Almond Protein Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

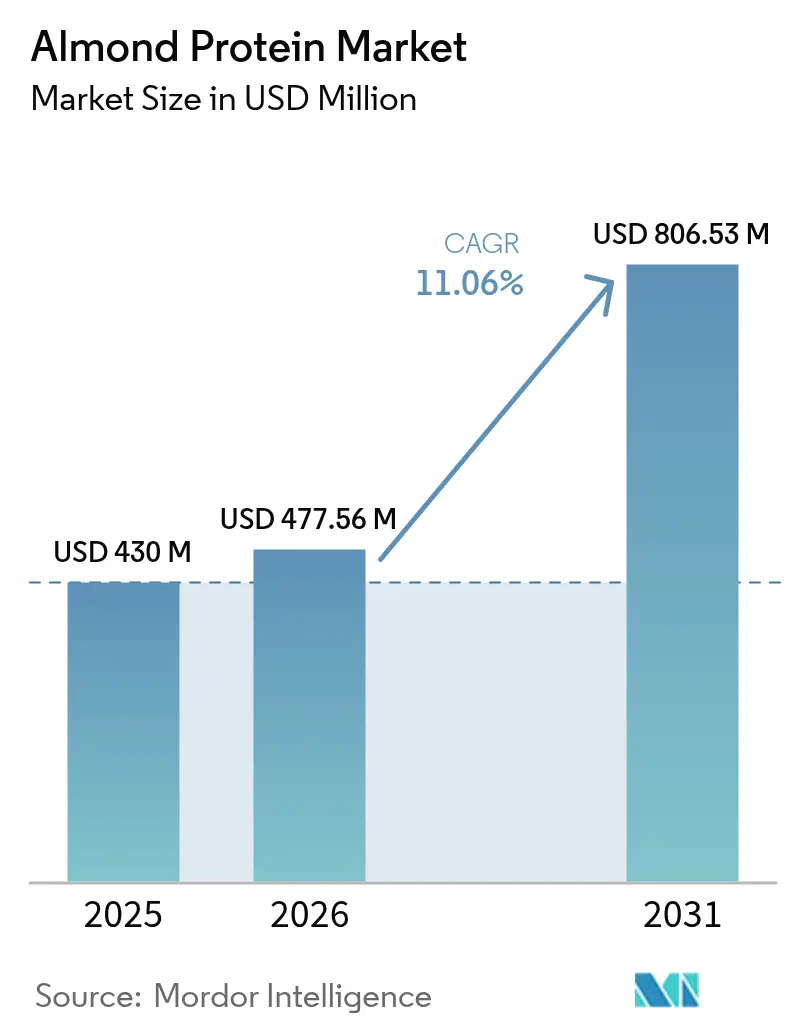

| Market Size (2026) | USD 477.56 Million |

| Market Size (2031) | USD 806.53 Million |

| Growth Rate (2026 - 2031) | 11.06% CAGR |

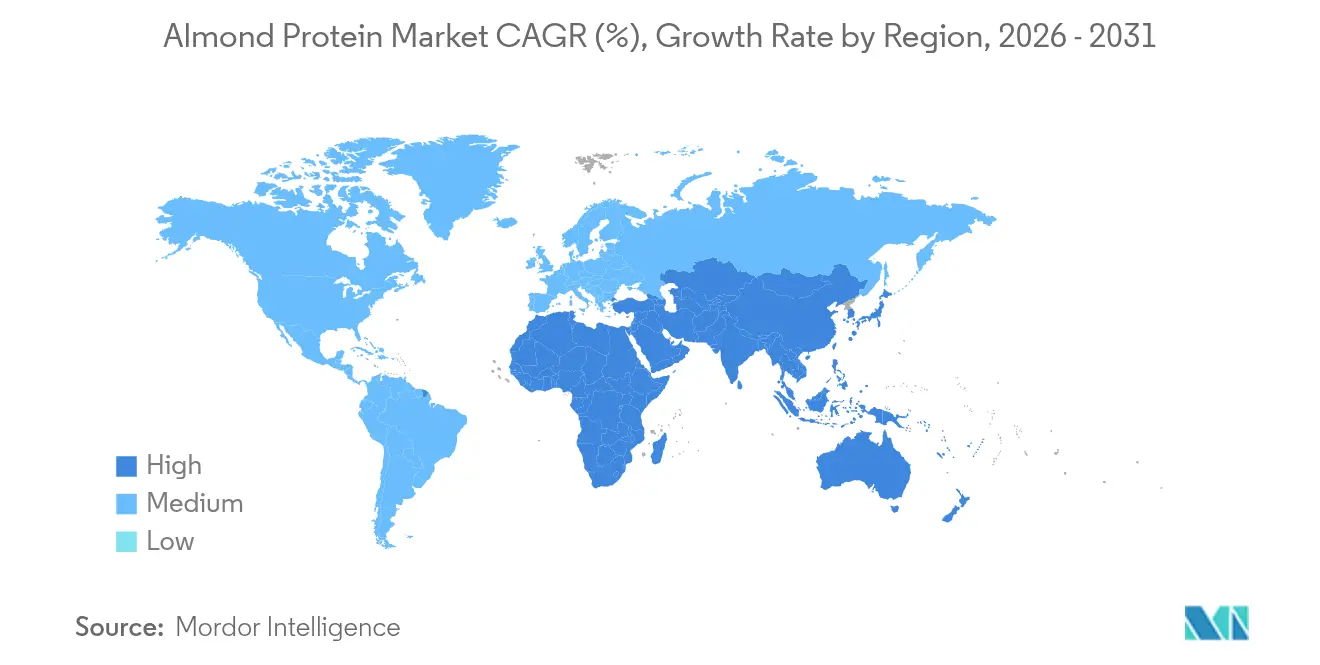

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Almond Protein Market Analysis by Mordor Intelligence

The almond protein market size was valued at USD 430 million in 2025 and estimated to grow from USD 477.56 million in 2026 to reach USD 806.53 million by 2031, at a CAGR of 11.06% during the forecast period (2026-2031). Globally, food and beverage and sports nutrition manufacturers are increasingly adopting almond protein due to health, dietary, and sustainability trends. Derived from nutrient-rich almonds, it serves as a clean-label, plant-based alternative to animal and soy proteins, meeting the demand for vegan, allergen-friendly, and minimally processed options. Its mild flavor, solubility, and versatility make it ideal for protein bars, dairy alternatives, shakes, and baked goods, driving product innovation. In the nutraceutical sector, almond protein is valued for its muscle-supporting amino acids and is seen as a natural choice compared to pea or rice isolates. Manufacturers are expanding their applications, fueling market growth. For instance, in late 2024, Almonesia entered the instant almond milk powder segment and plans to launch almond-based jams and nut milks under the John Farmer label. In sports nutrition, almond protein's high protein content, amino acids, and appealing taste make it a preferred ingredient for protein bars, shakes, and functional foods. Almonds' premium, heart-healthy image further boosts their appeal in health-focused markets. Rising demand for protein fortification across dairy alternatives, snacks, and baked goods is driving manufacturers to integrate almond protein, aligning with consumer preferences for nutrition and sustainability.

Key Report Takeaways

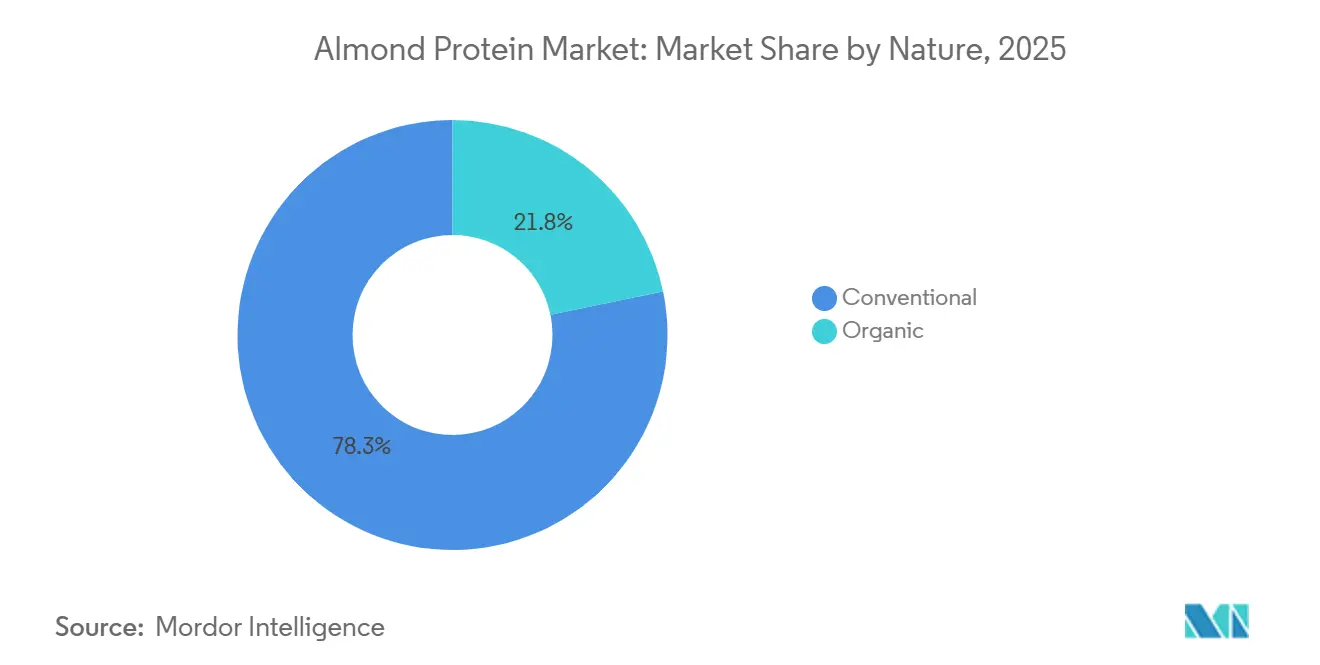

- By nature, the conventional segment held 78.25% of almond protein market share in 2025, whereas organic products are set to register a 12.05% CAGR through 2031.

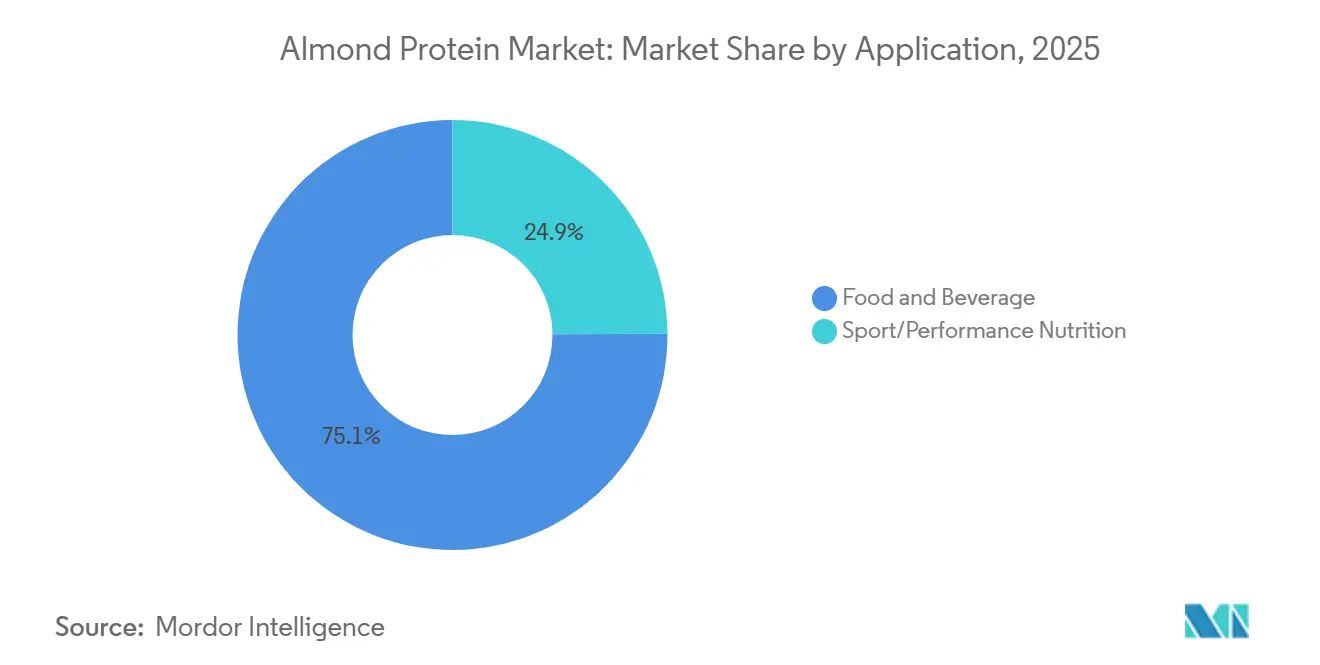

- By application, food and beverage products led with 75.10% revenue share in 2025; sports/performance nutrition is projected to grow at 12.18% CAGR to 2031.

- By geography, North America commanded 37.65% share of almond protein market size in 2025, while Asia-Pacific is expected to advance at 12.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Almond Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health consciousness drives plant-based protein adoption | +3.1% | Global, early traction in North America and Europe | Short term (≤ 2 years) |

| Sports nutrition demand accelerates functional applications | +2.8% | North America and Europe core, spill over to Asia-Pacific | Medium term (3-4 years) |

| Regulatory framework standardization reduces barriers | +2.2% | Global urban centers, strongest in Asia-Pacific | Medium term (3-4 years) |

| Supply-chain sustainability creates premium positioning | +1.9% | North America and Europe, niche gains in Latin America | Long term (≥ 5 years) |

| Growing application in protein bars, shakes, and bakery items | +1.7% | Global CPG hubs; strong in North America and Europe convenience channels | Short term (≤ 2 years) |

| Rich nutrient profile with high protein and healthy fats | +1.4% | Global, high resonance in Asia-Pacific and Europe wellness markets | Medium term (3-4 years) |

| Source: Mordor Intelligence | |||

Rising health consciousness drives plant-based protein adoption

As consumers increasingly recognize the connections between diet, wellness, and long-term health, there's a notable pivot towards plant-based nutrition. Almond protein stands out as a favored option, celebrated for its clean-label, non-GMO, and allergen-friendly attributes. In contrast to certain other plant proteins, almond protein boasts easy digestibility and is naturally abundant in fiber, healthy fats, and essential nutrients. This makes it particularly appealing for health-centric product formulations. The Almond Board of California highlights clinical evidence indicating that a daily intake of 2 oz of almonds can reduce creatine-kinase levels and expedite muscle recovery post-exercise. Consequently, almond protein is finding its way into diverse applications, from sports and performance nutrition to dairy alternatives, protein-enriched snacks, baked goods, and meal replacements. Additionally, the surging appetite for functional foods, those that aid in weight management, bolster heart health, and enhance energy further cements almond protein's role in daily diets, underscoring its significance in the expanding plant-based food movement.

Sports nutrition demand accelerates functional applications

As athletes and fitness enthusiasts increasingly prioritize clean, functional ingredients for muscle recovery, energy, and performance, almond protein has emerged as a sought-after plant-based alternative. Furthermore, heightened government regulations aimed at ensuring product quality and mandating warnings on food items are nudging manufacturers towards almond protein, bolstering the market's expansion. For example, the Bundesamt für Verbraucherschutz und Lebensmittelsicherheit (BVL) reported that, as of May 2024, the Federal Office of Consumer Protection and Food Safety issued 269 warnings related to food products. Almond protein's rich amino acid profile, elevated protein content, and natural origins render it perfect for protein bars, powders, ready-to-drink shakes, and functional snacks. The Almond Board of California highlights that a one-ounce serving has 13 grams of “good” unsaturated fats, just 1 gram of saturated fat, and, as always, almonds are cholesterol-free [1]Almond Board of California, "Key facts about almond nutrition", almonds.com. This allows for the creation of bars, ready-to-drink beverages, and recovery snacks without the need for masking agents. This heightened focus on clean-label, high-performance nutrition is driving manufacturers to weave almond protein into a broader spectrum of sports and active-lifestyle products, solidifying its position in the expansive functional food and beverage market.

Regulatory framework standardization reduces barriers

With regulatory bodies increasingly aligning on safety, labeling, and quality benchmarks for plant-based ingredients, manufacturers find it easier to formulate and distribute almond protein products on a global scale. For example, in January 2025, the U.S. FDA released draft guidance on labeling plant-based alternatives, clarifying the coexistence of nutrient statements and traditional dairy terms. This guidance diminishes uncertainty for smaller processors by setting clear expectations for protein quality claims, allowing for swifter product launches. Similarly, Blue Diamond's self-affirmed GRAS notice for its partially defatted almond protein flour underscores the viability of this pathway and paves the way for other derivative products. Such harmonization not only streamlines compliance but also accelerates time-to-market and curtails the costs and complexities tied to product development and export. Furthermore, clear labeling combats misleading marketing, spotlighting suppliers with verified nutrition data and authentic supply chains. This transparency bolsters consumer trust in the safety and consistency of almond protein, spurring its adoption in a range of applications, from dairy alternatives and nutritional supplements to infant nutrition and functional snacks. Consequently, these standardized regulations are not just facilitating almond protein's entry into new markets but are also spurring innovation and investment in plant-based product development within the global food and beverage landscape.

Supply-chain sustainability creates premium positioning

With environmental and ethical concerns shaping purchasing choices, sustainably sourced products, like almond protein, are increasingly seen as responsible and premium. Almond producers are adopting eco-friendly farming, prioritizing water conservation, and ensuring transparent sourcing. These efforts boost the ingredient's allure for brands and consumers who prioritize sustainability. For example, the Almond Board of California reports that since the 1990s, California almond growers have reduced orchard water use by 33%, aiming for another 20% cut by 2025. Such achievements not only meet retailers’ ESG criteria but also elevate almond protein's status as a climate-conscious choice. In a similar vein, OFI’s KIND Almond Acres Initiative harnesses AI on 500 acres to refine irrigation and protect pollinators, leading to reduced costs and enhanced yields. Additionally, Blue Diamond’s Orchard Stewardship Incentive Program, backed by the USDA, incentivizes growers to embrace regenerative practices, boosting certified organic and carbon-neutral acreage. This green, premium image empowers manufacturers to stand out in a saturated market and justify elevated price points. In the sports nutrition arena, where ethical sourcing and clean labels reign supreme, almond protein emerges as a plant-based, functional choice that marries performance with sustainability. Consequently, the emphasis on a sustainable supply chain not only bolsters consumer trust and brand allegiance but also propels the adoption of almond protein in an expanding array of health-centric and eco-conscious products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Production cost premiums limit mass market penetration | -1.7% | Global; acute in import-reliant Asia-Pacific | Short term (≤ 2 years) |

| Geographic supply concentration creates scalability constraints | -1.0% | Global processed-food formulators; higher in taste-sensitive Europe | Medium term (3-4 years) |

| Competition from alternative plant-based protein sources | -1.0% | Global; strong soy and pea presence in North America and Europe | Medium term (3-4 years) |

| Allergen concerns associated with nuts | -1.3% | National, heightened in United States school systems | Long term (≥ 5 years) |

| Source: Mordor Intelligence | |||

Production cost premiums limit mass market penetration

Producing almond protein is pricier than crafting other plant-based proteins, such as soy or pea. Manufacturers, feeling the pinch of these elevated costs, find almond protein less viable for large-scale, budget-conscious product lines targeting the average consumer. The need for specialized extraction equipment, coupled with the premium pricing of raw almonds, positions almond protein at a higher price point than bulk soy or pea isolates. Take Blue Diamond, for example: despite an uptick in volumes, the company's flat FY 2024 revenue of USD 1.33 billion highlights the margin pressures in a market saturated with cheaper alternatives. Consequently, almond protein finds its niche, often reserved for premium products aimed at health-conscious or environmentally aware consumers, rather than being a staple in everyday items. In the sports nutrition arena, there's a robust demand for clean-label and plant-based ingredients. Yet, price sensitivity looms large, especially in markets where consumers anticipate a high protein content without the hefty price tag. Furthermore, the global surge in almond protein costs can be traced back to an increasing reliance on almond imports. For instance, the USDA Foreign Agricultural Service reported that Canada’s almond imports for 2023/24 reached approximately 26 thousand metric tons [2]USDA Foreign Agricultural Service, "Tree Nuts: World Markets and Trade", apps.fas.usda.gov. In a similar vein, UN Comtrade noted that Argentina imported 2,174 metric tons of almonds in 2024. These rising local production costs act as a significant barrier, stifling the broader adoption and slowing the expansion of almond protein in the global functional food and beverage market.

Geographic supply concentration creates scalability constraints

Regions like California and parts of the Mediterranean dominate almond supply, creating scalability constraints that hinder the almond protein market's growth. This concentration limits the protein's application across food, beverage, and sports nutrition sectors. The heavy reliance on these key areas exposes the supply chain to challenges like drought, climate change, and regulatory pressures, leading to potential disruptions and volatility. For example, California and Australia, the primary suppliers of edible almonds, face risks from weather and logistics. Events like extreme heat or water shortages can limit kernel availability, forcing processors to ration or increase prices. While Australia's record 164,000-metric-ton harvest in 2024 offers some sourcing diversification, global shipping costs diminish competitiveness for major customers in Asia and Latin America. Such risks complicate manufacturers' efforts to secure consistent and affordable almond protein inputs, challenging their ability to meet rising global demand or explore new markets. Additionally, these geographic constraints stifle production scalability and deter long-term investments in almond protein innovation, particularly for firms valuing reliability and supply chain resilience. Consequently, this concentrated supply base acts as a bottleneck, hindering almond protein's mass-market integration and its adoption in cost-sensitive, high-volume product categories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Nature: Conventional Dominates, While Organic Certification Drives Premium Growth

In 2025, conventional products command a dominant 78.25% share of the almond protein market, leveraging their cost leadership and scale advantages. Food and beverage manufacturers, along with those in sports and performance nutrition, favor conventional almond protein ingredients. Their appeal lies in wider availability, cost-effectiveness, and established supply chains, all of which facilitate large-scale production and integration into mainstream product lines. Conventional almond protein fulfills essential functional and nutritional criteria boasting high protein content, a plant-based origin, and a clean-label allure—yet sidesteps the price premiums tied to organic certification. This pricing edge becomes crucial in competitive markets, where manufacturers juggle the dual demands of quality and price sensitivity.

Meanwhile, organic almond protein, appealing to consumers' growing preference for transparent sourcing, is on track to expand at a robust 12.05% CAGR through 2031. The demand for organic almond protein ingredients is steadily rising. This growth is fueled by a niche, yet expanding, demographic of health-conscious and environmentally-savvy consumers. These individuals prioritize clean, pesticide-free sourcing and champion sustainable farming practices. For instance, organic food revenues in Germany, as highlighted by the Bund Ökologische Lebensmittelwirtschaft (BÖLW) - the nation's leading association for organic farmers, processors, and retailers - surged to EUR 16.99 billion in 2024, marking an increase from EUR 16.08 billion the previous year . Yet, challenges loom: limited supply, elevated production costs, and the intricacies of certification hinder the organic segment's growth momentum. As organic farming practices gain traction and the demand for traceable, eco-friendly ingredients intensifies, the organic segment is poised for growth. However, conventional almond protein is likely to retain its dominant position in the short term, thanks to its economic and logistical benefits.

By Application: Food and Beverage Dominates, While Sports Nutrition Transforms Market Dynamics

In 2025, food and beverage applications claimed a dominant 75.10% revenue share, as almond protein seamlessly integrates into baked goods, flavored milks, and ready-to-eat cereals without the need for taste masking. Food and beverage manufacturers are increasingly turning to almond protein ingredients, drawn by their versatility, clean-label appeal, and alignment with the growing consumer trend towards plant-based and health-centric diets. Almond protein finds its way into a diverse array of applications, from dairy alternatives and baked goods to snacks and meal replacements. It offers functional advantages, including enhanced texture, a subtle flavor, and nutritional benefits, all while steering clear of common allergens like soy and dairy. Its standing as a natural, premium ingredient strikes a chord with mainstream consumers, making it a favored choice for large-scale incorporation into everyday products.

The sports and performance nutrition sector is on track to expand at a robust 12.18% CAGR, bolstered by human trials that link almond consumption to quicker exercise recovery and reduced creatine-kinase spikes. While there's a budding interest in almond protein within the sports nutrition realm, its growth has been more tempered. This sector has long been anchored by whey, soy, and pea proteins, celebrated for their high protein density and cost-effectiveness. Yet, as athletes and health-conscious consumers pivot towards cleaner, sustainable, and plant-based choices, the sports nutrition landscape is starting to recognize almond protein's functional merits. This shift hints at a promising growth trajectory in the years ahead. For instance, data from Canadian Grocer highlights that in 2024, almond drinks led the pack among plant-based beverages in Canada, capturing a notable 46% share, outpacing oat, soy, and coconut alternatives.

Geography Analysis

In 2025, North America commands a 37.65% share of the almond protein market, thanks to California's seamless integration from orchards to protein isolates. North American food and beverage manufacturers, especially in California – the globe's top almond producer – are responding to a robust demand for almond protein. This surge is fueled by consumers' strong preference for plant-based, clean-label, and allergen-friendly products. North American innovators are leading the charge in dairy alternatives, protein-enriched snacks, and functional foods, driving a heightened demand for almond protein as a health-centric ingredient. For example, in May 2024, Lactalis Canada, a subsidiary of France's Lactalis Group and the force behind renowned brands like Cracker Barrel and Black Diamond, unveiled its plant-based brand Enjoy!, debuting a high-protein almond drink. Additionally, Canada's growing appetite for plant proteins and Mexico's burgeoning wellness sectors present further regional opportunities.

Asia-Pacific is on a rapid ascent, forecasted to grow at a 12.22% CAGR through 2031, spurred by an urban middle class increasingly embracing nuts and proteins. As per the International Nut and Dried Fruit Council, South Koreans consumed approximately 2.14 kilograms of almonds per capita in 2023. The Asia-Pacific region is witnessing a surge in demand, driven by rising incomes, urbanization, and heightened health consciousness. Nations like China, India, and Australia are gravitating towards premium, Western-style health products, with almond protein emerging as a favored choice.

Europe's demand remains stable, bolstered by a seasoned market, stringent regulations, and a discerning consumer base. The continent's ongoing pursuit of sustainable and natural ingredients, coupled with transparent carbon-footprint labeling, underscores almond protein's appeal, especially given its noted water-use efficiencies. Germany, France, and the UK spearhead formulation activities, while southern European nut-centric diets foster cultural acceptance. In the Middle East and Africa, while premium almond protein appeals to affluent urbanites, infrastructural challenges hinder widespread distribution, necessitating strategic alliances with local beverage and bakery chains.

Competitive Landscape

The almond protein market is moderately concentrated. Blue Diamond Growers, Olam Group, and Harris Woolf, among others, are the major players operating in the market. Blue Diamond Growers, leveraging vertical integration and GRAS certifications, safeguards its formulations for bakery items, beverages, and nutrition bars. However, flat revenue growth underscores mounting operational expenses and competitive pricing pressures from more affordable proteins. Notably, the cooperative's expansion of distributors into Asia indicates a strategic shift towards regions with higher growth potential.

Olam Group stands out by harnessing technology, specifically AI irrigation models, to curtail water usage and bolster pollinator habitats in trial orchards. This strategy not only mitigates raw-material volatility but also enhances sustainability credentials, a pivotal factor for CPG brands. Moreover, companies are expanding their portfolios through acquisitions, gaining better access to texturizing and sweetening technologies that complement almond protein, offering holistic solutions.

Newer companies entering the market are developing advanced membrane filtration and enzymatic defatting methods, which compete with existing products in nutritional content. However, these companies face regulatory hurdles and production scale limitations that affect their market entry. Suppliers who can maintain consistent product batches, manage allergens effectively, and demonstrate environmental sustainability advantages are likely to secure key formulation contracts, particularly in markets where clean label products and functional benefits drive consumer purchases.

Almond Protein Industry Leaders

-

Blue Diamond Growers

-

Olam Group

-

Harris Woolf

-

Austrade Inc.

-

All Organic Treasures GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Blue Diamond Growers has partnered with Divert, Inc. to revolutionize the use of almond processing byproducts, including almond protein, by converting them into renewable energy. With Divert's cutting-edge technologies and eco-friendly infrastructure, Blue Diamond Growers aims to transform these low-value almond byproducts into a source of renewable energy.

- June 2024: Tate & Lyle acquired CP Kelco for USD 1.8 billion to create a diversified specialty-ingredients business. The acquisition aligns with growing consumer demand for plant-based, clean-label, and sustainable ingredients, enabling the combined entity to offer a broader range of solutions for healthier and tastier food and beverages.

Global Almond Protein Market Report Scope

The Global Almond Protein Market is segmented by application into Bakery, Nutritional Supplements, Beverages, Confectionery, and other Applications. Additionally by geography, the market is segemented by regions including North America, Europe, Asia-Pacific, South America and Middle East & Africa.

| Conventional |

| Organic |

| Food and Beverage | Bakery |

| Beverages (RTD and Powdered) | |

| Confectionery and Snacks | |

| Dairy and Dairy-Alternative Products | |

| Meat Analogues and Extenders | |

| Sport/Performance Nutrition |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Nature | Conventional | |

| Organic | ||

| By Application | Food and Beverage | Bakery |

| Beverages (RTD and Powdered) | ||

| Confectionery and Snacks | ||

| Dairy and Dairy-Alternative Products | ||

| Meat Analogues and Extenders | ||

| Sport/Performance Nutrition | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the almond protein market?

The market is valued at USD 477.56 million in 2026 and is projected to reach USD 806.53 million by 2031 at an 11.06% CAGR during the forecast period (2026-2031).

Which application segment is expanding the fastest?

Sports/performance nutrition is forecast to grow at 12.18% CAGR through 2031, outpacing other uses.

How big is the organic share of the almond protein market?

Organic products represent a smaller base today but are expected to grow at 12.05% CAGR, benefiting from clean-label demand.

Which region offers the strongest growth prospects?

Asia-Pacific is set to record a 12.22% CAGR through 2031, driven by rising Chinese nut intake and regional supply from Australia.

Why do processors favour almond protein over other plant proteins?

Almond protein provides a mild flavour, balanced minerals, and documented sustainability gains, reducing formulation complexity and supporting premium positioning.

What are the main challenges facing market expansion?

Higher production costs and reliance on California and Australia for raw nuts limit price competitiveness and supply scalability in cost-sensitive regions.

Page last updated on: