Cold Pressed Juice Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

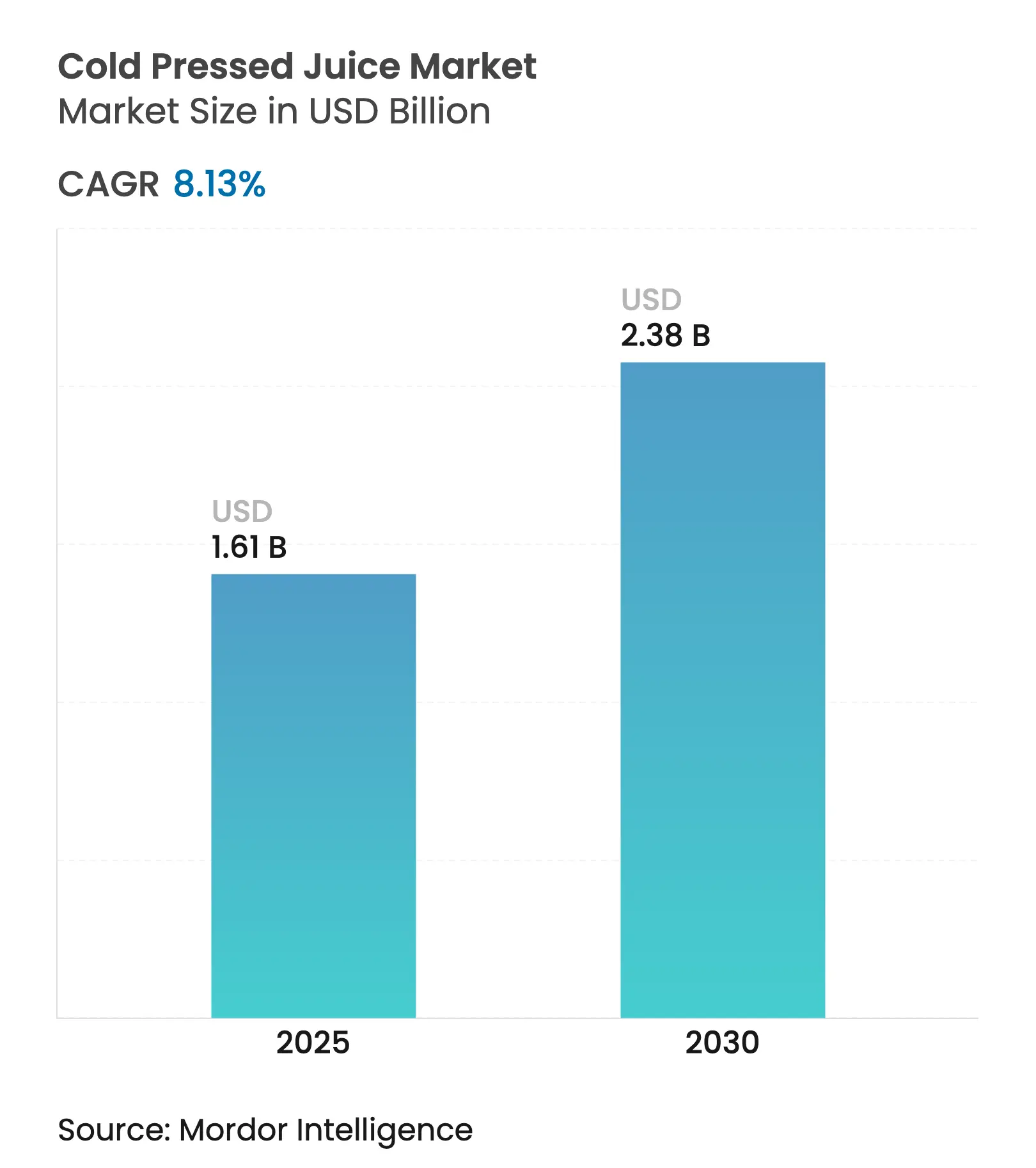

| Market Size (2025) | USD 1.61 Billion |

| Market Size (2030) | USD 2.38 Billion |

| Growth Rate (2025 - 2030) | 8.13 % CAGR |

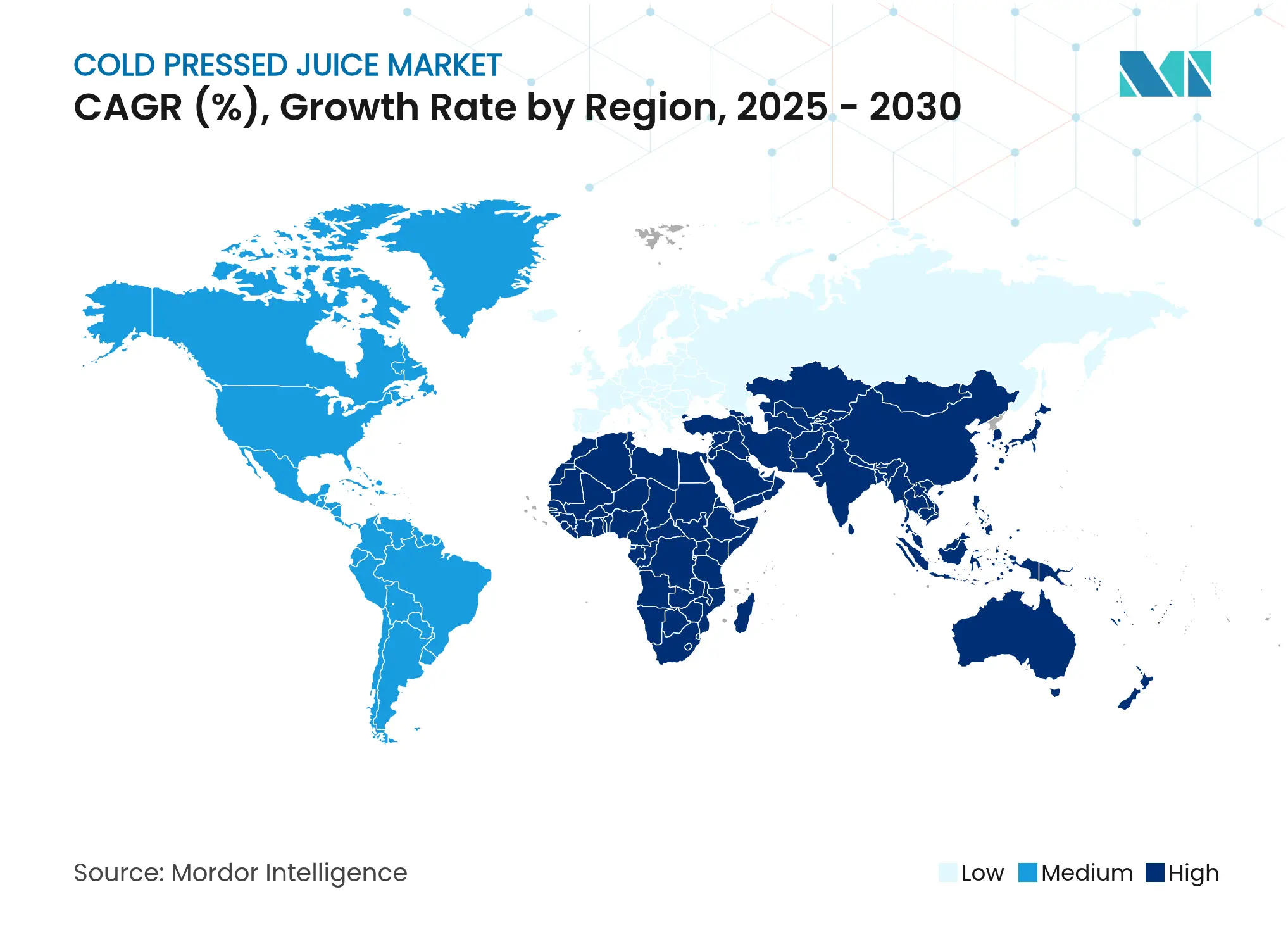

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

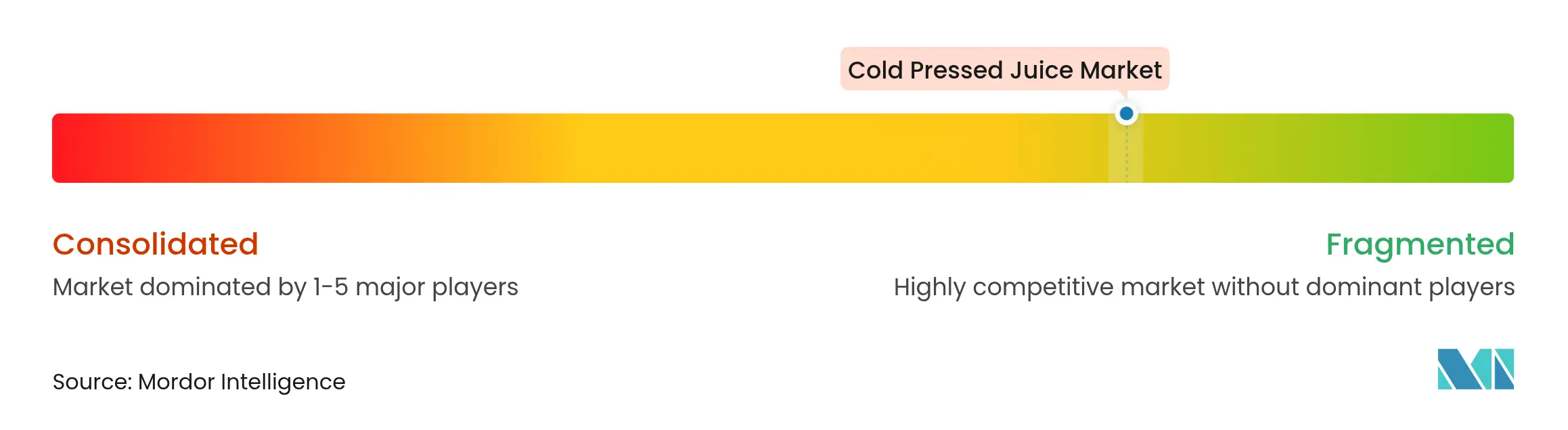

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Cold Pressed Juice Market Analysis by Mordor Intelligence

The cold-pressed juice market size is estimated to be USD 1.61 billion in 2025 to USD 2.38 billion by 2030, registering a CAGR of 8.13%. This growth is primarily driven by increasing global health awareness, a shift toward premium and convenient breakfast options, and advancements like high-pressure processing technology, which extends shelf life while retaining nutritional value. Regulatory standards, such as the FDA's Juice HACCP requirements, play a crucial role in enhancing consumer trust and encouraging product innovation. Additionally, the rising demand for functional wellness beverages, the expansion of online retail channels, and the adoption of sustainable packaging solutions are further strengthening the market's growth prospects.

Key Report Takeaways

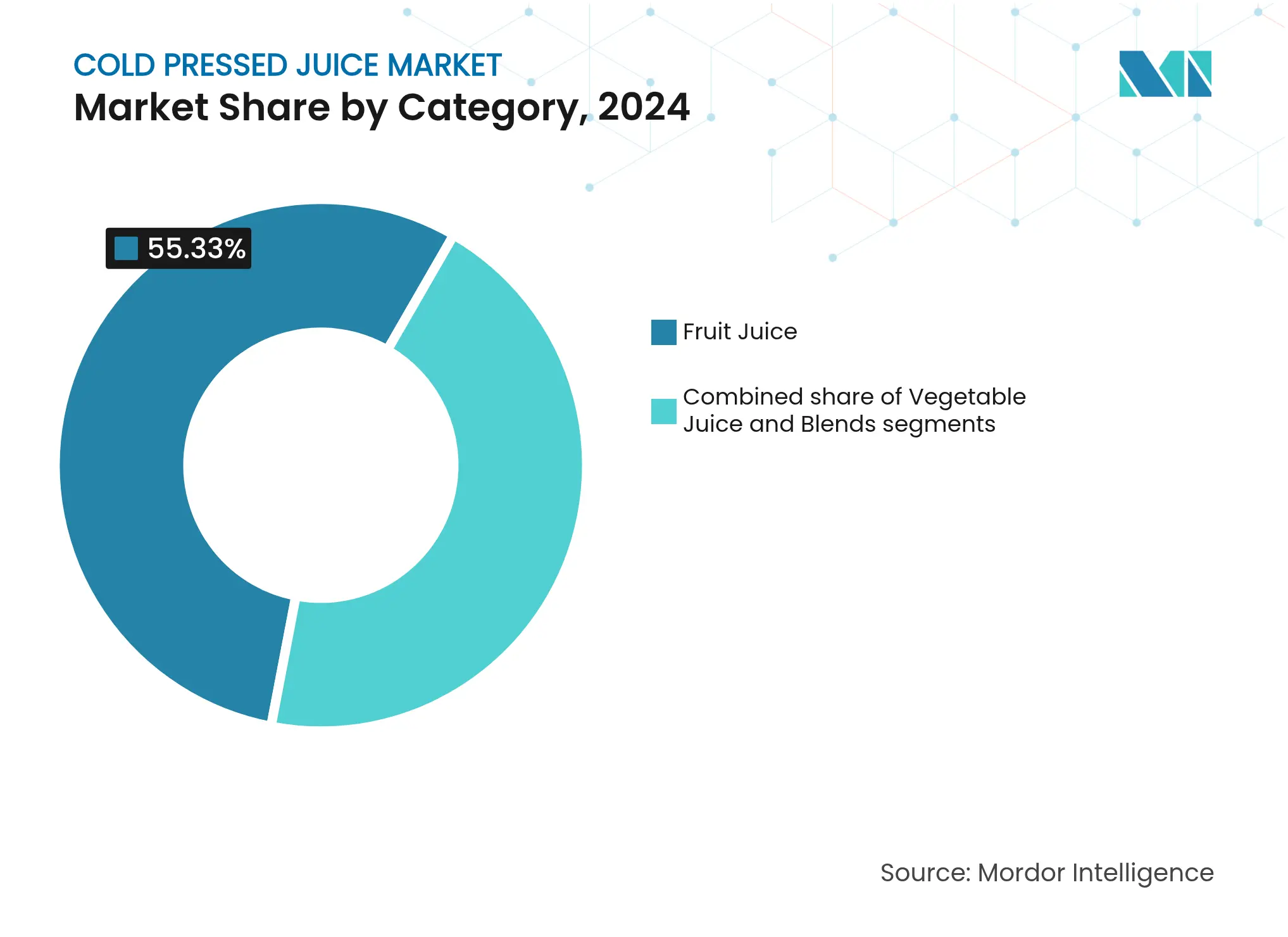

- By category, fruit juice led with 55.33% cold-pressed juice market share in 2024, whereas blends are forecast to expand at a 9.77% CAGR to 2030.

- By nature, conventional products captured 72.13% share of the cold-pressed juice market in 2024, while organic variants recorded the highest projected CAGR at 11.67% through 2030.

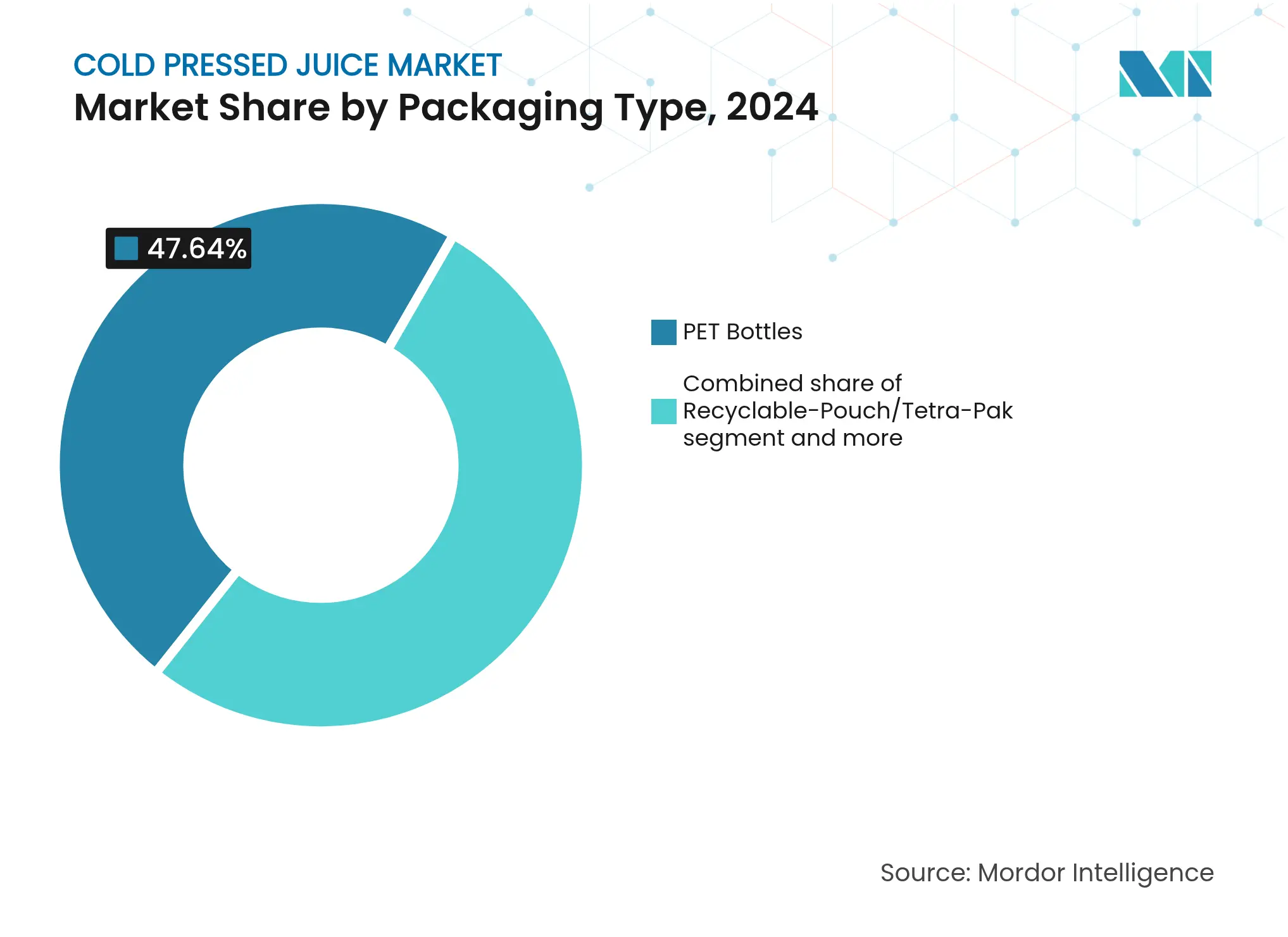

- By packaging, PET bottles held 47.64% revenue share in 2024; the recyclable-pouch/tetra-pak formats segment is set to grow at a 10.80% CAGR through 2030.

- By distribution channel, off-trade outlets maintained a 64.47% share in 2024, whereas online sales show the fastest 12.67% CAGR to 2030.

- By geography, North America commanded 33.67% of the cold-pressed juice market in 2024, and Asia-Pacific exhibits the quickest 11.93% CAGR through 2030.

Global Cold Pressed Juice Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising demand for functional-health beverages Rising demand for functional-health beverages | +1.2% | Global, with strong momentum in North America and Asia-Pacific | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:Global, with strong momentum in North America and Asia-Pacific | Impact Timeline:Medium term (2-4 years) |

Growing health consciousness Growing health consciousness | +0.8% | Global, particularly pronounced in developed markets | Long term (≥ 4 years) | |||

Premiumisation of on-the-go breakfast among consumers Premiumisation of on-the-go breakfast among consumers | +0.6% | North America and European Union core, expanding to Asia-Pacific urban centers | Medium term (2-4 years) | |||

Growing demand for clean label and organic juices Growing demand for clean label and organic juices | +0.4% | North America and European Union, with emerging traction in Asia-Pacific | Long term (≥ 4 years) | |||

Surge in D2C subscription models Surge in D2C subscription models | +0.3% | North America and European Union, early adoption in Asia-Pacific metros | Short term (≤ 2 years) | |||

Rising disposable incomes enabling premium purchases Rising disposable incomes enabling premium purchases | +0.2% | Asia-Pacific core, with spillover to emerging markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising demand for functional-health beverages

As consumers increasingly prioritize immunity support, gut health, and cognitive wellness, beverage formulations are evolving beyond their traditional nutritional profiles. The functional beverage segment is witnessing significant growth, driven by health-conscious consumers who now see beverages as conduits for targeted wellness benefits. In response, cold-pressed juice manufacturers are moving beyond general nutrition, infusing their products with adaptogens, probiotics, and botanical extracts tailored to specific health concerns. This trend isn't limited to ingredient enhancements; it also encompasses flavor profiles that resonate with wellness. Botanical flavors, such as lavender and rosemary, are gaining popularity as consumers link these tastes to therapeutic benefits. By positioning themselves as functional, brands not only differentiate from conventional juice offerings but also command premium pricing, carving out sustainable competitive advantages in a crowded marketplace.

Growing health consciousness

Consumers are increasingly focusing on preventive healthcare, paying closer attention to ingredient lists, and choosing products that align with their wellness goals. The USDA's updated definition of "healthy," set to take effect in February 2025, introduces new guidelines for nutrient content claims [1]Source: Federal Register, "Food Labeling: Nutrient Content Claims; Definition of Term “Healthy”", federalregister.gov . These changes are expected to significantly impact how cold-pressed juices are marketed and formulated. In 2024, 70% of consumers expressed trust in the USDA organic seal, according to the Organic Produce Network, reflecting a strong preference for transparent and regulated health claims over generic marketing messages. Younger consumers, who frequently use social media to research and verify health claims, are driving this trend. This shift creates opportunities for brands that can support their wellness claims with credible scientific evidence. As these younger, health-conscious consumers move into higher income brackets, their preferences are likely to continue fueling market growth.

Premiumisation of on-the-go breakfast among consumers

As busy lifestyles and health consciousness grow, consumers are increasingly seeking breakfast options that are both convenient and nutritious. Cold-pressed juices are emerging as a popular choice for meal replacements. For example, Generous Brands has launched its Super Smoothie platform, offering 12 grams of protein and 21 vitamins while containing 50% less sugar compared to traditional smoothies. This shift toward premium products goes beyond just nutrition, with brands focusing on innovative packaging designs. Features like ergonomic bottles and single-serving portion sizes cater to consumers who need portable and easy-to-consume options. By positioning themselves as breakfast alternatives, cold-pressed juice brands are directly competing with traditional breakfast categories while justifying higher price points through their nutritional value and convenience. Evolution Fresh illustrates this approach by pricing its 11-oz bottles at USD 3.99, showing that consumers are willing to pay more for products with clear health and functional benefits.

Growing demand for clean label and organic juices

The USDA's Strengthening Organic Enforcement (SOE) rule is driving greater transparency in the organic supply chain, which is essential for maintaining consumer trust in organic products. This rule requires an additional 4,000 to 5,000 companies in the organic supply chain to obtain certification, effectively reducing fraudulent organic claims. However, this increased regulation may lead to higher operational costs for legitimate producers. At the same time, it provides a competitive edge to established organic producers who have already invested in compliant and transparent supply chains. Additionally, the clean label trend is evolving beyond just organic certification. Consumers are increasingly demanding transparency in how products are processed. They prefer items that minimize the use of artificial preservatives and processing aids while still ensuring product safety and shelf life. This shift reflects a growing consumer focus on both product integrity and health-conscious choices.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Short shelf-life and availability of ambient juices Short shelf-life and availability of ambient juices | -0.7% | Global, particularly challenging in emerging markets with limited cold-chain infrastructure | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.7% | Geographic Relevance:Global, particularly challenging in emerging markets with limited cold-chain infrastructure | Impact Timeline:Short term (≤ 2 years) |

High price point limiting affordability High price point limiting affordability | -0.5% | Global, with pronounced impact in price-sensitive emerging markets | Medium term (2-4 years) | |||

Consumer perception of "high sugar" in fruit-dominant blends Consumer perception of "high sugar" in fruit-dominant blends | -0.3% | North America and European Union, where sugar awareness is highest | Medium term (2-4 years) | |||

Regulatory and labeling challenges on cold-pressed juices Regulatory and labeling challenges on cold-pressed juices | -0.2% | Global, with varying intensity based on local regulatory frameworks | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Short shelf-life and availability of ambient juices

The cold-pressed juice industry depends heavily on refrigerated distribution, but this reliance creates challenges in regions with inadequate cold-chain infrastructure. High-pressure processing (HPP) technology provides a solution by extending the shelf life of juices from 3-5 days to 30-45 days while preserving their nutritional value. However, the high cost of HPP equipment makes it difficult for smaller producers to adopt this technology. Studies show that using HPP at 450 MPa for 180 seconds effectively retains flavonoid content and ensures microbiological stability for up to 90 days, addressing the issue of limited shelf life. This limitation is particularly problematic for international markets and e-commerce, where longer transit times can affect product quality. Emerging technologies, such as cold plasma treatment, offer promising alternatives. These methods could help extend shelf life without requiring significant financial investment, making them more accessible to smaller producers.

High price point limiting affordability

Cold-pressed juice brands often price their 11-oz servings at USD 3.99, which limits their appeal to affluent consumers and creates barriers to wider market expansion. This price difference compared to conventional juices is due to higher production costs, driven by the use of premium ingredients, advanced processing equipment, and refrigerated distribution systems. However, such pricing strategies restrict volume growth and market penetration, especially in emerging economies where many consumers have lower disposable incomes and cannot afford premium beverages. The affordability issue is further exacerbated by the lack of economies of scale in cold-pressed juice production. The reliance on small-batch processing and an artisanal approach makes it difficult to reduce costs. To address these challenges, brands are introducing value-size packaging and subscription models to lower per-unit costs. Despite these efforts, the fundamental production costs continue to hinder accessibility for the mass market.

Segment Analysis

By Category: Blends Drive Innovation Despite Fruit Dominance

In 2024, fruit juice holds a leading 55.33% market share, driven by its strong consumer recognition and well-established distribution networks that favor single-fruit products. Traditional fruit juices benefit from clear FDA regulations, which outline specific standards for products like orange and grapefruit juices [2]Source: Code of Federal Regulations, "§ 146.135 Orange juice.", ecfr.gov . These regulations provide manufacturers with straightforward guidelines for compliance, ensuring product consistency and quality. On the other hand, vegetable juices maintain a smaller yet steady market share, supported by health-conscious consumers who prefer their lower sugar content and the added nutritional benefits of vegetable-based nutrients.

The blends category is the fastest-growing segment, with a notable 9.77% CAGR projected through 2030. This growth is fueled by increasing consumer interest in more complex flavor combinations and the enhanced nutritional value that blends offer compared to single-ingredient juices. Manufacturers are leveraging this demand by combining complementary ingredients to improve taste, boost nutritional content, and manage costs effectively. Recent innovations in this segment include the incorporation of functional ingredients such as adaptogens and botanicals, which appeal to health-focused consumers seeking specific wellness benefits. Additionally, the category benefits from flexible regulatory guidelines that allow creative ingredient combinations while ensuring compliance with FDA juice labeling standards.

Note: Segment shares of all individual segments available upon report purchase

By Nature: Organic Acceleration Challenges Conventional Leadership

The organic segment is projected to grow at an impressive CAGR of 11.67% through 2030, making it the fastest-growing category among all segments. This growth is primarily driven by consumers increasingly willing to pay a premium for clean-label products and transparent supply chains. The USDA's Strengthening Organic Enforcement rule is a significant factor in ensuring supply chain integrity, which has strengthened consumer trust in organic claims. The USDA organic seal, in particular, has become a widely recognized and trusted indicator of authenticity for many consumers.

In 2024, conventional products dominate the market with a substantial 72.13% share. This dominance is supported by well-established supply chains, lower production costs, and affordability, making these products accessible to price-sensitive consumers. However, the reliance on conventional products also reflects the current limitations of organic production, which cannot yet scale to meet the entire market demand. Despite this stability, conventional producers face growing pressure as consumers increasingly prioritize ingredient transparency and wellness-focused products. To maintain their market position, conventional producers must adapt by investing in clean-label formulations that align with shifting consumer preferences.

By Packaging Type: Sustainability Innovations Challenge PET Dominance

In 2024, PET bottles hold a 47.64% market share, driven by their affordability, durability during transportation, and strong consumer preference for this familiar packaging format. Their dominance is further supported by well-established supply chains and manufacturing systems that ensure efficient production and distribution processes. On the other hand, glass bottles cater to environmentally conscious consumers and brands aiming to stand out with sustainable packaging. However, their heavier weight and higher risk of breakage pose challenges to distribution efficiency, limiting their broader adoption.

The recyclable-pouch/tetra-pak category, which is projected to grow at a 10.80% CAGR through 2030, includes a range of innovative packaging solutions. These solutions feature recyclable pouches, plant-based materials, and advanced recycled content technologies. For instance, ALPLA's rePETec containers, made with up to 100% recycled PET, highlight how innovation in packaging can address sustainability concerns while maintaining functionality. Additionally, aseptic packaging formats like Tetra-Pak offer extended shelf life, which can help overcome refrigeration challenges in the cold-pressed juice industry. The growth of alternative packaging reflects increasing consumer demand for eco-friendly options and regulatory efforts to promote a circular economy.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Digital Transformation Accelerates Online Growth

In 2024, off-trade channels hold a significant 64.47% market share, highlighting the critical role of supermarkets, hypermarkets, and convenience stores in reaching a broad consumer base. These channels not only cater to mainstream consumers but also provide the necessary refrigerated infrastructure for distributing cold-pressed juices effectively. The strong performance of off-trade channels is driven by established partnerships between juice manufacturers and retail buyers, promotional campaigns that encourage both first-time and repeat purchases, and the ability to capitalize on impulse buying behavior. Supermarkets and hypermarkets ensure efficient distribution through their large-scale operations and cold-chain systems, while convenience stores offer easy access for consumers seeking quick, on-the-go options.

On-trade distribution through cafés, juice bars, restaurants, and wellness centres represents the fastest-growing segment in the cold-pressed juice market, with a projected CAGR of 12.67% through 2030. The growth is driven by consumer demand for fresh, on-demand juice products and the higher profit margins these venues generate. The on-trade channel enables cold-pressed juice manufacturers to benefit from direct consumption, increased market presence, and product demonstrations of fresh variants such as watermelon lemonade and vegetable blends at the point of sale. In the UK market, Daily Dose has implemented its distribution strategy through café chains including Gail's and Benugo, validating the effectiveness of product sampling and consumer interaction.

Geography Analysis

In 2024, North America holds the largest market share at 33.67%, driven by strong consumer acceptance of premium cold-pressed juice products and a well-established cold-chain infrastructure that ensures smooth distribution. The region's dominance is supported by regulatory frameworks like the FDA's HACCP requirements, which focus on maintaining product safety while encouraging innovation [3]Source: Code of Federal Regulations, "Part 120—Hazard Analysis And Critical Control Point (HACCP) Systems", ecfr.gov . The market's maturity is further highlighted by strategic moves such as Bolthouse Farms' acquisition of Evolution Fresh, aimed at improving operational efficiency and consolidating market presence.

Asia-Pacific is the fastest-growing market, with a projected CAGR of 11.93% through 2030. This rapid growth is fueled by urbanization, increasing disposable incomes, and a growing focus on health among the expanding middle class. Leading beverage companies, such as Asahi, are diversifying their product offerings to include health-focused beverages and alcohol alternatives, catering to the rising demand for functional drinks. Social media platforms like TikTok are influencing younger consumers to choose organic and functional beverages, creating significant opportunities for cold-pressed juice brands that effectively utilize digital marketing. Additionally, the region's growth is supported by improvements in retail infrastructure and cold-chain systems, enabling the distribution of premium products.

Europe continues to experience steady growth, driven by consumers' preference for sustainable and clean-label products. Regulatory support for organic and environmentally friendly practices further strengthens the market. Consumers in the region increasingly favor eco-friendly packaging and production methods, offering opportunities for brands that prioritize sustainability throughout their supply chains. In contrast, South America, and Middle East and Africa are emerging markets with notable growth potential. However, challenges such as limited cold-chain infrastructure and price sensitivity among consumers currently restrict their growth. Over time, economic development and urbanization in these regions are expected to create favorable conditions for the adoption of premium beverages.

Competitive Landscape

Market Concentration

The global cold-pressed juice market features intense competition, with both local and international players vying for dominance. Key players include PepsiCo Inc. (Naked Juice), Suja Life LLC, Pressed Juicery Inc., The Hain Celestial Group, Inc. (BluePrint), and Evolution Fresh. These companies carve out their niche by emphasizing unique flavor profiles, premium organic ingredients, and distinct functional benefits. By carefully selecting and blending ingredients like exotic fruits, nutrient-rich vegetables, and specialty herbs, they craft a diverse array of flavors that resonate with changing consumer tastes.

Brands intensify competition by incorporating functional ingredients, innovating with sustainable packaging, and developing direct-to-consumer channels. Adoption of technology, especially high-pressure processing (HPP) for extending shelf life, has shifted from being a differentiator to a competitive necessity. Companies are now heavily investing in processing capabilities to navigate distribution challenges while ensuring product integrity.

Opportunities abound in making products more affordable through value-size offerings, creating shelf-stable alternatives that retain nutritional benefits, and designing products that act as meal replacements instead of mere beverage supplements. The competitive landscape indicates that achieving success demands a delicate balance between premium positioning and operational efficiency. Furthermore, companies must stay attuned to evolving regulatory mandates, such as the USDA's Strengthening Organic Enforcement rule, which impacts supply chain transparency and certification processes.

Cold Pressed Juice Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Raw Generation introduced Little Sippers, a product line of cold-pressed juice blends formulated by nutritionists for children. The company developed seven flavors derived from 40 raw fruits and vegetables without added sugars or artificial ingredients. The 4-oz beverages delivered hydration, antioxidants, and electrolytes, providing children access to whole, unprocessed nutrition in a structured format to address childhood nutritional requirements.

- May 2025: Soluna launched its Apple Juice product, made from ANABP 01 apples (marketed as Bravo apples in Australia). The cold-pressed juice contained no additives and maintained its natural sweetness. The company utilized cold-pressing and High-Pressure Processing (HPP) methods to preserve nutrients and extend the product's shelf life to 90 days while maintaining freshness and food safety standards.

- May 2025: OMJOOS launched cold-pressed sugarcane juice, delivering a natural and healthy beverage for summer consumption. The company implemented a cold-pressing process that retained the juice's nutrients and flavor without adding preservatives or other ingredients. The product delivered hydration while containing antioxidants and minerals.

- March 2025: Wonder Juice introduced its organic cold-pressed juice line at Natural Products Expo West 2025. The company developed blends using organic fruits and vegetables, focusing on nutritional benefits and ingredient transparency.

Table of Contents for Cold Pressed Juice Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising demand for functional-health beverages

- 4.2.2Growing health consciousness

- 4.2.3Premiumisation of on-the-go breakfast among consumers

- 4.2.4Growing demand for clean label and organic juices

- 4.2.5Surge in D2C subscription models

- 4.2.6Rising disposable incomes enabling premium purchases

- 4.3Market Restraints

- 4.3.1Short shelf-life and availability of ambient juices

- 4.3.2High price point limiting affordability

- 4.3.3Consumer perception of “high sugar” in fruit-dominant blends

- 4.3.4Regulatory and labeling challenges on cold-pressed juices

- 4.4Value/Supply-Chain Analysis

- 4.5Regulatory and Technological Outlook

- 4.6Porter's Five Forces Analysis

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Suppliers

- 4.6.3Bargaining Power of Buyers/Consumers

- 4.6.4Threat of Substitute Products

- 4.6.5Intensity of Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Category

- 5.1.1Fruit Juice

- 5.1.2Vegetable Juice

- 5.1.3Blends

- 5.2By Nature

- 5.2.1Organic

- 5.2.2Conventional

- 5.3By Packaging Type

- 5.3.1PET Bottles

- 5.3.2Glass Bottles

- 5.3.3Recyclable-Pouch/Tetra-Pak

- 5.3.4Others (Cans/rPET/Plant-based Packaging)

- 5.4By Distribution Channel

- 5.4.1On-Trade

- 5.4.2Off-Trade

- 5.4.2.1Supermarkets/Hypermarkets

- 5.4.2.2Convenience/Grocery Stores

- 5.4.2.3Online Stores

- 5.4.2.4Other Off-Trade Channels

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.1.4Rest of North America

- 5.5.2South America

- 5.5.2.1Brazil

- 5.5.2.2Argentina

- 5.5.2.3Colombia

- 5.5.2.4Chile

- 5.5.2.5Peru

- 5.5.2.6Rest of South America

- 5.5.3Europe

- 5.5.3.1Germany

- 5.5.3.2United Kingdom

- 5.5.3.3Italy

- 5.5.3.4France

- 5.5.3.5Netherlands

- 5.5.3.6Poland

- 5.5.3.7Belgium

- 5.5.3.8Sweden

- 5.5.3.9Spain

- 5.5.3.10Rest of Europe

- 5.5.4Asia-Pacific

- 5.5.4.1China

- 5.5.4.2India

- 5.5.4.3Japan

- 5.5.4.4Australia

- 5.5.4.5Indonesia

- 5.5.4.6South Korea

- 5.5.4.7Thailand

- 5.5.4.8Singapore

- 5.5.4.9Rest of Asia-Pacific

- 5.5.5Middle East and Africa

- 5.5.5.1South Africa

- 5.5.5.2Saudi Arabia

- 5.5.5.3United Arab Emirates

- 5.5.5.4Nigeria

- 5.5.5.5Egypt

- 5.5.5.6Morocco

- 5.5.5.7Turkey

- 5.5.5.8Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1PepsiCo Inc. (Naked Juice)

- 6.4.2Suja Life LLC

- 6.4.3Pressed Juicery Inc.

- 6.4.4The Hain Celestial Group, Inc. (BluePrint)

- 6.4.5Evolution Fresh

- 6.4.6Juice Press LLC

- 6.4.7Cold-Pressed Juicery B.V.

- 6.4.8Raw Pressery Private Limited

- 6.4.9Greenhouse Juice Co.

- 6.4.10Village Juicery Inc.

- 6.4.11Little West

- 6.4.12Pure Green LLC

- 6.4.13Vive Organic

- 6.4.14Urban Remedy

- 6.4.15Juice Generation

- 6.4.16Rus Organic

- 6.4.17Fresh Press

- 6.4.18Kedia Organic

- 6.4.19Nutripress

- 6.4.20Lumi Juice

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Global Cold Pressed Juice Market Report Scope

Cold-pressed juices utilize cold-pressing technology for extraction. This method produces minimal heat, reducing the likelihood of microbial fermentation. As a result, cold-pressed juices can be stored and distributed with little to no preservatives.

The market is segmented by category, distribution channel, and geography. The cold-pressed juice market is segmented by type into fruit juice, vegetable Juice, and blends. The market is segmented by distribution channels into on-trade and off-trade. Off-trade is further segmented into online retail stores, hypermarkets/supermarkets, convenience/grocery stores, and other off-trade channel types. The market is segmented by geography into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa.

For each segment, the market sizing and forecasts have been done based on value (USD).