Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

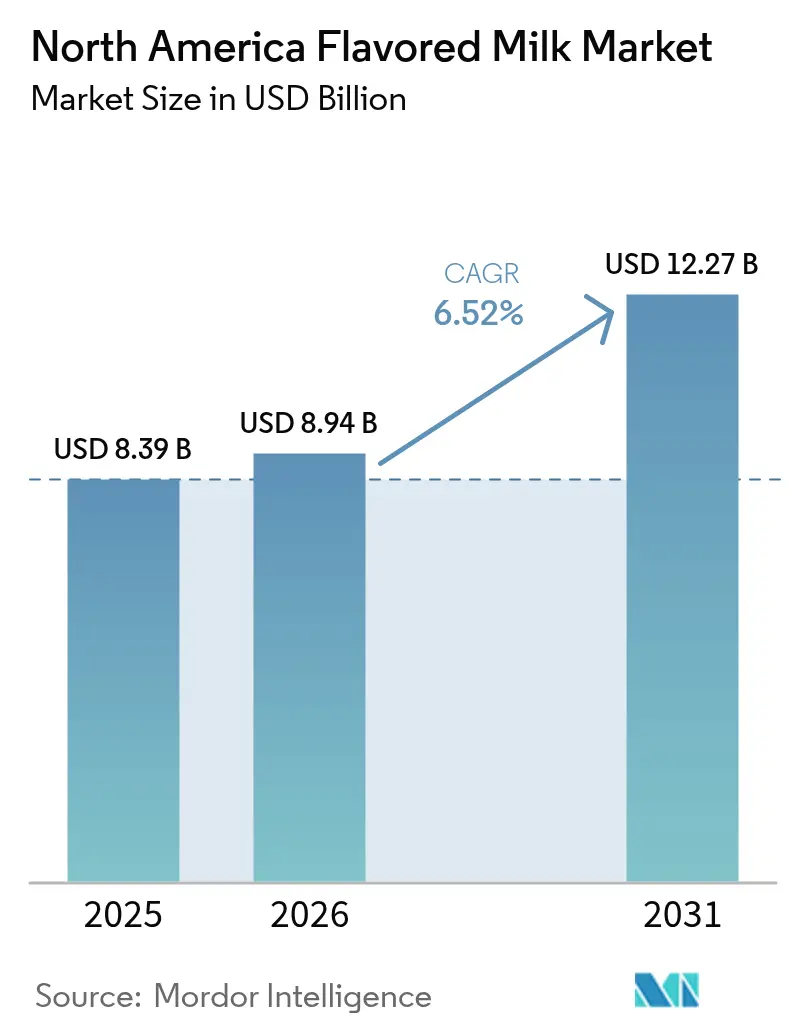

| Base Year Market Size (2025) | USD 8.39 Billion |

| Market Size (2026) | USD 8.94 Billion |

| Market Size (2031) | USD 12.27 Billion |

| Growth Rate (2026 - 2031) | 6.52% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Flavored Milk Market Analysis by Mordor Intelligence

North America flavored milk market size in 2026 is estimated at USD 8.94 billion, growing from 2025 value of USD 8.39 billion with 2031 projections showing USD 12.27 billion, growing at 6.52% CAGR over 2026-2031. This market size projection signals a clear growth runway that reflects resilient demand, widening product repertoires, and an active regulatory backdrop that favors innovation. Rising incomes in Mexico, continued private-label expansion in the United States, and sustained product reformulation to meet school nutrition rules keep volume momentum strong[1]U.S. Department of Agriculture, Food and Nutrition Service, “Biden-Harris Administration Announces New School Meal Standards to Strengthen Child Nutrition,” fns.usda.gov. Demand is further underpinned by supply-side advances in aseptic processing that lower logistics costs, investment in aluminum-free barriers that cut carton emissions by 61%, and a steady pipeline of fortified SKUs positioned as convenient protein sources for adults. Competitive intensity remains moderate as leading processors navigate carton shortages, acquire shelf-life assets, and diversify packaging, yet new entrants still find room in niche protein-enriched and plant-based lines. These factors collectively establish a positive near-term outlook for the North America flavored milk market even as pressure rises from sugar-reduction mandates and the fast-growing appeal of dairy alternatives.

Key Report Takeaways

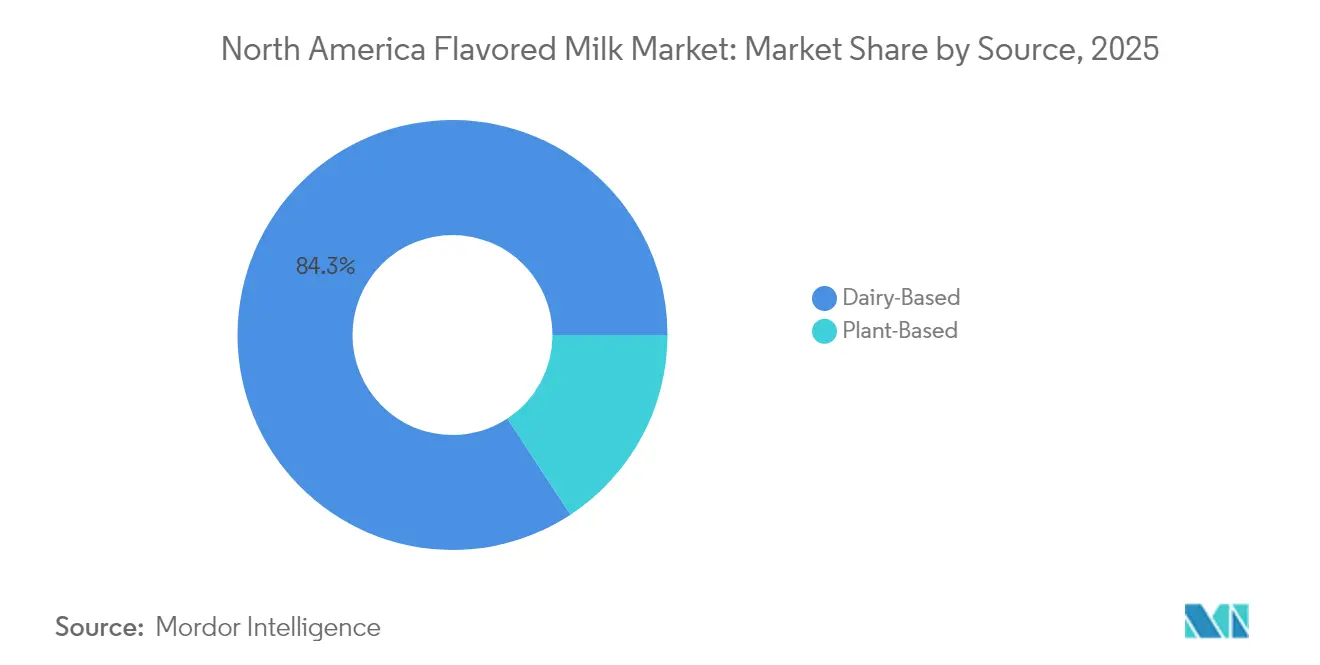

- By source, dairy-based products led with an 84.25% share of the North America flavored milk market in 2025; plant-based alternatives are projected to expand at 10.21% CAGR through 2031.

- By distribution channel, the off-trade segment commanded 71.05% of the North America flavored milk market size in 2025, while also recording the highest growth at 12.05% CAGR to 2031.

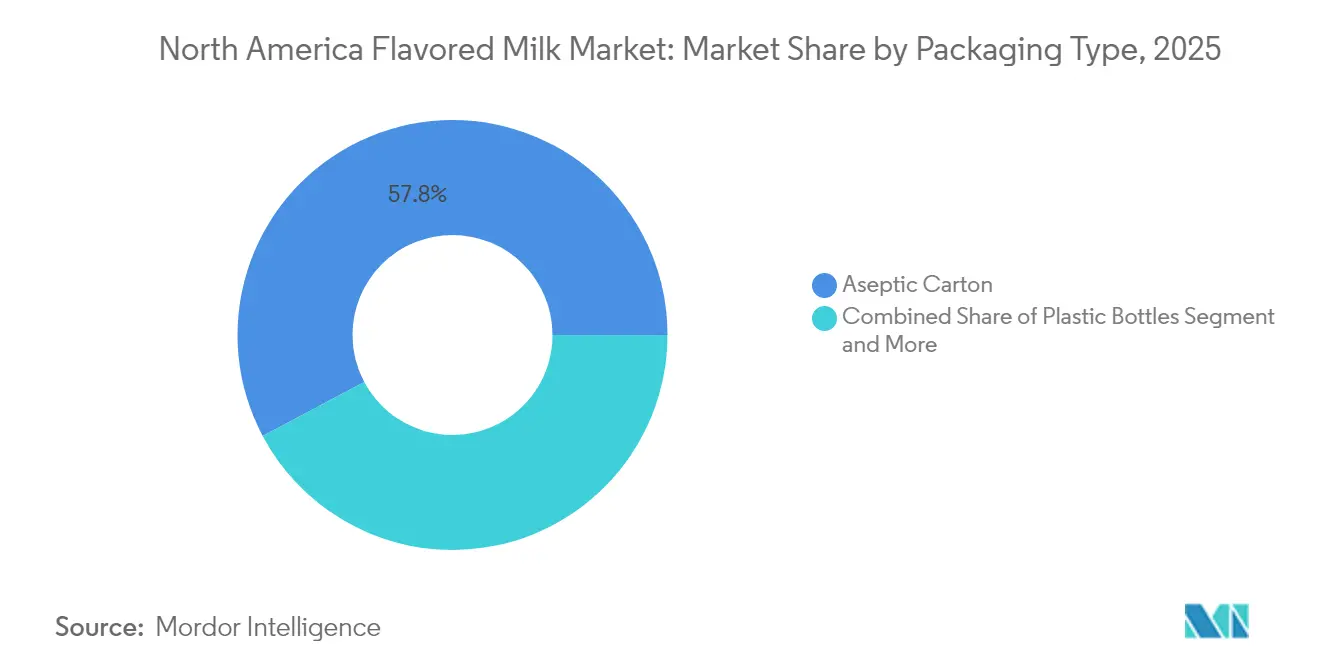

- By packaging type, aseptic cartons captured 57.78% revenue share in 2025; plastic bottles are advancing at an 8.52% CAGR through 2031.

- By geography, the United States accounted for 76.20% of North America flavored milk market share in 2025, whereas Mexico is forecast to grow the fastest at 6.58% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Flavored Milk Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenient, nutrient-dense RTD dairy beverages | +1.2% | North America-wide, strongest in urban centers | Medium term (2-4 years) |

| Product innovation in child-targeted flavors and formats | +0.8% | US and Canada school districts | Short term (≤ 2 years) |

| Fortified / protein-enriched SKUs for health-conscious adults | +0.9% | US metropolitan areas, expanding to Mexico | Medium term (2-4 years) |

| USDA post-2024 school meal rules boosting flavored low-fat milk | +1.5% | United States K-12 institutions | Short term (≤ 2 years) |

| Digital personalized-nutrition tie-ins for athletic recovery | +0.4% | North America fitness markets | Long term (≥ 4 years) |

| Advances in aseptic processing & shelf-life extension technologies lowering cold-chain dependence | +1.1% | Regional distribution networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Convenient, Nutrient-Dense RTD Dairy Beverages

Consumer migration toward ready-to-drink formats accelerates as lifestyle demands prioritize convenience without compromising nutritional density. The shift reflects broader demographic trends where 42% of US consumers purchased private-label products in 2024 to manage inflation pressures, creating opportunities for premium RTD flavored milk positioned as accessible nutrition[2]IDFA. "The Dairy Bar: Powered by Ever.Ag." IDFA (blog), February 5, 2025. https://www.idfa.org/news/the-dairy-bar-powered-by-ever-ag-45. Aseptic processing technologies enable ambient storage and extended distribution reach, reducing cold-chain dependencies that historically limited market penetration in rural and emerging regions. FDA regulations under 21 CFR 113 require validated thermal processes and continuous monitoring for commercially sterile RTD products, establishing quality benchmarks that differentiate premium offerings from commodity alternatives. The regulatory framework supports innovation in packaging formats, with SIG's aluminum-free barrier materials achieving 12-month shelf life while reducing carbon footprints by 61% compared to traditional aseptic cartons[3]Nikolova, Milana. "SIG unveils "first" aluminum-free full-barrier material for aseptic cartons." Packaging Insights, May 20–21, 2025. https://www.packaginginsights.com/news/sig-alu-free-aseptic-carton-innovation.html. This technological advancement addresses sustainability concerns while maintaining product integrity across temperature-variable distribution networks.

Product Innovation in Child-Targeted Flavors and Formats

The April 2024 USDA final rule caps added sugars at 10 g per 8-oz serving in schools, triggering widespread reformulation and flavor engineering to balance taste and compliance. Processors now integrate natural fruit concentrates and low-glycemic sweetener systems to maintain sensory appeal. FDA standards of identity under 21 CFR 131.110 allow characterizing flavor ingredients, granting flexibility for school-compliant innovations. Package-level engagement, such as interactive graphics on half-pints, bolsters lunchtime excitement while portion-control formats mitigate waste during ongoing carton supply shortages. These developments keep flavored milk entrenched as a preferred beverage in educational settings across the North America flavored milk market.

Fortified / Protein-Enriched SKUs for Health-Conscious Adults

Adult consumers adopt flavored milk as an accessible recovery beverage that naturally delivers casein, whey, and electrolytes often sought in sports drinks. FDA fortification policy sets vitamin A and D minima yet allows extra micronutrients, encouraging processors to add zinc, magnesium, or omega-3s for additional value. Retailers capitalize by dedicating chilled space to high-protein flavored milk lines that command premiums over conventional variants. Private labels leverage co-packing to test functional concepts, evidenced by refrigerated private-label foods rising 7.5% y-o-y in 2024. Consistent quality controls imposed by the Pasteurized Milk Ordinance allow processors to upscale without compromising safety, underscoring the North America flavored milk market’s reputation for trustworthy functional beverages.

USDA Post-2024 School Meal Rules Boosting Flavored Low-Fat Milk

School meal programs serve 30 million U.S. children daily and account for 427 million gallons of fluid milk sales, making compliance with added-sugar caps mission-critical. The Healthy School Milk Commitment covers processors responsible for over 90% of volume, guaranteeing supply pipelines for reformulated SKUs. Uniform specifications around fat-free and low-fat milk streamline procurement, lower switching costs, and cement flavored milk as a staple in meal reimbursements. Early-moving firms that developed compliant recipes enjoy first-mover shelf space advantages, reinforcing brand loyalty among younger demographics in the North America flavored milk market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened scrutiny of added sugars in beverages | -0.9% | US regulatory focus, expanding to Canada | Short term (≤ 2 years) |

| Shift toward plant-based lactose-free alternatives | -1.3% | Urban North America, strongest in US West Coast | Medium term (2-4 years) |

| Local school-district bans on flavored milk varieties | -0.6% | US school districts, particularly California and Northeast | Short term (≤ 2 years) |

| Supply tightness and price spikes in aseptic carton laminates | -0.8% | North America packaging supply chain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heightened Scrutiny of Added Sugars in Beverages

USDA restrictions represent the first nationwide sugar limits in school meals, capping flavored milk sugars at 10 g per serving from July 2025. Child and Adult Care Food Program guidance discourages high-sugar beverages, expanding institutional pressure beyond K-12. Public-health campaigns amplify messaging, nudging parents toward reduced-sugar choices. Reformulating without compromising taste elevates R&D costs, and natural sweeteners such as monk fruit or stevia alter flavor profiles that risk consumer attrition. Plant-based competitors highlight naturally lower sugars in their marketing, intensifying substitution threats within the North America flavored milk market.

Shift Toward Plant-Based Lactose-Free Alternatives

FDA draft guidance published in March 2025 permits terms like “soy milk” while encouraging voluntary nutrition comparisons, lowering labeling barriers for dairy alternatives. Plant-based household penetration climbed to 33% by 2016 and retail sales reached USD 2.4 billion by 2020, demonstrating rising mainstream acceptance. Institutional settings must still meet nutrient equivalency, yet these drinks escape dairy-specific sugar caps, giving them formulation latitude. Improvements in protein fortification close historic nutritional gaps, making alternatives more competitive on school menus if prices converge. These dynamics subtract incremental volume from the North America flavored milk market over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Dairy Leads While Plant-Based Rises

Dairy-based flavored milk held 84.25% North America flavored milk market share in 2025, anchored by established supply chains and nutritional superiority that satisfies federal meal guidelines. Consistent regulatory definitions under 21 CFR 131.110 shield dairy positioning, while the Pasteurized Milk Ordinance ensures quality integrity across state lines. The North America flavored milk market size for dairy-based offerings is forecast to climb to USD 9.94 billion by 2031 at a 5.86% CAGR, driven by shelf-life technologies that open low-frequency shopping regions and by fortified lines that command premium pricing. Large cooperatives such as Dairy Farmers of America capitalize on member milk pools to scale aseptic capacity efficiently, while brands like Nesquik exploit broad retail penetration to sustain volume leadership.

Plant-based alternatives accelerate at 10.21% CAGR through 2031, reaching USD 2.37 billion and eroding a portion of dairy share. FDA’s March 2025 guidance grants labeling certainty, and voluntary comparison statements incentivize manufacturers to bridge protein gaps through soy or pea fortification. Market entrants position oat-based drinks as allergen-friendly options with lower sugar, courting health-conscious millennials. Retailers dedicate end-caps to dairy-free flavored SKUs, supporting trial. The North America flavored milk industry adjusts by co-packing plant-based lines to hedge against share drift, while dairy lobbyists pursue legislative avenues to restrict the milk nomenclature, an outcome still uncertain.

By Distribution Channel: Off-Trade Dominance Continues

Off-trade outlets commanded 71.05% of the North America flavored milk market in 2025, aided by double-digit online grocery growth and the convenience of grab-and-go multi-packs. Private-label momentum is strong: refrigerated store brands advanced in 2024 as consumers traded down amid inflation. Retailers negotiate long-term supply partnerships that favor processors able to guarantee carton availability and school-compliant formulations. Promotions around family-size value packs stimulate pantry loading, supporting average price realizations.

On-trade growth lags amid lingering packaging volatility; still, institutional volumes remain steady given mandated school meal demand. Carton shortages in 2024 forced distributors to source generic labels and temporary plastic alternatives. Foodservice chains adopt portion-controlled plastic bottles with high-barrier films to extend shelf life, balancing cost pressures with waste-reduction targets. As supply normalizes, operators expect flavored milk rotation to regain historical cadence, yet tighter sugar rules may slightly temper volume gains in certain age cohorts.

By Packaging Type: Carton Stability Meets Bottle Innovation

Aseptic cartons retained 57.78% share of the North America flavored milk market in 2025 thanks to line speed, cost efficiency, and widespread equipment base. New aluminum-free full-barrier substrates lower carbon footprints and answer recycling critiques while preserving 12-month ambient shelf life. The North America flavored milk market size for aseptic cartons is anticipated to surpass USD 6.98 billion by 2031 as school programs and shelf-stable club packs keep demand solid. Industry groups encourage multi-supplier sourcing after the Pactiv Evergreen closure exposed single-point failure risk.

Plastic bottles grow at 8.52% CAGR, buoyed by resealability, portability, and premiumizing opportunities. Lightweight PET coupled with oxygen-scavenging layers reduces material use yet safeguards flavor stability. Processors deploy shrink-sleeve graphics to convey protein or sugar-reduction claims, capturing impulse buys at c-stores. Retail merchandisers favor upright visibility, and bottle multipacks facilitate ecommerce shipping, further expanding reach within the North America flavored milk market.

Geography Analysis

In 2025, the U.S. dominated North America's flavored milk market, holding a commanding 76.20% share. This dominance is bolstered by a robust refrigeration infrastructure, stringent adherence to FDA regulations, and the substantial demand from the National School Lunch Program. Innovations in private labels and a crossover with sports nutrition are driving heightened demand in grocery stores. Meanwhile, processors are channeling investments into UHT lines, eyeing export prospects in Latin America. When carton supply disruptions arose, the IDFA showcased its logistical agility by coordinating alternate sourcing, ensuring school deliveries remained uninterrupted. This adaptability not only resolved immediate challenges but also fortified the market's resilience. Mexico, though starting from a smaller base, is on track in the market. Factors like rising disposable incomes and modernized retail landscapes are making flavored milk more accessible in urban supermarkets. Thanks to the USMCA, cross-border supply synergies are not just streamlining operations but also fast-tracking technology transfers. Local plants are now installing aseptic fillers, a technology once exclusive to their northern counterparts. Multinational companies are ramping up marketing efforts around protein-fortified drinks, tapping into the burgeoning fitness culture and aiming to capture a larger slice of the North American flavored milk market.

Canada's flavored milk scene is characterized by mature yet consistent consumption patterns. Here, bilingual labeling and nutrient criteria are closely aligned with U.S. standards, albeit with some local tweaks. The country's supply-managed dairy system not only ensures top-notch raw milk quality but also offers pricing transparency, bolstering producer margins. With a growing emphasis on sustainability, there's a push for carton recycling and a keen interest in low-carbon packaging. In a forward-thinking move, processors are trialing aluminum-free barriers, anticipating a trend that may soon gain traction in the U.S. While certain provinces see a surge in plant-based products, innovations in flavors and lactose-free dairy options continue to win over loyal consumers.

Competitive Landscape

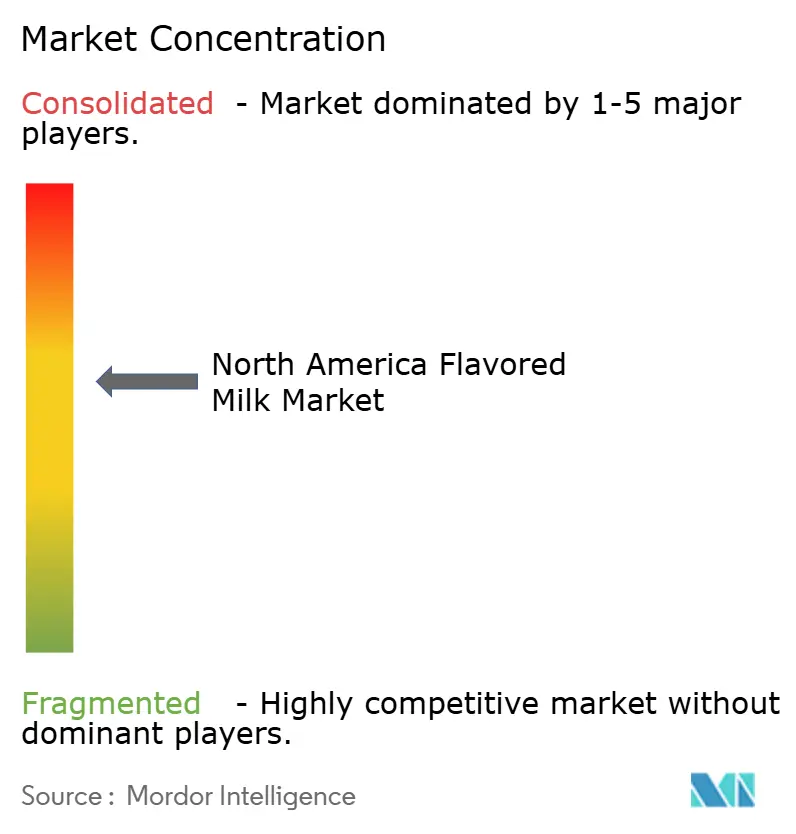

The North America flavored milk market shows a moderate concentration score of 6/10 as the top tier of processors commands a sizable yet not dominant slice of revenue. Nestlé leverages Nesquik’s brand equity and broad retail presence, upgrading recipes to sub-10 g sugar to retain shelf prominence in K-12 supply lists. Dairy Farmers of America capitalizes on cooperative milk supply and recently expanded aseptic filling at acquired facilities to meet private-label demand. Saputo diversifies with plant-based flavored beverages under recently purchased alt-dairy brands, hedging against dairy-volume risk in urban markets. Danone’s Horizon Organic line uses bottle lightweighting to appeal to environmentally conscious parents, while Kraft Heinz exploits cross-category synergy between cheese snacking and Kool-Aid flavored milk co-branding.

Consolidation continues as Maola Local Dairies acquired HP Hood’s Philadelphia UHT plant in March 2024, shoring up shelf-life capacity and retaining 160 union positions. Patent filings around aluminum-free aseptic materials, sugar-reduction enzymes, and extended-shelf-life filtration reflect sustained R&D outlays aimed at margin expansion. Start-ups emphasize direct-to-consumer fulfillment of fortified, lactose-free flavored milks in recyclable PET, targeting millennials seeking transparent sourcing. The interplay between scale advantages of incumbents and brand nimbleness of newcomers keeps price competition contained while encouraging premium innovation across the North America flavored milk market.

North America Flavored Milk Industry Leaders

-

Nestle S.A

-

Danone

-

Dairy Farmers of America

-

Saputo Inc.

-

The Kraft Heinz Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Dairy Farmers of America's (DFA) TruMoo brand has released TruMoo Zero, a high-protein chocolate milk that features 13 grams of protein per serving—50% more than regular chocolate milk—while containing no added sugar.

- April 2025: Maïzly has launched its innovative corn-based plant milk in the U.S. market, offering both original and chocolate flavors. This dairy-free, gluten-free milk alternative is made with non-GMO corn, chickpea protein, and coconut oil, fortified with vitamins D2, A, E, calcium, and contains only a quarter of the sugar found in dairy milk.

- February 2025: Jubilee’s Flavored Milk is launching a unique, shelf-stable flavored milk product designed especially for kids, featuring hidden vegetables, zero added sugar, and 7-8 grams of protein per serving. Created by Austin mom Ashley Waldman, the drink comes in nostalgic flavors like chocolate chip cookie, banana cream pie, and strawberry shortcake, offering a nutritious alternative that combines taste and health benefits.

North America Flavored Milk Market Report Scope

Flavored milk is a sweetened dairy drink made with milk, sugar, flavorings, and sometimes food colorings. The North America Flavored Milk Market is segmented into Dairy-based and Plant-based. Based on Distribution Channel, the market is segmented into supermarkets/ Hypermarkets, Convenience Stores, Specialist Stores, Online Retail Stores, and Other Distribution Channels. Based on Geography United States, Mexico, Canada, Rest of North America. The report offers market size and forecasts for the market in value (USD million) for all the above segments.

By Source

| Dairy-Based |

| Plant-Based |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets / Hypermarkets |

| Convenience Stores | |

| Specialist Stores | |

| Online Retail | |

| Other Channels |

By Packaging Type

| Aseptic Cartons |

| Plastic Bottles |

| Glass Bottles |

| Others |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Source | Dairy-Based | |

| Plant-Based | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets / Hypermarkets | |

| Convenience Stores | ||

| Specialist Stores | ||

| Online Retail | ||

| Other Channels | ||

| By Packaging Type | Aseptic Cartons | |

| Plastic Bottles | ||

| Glass Bottles | ||

| Others | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Key Questions Answered in the Report

How large is the North America flavored milk market in 2026?

It stands at USD 8.94 billion and is projected to grow at 6.52% CAGR to USD 12.27 billion by 2031 (2026-2031).

Which source segment is growing fastest?

Plant-based flavored milk is expanding at 10.21% CAGR, outpacing dairy-based lines yet still representing a smaller share.

Why are off-trade channels leading sales?

Consumers favor at-home consumption and private-label value, giving off-trade outlets a 71.05% share and the highest growth at 12.05% CAGR.

How will new USDA sugar limits affect flavored milk?

Processors must reformulate to cap added sugars at 10 g per 8-oz serving by July 2025, accelerating investment in low-sugar flavor systems.

What packaging innovation is most influential?

Aluminum-free full-barrier aseptic cartons cut carbon footprints by 61% while preserving 12-month shelf life, aligning with sustainability mandates.

Page last updated on: