Cereal Ingredients Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

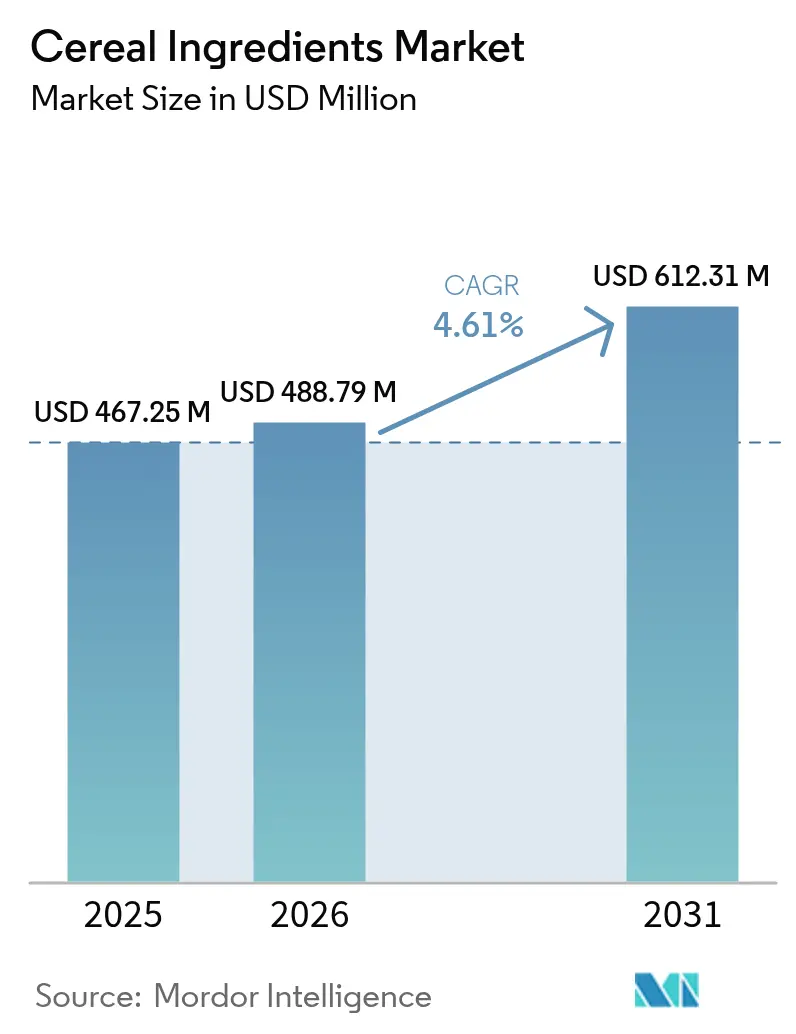

| Market Size (2026) | USD 488.79 Million |

| Market Size (2031) | USD 612.31 Million |

| Growth Rate (2026 - 2031) | 4.61% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cereal Ingredients Market Analysis by Mordor Intelligence

The global cereal ingredients market size in 2026 is estimated at USD 488.79 million, growing from 2025 value of USD 467.25 million with 2031 projections showing USD 612.31 million, growing at 4.61% CAGR over 2026-2031. The growth reflects the industry's response to consumer preferences for functional nutrition and clean-label products. Regulatory requirements for fortified ingredients in infant nutrition and whole-grain consumption have influenced procurement strategies. The market maintains its strength through traditional breakfast applications while expanding into snack food ingredients, as ready-to-eat cereals evolve from breakfast items to portable snacks. Wheat remains the dominant ingredient in the cereal ingredients market due to its extensive use in hot and cold cereals and its suitability for extruded and flaked formats. Oats show the highest growth rate, driven by demand for heart-healthy beta-glucan content and whole-grain, gluten-friendly options. Barley and rice ingredients maintain consistent growth, especially in regions focusing on diverse grain combinations for enhanced nutrition. The alternative grains segment, including millet, sorghum, and ancient grains, represents a specialized category that meets premium product demands and consumer interest in new textures and functional benefits. These changes in ingredient preferences indicate a market shift toward multi-grain formulations that meet dietary guidelines and individual nutrition requirements.

Key Report Takeaways

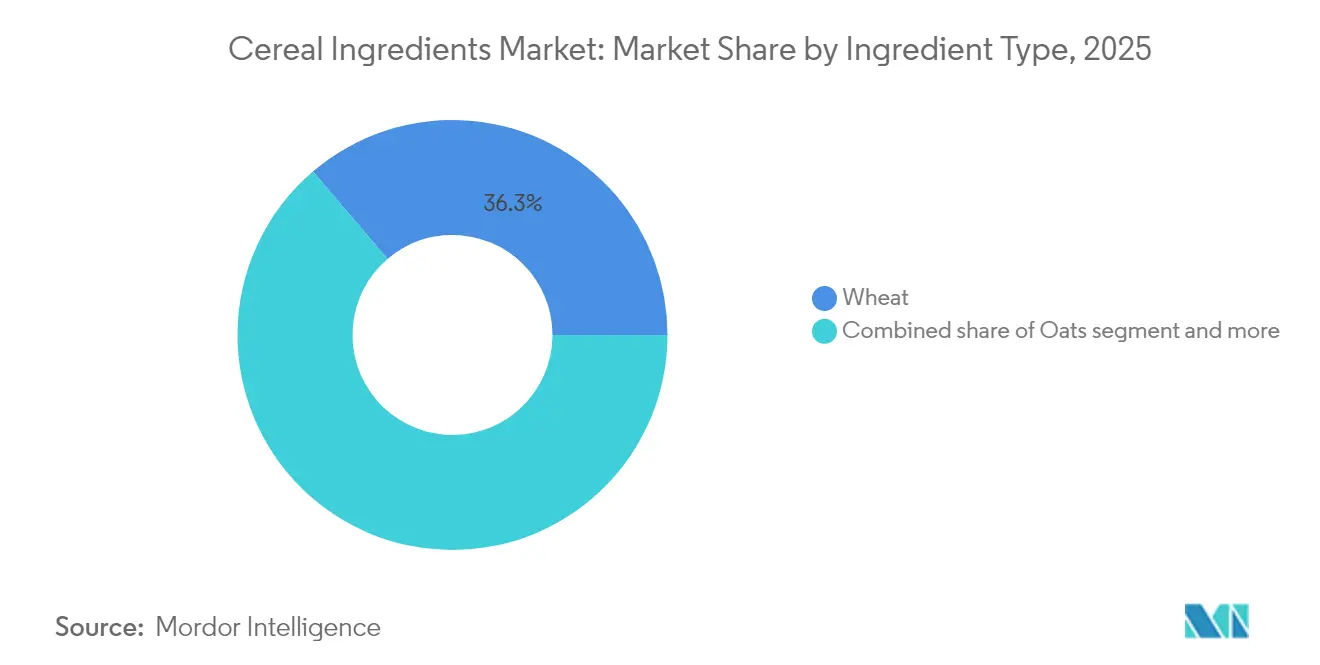

- By ingredient type, wheat held 36.25% of the cereal ingredients market share in 2025, while oats are forecast to lead growth at a 5.66% CAGR through 2031 across global applications.

- By form, flakes captured 29.05% of the cereal ingredients market share in 2025 and are also projected to expand at the highest 5.71% CAGR between 2026 and 2031 worldwide.

- By application, cold cereals commanded 67.90% share of the cereal ingredients market size in 2025, whereas hot cereals are expected to grow fastest at a 5.21% CAGR to 2031.

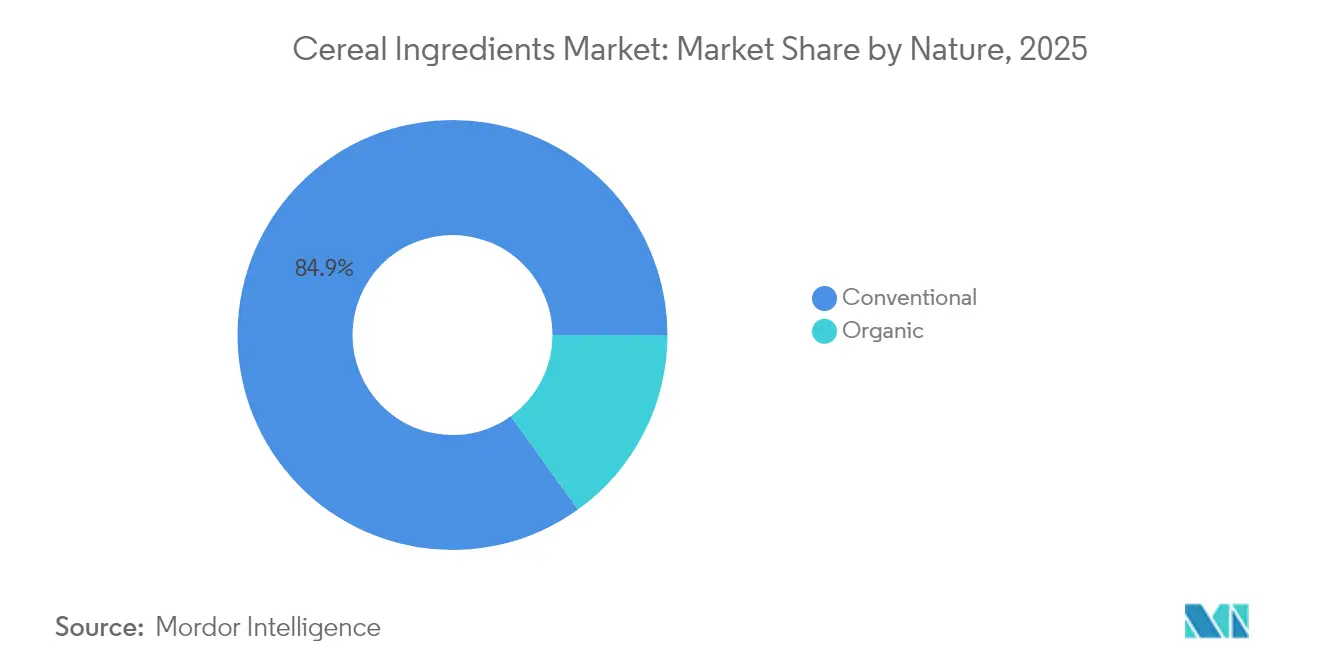

- By nature, the conventional segment dominated with an 84.92% share in 2025; the organic segment is poised for a 5.78% CAGR from 2026 to 2031 across key consuming regions.

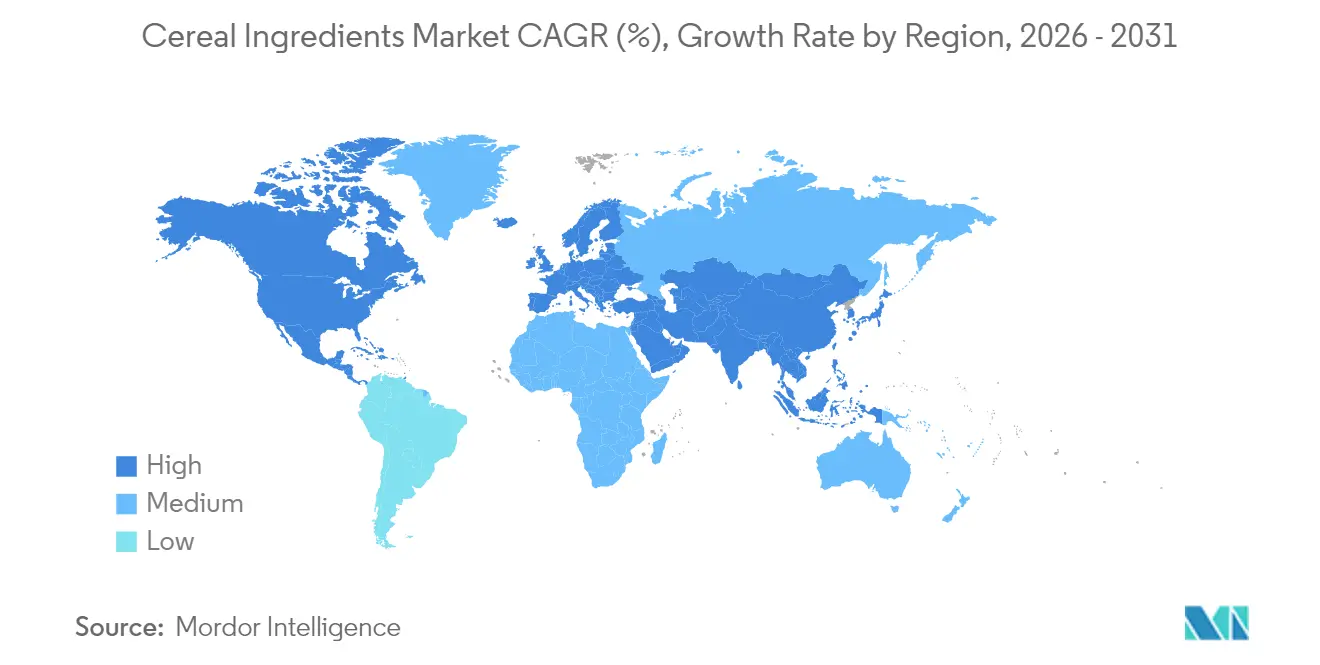

- By geography, North America led with 36.20% of the cereal ingredients market share in 2025, while Asia-Pacific is projected to record the fastest 5.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cereal Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for whole-grain and high fiber products | +1.2% | Global, with strongest uptake in North America and Europe | Medium term (2-4 years) |

| Health awareness boosting consumption of functional breakfast cereals | +0.9% | Global, led by developed markets, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Increased utilization of fortified cereal ingredients in infant nutrition | +0.7% | Global, with regulatory drivers in North America and Europe | Long term (≥ 4 years) |

| Adoption in snack bars, granola, and health mixes | +0.8% | North America and Europe core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Adoption of western-style breakfast habits in emerging economies | +1.1% | Asia-Pacific core, spill-over to Middle East and Africa and Latin America | Long term (≥ 4 years) |

| Growing consumption of cereal based snack food as meal replacement | +0.6% | Global, urbanization-driven in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Whole-Grain and High Fiber Products

As consumers increasingly prioritize preventive health and digestive wellness, demand for whole-grain and high-fiber products has surged, bolstering the cereal ingredients market. With dietary preferences shifting from refined carbohydrates to nutrient-rich alternatives, manufacturers are responding by boosting whole wheat, oats, barley, and multi-grain blends in their cereals. Heightened consumer scrutiny on dietary fiber has led to a rise in cereal ingredients like oat bran and barley flakes, known for their beta-glucans that aid cholesterol management and promote heart health. Consequently, there's a growing appetite for organic and clean-label cereals, where the prominence of whole grains and natural fibers underscores product transparency. According to a 2023 Whole Grains Council report, 38% of American consumers wanted to increase their whole grain bread, rolls, and buns consumption, 27% aimed to eat more whole grain crackers, snacks, rice, and grain sides, and 26% planned to consume more whole grain breakfast cereals [1]Source: Whole Grains Council, "These are the Whole Grain Products that Consumers Want More of," wholegrainscouncil.org.

Health Awareness Boosting Consumption of Functional Breakfast Cereals

Heightened health awareness among global consumers has emerged as a critical driver propelling the demand for functional breakfast cereals, thereby expanding opportunities within the cereal ingredients market. As individuals become more proactive in managing lifestyle-related health conditions such as obesity, high cholesterol, and type 2 diabetes, they are increasingly turning to breakfast cereals formulated with functional benefits. According to the Centers for Disease Control and Prevention (CDC), during 2021-2023, the prevalence of obesity in adults was 40.3%, with no significant differences between men and women. Obesity prevalence was higher in adults ages 40–59 than in those ages 20–39 and 60 and older [2]Source: Centers for Disease Control and Prevention CDC, "Obesity and Severe Obesity Prevalence in Adults: United States, August 2021–August 2023," cdc.gov. As consumers place a premium on preventive health and digestive wellness, the demand for whole-grain and high-fiber products has surged, propelling the growth of the cereal ingredients market. As dietary preferences pivot from refined carbohydrates to nutrient-dense alternatives, manufacturers are amplifying the inclusion of whole wheat, oats, barley, and multi-grain blends in their cereals.

Increased Utilization of Fortified Cereal Ingredients in Infant Nutrition

Food and Drug Administration (FDA) regulations under 21 CFR Part 107 establish stringent nutrient specifications for infant formulas, requiring precise levels of protein (1.8-4.5 grams per 100 kilocalories), vitamins, and minerals, creating a highly regulated market for cereal ingredients used in infant nutrition products [3]Source: Code of Federal Regulations, "107.100 Nutrient specifications," ecfr.gov. This regulatory framework ensures consistent demand for specialized cereal ingredients that meet bioavailability and safety standards far exceeding those required for general food applications. Infant nutrition manufacturers require suppliers to demonstrate not only nutritional compliance but also supply chain traceability and contamination control protocols that align with Food and Drug Administration (FDA) good manufacturing practices. The segment's growth potential extends beyond traditional formula applications into organic baby food categories, where cereal ingredients serve as texture modifiers and nutritional enhancers in pureed products.

Adoption in Snack Bars, Granola, and Health Mixes

Cereal ingredients are moving beyond their traditional role in breakfast, driving significant market growth. With a growing emphasis on convenience and nutrition, consumers are turning to cereal grains and their derivatives in snack bars, granola clusters, and health mixes. These options not only provide portability and portion control but also promise benefits like sustained energy, digestive wellness, and heart health. Manufacturers are tapping into a variety of cereal ingredients, from whole oats and wheat crisps to puffed barley and multigrain blends. This innovation in snack applications not only emphasizes a clean-label and natural approach but also caters to the increasing demand for protein and fiber enrichment. This momentum is reflected in consumer behavior trends documented by Glanbia Nutritionals, which reported that nearly one in four consumers, or 24%, regularly consumed granola, cereal, or snack bars in 2024 [4]Source: Glanbia Nutritionals, "What Americans Are Snacking On Today," glanbianutritionals.com. This strong uptake highlights how cereal ingredients are increasingly being utilized in on-the-go formats that extend well beyond breakfast, solidifying their place in the broader snacking and health foods landscape and opening new avenues for ingredient processors to develop versatile, value-added grain solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating prices of cereal crop due to climate impact | -1.4% | Global, with acute effects in major producing regions | Short term (≤ 2 years) |

| Rising consumer concern over carbohydrate and sugar content | -0.8% | Developed markets primarily, spreading to urban Asia-Pacific | Medium term (2-4 years) |

| Allergenic potential of gluten-containing cereal ingredients | -0.5% | Global, with strongest impact in North America and Europe | Long term (≥ 4 years) |

| Digestive sensitivities linked to certain whole-grain fibers | -0.3% | Developed markets with high whole grain consumption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fluctuating Prices of Cereal Crop Due to Climate Impact

Climate-related disruptions are causing significant challenges in the cereal ingredients market, primarily due to the volatility of cereal crop prices. Essential cereal crops, including wheat, oats, barley, and corn, are increasingly affected by unpredictable global weather patterns such as droughts, floods, and heat waves. These fluctuations lead to sudden increases in raw material costs and create uncertainties in supply for processors of cereal ingredients. Such price fluctuations ripple through the entire value chain, forcing manufacturers to either absorb the heightened costs or pass them onto consumers. This shift could diminish the demand for premium and specialty cereal products. Moreover, climate variability not only affects planting decisions and crop quality but also harvest timing, making it challenging to maintain consistent ingredient specifications. For ingredient buyers and food manufacturers, the challenge intensifies as they strive to meet specific certifications like non-GMO, organic, or gluten-free while navigating climate-induced supply variations. Consequently, climate change stands out as a dual-edged sword, posing both environmental and economic challenges to the growth of the cereal ingredients market by disrupting supply chains and leading to unpredictable cost surges.

Rising Consumer Concern Over Carbohydrate and Sugar Content

The breakfast cereal industry's experience with declining sales despite reformulation efforts illustrates how consumer concerns about carbohydrate content extend beyond simple sugar reduction to fundamental questions about grain-based products' role in healthy diets. This market challenge affects cereal ingredient suppliers, who must demonstrate that their products deliver functional nutrition benefits that justify the carbohydrate content in finished foods. The growing popularity of low-carbohydrate and ketogenic diets particularly impacts traditional cereal applications, requiring ingredient suppliers to develop specialized products that maintain functional properties while reducing overall carbohydrate density. In response, suppliers invest in processing technologies that concentrate protein and fiber content while reducing starch levels, creating premium ingredient categories that command higher prices but serve smaller market segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Oats Drive Premium Positioning

Wheat commands 36.25% market share in 2025, reflecting its versatility across applications from breakfast cereals to snack bars, while oats emerge as the fastest-growing ingredient type at 5.66% CAGR through 2031. The oats segment benefits from regulatory support, including Food and Drug Administration (FDA)-approved health claims for cholesterol reduction, which enables food manufacturers to command premium pricing for oat-containing products. Barley maintains steady demand in traditional applications but faces growth constraints due to gluten content concerns, while rice ingredients gain traction in gluten-free formulations targeting celiac and gluten-sensitive consumers.

The "Others" category, encompassing ancient grains like quinoa and amaranth, experiences robust growth as manufacturers seek differentiation through heritage varieties that appeal to consumers interested in nutritional diversity and sustainable agriculture practices. This segmentation shift reflects broader consumer trends toward functional ingredients that deliver measurable health benefits rather than simply serving as commodity carbohydrate sources in finished products.

By Form: Flakes Dominate Through Processing Innovation

Flakes represent both the largest segment at 29.05% market share in 2025 and the fastest-growing form at 5.71% CAGR through 2031, demonstrating how established processing technologies continue to evolve to meet changing consumer preferences. The flake format's success stems from its optimal balance of texture, nutritional retention, and manufacturing efficiency, enabling food producers to create products that meet consumer expectations for familiar eating experiences while incorporating functional ingredients. Puff forms serve specialized applications in children's cereals and snack products, while grit forms find primary use in hot cereal applications and as texture modifiers in baked goods.

The flake segment's growth acceleration reflects processing innovations that preserve nutritional integrity while enhancing flavor and texture characteristics that consumers associate with premium products. Manufacturers increasingly specify flaked ingredients for their ability to maintain structural integrity during mixing and packaging processes, reducing waste and improving finished product consistency. The "Others" category includes specialized forms like clusters and crisps that serve niche applications in granola and snack bar manufacturing, where unique textures command premium pricing but require specialized processing equipment and expertise that limit market entry for smaller suppliers.

By Nature: Organic Segment Commands Growth Premium

Conventional cereal ingredients maintain 84.92% market share in 2025, reflecting cost considerations and supply chain complexity that favor established production methods, while organic ingredients achieve 5.78% CAGR through 2031 as consumer willingness to pay premiums for sustainability credentials reshapes procurement priorities. The organic segment's growth trajectory reflects broader consumer trends toward transparency and environmental responsibility, with food manufacturers increasingly specifying organic ingredients to support clean-label positioning and premium pricing strategies. Organic certification requirements create supply chain barriers that limit competition while enabling certified suppliers to command significant price premiums over conventional alternatives.

The organic segment's expansion faces constraints from limited certified farmland and processing capacity, creating opportunities for suppliers who invest in organic certification and specialized handling systems that prevent cross-contamination with conventional products. Food manufacturers increasingly view organic cereal ingredients as strategic differentiators that justify premium pricing in competitive categories, driving demand growth that exceeds overall market expansion rates.

By Application: Cold Cereals Transition to Snacking

Cold cereals dominate the market with 67.90% of application demand in 2025, while hot cereals demonstrate stronger growth potential with a 5.21% CAGR through 2031. This shift reflects evolving consumption patterns as traditional breakfast occasions merge with snacking and meal replacement trends. The cold cereal segment maintains its market leadership due to established consumer preferences and distribution networks. However, growth faces limitations in developed markets where consumers increasingly prefer portable and protein-rich breakfast alternatives. Hot cereals gain market share through their health-focused positioning and customization options, allowing consumers to control nutritional content and flavor preferences.

Ready-to-eat cereals continue to expand beyond breakfast into snacking occasions, prompting manufacturers to develop convenient packaging formats and enhanced nutritional profiles. This market evolution creates opportunities for ingredient suppliers to develop specialized formulations that preserve texture and flavor in portable formats while delivering nutritional benefits. The increasing demand for cereal-based meal replacements drives the need for ingredients that provide sustained energy and satiety.

Geography Analysis

North America leads the cereal ingredients market with a 36.20% share in 2025, supported by established food processing infrastructure and regulatory frameworks that favor fortified ingredients, yet faces growth constraints from declining breakfast cereal consumption and increasing competition from alternative protein sources. The region's mature market dynamics create opportunities for suppliers who can develop specialized ingredients for emerging applications like plant-based meat alternatives and functional snack products that leverage cereal proteins and fibers for texture and nutritional enhancement.

Asia-Pacific emerges as the fastest-growing region at 5.89% CAGR through 2031, driven by urbanization patterns where traditional rice-based breakfast habits give way to Western-style convenience foods, with India and Southeast Asia projected to account for 31% of global agricultural consumption growth by 2033. This demographic shift creates substantial opportunities for cereal ingredient suppliers who can adapt their products to local taste preferences while maintaining the convenience and nutritional benefits that drive adoption of Western breakfast formats.

Europe maintains steady demand supported by regulatory frameworks that favor whole grain consumption and organic ingredients, while the Middle East and Africa represent emerging opportunities where urbanization and rising disposable incomes drive the adoption of processed breakfast products. South America shows potential for growth as economic development and urbanization create demand for processed food products, though political and economic instability in key markets creates challenges for suppliers seeking to establish long-term supply relationships and production facilities in the region.

Regulatory Landscape

Regulation for cereal ingredients is shaped by food additive specifications, requirements for vulnerable populations (infant and young-child foods), and rules governing nutrition and health claims for grain-derived components. In the United States, the FDA framework for infant formula under 21 CFR Part 107 sets tight nutrient and quality specifications, shaping procurement toward suppliers that can demonstrate traceability, contaminant control, and consistent functional performance for cereal-derived ingredients used in infant nutrition applications.

In Europe, 2026 regulatory actions tightened technical specifications for certain additives used in foods for vulnerable populations, raising the compliance bar around purity specifications and maximum levels that affect formulation choices. These changes influence supplier qualification for cereal-based products that rely on stabilizers and thickeners in sensitive-use categories. Across key emerging markets, authorities have continued to update additive permissions and category-specific requirements, including early-life nutrition, which increases the need for global suppliers to manage region-by-region specifications and documentation for cereal ingredient sales into multinational food manufacturing programs.

Value Chain Analysis

The cereal ingredients value chain starts with upstream grain cultivation (wheat, oats, barley, rice, and alternative grains), followed by collection and storage, cleaning and grading, and milling and fractionation (flour, grits). It then moves into further processing, including flaking, extrusion, and blending, to deliver standardized ingredient formats. Midstream participants include grain millers and specialty processors that provide functional specifications (particle size, water absorption, beta-glucan content). This stage is supported by testing labs, certification bodies (organic, non-GMO, gluten-free), and packaging providers, before ingredients are distributed through ingredient distributors or supplied direct to manufacturers for cold cereals, hot cereals, snack bars, and health mixes.

Specialized milling, flaking, and extrusion also concentrate capital requirements, creating structural bottlenecks. Identity-preserved programs add documentation and segregation requirements, which increases procurement complexity for organic and non-GMO cereal ingredients. In 2025-2026, more suppliers and downstream brands have been formalizing farm-to-factory programs tied to regenerative agriculture and direct grower relationships, improving traceability and continuity of supply, while tightening coordination between farms, elevators, processors, and brand owners.

Competitive Landscape

The cereal ingredients market has a moderately fragmented competitive landscape. Regional millers and specialty ingredient companies, including Bunge Global SA, Ingredion Incorporated, Grain Millers, and Groupe Limagrain Holding, contribute significantly to market competition. These companies offer organic, non-GMO, gluten-free, and ancient grain products, responding to consumer demand for clean-label and sustainable options. Their competitive advantages include operational flexibility, strong local grower relationships, and quick adaptation to dietary trends and regulations, enabling them to serve premium market segments and support cereal manufacturers' brand differentiation.

Large agricultural processors like Archer-Daniels-Midland Company and Cargill, Incorporated, also maintain market leadership through their scale advantages in procurement and processing. Specialized ingredient suppliers and regional millers serve local and niche markets, with smaller players focusing on specialized segments such as organic certification, ancient grain varieties, and functional ingredients that command premium pricing within targeted market segments. Strategic partnerships, certifications, and technological advancements drive market competition by improving traceability, nutritional profiles, and product development.

These innovations cater to both traditional consumption and on-the-go applications. The increasing focus on health-conscious consumption is expected to accelerate innovation in the cereal ingredients market. Companies are developing new grain-based solutions that combine functionality, taste, and sustainability, establishing cereal ingredients as a dynamic segment in the global food industry. Competitors are racing to deliver novel grain-based solutions that balance functionality, taste, and sustainability, solidifying cereal ingredients as a dynamic and evolving sector within the global food industry.

Cereal Ingredients Industry Leaders

-

Archer-Daniels-Midland Company

-

Cargill, Incorporated

-

Bunge Global SA

-

Ingredion Incorporated

-

Groupe Limagrain Holding

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product development whitespace is expanding where cereal ingredients deliver multiple functions at once, such as fiber enrichment plus texturization for snack bars, granola clusters, and portable cereal formats, and where ingredient processing can support clean-label positioning without adding long ingredient decks. Oats-based ingredients remain central to premiumization due to beta-glucan positioning and whole-grain demand translating into higher-value formulations, while gluten-friendly rice ingredients and multi-grain blends support differentiation for manufacturers addressing allergen and digestive-sensitivity concerns.

Emerging-market capacity buildouts and partnerships are also creating more localized supply options for value-added cereal-derived ingredients, especially in India. Investment activity there has targeted advanced starch derivatives and specialty ingredient production alongside base milling. Recent transactions and expansions in Indian grain processing, including acquisitions of wet milling assets and new capacity for derivatives such as maltodextrin and liquid glucose, show a push into higher-margin ingredient systems that feed into cereal-adjacent applications (confectionery, dairy, and infant nutrition). At the same time, regenerative agriculture declarations and brand-led sourcing programs are increasing demand for documented, identity-preserved grain inputs, creating room for ingredient suppliers that can execute traceability, certification, and consistent specifications at scale.

Recent Industry Developments

- May 2026: Cargill announced the commercial launch of NextCoa, a cocoa-free confectionery alternative, in North America in partnership with Voyage Foods. The launch expands Cargill's specialty ingredient offering for confectionery and frames alternative ingredient systems as a lever to manage commodity and supply risks in adjacent sweet applications that often include cereal-based components.

- March 2025: Cargill launched a new corn milling plant in Gwalior, Madhya Pradesh, India, in partnership with Saatvik Agro Processors. The added processing footprint strengthens regional availability of starch derivatives used across confectionery, dairy, and infant formula, improving lead times and enabling more localized sourcing for manufacturers.

- December 2024: Richardson International Ltd. announced an expansion of its oat mill and processing plant in South Sioux City, Nebraska, to double the facility's granola packaging capabilities. Higher packaging throughput supports larger-volume supply of oat-based formats used in cereals and snack applications, improving responsiveness to customer specifications and private-label programs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers cereal-based ingredients made from cereals such as wheat, corn, rice, oats, and barley that are processed into forms used by food makers, mainly for hot and cold cereal-style products and adjacent grain-based foods.

Scope exclusions: it does not count finished packaged breakfast cereal brands at retail value, and it also excludes non-cereal inputs such as dairy, nuts, and fruit that can be blended into final products.

Segmentation Overview

-

By Ingredient Type

- Wheat

- Barley

- Rice

- Oats

- Others

-

By Form

- Puff

- Grit

- Flake

- Others

-

By Nature

- Organic

- Conventional

-

By Application

- Hot Cereals

- Cold Cereals

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- France

- United Kingdom

- Spain

- Netherlands

- Italy

- Sweden

- Poland

- Belgium

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Indonesia

- Thailand

- Singapore

- Rest of Asia Pacific

-

South America

- Brazil

- Argentina

- Chile

- Colombia

- Peru

- Rest of South America

-

Middle East and Africa

- United Arab Emirates

- South Africa

- Nigeria

- Saudi Arabia

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries, list the ingredient forms that are actually traded, and understand where demand is coming from across regions. We relied on public sources such as USDA and Economic Research Service data, US Census trade statistics, Eurostat, FAOSTAT, and Codex Alimentarius and related national food safety guidance for product definitions and labeling references.

To keep assumptions realistic, we also reviewed company annual reports and investor presentations for capacity and category commentary, association websites for milling and grain processing indicators, and reputable press for expansion announcements. Where one dataset was not enough, a paid subscription database was used only for company financials and news tracking, along with a patent database to spot processing and formulation shifts that can change ingredient mix over time. These are illustrative sources only, and many other references were used for cross-checking, validation, and clarification during the work.

Primary Interviews and Surveys

Primary interviews and surveys were used to confirm how ingredient suppliers and buyers define cereal ingredients, how pricing is typically set (contracted versus spot), and what the usual conversion factors look like from grain input to ingredient output. We spoke with stakeholders across ingredient processing, food manufacturing, distribution, and procurement, and coverage was balanced across major consuming regions so assumptions on volumes, mix, and pricing could be stress-tested before finalizing totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 20% | APAC: 38% |

| Mid tier: 44% | Functional/Unit leaders: 37% | EMEA: 36% |

| Smaller Players: 20% | Managers: 43% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the demand pool from grain processing and usage signals, then applies conversion logic into ingredient forms used in cereal and related grain-based foods. After the regional demand pools were set, we ran selective bottom-up approximations using sampled supplier revenues, channel checks, and volume by average selling price (ASP) to validate totals and adjust where the two views did not line up.

Key inputs used in the model include reported cereal grain availability and processing volumes, mix split by ingredient form (flakes, puffs, grits, and similar), the organic versus conventional share, application mix across hot and cold cereal formats, and regional trade flows that indicate cross-border supply. Pricing was handled through a repeatable ASP method that ties raw material movement to processed ingredient pricing with lag assumptions, and it was checked in interviews so it reflects how contracts renew in practice.

For forecasting, scenario analysis was used with a small set of drivers, such as grain price outlook, demand growth in ready-to-eat and convenient grain-based foods, and expected capacity additions. The scenario path was reviewed with industry respondents to keep it grounded. Where bottom-up information was missing for smaller countries or niche forms, gaps were filled using proxy mix ratios from comparable markets and then normalized back to the regional totals.

Data Validation & Update Cycle

Outputs were triangulated across multiple angles, including volume signals, trade direction, and price progression, so single-source bias does not drive the final number. Outliers were flagged through variance checks at country and regional levels, then reviewed in a second analyst pass before sign-off.

The report is refreshed annually, and interim updates are triggered when material events occur, such as major capacity moves or sharp commodity-linked price changes that flow into ingredient ASPs. Before delivery, we do a final review pass so the model reflects the most recent publicly available signals and any new primary feedback.

Mordor Intelligence's Cereal Ingredients Market Estimate Compared With Other Published Estimates

Published market sizes for cereal ingredients can differ even when the topic name is the same, because the year used, the currency conversion timing, and the way pricing is averaged can change the total. Differences also come from what is counted as an ingredient market versus a finished food market, plus whether volumes are anchored to grain processing reality or to broader packaged-food revenue assumptions.

A refresh-led gap is common in this space because grain-linked ingredient pricing can move within a year, and some estimates smooth ASPs too aggressively or convert currencies at a single point in time. By re-checking ASP steps during the update cycle, applying consistent average-year currency timing, and re-contacting sources when volume and price signals diverge, Mordor Intelligence keeps the 2026 value closer to what suppliers and buyers say is being transacted in cereal ingredients.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 488.79 M (2026) | |

| Global Consultancy A | USD 457.53 M (2024) | Uses an earlier base year and may apply a broad average price across forms, which can understate value when ingredient mix shifts toward higher priced processed formats. |

| Industry Publisher B | USD 452.53 M (2024) | Keeps a 2024 base and likely relies more on standardized growth rates with limited re-validation of currency timing and contract lag effects, which can move totals in commodity-sensitive ingredients. |

The spread in the table is mainly explained by year choice and the way ASP and conversion timing are treated, rather than a real disagreement on demand direction. When scope is kept at ingredient-level revenues and the price logic is checked against how contracts reset, the resulting market size stays traceable to clear volume and mix inputs and can be repeated in future refreshes.

Key Questions Answered in the Report

What is the current value of the cereal ingredients market?

The cereal ingredients market is valued at USD 488.79 million in 2026 and is projected to reach USD 612.31 million by 2031.

Which ingredient type is growing fastest?

Oats post the highest 5.66% CAGR through 2031, fueled by beta-glucan health claims and broader beverage applications.

Why are flakes the leading form in the market?

Flakes balance familiar texture with efficient processing, giving them 29.05% share in 2025 and the swiftest 5.71% growth rate among forms.

Which region will drive future expansion?

Asia-Pacific is forecast to grow at 5.89% CAGR, propelled by urbanization and the adoption of Western-style convenience breakfasts.

Page last updated on: