Savory Ingredients Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 10.06 Billion |

| Market Size (2031) | USD 14.09 Billion |

| Growth Rate (2026 - 2031) | 6.97% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

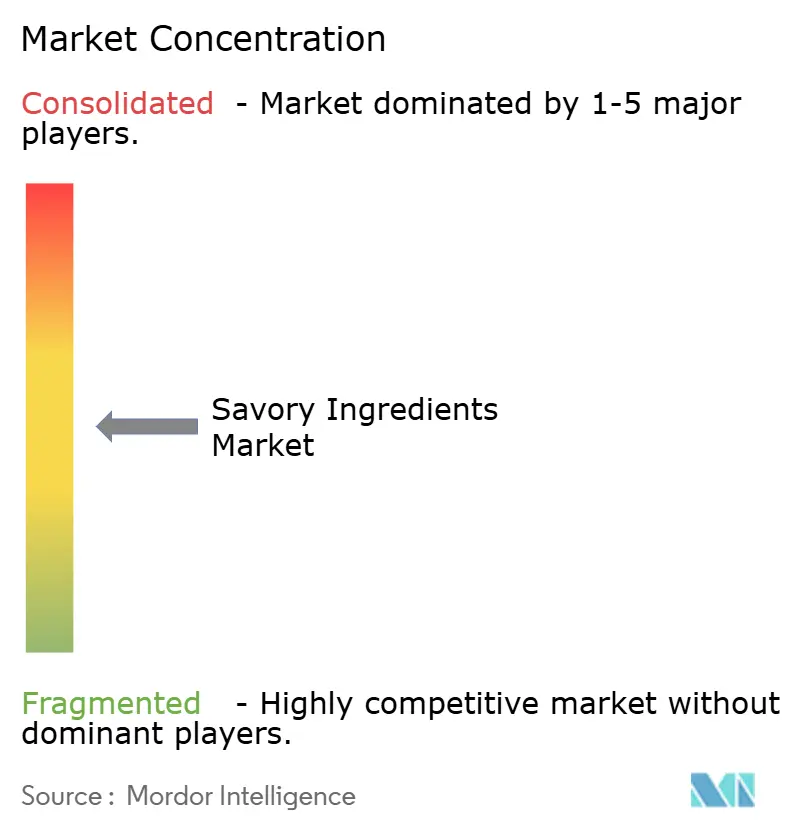

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Savory Ingredients Market Analysis by Mordor Intelligence

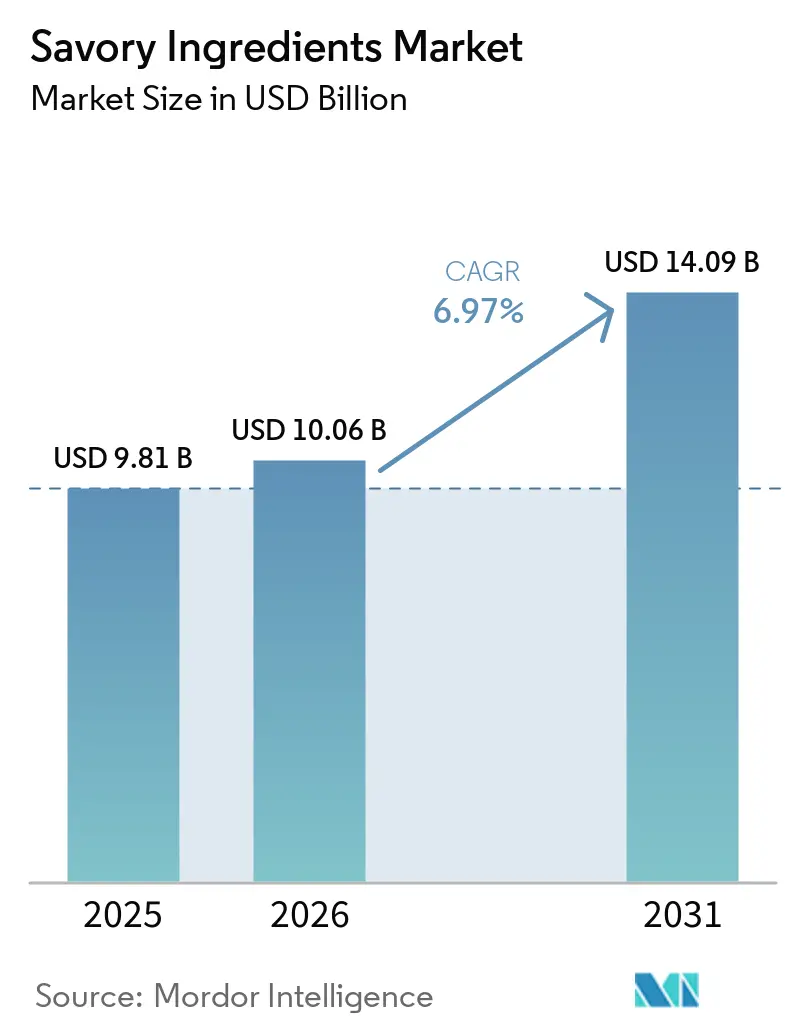

The savory ingredients market was valued at USD 9.81 billion in 2025 and is projected to grow from USD 10.06 billion in 2026 to USD 14.09 billion by 2031, registering a CAGR of 6.97% during the forecast period (2026-2031). Factors such as cost-efficient fermentation, increasing demand for clean-label flavors, and retailer requirements for recognizable ingredient lists are influencing competitive dynamics. Mid-tier yeast extract producers utilizing continuous fermentation are challenging traditional spray-drying manufacturers, while precision-fermented nucleotides are approaching cost equivalence with chemically synthesized alternatives. Additionally, stricter regulations on sodium and monosodium glutamate (MSG) are driving formulation budgets toward nucleotide–yeast extract blends, which help maintain flavor intensity at reduced inclusion levels.

Key Report Takeaways

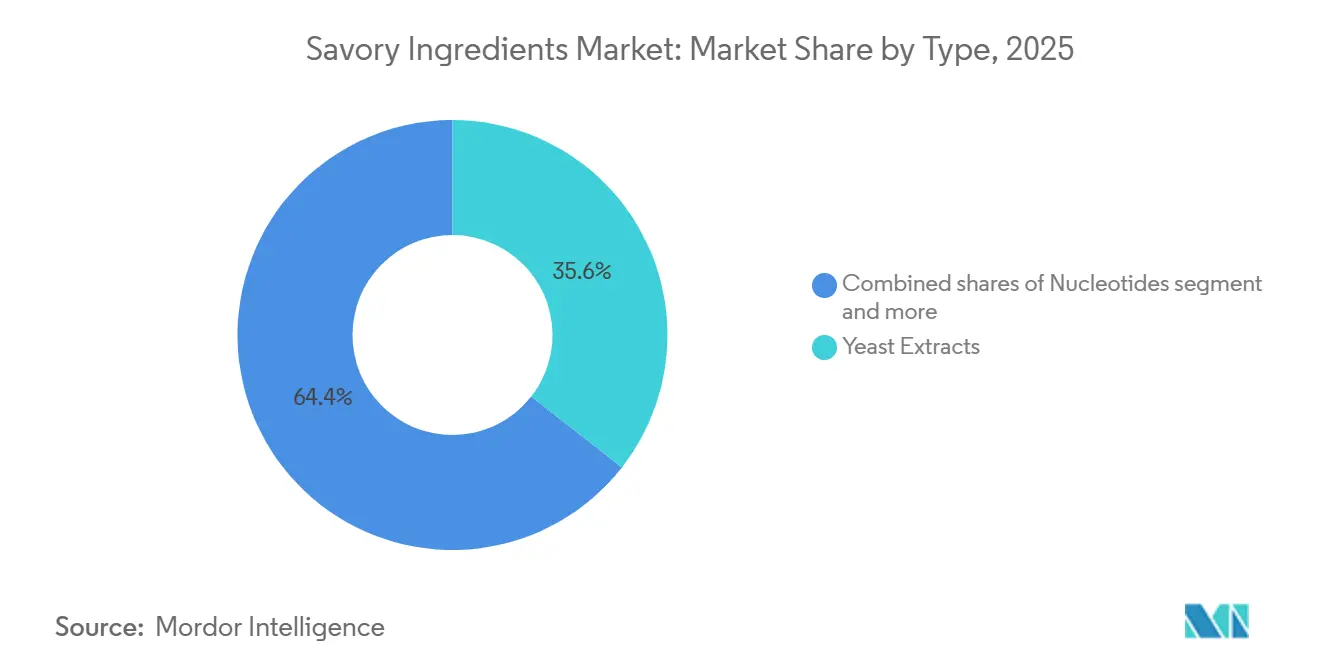

- By type, yeast extracts led with a 35.56% savory ingredients market share in 2025, while nucleotides are projected to post a 7.56% CAGR from 2026 to 2031.

- By form, powder products accounted for 66.17% of the savory ingredients market share in 2025; liquid and paste formats are set to expand at a 7.01% CAGR through 2031.

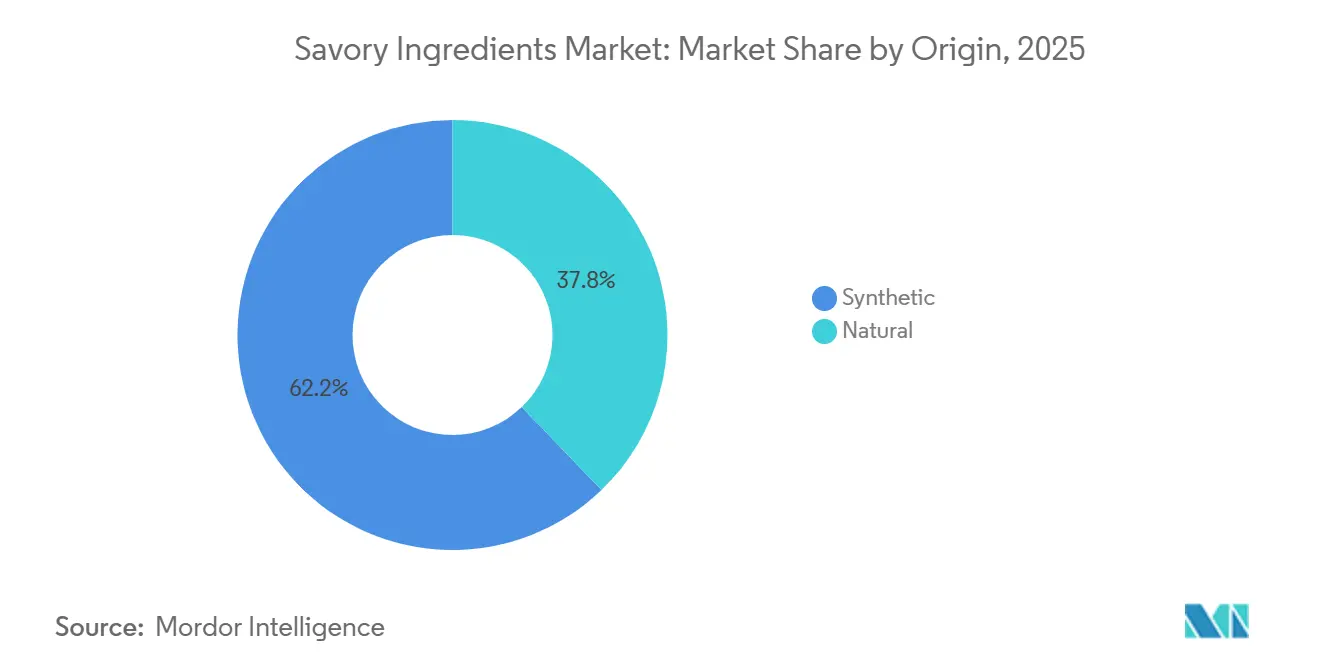

- By origin, synthetic ingredients captured 62.19% share of the savory ingredients market size in 2025, while natural ingredients are forecast to grow at a 7.87% CAGR to 2031.

- By application, snacks captured 37.19% share of the market in 2025, while ready meals are forecast to grow at an 7.81% CAGR through 2031.

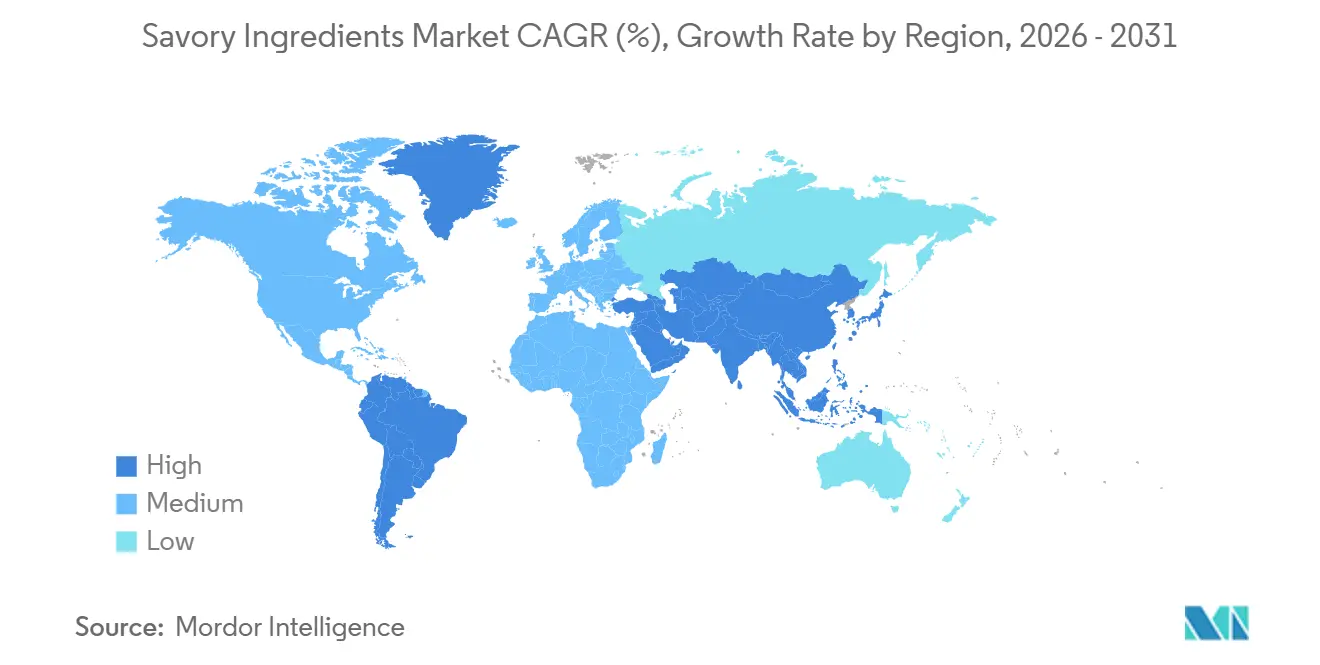

- By geography, Asia-Pacific dominated with 39.41% share of the savory ingredients market in 2025, while Europe is advancing at an 7.58% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Savory Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in convenience and ready-to-eat meals | +1.2% | Global, with Asia-Pacific and North America leading volume growth | Medium term (2-4 years) |

| Intensifying demand for plant-based umami solutions | +0.9% | North America and Europe core, expanding to Asia-Pacific urban centers | Long term (≥ 4 years) |

| Shift toward clean-label natural flavor enhancers | +0.8% | Europe leading, North America following, Asia-Pacific selective adoption | Medium term (2-4 years) |

| Fermentation-tech cost breakthroughs lowering yeast-extract prices | +0.7% | Global, with China and India scaling production fastest | Short term (≤ 2 years) |

| AI-driven flavor-personalization platforms adopted by CPG reserach and developemnt | +0.5% | North America and Europe innovation hubs, pilot rollouts in Asia-Pacific | Long term (≥ 4 years) |

| Upcycled side-stream proteins adopted in European flavor houses | +0.4% | Europe concentrated, early trials in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in convenience and ready-to-eat meals

The growing demand for convenience and ready-to-eat meals is a significant driver of the savory ingredients market. Modern consumers increasingly prioritize time-saving food solutions over concerns about processing. Factors such as urbanization, busy lifestyles, and the rise in dual-income households have led to a structural shift toward ready meals, frozen foods, snacks, and instant food formats. These products rely heavily on savory ingredients, including flavor enhancers, seasoning blends, and natural extracts, to ensure consistent taste and shelf stability. This trend is further supported by changing consumer behavior, where convenience often takes precedence over health concerns related to processing. For example, in 2025, 39% of U.S. consumers either do not avoid processed foods (21%) or do not consider processing at all when making purchasing decisions (18%), indicating a notable segment that remains indifferent to processing levels[1]Source: International Food Information Council (IFIC), "2025 IFIC Food & Health Survey", ific.orgi. Food manufacturers are increasingly investing in flavor systems to enhance taste, mask processing effects, and improve product appeal in convenient formats. Savory ingredients are essential for providing restaurant-like taste, extended shelf life, and sensory consistency, making them vital in the growing ready-to-eat market.

Intensifying demand for plant-based umami solutions

The growing demand for plant-based umami solutions is a significant driver for the savory ingredients market. The global shift toward plant-based diets has increased the need for flavor systems capable of replicating the depth, richness, and mouthfeel traditionally associated with meat. As consumers reduce their intake of animal protein, manufacturers face pressure to create authentic savory taste profiles in plant-based products. This has led to increased demand for ingredients such as yeast extracts, fermented bases, hydrolyzed vegetable proteins, and natural umami enhancers like rosemary and mushroom extracts. This trend is further bolstered by the rapid growth of the plant-based ecosystem. For example, a report from Argentina’s Association of Plant-Based Producers revealed that the sector includes over 1,200 companies during the period 2023-24, highlighting a dynamic and competitive market landscape [2]Source: egconomist, "Plant-Based Movement Steadily Gaining Momentum in Beef-Loving Argentina", vegconomist.com. This scale reflects strong supply-side momentum, along with heightened innovation and frequent product launches, all of which necessitate advanced savory solutions to enhance taste and consumer acceptance.

Shift toward clean-label natural flavor enhancers

The growing preference for clean-label natural flavor enhancers is a significant driver in the savory ingredients market. Consumers are increasingly prioritizing transparency, simplicity, and recognizable ingredients in food products. This trend is prompting manufacturers to replace synthetic additives, such as MSG and artificial flavorings, with natural alternatives like yeast extracts, plant-based extracts (e.g., rosemary), and fermentation-derived ingredients. These alternatives provide similar taste profiles while meeting clean-label expectations. Changing consumer behavior, particularly among Gen Z and Millennial shoppers, supports this shift. These groups were willing to pay 20–30% more as of 2025 for products labeled as organic, natural, high-protein, or free from artificial ingredients, presenting a clear opportunity for premiumization[3]Source: Ingredion "Less mystery, more meaning: Clean labels win consumer preference", ingredion.com. This trend is not only shaping purchasing decisions but also compelling food manufacturers to reformulate products and invest in natural flavor systems to remain competitive and maintain brand trust. Consequently, suppliers of savory ingredients are focusing on innovation in natural, minimally processed, and multifunctional flavor enhancers that deliver taste, preservation, and clean-label compliance simultaneously.

Fermentation-tech cost breakthroughs lowering yeast-extract prices

Advancements in continuous fermentation and membrane-separation technologies have reduced yeast-extract production costs by 15-20%, allowing competitors to offer competitive pricing while maintaining clean-label standards. Chinese yeast producers, including Angel Yeast and Meihua Holdings, implemented automated bioreactor systems during 2024-2025, reducing energy consumption per kilogram of extract by 18%, as reported in company sustainability disclosures. These efficiency improvements are diminishing the historical margin advantage held by European and North American producers, prompting strategic measures such as vertical integration into specialty nucleotide production or expansion into high-growth Asian markets. The resulting cost reductions benefit downstream food manufacturers, enabling higher inclusion rates of yeast extracts in value-tier product lines and broadening access to umami enhancement beyond premium product segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global limits on sodium and MSG inclusion levels | -0.6% | Global, with Europe and North America enforcement strictest | Short term (≤ 2 years) |

| Volatile raw-material pricing for yeast and soy proteins | -0.5% | Global, acute in regions reliant on imported molasses and soy | Short term (≤ 2 years) |

| Scale-up bottlenecks for precision-fermented nucleotides | -0.4% | North America and Europe research and development centers, with limited commercial capacity | Medium term (2-4 years) |

| Consumer skepticism toward "hydrolyzed" declarations | -0.3% | North America and Europe primary, emerging in Asia-Pacific affluent segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent global limits on sodium and MSG inclusion levels

Public health initiatives addressing hypertension and cardiovascular disease are enforcing stricter sodium limits in processed foods, driving the reformulation of low-sodium savory alternatives that retain flavor intensity. In 2024, the U.S. Food and Drug Administration finalized voluntary sodium-reduction targets for packaged foods, setting a limit of 2,300 milligrams per day across key categories. This indirectly impacts the use of monosodium glutamate (MSG), as it contains 12% sodium by weight. Similarly, the European Food Safety Authority reaffirmed its acceptable daily intake for glutamate at 30 milligrams per kilogram of body weight in 2024, supporting existing regulations that encourage the use of nucleotide-yeast extract blends to enhance umami flavor with lower sodium content. Compliance costs vary significantly; while multinational companies can manage reformulation expenses, regional players may face reduced profit margins or the need to streamline product offerings, potentially accelerating market consolidation.

Volatile raw-material pricing for yeast and soy proteins

Feedstock price fluctuations, influenced by weather disruptions, biofuel demand, and trade policies, are impacting ingredient economics. This has led suppliers to either pass on costs to customers or absorb margin reductions. Molasses, the primary substrate for yeast cultivation, experienced a 13% price increase in 2024 due to drought-induced declines in sugarcane yields in Brazil and India, as reported by agricultural commodity sources. Similarly, soy protein prices showed volatility, rising by 9% in early 2025 before stabilizing with normalized South American harvests. These price swings complicate long-term supply agreements and encourage vertical integration. Companies that manage their own fermentation feedstocks achieve greater pricing stability, while those dependent on spot markets face quarterly margin fluctuations, hindering strategic planning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Yeast Extracts Lead Market Share While Nucleotides Show Highest Growth Potential

Yeast extracts accounted for a 35.56% market share in 2025, driven by their versatility in applications such as snack seasonings, soup bases, and ready-meal formulations. These extracts provide umami flavor enhancement and help mask undesirable notes caused by reheating. Nucleotides, including inosine monophosphate, guanosine monophosphate, and adenosine monophosphate, are projected to grow at a CAGR of 7.56% through 2031, marking the fastest growth among all product types. This growth is attributed to their ability to synergistically enhance glutamate-derived savoriness, even at low inclusion rates of 0.02-0.05%.

Hydrolyzed vegetable protein remains a cost-effective option for value-tier applications. However, it faces challenges due to consumer concerns over "hydrolyzed" label declarations, which limit its growth in mature markets where price sensitivity takes precedence over clean-label preferences. The "Others" category, which includes fermented vegetable extracts and mushroom-derived umami compounds, is gaining popularity in plant-based analogs. This is because conventional yeast extracts can leave a residual bitterness that conflicts with vegetable protein bases, making alternatives more appealing in such applications.

By Form: Liquid Segment Gains Momentum in Processing Applications

The powder form is projected to hold a dominant 66.17% market share in 2025, attributed to its shelf stability, transportation efficiency, and versatility in food applications. This segment's market leadership is further supported by well-established supply chains and manufacturing processes, particularly in the production of yeast extract and hydrolyzed protein. Meanwhile, the liquid and paste form segment is expected to grow at a 7.01% CAGR through 2031, driven by increasing demand in ready-to-eat meals and beverages, where these forms offer better dispersion and enhanced flavor release. Food manufacturers favor liquid ingredients for their seamless integration into production processes, eliminating the need for hydration.

DSM-Firmenich's new Parma facility, dedicated to liquid flavors in dry blends, highlights the industry's focus on innovation in liquid form solutions. This facility allows manufacturers to leverage the benefits of liquid ingredients while maintaining the handling advantages of powder forms. The segmentation of the market by form reflects industry trends prioritizing convenience and processing efficiency, with liquid ingredients being particularly suited for automated and continuous processing systems. Companies are also developing hybrid solutions that combine the stability of powder with the functionality of liquid forms, aiming to capitalize on opportunities in both segments.

By Origin: Natural Segment Accelerates Through Regulatory Alignment

Synthetic origin ingredients are projected to hold a 62.19% market share in 2025, while natural ingredients are anticipated to grow at a compound annual growth rate (CAGR) of 7.87% through 2031. This growth is driven by regulatory alignment and increasing consumer preference for natural products. Regulatory changes, such as China's updated food additive standards, which restrict "no additives" claims and promote ingredient transparency, contribute to this trend. Similarly, European regulations, including EFSA's approval of precision fermentation-derived ingredients that retain a natural classification despite their biotechnology-based production, support the expansion of natural ingredients. In contrast, synthetic ingredients face heightened scrutiny in regions with stringent labeling requirements and high consumer awareness.

Technological advancements are facilitating the growth of the natural segment by enabling the commercial-scale production of natural ingredients. Precision fermentation technology allows manufacturers to produce naturally-derived ingredients using genetically modified microorganisms while ensuring the final products retain their natural classification. Companies investing in biotechnology infrastructure are gaining competitive advantages by addressing the growing demand for natural ingredients. This trend reflects an industry-wide shift toward sustainable production methods and clean-label formulations, with natural origin ingredients increasingly becoming a standard requirement across various applications rather than being positioned as a premium feature.

By Application: Snacks Lead Growth Through Premiumization Trends

The snacks segment is projected to account for a market share of 37.19% in 2025, while the ready meals segment is anticipated to achieve a CAGR of 7.81%. The snacks segment drives market growth through the development of premium products and flavor innovations, particularly in Asia-Pacific, where a significant portion of consumers is willing to pay a premium for gourmet ingredients. Trends in protein fortification further support the segment's growth, with high-protein claims becoming increasingly prevalent across snack categories. Emerging protein sources, such as yeast and precision fermentation-derived ingredients, are being introduced to meet this demand. The soups, sauces, and dressings segment maintains steady demand through traditional applications and clean-label reformulations. Meanwhile, the ready meals segment continues to expand, driven by consumer demand for convenience and enhanced flavors. In meat processing, the growing popularity of plant-based alternatives creates opportunities for umami enhancers that cater to both conventional and alternative protein products.

Seasoning blends are experiencing growth as manufacturers focus on creating distinct flavor profiles and offering functional benefits beyond taste enhancement. This diversification highlights the adaptability of savory ingredients and the ability of manufacturers to develop specialized formulations for specific applications. Companies that provide application-specific solutions and technical support achieve higher margins and strengthen customer relationships through their specialized expertise. The segment's shift toward premium products and functional benefits presents opportunities for ingredient suppliers to differentiate themselves through superior product performance and technical services.

Geography Analysis

Asia-Pacific held 39.41% of the global savory ingredients market in 2025, while Europe maintains the highest regional growth rate at 7.58% CAGR through 2031. This growth stems from increased middle-class consumption and premium snacking preferences. China's regulatory environment significantly influences regional dynamics, with the updated food additive standard (GB 2760-2024) affecting ingredient approval and labeling requirements. The region's consuming class is expected to reach 3 billion by 2030, with rising disposable income driving premiumization across food segments. The market shows significant potential for advanced ingredient applications, particularly in plant-based meat alternatives and premium snack products utilizing umami enhancement technologies.

North America and Europe maintain stable market positions with well-defined regulatory structures and consumer demand for clean-label ingredients. The U.S. Department of Commerce's antidumping ruling on Chinese MSG imports has influenced supply chain operations. Both regions emphasize biotechnology-driven ingredient production, exemplified by DSM-Firmenich's investments in manufacturing facilities for natural flavor solutions. These markets present opportunities for premium products and technological advancement, with manufacturers utilizing advanced production methods to increase margins through innovation.

South America, Middle East, and Africa offer growth potential through expanding food processing sectors and evolving consumer preferences. These regions leverage their agricultural resources and competitive feedstock production costs, providing opportunities for supply chain diversification. Market expansion aligns with economic development and urbanization trends, supporting increased processed food consumption and flavor enhancement requirements. Companies establishing operations in these regions aim to benefit from market maturation and shifting consumer preferences toward premium ingredients.

Mordor Intelligence provides coverage of the savory ingredients market across other key regional markets, including Asia, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The savory ingredients market demonstrates moderate concentration, characterized by the presence of diversified food-science multinationals alongside a dynamic group of specialist biotech firms. Established players utilize their extensive customer networks and broad product portfolios but are increasingly required to adopt fermentation technologies and AI-driven formulation processes to maintain their market share.

DSM-Firmenich’s recent development in Parma highlights its long-term focus on high-intensity savory blends, aligning with the growing demand for plant-based meat products. The company's collaboration with Meala FoodTech to enhance pea protein texturization underscores the trend of partnerships within the savory ingredients market, contributing to broader solutions in the protein ecosystem. Similarly, AI-driven initiatives, such as McCormick’s flavor-design collaboration with IBM, streamline formulation processes and secure proprietary data advantages without significant capital expenditure.

Emerging competitors are concentrating on upcycling by-products or engineering microbial strains to achieve higher nucleotide yields. Venture-backed start-ups specializing in fungal or insect proteins are targeting niche but rapidly expanding segments, often licensing their technologies to mid-sized regional manufacturers. Intellectual property portfolios and regulatory compliance documents are becoming critical assets in partnership negotiations, reflecting the industry's transition toward knowledge-driven competition.

Savory Ingredients Industry Leaders

-

Ajinomoto Co.

-

Kerry group Plc

-

DSM-Firmenich

-

Givaudan SA

-

Archer Daniels Midland Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Angel Yeast introduced a moisture-resistant yeast extract solution aimed at resolving moisture absorption and caking issues frequently encountered in powdered seasonings and food blends. The ingredient was developed using directional enzymatic hydrolysis and spray-drying technologies to enhance fluidity, reduce hygroscopicity, and improve storage stability in humid processing conditions.

- June 2025: MicroBioGen, an Australian yeast biotechnology company, and Lesaffre, a global fermentation company, have entered into an exclusive worldwide licensing and collaboration agreement to develop yeast solutions for the baking, food, and biochemicals markets. This partnership combines MicroBioGen's yeast strain platform and 20-year genetic library with Lesaffre's bioengineering expertise.

- December 2024: Lesaffre has acquired DSM-Firmenich's yeast extract business, incorporating its sales organization, processing technologies, and 46 employees into its Biospringer division. This acquisition aligns with Lesaffre's objective to establish itself as a global leader in yeast extracts and derivatives for the savory ingredients market. The company aims to enhance its manufacturing capabilities, research and development efforts, and expand its product portfolio.

- August 2024: AB Mauri North America has acquired Omega Yeast Labs LLC. Omega Yeast Labs operates from a 14,000-square-foot facility in Chicago, focusing on research, development, and production, with additional locations across the Midwest. AB Mauri has integrated this acquisition into its AB Biotek division, which specializes in developing specialty yeast solutions for alcoholic beverages.

Global Savory Ingredients Market Report Scope

| Yeast Extracts |

| Hydrolyzed Vegetable Protein (HVP) |

| Hydrolyzed Animal Protein (HAP) |

| Monosodium Glutamate (MSG) |

| Nucleotides (IMP, GMP, AMP) |

| Others |

| Powder |

| Liquid and Paste |

| Synthetic |

| Natural |

| Snacks |

| Soups, Sauces, and Dressings |

| Ready Meals |

| Meat Processing |

| Seasoning Blends |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Yeast Extracts | |

| Hydrolyzed Vegetable Protein (HVP) | ||

| Hydrolyzed Animal Protein (HAP) | ||

| Monosodium Glutamate (MSG) | ||

| Nucleotides (IMP, GMP, AMP) | ||

| Others | ||

| By Form | Powder | |

| Liquid and Paste | ||

| By Origin | Synthetic | |

| Natural | ||

| By Application | Snacks | |

| Soups, Sauces, and Dressings | ||

| Ready Meals | ||

| Meat Processing | ||

| Seasoning Blends | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the savory ingredients market?

The savory ingredients market size stood at USD 10.06 billion in 2026.

Which segment is growing fastest within savory flavors?

Nucleotides lead growth with a projected 7.56% CAGR through 2031.

Why are natural savory ingredients gaining share?

Retailer clean-label mandates and EU disclosure rules favor fermentation-derived yeast extracts over synthetic or acid-hydrolyzed options.

Which region will see the quickest expansion?

Europe is forecast to grow at 7.58% CAGR, driven by upcycled protein adoption and natural flavor regulations.

Page last updated on: