Sacral Nerve Stimulation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.81 Billion |

| Market Size (2031) | USD 2.94 Billion |

| Growth Rate (2026 - 2031) | 10.18% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sacral Nerve Stimulation Market Analysis by Mordor Intelligence

The sacral nerve stimulation market size was valued at USD 1.64 billion in 2025 and estimated to grow from USD 1.81 billion in 2026 to reach USD 2.94 billion by 2031, at a CAGR of 10.18% during the forecast period (2026-2031). Device miniaturization, MRI-compatible circuitry, and closed-loop software are removing historic barriers to adoption, while favorable payer policies shorten the time from diagnosis to permanent implantation in key jurisdictions. Competitive intensity is rising as Boston Scientific, Medtronic, and a cohort of venture-backed entrants roll out fourth- and fifth-generation systems that promise longer battery life, streamlined recharging, and enhanced physiological feedback. Strategic interest is further amplified by the push to shift procedures into ambulatory settings, an approach that lowers facility costs and aligns with value-based care mandates in North America and Europe. At the same time, Asia-Pacific health ministries are widening market access through faster approvals and localized reimbursement, setting the stage for outsized regional demand over the next five years.

Key Report Takeaways

- By product type, implantable systems held 85.92% of the sacral nerve stimulation market share in 2025 and are forecast to expand at a 10.05% CAGR to 2031.

- By application, urge urinary incontinence accounted for 46.88% of the sacral nerve stimulation market size in 2025, while chronic anal fissure therapy is projected to post the fastest 11.38% CAGR through 2031.

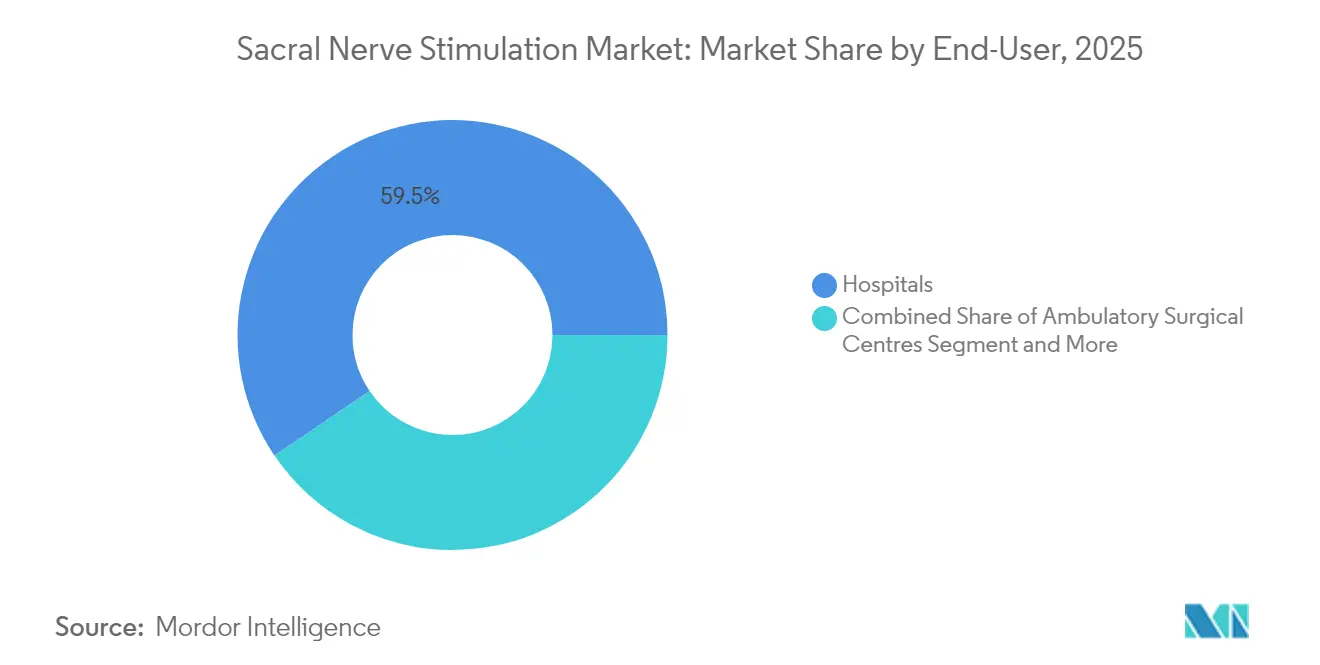

- By end-user, hospitals led with 59.47% revenue in 2025, whereas ambulatory surgical centers are on track for an 11.62% CAGR to 2031 as outpatient volumes climb.

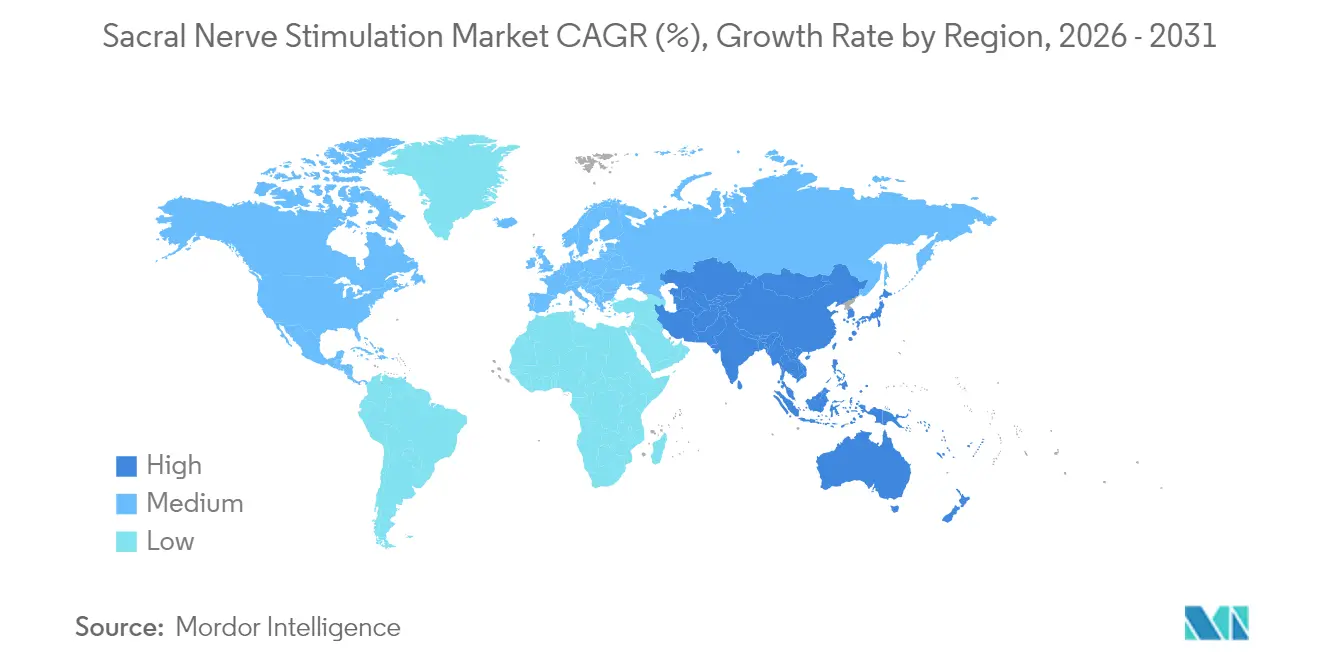

- By geography, North America contributed 45.58% of 2025 sales, yet Asia-Pacific is set to record the highest 12.29% CAGR across the forecast horizon owing to fresh approvals in Australia and Japan.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sacral Nerve Stimulation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of overactive bladder & urge/fecal incontinence | +2.8% | North America, Europe, APAC | Long term (≥ 4 years) |

| Favourable reimbursement & coverage expansions | +2.1% | North America, EU, expanding APAC | Medium term (2-4 years) |

| Miniaturised, MRI-compatible, rechargeable implant designs | +1.9% | Global, early adoption in developed markets | Short term (≤ 2 years) |

| AI-enabled closed-loop neuromodulation algorithms | +1.4% | North America, Europe | Medium term (2-4 years) |

| Growth of outpatient ASC-based implantation pathways | +1.2% | Primarily North America | Short term (≤ 2 years) |

| Adjacent tibial/genital nerve stimulation broadening patient pool | +0.9% | Global research in EU & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence Of Overactive Bladder & Urge/Fecal Incontinence

Global aging and rising obesity levels continue to enlarge the clinical pool of patients who do not respond to behavioral therapy or pharmacologics. National Health and Nutrition Examination Survey data show urinary incontinence symptoms in 61.8% of women, a marked uptick versus prior cycles[1]Ushma J. Patel et al., “Updated Prevalence of Urinary Incontinence in Women,” Female Pelvic Medicine & Reconstructive Surgery, lww.com. Overactive bladder affects 27.4% of mixed-gender cohorts according to recent cross-sectional studies, with nocturia singled out as the most disruptive symptom to daily living. As symptom burden rises, neuromodulation gains traction when first-line antimuscarinics or β3-agonists fail. Clinicians now position sacral nerve stimulation earlier in care algorithms, particularly for patients aiming to curb anticholinergic side effects. The mounting prevalence thus exerts a sustained pull on procedure volumes over the long term.

Favourable Reimbursement & Coverage Expansions

The U.S. Centers for Medicare & Medicaid Services introduced explicit HCPCS codes for both trial and permanent implants, narrowing administrative ambiguity and leveling payment across provider sites. The 2026 proposed ASC Covered Procedures List adds hundreds of codes that could further migrate volumes to lower-cost outpatient centers. Private payers are aligning, routinely covering permanent implants after ≥50% symptom improvement during the trial. Outside the United States, Australia’s Prostheses List and Japan’s accelerated review channels now reimburse next-generation rechargeable systems, an approach that trims patient out-of-pocket spends and accelerates hospital adoption. Collectively, these policies raise the accessible patient pool in both developed and emerging economies.

Miniaturised, MRI-Compatible, Rechargeable Implant Designs

Manufacturers have cut device mass below 8 g, enabling minimally invasive pocket creation and superior cosmetic profiles. Medtronic’s InterStim Micro weighs 7.3 g, incorporates SureScan coil architecture, and promises 15-year longevity under standard duty cycles[2]Medtronic, “InterStim Micro,” medtronic.com. Axonics’ F15 delivers a similar service life with 20% volume reduction and no recharge requirement, removing a common patient adherence barrier. Universal 3 T MRI-conditional labeling eliminates prior exclusions for imaging follow-up, expanding clinical eligibility. These specifications feed directly into surgeon preference, reduce explant rates tied to battery depletion, and strengthen the overall value proposition of sacral nerve stimulation market therapy.

AI-Enabled Closed-Loop Neuromodulation Algorithms

Closed-loop platforms sense ECAP signals and auto-adjust amplitude in real time, cutting overstimulation complaints by 93% in early use cohorts. U.S. guidelines released in 2025 spell out patient selection and programming protocols, providing the clinical scaffolding for wider uptake. European real-world registries echo this success, reporting 92% satisfaction and durable pain control at one year. As sacral applications borrow these algorithms from spinal cord stimulators, therapy becomes individualized, boosting responder rates and compressing trial-to-implant conversion timelines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Device-related adverse events & high revision rates | -1.8% | Global, higher impact in emerging markets | Short term (≤ 2 years) |

| High implant costs & limited surgeon training outside tier-1 centres | -1.5% | Global, especially rural regions | Long term (≥ 4 years) |

| Rising adoption of less-invasive tibial nerve stimulation alternatives | -1.2% | North America & EU | Medium term (2-4 years) |

| Escalating patent litigation & supply-chain disruption risks | -0.9% | Global manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Device-Related Adverse Events & High Revision Rates

Single-center audits of 155 implants documented 38.2% reoperation within five years, driven by lead migration, pain, and hardware failure. Multicenter colon-rectal cohorts noted 35.5% revision or explant despite preserved efficacy, pointing to durability rather than therapeutic failure issues. Australian regulator surveillance shows roughly 4 explants per 10 spinal cord stimulators annually, stoking clinician caution when counseling candidates. While next-generation hardware should trim mechanical failures, the near-term perception of high revision risk persists, dampening penetration in risk-averse markets.

High Implant Costs & Limited Surgeon Training Outside Tier-1 Centres

Total episode costs range USD 35,000–70,000, challenging healthcare budgets in developing economies and smaller U.S. payers. Fellowship seats in urogynecology and reconstructive pelvic surgery remain concentrated in major academic hubs, leaving rural patients with long travel times or no access. Digital and tele-proctoring initiatives are growing, yet many centers still lack the capital equipment or IT backbone to host them, prolonging the workforce gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Implantable Systems Drive Market Dominance

Implantable systems captured 85.92% of the sacral nerve stimulation market in 2025 on the back of superior efficacy and convenience over external options. This product class promises uninterrupted therapy for 10–15 years, eliminating compliance gaps that can erode outcomes in external trials. Rechargeable chemistries now deliver monthly charging routines of roughly 60 minutes, a compromise most patients accept when weighed against reoperations for battery replacement. Hospital procurement committees lean toward implantable platforms as they spread capital cost over extended life cycles, boosting return on investment.

External systems, though accounting for a modest slice of 2025 revenues, are logging a 12.44% CAGR and serve a critical role in patient screening. Smartphone-linked controllers and cloud dashboards enable clinicians to measure symptom logs remotely, refining candidate selection and cutting failed permanent implants. Regulatory bodies cemented this workflow by carving out dedicated reimbursement codes, giving payers an auditable pathway from diagnosis to trial to implant. In emerging markets where procedural budgets run tight, external devices also satisfy unmet need among patients unwilling or unable to fund full surgery.

By Application: Urge Incontinence Leads While Anal Fissure Shows Promise

Urge urinary incontinence held 46.88% of the sacral nerve stimulation market share in 2025, anchored by robust responder rates such as the 93% success observed in the ARTISAN-SNM pivotal trial. Urologists have thus formalized neuromodulation as a third-line therapy directly after pharmacologic failure. Mixed bowel and bladder subtypes further enlarge volume as clinicians recognize cross-organ benefits. At the other end, chronic anal fissure is advancing at an 11.38% CAGR as colorectal surgeons publish encouraging case series and leverage compassionate use pathways to secure implants for refractory patients.

Therapeutic breadth is widening alongside evidence in pelvic pain, interstitial cystitis, and pediatric constipation. Finnish investigators reported long-term pain score cuts from 7.4 to 2.3 in endometriosis cases, hinting at future label extensions. Randomized pediatric trials comparing invasive against non-invasive protocols are underway, a sign that clinicians are probing the lower age boundary for durable neuromodulation benefits. Each incremental indication raises the sacral nerve stimulation market size ceiling and bolsters utilization curves.

By End-User: Hospital Dominance Faces ASC Challenge

Hospitals contributed 59.47% to 2025 revenues owing to in-house imaging, anesthesia, and multidisciplinary clinics that simplify complex case work-up. Tertiary centers often bundle sacral implants with concomitant pelvic floor reconstructions or bowel surgeries, capturing synergies impossible in smaller venues. They also shoulder most revisions—an activity that preserves technical know-how yet elevates cost per case.

Ambulatory surgical centers, however, are gaining ground at an 11.62% CAGR thanks to lower overhead, rapid discharge, and payer steering. Many leading urologists now split surgical time between hospital and ASC sites, reserving low-risk implants for outpatient suites. Specialty continence clinics add further diversity, integrating nurse practitioners, physiotherapists, and telehealth consults to handle follow-up remotely. This multi-site ecosystem forces device vendors to craft training curricula that accommodate varying OR workflows and capital budgets, an evolution that differentiates commercial support packages.

Geography Analysis

North America retained 45.58% of 2025 sales, cemented by three decades of physician familiarity and a mature reimbursement backbone that pays for both trial and permanent stages. U.S. procedure growth now revolves around technology refresh cycles—clinics upgrading to MRI-safe, rechargeable, or closed-loop platforms—as opposed to expanding the naïve patient base. Canada mirrors these maturation dynamics but faces province-by-province funding variability that introduces waiting lists in less-populated regions. Mexico’s private hospital chains are piloting sacral nerve stimulation market offerings to capture inbound medical tourism, enriching the regional mix.

Europe combines broad statutory coverage with stringent Medical Device Regulation audits that elevate quality thresholds yet elongate filings. Germany and France are the volume anchors where high-density specialist centers coexist with aging demographics prone to incontinence. The United Kingdom is investing in community continence clinics aimed at earlier identification of candidates, potentially shifting initiation of neuromodulation further upstream in the care pathway.

Asia-Pacific is the growth pacesetter at 12.29% CAGR, fueled by Australia’s 2024 approval of Axonics’ fourth-generation system and Japan’s expedited review designations for breakthrough neuromodulation devices. Both countries pair regulatory agility with reimbursement, catalyzing procedure ramp-up. In China and India, private hospitals are opting for external trial systems first, a cost-savvy route that seeds future implant demand. Coupled with the region’s swift urbanization and expanding middle class healthcare budgets, these moves underpin long-run upside for the sacral nerve stimulation market.

Rest-of-world jurisdictions such as Latin America and the Middle East remain nascent but opportunistic. Select Gulf states fund implants for nationals traveling abroad, while flagship academic hospitals in Brazil and Saudi Arabia are enrolling in multinational closed-loop trials to leapfrog legacy technology. Overall, accelerating global diffusion combined with local reimbursement gains fortifies the international expansion narrative.

Competitive Landscape

The field shows moderate concentration, with the top two players accounting for significant revenue following Boston Scientific’s USD 3.7 billion takeover of Axonics. Medtronic defends incumbency through its InterStim franchise, newly refreshed with fifth-generation batteries and expanded MRI indications that appeal to an installed base exceeding 425,000 patients worldwide. The takeover grants Boston Scientific portfolio breadth across both rechargeable and recharge-free options, plus an entry to urology customers previously outside its neuromodulation scope.

Litigation remains a defining feature; Medtronic’s 2024 ITC complaint seeks to block alleged MRI-coil infringements, while Axonics (now Boston Scientific) counters with petitions against stimulator amplitude algorithms. This intellectual property crossfire raises switching costs for hospitals wary of adopting systems that might face import bans.

Innovation pipelines are robust. Neuspera won FDA approval in June 2025 for a battery-free platform that uses external inductive power, potentially erasing reoperation tied to battery depletion. Start-ups like Stimvia secured MDR certification for ultra-miniaturized modules intended for tibial placement, hinting at convergence between peripheral and sacral therapies. Incumbents answer by bundling remote monitoring portals, AI-driven programming, and surgeon education grants that nurture brand stickiness across the care continuum.

Lastly, horizontal deal activity is heating up in adjacent pain and spine markets—evidenced by Globus Medical’s agreement to buy Nevro—in a bid to amass broader neuromodulation toolkits and hedge product risk. The consolidation wave signals that scale and diversified IP matter more than ever as the sacral nerve stimulation market races toward next-generation closed-loop autonomy.

Sacral Nerve Stimulation Industry Leaders

Medtronic plc

Axonics Inc.

Nevro Corp.

Boston Scientific Corp.

Nuvectra Corp.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Reimbursement clarity and site-of-care shifts are creating near-term whitespace around outpatient delivery and newer device architectures. In the United States, CMS has been assigning explicit payment pathways for sacral neuromodulation procedures and devices, and in July 2026 CMS placed the Neuspera SNM system into APC 5464 in the proposed CY 2027 OPPS rule (proposed payment rate USD 22,150). This is a concrete sign that integrated, externally powered systems are being mapped into mainstream hospital outpatient payment mechanics. On the provider side, coding and payment guides from major manufacturers are being used to standardize billing workflows for trial-to-permanent pathways, supporting broader participation beyond flagship tertiary centers.

Technology-driven opportunity is concentrating in miniaturized, MRI-compatible platforms, external power delivery, and sensing-enabled programming that can reduce revisions and improve trial conversion. Neuspera Medical’s iSNM system, cleared by the U.S. FDA in June 2025 for urinary urge incontinence, uses a miniaturized implant powered by an external disc. That clearance opened a competitive lane alongside established rechargeable and recharge-free implantable systems. Ongoing clinical work such as Medtronics PEER 2 study (NCT05200923), updated as recently as March 2026 with an estimated completion in December 2026, points to continued investment in pelvic-health sensing and objective feedback approaches that can translate into differentiated programming, remote follow-up, and more repeatable outcomes across hospitals and ambulatory surgical centers.

Recent Industry Developments

- July 2026: CMS placed the Neuspera SNM system into APC 5464 in the proposed CY 2027 OPPS rule, outlining a defined hospital outpatient payment level for the technology. The proposal supports the reimbursement pathway for integrated, externally powered sacral neuromodulation systems and reduces financial ambiguity for hospitals evaluating adoption.

- May 2026: The US FDA approved a 30-day notice supplement for the Axonics Sacral Neuromodulation System (P190006), authorizing the use of additional alternate capacitors in production. This type of manufacturing change supports supply continuity and component resilience for a high-volume implantable platform following the brand's integration into Boston Scientific.

- June 2025: Neuspera Medical received US FDA approval for its integrated sacral neuromodulation (iSNM) system for urinary urge incontinence, using a miniaturized implant powered by an external disc. The clearance broadened the competitive set beyond conventional battery-based implants and highlighted a design direction focused on reducing long-term surgical burden related to battery replacement.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from sacral nerve stimulation therapy systems used to manage bladder and bowel control disorders, including implantable and external systems sold and used across major healthcare settings worldwide.

Scope exclusions: We exclude general pelvic floor therapies, drugs, and unrelated neuromodulation procedures that do not involve sacral nerve stimulation systems.

Segmentation Overview

- By Product Type

- External Sacral Nerve Stimulation Systems

- Implantable Sacral Nerve Stimulation Systems

- By Application

- Urge Urinary Incontinence

- Urinary & Fecal Incontinence (Mixed)

- Chronic Anal Fissure

- Other Neuromodulation-responsive Disorders

- By End-User

- Hospitals

- Ambulatory Surgical Centres

- Specialty Continence Clinics

- Others

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the patient and procedure context, then mapping it to device adoption and pricing. We used public sources to understand disease burden, care pathways, and clinical usage patterns, including CDC data, NIH and PubMed articles, FDA device databases, CMS coverage and payment references, and OECD health statistics. These inputs help set practical ranges for eligible patients, implant rates, and how quickly newer features (for example, MRI compatibility) can change adoption.

We also reviewed company filings and investor materials, conference abstracts, and hospital system publications to cross-check therapy volume assumptions and replacement cycles. Where helpful, paid subscriptions were used for company financials and intelligence, news and financials, and patent databases to confirm product refresh timing and portfolio breadth. The desk sources listed here are illustrative, and additional sources were consulted during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs were collected through expert conversations and structured surveys with clinicians involved in implantation, hospital and ASC procurement staff, and industry participants supporting distribution and service. For this global market, we covered the Americas, EMEA, and APAC so regional reimbursement approaches, referral patterns, and adoption barriers could be reflected in the model assumptions and not treated as uniform across geographies.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 19% | APAC: 38% |

| Mid tier: 53% | Functional/Unit leaders: 24% | EMEA: 37% |

| Smaller Players: 19% | Managers: 57% | Americas: 25% |

Market-Sizing & Forecasting

Our sizing starts from a top-down demand pool build based on treatable cohorts and procedure activity, then translates that into device revenue using typical therapy pathways. The model follows patient movement from diagnosis to trial and then to permanent implantation. It also models initial implants and replacements separately so the installed-base effect is not missed. To keep totals realistic, we corroborate with selective bottom-up checks, including sampled average selling price (ASP) by system type multiplied by implied unit volumes, plus channel checks on therapy mix.

Key inputs include procedure setting mix (hospital versus ASC), trial-to-implant conversion, replacement timing, implantable versus external system share, and ASP movement linked to technology upgrades and reimbursement changes. Forecasting uses scenario analysis based on expert views on how quickly MRI-compatible systems, miniaturization, and follow-up workflow improvements are taken up, and on whether payer policies speed or slow referrals. When a bottom-up view is incomplete for smaller countries, gaps are handled by using proxy adoption rates anchored to comparable health system access and urology and colorectal procedure intensity.

Data Validation & Update Cycle

Validation is performed by comparing model outputs with independent signals, including region-level procedure trends, reimbursement markers, and the implied installed base needed to support replacement revenues. Outliers are flagged and the underlying assumptions are revisited before totals are finalized, followed by an internal multi-step review where calculations and logic are rechecked.

Reports are refreshed annually, with interim updates when material events occur, such as major approvals, reimbursement changes, or meaningful pricing shifts. Before delivery, a final review pass is completed so clients receive the most recent updated view based on the latest available information.

Mordor Intelligence's Sacral Nerve Stimulation Market Size Measured Against Other Published Estimates

Published estimates for this market can vary because firms choose different boundaries for what gets counted, and they do not always align on the year used for the stated market value. Differences also show up when one model assumes faster adoption of newer implant systems, or when ASPs are projected with simple growth rates instead of being tied to product and reimbursement changes.

By tracking procedure pathway rates and refreshing ASP assumptions using implant mix and replacement timing checks, Mordor Intelligence keeps the total tied to therapy revenues from sacral nerve stimulation systems and avoids blending in broader neuromodulation device pools.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.64 B (2025) | |

| Trade Journal A | USD 1.78 B (2024) | Uses an earlier base year and appears to extend scope with broader revenue capture assumptions, which can lift totals when procedure conversion and replacement cadence are not explicitly modeled. |

| Regional Consultancy B | USD 2.20 B (2025) | Likely applies higher penetration and ASP growth expectations across regions, and may include adjacent neuromodulation revenues or services that are not restricted to sacral nerve stimulation systems. |

The spread in values is mainly explained by scope edges, year alignment, and how adoption and pricing are projected. With clear links to procedure flow, implant mix, and replacement behavior, the sizing steps remain traceable and can be repeated as new clinical and reimbursement signals emerge.

Key Questions Answered in the Report

What is the projected value of the sacral nerve stimulation market in 2031?

Forecasts point to USD 2.94 billion by 2031 as procedural volumes expand and new indications reach the clinic.

Which product category dominates current revenue?

Implantable systems deliver 85.92% of 2025 revenue thanks to proven durability and continuous stimulation.

Which region is projected to grow fastest?

Asia-Pacific leads with a 12.29% CAGR on the back of fresh approvals in Australia and Japan and rising healthcare investment.

How are ambulatory surgical centers influencing adoption?

ASC pathways cut facility costs by up to 30% and are posting an 11.62% CAGR, drawing volume away from traditional hospital settings.

What technological advance is most differentiating next-gen devices?

Closed-loop algorithms that auto-adjust stimulation using ECAP feedback are reducing overstimulation complaints by more than 90%.

Which company recently entered the market with a battery-free system?

Neuspera Medical secured FDA clearance in June 2025 for its inductively powered iSNM platform.

Page last updated on: