China Formwork Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

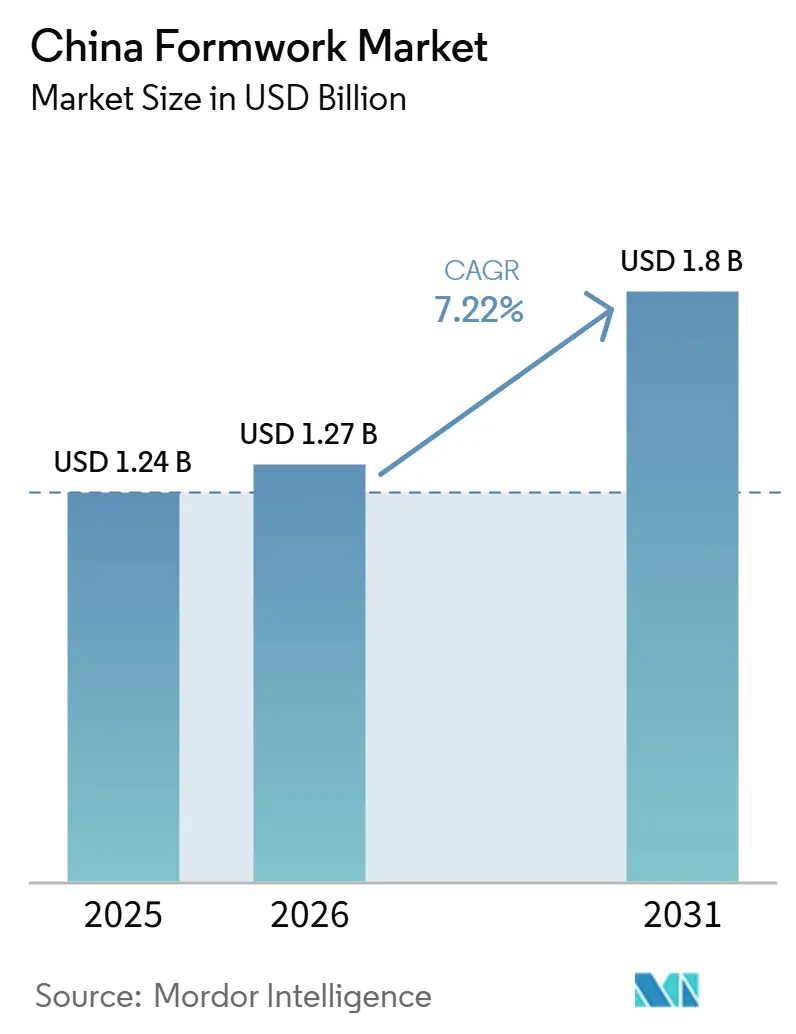

| Base Year Market Size (2025) | USD 1.24 Billion |

| Market Size (2026) | USD 1.27 Billion |

| Market Size (2031) | USD 1.8 Billion |

| Growth Rate (2026 - 2031) | 7.22% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Formwork Market Analysis by Mordor Intelligence

The China Formwork Market size is projected to be USD 1.24 billion in 2025, USD 1.27 billion in 2026, and reach USD 1.8 billion by 2031, growing at a CAGR of 7.22% from 2026 to 2031.

The current expansion path reflects a clear shift in demand, as private housing activity has weakened. At the same time, state-backed infrastructure has taken a larger role in sustaining the China formwork market. China’s Six Networks program is expected to direct CNY 7 trillion (USD 1.02 trillion) into power grids, gas and water pipelines, computing infrastructure, and logistics networks in 2026, which supports a broad pipeline for cast-in-place concrete works and higher-cycle formwork systems. Infrastructure investment rose 8.9% year on year in Q1 2026, helping reverse the softer construction backdrop seen in 2025 and providing the China formwork market with a more durable project base. Demand is also moving toward reusable, engineered systems because labor efficiency, carbon compliance, and project standardization now matter more in procurement than simple upfront material cost. The competitive setting, therefore, favors suppliers with scale in rental fleets, specialization in climbing and modular systems, and the ability to support complex public works and export-linked projects rather than companies tied mainly to conventional residential construction.

Key Report Takeaways

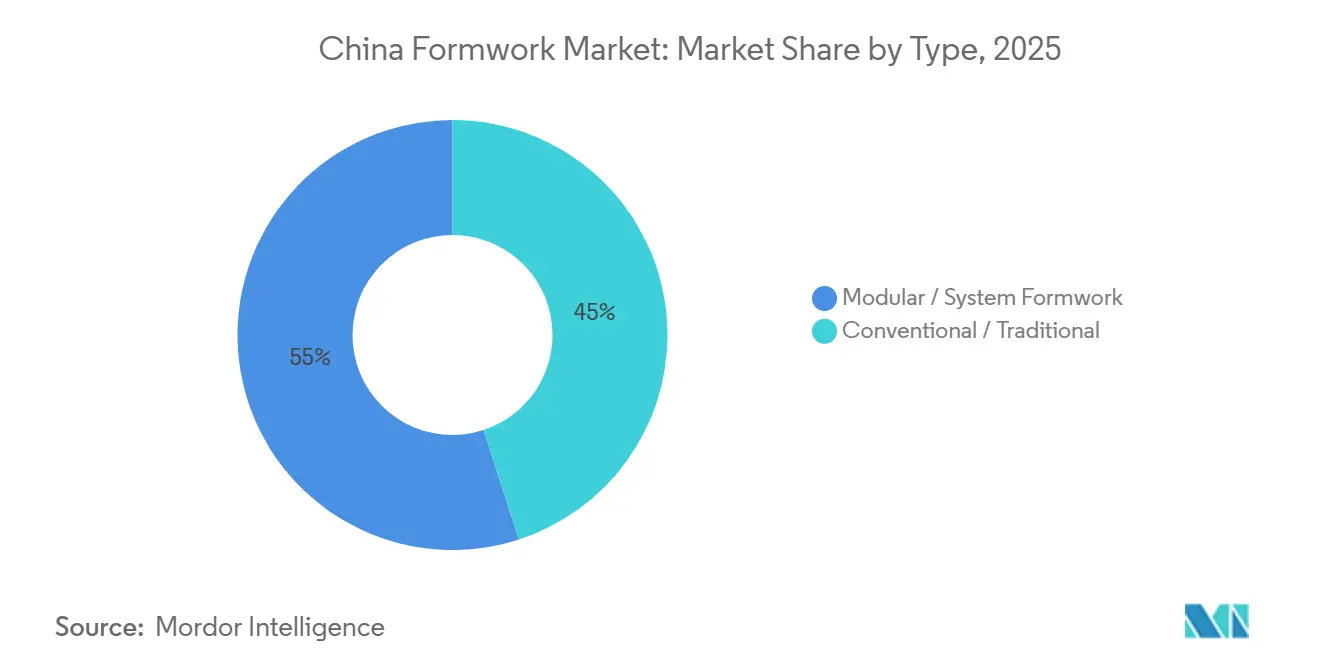

- By type, modular / system formwork held 55% of the China formwork market share in 2025 and is also the fastest-growing type, with an 8.6% CAGR through 2031.

- By configuration, climbing systems held 30% share and recorded the fastest CAGR at 8.54% through 2031.

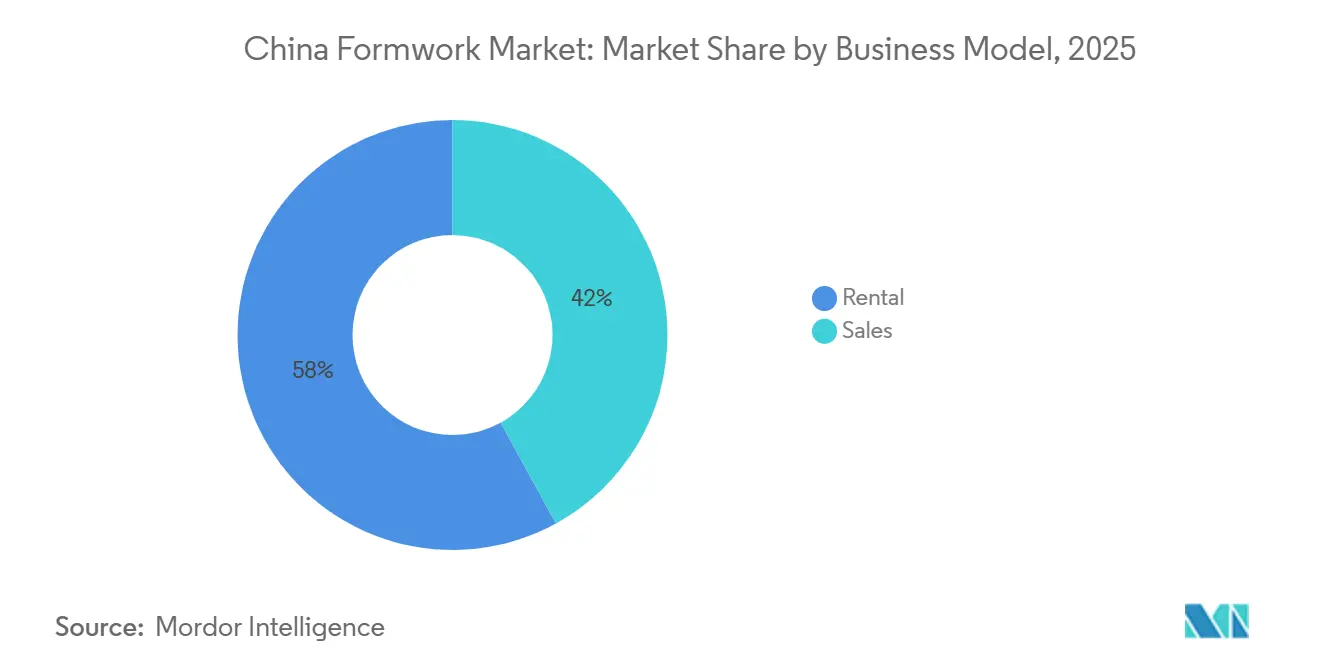

- By business model, rental accounted for 58% of the China formwork market size in 2025 and posted the highest projected CAGR of 8.40% through 2031.

- By sector, residential construction held 38% share in 2025, while infrastructure is forecast to expand at the fastest CAGR of 9.00% through 2031.

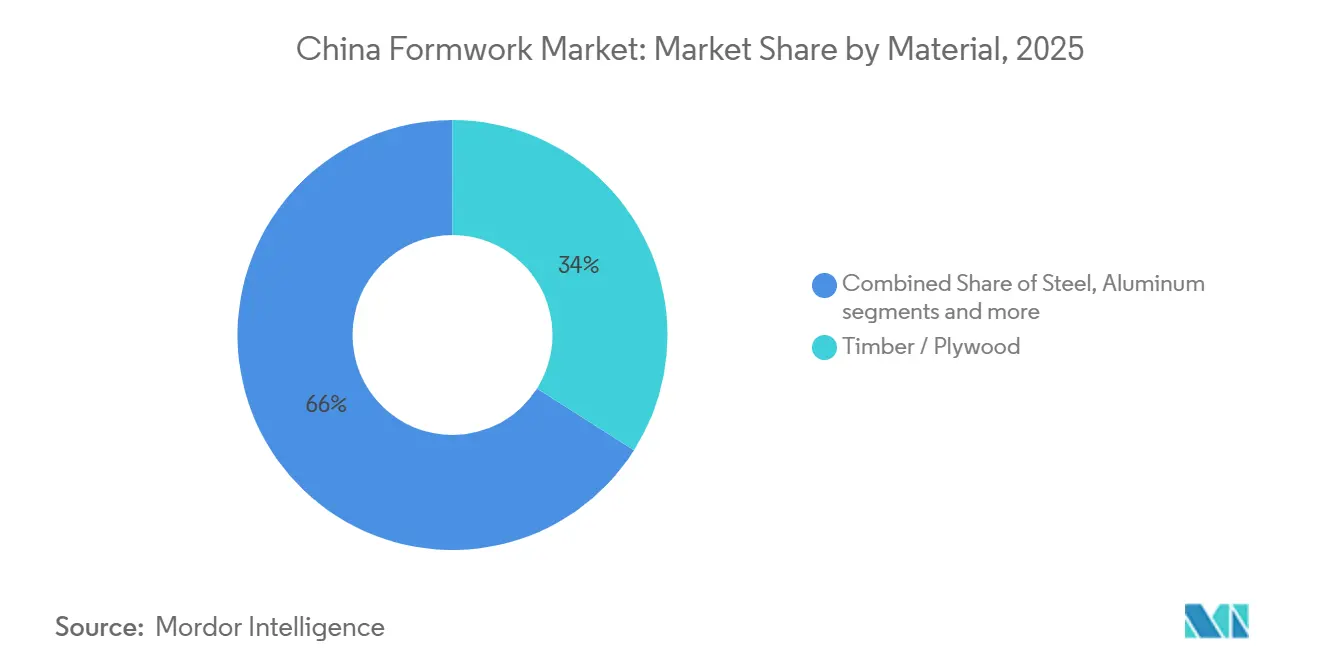

- By material, timber / plywood accounted for 34% of the market in 2025, while aluminum is projected to grow the fastest at a 7.80% CAGR through 2031.

- By geography, East China held 31% share in 2025, while Southwest China is set to record the highest CAGR at 8.70% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Formwork Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure Modernization and Urban Renewal Drive Formwork Demand | +2.00% | National, concentrated in East China, North China, and Southwest China | Medium term (2-4 years) |

| Dual Carbon Goals Accelerate Adoption of Reusable Formwork Systems | +1.50% | National, stronger compliance enforcement in Tier-1 and Tier-2 cities | Medium term (2-4 years) |

| Labor Shortages and Productivity Needs Boost Engineered Formwork Usage | +1.20% | National, most acute in Beijing, Shanghai, Guangzhou, and Shenzhen | Short term (≤ 2 years) |

| Digital Formwork Planning and Asset Tracking Improve Project Efficiency | +0.90% | East China and South China, with spillover into Central China | Medium term (2-4 years) |

| Urbanization in Lower-Tier Cities Supports Replacement Construction Demand | +0.80% | Southwest China, Central China, Northwest China | Long term (≥ 4 years) |

| Belt and Road Projects Expand Export Demand for Formwork Systems | +0.50% | National, centered on export-oriented manufacturing hubs in East and South China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Infrastructure Modernization and Urban Renewal Drive Formwork Demand

The main construction engine has shifted from private residential towers to publicly funded infrastructure, and that change has improved the quality of demand in the China formwork market. Infrastructure jobs usually require more durable, specialized systems, including climbing rigs for bridge piers, slipform solutions for towers and silos, and tunnel formwork for metro and highway works, rather than the simpler, plywood-heavy setups common in housing projects. The 15th Five-Year Plan for 2026 to 2030 commits CNY 5 trillion (USD 1 trillion) to gas, water, drainage, and heating pipeline upgrades across 770,000 kilometers, and another CNY 5 trillion (USD 1 trillion) to power grid expansion and inter-provincial transmission corridors, which keeps concrete-intensive work elevated across several project categories[1] Xinhua, “China's Massive Infrastructure Push Targets Domestic Demand, Growth Stabilization,” Xinhua News Agency, news.cn. Infrastructure investment increased 11.4% in January and February 2026 and 8.9% in Q1 2026, outpacing broader fixed-asset investment and providing formwork suppliers with better multi-year visibility than the private building segment could offer. Urban renewal adds another layer of demand because underground pipeline rehabilitation and sponge-city works favor modular systems that can be cycled repeatedly in tight sites where space efficiency and predictable assembly matter.

Dual Carbon Goals Accelerate Adoption of Reusable Formwork Systems

Carbon policy is changing project-level material choices, pushing the China formwork market toward reusable systems rather than products chosen only for low initial cost. Prefabricated building construction reached 672 million square meters under construction in 2024, representing more than 30% of all new building floor area, underscoring how deeply industrialized building methods are now embedded in the construction system. The industry standard T/CCIAT 0104-2025, which took effect on March 1, 2026, set out carbon-reduction procedures for building engineering, including calculation methods for construction-phase emissions and the formal accounting of formwork use cycles. The green building evaluation standard GB/T 50378-2024 also raises the compliance threshold for premium projects, as three-star-certified buildings must use reusable formwork at a rate of at least 70%, thereby narrowing the role of single-use conventional plywood in high-grade developments. Within that setting, aluminum systems benefit from both regulatory alignment and lifecycle economics, as their reuse potential is materially higher than timber's and their fit with standardized project delivery is stronger.

Labor Shortages and Productivity Needs Boost Engineered Formwork Usage

The labor side of construction has tightened, and that pressure is raising the value of systems that reduce manual setup time, stripping time, and repositioning effort across the China formwork market. Project teams are therefore placing greater weight on engineered formwork because predictable assembly reduces dependence on hard-to-source skilled crews and helps contractors hold slab-cycle schedules when labor availability becomes uneven. The construction industry’s statistical analysis for H1 2025 showed that labor productivity improved even as overall output softened, indicating that surviving crews were already relying more on standardized tools and more efficient site practices. That pattern supports modular systems and self-climbing configurations, since both shorten repetitive work cycles and allow contractors to stabilize productivity under constrained staffing conditions. The result is that labor efficiency is no longer a secondary selling point in the China formwork market, because it now shapes equipment choice, rental preference, and the willingness to pay for higher-specification systems.

Digital Formwork Planning and Asset Tracking Improve Project Efficiency

Digital planning is moving from a useful add-on to a practical requirement in the China formwork market, as project complexity, tighter timelines, and larger public contracts reward greater coordination accuracy. The construction industry’s 14th Five-Year Plan set a target for 90% of new government-invested projects to achieve full Building Information Modeling (BIM) application by 2025, and a national standard issued in June 2025 formalized BIM-based construction management procedures for building engineering. Once formwork planning is integrated with material logistics, on-site monitoring, and asset tracking, contractors can reduce waste, improve cycle predictability, and gain better visibility into fleet utilization across multiple projects. PERI’s 2025 joint venture with DataB and Doka’s Doka 360 platform both reflect this direction, tying planning, production, ordering, and return logistics into a more integrated workflow that strengthens customer retention beyond simple product supply. Suppliers that combine physical systems with digital planning support are therefore better placed to defend pricing and lengthen contract duration. At the same time, mid-tier domestic operators still have room to build capability through partnerships and software-led service upgrades.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Property Sector Weakness Reduces Private Residential Construction Activity | -1.8% | National, most acute in Tier-2 and Tier-3 cities with housing surplus | Short term (≤ 2 years) |

| High Upfront Cost of Aluminum and Steel Formwork Limits Adoption | -0.7% | National, most pronounced among smaller contractors in Tier-3 and Tier-4 cities | Medium term (2-4 years) |

| Steel and Aluminum Price Volatility Pressures Manufacturer Margins | -0.6% | National, with the strongest effect on SME manufacturers | Short term (≤ 2 years) |

| Fragmented Rental Market Restricts Nationwide Standardization | -0.5% | National, more dispersed in Central, Northwest, and Northeast China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Property Sector Weakness Reduces Private Residential Construction Activity

Private housing remains the main drag on the China formwork market because the property adjustment has continued into 2026 and continues to weigh on new project starts, contractor cash flow, and demand for conventional slab and wall systems. The heaviest pressure falls on timber and plywood-heavy applications, since those materials are most exposed in mid-rise and volume residential construction, which had been the largest historical outlet before public infrastructure gained share. This matters because residential work still represented the largest sectoral share in 2025, so even a gradual weakening in private builds affects equipment utilization, replenishment decisions, and fleet deployment across many local suppliers. Government-supported affordable housing, urban village renovation, and dual-use public infrastructure provide partial offsets. Still, they do not fully replace the mix or timing of demand previously generated by private high-rise development. Companies with stronger links to state-funded projects are therefore in a more resilient position than operators whose installed base and customer relationships remain concentrated in privately financed residential construction.

High Upfront Cost of Aluminum and Steel Formwork Limits Adoption

The upfront cost of premium systems still limits the speed at which the China formwork market can shift away from lower-cost conventional materials. Aluminum and steel formwork perform best when utilization is high, project design is repetitive, and schedules are stable, because those conditions allow reuse cycles to spread the initial investment over a larger volume of work. A 2026 study on projects in Northeast China confirmed that aluminum formwork offers economic benefits throughout the project lifecycle. Still, it also showed why smaller contractors remain cautious at the point of first purchase when capital budgets are tight. The issue is sharper outside the largest cities, where the contractor base is more fragmented, and project pipelines are less predictable, which weakens the confidence needed to invest in premium fleets. As a result, adoption rises fastest where contractors can lock in repeat work and achieve high utilization, while smaller firms continue to balance lifecycle efficiency with immediate procurement costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Modular / System Formwork Consolidates its Majority Position

Modular / system formwork held 55% of the China formwork market share in 2025, and this segment is also projected to expand at the fastest pace with an 8.60% CAGR through 2031. That lead reflects a clear contractor preference for engineered systems that shorten assembly time, improve cycle predictability, and reduce dependence on manual labor in repetitive structural work. Modular / system formwork has become more attractive because project owners and main contractors now place greater value on productivity, tighter quality control, and reuse efficiency than they did when labor was easier to source, and residential builds set the dominant pace. In the China formwork market, this gives modular platforms a structural edge in high-cycle infrastructure work, large mixed-use projects, and standardized public developments where the benefits of repeat deployment are easier to capture. It also strengthens the case for suppliers that can provide design support, faster site turnaround, and stronger after-sales service, rather than only panels and accessories.

Conventional / traditional formwork still accounted for 45% of demand in 2025, indicating that the installed base, local sourcing habits, and contractor familiarity built over many years still carry weight across broad parts of the country. This segment remains most relevant in lower-tier cities and rural projects where timber is accessible, work scopes are simpler, and the capital required for advanced systems can be hard to justify at a small project scale. Even so, the direction of travel is changing because green building requirements, construction industrialization policies, and the wider use of prefabricated methods are gradually reducing the practical space for single-use solutions in better-specified projects. Research published in 2025 found that higher prefabrication rates, stronger policy implementation, and greater patent activity are linked to better energy-efficiency outcomes in construction, which supports the broader move toward more industrialized building practices[2]Lin X. et al., “Threshold Effect Study on the Development of Prefabricated Buildings for Energy Conservation and Emission Reduction in the Construction Industry,” Scientific Reports, nature.com. The implication for the China formwork market is not a sudden collapse in conventional demand, but a steady shift away from premium applications toward reusable systems that better align with labor, compliance, and industrialization priorities.

By Configuration: Climbing Systems Scale with China’s Vertical Ambitions

Climbing systems held 30% of the segment share in 2025 and posted the fastest growth rate of 8.54% through 2031, placing them at the more specialized end of the China formwork market. Their expansion is tied to supertall buildings, bridge piers, dam cores, and other vertical concrete structures where self-climbing systems reduce crane dependence and improve productivity on difficult sites. Research on overall aerial building formwork equipment for structures above 200 meters found that integrated lightweight climbing platforms deliver strong engineering performance and better construction productivity in extreme-height applications. This aligns with the reality that vertical infrastructure and high-rise cores require more than simple panel supply, as they depend on system engineering, site safety coordination, and repeatable lifting performance across long project cycles. It also explains why multinational specialists and advanced domestic players have stronger pricing power in this configuration than in more standardized products.

Static formwork supports a broad range of conventional residential and commercial concrete applications across floors, walls, and columns. Slipform and tunnel solutions occupy smaller positions, but both are gaining relevance as energy facilities, transport corridors, and underground works expand under public investment programs. This mix shift matters because specialized configurations usually deliver higher rental rates and service revenue per cycle than standard static systems, especially when they require technical setup and engineering supervision. As those categories grow, average revenue quality in the China formwork market improves, even as headline volume growth remains measured. That shift also raises the importance of fleet sophistication and technical support capability, because customers in these applications are buying reliable execution as much as they are renting hardware.

By Business Model: Rental Solidifies as the Industry Operating Standard

Rental accounted for 58% of the China formwork market share in 2025 and is expected to record the fastest CAGR of 8.40% through 2031. The preference for rental is grounded in contractor economics, since it reduces inventory risk, limits maintenance burdens, and transfers part of the compliance upgrade cycle to the equipment provider. This has become more important as reusable systems grow in importance, because contractors do not all want to carry the capital cost of premium aluminum, steel, or climbing fleets on their own balance sheets. In the China formwork market, rental also suits a project environment where work types change quickly, and firms want the flexibility to switch between conventional, modular, and specialized systems without owning every asset category. The model is therefore moving beyond equipment access and becoming a broader operating choice tied to risk management, fleet efficiency, and procurement discipline.

Sales still accounted for 42% of demand in 2025, supported mainly by large state-owned construction groups and other major contractors that operate proprietary fleets across multiple internal project pipelines. Ownership remains attractive when project volumes are large, work specifications are predictable, and a company can maintain high utilization across multiple sites over several years. Even so, the broader structure still favors gains in rental penetration because fragmentation across the contractor base makes asset-light access more practical than direct ownership for many users. The sector’s long tail of regional rental operators also creates consolidation pressure, since standardization, utilization management, and digital tracking are easier to implement at a larger scale than in very local fleets. For the China formwork market, that means value is likely to shift toward operators that can combine regional density, engineering support, and digital fleet visibility into a more dependable service offer.

By Sector: Infrastructure Overtakes Residential as the Growth Engine

Residential construction held the largest sectoral share at 38% of the China formwork market in 2025, reflecting the legacy importance of housing activity in total construction demand. That position, however, no longer translates into the strongest outlook, because the property cycle continues to pressure new housing starts and to weaken demand for conventional slab-and-wall systems used heavily in private developments. Commercial buildings and industrial and logistics projects provide a stabilizing middle layer, especially where data centers, factories, and warehousing facilities offer shorter build cycles and repeatable layouts. These projects do not fully replace residential’s historical volume-weight. Still, they do support a steadier demand for modular systems and reusable materials, as standardization tends to be higher than in bespoke private towers. Their role becomes more important while housing remains under pressure and while public infrastructure absorbs a larger share of construction capital.

Infrastructure is set to expand at the fastest pace with a 9.00% CAGR through 2031, making it the clearest growth engine in the China formwork market. The National Development and Reform Commission allocated CNY 216.8 billion (USD 31.4 billion) in ultra-long special treasury bonds to 336 major projects in the second 2026 disbursement batch, and local governments had already issued CNY 1.33 trillion (USD 193.5 billion) in new special bonds through April 2026. These works are formwork-intensive in a different way from residential buildings, because bridge piers, viaducts, tunnels, and utility corridors require higher-specification systems with stronger engineering content and higher service value per cycle. That makes infrastructure not only faster-growing but also more favorable to suppliers with climbing, slipform, tunnel, and modular capabilities. Companies that deepen ties with large state-backed infrastructure builders are therefore positioned to outperform the overall China formwork market as demand composition continues to shift.

By Material: Timber / Plywood Defends Volume While Aluminum Reshapes the Premium Tier

Timber / plywood accounted for 34% of demand in 2025, giving it the largest share by volume in the China formwork market. Their position rests on low entry cost, broad local availability, and long-standing contractor familiarity, especially in conventional residential work and smaller projects where budgets remain tight, and reuse intensity is limited. Timber also benefits from the fact that a large part of the market still operates below the strictest green-building thresholds, which allows lower-cost solutions to remain viable in volume applications. Steel plays an important role in heavy civil work and reusable wall systems, while plastic / fiberglass holds smaller niches in circular columns and underground utility work, where handling and shape requirements differ from those of mainstream slab and wall work. The material mix, therefore, remains diverse, but it is increasingly split between low-cost, volume-driven demand and higher-specification, reuse-led demand.

Aluminum is the fastest-growing material, with a 7.80% CAGR through 2031, and its rise is closely linked to the evolution of compliance and industrialized construction. Requirements under GB/T 50378-2024 make reusable formwork more important in better-specified projects, especially in public or government-supported housing and renewal work, where repeatability and documentation standards are higher. A 2025 study on green construction technology also confirmed that reusable formwork systems can lower lifecycle cost and carbon outcomes relative to conventional plywood baselines, which supports the commercial case for premium materials. Aluminum also fits well with prefabricated and standardized structures because repetitive geometries improve reuse economics and reduce waste across long project runs. In the China formwork market, this means timber is likely to retain broad market relevance. At the same time, aluminum continues to reshape the premium tier, where compliance, repeatability, and lifetime efficiency carry more weight than initial purchase cost.

Geography Analysis

East China accounted for 31% of the China formwork market share in 2025, which made it the largest regional cluster by value and activity. The region benefits from the dense construction base of Shanghai, Jiangsu, Zhejiang, and Shandong, where project volumes, supplier networks, and contractor sophistication are all stronger than the national average. It also hosts a high concentration of aluminum formwork manufacturers, reducing logistics friction and enabling faster deployment cycles for reusable systems. East China’s digital maturity is another advantage, as Building Information Modeling (BIM) adoption is more advanced across major design institutes and contractors, helping system formwork gain share in projects with more integrated planning. Research published in 2025 on BIM policy diffusion and BIM adoption modes in China supports the view that digitally stronger ecosystems are better placed to scale standardized construction workflows[3]Yang Y. et al., “Multilevel Institutional Analysis of BIM Policy Diffusion in China's Construction Industry, A Spatiotemporal Perspective,” Ain Shams Engineering Journal, doi.org.

North and South China make up the second tier of the China formwork market. North China’s demand is linked to infrastructure and integration-zone projects in the Beijing-Tianjin-Hebei corridor. At the same time, South China benefits from the Pearl River Delta’s commercial, mixed-use, and higher-specification construction base. Central China remains an important volume region for conventional systems, and it also offers room for rental operators expanding from coastal bases into urban renewal programs in cities such as Wuhan, Zhengzhou, and Changsha. Northwest and Northeast China are smaller by value, but both gain from energy projects and grid-related construction that favor specialized systems, including climbing and slipform solutions.

Southwest China is projected to record the fastest growth at 8.70% through 2031, which gives it the strongest regional momentum in the China formwork market size outlook. The Chengdu-Chongqing Economic Circle is the main reason, as its 350 key projects carried a planned 2026 investment of CNY 499.2 billion (USD 72.32 billion) and Q1 2026 investment of CNY 132.73 billion (USD 19.47 billion), already running ahead of plan. The region's combined Gross Domestic Product (GDP) neared CNY 10 trillion (USD 1.5 trillion) in 2025, underscoring the scale of industrial and urban investment concentrated there. Chongqing’s 2026 to 2030 action plan also targets new trillion-yuan industrial clusters that support civil and industrial construction demand over the medium term. Research published in January 2026 found that new urbanization and green land-use efficiency are reinforcing each other in Southwest China’s urban agglomerations, which supports sustained construction activity beyond single-year stimulus cycles.

Competitive Landscape

The China formwork market remains fragmented, even though a small group of multinational specialists and listed domestic companies hold stronger positions in the most technical product areas. International firms retain an advantage in climbing systems, hydraulic platforms, and digital planning tools because those categories depend on proprietary engineering, safety validation, and integrated software support. Domestic firms are still expanding their capabilities, and the stronger ones are no longer limited to local mass segments, as they are also competing in overseas infrastructure projects linked to Belt and Road initiatives. Belt and Road construction contracts reached USD 128.4 billion in 2025, up 81% from 2024, and the average deal size rose to USD 964 million, exposing Chinese suppliers to larger, more demanding project environments. This backdrop favors suppliers that can move beyond low-price competition and offer repeatable engineering support across complex sites and export markets.

Technical standards are also raising the floor in the China formwork market. The technical specification T/CASMES 623-2025, issued in November 2025, strengthens minimum requirements for building engineering formwork support systems, which benefits companies with certified product lines and documented engineering processes more than small regional fleets with uneven quality controls. At the same time, carbon and reuse requirements are reducing the old cost advantage of single-use conventional products in premium jobs, because compliance and lifecycle performance now influence procurement more directly. The result is a more selective market where technology depth, documentation quality, and ability to serve high-cycle projects matter more than simple installed presence.

Strategic moves by leading companies show where competition is heading. Doka launched the Shear Wall Climber SCP with FormDrive and introduced the Doka 360 digital customer platform in March 2026, reinforcing the company’s focus on crane-independent high-rise core work and integrated customer workflow management. GETO received a Smart Factory designation and became the first aluminum formwork enterprise in China to obtain the Three-Star China Green Building Material Product Certification in 2025, which strengthened its position in sustainability-led competition. GETO also signed a strategic cooperation framework agreement with the Southwest Regional Headquarters of China Energy Engineering Corporation in 2025, which further aligns its capabilities with green infrastructure and international project execution. The China formwork market is therefore likely to keep consolidating around players that can combine standardized fleets, digital visibility, sustainability credentials, and access to infrastructure-led demand.

China Formwork Industry Leaders

Doka (China) Co., Ltd.

PERI (China) Co., Ltd.

ULMA Construction

China State Construction Engineering Corporation

China Railway Group Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: GETO New Materials participated in the 139th Canton Fair with a dual-exhibition setup spanning formwork, scaffolding, and modular construction, targeting expansion in Southeast Asia, the Middle East, and African markets.

- March 2026: Doka launched the Shear Wall Climber SCP with FormDrive and the Doka 360 digital customer platform at CONEXPO-CON/AGG 2026 in Las Vegas. The Shear Wall Climber SCP eliminates crane dependency with 90 kips of hydraulic lifting capacity, repositioning a typical 500-kips core in minutes and maintaining consistent slab-cycle performance on high-rise core construction.

- December 2025: GETO signed a strategic cooperation framework agreement with the Southwest Regional Headquarters of China Energy Engineering Corporation, targeting joint development in green infrastructure, equipment manufacturing, and international projects.

China Formwork Market Report Scope

The China Formwork Market Report is Segmented by Type (Conventional / Traditional and Modular / System Formwork), Configuration (Static, Climbing, Slipform, and Tunnel), Business Model (Sales and Rental), Sector (Residential, Commercial, Industrial & Logistics and Infrastructure), Material (Timber / Plywood, and More), and Region (North China, East China, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Conventional / Traditional |

| Modular / System Formwork |

| Static |

| Climbing |

| Slipform |

| Tunnel |

| Sales |

| Rental |

| Residential |

| Commercial |

| Industrial and Logistics |

| Infrastructure |

| Timber / Plywood |

| Steel |

| Aluminium |

| Plastic / Fiberglass |

| Other Materials |

| North China |

| East China |

| South China |

| Central China |

| Southwest China |

| Northwest China |

| Northeast China |

| By Type | Conventional / Traditional |

| Modular / System Formwork | |

| By Configuration | Static |

| Climbing | |

| Slipform | |

| Tunnel | |

| By Business Model | Sales |

| Rental | |

| By Sector | Residential |

| Commercial | |

| Industrial and Logistics | |

| Infrastructure | |

| By Material | Timber / Plywood |

| Steel | |

| Aluminium | |

| Plastic / Fiberglass | |

| Other Materials | |

| By Region | North China |

| East China | |

| South China | |

| Central China | |

| Southwest China | |

| Northwest China | |

| Northeast China |

Key Questions Answered in the Report

What is the current size outlook for China formwork demand?

The China formwork market size is projected at USD 1.24 billion in 2025, USD 1.27 billion in 2026, and USD 1.80 billion by 2031, with a 7.22% CAGR over 2026 to 2031.

Which product type leads demand in China?

Modular / system formwork led with 55% share in 2025, and it is also the fastest-growing type with an 8.60% CAGR through 2031.

Why is infrastructure becoming more important for formwork suppliers in China?

Infrastructure is the fastest-growing sector at a 9% CAGR through 2031, and projects in bridges, tunnels, grids, and urban utilities require more specialized and reusable systems than many residential jobs.

Why is rental gaining more acceptance among contractors?

Rental held 58% share in 2025 because it reduces ownership risk, lowers maintenance burden, and gives contractors access to higher-specification systems without carrying full fleet investment.

Page last updated on: