Brain Implants Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

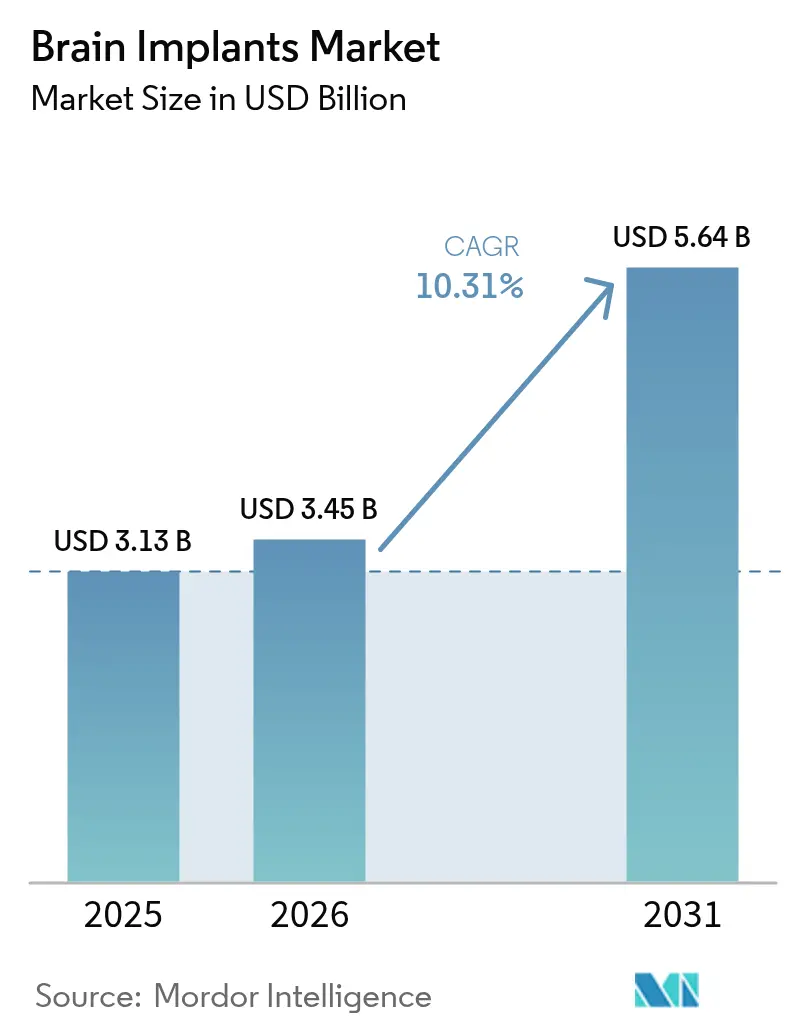

| Market Size (2026) | USD 3.45 Billion |

| Market Size (2031) | USD 5.64 Billion |

| Growth Rate (2026 - 2031) | 10.31% CAGR |

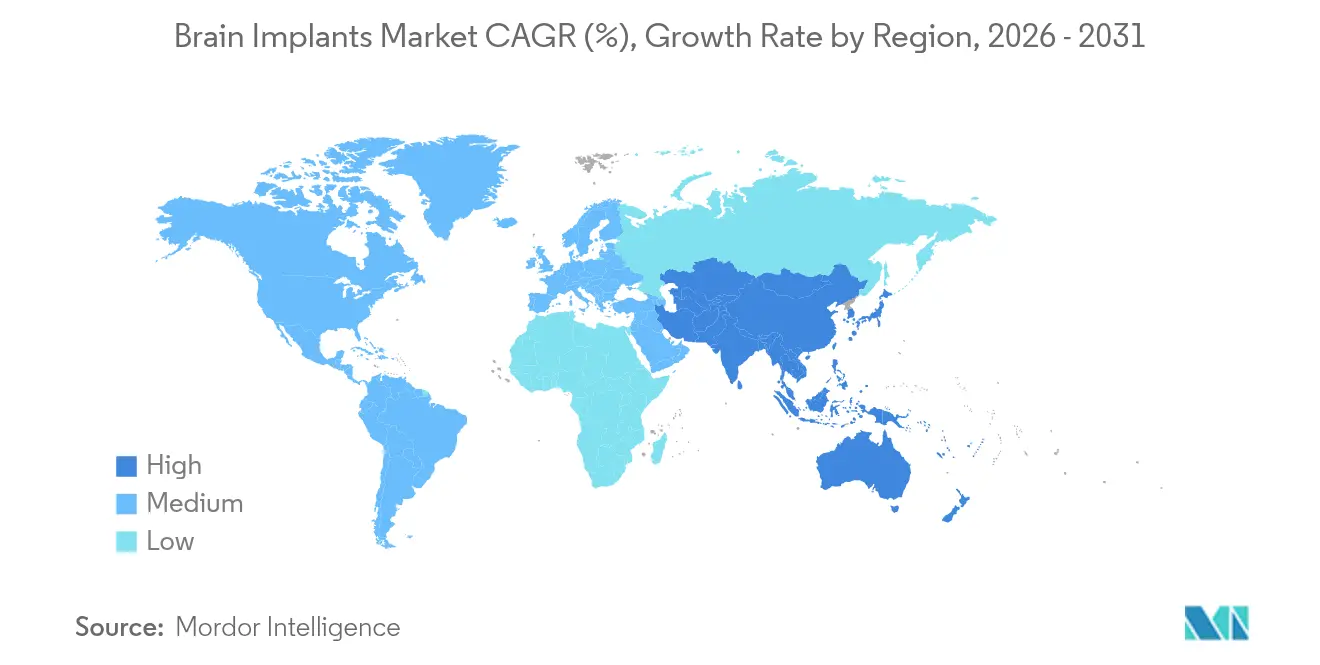

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brain Implants Market Analysis by Mordor Intelligence

The brain implants market size was valued at USD 3.13 billion in 2025 and estimated to grow from USD 3.45 billion in 2026 to reach USD 5.64 billion by 2031, at a CAGR of 10.31% during the forecast period (2026-2031). Broader payer acceptance, sensor miniaturization, and AI-enabled closed-loop systems are collectively redefining neuro-intervention strategies, creating new avenues for deep brain stimulation (DBS), vagus nerve stimulation (VNS), and emerging brain-computer interface (BCI) solutions. Players are aggressively integrating graphene electrodes and biocompatible coatings to extend device longevity, while flexible microelectrode arrays reduce tissue trauma and accelerate post-operative recovery. Venture capital inflows—led by nine-figure rounds such as Blackrock Neurotech’s USD 200 million raise—validate commercial readiness across several therapeutic categories.[1]FinSMEs, “Blackrock Neurotech Raises USD 200M,” finsmes.comMeanwhile, FDA Breakthrough Device and EU MDR fast-track pathways continue to compress approval timelines for next-generation neural technologies and cement North America’s leadership position even as Asia-Pacific accelerates system-wide adoption.

Key Report Takeaways

- By product type, deep brain stimulators led with 42.10% of brain implants market share in 2025, whereas vagus nerve stimulators are advancing at 11.22% CAGR through 2031.

- By technology, invasive surgical approaches captured 70.85% share of the brain implants market in 2025; minimally-invasive percutaneous methods record the quickest growth at 11.74% CAGR.

- By application, chronic pain accounted for 32.40% share of the brain implants market size in 2025, while Parkinson’s disease therapy is forecast to expand at 11.29% CAGR to 2031.

- By end user, hospitals and neurosurgical centers held 58.10% share in 2025; ambulatory surgical centers exhibit the highest projected 11.95% CAGR.

- By geography, North America retained 52.70% share of the brain implants market in 2025, yet Asia-Pacific is set to post a 12.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Brain Implants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of neuro-degenerative & movement disorders | +2.3% | Global; concentrated in North America, Europe, Japan | Long term (≥ 4 years) |

| Miniaturization & closed-loop technology advances | +1.8% | North America & EU; rapid uptake in Asia-Pacific | Medium term (2-4 years) |

| Favorable reimbursement expansion in U.S./EU | +1.2% | North America & EU; spillover to select Asia-Pacific markets | Medium term (2-4 years) |

| AI-driven adaptive stimulation algorithms | +0.9% | Early adoption in developed markets worldwide | Short term (≤ 2 years) |

| FDA Breakthrough & EU MDR fast-track pathways | +0.7% | North America & EU; shaping global standards | Short term (≤ 2 years) |

| Surge in neurotech mega-funding & VC activity | +0.6% | Global; investment hubs in North America & Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Neuro-degenerative & Movement Disorders

Global Parkinson’s disease cases are on track to hit 25.2 million by 2050, doubling today’s burden and widening the pool of DBS candidates. Drug-resistant epilepsy already affects 10.1 million people who remain eligible for surgical intervention, while treatment-resistant depression continues to drive psychiatric device adoption. Aging demographics in developed markets and improved diagnostic resources in emerging economies combine to ensure consistent procedure volumes. Health-economic studies showed 2024 DBS procedures saving USD 20,000–35,000 per patient annually in medication costs, keeping total expenditures below commonly accepted cost-effectiveness thresholds.

Miniaturization & Closed-loop Technology Advances

Graphene electrodes and nanoporous metals have shrunk implant footprints by up to 70%, improving signal fidelity and lowering post-surgical inflammation. Batteries now last longer thanks to neuromorphic processors that cut power draw, with rechargeable platforms such as Abbott’s Infinity DBS allowing smartphone-based parameter updates.[2]Source: Abbott Laboratories, “Infinity DBS System Product Brief,” abbott.com On-device machine-learning firmware adjusts stimulation in real time, moving therapy from static settings to dynamic, patient-specific protocols. These advances collectively accelerate outpatient recovery, lift long-term efficacy, and fuel wider physician acceptance.

Favorable Reimbursement Expansion in U.S./EU

Medicare broadened DBS coverage to include essential tremor and dystonia, adding specific billing codes that streamline claims processing. European HTA bodies now apply value-based frameworks that capture lifetime savings from reduced pharmacotherapy, spurring payer alignment in France, Germany, and the United Kingdom. Pilot schemes evaluating depression-related neurostimulation coverage could unlock sizeable addressable populations once finalised, reinforcing revenue predictability for device makers and hospitals alike.

AI-driven Adaptive Stimulation Algorithms

Synchron’s BCI integrates large-language models to translate neural intent into external device commands for patients with severe mobility loss. Real-time analytics refine pulse width, amplitude, and frequency based on intra-cortical feedback, diminishing manual programming visits. Emerging foundation models for neural signal decoding promise standardised calibration across diverse patient anatomies, which may lower training time and broaden clinician adoption. On-board encryption simultaneously mitigates privacy risks while enabling secure tele-programming.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device & surgical procedure cost | -1.1% | Global; pronounced in cost-sensitive and emerging health systems | Long term (≥ 4 years) |

| Limited long-term clinical evidence in some indications | -0.7% | Worldwide; greater scrutiny in evidence-driven markets | Medium term (2-4 years) |

| Cybersecurity & data-privacy concerns | -0.6% | Global; heightened focus in EU and privacy-centric Asia-Pacific states | Medium term (2-4 years) |

| Scarcity of specialist neurosurgeons | -0.8% | Emerging regions, notably Southeast Asia, Africa, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Device & Surgical Procedure Cost

A full DBS episode, including hardware, surgery, and year-one programming, ranges from USD 140,000 to 190,000, with follow-up maintenance at USD 4,500–7,800 per year. In many emerging countries these fees outstrip annual household income, curbing penetration. Value-based contracting between providers and manufacturers is evolving, yet remains confined to a handful of high-income settings, prolonging the affordability gap.

Cybersecurity & Data-privacy Concerns

Wireless interfaces built on Bluetooth LE and Wi-Fi simplify remote programming but present “brainjacking” risks if left unsecured. New FDA guidance mandates encrypted communication and multi-factor authentication for neural devices, adding design complexity and cost. The EU’s GDPR introduces strict consent and data portability rules, compelling manufacturers to embed compliance features early in the product lifecycle.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Deep Brain Stimulators Sustain Leadership amid Rapid VNS Upside

Deep brain stimulators held a commanding 42.10% of brain implants market share in 2025, anchored by three-decade clinical evidence for Parkinson’s, essential tremor, and dystonia. More than 160,000 implants have been placed worldwide, giving the modality unrivalled procedural familiarity among surgeons and payers. Global growth remains healthy as new indications such as obsessive-compulsive disorder move past pivotal trials. Meanwhile, spinal cord stimulators maintain solid volumes across chronic pain and diabetic neuropathy cases, further diversifying revenue streams for incumbents.

Vagus nerve stimulators represent the fastest-moving opportunity, charting an 11.22% CAGR through 2031. Multipronged utility in drug-resistant epilepsy, treatment-resistant depression, and inflammatory disorders boosts cross-specialty adoption. Technology front-runners are miniaturising pulse generators and improving lead durability, allowing shorter operating times and fewer revision surgeries. Overall, the brain implants market remains product-innovation led, with closed-loop DBS systems and seizure-responsive neurostimulators expanding use cases while supporting stable ASPs.

By Technology: Invasive Procedures Dominate, Yet Minimally-Invasive Techniques Accelerate

Invasive stereotactic surgery continues to account for a 70.85% foothold within the brain implants market in 2025 thanks to precise electrode positioning and well-reimbursed care pathways. Meta-analyses covering 2025 cohorts document cerebrovascular events at 2.71%, permanent impairment at 1.0%, and mortality at 0.4%, numbers that reassure surgeons and regulators alike. Concurrent adoption of robot-assisted navigation and 3-Tesla MRI guidance keeps complication rates on a downward trajectory.

Yet, minimally-invasive approaches such as Synchron’s endovascular Stentrode are gaining momentum with a forecast 11.74% CAGR. Implantation via the jugular vein eliminates craniotomy, cuts procedure time, and may allow expansion into ambulatory surgical centers. Flexible polymer leads coated with anti-inflammatory agents reduce foreign-body responses, while single-access delivery lowers infection risks. As these less-invasive strategies mature, they broaden candidate pools and speed geographic roll-outs, propelling incremental volume growth.

By Application: Chronic Pain Leads, Parkinson’s Therapy Posts Fastest Expansion

Chronic pain accounts for 32.40% of total procedures, buoyed by robust evidence supporting spinal cord stimulation for failed back surgery syndrome and complex regional pain syndrome. FDA approvals for diabetic neuropathy have opened new referral channels, pushing utilisation in pain clinics and integrated health networks.

Parkinson’s disease treatment is the fastest-rising segment with an 11.29% CAGR. Earlier intervention protocols, refined targeting of the subthalamic nucleus, and cost-effectiveness ratios below USD 50,000 per quality-adjusted life year sustain payers’ confidence. Epilepsy maintains steady volumes as responsive neurostimulation devices demonstrate durable seizure reduction over nine-year follow-up, while psychiatric uses—led by depression—edge closer to commercial inflection as pivotal trials mature.

By End User: Hospitals Continue to Dominate while Ambulatory Centers Gain Ground

Hospitals and neurosurgical centers controlled 58.10% of 2025 procedure volume, reflecting the infrastructure needs of stereotactic operations and postoperative care. Mature reimbursement frameworks encourage inpatient billing, and multi-disciplinary teams simplify peri-operative management.

Ambulatory surgical centers log the highest 11.95% CAGR, particularly in the United States, where payers incentivise lower-cost settings and minimally-invasive devices shorten observation periods. Community-based movement-disorder clinics are increasingly equipped to handle programming and battery maintenance, further redistributing long-term follow-up from tertiary hospitals to outpatient environments.

Geography Analysis

North America retains primacy, contributing 52.70% of global revenue, anchored by FDA fast-track pathways, deep capital pools, and entrenched reimbursement coverage for multiple indications. U.S. hospitals also benefit from a dense concentration of fellowship-trained functional neurosurgeons and a flourishing start-up ecosystem led by Neuralink, Precision Neuroscience, and Synchron. Canada amplifies regional totals through universal health insurance that recognises DBS as medically necessary for Parkinson’s and essential tremor.

Europe follows closely, underpinned by coordinated HTA processes and EU MDR accelerated review tracks that expedite innovative implants. Germany, France, and the United Kingdom collectively host scores of DBS centers of excellence and continue to pilot large-scale VNS and RNS reimbursements. Nordic countries leverage digital health frameworks to support remote DBS programming, demonstrating efficient long-distance care models.

Asia-Pacific emerges as the most dynamic corridor with a 12.11% CAGR outlook. China invests heavily in neuroscience R&D and high-end device manufacturing, narrowing technology gaps with Western peers. Japan’s aging population fuels strong demand for movement-disorder solutions, while the nation’s universal insurance simplifies patient uptake. India, South Korea, and Australia round out regional growth by combining public-private partnerships with leading academic research to spur clinical trial throughput. The Middle East & Africa and South America remain nascent yet promising. GCC states back flagship neurosurgical hubs as part of national health-innovation agendas, while Brazil and Argentina push forward targeted reimbursement pilots despite macroeconomic volatility. Long-term upside hinges on scaling specialist training, stabilizing currency risk, and expanding tele-programming infrastructure in rural locales.

Competitive Landscape

Market structure is moderately concentrated. The top three—Medtronic, Abbott, and Boston Scientific—maintain leadership by pairing diversified neurostimulation portfolios with entrenched surgeon relationships developed over decades. Each invests in AI-enabled closed-loop algorithms, rechargeable power platforms, and smartphone integration to refresh installed bases without resorting to aggressive price cuts.

Disruptors such as Synchron, Blackrock Neurotech, and Precision Neuroscience attack legacy surgical models with less-invasive BCIs that promise shorter procedure times and expanded outpatient adoption. Synchron’s jugular-vein Stentrode has advanced into pivotal U.S. trials under Breakthrough Device status, while Blackrock’s precision micro-array aims to restore motor function in paralysis patients. Heavy venture backing fuels aggressive clinical timelines and rapid manufacturing scale-up, intensifying competition for neurologists’ mindshare.

Collaborations between device firms and cloud-AI leaders (e.g., Synchron-NVIDIA’s Chiral model) demonstrate an ecosystem pivot toward software-defined therapy differentiation.[3]Pharmaphorum, “Synchron-NVIDIA Reveal Chiral Model,” pharmaphorum.com Incumbents answer by acquiring algorithm-rich start-ups or co-developing analytics suites that generate automated programming recommendations. Overall, proprietary data-science capabilities now weigh as heavily as hardware reliability in hospital tenders, reshaping competitive dynamics across the brain implants market.

Brain Implants Industry Leaders

Boston Scientific Corporation

Renishaw PLC

Medtronic

Abbott

LivaNova Plc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Synchron and NVIDIA unveiled the Chiral AI model at GTC 2025, enabling ALS patients to control external devices via thought commands.

- July 2024: Synchron integrated its BCI with Apple’s Vision Pro headset to allow hands-free mixed-reality navigation for mobility-impaired users.

- April 2024: Blackrock Neurotech secured USD 200 million from Tether to fund the commercialization of precision electrode arrays for paralysis and neurological disorders.

- March 2024: Leading implant developers formed a dedicated industry consortium to harmonize standards and accelerate neurotech adoption.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the brain implants market as the global revenue earned from fully implantable neuro-stimulation or neural-signal recording devices, including deep brain stimulators, spinal cord stimulators, vagus nerve stimulators, responsive neuro-stimulators, and emerging cortical interface chips, that are surgically placed inside the cranium or along the spinal neural axis to deliver therapeutic impulses or decode neural activity for clinical use. The value captured covers factory-new pulse generators, implantable leads, and power modules.

Scope Exclusion: We exclude external stimulators, wearable EEG headsets, refurbishment services, and implants intended solely for orthopedic or cardiac therapy.

Segmentation Overview

- By Product Type

- Deep Brain Stimulators

- Spinal Cord Stimulators

- Vagus Nerve Stimulators

- By Technology

- Invasive (Surgical)

- Minimally-Invasive / Percutaneous

- Non-invasive (Trans-cranial)

- By Application

- Parkinson’s Disease

- Chronic Pain

- Epilepsy

- Depression & Psychiatric Disorders

- Essential Tremor

- Other Applications

- By End User

- Hospitals & Neurosurgical Centers

- Specialty Clinics

- Ambulatory Surgical Centers

- Academic & Research Institutes

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of APAC

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed neurosurgeons, hospital procurement leads, and engineering directors across North America, Europe, China, and Japan. The conversations refined average selling prices, penetration ceilings, and the early adoption curve for closed-loop stimulators.

Desk Research

We began with epidemiology datasets from the World Health Organization, the Global Burden of Disease study, and the International Parkinson and Movement Disorder Society to size patient pools. Device clearance registers of the US FDA and EU MDR, procedure tariffs held by the Centers for Medicare & Medicaid Services, and customs records accessed through Dow Jones Factiva anchored unit flows and export prices. Annual reports and 10-Ks of leading suppliers revealed product mix insights, while PubMed literature and International Neuromodulation Society briefs clarified revision rates and device lifecycles. These sources are illustrative; many additional public and subscription databases informed our desk analysis.

Market-Sizing & Forecasting

We run a top-down prevalence-to-treated-patient build that converts Parkinson's, epilepsy, chronic pain, and depression cohorts into procedure counts. We then apply regional ASPs. Supplier roll-ups from sample hospitals provide a bottom-up check, and we cross-validate totals. Key variables include diagnosed incidence, device penetration, replacement interval, regulatory pipeline, and reimbursement wins. An ARIMA-assisted multivariate regression projects value through 2030.

Data Validation & Update Cycle

Our outputs pass peer review, variance screens against shipment summaries, and senior sign-off. Models refresh annually, with interim updates triggered by recalls, pivotal trials, or major payer decisions.

Why Our Brain Implants Baseline Commands Reliability

Published estimates differ because firms choose distinct device sets, price bases, and update cadences.

By restricting scope to wholly implantable neuro-stimulators and applying uniform 2024 ASP resets, Mordor delivers a steady, decision-ready baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.13 B | Mordor Intelligence | - |

| USD 6.97 B | Global Consultancy A | Includes wearables and list prices without regional discounting |

| USD 2.36 B | Industry Journal B | Uses hospital charge data from five countries only, limited expert validation |

The comparison shows that our disciplined scope selection and yearly recalibration give stakeholders a transparent baseline they can trace to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current brain implants market size?

The brain implants market size is USD 3.45 billion in 2026 and is set to reach USD 5.64 billion by 2031.

Which product segment leads the market?

Deep brain stimulators command the largest 42.10% share due to strong clinical evidence across movement disorders.

Which geographic region is growing the fastest?

Asia-Pacific shows the quickest expansion at a projected 12.11% CAGR through 2031, fueled by infrastructure upgrades and regulatory harmonisation.

What technological trend is reshaping therapy delivery?

AI-enabled closed-loop systems that dynamically adjust stimulation parameters in real time are transforming treatment precision.

Page last updated on: