Brain Ischemia Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.64 Billion |

| Market Size (2030) | USD 2.45 Billion |

| Growth Rate (2025 - 2030) | 8.38% CAGR |

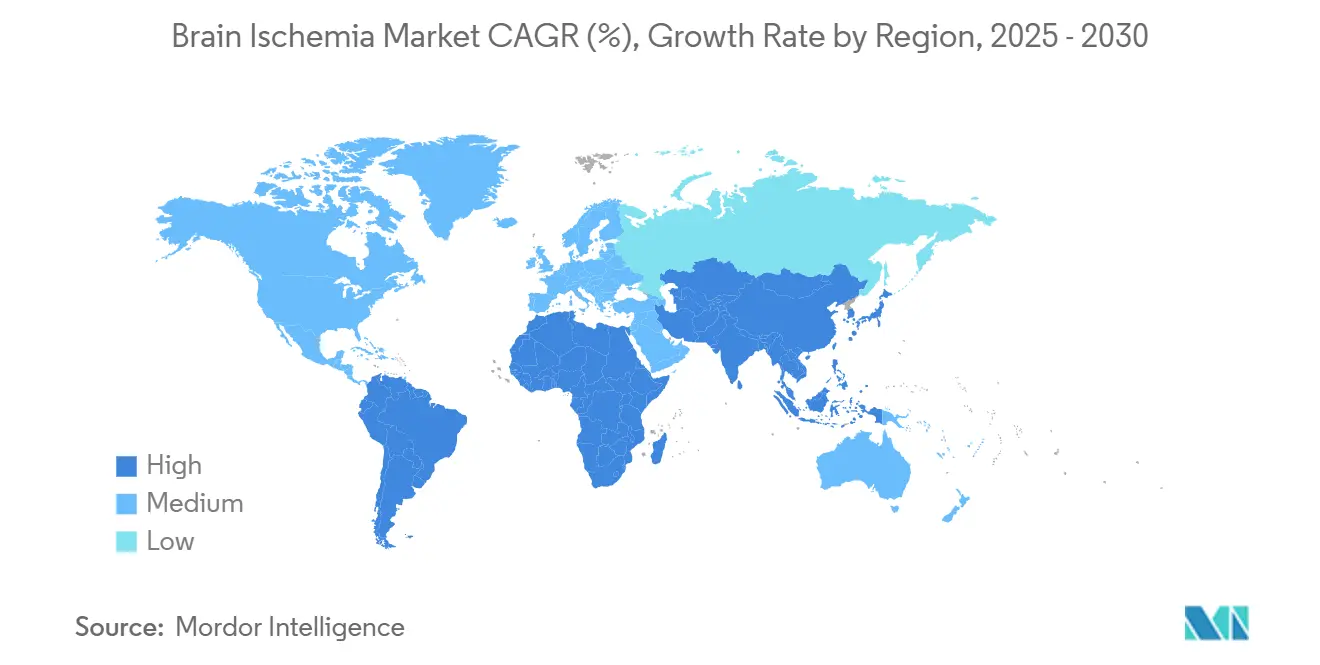

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

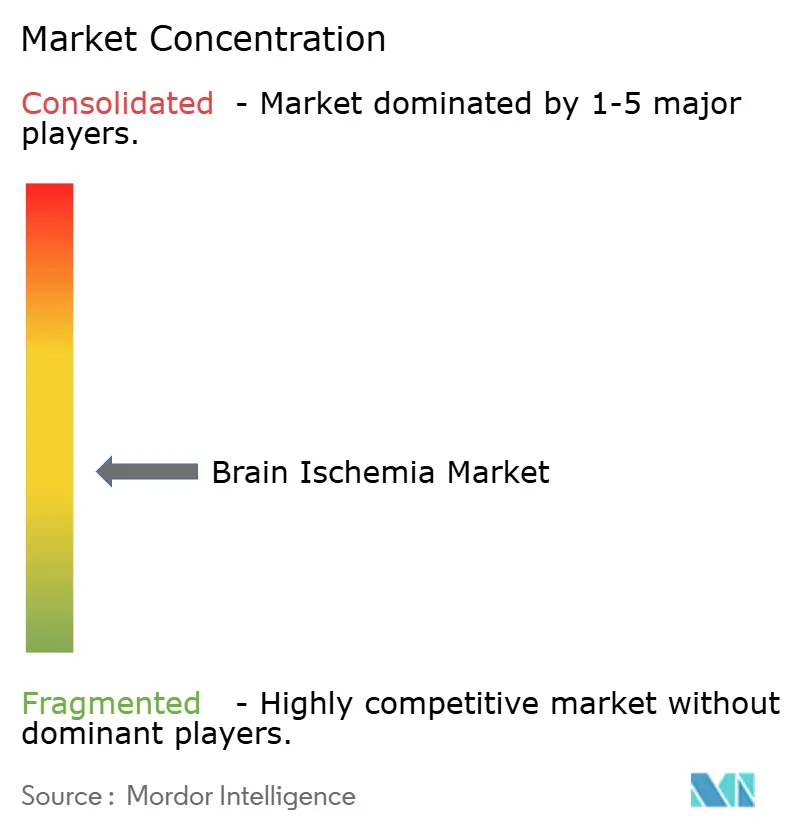

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brain Ischemia Market Analysis by Mordor Intelligence

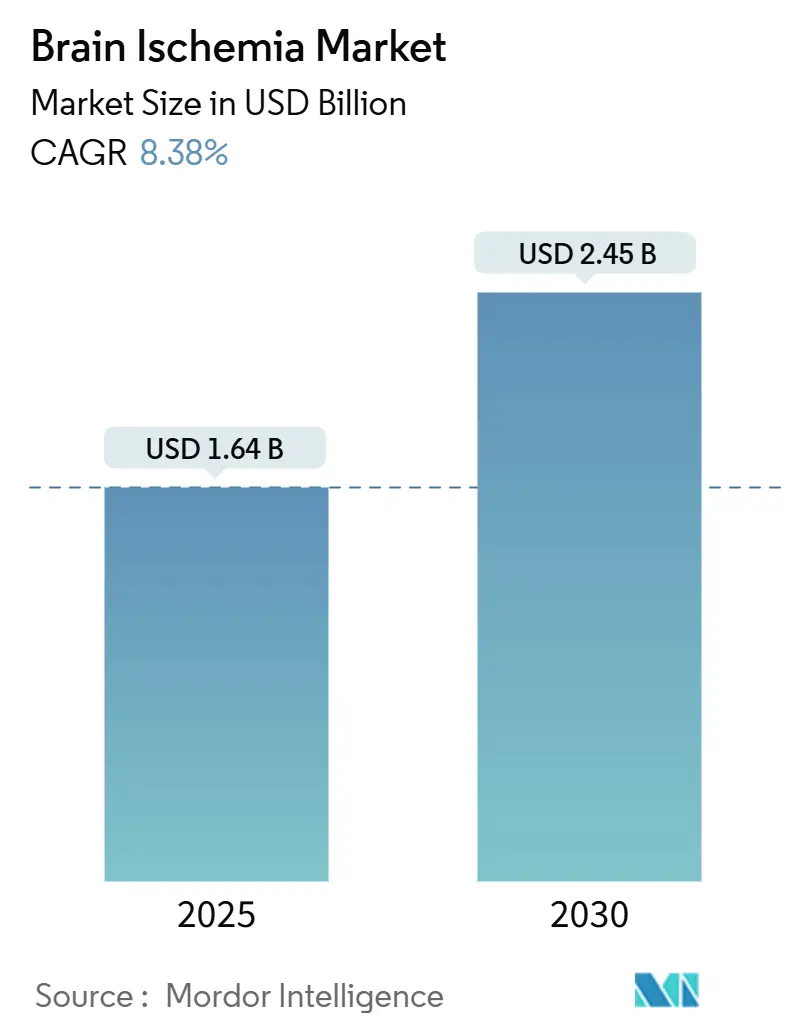

The global brain ischemia market size stands at USD 1.64 billion in 2025 and is forecast to reach USD 2.45 billion by 2030, reflecting an 8.38% CAGR over the outlook period. Breakthrough regulatory approvals, notably the U.S. Food and Drug Administration’s clearance of tenecteplase in March 2025, are expanding therapeutic options and reshaping competitive strategies.[1]American Heart Association Staff Writers, “ISC 2025 Session Report: New and Alternative Thrombolytic Therapies,” American Heart Association, ahajournals.org Mechanical thrombectomy devices continue to lift procedural volumes as clinical studies show 20% higher functional-independence rates than intravenous thrombolysis alone.[2]Marc Taylor, “Advances in Endovascular Thrombectomy for the Treatment of Acute Ischemic Stroke,” Taylor & Francis Online, tandfonline.com Rapid uptake of artificial-intelligence imaging platforms, favorable reimbursement reforms in Europe, and growing investment across Asia-Pacific reinforce an optimistic demand trajectory. Meanwhile, specialist shortages and cost-coverage gaps temper near-term adoption of advanced neurovascular devices, spurring efficiency innovations and bundled-payment experimentation.

Key Report Takeaways

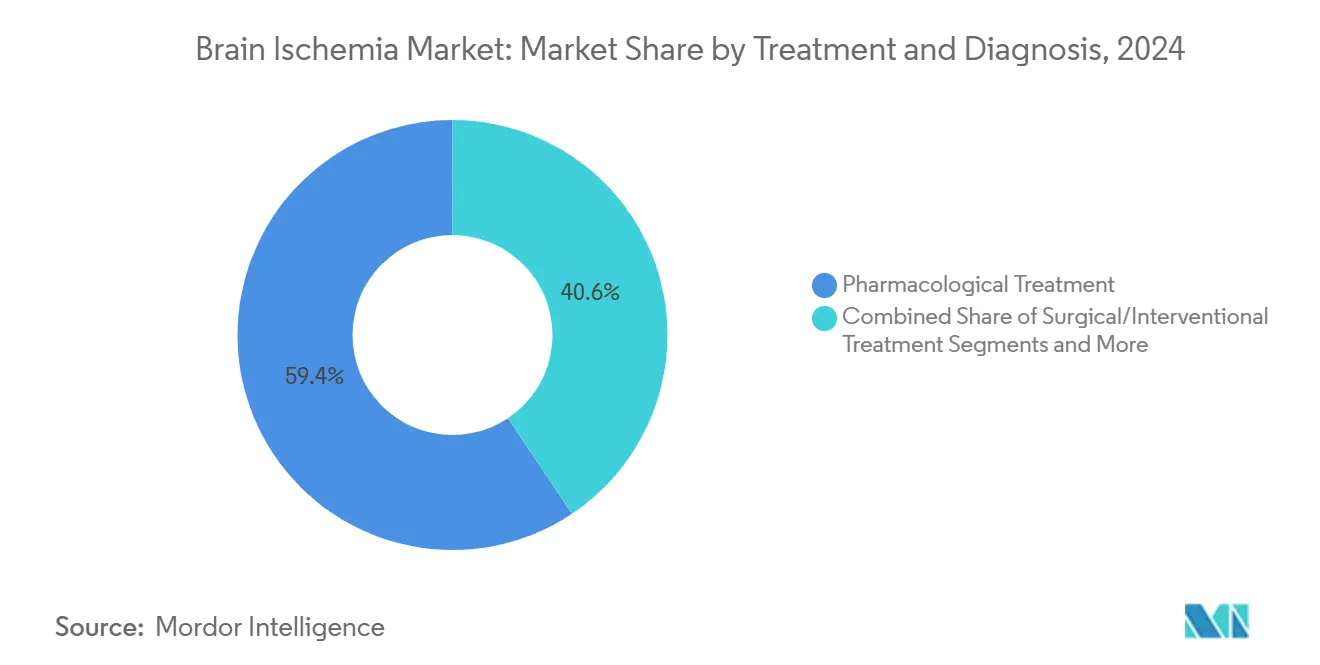

- By treatment & diagnosis, pharmacological approaches led with 59.37% share in 2024, while surgical and interventional treatments are projected to advance at an 11.79% CAGR through 2030.

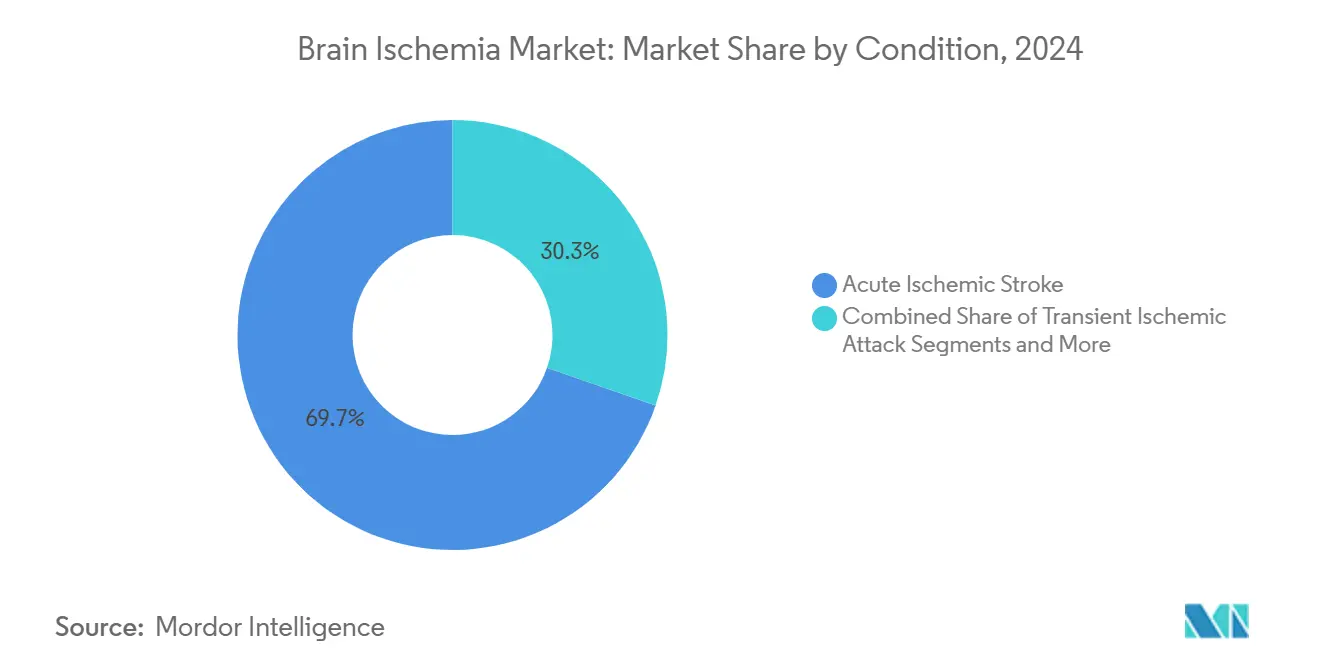

- By condition, acute ischemic stroke accounted for 69.68% share in 2024, whereas ischemia-reperfusion injury is poised for 10.48% CAGR growth to 2030.

- By end user, hospitals captured 56.66% of the 2024 landscape; ambulatory surgical centers are forecast to post an 11.04% CAGR by 2030.

- By geography, North America commanded 34.91% revenue share in 2024, and Asia-Pacific is set to expand at an 11.66% CAGR over the forecast horizon.

Global Brain Ischemia Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of ischemic stroke | +2.1% | Global, highest in Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| Favorable reimbursement for thrombectomy procedures | +1.8% | North America & EU, selective coverage in APAC | Medium term (2-4 years) |

| Advances in rapid neuro-imaging & diagnostics | +1.5% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Tenecteplase adoption improving economics | +1.3% | Global, led by North America & Europe | Short term (≤ 2 years) |

| AI-enabled pre-hospital stroke triage platforms | +1.0% | North America & EU, expanding urban APAC centers | Medium term (2-4 years) |

| Nanoparticle neuro-protective delivery breakthroughs | +0.7% | Global research hubs, clinical translation pending | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Ischemic Stroke

Ischemic stroke remains the second-leading cause of death worldwide, affecting roughly 12 million people each year. China exemplifies this pressure, with stroke now the leading cause of disability across Asia-Pacific populations.[3]Y. Zhang et al., “A Scoping Review of the Utilization of Mobile Stroke Units in Low and Lower Middle-Income Countries,” BMC Health Services Research, bmchealthservres.biomedcentral.comGlobal stroke-related costs are projected to climb toward USD 1.6 trillion annually, propelling health systems to expand emergency intervention capacity. Only 5% of eligible patients presently receive thrombectomy, signaling significant untapped demand. Heightened diabetes prevalence also intensifies risk, catalyzing interest in dual-indication therapies such as GLP-1 agonists that exhibit neuro-protective effects.

Favorable Reimbursement for Thrombectomy Procedures

Reimbursement trends directly influence provider adoption of advanced neurovascular tools. While Medicare reimburses just 18–21% of an estimated USD 13,000 thrombectomy cost in the United States, bundled-payment pilots have trimmed systemwide expenditures by USD 2,900 per case. European payers report even stronger savings, with direct transfer to angiography suites reducing costs by €2,848 per patient. FDA Breakthrough Device designations accelerate commercial timelines, enabling suppliers to pursue premium pricing tied to demonstrable outcome improvements.

Advances in Rapid Neuro-Imaging & Diagnostics

AI-based imaging suites deliver 451% five-year returns through workflow efficiency gains and improved triage accuracy. Blood-based GFAP assays distinguish ischemic versus hemorrhagic stroke with up to 95% accuracy before hospital arrival, potentially reshaping pre-hospital protocols. Extended perfusion-imaging treatment windows of 24 hours post-onset have yielded 54% higher rates of functional recovery when alteplase is administered within this timeframe.

Tenecteplase Adoption Improving Economics

Tenecteplase secured FDA approval in March 2025 as the first new stroke thrombolytic in three decades, offering single-bolus dosing that lowers nursing complexity and medication error risk. Clinical trials show better recanalization rates in large-vessel occlusions relative to alteplase, particularly when paired with thrombectomy. Manufacturing efficiencies underpin competitive drug pricing, improving payer economics and widening patient access.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Narrow therapeutic window for thrombolytics | −1.4% | Global, acute in resource-limited settings | Medium term (2-4 years) |

| High cost of neurovascular devices & procedures | −1.2% | Global, most severe in emerging markets | Long term (≥ 4 years) |

| Shortage of interventional neuroradiologists | −0.9% | Global, steepest in low-income economies | Long term (≥ 4 years) |

| Liability risks of off-label antiplatelet combos | −0.6% | North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Narrow Therapeutic Window for Thrombolytics

Traditional 4.5-hour dosing limits exclude many patients, particularly in rural areas lacking rapid imaging capacity. CT perfusion protocols extend eligibility to 24 hours but depend on advanced infrastructure. Liability fears deter off-label dosing extensions, reinforcing inequitable access patterns.

High Cost of Neurovascular Devices & Procedures

With average thrombectomy costs near USD 13,000 and sub-20% Medicare reimbursement, hospitals subsidize stroke programs. In India, only 2,000–3,000 of the required 200,000 annual thrombectomies occur due to financing constraints. Import duties, limited competition, and volatile currencies further elevate device prices in developing regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment & Diagnosis: Surgical Innovation Drives Growth

Mechanical thrombectomy devices anchor the fastest-growing subsegment with an 11.79% CAGR, catalyzed by 20% superior functional-independence outcomes versus drug therapy alone. Pharmacological interventions still hold 59.37% of 2024 revenue, but their relative expansion slows as interventional modalities gain favor. FDA’s Breakthrough Device Program accelerates market entry for next-generation aspiration catheters, stent retrievers, and distal-access systems. Diagnostic imaging, notably AI-enhanced CT perfusion, now determines candidacy for up to 24-hour treatment windows, increasing procedure volumes. Monitoring and post-acute tools, including home-based robotics, strengthen functional recovery benchmarks, while early-stage stem-cell studies hint at longer-term regenerative possibilities.

Combined regimens that bridge intravenous thrombolysis and thrombectomy boost recanalization, underpinning value-based payment models focused on 90-day modified Rankin outcomes. Suppliers that integrate imaging, device, and data-analytics portfolios are well positioned to capture incremental wallet share as hospitals seek streamlined, evidence-based stroke pathways. These cross-platform ecosystems underpin a rising focus on procedure standardization and predictable economics within the brain ischemia market.

By Condition: Ischemia-Reperfusion Injury Gains Prominence

Acute ischemic stroke maintains a 69.68% share, but ischemia-reperfusion injury is forecast to grow at a 10.48% CAGR as researchers target secondary tissue damage pathways. Emerging neuroprotective agents such as GAI-17 are specifically engineered to limit reperfusion-induced apoptosis, expanding the therapeutic tool-kit beyond primary recanalization. Heightened imaging sensitivity is uncovering silent and small-vessel strokes, creating fresh diagnostic subsegments. Preventive management of transient ischemic attacks gains traction as public-awareness campaigns drive earlier presentation, while cerebral small-vessel disease research now connects micro-infarcts with cognitive decline.

Investment in combination therapies targeting both occlusion and reperfusion extends the commercial runway for biopharma entrants. Consequently, the brain ischemia market size tied to adjunctive neuroprotection could outpace historical trends, once pivotal trials translate into regulatory approvals and reimbursement support.

By End User: Ambulatory Centers Capture Market Share

Hospitals retain 56.66% dominance due to comprehensive stroke-center infrastructure; however, ambulatory surgical centers are projected to post an 11.04% CAGR through 2030. Shorter procedure times, streamlined anesthesia, and lower overhead make select diagnostic and low-risk interventions feasible in outpatient environments. Specialty neurology clinics bridge acute-care discharge and long-term rehabilitation, adopting tele-monitoring systems that enable remote modified Rankin scoring. Academic institutions remain pivotal innovation nodes, advancing agents such as DM199 into Phase 2/3 study under the ReMEDy2 program.

Value-based contracting accelerates cross-setting coordination. Integrated delivery networks that align imaging, procedure, and follow-up services under unified dashboards are positioned to capture rising demand across the brain ischemia market share continuum.

Geography Analysis

North America contributed 34.91% of 2024 revenue, leveraging a dense network of comprehensive stroke centers and the FDA’s expedited pathways. Reimbursement pressures persist, yet AI-assisted imaging and bundled-payment pilots are improving throughput and economics. Canada’s publicly funded model drives equitable access, while Mexico invests in urban stroke hubs.

Asia-Pacific is projected for 11.66% CAGR as aging demographics and lifestyle shifts inflate stroke incidence. China’s healthcare reforms expand thrombectomy penetration, and Japan continues pioneering neuro-rehabilitation robotics. India faces acute device-cost and specialist-shortage barriers, performing barely 1% of its estimated thrombectomy need. Australia and South Korea echo Western adoption curves, whereas Southeast Asian economies focus on foundational stroke infrastructure.

Europe benefits from integrated healthcare systems and the EUR 26.9 million UMBRELLA initiative aimed at standardizing AI-guided stroke care. Central-Eastern countries are catching up through cross-border training and technology-leasing programs. The Middle East and Africa invest selectively in tertiary centers, particularly across the Gulf Cooperation Council, while South America’s momentum rests on Brazil’s and Argentina’s expanding neurologic emergency networks.

Competitive Landscape

The competitive set blends diversified device majors with nimble neurovascular specialists and AI-software pioneers. Stryker’s USD 4.9 billion acquisition of Inari Medical strengthens its aspiration portfolio, while Johnson & Johnson evaluates a USD 1 billion divestiture of Cerenovus to refocus capital. Medtronic leverages its geographic breadth to pilot robotic-assisted thrombectomy platforms. Smaller innovators, including DiaMedica Therapeutics, carve niches through first-in-class biology such as kallikrein-1 modulation.

AI-driven workflow vendors like RapidAI and Brainomix cement partnerships with scanner OEMs, embedding analytics within modality sales. Nanoparticle developers pursue strategic alliances to de-risk clinical translation. As reimbursement ties to outcome metrics tighten, suppliers that bundle devices, drugs, and data into provable economic value are poised to consolidate brain ischemia market share.

Brain Ischemia Industry Leaders

Boehringer Ingelheim

F. Hoffmann-La Roche Ltd

Medtronic

Stryker

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Revalesio received FDA Fast Track for RNS60, a neuro-protective therapy aimed at preserving brain tissue after reperfusion.

- May 2025: Tenecteplase gained FDA approval as the first novel stroke thrombolytic since the 1990s, simplifying dosing and improving economics.

- February 2025: DiaMedica Therapeutics published peer-reviewed evidence of DM199’s collateral-circulation benefits, reinforcing its Phase 2/3 study momentum.

Global Brain Ischemia Market Report Scope

| Pharmacological Treatment | Thrombolytics |

| Antiplatelet Agents | |

| Anticoagulants | |

| Neuro-protective Agents | |

| Regenerative / Stem-Cell Therapy | |

| Combination Therapies | |

| Surgical/Interventional Treatment | Mechanical Thrombectomy Devices |

| Embolization & Coiling Devices | |

| Stents & Flow Diverters | |

| Diagnostic Imaging | |

| Monitoring & Post-Acute Management |

| Acute Ischemic Stroke |

| Transient Ischemic Attack |

| Cerebral Small-Vessel Disease |

| Silent Brain Infarction |

| Ischemia-Reperfusion Injury |

| Hospitals |

| Specialty Neurology Clinics |

| Ambulatory Surgical Centers |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment & Diagnosis | Pharmacological Treatment | Thrombolytics |

| Antiplatelet Agents | ||

| Anticoagulants | ||

| Neuro-protective Agents | ||

| Regenerative / Stem-Cell Therapy | ||

| Combination Therapies | ||

| Surgical/Interventional Treatment | Mechanical Thrombectomy Devices | |

| Embolization & Coiling Devices | ||

| Stents & Flow Diverters | ||

| Diagnostic Imaging | ||

| Monitoring & Post-Acute Management | ||

| By Condition | Acute Ischemic Stroke | |

| Transient Ischemic Attack | ||

| Cerebral Small-Vessel Disease | ||

| Silent Brain Infarction | ||

| Ischemia-Reperfusion Injury | ||

| By End User | Hospitals | |

| Specialty Neurology Clinics | ||

| Ambulatory Surgical Centers | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the brain ischemia market in 2025?

The brain ischemia market size is USD 1.64 billion in 2025 with an 8.38% CAGR projected through 2030.

Which treatment type shows the fastest growth momentum?

Surgical and interventional procedures, led by mechanical thrombectomy, are poised for an 11.79% CAGR through 2030 due to superior functional outcomes.

Why is tenecteplase considered a game changer?

Tenecteplase offers single-bolus dosing, stronger large-vessel recanalization, and lower administration costs than alteplase, driving rapid adoption since its 2025 FDA approval.

Which region will expand the most through 2030?

Asia-Pacific is forecast to grow at 11.66% CAGR, propelled by rising stroke burden and increased investment in neurovascular infrastructure.

What limits broader thrombectomy adoption today?

High device and procedural costs, limited reimbursement, and a worldwide shortage of interventional neuroradiologists constrain utilization despite strong clinical evidence.

Page last updated on: