Electroencephalography Systems/Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.62 Billion |

| Market Size (2031) | USD 2.59 Billion |

| Growth Rate (2026 - 2031) | 9.86% CAGR |

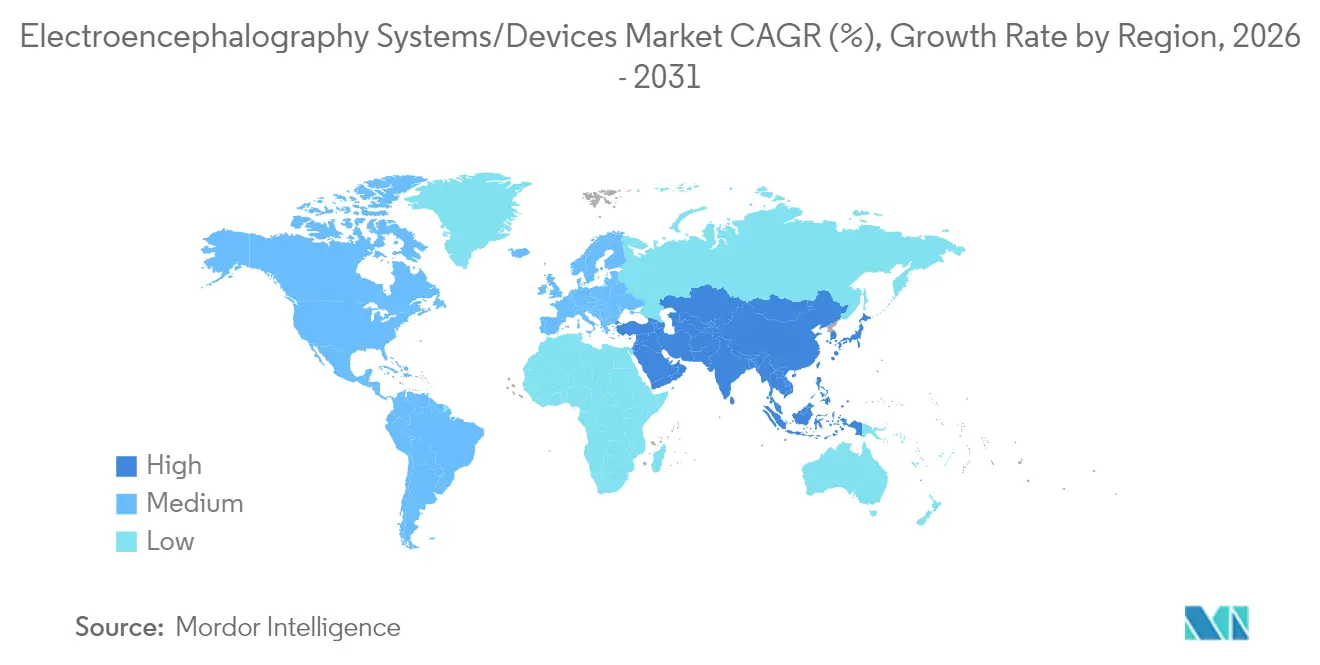

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electroencephalography Systems/Devices Market Analysis by Mordor Intelligence

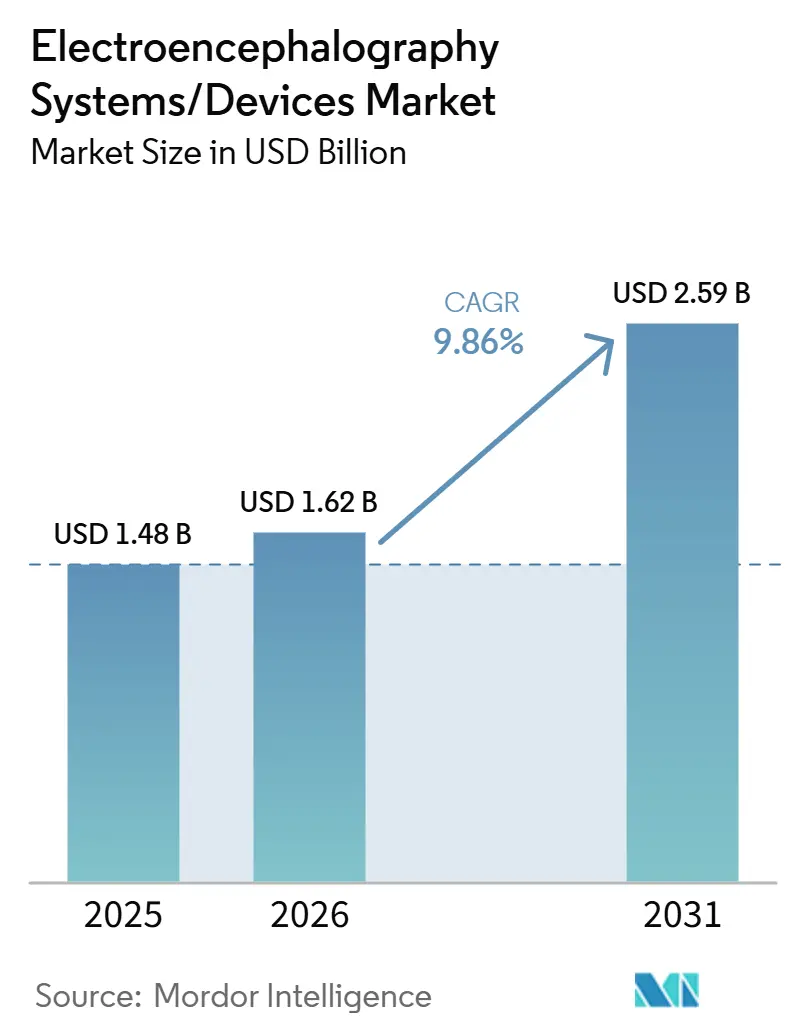

The Electroencephalography Systems/Devices Market size is projected to expand from USD 1.48 billion in 2025 and USD 1.62 billion in 2026 to USD 2.59 billion by 2031, registering a CAGR of 9.86% between 2026 to 2031.

Demand accelerates as neurological disorders overtake cardiovascular diseases as the leading cause of global health loss, a shift that keeps diagnostic volumes rising in hospitals, ambulances, and homes. Product innovation in dry electrodes, low-power sensors, and AI-enabled analytics shortens set-up times and automates triage, helping providers counter persistent shortages of trained neuro-diagnostic technologists. Government programs—most notably the NIH BRAIN Initiative—and parallel funding mechanisms in China and Japan are widening the pipeline of clinical-grade prototypes, while new reimbursement codes improve economic viability for long-term ambulatory monitoring. Commercial strategies increasingly revolve around full-stack platforms that bundle hardware, cloud analytics, and service contracts, enabling recurring revenue and faster update cycles for regional user needs.

Key Report Takeaways

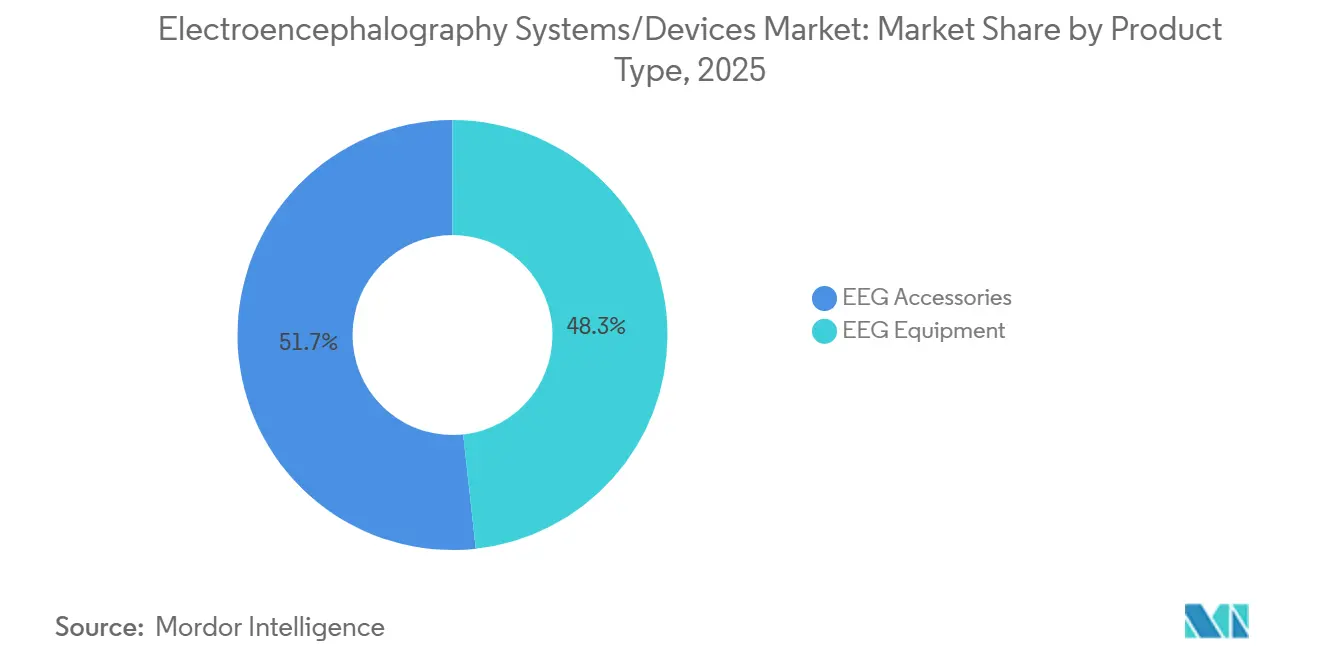

- By product type, EEG accessories led with 51.72% revenue share in 2025, and it is projected to expand at a 10.23% CAGR through 2031.

- By modality, stationary systems held 61.33% of the electroencephalography systems/devices market share in 2025; portable/wearable systems are expected to post a 13.07% CAGR to 2031.

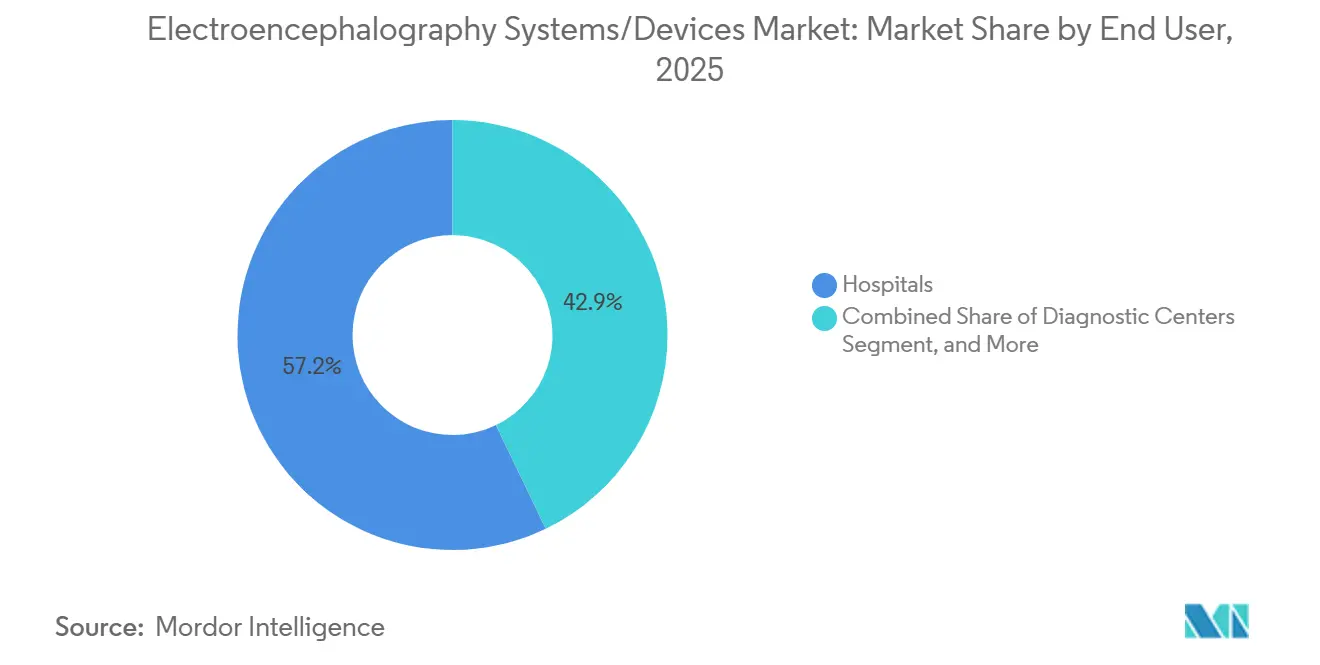

- By end user, hospitals captured 57.15% of the electroencephalography systems/devices market size in 2025, whereas home-care settings recorded the fastest growth at an 12.91% CAGR between 2026-2031.

- By application, disease diagnosis commanded 46.18% revenue share in 2025; brain-computer interface & neurofeedback is forecast to grow at 13.04% CAGR to 2031.

- By geography, North America accounted for 37.41% of 2025 revenue; Asia-Pacific is projected to grow at 10.93% CAGR, the fastest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electroencephalography Systems/Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of epilepsy and other neurological disorders | +2.80% | Global, highest impact in aging populations of North America and Europe | Long term (≥ 4 years) |

| Growing adoption of portable and wireless Electroencephalography systems | +2.10% | Early adoption in North America, rapid expansion in Asia-Pacific | Medium term (2-4 years) |

| Government and private funding for neuroscience research | +1.50% | North America and EU lead; emerging programs in China and Japan | Long term (≥ 4 years) |

| Integration of Electroencephalography sensors into VR/AR wearables | +0.90% | North America and Asia-Pacific core markets | Medium term (2-4 years) |

| Low-cost in-ear and dry-electrode technologies | +1.20% | Highest adoption in cost-sensitive emerging markets | Short term (≤ 2 years) |

| AI-powered edge analytics for automated triage | +0.80% | North America and EU lead, gradual uptake in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising incidence of epilepsy and other neurological disorders

Neurological illnesses now contribute 443 million disability-adjusted life years worldwide, pushing clinicians to broaden Electroencephalography capacity in emergency and outpatient settings. In the United States, 1.2% of adults—around 3 million individuals—live with active epilepsy, and half of them report memory difficulties, indicating unmet needs for high-resolution functional brain assessments [1]Source: Centers for Disease Control and Prevention, “Epilepsy Data and Statistics,” cdc.gov . Global brain disorder cases are expected to increase from 4 billion in 2025 to 4.9 billion by 2050, magnifying the burden on health systems. Academic centers respond with tools such as Johns Hopkins University’s EpiScalp, which lowers epilepsy misdiagnoses by 70% using routine Electroencephalography recordings [2]Source: Johns Hopkins University, “EpiScalp Shows 70% Reduction in Misdiagnoses,” jhu.edu. These developments extend clinical demand into primary care and home monitoring programs, reinforcing volume growth for the electroencephalography systems/devices market.

Growing adoption of portable and wireless Electroencephalography systems

Clearances for wireless headsets with dry electrodes now permit self-installation, enabling decentralized trials and long-term seizure monitoring without hospital stays. Research on ear-Electroencephalography reaches 87.5% seizure detection sensitivity with just 0.1 false alarms per day, proving performance under real-world conditions. Surveys in Finland show elderly patients readily accept home-based Electroencephalography when caregivers provide basic set-up assistance. These trends pivot the electroencephalography systems/devices market toward continuous ambulatory services that reduce readmissions and expand data sets for AI model training.

Government and private funding for neuroscience research

The NIH allocates USD 15 million annually to targeted circuit mapping, and additional notices of funding opportunities appear for low-power wireless sensors under the BRAIN Initiative. Parallel schemes in Japan’s Moonshot R&D and China’s 2030 Brain Project further accelerate academic–industry consortia. Venture investors back complementary platforms, such as a USD 6 million deal that enlarged Firefly Neuroscience’s event-related potential database to 180,000 records. Capital flows shorten development cycles, increase multi-modal data sets, and diversify the supplier base, sustaining double-digit growth in the electroencephalography systems/devices market.

Signal-quality limits in ultra-portable devices

Studies find that cable sway and electrode mass raise motion artifacts, with dry-electrode sets rejecting up to 40% of epochs during walking tasks. Clinical users therefore prefer gel-based systems for intraoperative monitoring, muting adoption of certain consumer-grade models until algorithmic noise suppression improves.

Restraints Impact Analysis*

| Restraint | (≈)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost and maintenance of advanced systems | -1.80% | Highest impact in emerging markets and smaller facilities worldwide | Short term (≤ 2 years) |

| Shortage of trained neuro-diagnostic technologists | -1.20% | North America and EU primarily; growing concern in Asia-Pacific | Medium term (2-4 years) |

| Data-privacy and neuro-ethics concerns | -0.70% | EU leads regulatory debate; expanding to North America and Asia-Pacific | Long term (≥ 4 years) |

| Signal-quality limits in ultra-portable devices | -0.90% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High upfront cost and maintenance of advanced systems

Hospitals often defer capital purchases because premium 256-channel workstations can exceed USD 250,000, while comprehensive service contracts add another USD 20,000 annually. After-hour EEG services further inflate operating costs; studies of U.S. trauma centers reveal staffing is the largest component, prompting mid-size hospitals to explore outsourcing or hybrid models. Dry-electrode platforms promise relief, yet initial acquisition prices still deter under-resourced clinics, tempering near-term installations in the electroencephalography systems/devices market.

Shortage of trained neuro-diagnostic technologists

Enrollment in accredited EEG technologist programs lags growing demand, and retirement rates among senior staff reach 8% annually in some U.S. states. Facilities report difficulty sustaining 24-hour coverage, especially during holidays, leading to diagnostic delays. Tele-EEG services and auto-scoring algorithms close part of the gap, but licensure requirements and liability issues slow adoption, constraining growth potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Equipment innovation drives market evolution

EEG Accessories held 51.72% of 2025 revenue, buoyed by recurring orders for disposable electrodes, gels, and caps that accompany every patient session, growing at 10.45% CAGR through 2031 as hospitals and ambulatory centers refresh installed bases with AI-ready consoles. The electroencephalography systems/devices market size for equipment is projected to climb alongside expanding cohorts of home monitoring programs, where plug-and-play devices reduce training burdens. Nihon Kohden’s 71.4% stake in NeuroAdvanced Corp. enhances its vertical portfolio across consoles and invasive electrodes, signaling further consolidation. Next-generation equipment now ships with built-in cloud APIs and embedded inference chips, letting clinics add algorithm updates via software licenses rather than full hardware swaps.

Consumable demand remains resilient because dry-electrode adoption is incremental, not wholesale. Semi-dry hydrogels extend usable life to several hours, but infection-control policies still necessitate single-patient disposables in intensive care units. Vendors are redesigning accessory kits with color-coded sensors and QR-based re-order tags, promoting automatic replenishment contracts that lock in account stickiness. Over the forecast period, value will migrate to integrated offerings that bundle capital equipment, replaceable parts, and analytics subscriptions, aligning with the subscription economics now common in the electroencephalography systems/devices market.

By Modality: Portable systems challenge traditional dominance

Stationary rigs held 61.33% of 2025 revenue due to dominate academic labs and epilepsy monitoring units due to their ability to support 256 channels and high-sampling rates. Even so, portable wearables expand at an 13.07% CAGR, carving out a share in emergency departments and telehealth programs. The electroencephalography systems/devices market share for portable devices is expected to widen markedly after multiple 510(k) clearances for self-applied headsets, some of which complete a full setup in under five minutes. Lightweight belt-worn amplifiers with Bluetooth Low Energy extend continuous recording beyond 72 hours, capturing intermittent events that hospital stays miss.

Regulators recognize performance parity in targeted use cases; for example, wireless eight-channel patches demonstrate non-inferior seizure detection relative to 19-channel scalp arrays when paired with AI post-processing. Players now offer modular kits combining core amplifiers with clip-on battery packs and electrode arrays, letting clinicians reconfigure density based on study protocol. Research units increasingly deploy hybrid models, anchoring high-density stationary hubs in the lab and issuing companion wearables for follow-up sessions in the field, blending the advantages of both modalities in the electroencephalography systems/devices market.

By End User: Home-care settings drive decentralization

Hospitals generated 57.15% of 2025 revenue, leveraging insurance coverage and critical-care demand. Yet the most rapid growth belongs to Ambulatory Surgical Centers & Clinics at 11.05% CAGR through 2031 as payers reimburse prolonged ambulatory EEG. The electroencephalography systems/devices market size is attributed to domiciliary monitoring, thus scales quickly, aided by patient preference to avoid overnight hospital stays. Elderly neurological patients show high acceptance when caregivers assist with electrode placement, creating a viable model for remote regions and post-stroke rehabilitation.

Diagnostic centers remain pivotal for specialized studies such as long-term stereo-EEG, and academic institutes keep pushing research boundaries. However, workforce constraints prompt hospitals to subcontract overflow studies to tele-EEG service providers, accelerating uptake in outpatient settings. Subscription-based platforms that bundle headset rental, cloud interpretation, and automated alerts lower entry barriers for small practices, dispersing volumes away from centralized units within the electroencephalography systems/devices market.

By Application: Brain-computer interfaces expand therapeutic horizons

Disease Diagnosis maintains primacy with 46.18% revenue share, covering epilepsy, sleep, and intraoperative monitoring. Brain-computer interface and neurofeedback lines rise at 13.04% CAGR as rehabilitation centers adopt closed-loop feedback for stroke, pain, and anxiety management. The electroencephalography systems/devices market size for BCIs grows in parallel with the launch of adaptive deep brain stimulation systems that adjust stimulation using live cortical signals. Consumer markets such as attention training games remain small but create proof-of-concept showcases that attract venture capital.

Sleep monitoring holds steady as insurers realize the cost savings of home polysomnography versus in-lab tests. Meanwhile, anesthesia monitoring sustains demand in surgical suites where EEG-derived indices reduce drug use and shorten recovery times. Hybrid applications surface, for instance, combining cognitive load tracking with VR exposure therapy, widening cross-disciplinary opportunities within the electroencephalography systems/devices market.

Geography Analysis

North America generated 37.41% of 2025 revenue, anchored by the United States’ dense network of level IV epilepsy centers and consistent NIH funding. Reimbursement frameworks, including CPT code revisions for extended EEG, reinforce upgrade cycles as providers swap legacy recorders for cloud-connected units. The electroencephalography systems/devices market size in the region also benefits from strong venture activity that finances AI model training on diverse clinical datasets.

Europe occupies the second-largest share, buoyed by public health systems that standardize care pathways for stroke and dementia. The region’s MDR regulatory regime, although strict, now offers clearer guidance for AI as a Medical Device, giving suppliers confidence to seek multi-country approvals. Partnerships between university hospitals in Germany, France, and Sweden accelerate cross-border clinical trials, adding demand for interoperable data formats in the electroencephalography systems/devices market.

Asia-Pacific records the fastest expansion at 10.93% CAGR through 2031 as China’s 2030 Brain Project and Japan’s Moonshot R&D drive domestic innovation. Growing middle-class healthcare spending, combined with urban hospital construction, lifts baseline unit orders. Tier-one Chinese hospitals pilot integrated neuro-ICUs that combine EEG, fNIRS, and intracranial pressure monitoring, foreshadowing bundled procurement opportunities. In India and Southeast Asia, mobile EEG vans bring diagnostics to rural clinics, exploiting portable headsets’ low power draw. Latin America and the Middle East trail but show steady adoption as private hospital groups import turnkey neurodiagnostic suites, widening the footprint of the electroencephalography systems/devices market.

Regulatory Landscape

Electroencephalographs are regulated as Class II devices in the United States under FDA oversight (21 CFR 882.1400), so product iterations in portable headsets, caps, and amplifiers typically route through the 510(k) pathway. Recent clearances include Zeto, Inc.'s FDA 510(k) clearance (K260455) for its New Wave system in March 2026, Ceribell, Inc.'s FDA 510(k) clearance (K251381) for its Instant EEG Headcap in October 2025 (Product Code GXY), and Epitel, Inc.'s FDA 510(k) clearance (K243185) for its REMI Remote EEG Monitoring System in March 2025, which reinforces momentum around outpatient and remote monitoring workflows.

In Europe, market access remains governed by the EU Medical Device Regulation (EU) 2017/745 (MDR), with transition provisions for certain legacy devices extended to 31 December 2027 or 31 December 2028 under Regulation (EU) 2023/607 when specified conditions are met. IEC 80601-2-26 (including the 2024 amendment) anchors basic safety and essential performance requirements for electroencephalographs across professional, emergency, and home healthcare environments, shaping supplier design controls and verification test plans. International alignment through the International Medical Device Regulators Forum (IMDRF) supports convergence on core principles, but manufacturers still need to manage jurisdiction-specific expectations for cybersecurity, clinical performance evidence, and software updates when EEG platforms include cloud analytics and automated interpretation aids.

Value Chain Analysis

The EEG systems value chain begins with upstream electronic components and sensing consumables, moves through device design and manufacturing, and ends with distribution, installation, and service. Upstream inputs include low-noise analog front ends, microcontrollers or processing hardware for embedded analytics, batteries and wireless modules for portable devices, and high-turn consumables such as electrodes, gels, caps, and lead sets. A key constraint for OEMs is dependence on specialized low-noise components that can become single-source bottlenecks, making multi-sourcing and design-for-availability choices more important as portable and wearable systems target lower power draw and smaller form factors.

Midstream activities cover device assembly, software development (including AI-assisted review and workflow tools), quality management, and regulatory documentation. The compliance layer shapes supplier qualification and production readiness; for example, the FDA Quality Management System Regulation (QMSR) took effect on February 2, 2026, aligning US quality requirements more closely with ISO 13485:2016, while EU MDR continues to drive technical documentation depth and post-market obligations for CE-marked systems. Downstream, value increasingly concentrates in software, service contracts, and recurring consumables, with distribution via direct hospital accounts, neurodiagnostic labs, and home-monitoring programs supported by training, remote support, and data integration. The March 2026 global launch of Natus Medical Incorporated's autoSCORE AI analysis tool shows how interpretation support and workflow automation are being productized alongside hardware to address staffing constraints and improve clinical throughput.

Competitive Landscape

Competitive intensity remains moderate, with a long-tail of regional suppliers balanced against global incumbents. The top five players hold just under 45% of revenue, reflecting a shift toward modular ecosystems where third-party analytics plug into open hardware. Nihon Kohden’s 2024 acquisition spree positions the firm to offer complete epilepsy care packages that pair scalp systems with invasive monitoring grids. U.S. start-ups capture attention by embedding AI inference chips inside headsets, reducing cloud fees and protecting patient privacy during in-ambulance triage.

Strategic differentiation increasingly hinges on software update cadence, algorithm transparency, and cybersecurity compliance. Vendors emphasize ISO/IEC 27001 certification and edge encryption to answer neuro-ethics concerns. Joint ventures between component manufacturers and cloud AI firms accelerate development; for example, European amplifier specialists partner with American algorithm houses to co-market CE-marked seizure detection modules. Distribution rights in high-growth Asia-Pacific markets become critical bargaining chips, and multinationals acquire minority stakes in local distributors to secure channel access. Amid these maneuvers, pricing pressure persists for commodity accessories, prompting suppliers to bundle disposables with extended warranties on capital equipment, a tactic gaining traction in the electroencephalography systems/devices market.

Electroencephalography Systems/Devices Industry Leaders

Natus Medical, Inc.

NeuroWave Systems, Inc

Cadwell Industries, Inc.

Nihon Kohden Corporation

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Decentralized EEG delivery models are creating white space by reducing dependence on scarce neuro-diagnostic technologists and shifting testing toward outpatient and home settings. FDA 510(k) clearances for remote and rapid-setup products provide near-term proof points for these workflows, including Epitel's REMI Remote EEG Monitoring System (March 2025) and Ceribell's Instant EEG Headcap (October 2025). Zeto's FDA-cleared New Wave system (March 2026) further supports outpatient EEG efficiency, aligning with provider efforts to shorten setup time and expand study volumes beyond traditional epilepsy monitoring units.

Software-led differentiation is also gaining traction, particularly where health systems face 24-hour coverage gaps and need consistent interpretation at higher throughput. Natus Medical Incorporated's global launch of the autoSCORE AI analysis tool (March 2026) indicates ongoing vendor investment in routine EEG, long-term monitoring, and ambulatory study workflows, supporting platform bundling strategies that pair hardware, analytics, and service. Safety and performance expectations for professional, emergency, and home healthcare environments are reinforced through IEC 80601-2-26 (with the 2024 amendment), which encourages manufacturers to design portable systems that meet clinical-grade requirements while expanding into new care pathways. Taken together, these signals align with product migration toward wearable form factors, standardized data pipelines, and service models that bundle consumables, device rental, cloud analytics, and remote review.

Recent Industry Developments

- May 2026: Cadwell Industries, Inc. launched the Cadwell Guardian intraoperative neuromonitoring (IONM) system in the United States, featuring a pod-based architecture with Cascade Surgical Studio 4.0 software. The launch strengthens Cadwell's neurodiagnostics footprint around scalable platform configurations and supports bundled offerings that connect perioperative monitoring with broader electrophysiology workflows.

- March 2026: Natus Medical Incorporated announced the global launch of its autoSCORE AI-driven analysis tool for routine EEG, long-term monitoring, and ambulatory studies. This expands the company's software value layer and addresses operational bottlenecks by standardizing parts of the review workflow in settings facing EEG technologist shortages.

- November 2024: Nihon Kohden bought a 71.4% stake in NeuroAdvanced Corp., parent of Ad-Tech Medical Instrument, expanding its portfolio across scalp and invasive electrode offerings for epilepsy care. The transaction reinforced vertical integration and broadened the installed-base pathway for consolidated epilepsy monitoring solutions across hospital and specialized diagnostic channels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenues generated from electroencephalography (EEG) systems and devices used to record and digitize brain electrical activity in clinical diagnosis, monitoring, and research settings, including standard accessories sold with the system.

Scope exclusions: Invasive depth electrodes and combined multimodal EEG-EMG workstations marketed as bundled platforms are excluded.

Segmentation Overview

- By Product

- EEG Equipment

- EEG Accessories

- By Modality

- Stand-alone (Stationary) Systems

- Portable / Wearable Systems

- By End User

- Hospitals

- Diagnostic Centers

- Ambulatory Surgical Centers & Clinics

- Research & Academic Institutes

- Home-Care Settings

- By Application

- Disease Diagnosis

- Sleep Monitoring

- Anesthesia Monitoring

- Brain-Computer Interface & Neurofeedback

- Other Applications

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public health and utilization signals that sit upstream of EEG demand, then shifted into device supply and pricing context so our assumptions did not drift. Sources reviewed included, for example, the CDC for epilepsy and sleep related statistics, the NIH and PubMed indexed journals for clinical practice and evidence trends, and the FDA for device clearance context and technology direction.

We also checked payer and care delivery indicators from bodies such as CMS, along with hospital procedure and neurology service line information that is commonly shared in annual reports and investor presentations. Trade and production context was supported using government trade statistics portals and an import and export shipment level database to sense-check unit flows where disclosure was limited. The sources listed here are not exhaustive, and additional public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions were used to pressure-test what gets counted as an EEG system sale versus an accessory refresh, and to align average selling price logic with real procurement patterns across hospitals, diagnostic centers, and research users. Inputs were also gathered on channel mix, typical replacement cycles, and how portable systems are being adopted across APAC, EMEA, and the Americas so the regional split stayed realistic.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 16% | APAC: 43% |

| Mid tier: 55% | Functional/Unit leaders: 32% | EMEA: 37% |

| Smaller Players: 18% | Managers: 52% | Americas: 20% |

Market-Sizing & Forecasting

Sizing was built from the demand pool outward, where procedure and patient workload indicators are translated into expected EEG system usage, before revenue is reconstructed using unit needs and pricing. We used the top-down approach once by linking neurology and sleep diagnostics activity to EEG install base needs, then mapping replacement and new additions into annual units.

To keep it grounded, selective bottom-up approximations were used as checks, such as sampled price by typical configuration, channel markups seen in tenders, and supplier revenue disclosures where available. Those checks are then used to adjust totals when the two views drift. Model inputs included, in an illustrative way, EEG test volumes (routine, ambulatory, and sleep lab use), installed base replacement cycles, average channels per system as a proxy for configuration value, accessory attach rates, and regional hospital and diagnostic center capacity additions. For forecasting, scenario analysis was applied around adoption of portable systems, reimbursement stability, and hospital capital spending timing, and the final outlook was aligned to what interviewees described as the most likely purchasing cadence.

Data Validation & Update Cycle

Outputs were validated through cross-checks against independent signals, including procedure growth, tender activity patterns, and implied unit shipments based on trade movement where relevant. When a region showed an unusual jump, assumptions were re-opened and follow-up questions were triggered, with sources used to confirm whether it was a one-time procurement wave or a real step-up.

Each model goes through multi-step analyst review so drivers, calculations, and currency handling are consistent across years. The report is refreshed annually, and interim updates are made when material events can change demand or pricing, followed by a final pre-delivery review so clients receive the latest updated view.

Mordor Intelligence's Electroencephalography Systems Devices Market Sizing Compared With Other Published Estimates

Published EEG market values can vary even when they appear to cover the same product category, because coverage boundaries, year labeling, and pricing mechanics are not handled the same way. The spread usually becomes larger when one estimate mixes accessories, software, or services differently, or when conversion into USD is done using a different timing.

One driver in this market is how average selling prices are carried forward, since portable systems and higher channel configurations can shift the blended ASP without a matching change in unit volumes. Another driver is update cadence, where price revisions and hospital purchasing delays can make one year look higher or lower than another, and the model can drift if these are not rechecked against procedure and procurement signals. For that reason, the refresh and currency timing rules applied by Mordor Intelligence can land at a different 2026 value than sources anchored to older base years.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.93 B (2026) | |

| Global Consultancy A | USD 1.32 B (2024) | Uses a different base year and forecast window, and the scope appears to emphasize device revenues without clearly separating system sales from accessory refresh effects, which can compress the value versus a later-year, replacement-cycle-led build. |

| Industry Publisher B | USD 1.61 B (2024) | Anchors the market to 2024 and applies a steady growth path, but the disclosure does not make currency timing, ASP progression by configuration, or the handling of portable versus standalone system mixes explicit, which can shift the implied jump into 2026. |

Overall, differences are mostly explained by year anchoring and how price and mix are carried through the model, rather than a disagreement that EEG is growing. When scope lines are drawn clearly, and the pricing and replacement cycle checks are kept consistent, the resulting number is easier for users to trace back to real demand and procurement behavior.

Key Questions Answered in the Report

What is the current size of the electroencephalography systems/devices market?

The market stands at USD 1.62 billion in 2026 and is forecast to reach USD 2.59 billion by 2031.

How fast is the electroencephalography systems/devices market expected to grow?

Industry revenue is projected to increase at a 9.86% compound annual growth rate through 2031.

Which product segment is expanding the quickest?

Portable and wearable EEG equipment is the fastest-growing segment, set to post an 13.07% CAGR on the back of dry-electrode advances and home-monitoring demand.

What technology trend is reshaping competitive strategies?

AI-powered edge analytics now automate seizure detection and trim set-up time, allowing providers to mitigate shortages of trained EEG technologists.

Where does the strongest regional upside lie?

Asia-Pacific shows the highest upside with a 10.93% CAGR, driven by widening healthcare access and government-backed neurotechnology programs.

Page last updated on: