Electrophysiology Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

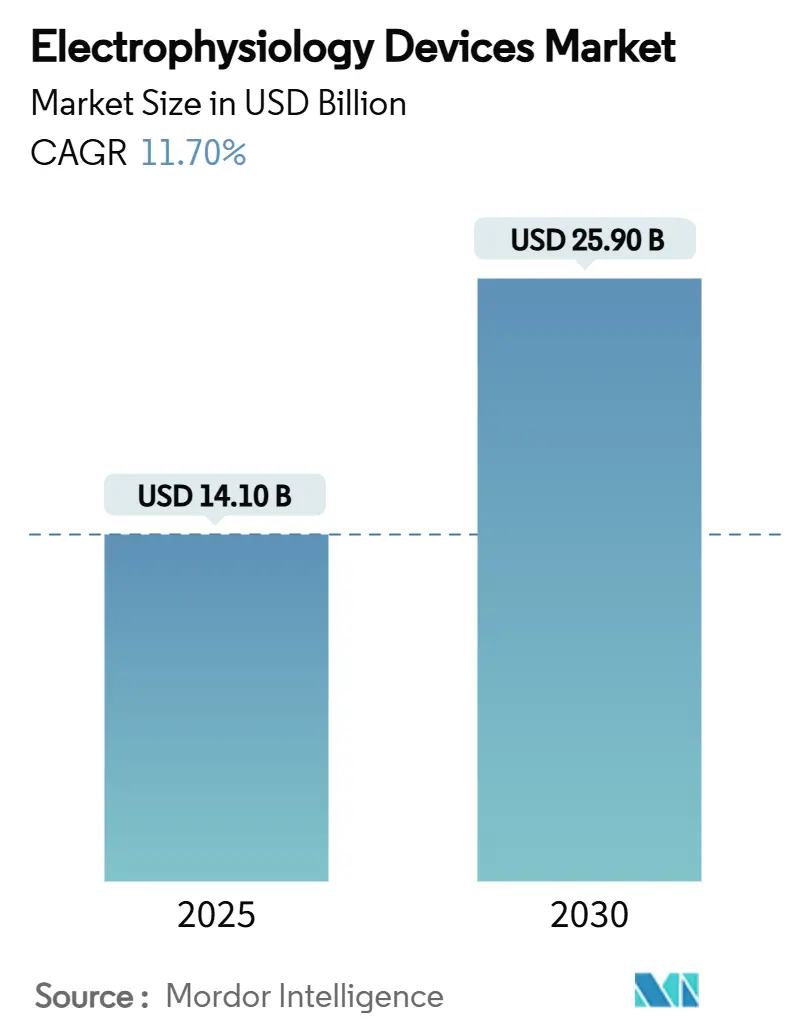

| Market Size (2025) | USD 14.10 Billion |

| Market Size (2030) | USD 25.90 Billion |

| Growth Rate (2025 - 2030) | 11.70% CAGR |

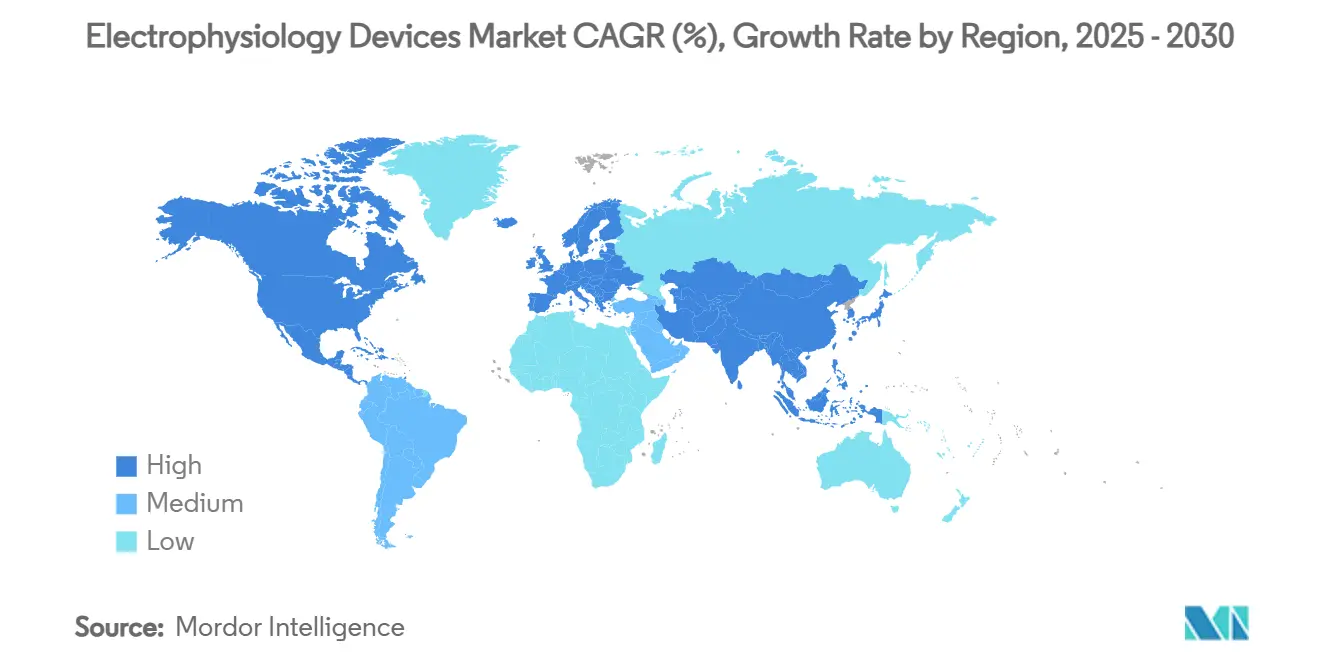

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electrophysiology Devices Market Analysis by Mordor Intelligence

The electrophysiology devices market size reached USD 14.1 billion in 2025 and is projected to climb to USD 25.9 billion by 2030, reflecting an 11.70% CAGR. Growth momentum is anchored in an aging population that experiences a doubling of atrial-fibrillation prevalence every decade after age 60, the steady migration toward minimally invasive catheter therapies, and a wave of technology that shortens procedure times and improves safety. Sustained investment in pulsed-field ablation (PFA) platforms, AI-enabled mapping software, and leadless implantable has unlocked new revenue pools while widening the addressable patient base for the Electrophysiology devices market. Market expansion is further supported by reimbursement reforms that open outpatient sites of service and by strong clinical data demonstrating 99.1% pulmonary-vein isolation success for PFA versus thermal approaches. Short-term headwinds remain, however, including fluoropolymer supply constraints and a limited pool of trained specialists that threaten to cap procedural volumes in high-growth regions.

Key Report Takeaways

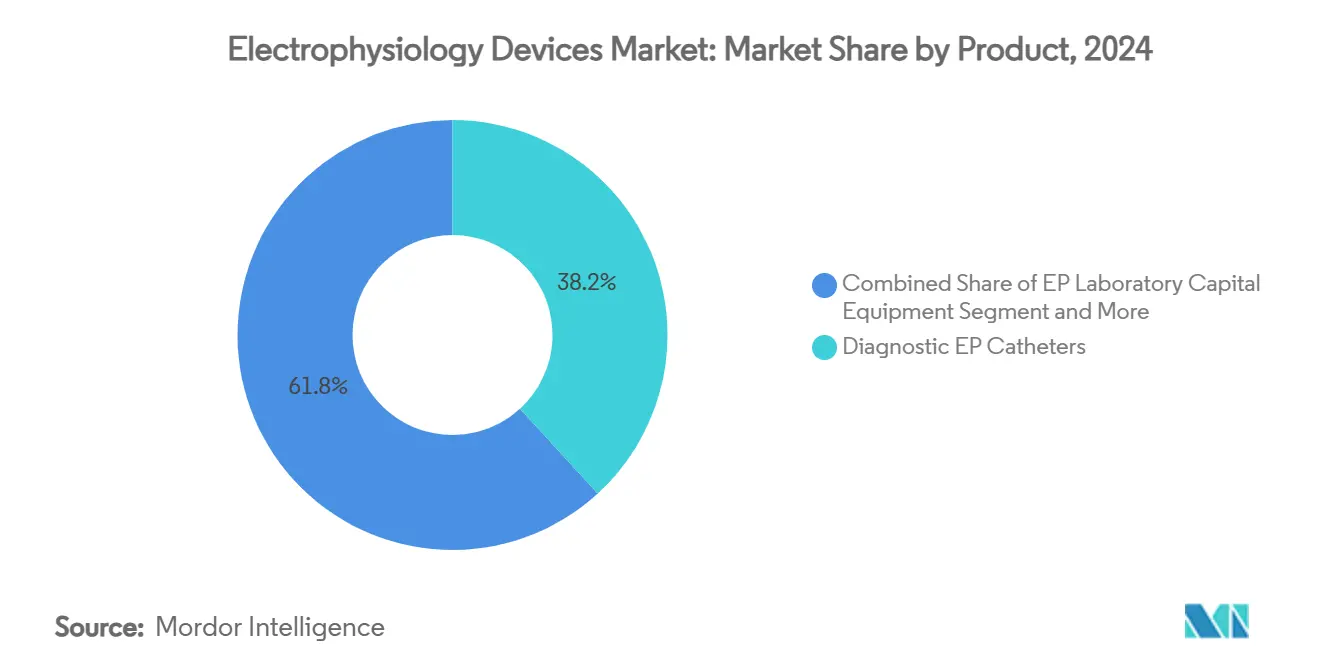

- By product category, diagnostic EP catheters led with 38.2% of the Electrophysiology devices market share in 2024, while pulsed-field ablation catheters are forecast to expand at a 17.5% CAGR through 2030.

- By application, atrial fibrillation procedures accounted for 40.7% of the Electrophysiology devices market size in 2024 and are expected to advance at a 13.2% CAGR to 2030.

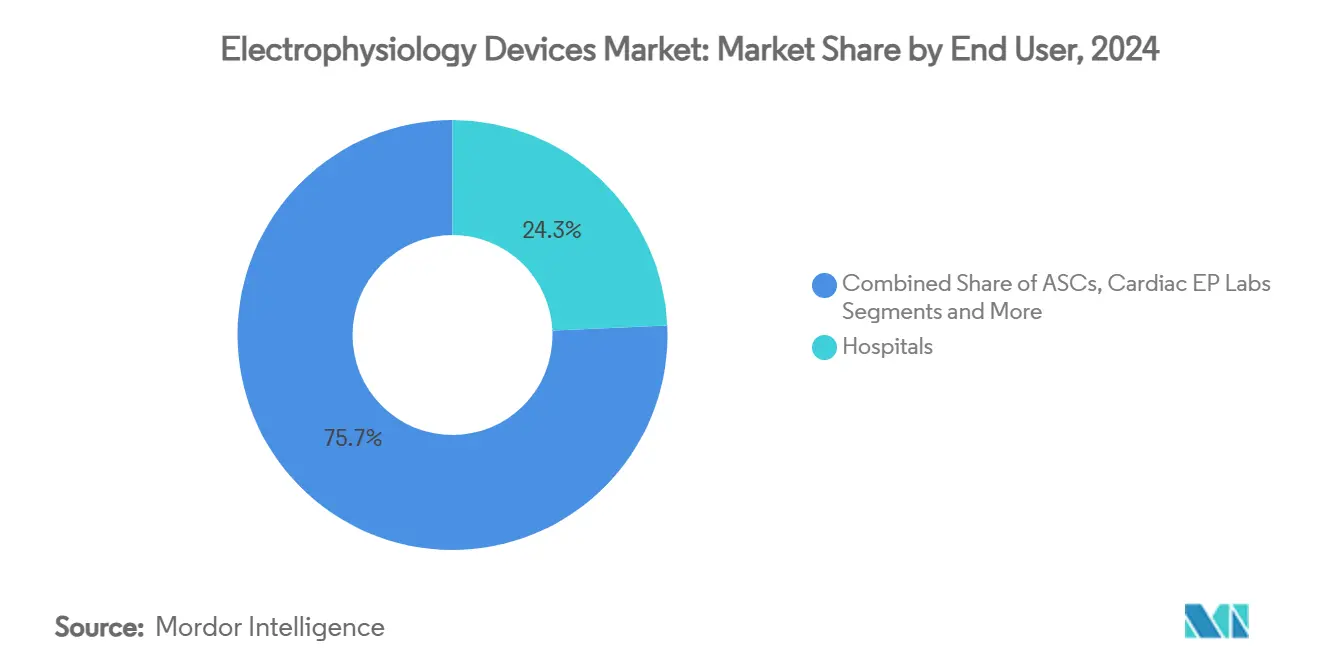

- By end user, hospitals held 24.3% revenue share of the Electrophysiology devices market in 2024, whereas ambulatory surgical centers posted the fastest growth at 12.8% CAGR through 2030.

- By geography, North America commanded 24.9% of the Electrophysiology devices market in 2024; Asia Pacific is poised for the strongest regional ascent at an 11.4% CAGR to 2030.

Global Electrophysiology Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global atrial-fibrillation prevalence | +3.20% | Global, highest in North America & Europe | Long term (≥ 4 years) |

| Rapid adoption of 3-D mapping & navigation systems | +2.80% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Shift toward minimally invasive catheter ablation | +2.10% | Global, led by developed markets | Medium term (2-4 years) |

| Emergence of AI-assisted EP workflows | +1.90% | North America & EU core, early APAC adoption | Long term (≥ 4 years) |

| Ageing population & cardiovascular-disease burden | +1.50% | Global, highest in developed economies | Long term (≥ 4 years) |

| Outpatient EP labs boosted by reimbursement reforms | +1.20% | North America primarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Atrial-Fibrillation Prevalence

Surging arrhythmia incidence remains the primary volume catalyst for the Electrophysiology devices market. Global cases rose to 37.6 million in 2017 and are projected to exceed 60 million by 2050. Prevalence already surpasses 10% among adults older than 80, generating a steady pipeline of patients who no longer respond to drug therapy alone. The population shift lifts demand for diagnostic catheters, mapping consoles, and implantable devices while inflating the economic burden of secondary stroke. Health systems therefore prioritize early ablation, a strategy that translates directly into higher device utilization rates within the Electrophysiology devices market. Long-range forecasts assign a +3.2% CAGR lift to this single demographic tailwind.

Rapid Adoption of 3-D Mapping & Navigation Systems

Electroanatomical mapping suites now gather more than 1 million data points per case, allowing precise lesion placement and shorter fluoroscopy times. Abbott’s EnSite X, Johnson & Johnson’s CARTO 3 V8, and Boston Scientific’s Rhythmia platform dominate this segment. Clinical studies show 23% reductions in procedure length and 18% throughput gains following a mapping-lab upgrade. Hospitals that embrace these systems improve patient turnover, revenue per room, and ablation outcomes, reinforcing recurrent capital spending across the Electrophysiology devices market. Momentum will intensify as AI modules automate voltage-map interpretation, further trimming staff workload.

Shift Toward Minimally Invasive Catheter Ablation

Catheter ablation secures sinus rhythm in 75% of atrial fibrillation patients versus surgery and demands fewer inpatient days.[1]Harvard Health Publishing Editors, “Catheter Ablation: A Minimally Invasive Option for Treating Atrial Fibrillation,” Harvard Health, health.harvard.edu PFA has altered risk–benefit calculus by using electroporation to spare adjacent tissue, cutting procedural complications while slashing energy-delivery time. Early U.S. experience at the Mayo Clinic recorded favorable safety in 53 patients treated since February 2024, and CMS projects USD 450 million in Medicare savings over 10 years as ablation migrates to outpatient sites.[2]Centers for Medicare & Medicaid Services, “Site-of-Service Differential Analysis,” cms.gov These economics accelerate adoption among ASC networks and underpin double-digit volume growth for the Electrophysiology devices market.

Emergence of AI-Assisted EP Workflows

Algorithms now pinpoint arrhythmia foci in under one minute, with Vektor Medical’s vMap achieving 98.7% regional accuracy across nine arrhythmia types. AI-guided ablation lifted 12-month freedom-from-AF rates to 88% in the TAILORED-AF trial compared with 70% for conventional pulmonary-vein isolation. Applications extend to ECG triage, sudden-death risk prediction, and predictive maintenance of lab assets. Network effects promise continuous model improvement, giving early adopters of AI technology an efficiency moat that reshapes competitive dynamics inside the Electrophysiology devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Procedure & Device Costs | -2.40% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| Limited Pool Of Trained Electrophysiologists | -1.80% | Global, acute in rural and underserved areas | Long term (≥ 4 years) |

| Fluoropolymer Supply-Chain Bottlenecks For Advanced Catheters | -1.30% | Global, concentrated in high-tech catheter segments | Short term (≤ 2 years) |

| Cyber-Security & Interoperability Hurdles In Connected EP Devices | -0.90% | North America & EU primarily, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Procedure & Device Costs

Successive Medicare cuts have lowered U.S. reimbursement for atrial-fibrillation ablation by 35.7% over two years, eroding provider margins. Capital outlays for next-generation PFA generators and mapping suites can exceed USD 1 million per lab, a hurdle for smaller centers. Price pressure is amplified in lower-income countries where insurance penetration is low and public budgets are thin. If costs remain unchecked, emerging-market penetration for the Electrophysiology devices market could decelerate despite strong demographic demand.

Limited Pool of Trained Electrophysiologists

Only 2,571 board-certified electrophysiologists practice in the United States, and retirements threaten a 29% drop in pediatric coverage by 2032.[3]Heart BMJ Editorial Team, “Global burden of cardiac electrophysiology,” heart.bmj.com Europe shows uneven training access, with structured fellowships available in 49% of ESC member nations. Skill scarcity lengthens patient waitlists and discourages hospitals from investing in new EP suites, capping procedure capacity in fast-growing corners of the Electrophysiology devices market. AI guidance and remote mentoring may ease the bottleneck, yet the timeline for material relief spans the next decade.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: PFA Technology Disrupts Traditional Ablation

Diagnostic EP catheters maintained a 38.2% share of the electrophysiology devices market in 2024, underscoring their indispensable role in signal acquisition and pacing. Revenue, however, is migrating toward pulsed-field ablation catheters, forecast to grow 17.5% annually as clinicians embrace tissue-selective energy that avoids collateral damage. Boston Scientific’s FARAPULSE and Medtronic’s PulseSelect systems complete pulmonary-vein isolation in under 30 minutes, shrinking lab turnover times and driving repeat capital sales for generators and disposable sleeves.

Traditional RF and cryo-ablation platforms now compete on price as PFA raises efficacy benchmarks. Abbott’s Volt system reached 99.1% isolation success with fewer energy applications, prompting many centers to phase out thermal catheters. Mapping consoles, RF generators, and capital accessories, therefore, remain resilient, buoyed by upgrade cycles to PFA-compatible modules. Within this evolution, the Electrophysiology devices industry sees rising demand for integrated diagnostic-therapeutic toolkits that link catheter data, hemodynamic metrics, and imaging streams into one dashboard, advancing lab ergonomics and clinical outcomes.

By Application: Atrial Fibrillation Dominance Drives Innovation

Atrial-fibrillation procedures represented 40.7% of the Electrophysiology devices market size in 2024 and are projected to expand at a 13.2% CAGR through 2030. Earlier-stage intervention policy has moved ablation into the first-line setting for many symptomatic patients, lifting volumes even in resource-constrained systems. AI-augmented mapping and ultra-low energy PFA lessen complication rates, inviting wider patient eligibility and swelling the addressable Electrophysiology devices market.

Other arrhythmias, such as atrial flutter, AVNRT, Wolff-Parkinson-White syndrome, and ventricular tachycardia, sustain specialty demand. Ventricular-tachycardia cases remain fewer yet command premium device pricing due to complex substrate mapping. AI-guided lesion sets improve success in those challenging scenarios; early data show 82% arrhythmia-free survival at one-year follow-up when AI directs target selection. As emerging algorithms mature, care teams expect cross-application learning curves that will further widen the Electrophysiology devices market.

By End User: ASC Growth Challenges Hospital Dominance

Hospitals retained 24.3% revenue leadership in 2024, yet ASC procedural share is scaling quickly as reimbursement reforms unlock outpatient service lines. CMS projects USD 450 million in Medicare savings over a decade by shifting cardiac ablation into freestanding centers, propelling a 12.8% CAGR for ASC purchases across the Electrophysiology devices market. PFA’s shorter anesthesia and recovery requirements suit the one-day discharge model and incentivize expansion into suburban catchment areas.

Dedicated EP labs inside tertiary hospitals, meanwhile, capitalize on complex arrhythmia referrals that sustain high-margin device sales, notably implantables and 3-D mapping consoles. Academic institutions spearhead clinical trials and fellowship training, nurturing long-term demand for leading-edge hardware. The Electrophysiology devices industry, therefore, balances efficiency-driven ASC uptake with research-intensive hospital settings that remain central to innovation diffusion.

Geography Analysis

North America captured 24.9% of the Electrophysiology devices market in 2024, supported by a dense network of EP labs, favorable FDA breakthrough pathways, and rapid AI adoption. Yet reimbursement cuts threaten near-term equipment refresh cycles, prompting providers to negotiate pricing concessions with vendors. Europe maintains a sizeable volume driven by aging demographics; streamlined CE-mark procedures enable faster device launches, though variability in structured training moderates the market’s growth potential.

Asia Pacific is the fastest rising region with an 11.4% CAGR through 2030. Expanding middle-class health spending, ambitious hospital-building programs, and local manufacturing capacity create a fertile backdrop for the penetration of electrophysiology devices in the market. China’s 2025 approval of FARAPULSE signals regulatory openness to foreign technologies, while India reports a steep rise in electrophysiology research output that will likely translate into stronger domestic demand. Sub-scale rural infrastructure and pricing sensitivity, however, necessitate frugal-innovation business models, leading many suppliers to adopt tiered product portfolios that match varied purchasing power across the region.

Latin America, the Middle East, and Africa remain smaller contributors but hold untapped potential as public-health planners prioritize non-communicable disease management. Vendor strategies that couple physician-training programs with affordable service contracts can unlock incremental Electrophysiology devices market volumes in these geographies over the long term.

Competitive Landscape

Competition revolves around four incumbents—Abbott, Johnson & Johnson’s Biosense Webster, Medtronic, and Boston Scientific—that collectively set the technology agenda for the Electrophysiology devices market. Boston Scientific has executed bolt-on acquisitions of Cortex and SoniVie to extend its atrial-fibrillation toolset. Medtronic leverages first-to-market PulseSelect FDA clearance to capture early PFA share, while Biosense Webster exploits the deep CARTO installed base to cross-sell catheters and analytics modules. Abbott positions Volt PFA alongside its EnSite mapping system, delivering an end-to-end workflow that deepens customer lock-in.

Disruptors target software gaps. Vektor Medical’s cloud-based vMap delivers AI arrhythmia localization without catheter contact, promising large-lab productivity gains. Supply-chain resilience has become a strategic differentiator following the 2024 fluoropolymer shortages that throttled high-performance catheter output. Vendors with diversified material sourcing redirected inventory faster, cushioning revenue impact and strengthening customer loyalty inside the Electrophysiology devices market. Patent races in PFA energy-delivery waveforms and AI mapping algorithms will likely dictate the next wave of competitive realignment.

Electrophysiology Devices Industry Leaders

Johnson & Johnson

Abbott Laboratories

Medtronic plc

Boston Scientific Corporation

Biotronik SE & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Abbott secured CE-mark approval for the Volt PFA System, accelerating its European launch cadence.

- June 2025: The FDA cleared Abbott’s Volt PFA System for U.S. commercialization following pivotal-trial success.

- April 2025: Abbott commenced the ASCEND CSP pivotal trial for its conduction-system-pacing ICD lead.

- March 2025: Boston Scientific acquired SoniVie, adding the Tivus ultrasound ablation platform to its portfolio.

Global Electrophysiology Devices Market Report Scope

| Diagnostic EP Catheters | Conventional |

| Advanced (steerable, irrigated) | |

| Ultrasound | |

| Ablation Catheters | Radio-frequency |

| Cryoablation | |

| Pulsed-field (PFA) | |

| EP Laboratory Capital Equipment | 3-D Mapping Systems |

| Recording Systems | |

| RF Generators & Cryo Consoles | |

| Implantable Electrophysiology Devices | Cardiac Pacemakers |

| Implantable Cardioverter-Defibrillators (ICDs) |

| Atrial Fibrillation |

| Atrial Flutter |

| Atrioventricular Nodal Re-entrant Tachycardia (AVNRT) |

| Wolff–Parkinson–White (WPW) Syndrome |

| Ventricular Tachycardia |

| Other Arrhythmias |

| Hospitals |

| Ambulatory Surgical Centers |

| Cardiac Electrophysiology Labs |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Diagnostic EP Catheters | Conventional |

| Advanced (steerable, irrigated) | ||

| Ultrasound | ||

| Ablation Catheters | Radio-frequency | |

| Cryoablation | ||

| Pulsed-field (PFA) | ||

| EP Laboratory Capital Equipment | 3-D Mapping Systems | |

| Recording Systems | ||

| RF Generators & Cryo Consoles | ||

| Implantable Electrophysiology Devices | Cardiac Pacemakers | |

| Implantable Cardioverter-Defibrillators (ICDs) | ||

| By Application | Atrial Fibrillation | |

| Atrial Flutter | ||

| Atrioventricular Nodal Re-entrant Tachycardia (AVNRT) | ||

| Wolff–Parkinson–White (WPW) Syndrome | ||

| Ventricular Tachycardia | ||

| Other Arrhythmias | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Cardiac Electrophysiology Labs | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the Electrophysiology devices market?

The Electrophysiology devices market size reached USD 14.1 billion in 2025.

How fast will the Electrophysiology devices market grow through 2030?

Market revenue is projected to expand at an 11.7% CAGR, reaching USD 25.9 billion by 2030.

Which product segment is growing the quickest?

Pulsed-field ablation catheters are forecast to rise at a 17.5% CAGR as physicians transition away from thermal energy systems.

Why is Asia Pacific considered the next growth frontier?

The region offers an 11.4% CAGR outlook due to hospital-build programs, larger cardiovascular disease burden, and accelerated regulatory approvals such as China’s nod for FARAPULSE.

What limits broader adoption in emerging markets?

High device costs and a shortage of trained electrophysiologists remain primary barriers despite strong underlying demand.

How is artificial intelligence influencing procedural efficiency?

AI mapping tools like vMap localize arrhythmia sources in under one minute and have boosted 12-month freedom-from-arrhythmia rates to 88% in recent clinical trials.

Page last updated on: