Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

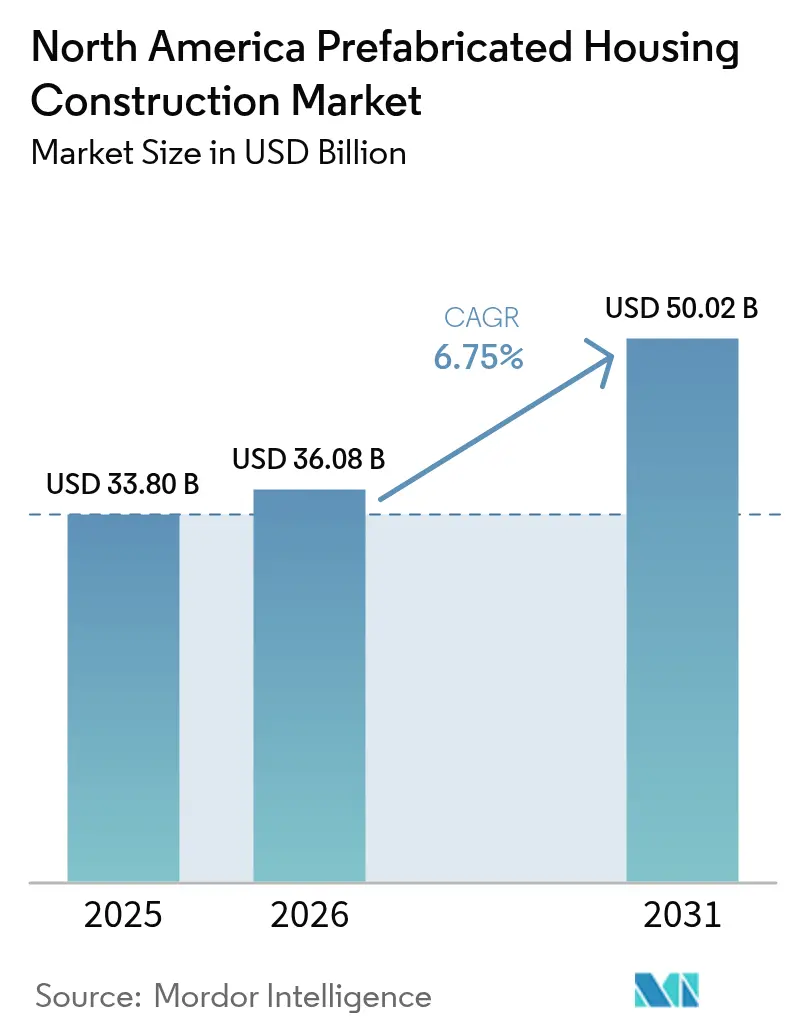

| Base Year Market Size (2025) | USD 33.80 Billion |

| Market Size (2026) | USD 36.08 Billion |

| Market Size (2031) | USD 50.02 Billion |

| Growth Rate (2026 - 2031) | 6.75% CAGR |

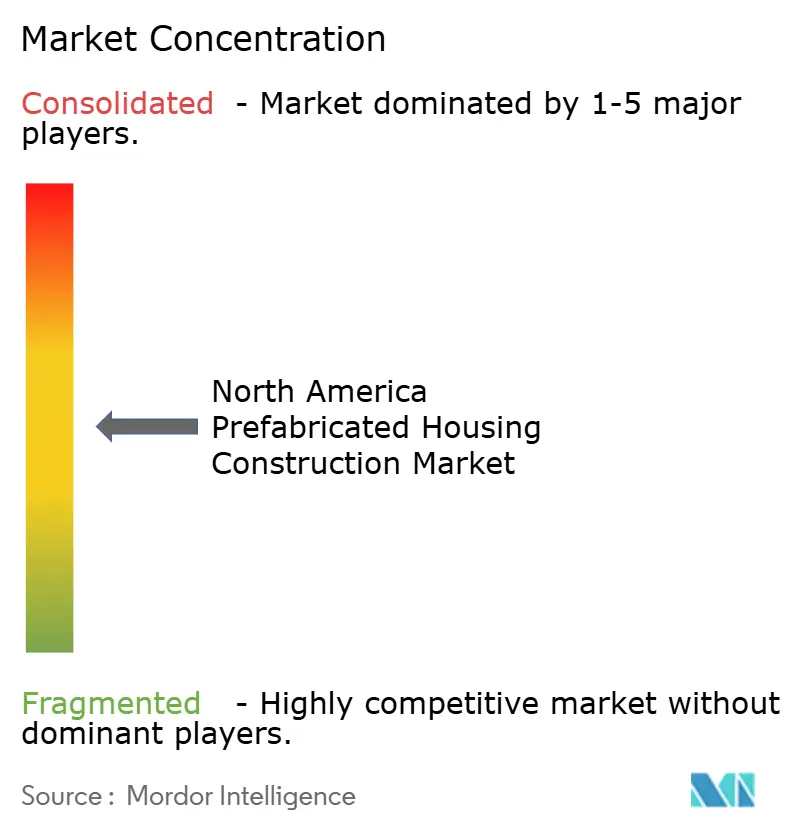

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Prefabricated Housing Construction Market Analysis by Mordor Intelligence

The North America Prefabricated Housing Construction Market size is projected to be USD 33.80 billion in 2025, USD 36.08 billion in 2026, and reach USD 50.02 billion by 2031, growing at a CAGR of 6.75% from 2026 to 2031.

Rising labor shortages, escalating on-site construction costs, and continued housing affordability pressures are steering developers toward factory-based production models that deliver tighter cost control and faster schedules. Builders report that labor now represents 64.4% of median home prices, compressing margins and stimulating demand for modular and panelized solutions that standardize workflows. Institutional investors are channeling capital into build-to-rent portfolios that require rapid, repeatable home delivery, while zoning reforms in several U.S. states are widening the addressable base for factory-built units. Together, these factors are shifting the North America prefabricated housing construction market from a cyclical niche to a structural growth segment.

Key Report Takeaways

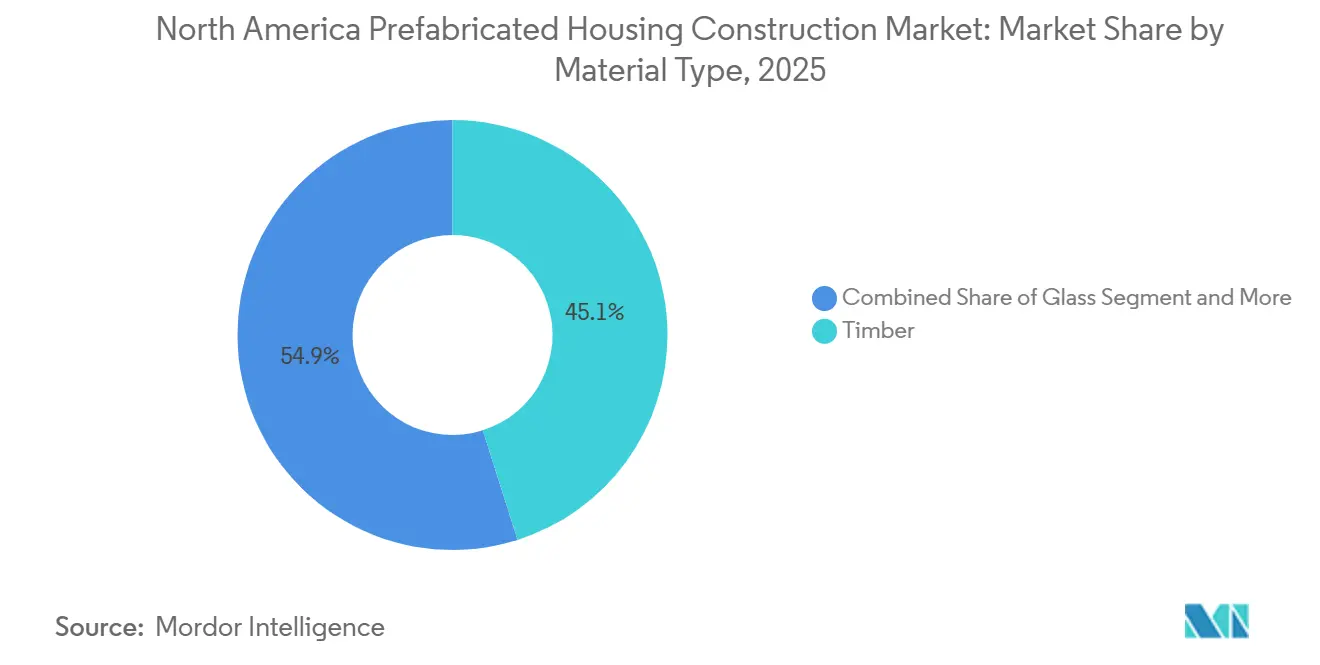

- By material, timber systems led with 45.1% of the North America prefabricated housing construction market share in 2025, while concrete prefabrication is forecast to post the fastest 7.29% CAGR through 2031.

- By housing type, single-family formats captured 61.2% share of the North America prefabricated housing construction market size in 2025, whereas multi-family is projected to advance at 7.16% CAGR to 2031.

- By product type, modular units accounted for 43.4% revenue share in 2025, yet panelized systems are on track for the highest 7.40% CAGR over 2026–2031.

- By geography, the United States held 70.6% of regional revenue in 2025, and Mexico is expected to record the fastest 7.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Prefabricated Housing Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled labor shortages are accelerating the shift to factory-built construction models | +2.1% | United States, Canada | Short term (≤ 2 years) |

| Housing affordability gaps are increasing the demand for lower-cost off-site homes | +1.8% | United States, Canada, Mexico urban centers | Medium term (2–4 years) |

| Rising demand for single-family rentals and build-to-rent communities is boosting volume | +1.6% | United States, early adoption in Canada | Long term (≥ 4 years) |

| Faster project delivery needs supporting modular and panelized adoption | +1.3% | U.S. metro markets, Canadian urban infill | Medium term (2–4 years) |

| Advances in standardized designs and factory automation are improving quality and throughput | +1.2% | United States, Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortages Accelerating Shift to Factory-Built Construction Models

The residential sector will need up to 456,000 additional workers by 2027, yet 92% of contractors already report hiring difficulties[1]Associated General Contractors of America, “Construction Workforce Survey 2025,” agc.org. Factory environments centralize training, enable real-time productivity monitoring, and integrate robotics that slash headcount for repetitive tasks such as panel cutting and fastening. Safety records also improve because high-risk rooftop and scaffolding activities move indoors. These workforce efficiencies translate directly into shorter schedules and more predictable budgets, making off-site methods an attractive hedge against persistent trade shortages across North America.

Housing Affordability Gaps Increasing Demand for Lower-Cost Off-Site Homes

Median U.S. single-family prices hovered between USD 414,000 and USD 446,000 in 2025, and builders faced record material and labor input ratios. Factory-built production lowers waste, eliminates weather delays, and leverages bulk procurement, pushing total delivered cost down by as much as 15% relative to site-built equivalents[2]National Association of Home Builders, “The Cost of Labor Shortages,” nahb.org. Institutional landlords use these savings to offer competitive rents, particularly in Sun Belt states that have relaxed zoning barriers. Policy proposals announced in 2025 favor new construction over resale acquisitions, further redirecting capital into standardized off-site units. As cost pressures persist, affordability remains the single strongest tailwind for the North America prefabricated housing construction market.

Rising Demand for Single-Family Rentals and Build-to-Rent Communities Boosting Volume

Inventory under construction for U.S. build-to-rent climbed 53.5% in 2025 as large landlords sought scale and speed. Standardized factory layouts support rapid portfolio expansion: Invitation Homes inked supply agreements that guarantee modular delivery within 12 months, stabilizing cash flows sooner and reducing maintenance variability across dispersed assets. Legislative signals favoring new-build rentals further concentrate demand in this sub-segment, anchoring volumes for the North America prefabricated housing construction market well into the next decade.

Faster Project Delivery Needs Supporting Modular and Panelized Adoption

Developers face tighter financing covenants and carry costs that penalize overruns. Modular production permits parallel site work and factory fabrication, trimming critical paths by up to 50% and enabling earlier revenue recognition. A 290-unit Los Angeles affordable project is scheduled for completion in 14 months using volumetric modules, compared with 20-plus months for conventional framing. Prefinished wall panels embed plumbing and HVAC lines, cutting weeks of on-site coordination. Faster delivery strengthens lender confidence and qualifies projects for lower borrowing rates, reinforcing the appeal of prefabrication in capital-intensive urban markets.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Zoning and permitting barriers limiting placement and project approvals | -1.4% | U.S. Northeast, select Canadian provinces | Medium term (2–4 years) |

| High transportation and craneage costs reduce savings versus site-built homes | -1.1% | Rural U.S. markets more than 300 miles from factories | Short term (≤ 2 years) |

| Financing and appraisal challenges are slowing buyer and developer adoption | -0.9% | United States, Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Zoning and Permitting Barriers Limiting Placement and Project Approvals

Over 20,000 U.S. permitting authorities apply divergent interpretations of building codes, creating a maze of requirements that dilute the speed edge of factory manufacturing[3]U.S. Department of Housing and Urban Development, “Regulatory Barriers to Factory-Built Housing,” hud.gov. Aesthetic mandates, foundation standards, and minimum lot sizes all inject cost and delay. While Colorado and Texas eased rules in 2025, enforcement remains local, forcing manufacturers into case-by-case compliance and discouraging scale economies. Appraisers unfamiliar with modular valuation further depress loan amounts, compounding the regulatory headwind.

High Transportation and Cranage Costs Reduce Savings Over Site-Built Homes

Volumetric modules often weigh more than 20 tons and require oversize permits, police escorts, and restricted travel windows once haul distances exceed 200–300 miles. Crane packages for multistory sets add USD 15,000–30,000 per site, absorbing much of the factory cost advantage where fuel surcharges and structural steel rentals trend higher. The economics favor panelized formats that ship flat and assemble on-site, yet even panels face freight rate volatility and driver shortages that raise landed costs in remote regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Concrete Gains Ground on Fire and Durability Mandates

Timber held 45.1% of the North America prefabricated housing construction market share in 2025, reflecting entrenched softwood supply chains and decades of builder familiarity. Concrete systems, however, are projected to deliver the fastest 7.29% CAGR through 2031 as wildfire, hurricane, and freeze–thaw concerns push developers toward non-combustible, high-durability envelopes. Precast panels deliver multi-hour fire ratings that lower insurance premiums and achieve Title 24 energy benchmarks in California. Developers along Florida’s Gulf Coast cite concrete’s wind-load resilience as justification for the roughly 12% higher shell cost, an upcharge offset by lower life-cycle maintenance.

Concrete’s rise transforms supply dynamics. Regional precast yards, scale batch plants, and low-carbon cement blends gain traction as ESG targets tighten. Yet timber retains speed advantages. Automated CNC lines cut and fasten cross-laminated timber walls every 10 minutes, providing rapid-cycle framing for smaller builders. Hybrid assemblies are emerging, where light-gauge steel or engineered wood frames combine with concrete floor plates to meet both seismic and thermal codes, underlining material pragmatism in a performance-driven market.

By Housing Type: Multi-Family Adoption Accelerates in Urban Infill Markets

Single-family models dominated with 61.2% of 2025 shipments inside the North America prefabricated housing construction market. Multi-family formats, though, are forecast to log a 7.16% CAGR to 2031 on the back of dense zoning reforms and urgent affordable-housing mandates. The Los Angeles 290-unit modular project reached vertical completion in under four months of site time, proving volumetric stacking can unlock urban land even under tight crane swing constraints. Mid-rise dormitory and workforce-housing schemes echo that template across California, Oregon, and British Columbia universities.

In single-family, institutional landlords favor cookie-cutter floor plans that amortize tooling and design over hundreds of units, while custom homeowners value factory precision and shorter weather windows. For apartments, developers weigh interest-carry savings against upfront module logistics, finding breakeven points at roughly 150 units per site. As rent pressure persists in gateway metros, multi-family prefab captures incremental demand that stick-built crews cannot fulfill in the current labor context.

By Product Type: Panelized Systems Outpace Modular on Transportation Economics

Modular units retained a 43.4% share in 2025, yet panelized systems are on track for a 7.40% CAGR, reflecting the cost benefit of flat-pack logistics that cut freight expenses by up to 60%. One 120-home project in Phoenix shipped full sets of exterior walls on conventional flatbeds, avoiding escort fees and wide-load routing. Architects also appreciate panel flexibility, specifying nonstandard window placements that volumetric widths cannot accommodate.

Manufactured HUD-code homes remain pivotal for entry-level buyers but face financing limitations that confine their market. Hybrid approaches combine factory-finished bathroom pods with site-framed exteriors, allowing higher customization without surrendering the productivity of repeatable wet-area production. As transport costs rise and emissions accounting intensifies, panelized methods stand to erode modular share across longer-haul corridors of the North America prefabricated housing construction market.

Geography Analysis

The United States generated 70.6% of 2025 regional revenue as Sun Belt states lifted zoning barriers and institutional investors scaled build-to-rent pipelines. Fannie Mae and Freddie Mac programs widened funding access, while venture-backed robotics outfits in California and Texas demonstrated 70% faster build cycles that attracted media and municipal attention. These dynamics positioned the United States as both the largest and most technologically dynamic node in the North America prefabricated housing construction market.

Mexico delivers the fastest projected 7.71% CAGR through 2031. An expanding middle class, lower land costs, and parallel labor shortages make factory approaches attractive, even though local supply chains remain nascent. Federal code updates aim to streamline modular approvals, yet developers must manage peso volatility and import tariffs, which favor domestically sourced wall panels and concrete components. Early movers with peso-denominated production bases secure an inherent pricing edge.

Canada trails in market maturity due to fragmented provincial codes and extended haul distances between factories and major metros. Still, federal grant programs launched in 2025 are incentivizing new off-site lines in Ontario and British Columbia, and the Canada Mortgage and Housing Corporation issued template guidelines to standardize appraisals. If interprovincial code harmonization progresses, the Canadian segment could accelerate in the back half of the forecast, particularly in regions battling the widest affordability gaps.

Competitive Landscape

The North America prefabricated housing construction market remains moderately concentrated. The leading manufacturers, including Cavco Industries, Champion Homes, Sekisui House, Legacy Housing, and Skyline Champion, accounted for a significant share of total manufactured housing shipments in 2025. Each operates multiple production plants paired with direct retail or builder networks, leveraging vertical integration to secure lumber supply and guarantee delivery slots. Consolidation intensified in 2025, most notably Cavco’s USD 190 million purchase of American Homestar, which added two Texas factories and 19 retail outlets.

Strategic emphasis centers on automation. ABB-equipped lines in Sekisui’s Nevada plant reduced panel labor hours by 30% within its first year of commissioning, while Champion Homes rolled out BIM-to-shop-floor workflows that shorten engineering lead times to 48 hours. Concurrently, incumbents are forming forward-supply contracts with institutional landlords; Invitation Homes locked a three-year call-off with two leading modular vendors for Sun Belt subdivisions, guaranteeing a baseline volume that underwrites new capacity investments.

Disruptors target cost and design flexibility. ICON is field-testing concrete printers that embed rebar and insulation in a single pass, promising threefold site speed gains. Boxabl raised USD 170 million to scale 400,000 sq ft of folding-module capacity but still battles regulatory delays, highlighting the persistent importance of code alignment. The race for market share now hinges on balancing capital-intensive automation with the agility to navigate local zoning, financing, and logistics realities.

North America Prefabricated Housing Construction Industry Leaders

Clayton Homes

Skyline Champion Corporation

Cavco Industries

Champion Home Builders

Ritz-Craft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Stanley Martin Homes agreed to acquire United Homes Group for USD 221 million, expanding Southeast capacity for modular and panelized lines.

- January 2026: Invitation Homes purchased ResiBuilt Homes for USD 89 million, vertically integrating its build-to-rent supply chain.

- November 2025: Legacy Housing bought AmeriCasa Solutions and the FutureHomeX AI platform in an all-cash deal, broadening digital sales and finance channels.

- October 2025: Sekisui House upsized its U.S. credit facility to USD 1.4 billion, earmarking funds for land and modular capacity expansion.

North America Prefabricated Housing Construction Market Report Scope

By Material

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Housing Type

| Single-Family |

| Multi-Family |

By Product Type

| Modular Homes |

| Panelized & Componentized Systems |

| Manufactured Homes |

| Other Prefab Types |

By Country

| United States |

| Canada |

| Mexico |

| By Material | Concrete |

| Glass | |

| Metal | |

| Timber | |

| Other Materials | |

| By Housing Type | Single-Family |

| Multi-Family | |

| By Product Type | Modular Homes |

| Panelized & Componentized Systems | |

| Manufactured Homes | |

| Other Prefab Types | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How big will factory-built housing be in North America by 2031?

The North America prefabricated housing construction market size is forecast to reach USD 50.02 billion by 2031, growing at a 6.75% CAGR from 2026.

Which material is gaining the fastest in off-site homebuilding?

Precast concrete is the fastest-growing material, set for a 7.29% CAGR through 2031 because of superior fire and storm resilience.

What is driving investor interest in build-to-rent prefabs?

Institutional landlords favor standardized factory output that accelerates lease-up and controls maintenance costs, especially in Sun Belt states with strong population inflows.

Why are panelized systems growing faster than full modular units?

Flat-pack panels avoid oversize hauling fees and permit wider design flexibility, which cuts delivered cost by up to 60% on routes longer than 300 miles.

Which country will post the highest growth through 2031?

Mexico is projected to expand at a 7.71% CAGR as middle-income demand rises and new factories come online.

What limits broader prefab adoption today?

Patchwork zoning rules, oversized transport costs, and inconsistent appraisals remain the main barriers yet to be fully resolved across North America.

Page last updated on: