Germany Formwork Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

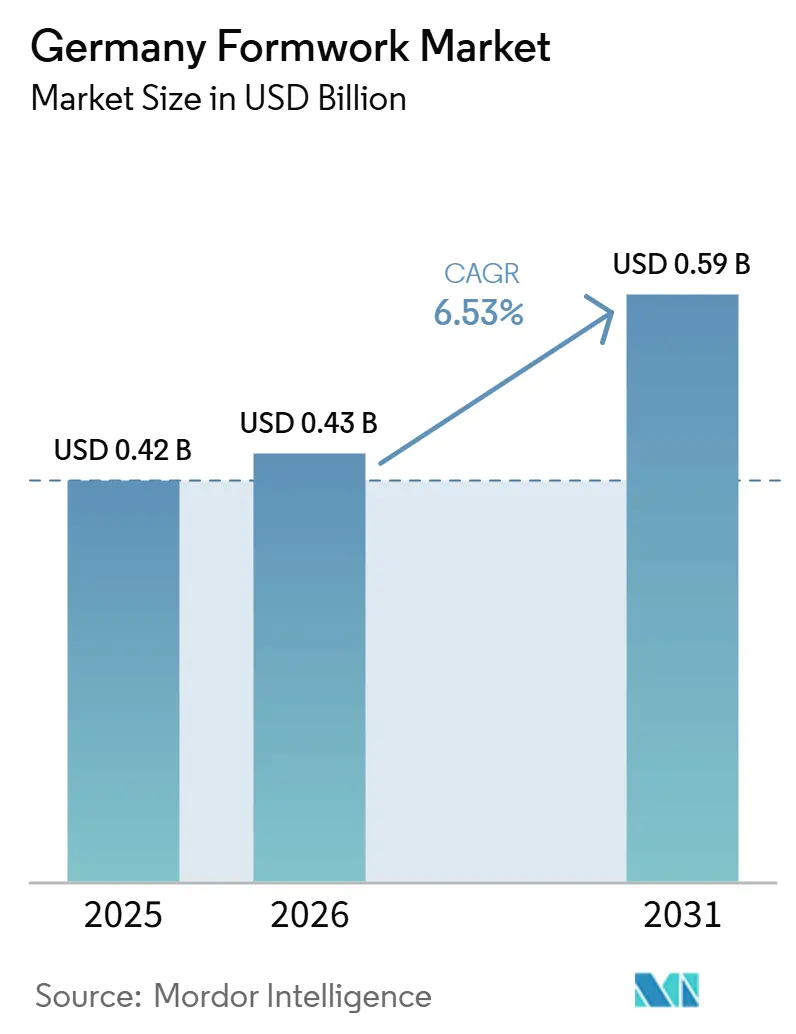

| Base Year Market Size (2025) | USD 0.42 Billion |

| Market Size (2026) | USD 0.43 Billion |

| Market Size (2031) | USD 0.59 Billion |

| Growth Rate (2026 - 2031) | 6.53% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Formwork Market Analysis by Mordor Intelligence

The Germany Formwork Market size is projected to be USD 0.42 billion in 2025, USD 0.43 billion in 2026, and reach USD 0.59 billion by 2031, growing at a CAGR of 6.53% from 2026 to 2031.

Demand is being shaped by a construction pipeline that is recovering first in large urban centers and infrastructure corridors, which gives the Germany formwork market a steadier path than the broader building cycle suggests. Public rail and transport commitments are giving suppliers a clearer base load for fleet planning, engineering support, and capacity allocation across civil works that require repeated concrete pours. Labor scarcity is also changing buying behavior because contractors increasingly value lighter systems, reusable modules, and climbing solutions that reduce crew pressure and shorten installation time. Retrofit and modernization activities are widening the demand base because structural upgrades to existing assets create concrete work outside the normal new-build cycle. Competition remains moderately consolidated, and suppliers that combine rental reach, engineered systems, product innovation, and faster planning support are better placed to capture the next stage of growth in the Germany formwork market.

Key Report Takeaways

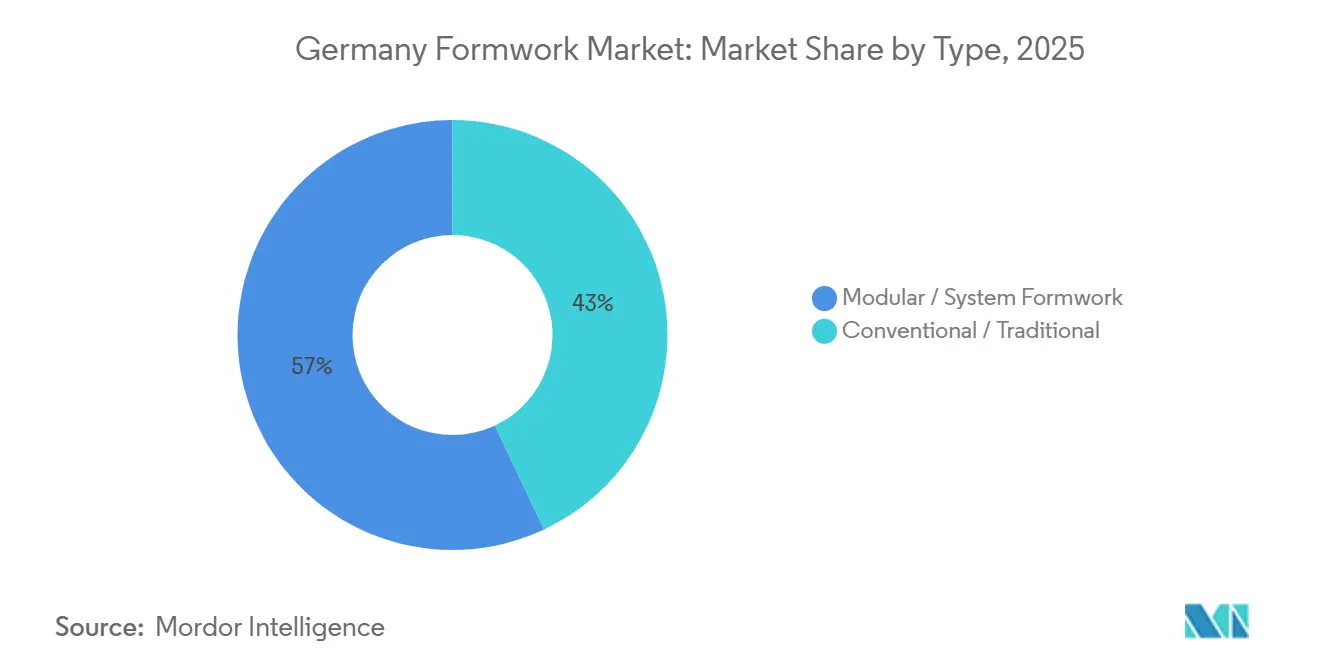

- By type, modular / system formwork held 57% of the Germany formwork market size in 2025, while the same segment is forecast to grow at 6.90% through 2031.

- By configuration, static formwork accounted for 41% of revenue in 2025, while climbing systems posted the highest projected CAGR of 7.80% through 2031.

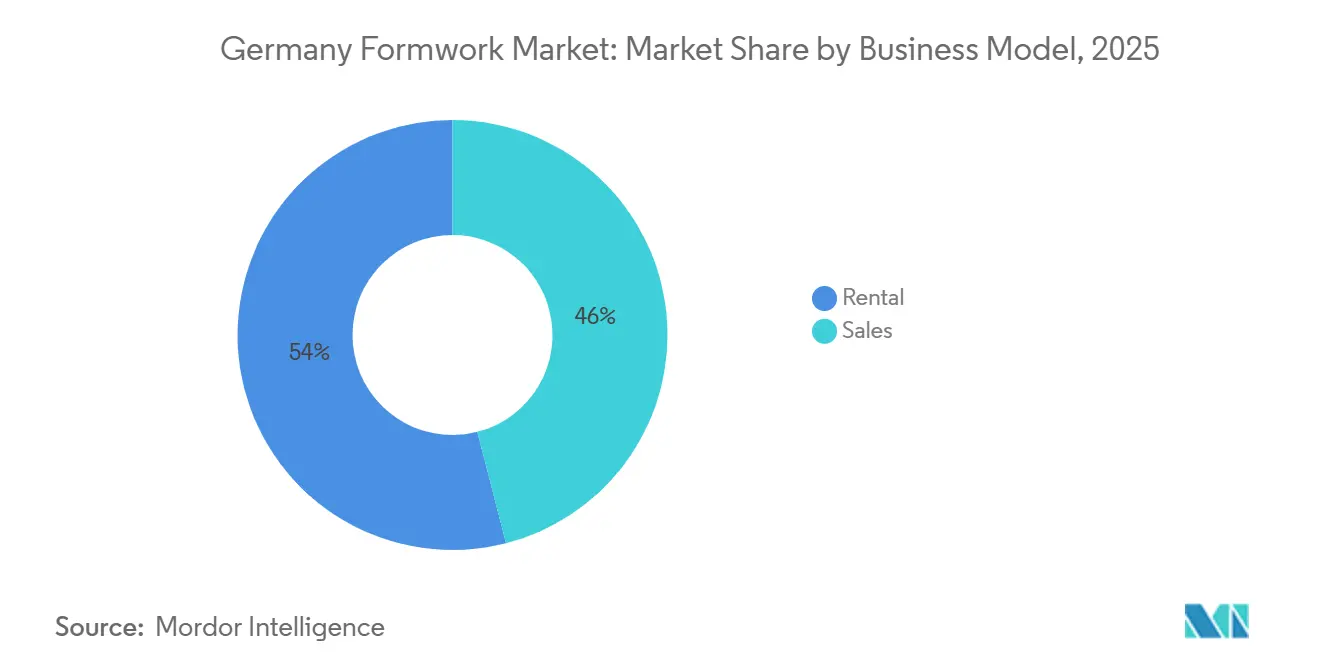

- By business model, rental held 54% of the Germany formwork market share in 2025, while rental also posted the fastest projected CAGR at 6.96% through 2031.

- By sector, infrastructure accounted for 33% of revenue in 2025 and recorded the highest projected CAGR of 7.20% through 2031.

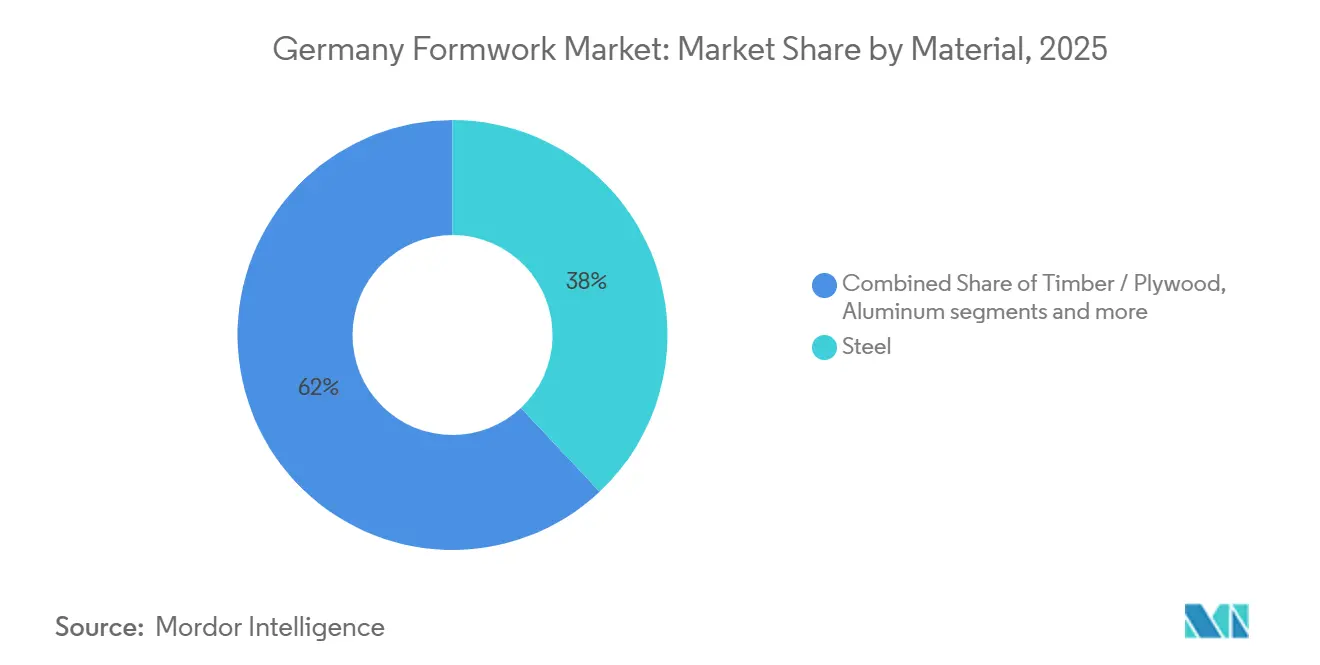

- By material, steel held 38% of revenue in 2025, while aluminum is forecast to expand at a 7.10% CAGR through 2031.

- By city, Berlin held 20% of revenue in 2025, while Leipzig recorded the highest projected CAGR at 7.99% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Formwork Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Public Infrastructure Stimulus and Rail Modernization | +1.8% | National, strongest in NRW, Bavaria, and the Hamburg-Berlin axis | Medium term (2-4 years) |

| Housing Shortage and Multi-Family Construction Recovery | +1.4% | National, concentrated in Berlin, Munich, Frankfurt, and Leipzig | Short term (≤ 2 years) |

| Shift Toward Reusable and Low-Waste Formwork Systems | +0.9% | National | Medium term (2-4 years) |

| Labor Scarcity Accelerating Productivity-Focused Formwork Adoption | +0.8% | National, most acute in urban construction centers | Medium term (2-4 years) |

| Renovation, Retrofit, and Energy-Efficiency Works Expanding Formwork Demand | +0.7% | National, with early gains in major metropolitan areas | Long term (≥ 4 years) |

| Growth of Complex Urban Projects Requiring Climbing and Slipform Solutions | +0.6% | Berlin, Munich, Frankfurt, and Leipzig | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Public Infrastructure Stimulus and Rail Modernization

Public infrastructure investment is the strongest medium-term demand driver for the Germany formwork market because rail, road, and water projects create long-duration concrete packages. Germany committed EUR 107 billion (USD 116.6 billion) for rail infrastructure through 2029, and total infrastructure spending across rail, roads, and waterways reached EUR 166 billion (USD 180.9 billion)[1]Zeit Online Redaktion, “Schiene Bekommt Bis 2029 Mehr Als 100 Milliarden Euro,” Die Zeit, zeit.de. Deutsche Bahn’s 2026 investment plan exceeded EUR 23 billion (USD 25.3 billion) for rail network maintenance and modernization, which supports ongoing demand for bridge abutments, retaining walls, station works, and tunnel portals. This matters for the Germany formwork market because those applications usually favor durable steel systems, climbing configurations, and high-utilization rental fleets rather than ad hoc site-built solutions. DB InfraGO’s corridor program now runs through 2036, providing suppliers with unusual visibility into future demand and supporting investment in fleet capacity and service networks. The Bundestag’s approval of additional railway projects in May 2026 extends that pipeline further and strengthens the medium-term outlook for the Germany formwork market.

Housing Shortage and Multi-Family Construction Recovery

Germany’s housing shortage keeps multi-family building relevant for the Germany formwork market even when the wider construction cycle remains uneven. Demand is concentrated in major cities where housing pressure is strongest and where larger residential blocks require repeated slab, wall, and core concrete work. The large stock of permitted and partially advanced housing projects provides formwork suppliers with a visible pool of work that is already more advanced than early-stage land planning. Public support for social housing also adds a demand floor that helps protect the Germany formwork market from a fully private-sector slowdown. The practical effect is that modular wall systems, slab systems, and reusable panels remain well aligned with the kinds of projects that are most likely to move first. This keeps residential demand important for the Germany formwork market even if growth remains stronger in infrastructure and major urban projects.

Shift Toward Reusable and Low-Waste Formwork Systems

The Germany formwork market is moving further toward reusable systems because contractors are under pressure to cut waste, improve cycle times, and maintain consistent concrete quality. That shift supports system formwork over one-off timber solutions in projects where repetition, dimensional control, and cleaner surfaces matter. Compliance expectations for concrete execution also favor engineered systems because they are easier to standardize across different crews and job sites. MEVA’s Alu-Platform reflects that direction because it was designed for compatibility across several formwork systems and for crane-free handling, which improves logistics and site efficiency. The longer reuse life of system formwork also improves the economics of rental fleets, strengthening larger suppliers that can spread fleet costs across many projects. Over time, this creates stickier customer relationships and gives the Germany formwork market a stronger tilt toward modern fleet-based business models.

Labor Scarcity Accelerating Productivity-Focused Formwork Adoption

Labor scarcity is reshaping product choice across the Germany formwork market because contractors increasingly need systems that can be installed with fewer workers and less crane time. In January 2026, 30.4% of construction firms reported unfilled skilled worker positions, which shows that labor pressure remained significant even in a softer macro environment. The Organisation for Economic Co-operation and Development (OECD) also identified the shortage of qualified construction workers as a material bottleneck in infrastructure delivery, making labor-saving systems more valuable than before. PASCHAL’s NeoR aluminum panel and Hunnebeck’s SCF 60 self-climbing system both respond to this need by reducing handling effort and limiting dependence on repeated crane lifts. This means demand in the Germany formwork market is increasingly linked not only to project volume but also to the need for productivity tools at the jobsite. Suppliers that build crew reduction into product design are therefore better positioned to gain share in the Germany formwork market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Engineered Formwork Systems | -1.2% | National, most pronounced among SME contractors | Medium term (2-4 years) |

| Weak Residential New-Build Starts in Smaller Municipalities | -0.9% | Rural and secondary cities across non-metropolitan Germany | Short term (≤ 2 years) |

| Project Delays From Permitting, Financing, and Procurement Complexity | -0.8% | National | Medium term (2-4 years) |

| High Logistics Burden and Return-Handling Costs for Rental Equipment | -0.5% | National, most acute in geographically dispersed smaller projects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Engineered Formwork Systems

The high purchase cost of engineered systems still limits faster adoption across the Germany formwork market, especially among smaller contractors. Many Small- and Medium-Sized Enterprise builders can see the labor and quality benefits of system formwork. Still, the financial case is less attractive when a project offers only a short reuse window. This is particularly relevant in small residential and local renovation work where job sizes are modest, and project repetition is limited. Financing conditions have improved from their worst levels, yet many contractors still prefer to avoid large balance-sheet commitments for owned fleets. That is one reason rental continues to hold a strong position in the Germany formwork market, even though rental also adds transport, planning, and return-handling costs. The result is a market where advanced systems gain ground, but adoption still depends heavily on access to rental networks and project scale.

Weak Residential New-Build Starts in Smaller Municipalities

Weak residential starts outside the main metropolitan clusters still restrain the Germany formwork market because project economics are less favorable in smaller cities and rural areas. Recovery remains uneven, with large cities drawing more capital and stronger demand while lower-rent locations continue to struggle with viability. This affects the Germany formwork market in a practical way because low project density makes it harder for suppliers to deploy rental fleets efficiently across dispersed sites. When fleet density falls, transport and handling costs rise, which weakens the value proposition of reusable systems for smaller projects. Conventional solutions can remain competitive in those locations because they avoid some of the logistics burden associated with modern fleet operations. As a result, demand growth in the Germany formwork market is still stronger in urban and infrastructure corridors than in smaller municipal housing markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Engineered Systems Displace Conventional Across Project Categories

Modular / system formwork held 57% of Germany formwork market share in 2025, and the segment is projected to expand at a 6.90% CAGR through 2031. That position shows that engineered solutions are no longer limited to only the largest projects in the Germany formwork market. Contractors increasingly prefer reusable systems because they support faster cycles, more consistent dimensional control, and lower labor input per pour. The same preference is visible in both residential blocks and major infrastructure jobs where repeatability and schedule certainty matter. PERI's January 2025 joint venture with DataB, which established DataForm.Work GmbH, is a clear example of how leading suppliers are strengthening the link between digital planning and fabrication speed.[2]PERI GmbH, “Milestone in the Field of Digital Construction – PERI and DataB Establish Joint Venture,” PERI, peri.com.

That move matters because faster model-to-production conversion makes engineered formwork easier to deploy on bespoke pours that once favored more manual methods. In the Germany formwork market, this reduces the practical advantage that conventional timber solutions held in irregular applications. Conventional formwork still serves non-standard pours, short reuse projects, and rural jobs where site-sourced materials remain economical. It also remains relevant where transport distances or low repetition weaken the economics of full system deployment. Even so, the broader direction of the Germany formwork market remains clear because higher complexity, tighter labor availability, and stronger quality expectations continue to shift demand toward modular and system formats.

By Configuration: Self-Climbing Systems Gain Momentum in High-Rise and Energy Works

Climbing systems are the fastest-growing configuration in the Germany formwork market, with a projected 7.80% CAGR from 2026 to 2031. Their growth reflects the types of work now driving the market, including high-rise housing, energy structures, retaining walls, and vertically repetitive civil works. These applications reward systems that can move upward safely and efficiently without relying on heavy crane usage at every stage. Hunnebeck’s SCF 60 self-climbing system fits that requirement because it uses hydraulic self-climbing in addition to crane operation and supports flexible platform expansion with standard components. For the Germany formwork market, that lowers labor pressure and supports schedule control on projects where vertical progress is critical.

Static formwork still held the largest share at 41% in 2025, as slab and low-rise wall work remain widespread across warehousing, logistics, and residential construction. This gives the Germany formwork market a broad installed base that still depends on more conventional horizontal applications. Slipform and tunnel systems remain important in rail and civil engineering because they suit continuous or highly repetitive structural work. DB InfraGO’s corridor program has already entered an intensive construction phase on key routes, which supports current demand for tunnel-related and retaining-wall formwork applications. The result is a configuration mix where static systems still anchor volume, while climbing solutions define the growth edge of the Germany formwork market.

By Business Model: Rental as Structural Market Architecture

Rental accounted for 54% share of the Germany formwork market size in 2025, and the segment is projected to grow at a 6.96% CAGR through 2031. That lead shows that rental is a structural feature of the Germany formwork market rather than a short-term response to weak confidence. Contractors use rental to access modern systems without carrying the full capital burden of ownership on their balance sheets. The model also shifts maintenance, refurbishment, and obsolescence risk to the supplier, which is valuable as product cycles become more technology-led. In practical terms, rental makes advanced systems accessible to a wider contractor base across both public and private work.

The strategic value of rental goes beyond financing because it generates recurring revenue and richer utilization data for the supplier. In the German formwork market, this data helps companies decide where to expand fleets, how to allocate stock, and which configurations are gaining share by project type. Rental also deepens customer ties through logistics, planning support, site service, and quicker replacement if project conditions change. Sales remain relevant for large contractors that can keep fleets busy across long-duration programs, especially in infrastructure and energy work. Even so, the weight of the Germany formwork market still favors rental because flexibility and capital discipline remain central to procurement decisions.

By Sector: Infrastructure-Led Growth Reinforced by Housing Recovery

Infrastructure accounted for 33% share of the Germany formwork market size in 2025, and it is projected to grow at a 7.20% CAGR through 2031. That makes infrastructure both the largest and the fastest-growing sector in the Germany formwork market. The rail commitment through 2029 supports a long stream of bridge, tunnel, station, and retaining wall work that depends on durable, reusable formwork systems. PASCHAL’s deployment of LOGO.3 formwork on the BW13 bridge in Potsdam and its special tunnel formwork at the Happurg pumped storage plant show how broad infrastructure use cases have become across the Germany formwork market. The reopening of the Hamburg-Berlin corridor after a 10-month renovation also shows that these rail programs are now in physical execution rather than early planning.

Residential construction still matters because it supports slab systems, wall formwork, and conventional applications across a wide range of projects. Multi-family recovery in major cities is important for the Germany formwork market because larger residential blocks create more repetition and better economics for engineered systems. Commercial and industrial projects also provide stable volume through logistics parks, data centers, utility structures, and retrofit work in major economic corridors. Those sectors may not lead growth, but they help balance the demand profile of the Germany formwork market across building types. Overall, infrastructure provides the market with its strongest growth engine, while the housing recovery and steady non-residential work broaden the demand base.

By Material: Aluminum Accelerates as Ergonomics Become Competitive Criteria

Steel retained the largest material share at 38% in 2025, while aluminum is forecast to expand at a 7.10% CAGR through 2031. This split shows that the Germany formwork market still relies on steel, where high load-bearing performance is essential, especially in heavy civil and infrastructure work. At the same time, labor pressure is pushing more contractors toward lighter systems that can be moved and installed with less effort. PASCHAL’s NeoR aluminum panel was introduced at Bauma 2025, weighing 23 kg for a 75×150 cm panel and compatible with existing steel NeoR elements, reflecting a clear focus on crane-free handling. In the Germany formwork market, that matters because product ergonomics are increasingly tied to crew productivity and site planning flexibility.

Timber / plywood is losing relative share as reuse, waste reduction, and consistency become more important in larger projects. Plastic / fiberglass remains a specialist material for repetitive or chemically demanding applications where durability and reuse cycles can justify its use. The German formwork market, therefore, shows a material hierarchy in which steel retains its role in demanding structural work, while aluminum gains share through labor and handling advantages. Geoplast’s patent enforcement success in Germany underlines that differentiation in alternative materials can be commercially meaningful and legally protected. That reinforces the idea that innovation in the Germany formwork market is not only about geometry and load performance but also about materials, handling, and repeatable site efficiency.

Geography Analysis

Berlin, Munich, and Frankfurt formed the densest demand cluster in the Germany formwork market in 2026 because they combine residential recovery, commercial building activity, and public infrastructure work. Berlin’s 20% revenue share in 2025 shows how much weight one city carries in national demand. That concentration matters because the Germany formwork market depends heavily on places where large projects can support strong fleet utilization and repeat engineering work. Berlin is especially important because it spans several construction categories at once, including high-rise housing, transport infrastructure, logistics assets, and commercial structures. Munich and Frankfurt add resilience through office, technology, utility, and mobility-linked construction, which broadens the metropolitan demand profile. Together, these cities create the most efficient operating geography for the Germany formwork market because dense project pipelines support faster asset turns, stronger service economics, and wider use of engineered systems.

Eastern Germany is the fastest-growing geography within the Germany formwork market, led by Leipzig and supported by Dresden’s advanced manufacturing construction base. Leipzig’s projected 7.99% CAGR makes it the clearest growth story among named city markets. The city benefits from a pipeline that includes large residential schemes and long-duration municipal housing delivery, creating recurring demand for wall, slab, and climbing applications. Dresden adds a different demand profile because semiconductor and utility-related structures require large concrete volumes and more exacting execution standards. For the Germany formwork market, this means eastern growth is not tied to one single end use but to a broader mix of urban housing and advanced industrial construction. That mix is useful because it supports both rental and sales models while also raising demand for more specialized systems.

The rest of Germany remains important to the Germany formwork market because it contributes the widest project count even if growth is slower and more uneven. In these areas, infrastructure and distributed logistics work often sustain base demand more reliably than residential construction. The challenge is that smaller, more dispersed projects increase transport and return-handling costs, which weaken the economics of fleet-heavy business models. This keeps static and conventional applications relevant across regional markets even as modern systems gain share nationally. Over time, the geography of the Germany formwork market is likely to remain two-speed, with faster expansion in metropolitan and corridor-based demand centers and a slower recovery across smaller municipal housing markets.

Competitive Landscape

The Germany formwork market is moderately consolidated, with PERI GmbH and Doka GmbH in the top tier and MEVA, PASCHAL, and Hunnebeck forming a strong second group. Competition is increasingly shaped by service depth, digital planning, rental reach, and product adaptation rather than by panel supply alone. This matters because customers in the Germany formwork market are placing more value on cycle time, engineering support, and site productivity than on hardware cost in isolation. PERI’s January 2025 joint venture with DataB, which created DataForm.Work GmbH is one of the clearest strategic moves in the market because it connects 3D planning with automated CNC-ready fabrication. That strengthens PERI’s position in bespoke and complex pours where speed from design to delivery can influence project selection.

Hunnebeck has also made a targeted move that fits the current direction of the Germany formwork market. Its SCF 60 self-climbing system addresses vertical projects where labor scarcity and crane dependence are major constraints, which gives the company a sharper proposition in high-rise and infrastructure work[3]Hünnebeck GmbH, “Formwork and Access Solutions for Safe High-Rise Construction,” Hünnebeck, huennebeck.com. PASCHAL’s NeoR aluminum panel addresses the same labor problem from a different angle, improving manual handling and enabling crane-free assembly on constrained sites. MEVA’s Alu-Platform adds another layer of competition by focusing on compatibility and easier handling across multiple system lines. These moves show that the Germany formwork market is rewarding practical jobsite advantages more than abstract product breadth.

Barriers to entry remain meaningful in the Germany formwork market because fleet investment, logistics coverage, engineering know-how, and compliance expectations all take time and capital to build. Established suppliers also benefit from installed customer relationships and from the ability to bundle rental, planning, refurbishment, and technical support. Intellectual property can still matter, as Geoplast’s legal success in Germany showed in the plastic formwork segment. Even with these barriers, specialist firms can still hold ground by focusing on digital planning, niche rental needs, or regional responsiveness. The result is a Germany formwork market where leadership is stable, but competitive gains still come from targeted innovation and service execution rather than from scale alone.

Germany Formwork Industry Leaders

PERI GmbH

Doka GmbH

MEVA Schalungssysteme GmbH

PASCHAL-Werk G. Maier GmbH

Hunnebeck GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: DB InfraGO reopened the Hamburg-Berlin high-performance rail corridor following a 10-month renovation, the largest single Generalsanierung project completed to date, confirming that the program's execution cadence is now operational at scale.

- May 2026: Germany's federal cabinet adopted the Gebäudemodernisierungsgesetz (GModG), replacing the Gebäudeenergiegesetz (GEG) to transpose the European Union Energy Performance of Buildings Directive into national law. The law mandates renovation roadmaps for all existing buildings, broadening the scope of energy-certified structural retrofits and creating a long-horizon incremental demand category for formwork in modification and strengthening works.

- February 2026: DB InfraGO entered the intensive construction phase for the Hagen-Wuppertal-Cologne and Nuremberg-Regensburg rail corridors, with all contracts pre-awarded. Both corridors involve formwork-intensive bridge, tunnel, and retaining wall elements as part of Germany's multi-decade rail Generalsanierung program.

Germany Formwork Market Report Scope

The Germany Formwork Market is Segmented by Type (Conventional / Traditional and Modular / System Formwork), Configuration (Static, Climbing, Slipform, and Tunnel), Business Model (Sales and Rental), Sector (Residential, Commercial, Industrial & Logistics and Infrastructure), Material (Timber / Plywood, and More), and City (Berlin, Munich, Frankfurt, Leipzig, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Conventional / Traditional |

| Modular / System Formwork |

| Static |

| Climbing |

| Slipform |

| Tunnel |

| Sales |

| Rental |

| Residential |

| Commercial |

| Industrial and Logistics |

| Infrastructure |

| Timber / Plywood |

| Steel |

| Aluminum |

| Plastic / Fiberglass |

| Other Material Types |

| Berlin |

| Munich |

| Frankfurt |

| Leipzig |

| Rest of Germany |

| By Type | Conventional / Traditional |

| Modular / System Formwork | |

| By Configuration | Static |

| Climbing | |

| Slipform | |

| Tunnel | |

| By Business Model | Sales |

| Rental | |

| By Sector | Residential |

| Commercial | |

| Industrial and Logistics | |

| Infrastructure | |

| By Material | Timber / Plywood |

| Steel | |

| Aluminum | |

| Plastic / Fiberglass | |

| Other Material Types | |

| By City | Berlin |

| Munich | |

| Frankfurt | |

| Leipzig | |

| Rest of Germany |

Key Questions Answered in the Report

What is the 2026 value of the Germany formwork market?

The Germany formwork market stands at USD 0.43 billion in 2026 and is forecast to reach USD 0.59 billion by 2031 at a 6.53% CAGR.

Which formwork type leads demand in Germany?

Modular / system formwork led with 57% of revenue in 2025, showing contractor preference for reusable and engineered solutions.

Which configuration is growing the fastest through 2031?

Climbing systems are projected to record the highest CAGR at 7.80% because vertical and infrastructure projects need safer and more productive repeat pours.

Why is rental so important in Germany?

Rental held 54% of revenue in 2025 because it gives contractors access to advanced systems without large upfront ownership costs.

Page last updated on: