Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

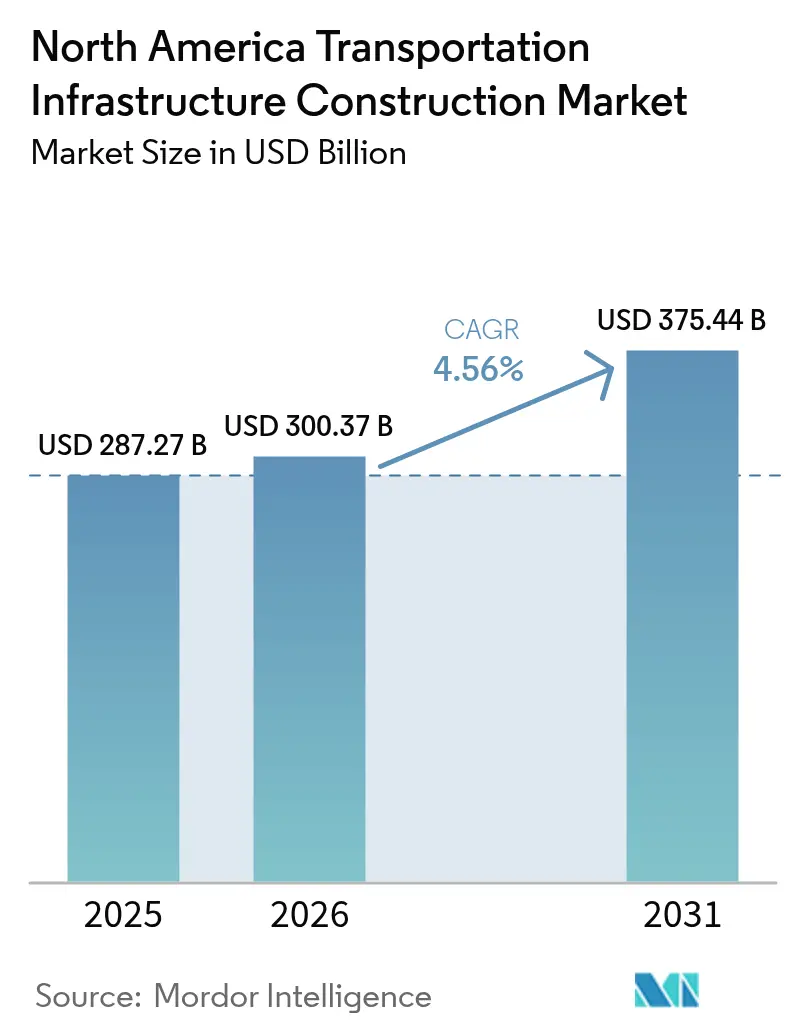

| Base Year Market Size (2025) | USD 287.27 Billion |

| Market Size (2026) | USD 300.37 Billion |

| Market Size (2031) | USD 375.44 Billion |

| Growth Rate (2026 - 2031) | 4.56% CAGR |

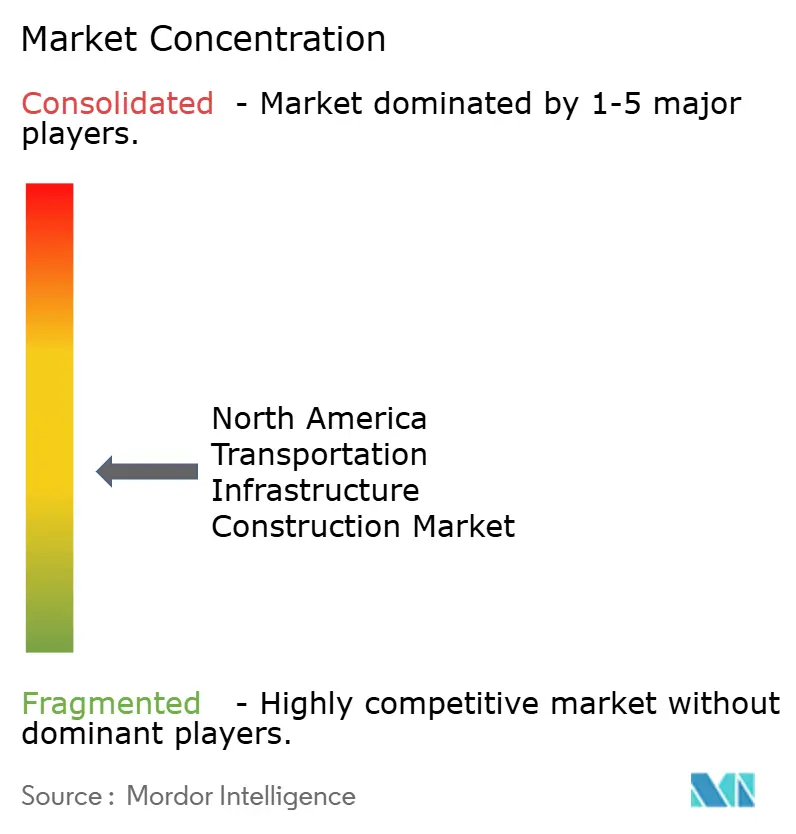

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Transportation Infrastructure Construction Market Analysis by Mordor Intelligence

North America Transportation Infrastructure Construction Market size in 2026 is estimated at USD 300.37 billion, growing from 2025 value of USD 287.27 billion with 2031 projections showing USD 375.44 billion, growing at 4.56% CAGR over 2026-2031. The modest but durable growth path reflects sustained federal and provincial appropriations in the United States and Canada alongside a revitalised project pipeline in Mexico. Multi-year surface-transport authorisations, green energy transition goals, and near-shoring–linked trade corridors are widening the addressable opportunity base for contractors, materials suppliers, and technology vendors. At the same time, the share of projects incorporating digital twins, advanced traffic-management systems, and climate-resilient design features continues to rise, creating new value pools beyond traditional civil works. Contractors that align integrated design–build capabilities with workforce development and supply-chain risk management are best positioned to defend margins in the face of lingering cost inflation and labour scarcity.

Key Report Takeaways

- By type, roadways led with a 53.40% share of the North American transportation infrastructure construction market in 2025; railways is forecast to expand at a 5.45% CAGR through 2031.

- By construction activity, new construction captured 69.30% of spending in 2025, and the same segment is projected to grow at a 5.05% CAGR between 2026 and 2031.

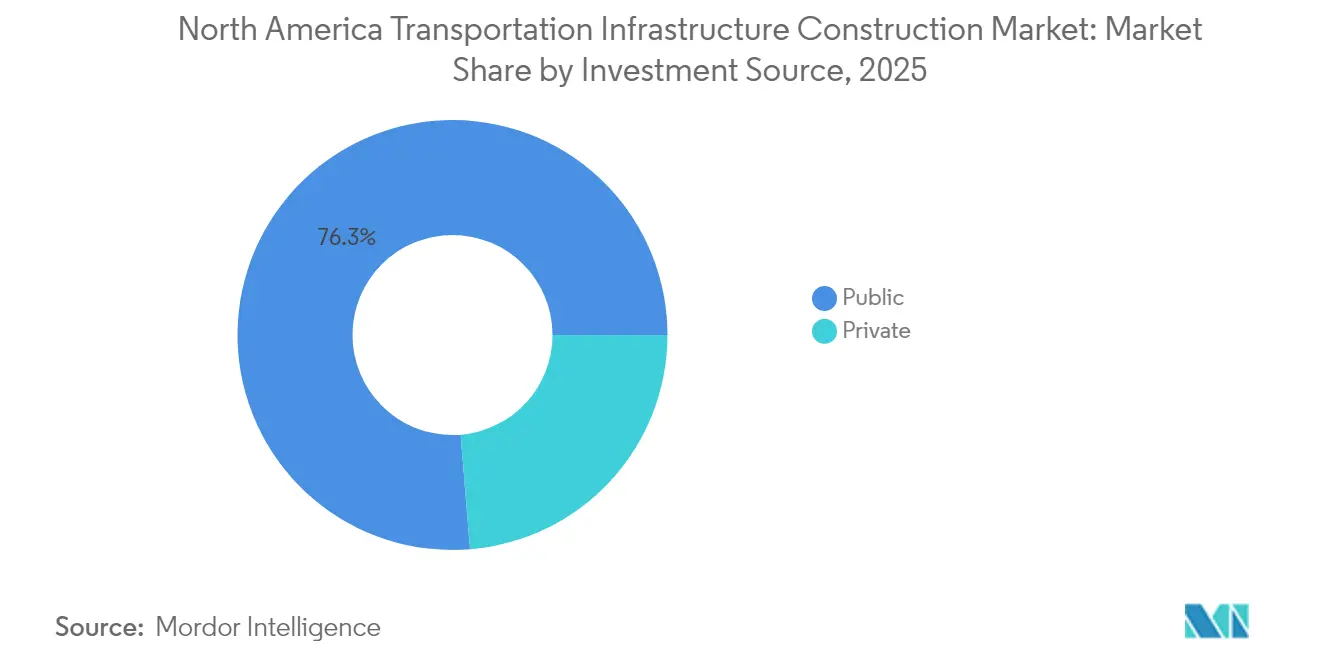

- By investment source, public funding accounted for 76.30% of 2025 expenditures, whereas private capital is expected to advance at a 5.60% CAGR over 2026-2031.

- By country, the United States dominated with 80.50% of the North American transportation infrastructure construction market share in 2025, while Mexico is set to record the fastest growth at 5.85% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Transportation Infrastructure Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal and provincial infrastructure stimulus programs | +1.8% | United States, Canada | Medium term (2-4 years) |

| Modernisation of aging bridges, tunnels and transit systems | +1.4% | United States, Canada | Long term (≥ 4 years) |

| Expansion of multimodal freight and passenger corridors | +1.2% | Cross-border North America | Medium term (2-4 years) |

| Rise of electric and autonomous mobility driving smart highways & ITS | +0.9% | Urban United States & Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Federal and Provincial Infrastructure Stimulus Programs Driving Long-Term Transport Investment Across the Region

Unprecedented fiscal support is flowing into highways, bridges, rail and transit. The United States has budgeted more than USD 350 billion for federal highway programs through 2026, with formula allocations and competitive grants already supporting more than 66,000 projects and sustaining nearly 1 million construction jobs.[1]U.S. Department of Transportation – “Infrastructure Investment and Jobs Act Funding” Provinces follow similar paths: Québec’s ten-year plan designates USD 131.2 billion for wide-ranging infrastructure additions, including USD 28.7 billion for road networks and USD 11.6 billion for public transit. Staggered release of funds has produced a counter-cyclical buffer that shelters the construction supply chain from wider economic slowdowns, while multi-year capital plans give contractors line-of-sight on workloads and foster longer equipment-leasing and workforce-training commitments.

Widespread Modernisation of Aging Bridges, Tunnels and Transit Systems to Meet Safety and Capacity Demands

An expanding share of public dollars is earmarked for repairing infrastructure rated structurally deficient. The 2025 Infrastructure Report Card shows 6.7% of U.S. bridges in poor condition, prompting large-scale rehabilitation programs such as the Portal North Bridge upgrade, now three-quarters complete, and New York’s Grand Central Artery restoration.[2]American Society of Civil Engineers – “2025 Infrastructure Report Card” Modernisation extends beyond steel and concrete replacement: asset owners are embedding digital twins, fibre-optic sensing and condition-based maintenance to prolong asset life and cut lifecycle cost. The Metropolitan Transportation Authority’s USD 68.4 billion capital plan prioritises power-system upgrades and flood resilience, signalling a pivot to performance-based asset management instead of piecemeal repairs.

Expansion of Multimodal Freight and Passenger Corridors to Enhance Regional Connectivity and Trade Efficiency

Freight bottlenecks along the United States-Mexico-Canada trade routes are being eased through purpose-built corridors that integrate rail, road and port facilities. Mexico’s Isthmus of Tehuantepec Interoceanic Corridor links 1,189 km of railway with parallel highways and modernised ports to create an alternative to the Panama Canal. In the United States, USD 2.4 billion in recent federal grants funds 122 rail projects that strengthen first- and last-mile links for shippers and commuters. These corridors underpin the USMCA framework by cutting transit times, lowering transport cost and widening inland market access for Canadian exporters. Local economies along new alignments experience secondary benefits such as warehousing, light manufacturing and services cluster formation.

Rise of Electric and Autonomous Mobility Accelerating Deployment of Smart Highways and Intelligent Transport Systems

Shift toward battery-electric fleets and self-driving logistics vehicles is accelerating sensor-heavy infrastructure rollouts. The Advanced Transportation Technology and Innovation program recently awarded USD 96 million for projects including vehicle-to-everything corridors, AI-driven traffic management and automated incident detection. States are layering adaptive signals and edge computing onto heavily travelled arterials, reducing travel time, fuel burn and crash risk. Transit agencies target fleet electrification goals—20% of the New York metropolitan bus fleet will be electric by 2029—spurring parallel investment in charging lanes, substations and grid upgrades. Contractors with software-integration expertise and control-centre build capabilities are differentiating themselves as project scopes extend beyond civil works into communications and cyber-security domains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic shortages of skilled labour in civil and transportation trades | –1.1% | United States, Canada | Medium term (2-4 years) |

| Persistently high construction material prices | –0.7% | United States-focused | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic Shortages of Skilled Labour in Civil and Transportation Trades Increasing Project Delivery Risk

Labour availability remains the principal hurdle for on-time project delivery. Ninety-three percent of contractors report open craft positions, while vocational enrolment declines and retirements accelerate—41% of transportation construction workers reach retirement eligibility by 2031. The industry recorded 248,000 unfilled jobs in April 2025, pressuring wages and elongating bid schedules. Owners are responding with larger contingency allowances, while contractors expand modular fabrication, invest in machine control and widen outreach to under-represented workforce segments. Federal and state apprenticeship incentives are helping, yet the gap between project authorisation and crew mobilisation threatens schedule certainty for megaprojects.

Persistently High Construction Material Prices Undermining Budget Reliability and Delaying Procurement Decisions

Material inflation remains elevated: composite input costs are forecast to rise 5-7% during 2025, led by volatility in structural steel, lumber and electrical gear. Supply chain disruptions and tariff risk compound uncertainty, forcing agencies to include higher escalation clauses and, in some cases, split procurements to lock in prices earlier. The Los Angeles transit authority flagged cost creep as a contributor to scope deferral on several extensions, signalling how price instability can distort prioritisation. Contractors adopt hedging instruments and explore alternative materials, but budget overruns continue to deter marginal projects, creating uneven investment patterns across states and provinces.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Railways Gain Momentum Amid Modal Shift

Spending on roadways reached USD 153.4 billion in 2025, equating to 53.40% of the North American transportation infrastructure construction market. State and provincial highway programmes fund extensive resurfacing, lane-widening and interchange reconstructions aimed at relieving chronic congestion. Emission-reduction mandates encourage agencies to experiment with warm-mix asphalt, reclaimed pavement and permeable shoulders, broadening material specifications and opening new niches for suppliers.

Railways, which represented 28.70% of 2025 outlays, is slated for a 5.45% CAGR through 2031—the fastest among modal types. Federal passenger-rail grants, freight-operator capital plans and binational high-frequency corridors anchor this momentum. Recent service-quality lapses on congested rail links have prompted urgent investments in signalling, track duplication and grade-separation works. Consequently, the North American transportation infrastructure construction market size allocated to railways is projected to grow steadily, gaining ground on the historically dominant highway segment.

By Construction Type: Renovation Demand Rises as Infrastructure Ages

New construction commanded 69.30% of 2025 spend, underscoring ongoing demand for greenfield corridors, intermodal hubs and replacement facilities. Multi-year design-build-finance-operate contracts continue to set new benchmarks for schedule certainty and cost predictability, reinforcing owner confidence in private-sector delivery models. Smart sensors embedded during the build phase feed real-time data to asset-management dashboards, compressing commissioning periods and supporting rapid revenue service.

Renovation and upgrade activity, while holding a 30.70% share in 2025, is expanding at a brisk pace due to mandatory bridge-condition reporting and tunnel-safety directives. Owners now couple structural repair with technology retrofits—installing fibre conduits, electronic tolling gantries and advanced CCTV—to prolong asset lifespan and improve revenue capture. The heightened emphasis on resiliency is injecting fresh complexity into renewal scopes, rewarding firms with integrated design and construction management capabilities.

By Investment Source: Private Capital Accelerates Growth

Public entities financed 76.30% of the North American transportation infrastructure construction market in 2025 through grant programs, trust-fund disbursements and municipal bonds. The predominance of public funding stems from the public-goods nature of major transport arteries and the need for inter-jurisdictional coordination.

Private investment, accounting for the remaining 23.70% in 2025, is on course for a 5.60% CAGR to 2031—ahead of total-market growth. Pension funds, insurance houses and specialist infrastructure investors are structuring revenue-risk-sharing agreements around toll lanes, electrified intercity rail and data-rich traffic-management platforms. These investors value the long-duration, inflation-linked cash flows typical of mature transportation concessions, thereby broadening the capital stack available to project sponsors and amplifying expansion capacity across the North American transportation infrastructure construction market.

Geography Analysis

The United States remained the powerhouse in 2025, contributing 80.50% of total spending. High-visibility megaprojects—from the re-imagined Hudson River rail tunnel to Texas’ multi-lane interstate upgrades—headline the country’s forward programme. Federal technology grants incentivise deployment of vehicle-to-everything infrastructure, advanced traffic analytics and zero-emission transit fleets, elevating the sophistication of project scopes and raising the skills bar for bidding consortia.

Canada accounts for a smaller but strategically important share. The federal high-frequency rail initiative linking Québec City to Toronto will modernise 1,000 km of rail corridor, while prairie-province freight-rail upgrades unlock grain-export capacity. Provincial commitments to reduce tailpipe emissions accelerate procurement of fully electric bus rapid-transit networks and smart-signal corridors. These developments ensure that Canada remains a growth contributor within the broader North American transportation infrastructure construction market.

Mexico is the regional out-performer, advancing at a 5.85% CAGR on the back of flagship programmes such as Tren Maya and the Isthmus of Tehuantepec corridor. Fiscal constraints necessitate blended-finance structures involving development banks, pension funds and concessionaires. Successful execution of these schemes will relieve logistics chokepoints, attract manufacturing reshoring and deepen the project pipeline feeding the North American transportation infrastructure construction market.

Competitive Landscape

Industry structure is moderately consolidated, with the five largest contractors controlling roughly 45% of revenue. Integrated engineering-procurement-construction firms leverage balance-sheet strength, digital fluency and self-perform capacity to secure multi-billion-dollar packages. Mid-tier players pursue mergers to increase geographic reach and asset-maintenance portfolios, as evidenced by recent asphalt-plant acquisitions aimed at vertical integration.

Technology competencies weigh increasingly on award decisions. Owners now evaluate bidder proficiency in BIM-enabled quantity take-off, drone-based progress tracking and AI-driven safety analytics. Firms able to document reduced rework, improved schedule adherence and lower on-site emissions gain scoring advantages. The North American transportation infrastructure construction market therefore rewards contractors that combine traditional heavy civil expertise with data-engineering capabilities.

Workforce renewal tops corporate risk agendas. Leading contractors partner with community colleges, veterans’ programmes and Indigenous-training initiatives to widen recruitment funnels. Augmented-reality field training, exoskeletons and semi-autonomous earth-moving equipment help improve productivity per labour-hour, partially offsetting crew shortages. Firms that institutionalise such measures are more likely to meet liquidated-damages milestones and protect profit margins.

North America Transportation Infrastructure Construction Industry Leaders

Bechtel Corporation

ACS Group (Dragados & Hochtief)

Fluor Corporation

AECOM

Kiewit Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The Port Authority of New York and New Jersey broke ground on the USD 10 billion Midtown Bus Terminal replacement, the world’s largest zero-emission bus hub.

- May 2025: Canadian National Railway unveiled a USD 2.7 billion capital program focused on Western Canada capacity expansion and safety upgrades.

- May 2025: The California Independent System Operator approved a USD 4.8 billion transmission plan covering 31 projects to meet load growth.

- March 2025: The U.S. Department of Transportation proposed nearly USD 4 billion for 14 transit megaprojects, including the Chicago Red Line Extension and the Hudson Tunnel.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study frames the North America transportation infrastructure construction market as all capital spending directed toward planning, building, enlarging, rehabilitating, or demolishing publicly accessible roadways, rail lines, airports, and seaports across the United States, Canada, and Mexico during the project life-cycle. Spending linked solely to rolling stock, logistics services, or private industrial networks sits outside this boundary.

Scope Exclusion: proprietary freight yards, maintenance depots, and privately owned mining or energy corridors are not tracked.

Segmentation Overview

- By Type

- Roadways

- Railways

- Airways

- Ports and Inland Waterways

- By Construction Type

- New Construction

- Renovation

- By Investment Source

- Public

- Private

- By Country

- United States

- Canada

- Mexico

Detailed Research Methodology and Data Validation

Primary Research

We interviewed senior procurement officers at state DOTs, engineering consultants overseeing mega-projects, and lenders structuring public-private partnerships across all three countries. Their inputs clarified prevailing lane-mile cost ranges, emerging asset classes (EV-ready corridors, resilient bridges), and realistic construction-start schedules, which sharpened model assumptions.

Desk Research

Mordor analysts first mapped historical outlays using publicly available macro-datasets from agencies such as the U.S. Office of Management & Budget, Federal Highway Administration, Statistics Canada, Secretaria de Infraestructura, Comunicaciones y Transportes, and the World Bank; project-level insights were verified through reputable trade bodies like AASHTO and the Railway Association of Canada. Financial disclosures from leading contractors, infrastructure bills, and press releases were screened via Dow Jones Factiva and D&B Hoovers to benchmark cost norms and contract pipelines. These examples illustrate, not exhaust, the secondary sources referenced.

Market-Sizing & Forecasting

A top-down roll-up of federal, provincial, and state capital budgets, adjusted for historic utilization rates, set the initial 2025 base. We then cross-checked totals with selective bottom-up snapshots, sampled contractor revenue, cement shipments, and Class I railroad capex to fine-tune gaps. Key variables include IIJA disbursement velocity, steel rebar price index, truck freight ton-miles, passenger-mile growth, and public-private partnership closure rates. Multivariate regression, reinforced by expert consensus scenarios, projects value through 2030. Where data lags, we imputed using three-year moving averages anchored to GDP and construction cost deflators.

Data Validation & Update Cycle

Outputs undergo variance screening against independent indicators such as cement consumption and contractor backlog trends before a senior reviewer signs off. Reports refresh annually, with interim recalibrations when funding legislation, material prices, or major project awards shift materially.

Why Our North America Transportation Infrastructure Construction Baseline Earns Confidence

Published estimates rarely align because firms diverge on asset mix, inflation handling, and refresh cadence.

Key gap drivers: some limit estimates to roads, others omit renovation spend, and many still rely on three-year-old cost factors explain the spread visible below.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 287.27 B (2025) | Mordor Intelligence | - |

| USD 214.3 B (2024) | Global Consultancy A | Excludes rehabilitation projects and ports; applies a conservative 2019 cost index |

| USD 211.8 B (2023) | Industry Analyst B | Captures only roads and bridges; refreshes every four years; omits PPP pipelines |

The comparison shows that Mordor's disciplined scope selection, annual refresh cycle, and dual-path validation deliver a balanced, transparent baseline that decision-makers can trace directly to verifiable budgets, cost drivers, and construction activity signals.

Key Questions Answered in the Report

What is the current size of the North American transportation infrastructure construction market?

The market is valued at USD 300.37 billion in 2026 and is projected to reach USD 375.44 billion by 2031.

Which segment is growing fastest within the market?

Railways leads growth with a 5.45% CAGR expected between 2026 and 2031, driven by substantial public and private rail investments.

How significant is private financing in regional projects?

Private capital funded 23.70% of 2025 spending and is rising at a 5.60% CAGR over 2026-2031 as public-private partnership models gain wider acceptance.

Why are smart highways important for future infrastructure?

Smart highways integrate sensors, communications and analytics to cut congestion, lower emissions and prepare networks for autonomous and electric vehicles.

What major challenge threatens project schedules?

Skilled-labour shortages persist, with 93% of contractors unable to fill craft positions, causing higher labour costs and potential delays.

Which country is expected to post the highest growth rate?

Mexico is set to record a 5.85% CAGR through 2031, propelled by flagship projects such as Tren Maya and the Isthmus of Tehuantepec Corridor.

Page last updated on: