Non-invasive Brain Stimulation System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

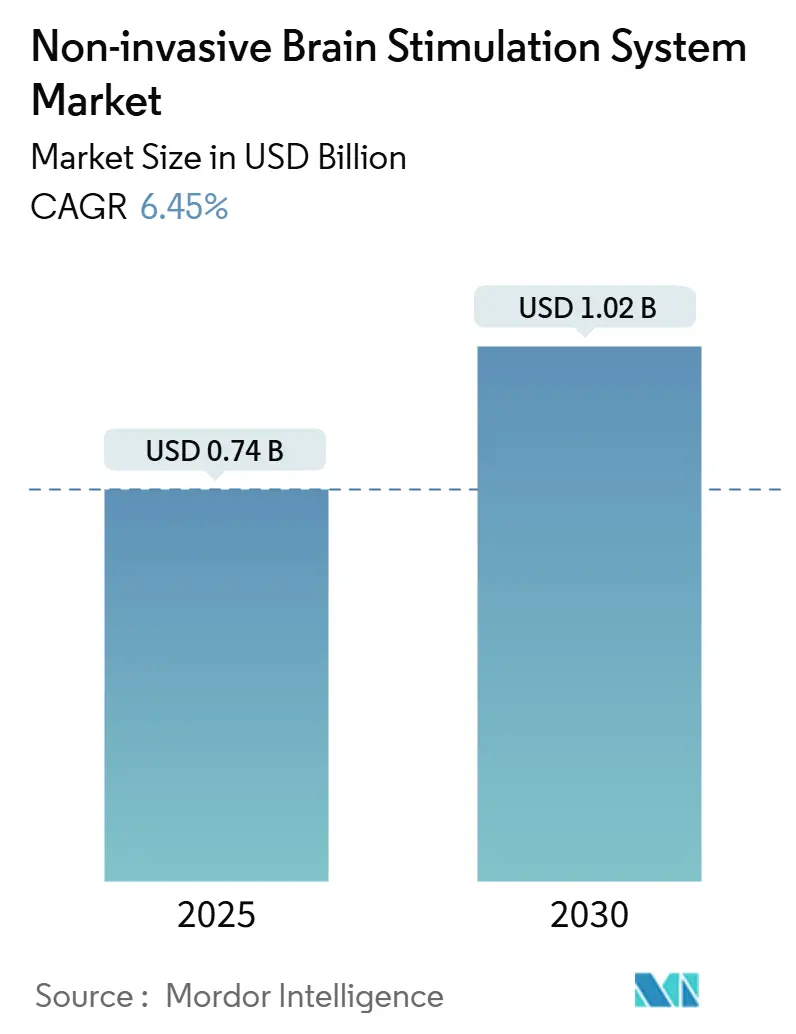

| Market Size (2025) | USD 0.74 Billion |

| Market Size (2030) | USD 1.02 Billion |

| Growth Rate (2025 - 2030) | 6.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non-invasive Brain Stimulation System Market Analysis by Mordor Intelligence

The non-invasive brain stimulation system market size is USD 0.74 billion in 2025 and, at a 6.45% CAGR, is forecast to reach USD 1.02 billion by 2030. Regulatory green lights for treatment-resistant depression, algorithm-guided dosing, and real-time imaging feedback underpin demand momentum. Home-use wearables priced below USD 500 shift volumes from hospitals to living rooms, while closed-loop magnetic and electrical stimulators command premium prices in specialty clinics. Regional growth also hinges on streamlined approvals in the Asia Pacific and sustained Medicare reimbursement in the United States. Supply-chain stress around rare-earth magnets inflates coil costs but simultaneously pushes innovators toward electrical systems that depend on standard semiconductors. Venture capital injections of USD 183 million during 2024 illustrate faith in subscription-based software ecosystems layered on top of hardware.

Key Report Takeaways

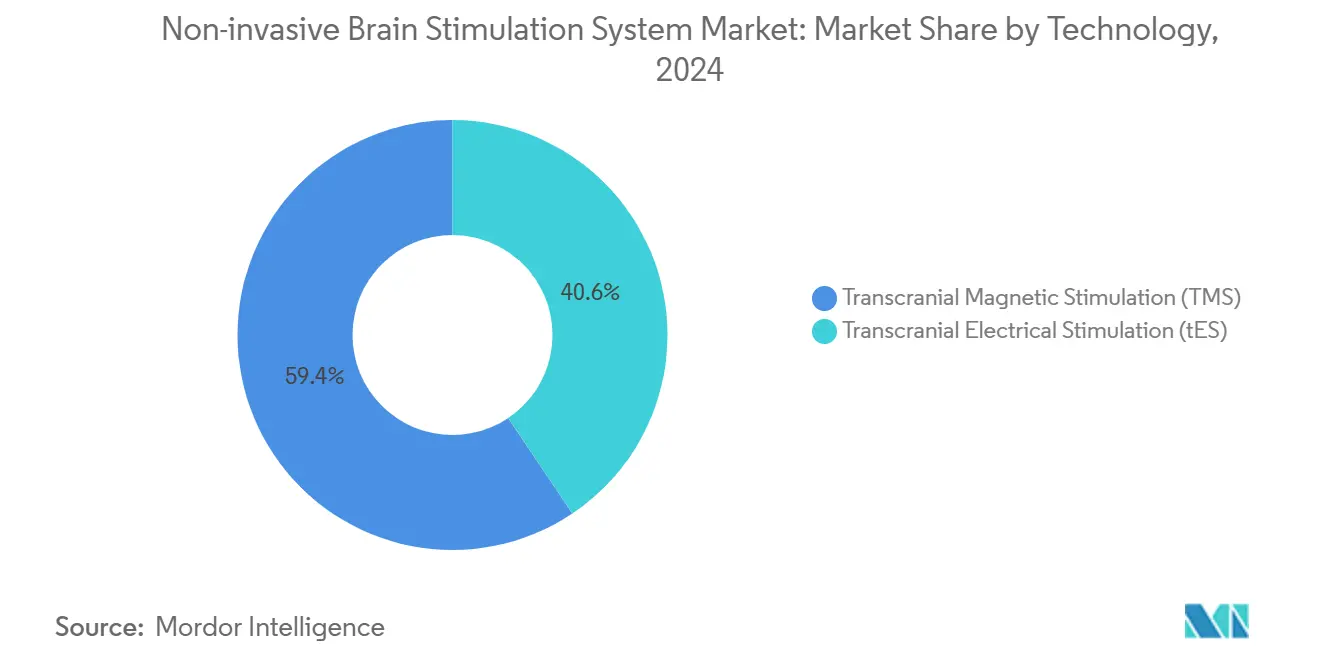

- By technology, TMS held 59.4% of the non-invasive brain stimulation system market share in 2024; tES is on course for a 14.0% CAGR through 2030.

- By application, major depressive disorder controlled 43.7% of the non-invasive brain stimulation system market size in 2024, while cognitive enhancement & ADHD are expanding at a 17.3% CAGR between 2025 and 2030.

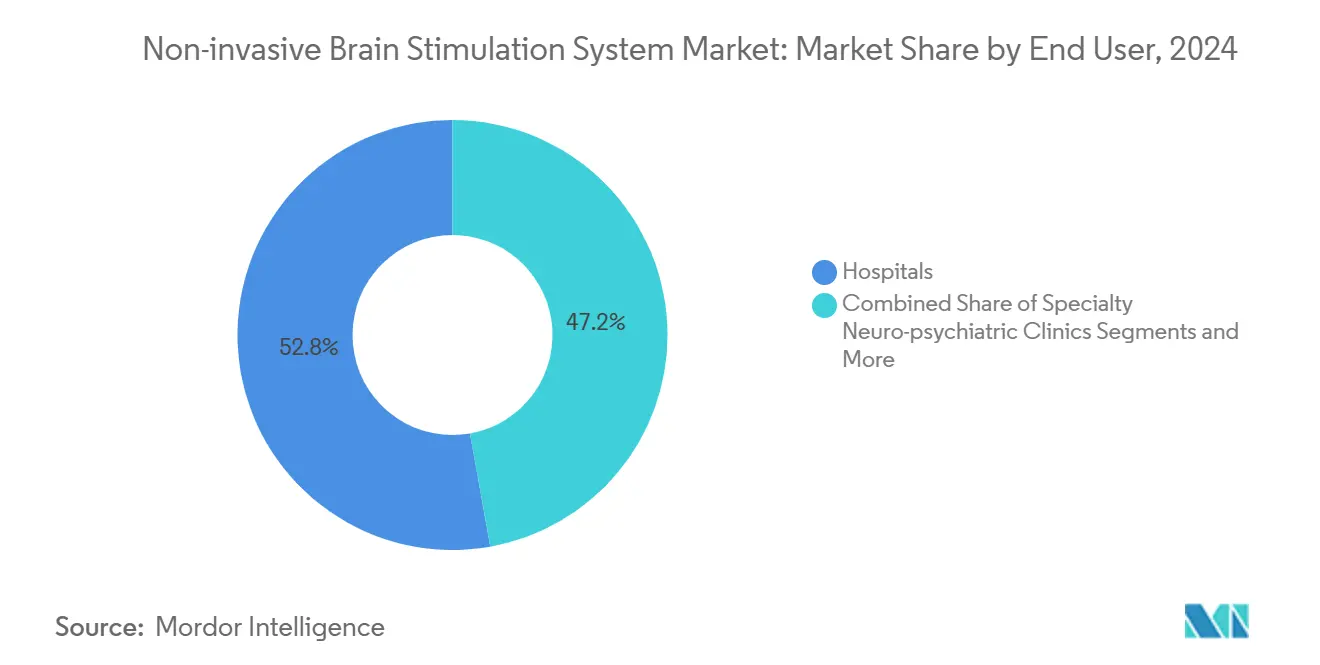

- By end user, hospitals contributed 52.8% of the non-invasive brain stimulation system market size in 2024; home-care settings will rise at a 16.4% CAGR in the same horizon.

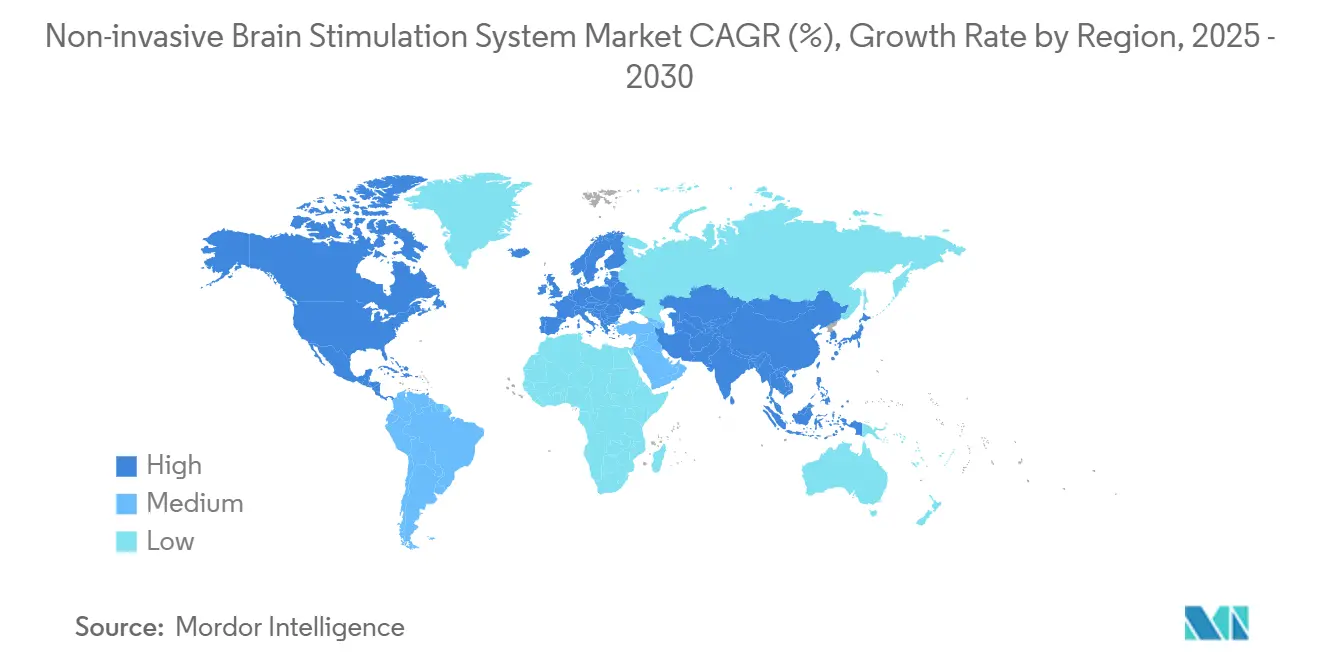

- By geography, North America led with 39.3% non-invasive brain stimulation system market share in 2024; Asia Pacific is growing fastest at 11.4% CAGR to 2030.

Global Non-invasive Brain Stimulation System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Algorithm-guided personalized stimulation protocols | +1.80% | North America & Europe ahead, global later | Medium term (2-4 years) |

| Rapid clinical adoption for treatment-resistant depression | +1.50% | North America & Europe, Asia Pacific catching up | Short term (≤ 2 years) |

| Expansion of home-use tDCS wearables | +1.20% | North America, Europe, APAC spill-over | Medium term (2-4 years) |

| Integration with real-time neuro-imaging | +0.90% | North America & Europe | Long term (≥ 4 years) |

| Corporate mental-wellness programs | +0.70% | North America & Europe, APAC urban hubs | Medium term (2-4 years) |

| Venture funding surge in neuromod-as-a-service | +0.40% | Concentrated in North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Algorithm-Guided Personalized Stimulation Protocols

FDA clearances in 2024 for AI-tuned theta-burst dosing validated a pivot from one-size-fits-all to individualized regimens, delivering 60% symptom relief versus 40% under fixed protocols.[1]Klietz David, “Theta Burst Stimulation for Major Depression,” Journal of Affective Disorders, pubmed.ncbi.nlm.nih.gov Multimodal language models now parse EEG feeds in real time and nudge pulse patterns mid-session, curbing variability that long hampered efficacy. Higher success rates justify premium pricing and broaden payer acceptance, reinforcing hospital ROI. Machine-learning classifiers trained on large imaging datasets flag probable responders before therapy begins, shaving trial-and-error costs. As data lakes deepen, insurers may green-light preventive indications such as early cognitive decline, extending the non-invasive brain stimulation system market well beyond psychiatry.

Rapid Clinical Adoption for Treatment-Resistant Depression

Roughly 30% of depressed patients fail two medications, propelling hospitals toward TMS protocols that condense courses from six weeks to two while retaining efficacy parity.[2]Holgado Arturo, “AI-Optimized Neuromodulation Protocols,” Frontiers in Neuroscience, frontiersin.org Medicare’s reimbursement of 30 sessions per episode removes major cost hurdles and encourages capital investment in rural centers. Dual-site magnetic stimulation addresses refractory cases unresponsive to single-target therapy, and maintenance regimens—now experimental—look poised for coverage once multi-year evidence matures. Clinics tout non-pharmaceutical safety and faster functional recovery, achievements that anchor the non-invasive brain stimulation system market in mainstream psychiatry.

Expansion of Home-Use tDCS Wearables

Class II clearance for cranial electrotherapy devices treating anxiety and insomnia legitimized consumer-grade neuromodulation. European agencies go further, approving home-use kits for depression under tele-monitoring. Units priced USD 100-500 democratize therapy and feed anonymized compliance data to clinicians, who remotely adjust settings. Millennial and Gen Z users prefer app-enabled interventions over in-clinic visits, translating lifestyle appeal into future volume for the non-invasive brain stimulation system market.

Integration with Real-Time Neuro-Imaging for Closed-Loop Therapy

fMRI-guided rTMS pinpoints sub-millimeter targets to boost remission odds while EEG-linked coils adjust intensity every few stimuli, keeping cortical excitability inside therapeutic windows. Though capital-intensive, closed-loop suites command premium tags and generate robust longitudinal datasets vital for next-gen algorithm training. Portable EEG and functional near-infrared spectroscopy units lower infrastructure barriers, allowing secondary hospitals to enter the non-invasive brain stimulation system market with precision capabilities once reserved for tertiary centers.

Restraints Impact Analysis*

| Restraint | ~ % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of long-term safety data beyond five years | -1.10% | Strongest in Europe & APAC | Long term (≥ 4 years) |

| Reimbursement gaps for out-of-hospital indications | -0.80% | North America & Europe | Medium term (2-4 years) |

| Device misuse in bio-hacking communities | -0.60% | North America & Europe, APAC cities | Short term (≤ 2 years) |

| Rare-earth magnet supply bottlenecks | -0.90% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Long-Term Safety Data Beyond Five-Year Horizon

Most trials cap at 12-month endpoints, leaving regulators wary of cumulative exposure over decades. Post-market surveillance mandates add compliance costs that smaller entrants cannot shoulder easily, slowing portfolio expansion. Pediatric and preventive niches remain tentative until registries yield conclusive longitudinal evidence, tempering the non-invasive brain stimulation system market trajectory in those segments.

Reimbursement Gaps for Out-of-Hospital Indications

Medicare labels maintenance TMS experimental, forcing patients to absorb annual costs surpassing USD 10,000.[3]Brain2Mind Consortium, “Global Magnet Supply Chain Report,” brain2mind.org Commercial insurers differ widely by state and ICD-10 code, complicating provider economics. The lack of CPT codes for tES and closed-loop platforms delays claims processing. Demonstrating cost-utility against chronic drug therapy through multi-year health-economics studies is essential to normalizing payer policies and fortifying the non-invasive brain stimulation system market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: TMS Dominance Faces tES Disruption

Transcranial magnetic stimulation held 59.4% of revenue in 2024 thanks to robust evidence and wide reimbursement. Nevertheless, tES is forecast to log a 14.0% CAGR, driven by low-cost wearables that favor remote supervision. The non-invasive brain stimulation system market size for tES devices could eclipse USD 0.41 billion by 2030, assuming the current growth pace. A 500% spike in neodymium-iron-boron coil prices raised TMS unit costs, nudging clinics toward electrical systems that sidestep magnet imports.

Enhanced tES models offering multi-channel high-definition targeting now rival magnetic spatial resolution. Vendors integrate cloud-based protocol libraries and user-level compliance tracking, step-changing data granularity. Meanwhile, TMS manufacturers respond with neuronavigation upgrades and coil designs optimized for algorithm-guided dosing, defending their stake in the non-invasive brain stimulation system market.

By Application: Depression Leadership Challenged by Cognitive Enhancement

Major depressive disorder accounted for 43.7% of 2024 demand, stabilized by adolescent approvals and two-week theta-burst regimens. Yet cognitive enhancement & ADHD share is rising swiftly at 17.3% CAGR, fueled by corporate performance programs and emerging literature on attention gains in healthy adults. The non-invasive brain stimulation system market share for cognitive applications could top 20% by 2030 if current momentum persists.

Chronic pain, Parkinson’s, epilepsy, and stroke rehabilitation form a long tail of indications collectively contributing to double-digit growth. Payers remain cautious, but evidence accumulation and algorithmic precision promise coverage expansion, widening the non-invasive brain stimulation system market reach.

By End User: Hospital Dominance Shifts Toward Home Care

Hospitals generated 52.8% of 2024 billings as capital budgets covered magnetic chairs and nursing oversight. However, home-care settings are set to climb 16.4% annually with tele-supervised tES that frees patients from weekly commutes. The non-invasive brain stimulation system market size in domestic environments benefits from smartphone tracking, automated dose logs and AI-powered safety failsafes.

Specialty neuro-psychiatric clinics target complex cases requiring high-dose or closed-loop protocols, while academic labs push envelope indications using research-grade gear exceeding USD 10,000. Mobile TMS vans extend access to rural zones, underscoring how geography barriers erode in the evolving non-invasive brain stimulation system market.

Geography Analysis

North America’s 39.3% lead rests on transparent FDA pathways and consistent Medicare coverage. Dense provider networks integrate stimulation into everyday psychiatry, while private insurers trend toward parity reimbursement. Canada’s uptake grows after provincial funding mandates, and Mexico leverages medical tourism, widening regional throughput for the non-invasive brain stimulation system market.

Asia Pacific is the fastest-growing theater at 11.4% CAGR. China’s 4.9% rise interacts with hospital modernization and local magnet supply, reinforcing self-reliance. Japan and South Korea approve multiple platforms, and Australia funds pilot schemes through universal insurance. India’s private sector pioneers app-supervised wearables in urban centers. Regional semiconductor capacity aids cost-down manufacturing, enlarging the non-invasive brain stimulation system market.

Europe delivers measured expansion under well-resourced health systems. Germany dominates on compulsory insurer coverage; the United Kingdom’s NHS recognized TMS for refractory depression in 2024; France and Italy see private demand overtaking public volumes. EU harmonization streamlines certification but enforces stringent post-market surveillance, favoring evidence-rich vendors poised to scale in the non-invasive brain stimulation system market.

Competitive Landscape

Neuronetics’ 60% revenue share, fortified by the Greenbrook TMS acquisition, makes it the lone fully vertically integrated player—manufacturing hardware and operating clinics under one roof. BrainsWay pursues deep-field coils to activate broader cortical areas, while MagVenture banks on modular architecture and neuronavigation. Highland Instruments and Soterix Medical chase closed-loop tES with breakthrough designations, aiming for precision in remote settings.

Flow Neuroscience sells USD 399 app-controlled headsets by subscription, challenging the hardware-ownership model. Patent battles intensify around AI dosing engines and cloud compliance platforms. Chinese magnet export caps propel dual sourcing and alloy verticalization strategies among incumbents. The non-invasive brain stimulation system market now rewards hybrid business plans that merge devices with data to capture lifetime patient value.

Non-invasive Brain Stimulation System Industry Leaders

Medtronic plc

Boston Scientific Corporation

BrainsWay Ltd

Neuronetics Inc.

Magstim Group Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Neuronetics bought Greenbrook TMS for USD 83 million, lifting annual capacity above 10,000 patients.

- January 2025: FDA granted breakthrough status to Soterix Medical’s EEG-linked tDCS platform.

- June 2024: Ybrain secured Korean approval for ADHD-targeted tDCS.

Global Non-invasive Brain Stimulation System Market Report Scope

| Transcranial Magnetic Stimulation (TMS) |

| Transcranial Electrical Stimulation (tES) |

| Major Depressive Disorder |

| Chronic Pain Management |

| Parkinson's Disease |

| Epilepsy |

| Stroke Rehabilitation |

| Cognitive Enhancement & ADHD |

| Others (Anxiety, Insomnia, Alzheimer's) |

| Hospitals |

| Specialty Neuro-psychiatric Clinics |

| Out-patient Rehabilitation Centers |

| Home-care Settings |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Transcranial Magnetic Stimulation (TMS) | |

| Transcranial Electrical Stimulation (tES) | ||

| By Application | Major Depressive Disorder | |

| Chronic Pain Management | ||

| Parkinson's Disease | ||

| Epilepsy | ||

| Stroke Rehabilitation | ||

| Cognitive Enhancement & ADHD | ||

| Others (Anxiety, Insomnia, Alzheimer's) | ||

| By End User | Hospitals | |

| Specialty Neuro-psychiatric Clinics | ||

| Out-patient Rehabilitation Centers | ||

| Home-care Settings | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the non-invasive brain stimulation system market expected to grow by 2030?

It is projected to expand at a 6.45% CAGR, moving from USD 0.74 billion in 2025 to USD 1.02 billion in 2030.

Which region shows the highest growth potential for non-invasive brain stimulation systems?

Asia Pacific, driven by streamlined approvals and hospital investment, is forecast to climb at an 11.4% CAGR through 2030.

What technology leads current revenues?

Transcranial magnetic stimulation (TMS) holds 59.4% of 2024 revenue due to broad clinical validation and reimbursement.

Why are home-use devices gaining momentum?

Class II clearances for tDCS wearables and tele-supervision capabilities offer convenience and lower treatment costs, fueling 16.4% CAGR in home-care settings.

Which company is the market frontrunner?

Neuronetics, after acquiring Greenbrook TMS, controls about 60% of global revenue and operates the largest integrated treatment network.

Page last updated on: