Neurointerventional Devices Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 2.84 Billion |

| Market Size (2031) | USD 3.55 Billion |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

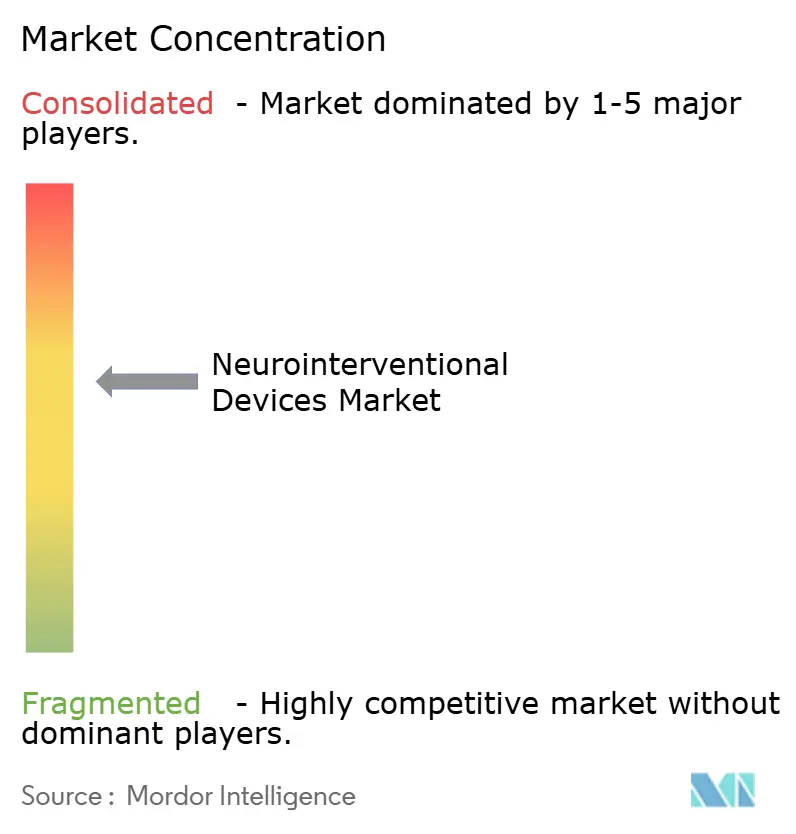

| Market Concentration | Medium |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neurointerventional Devices Market Analysis by Mordor Intelligence

The neurointerventional devices market size in 2026 is estimated at USD 2.84 billion, growing from 2025 value of USD 2.71 billion with 2031 projections showing USD 3.55 billion, growing at 4.62% CAGR over 2026-2031. Growing preference for minimally invasive endovascular approaches, rising global stroke incidence, and continuous device innovation sustain demand. The neurointerventional devices market also benefits from the wider availability of advanced imaging and artificial intelligence tools that improve procedural planning and speed. Expansion of mechanical thrombectomy indications, combined with favorable reimbursement revisions in several countries, opens new patient pools. Meanwhile, shifting care toward outpatient settings places cost-effective devices in a strong position across the neurointerventional devices market.

Key Report Takeaways

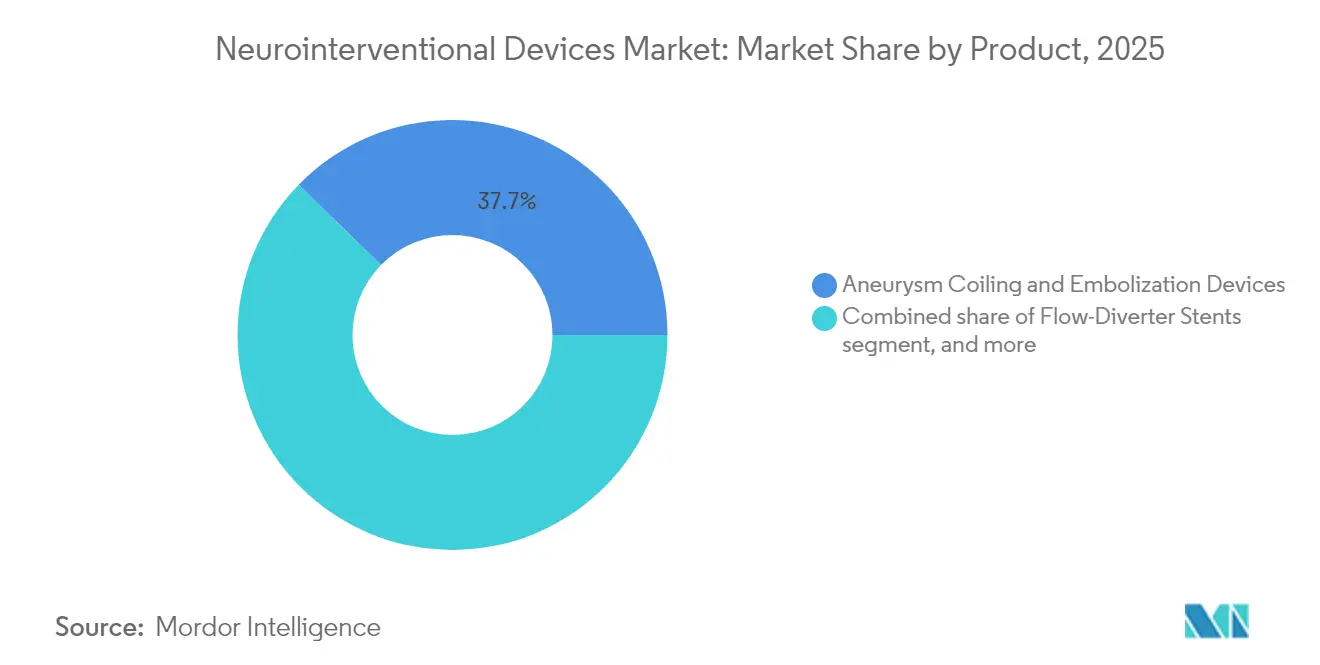

- By product category, aneurysm coiling and embolization devices led with 37.68% revenue share in 2025, while mechanical thrombectomy is advancing at a 6.42% CAGR through 2031.

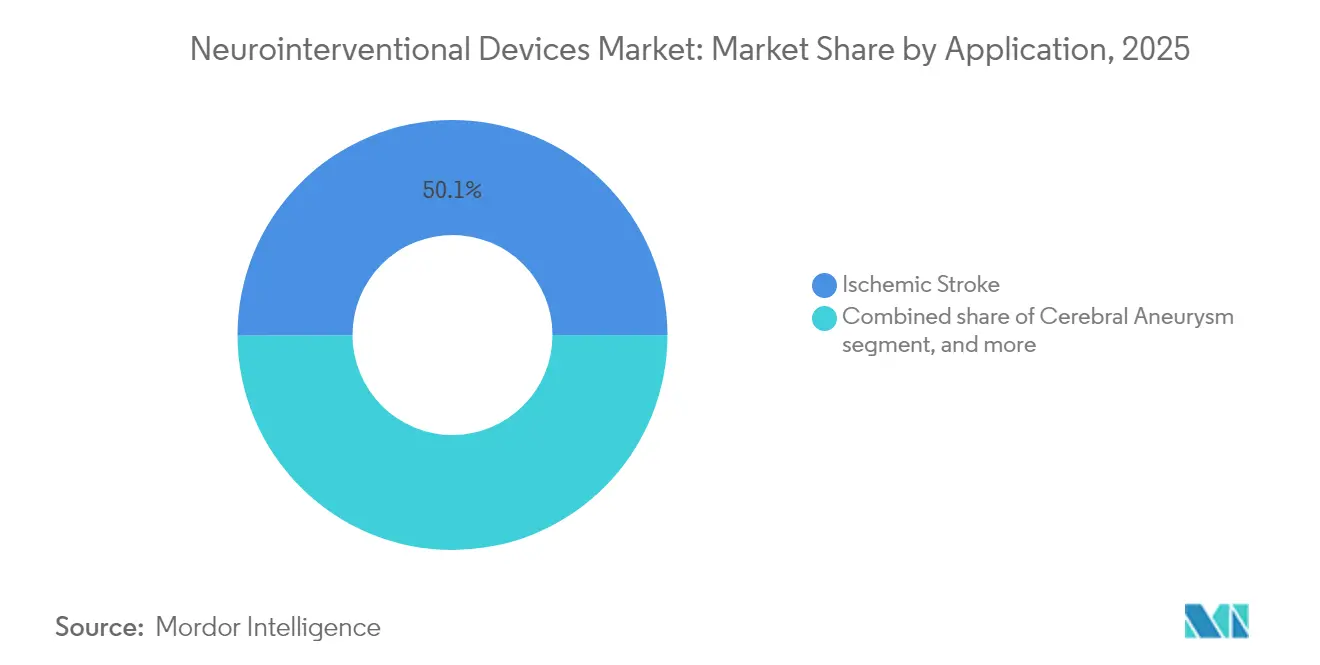

- By application, ischemic stroke accounted for 50.05% of neurointerventional devices market share in 2025 and is expanding at a 6.9% CAGR to 2031.

- By end-user, tertiary hospitals captured 70.62% share of the neurointerventional devices market size in 2025, yet ambulatory centers are growing fastest at 7.12% CAGR.

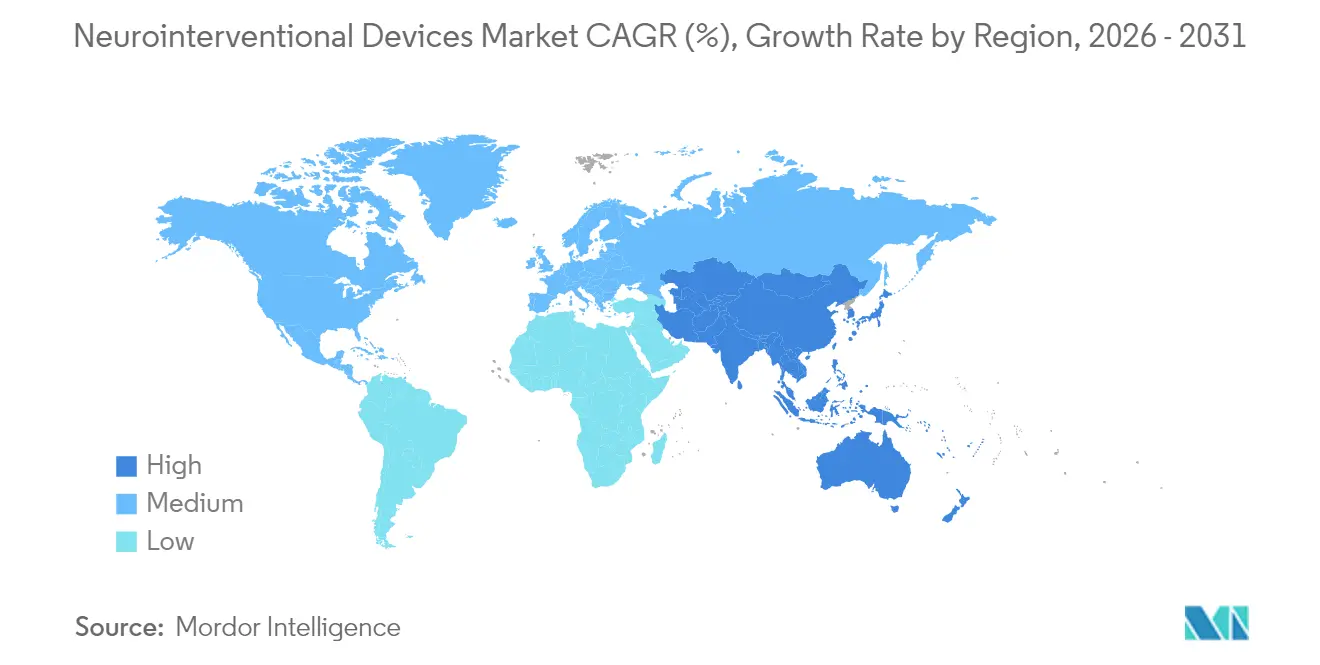

- By geography, North America held 40.12% share in 2025, whereas Asia-Pacific is projected to grow at 5.28% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Neurointerventional Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of stroke and cerebral aneurysm | +1.2% | Global, strongest in aging regions of North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Continuous technological innovations in neurovascular devices | +1.1% | Global, led by North America and Europe innovation hubs | Medium term (2-4 years) |

| Expanding reimbursement coverage for endovascular procedures | +0.8% | North America and Europe; emerging momentum in Asia-Pacific | Medium term (2-4 years) |

| Growing acceptance of mechanical thrombectomy as standard of care | +0.9% | Global, rapid uptake in developed markets | Short term (≤ 2 years) |

| Penetration of neurointerventional suites in secondary hospitals | +0.6% | Emerging and rural settings in North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Integration of robotics and artificial intelligence for precision navigation | +0.7% | Global, early adoption in high-income countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Stroke and Cerebral Aneurysm

Stroke remained the second leading global cause of death in 2019, affecting 12.2 million people annually. Aging demographics in developed economies and climbing hypertension and diabetes prevalence in emerging regions intensify demand for neurovascular solutions. Mechanical thrombectomy volumes nearly tripled between 2017 and 2019 after treatment time windows expanded, underscoring the clinical shift toward endovascular therapy. Middle meningeal artery embolization procedures climbed from 4,014 in 2019 to 20,836 in 2023 with forecasts of 79,483 by 2029, proving sustained procedure growth[1]Journal of NeuroInterventional Surgery, “Worldwide Mechanical Thrombectomy Trends,” jnis.bmj.com. Wider adoption of minimally invasive approaches lowers overall hospital stays and costs, cementing long-term demand for the neurointerventional devices market.

Continuous Technological Innovations in Neurovascular Devices

Rapid engineering cycles introduce tools that lift success rates and broaden eligibility. Milli-spinner thrombectomy technology reaches clot-removal success above 90%, doubling traditional performance by densifying fibrin networks[2]Stanford News, “Milli-Spinner Technology Improves Clot Removal,” news.stanford.edu. AI-guided cerebral aneurysm coiling demonstrated 92.7% precision and 97.2% recall in first-in-human trials. Fourth-generation flow diverters such as Pipeline Vantage achieved 81.7% occlusion at six months with flawless deployment, while robotic systems like CorPath GRX delivered 94% procedural effectiveness across 117 embolization patients. These breakthroughs fuel competitive differentiation and uplift the neurointerventional devices market.

Growing Acceptance of Mechanical Thrombectomy as Standard of Care

Landmark trials SELECT2, ANGEL-ASPECT, and TENSION reported functional independence of 20-30% versus 7-12% for medical management, solidifying thrombectomy guidelines worldwide[3]American Heart Association, “SELECT2, ANGEL-ASPECT, and TENSION Trial Results,” strokeaha.org. Treatment windows now extend to 24 hours, increasing the eligible patient base and spurring near-threefold procedural growth after 2018. Nationwide registries like EXCELLENT logged 94.5% final recanalization in nearly 1,000 patients, validating real-world outcomes. Standardized protocols and wider training accelerate diffusion beyond comprehensive stroke centers, enlarging the neurointerventional devices market.

Integration of Robotics and Artificial Intelligence for Precision Navigation

Robotic diagnostic cerebral angiography completed 77.9% of 113 cases without manual conversion and limited mean fluoroscopy time to 13.2 minutes. AI-powered navigation platforms alert clinicians to micro-movements during aneurysm coiling, while predictive models outperform clinicians in detecting large-vessel occlusions. These tools help compensate for specialist shortages and deliver standardized high-quality care. Growing adoption of robotics and AI therefore strengthens the long-term outlook for the neurointerventional devices market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent multiregional regulatory approval processes | -0.7% | Global, variable across FDA, CE Mark, NMPA | Long term (≥ 4 years) |

| Limited availability of skilled neurointerventional specialists | -0.5% | Global, most acute in emerging markets and rural areas | Long term (≥ 4 years) |

| High capital and procedure costs in resource-constrained settings | -0.6% | Low- and middle-income countries; community hospitals worldwide | Medium term (2-4 years) |

| Volatility in platinum and cobalt supply chains affecting device pricing | -0.3% | Global, with supply shocks impacting manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Multiregional Regulatory Approval Processes

Differing FDA, European, and NMPA requirements elongate time-to-market and inflate development costs. The EU Medical Device Regulation adds extra post-market obligations, while the FDA’s neuroendovascular surveillance mandates remain uneven. China’s updated Class III device rules require domestic clinical data and comprehensive quality systems, limiting acceptance of overseas trials. Novel AI-enabled and robotic devices face evolving frameworks that remain under development, delaying broad commercialization and tempering progress in the neurointerventional devices market.

Limited Availability of Skilled Neurointerventional Specialists

Training pathways produce relatively few specialists each year compared with growing demand. Rural areas and emerging economies struggle most with access. Medicare covers only 18-22% of thrombectomy costs, discouraging hospital investment in programs that attract and retain professionals. Multidisciplinary team requirements further constrain expansion in underserved settings, placing structural limits on near-term growth for the neurointerventional devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Mechanical Thrombectomy Drives Innovation

Aneurysm coiling and embolization devices sustained leadership with 37.68% share in 2025. Flow-diverter stents such as Pipeline Vantage reached 81.7% six-month occlusion while liquid embolics like Artisse recorded 96.6% implantation success. Mechanical thrombectomy, though smaller, is the fastest rising category at 6.42% CAGR. The neurointerventional devices market size for mechanical thrombectomy is projected to expand sharply as milli-spinner systems exceed 90% removal success on fibrin-rich clots. FreeClimb 88 aspiration catheters delivered 67.9% first-pass recanalization without complications, reinforcing clinician confidence. Expanded indications into large infarcts and distal occlusions broaden its addressable base, lifting the neurointerventional devices market.

Competitive traction continues as manufacturers bundle next-generation catheters with AI-guided imaging. Such integrated solutions drive premium adoption because they shorten procedure times and lower complication rates. Clinical evidence supporting mechanical thrombectomy across previously excluded populations encourages procurement committees to allocate higher budgets, thereby sustaining the neurointerventional devices market share of this product class.

By Application: Ischemic Stroke Dominance Accelerates

Ischemic stroke represented 50.05% of 2025 revenue and leads growth at 6.9% CAGR. High prevalence explains volume strength, while endovascular therapy’s proven superiority over medical management fuels value. Tenecteplase approval brings a faster thrombolytic option that pairs well with thrombectomy workflows. Flow diverters and intrasaccular devices widen cerebral aneurysm care, yet stroke keeps commanding the neurointerventional devices market size due to sheer caseload.

Emerging applications in medium vessel occlusions will further energize future sales. Early evidence in distal territories encourages specialized catheter design. Meanwhile, arteriovenous malformation treatments benefit from radiopaque liquid embolics reaching 99% effectiveness. Collectively these advances secure ischemic stroke’s status as the principal revenue pillar of the neurointerventional devices market.

By End User: Ambulatory Centers Gain Momentum

Tertiary hospitals captured 70.62% share in 2025 through comprehensive stroke centers and 24-hour capability. Specialized neuroscience institutes add niche demand supported by advanced imaging. However, ambulatory surgical and cath-lab centers show the highest 7.12% CAGR as outpatient models gain payer support and device profiles slim down. Supply-cost bundling in stroke care delivers average savings of USD 2,900.93 per case, a compelling economic lever for payers.

Medicare coverage expansion for carotid stenting raises outpatient volumes, although reimbursement gaps persist. Manufacturers respond by designing low-profile systems compatible with standard cath-lab infrastructure, enabling more procedures outside tertiary settings and broadening the neurointerventional devices market.

Geography Analysis

North America held 40.12% of revenue in 2025 owing to advanced infrastructure, abundant clinical trials, and early product launches. FDA clearances for Terumo Neuro’s dual-layer carotid stent and Crossroads’ balloon guide catheter refreshed growth pipelines. The region faces pressure from Medicare undervaluations that cover just one fifth of thrombectomy cost, challenging hospital economics. Strategic acquisitions such as Stryker buying Inari for USD 4.9 billion add breadth to portfolios, keeping the neurointerventional devices market competitive.

Asia-Pacific is the fastest growing at 5.28% CAGR. China’s NMPA approved 12,213 medical device applications in 2023, a 25.4% rise that signals regulatory openness. Broader insurance and capacity investments boost procedure penetration, though skill shortages and country-specific rules persist. Japan’s structured surveillance for flow diverters emphasizes safety and fosters confidence. Collectively, modernization and demographic aging drive strong upside for the neurointerventional devices market in the region.

Europe shows steady advancement supported by Medical Device Regulation alignment and strong clinical research. Market players introduced Cerenovus’s CEREGLIDE 71 and Penumbra’s neuro access suite, underscoring ongoing innovation. Still, reimbursement varies across member states, leading companies to sequence launches strategically. Strength of value-based care programs underscores the importance of long-term outcome data for sustaining neurointerventional devices market penetration.

Regulatory Landscape

Regulatory requirements for neurointerventional devices continue to diverge by region across the United States (FDA), Europe (EU MDR), and China (NMPA), which results in staggered evidence and quality-system obligations for Class III, high-risk implantables and thrombectomy systems. In the United States, the FDA moved device manufacturers toward closer alignment with ISO 13485 through the Quality Management System Regulation (QMSR), with an effective date in February 2026, while PMA lifecycle updates remain active for neurovascular platforms such as Pipeline Flex and Pipeline Vantage via FDA PMA supplements (e.g., P100018/S052 decision dated Feb 20, 2026).

In Europe, MDR transition and Notified Body capacity continue to shape commercialization sequencing. The European Commission adopted Commission Implementing Regulation (EU) 2026/977 in May 2026 to standardize Notified Body expectations, timelines, and re-certification practices, while MDR compliance requirements tighten around high-risk implantables with dated transition milestones. In China, NMPA is updating registration and clinical-evaluation guidance for Class III devices through the 2026 Medical Device Guidelines Revisions Plan (April 2026) and new clinical evaluation guidelines for Class III devices, alongside a new medical device GMP taking effect in November 2026, raising the bar for renewals and post-market compliance for both imported and domestic neurointerventional portfolios.

Competitive Landscape

The neurointerventional devices market exhibits moderate consolidation as top firms pursue technology differentiation and acquisition. Medtronic, Stryker, Johnson & Johnson, and Penumbra anchor global portfolios. Stryker’s USD 4.9 billion acquisition of Inari broadens thrombectomy into peripheral vascular, creating synergy with its neuro lines. Johnson & Johnson’s exploration to sell Cerenovus for about USD 1 billion may unlock opportunity for agile entrants.

Start-ups like Imperative Care and Route 92 target mechanical thrombectomy with focused innovation. FDA clearances for Crossroads Neurovascular, Perfuze, and CereVasc add fresh competition and expand treatment niches. Technology races center on AI integration, robotics, and advanced materials that improve deliverability and occlusion rates, sustaining high R&D intensity within the neurointerventional devices market.

Regional consolidation pairs with portfolio pruning as firms prioritize high-margin segments. Those with comprehensive vascular platforms, from brain to peripheral, leverage cross-selling and hospital contracting power. This dynamic sustains healthy rivalry yet presents high entry barriers, shaping the neurointerventional devices market’s medium-term trajectory.

Neurointerventional Devices Industry Leaders

Stryker

Penumbra, Inc.

Medtronic

Abbott

Johnson & Johnson (Cerenovus)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunity is expanding around complete stroke-procedure workflows as device makers build stronger positions in access plus therapy rather than selling isolated tools. Medtronic completed its USD 550 million acquisition of Scientia Vascular in June 2026, adding guidewires and catheter access products to complement therapeutic neurovascular offerings, which supports broader contracting with comprehensive stroke centers and enables more standardized kit-based procurement.

A key focus is differentiated aspiration and computer-assisted thrombectomy platforms that simplify technique and target harder-to-treat anatomies and distal occlusions. Penumbra received FDA clearance in June 2026 for THUNDERBOLT, a computer-assisted vacuum thrombectomy (CAVT) system for acute ischemic stroke, and moved clinical evidence generation forward by initiating the Forward study in July 2026 for distal acute ischemic stroke. In parallel, Perfuze received FDA 510(k) clearance in March 2026 for its Millipede88 aspiration catheter for standalone direct aspiration. Beyond core ischemic stroke, product innovation is also broadening into niche neurovascular indications supported by regulatory pathways, including FDA HDE approval in March 2026 for Serenity Medicals River stent for severe refractory idiopathic intracranial hypertension, indicating room for specialized devices with focused clinical value propositions.

Recent Industry Developments

- July 2026: Penumbra initiated the Forward study, an international prospective clinical trial evaluating mechanical thrombectomy and its computer-assisted vacuum thrombectomy (CAVT) approach for distal acute ischemic stroke. The program strengthens clinical evidence generation for distal-territory intervention and supports broader adoption discussions with hospitals and payers as treatment moves beyond large-vessel occlusions.

- June 2026: Medtronic completed its USD 550 million acquisition of Scientia Vascular, adding neurovascular access products such as guidewires and catheters to its portfolio. The deal deepens Medtronic end-to-end procedural coverage from access to therapy, sharpening its ability to compete for integrated neurointerventional supply contracts.

- June 2026: Penumbra received US FDA clearance for THUNDERBOLT, a computer-assisted vacuum thrombectomy (CAVT) device for acute ischemic stroke, and also secured a CE Mark in Europe for the same platform. Dual-region clearances expand commercialization reach and raise competitive pressure on conventional thrombectomy approaches by introducing a technology-differentiated, aspiration-driven system.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from devices used in minimally invasive, catheter-based neurovascular procedures to treat conditions such as stroke and intracranial aneurysms, across hospitals and specialized neuro centers. The sizing is built in value terms at the point of sale into the healthcare delivery setting.

Scope exclusions: Non-neurovascular CNS devices and general neurosurgery tools that are not used for endovascular neurointerventions are excluded.

Segmentation Overview

- By Product

- Aneurysm Coiling & Embolization Devices

- Flow-Diverter Stents

- Cerebral Balloon Angioplasty & Stenting Systems

- Mechanical Thrombectomy Devices

- Liquid Embolics & Intrasaccular Implants

- By Application

- Ischemic Stroke

- Cerebral Aneurysm

- Arteriovenous Malformations/Fistulas

- Intracerebral Hemorrhage

- By End User

- Tertiary Care Hospitals

- Specialized Neuroscience Centers

- Ambulatory Surgical & Cath-Lab Centers

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with public sources that help map procedure volumes, disease burden, and policy signals that can affect adoption. We use the World Health Organization for stroke burden context, the US CDC for related risk factor trends, and the OECD for comparable health system indicators across major economies.

We also scan regulatory and safety disclosures and medical literature to understand which device categories are being used, and how practice patterns are shifting. Illustrative sources include the US FDA device databases, Europe focused regulatory notices, peer reviewed journals indexed on PubMed, and websites of stroke and neurointerventional societies. Company annual reports, investor presentations, and reputable press releases are used to cross-check product mix, regional exposure, and pricing commentary, and a paid subscription for company financials and patent databases is used selectively where public disclosures are thin. These sources are not exhaustive, and many other public documents were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work is used to pressure test the demand pool and pricing logic with people who see the market daily, including hospital procurement teams, neurointerventional clinicians, distributors, and product managers. Since this is a global market, inputs are checked across APAC, EMEA, and the Americas so regional reimbursement patterns, site of care shifts, and stroke pathway maturity are reflected in the final assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 14% | APAC: 47% |

| Mid tier: 47% | Functional/Unit leaders: 41% | EMEA: 31% |

| Smaller Players: 17% | Managers: 45% | Americas: 22% |

Market-Sizing & Forecasting

The core model uses a top-down approach where disease prevalence and treated cohort logic are translated into likely procedure volumes, then converted into value using device mix and average selling price ranges. To keep the totals realistic, we corroborate results with selective bottom-up checks such as sampled ASP times volume for key device groups, plus channel discussions on unit throughput in major care centers.

Model inputs include ischemic stroke incidence and thrombectomy eligibility rates, intracranial aneurysm treatment rates, average devices used per procedure (for example, coils, stents, and adjunct catheters), mix shifts toward thrombectomy and flow diversion, and pricing movement driven by tendering and new product introductions. When certain countries have limited public data, we use proxy indicators such as neurointerventional center counts, specialist density, and import patterns, then adjust using primary feedback so the gap handling remains consistent.

For forecasting, scenario analysis is applied around a base case informed by expert consensus on factors such as expanding thrombectomy windows, guideline updates, and reimbursement stability. Scenarios are translated into yearly growth paths, then checked for reasonableness against procedure growth trends and expected pricing changes.

Data Validation & Update Cycle

Validation is done through multiple checks so unusual jumps are caught early and assumptions can be corrected before final sign off. We compare modeled totals against independent signals such as procedure trend direction, hospital budget cycles for high value consumables, and regional adoption patterns, then investigate large variances at the country and device group level.

An internal multi step review is followed, and re-contacts are triggered when a key assumption changes, such as a reimbursement update, a safety alert, or a sudden shift in procedure volumes. The report is refreshed annually, and interim updates are made when material events occur. Before delivery, a fresh pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Neurointerventional Devices Market Size Measured Against Other Published Estimates

Published market sizes for neurointerventional devices often differ because each publisher selects a device list, a pricing basis, and a base year, then applies different growth assumptions. Differences also show up depending on whether one source follows a procedure-driven view while another relies more on broad device shipment narratives.

Some estimates include wider neurovascular device groupings or use earlier base years with faster uptake curves for thrombectomy and flow diversion. In Mordor Intelligence, the sizing stays within neurointerventional device categories tied to endovascular neuro procedures, and non-neurovascular CNS devices are not counted, which changes the total even before forecasting choices are applied.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.84 B (2026) | |

| Global Consultancy A | USD 3.00 B (2023) | Uses an earlier base year and applies a higher growth path into 2031, and the disclosed scope language is broad enough that adjacent neurovascular device categories can be captured alongside core neurointerventional products. |

| Industry Research Desk B | USD 2.10 B (2024) | Starts from a narrower 2024 value and appears to rely more on macro growth assumptions, with limited detail on device mix, ASP progression, and country level validation steps, which can pull the total down. |

The spread in the table is mainly explained by scope choices and by how base year procedure momentum and pricing are carried forward into the forecast years. By tying demand to treated cohorts, device use per procedure, and practical price ranges, the model stays traceable to inputs that can be checked and repeated.

Key Questions Answered in the Report

Which products dominate global sales of neurointerventional devices?

Aneurysm coiling and embolization devices led with 37.68% share in 2025, reflecting mature clinical acceptance.

How fast is mechanical thrombectomy growing?

Mechanical thrombectomy revenue is rising at a 6.42% CAGR from 2026-2031, making it the fastest-advancing product class.

What region expands the market most rapidly?

Asia-Pacific is the quickest-growing geography with a 5.28% CAGR, encouraged by regulatory reforms and broader healthcare access.

Where do most procedures take place today?

Tertiary care hospitals performed 70.62% of interventions in 2025 due to comprehensive stroke capabilities.

What are the key restraints limiting growth?

Prolonged multiregional regulatory approval timelines and a global shortage of trained neurointerventionalists temper expansion.

Which recent FDA approval is most significant?

Tenecteplase approval in March 2025 offers the first new thrombolytic option for acute ischemic stroke in 30 years, streamlining workflows.

What is the current global market size for neurointerventional devices?

The market is valued at USD 2.84 billion in 2026 and is projected to reach USD 3.55 billion by 2031.

Page last updated on: