Apple Juice Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 20.77 Billion |

| Market Size (2031) | USD 28.32 Billion |

| Growth Rate (2026 - 2031) | 6.39% CAGR |

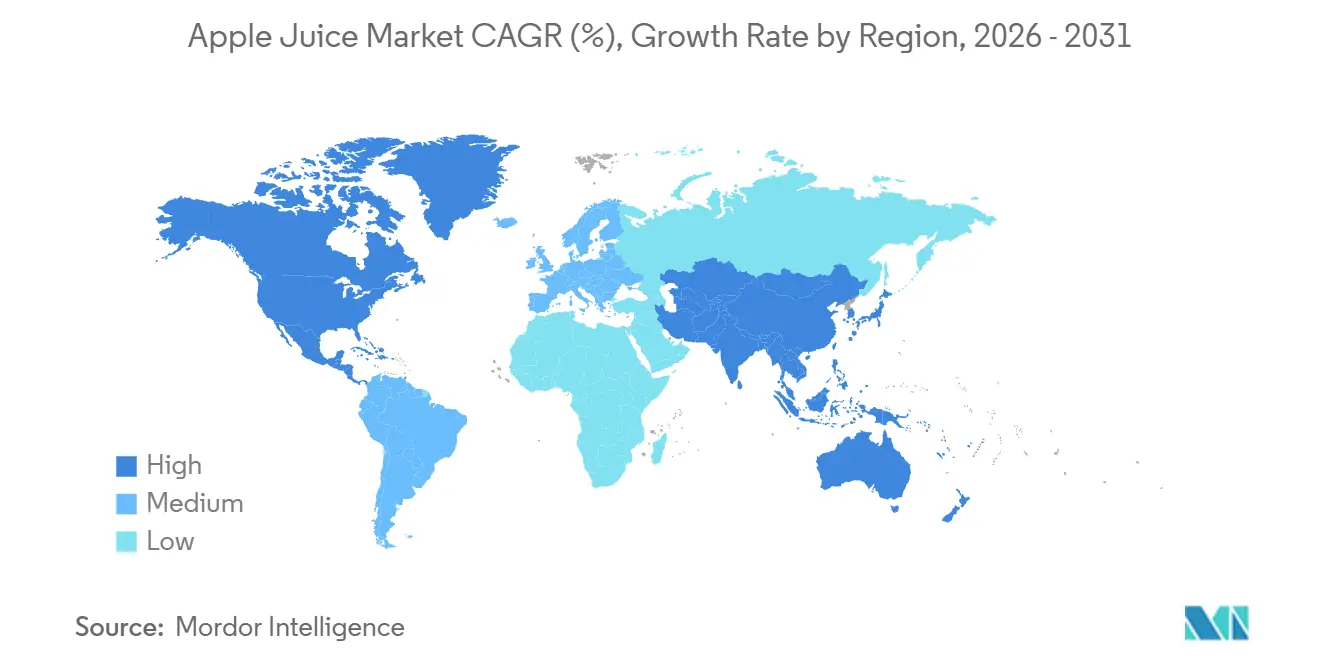

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Apple Juice Market Analysis by Mordor Intelligence

The apple juice market reached USD 19.56 billion in 2025, is expected to reach USD 20.77 billion in 2026, and is forecast to attain USD 28.32 billion by 2031, advancing at a CAGR of 6.39% during 2026-2031. This trajectory reflects sustained consumer preference for convenient, nutritious beverages amid rising health consciousness and on-the-go consumption patterns. Portable packs, especially pouches, are redefining on-the-go consumption, driving growth as schools and convenience stores expand single-serve listings. North America leads the market, driven by established breakfast routines and institutional demand, while Asia-Pacific has emerged as the fastest-growing region, propelled by urbanization, expanding middle-class spending, and retail modernization across China, India, and Southeast Asia. Strategic differentiation focuses on varietal labeling, functional fortification, organic certification, and packaging innovation to mitigate commodity pricing pressure. A critical supply-side tension persists as China supplies approximately two-thirds of U.S. apple juice concentrate imports, creating exposure to trade policy shifts, quality scrutiny, and geopolitical risks. Meanwhile, alternative sourcing from Poland, Turkey, Ukraine, and Moldova is expanding to diversify procurement.

Key Report Takeaways

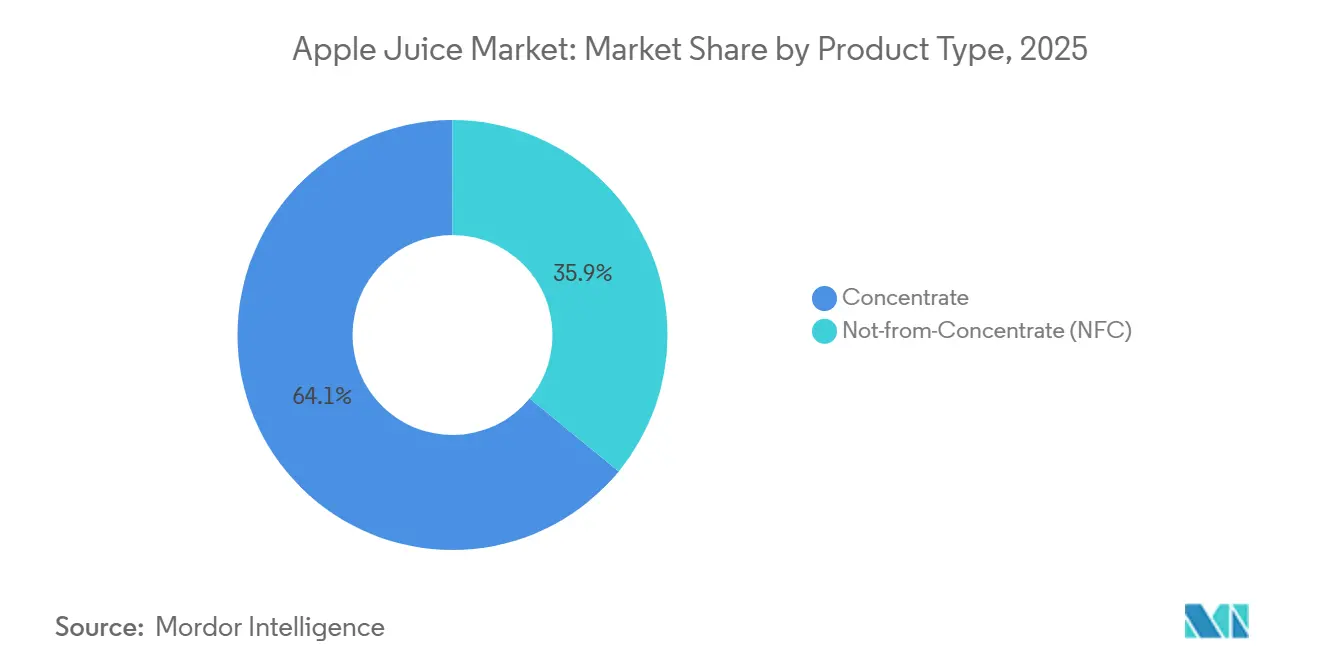

- By product type, concentrate commanded 64.04% share of the apple juice market size in 2025, while Not-from-Concentrate (NFC) is projected to log the segment-leading 7.24% CAGR through 2031.

- By nature, conventional products held 88.23% of 2025 sales, whereas organic juice charts the fastest growth at an 8.05% CAGR over 2026-2031.

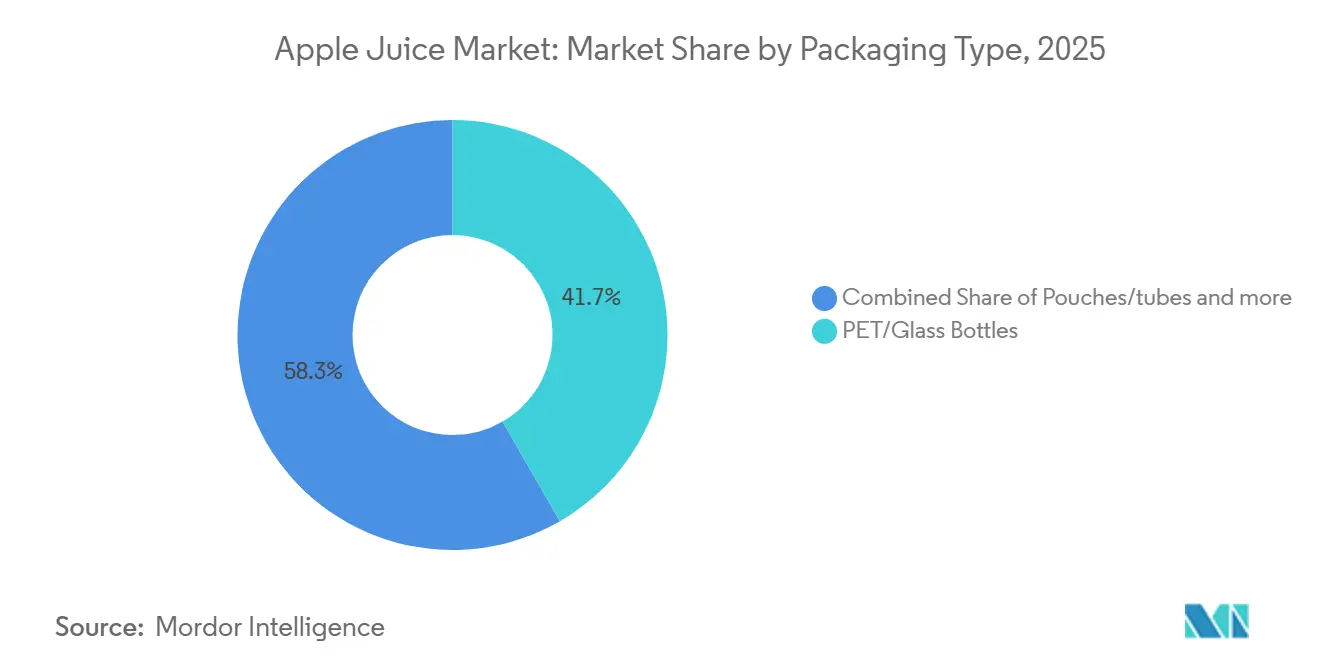

- By packaging type, PET/glass bottles led with 41.67% of 2025 revenues; pouches/tubes offer the strongest upside at an 8.22% CAGR to 2031.

- By distribution channel, retail channels accounted for 73.21% of global 2025 turnover, but foodservice and HoReCa are expanding at a 6.89% CAGR from 2026-2031.

- By geography, North America dominated at 37.66% share in 2025 and Asia-Pacific is slated to register the swiftest 6.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Apple Juice Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for on-the-go juice packaging | +0.9% | North America and Western Europe lead; emerging in urban Asia-Pacific | Medium term (2-4 years) |

| Increasing demand for juices in hotel breakfast menus | +0.7% | Global, with regional peaks (North America autumn/winter; Asia-Pacific Lunar New Year; Middle East Ramadan) | Medium term (2-4 years) |

| Growing preference for premium and organic juices | +1.2% | Global, particularly North America and Europe | Long term (≥4 years) |

| Seasonal promotions and festival-driven consumption | +0.5% | Global, with higher impact in emerging markets building brand trust | Short term (≤2 years) |

| Marketing campaigns highlighting wellness benefits | +0.8% | North America and Western Europe lead; emerging in urban Asia-Pacific | Medium term (2-4 years) |

| Consumer attraction to recognizable brands | +0.6% | Global, with regional peaks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for on-the-go juice packaging

Single-serve and portable formats are transforming apple juice distribution as urbanization and fast-paced lifestyles drive demand for convenient, on-the-go beverage options. Convenience stores are increasingly prioritizing apple juice pouches and cans, catering to impulse purchases and children's lunchboxes. Additionally, the growing preference for healthier beverage choices among consumers has further boosted the demand for single-serve apple juice products. Tetra Pak's introduction of paper-based barrier technology for aseptic cartons in Spain, featuring up to 92% renewable content and a Carbon Trust-verified 43% lower carbon footprint compared to aluminum-foil cartons, highlights the rising importance of sustainable packaging solutions. This innovation positions eco-friendly on-the-go packaging as a key competitive differentiator for premium apple juice brands. Furthermore, bag-in-box formats, which offer airtight dispensing and reduced oxidation, are gaining popularity in foodservice and institutional channels. These formats address critical needs such as cost efficiency per serving and extended freshness post-opening, making them an attractive option for bulk consumption in hotels, restaurants, and catering services.

Increasing demand for juices in hotels' breakfast menu

Juice remains a breakfast staple in foodservice, with consumers frequently ordering apple juice during breakfast hours. Operators are differentiating their offerings through fresh-pressed, functional, and seasonal juice options. Apple juice is often incorporated into multi-ingredient blends, such as Snooze's Super Greens (kale, cucumber, celery, ginger, apple, lemon, agave) and First Watch's Morning Meditation (orange, lemon, turmeric, ginger, agave, beets), leveraging apple's natural sweetness to balance vegetable and spice notes. Premium hotels and brunch venues are introducing juice flights and small-format pours paired with bite-sized foods, borrowing from wine-tasting formats to encourage sampling and upselling. The sober-curious movement is expanding nonalcoholic beverage programs, where single-fruit apple juices and apple-based mocktails serve as sophisticated alternatives to alcohol, appealing to wellness-focused and inclusive dining experiences. Spiced apple cider with star anise and other culinary-driven preparations are featured in holiday pop-up bars, positioning apple juice as a versatile ingredient for limited-time offerings and seasonal menus.

Growing preference for premium and organic juices

Organic apple juice sales have witnessed significant growth, driven by increasing consumer demand for clean-label products. The U.S. organic beverage market has shown strong performance, with sales in the organic beverage segment growing, alongside the rising popularity of new organic apple varieties [1]Organic Trade Association, "Growth of U.S. Organic Marketplace Accelerated in 2024", ota.com. This trend reflects a preference for avoiding synthetic pesticides, embracing non-GMO options, and aligning with popular dietary trends such as keto and paleo. Not-from-concentrate processing, which retains the natural flavor, color, and nutritional benefits through minimal heat exposure, is perceived as more natural and continues to command premium pricing despite offering similar nutritional profiles to reconstituted juice. Additionally, cold-pressed and cloudy apple juice variants, known for preserving polyphenols and antioxidants, are gaining traction. These variants are increasingly available in specialty stores and e-commerce platforms, often marketed with attributes such as low-calorie content, organic certification, or functional health benefits. The growing focus on health-conscious consumption and sustainable production practices is expected to further drive the demand for organic and minimally processed apple juice in the coming years.

Seasonal promotions and festival-driven consumption

Seasonal promotions capitalize on this cyclical demand, with retailers prominently featuring apple juice and cider in September-November displays alongside Halloween and Thanksgiving meal bundles. These promotions often include recipe suggestions, such as apple cider-based cocktails or desserts, to drive consumer engagement. In the Middle East, Ramadan drives elevated juice consumption for iftar meals, with apple juice blends and fortified variants positioned as hydration and energy solutions after fasting. Similarly, Asia-Pacific markets experience demand spikes during Lunar New Year and Mid-Autumn Festival, where gifting premium juice sets and organic apple juice is a common tradition. Festival-specific packaging, limited-edition flavors (e.g., spiced apple, apple-cinnamon), and multi-pack promotions enable brands to capture incremental volume and encourage trial during high-traffic periods. Additionally, brands are leveraging digital marketing campaigns and influencer partnerships to highlight the versatility of apple juice in festive recipes and celebrations. Inventory planning and marketing alignment to these seasonal peaks are critical for maximizing sales and minimizing post-season markdowns, particularly for perishable Not-from-concentrate (NFC) and fresh-pressed products with shorter shelf lives.

High sugar content concerns among consumers

Apple juice contains sugar and lacks the fiber present in whole apples, leading to rapid glucose absorption and reduced satiety. Health Canada's front-of-package nutrition symbol regulations, enforced from January 2026, will require "high in sugars" warnings on most apple juice products when sugar content exceeds 15% of the daily value per reference amount [2]Health Canada, "Front-of-package nutrition symbol labelling guide for industry", canada.ca. This regulation is expected to deter health-conscious consumers and limit promotional claims on principal display panels. Additionally, pediatric guidelines from the American Academy of Pediatrics recommend restricting juice intake to 4 oz daily for children aged 1-3, 6 oz for ages 4-6, and 8 oz for ages 7-18, while advising against juice consumption for infants under 12 months. These guidelines further constrain the primary consumer demographic. In response, brands are introducing diluted juice options, sugar-reduced formulations, and functional blends incorporating vegetables, spices, or protein to enhance nutritional profiles and appeal to wellness-focused parents. However, reformulation poses challenges, as it may alter taste and affect consumer acceptance. Furthermore, "no added sugar" labeling does not address concerns about the glycemic impact of naturally occurring sugars, limiting the effectiveness of these strategies in fully addressing sugar-content scrutiny.

Volatility in apple raw material prices

Apple raw material prices are influenced by harvest variability, weather shocks, labor cost inflation, and trade policy shifts, creating procurement challenges for juice processors. Rising labor costs have increased due to higher H-2A minimum wage rates and regulatory compliance, doubling breakeven costs for some orchards and threatening their long-term viability. Europe's apple production for 2025-2026 has been revised upward to 10.9-11.0 million tonnes; however, quality issues have redirected higher volumes toward processing, balancing fresh-market potential while tightening stocks later in the season [3]Poland Fruits Trade Cooperation, "Prognosfruit 2025/2026: EU Apple and Pear Production Revised Upwards", polandfruits.pl. In China, apple juice concentrate exports have declined significantly, from 1,031,000 tonnes in 2007 to 268,000 tonnes in 2023, due to rising domestic consumption and quality and safety concerns. This has forced U.S. importers to diversify sourcing to countries like Poland, Turkey, Ukraine, and Moldova, where lower labor costs and favorable production conditions offer competitive pricing but introduce new supply chain risks. To mitigate price volatility and ensure consistent raw material availability, processors are adopting forward contracts, investing in precision agriculture and yield forecasting, and building relationships with multiple regional suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Concentrate Dominance Faces NFC Quality Challenge

Apple juice concentrate accounted for 64.04% of the market share in 2025, driven by its cost advantages, extended shelf life, and ease of transport. These factors make concentrate the preferred format for large-scale manufacturers, foodservice operators, and export markets. The production process for concentrate involves removing water through evaporation, reducing volume and weight. This reduction lowers logistics costs and enables ambient storage, which is crucial for markets with limited cold-chain infrastructure. Despite a decline from historical peaks, China's concentrated apple juice exports still supplied approximately two-thirds of U.S. apple juice concentrate imports in recent years, underscoring concentrate's role as a tradable commodity and a key component of the global supply chain. Concentrate remains dominant in price-sensitive segments, private-label products, and bulk ingredient supply to food manufacturers.

Not-from-concentrate (NFC) apple juice is projected to grow at a CAGR of 7.24% through 2031, driven by consumer perceptions that NFC products are more natural, retain superior flavor and aroma, and preserve higher levels of vitamin C and polyphenols compared to reconstituted juice. NFC processing minimizes heat exposure and oxidation, utilizing high-pressure processing and cold-chain logistics to maintain fresh-like quality. This format commands premium pricing despite having similar nutritional profiles to concentrate-based juice. Processors are increasingly investing in NFC capacity to meet the growing demand for premiumization. NFC is well-positioned for retail premium tiers, specialty stores, and organic channels, where quality perception justifies higher prices.

By Nature: Organic Surge Challenges Conventional Scale

Conventional apple juice accounted for 88.23% of the market share in 2025, driven by well-established supply chains, cost-effective production methods, and widespread availability across retail and foodservice channels. The use of synthetic fertilizers, pesticides, and post-harvest treatments in conventional production ensures higher yields and reduced crop losses, enabling processors to procure apples at competitive prices. This cost advantage allows manufacturers to maintain pricing flexibility and cater to a broad consumer base. The segment's growth is also supported by advancements in processing technologies, which enhance product shelf life and quality while keeping production costs low. Conventional apple juice is expected to sustain its leadership position through value-driven pricing strategies, extensive distribution networks, and consistent product availability.

Organic apple juice is accelerating at an 8.05% CAGR through 2031, capturing consumer demand for clean-label, non-GMO, and pesticide-free products aligned with health and environmental values. Strategic shifts toward organic processing near orchard sources aim to reduce emissions and improve efficiency. This cost disparity limits organic juice's ability to compete on price with conventional options. However, the segment's growth trajectory indicates sustained consumer willingness to pay a premium for perceived health and sustainability benefits. Regulatory frameworks such as USDA Organic, EU Organic, and emerging standards in the Asia-Pacific region are critical for organic market access and consumer trust.

By Packaging type: PET Bottles Lead, Pouches Capture Convenience

PET/glass bottles accounted for 41.67% of apple juice packaging in 2025, reflecting consumer familiarity, retail shelf compatibility, and versatility across pack sizes from single-serve 250 ml to family-size 1.5-2 liter formats. PET offers lightweight, shatter-resistant, and recyclable properties, with oxygen-barrier PET technologies extending shelf life and protecting flavor and vitamin content, making it the preferred material for mainstream retail distribution. Glass bottles, exemplified by premium quality, nostalgia, and gift-worthiness, command higher price points and shelf differentiation in specialty and organic segments. Sustainability pressures are accelerating the adoption of recyclable, biodegradable, and renewable-content packaging, with brands balancing environmental claims, regulatory compliance (e.g., plastic waste management rules), and consumer willingness to pay for eco-friendly materials.

Pouches/tubes are expanding at 8.22% CAGR through 2031, driven by portability, single-serve convenience, and appeal to children and on-the-go consumers. These formats are particularly popular in school lunch programs, outdoor activities, and travel-friendly scenarios due to their lightweight and spill-resistant designs. Innovations such as resealable spouts, eco-friendly materials, and vibrant branding are further enhancing their appeal. Tetra Pak aseptic cartons, while not separately quantified in the segmentation, held significant share in ambient juice distribution, and Tetra Pak's December 2025 launch of paper-based barrier technology in Spain, featuring up to 92% renewable content and a 43% lower carbon footprint versus aluminum-foil cartons, positions sustainable aseptic packaging as a competitive differentiator for environmentally conscious brands. Cans, though a smaller segment, offer durability, rapid chilling, and vending-machine compatibility, appealing to foodservice and impulse-purchase occasions. Bag-in-box formats, used primarily in foodservice and institutional channels, provide cost-effective bulk dispensing, extended post-opening freshness through collapsing bag design that minimizes air contact, and reduced packaging waste, making them attractive for schools, cafeterias, and catering.

By Distribution Channel: Retail Dominance, Foodservice Acceleration

Retail channels accounted for 73.21% of apple juice distribution in 2025, encompassing supermarkets, hypermarkets, specialty stores, online retail, and other outlets catering to household consumption. Supermarkets and hypermarkets drove volume sales through wide assortments, competitive pricing, and promotional visibility, with a significant share of fruit juice sold in 1-liter and 1.5-liter PET formats. Specialty stores, while smaller in absolute volume, focused on organic, premium, and cold-pressed apple juice offerings that commanded higher margins and attracted health-conscious shoppers. Online retail gained traction with subscription models and direct-to-consumer platforms, enabling niche and organic brands to reach consumers without traditional retail distribution, reducing intermediary costs, and fostering direct customer relationships.

Foodservice/HoReCa channels are projected to grow at a 6.89% CAGR through 2031, driven by breakfast menu innovation, premium juice offerings in hotels and restaurants, and fresh-pressed juice programs that enhance dining experiences. Sober-curious and wellness trends are expanding nonalcoholic beverage programs in bars and restaurants, where apple juice and apple-based mocktails serve as sophisticated alternatives to alcohol, capturing incremental sales occasions beyond traditional breakfast and brunch. Foodservice channels also benefit from bulk packaging formats, such as bag-in-box and 1,000-liter totes, which reduce per-serving costs and simplify inventory management, making apple juice an economical beverage option for schools, hospitals, airlines, and corporate cafeterias.

Geography Analysis

North America held 37.66% market share in 2025, driven by entrenched breakfast routines, institutional demand from schools and hospitals, and established retail distribution across supermarkets, convenience stores, and foodservice operators. Regulatory pressures are intensifying, with Health Canada's front-of-package "high in sugars" labeling is potentially dampening impulse purchases and requiring brands to adjust marketing strategies. North America's mature market status, declining per-capita juice consumption, and competition from alternative beverages constrain growth, yet premiumization, organic expansion, and functional fortification offer pathways to sustain value growth even as volume stagnates.

Asia-Pacific emerged as the fastest-growing region with a projected CAGR of 6.74% through 2031, propelled by urbanization, rising disposable incomes, expanding middle-class populations, and retail modernization across China, India, Japan, and Southeast Asia. China dominates apple concentrate exports internationally, though domestic consumption is rising and export volumes have declined from historical peaks as affluence shifts demand toward fresh fruit and premium beverages. India is experiencing rapid growth in organized retail and e-commerce, improving accessibility to packaged juices and enabling brands to reach tier-2 and tier-3 cities previously underserved by traditional distribution. Japan's aging population and health consciousness are driving demand for functional and fortified apple juice variants enriched with calcium, vitamin D, and probiotics, while South Korea and Singapore exhibit high per-capita juice consumption and willingness to pay premiums for imported organic and cold-pressed products. However, competition from locally abundant tropical fruit juices (mango, guava, pineapple) and lower price points for domestic products present challenges for apple juice penetration.

Europe's apple juice market benefits from strong 100% juice consumption. The 2025-2026 EU apple crop was revised upward to 10.9-11.0 million tonnes, ranking as the sixth-largest crop of the decade, with Poland, Germany, Belgium, France, and the Netherlands contributing most of the upward revision. Turkey's apple juice concentrate exports increased to 167,000 tonnes in 2023 with a strong revealed comparative advantage (RCA >4), supported by favorable production conditions and lower-cost structures. Germany, the United Kingdom, and the Netherlands are major importers, with Germany historically receiving majority of Poland's apple juice concentrate exports, though Poland's export destinations have diversified in recent years. Europe's emphasis on sustainability, recyclable packaging, and organic certification is driving innovation, and brands adopting paper-based barriers, reduced plastic, and carbon-neutral production to meet consumer and regulatory expectations.

Competitive Landscape

The apple juice market exhibits moderate consolidation, characterized by a mix of multinational beverage conglomerates, regional cooperatives, private-label suppliers, and niche organic brands competing across various price tiers, distribution channels, and product formats. Leading multinational players such as The Coca-Cola Company (Minute Maid), PepsiCo (Tropicana), and Kraft Heinz (Capri Sun) leverage extensive global distribution networks, strong brand equity, and large-scale marketing capabilities to dominate mainstream retail and foodservice channels. Meanwhile, farmer-owned cooperatives like Tree Top and Knouse Foods hold significant processing capacity and raw material sourcing advantages in North America, enabling vertical integration and cost efficiency. For instance, Tree Top operates eight facilities across Washington, Oregon, and California, processes approximately 1 billion pounds of fruit annually, and supplies both branded consumer products and bulk ingredients to major food and beverage manufacturers, including PepsiCo and Quaker.

Strategic differentiation in the market focuses on varietal labeling (e.g., Honeycrisp, Cosmic Crisp), functional fortification (e.g., calcium, vitamin D, probiotics), organic certification, and packaging innovation to mitigate commodity pricing pressures and justify premium pricing. Opportunities for growth include functional apple juice blends (e.g., apple-ginger-turmeric, apple-chia), low-sugar reformulations, sustainable packaging solutions (e.g., paper-based barriers, biodegradable materials), and direct-to-consumer e-commerce channels that bypass traditional retail intermediaries, enabling higher margins and enhanced consumer data collection. Emerging disruptors in the market include cold-pressed juice startups, organic-focused brands emphasizing traceability and origin storytelling, and co-packers offering flexible manufacturing solutions for smaller brands seeking market entry without significant capital investments.

Technological advancements such as precision agriculture, yield forecasting, blockchain traceability, and aseptic processing innovations are enabling processors to optimize raw material utilization, reduce waste, ensure food safety, and meet retailer and regulatory demands for transparency and sustainability. However, intense competition, retailer consolidation, and consumer price sensitivity continue to constrain profitability. Many growers face prices below production costs, while processors operate on thin margins, necessitating ongoing efficiency improvements, scale advantages, and product innovation to remain viable in this mature and commoditized market.

Apple Juice Industry Leaders

-

The Coca-Cola Company

-

PepsiCo Inc.

-

Tree Top Inc.

-

Old Orchard Brands, LLC

-

Mott's LLP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Tree Top Inc. announced plans to acquire 40 acres from the Port of Benton adjacent to its Prosser, Washington facility for approximately USD 2 million, with proposed investments of USD 22-25 million in developing a new warehouse and, eventually, manufacturing facilities on the site.

- February 2026: Refresco agreed to acquire SunOpta in an all-cash transaction valuing SunOpta at USD 6.50 per share, amounting to approximately USD 1.1 billion. The acquisition, expected to close in Q2 2026, aims to expand Refresco's presence in the plant-based beverages market while strengthening its North American footprint to achieve a more balanced geographic portfolio.

- October 2025: Manzana Products Co. relocated its entire operation from California to Sunnyside, Washington, leasing and developing a 275,895 sq ft facility (former Seneca Foods site) to produce organic apple juices, applesauce, sauces, and cider vinegar.

- October 2025: ALCA Corp launched the first products filled on SIG's new SIG Prime 55 In-Line Aseptic spouted pouch system, featuring in-line pouch sterilization, up to 55 pouches per minute fill capacity, and 30-500 ml fill volumes, reducing operating costs and enabling aseptic retail spouted pouches for juice brands.

Global Apple Juice Market Report Scope

The apple juice market is segmented by product type, nature, packaging, distribution channel, and geography. Based on product type, the market is segmented into apple juice concentrate and not-from-concentrate (NFC). By nature, the market is segmented into conventional and organic. By packaging, the market has been segmented into PET/glass bottles, Tetra Pak, cans, pouches/tubes, and others. By distribution channels, the market has been segmented into foodservice/HoReCa and retail. By retail, the market has been segmented into supermarkets/hypermarkets, specialty stores, online retail stores, and other distribution channels. By geography, the market has been segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (USD) and volume (Tons).

| Apple Juice Concentrate |

| Not-from-Concentrate (NFC) |

| Organic |

| Conventional |

| PET/Glass Bottles |

| Tetra Pak |

| Cans |

| Pouches/tubes |

| Others |

| Foodservice/HoReCa | |

| Retail | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

| By Product Type | Apple Juice Concentrate | |

| Not-from-Concentrate (NFC) | ||

| By Nature | Organic | |

| Conventional | ||

| By Packaging Type | PET/Glass Bottles | |

| Tetra Pak | ||

| Cans | ||

| Pouches/tubes | ||

| Others | ||

| By Distribution Channel | Foodservice/HoReCa | |

| Retail | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the apple juice market?

The apple juice market size is USD 19.56 billion in 2025 and is forecast to reach USD 28.3 billion by 2031.

Which region will post the fastest advance through 2031?

Asia-Pacific is forecast to achieve a 6.74% CAGR on urbanization, retail modernization, and rising middle-class spending.

What packaging format is growing quickest?

Pouches and tubes, propelled by school lunchbox demand and aseptic technology improvements, are expanding at 8.22% CAGR.

Why are NFC products gaining share over concentrate?

NFC retains fresher taste and up to 30% more vitamin C, supporting a 7.24% CAGR despite higher logistics costs.

How big is the organic slice and how fast is it growing?

Organic juice represented 11.77% of 2025 sales and is scaling at an 8.05% CAGR on clean-label and premium trends.

Page last updated on: