from orchard to branded products, these players ensure raw material availability, stabilize margins, and speed up product innovation.

Technological differentiation plays a pivotal role. Innovations like AI-assisted pollinator monitoring, variable-rate irrigation, and blockchain traceability not only reduce input costs but also guarantee buyers' ethical sourcing. On another front, OFI’s KIND Almond Acres Initiative is testing regenerative farming on 500 acres, with goals of enhancing soil health and pollinator habitats, crucial for sustained yields.

Additionally, niche players are carving out premium segments, leveraging organic certifications, single-origin narratives, and refining oils for cosmetic use, all commanding higher prices in beauty markets.

Almond Ingredients Industry Leaders

-

Blue Diamond Growers

-

John B. Sanfilippo and Son Inc.

-

Borges Agricultural & Industrial Nuts, S.A

-

Royal Nut Company

-

Barry Callebaut AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Blue Diamond Growers partnered with Kagome Co., Ltd. for all production and distribution of Almond Breeze in Japan. The new partnership is focused on accelerating market growth and driving new demand for Almond Breeze. The new partnership was asserted to harness the qualities of Almond Breeze while leveraging the in-market expertise of Kagome to drive additional consumption within Japan.

- July 2024: Sabinsa debuted Promond, a water-soluble almond protein made from Indian-grown almonds, boasting a complete amino acid profile. It is positioned for nutraceuticals and sports nutrition, with applications extending to drinks and supplements.

- February 2024: SunnyGem, a key California almond supplier, released SunnyGem Almond Oil, its first direct-to-consumer, premium food-grade almond oil, offering a high-quality ingredient for culinary, food processing, and flavor applications.

Global Almond Ingredients Market Report Scope

Almond ingredients are derived from one of the popularly consumed tree nut almonds packed with nutrients. Almonds are a good source of healthy fats, protein, fiber, vitamin E, calcium, magnesium, and other essential vitamins and minerals. They come in various forms and can be consumed raw, roasted, or salted. Beyond snacking, almonds are a versatile ingredient used in baking, preparing desserts, and even savory dishes. The almond ingredients market scope encompasses the following segments - type, application, and geography. By type, the market is further sub-segmented into whole almond, almond pieces, almond flour, almond paste, almond milk, and other types. The application segment is subdivided into bakery, dairy, confectionery, sweet and savory snacks, and other applications. The geography is also further sub-segmented into North America, Europe, Asia Pacific, South America, and Middle East and Africa. The market sizing and forecasts have been done for each segment based on value (USD).

| Whole Almond |

| Almond Pieces |

| Almond Flour |

| Almond Paste |

| Almond Milk |

| Almond Oil |

| Almond Extract |

| Other Types |

| Conventional |

| Organic |

| Food and Beverage | Bakery and Confectionery |

| Dairy and Dairy Alternatives | |

| Sweet and Savory Snacks | |

| Beverages | |

| Other Food and Beverages | |

| Personal Care and Cosmetics | |

| Dietary Supplements | |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Whole Almond | |

| Almond Pieces | ||

| Almond Flour | ||

| Almond Paste | ||

| Almond Milk | ||

| Almond Oil | ||

| Almond Extract | ||

| Other Types | ||

| By Nature | Conventional | |

| Organic | ||

| By Application | Food and Beverage | Bakery and Confectionery |

| Dairy and Dairy Alternatives | ||

| Sweet and Savory Snacks | ||

| Beverages | ||

| Other Food and Beverages | ||

| Personal Care and Cosmetics | ||

| Dietary Supplements | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Almond market size and how fast is it growing?

The Almond market size stands at USD 16.78 billion in 2026 and is projected to expand to USD 25.77 billion by 2031 at a 8.96% CAGR.

Which product segment is expanding the fastest?

Almond Oil is the quickest-growing product, forecast to post an 10.78% CAGR through 2031 thanks to rising demand in skincare and premium culinary oils.

Which application segment holds the largest share?

Food and Beverage leads with 70.12% revenue share in 2025, fueled by bakery, confectionery, and dairy-alternative uses.

Why is Asia-Pacific considered the growth engine for almonds?

The region’s 10.41% forecast CAGR is propelled by China’s doubling nut consumption, India’s lower import tariffs, and expanding e-commerce distribution networks that make almonds more accessible to urban consumers.

What are the main risks facing almond suppliers?

Price volatility tied to California’s climate, water scarcity, and allergen regulations present the key risks that can disrupt supply chains and raise compliance costs.

How are companies addressing sustainability concerns in almond production?

Leading processors invest in micro-irrigation, AI-guided pollinator health programs, and by-product-to-energy projects that reduce water use and carbon emissions while safeguarding long-term yields.

Page last updated on: