Transcranial Magnetic Stimulator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.58 Billion |

| Market Size (2031) | USD 2.48 Billion |

| Growth Rate (2026 - 2031) | 9.45% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

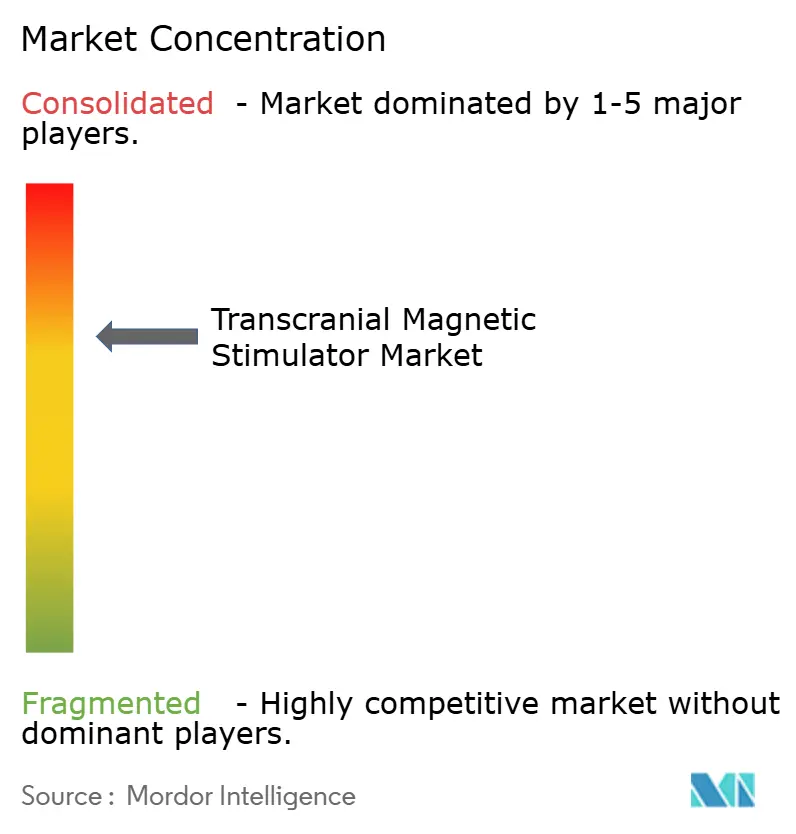

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Transcranial Magnetic Stimulator Market Analysis by Mordor Intelligence

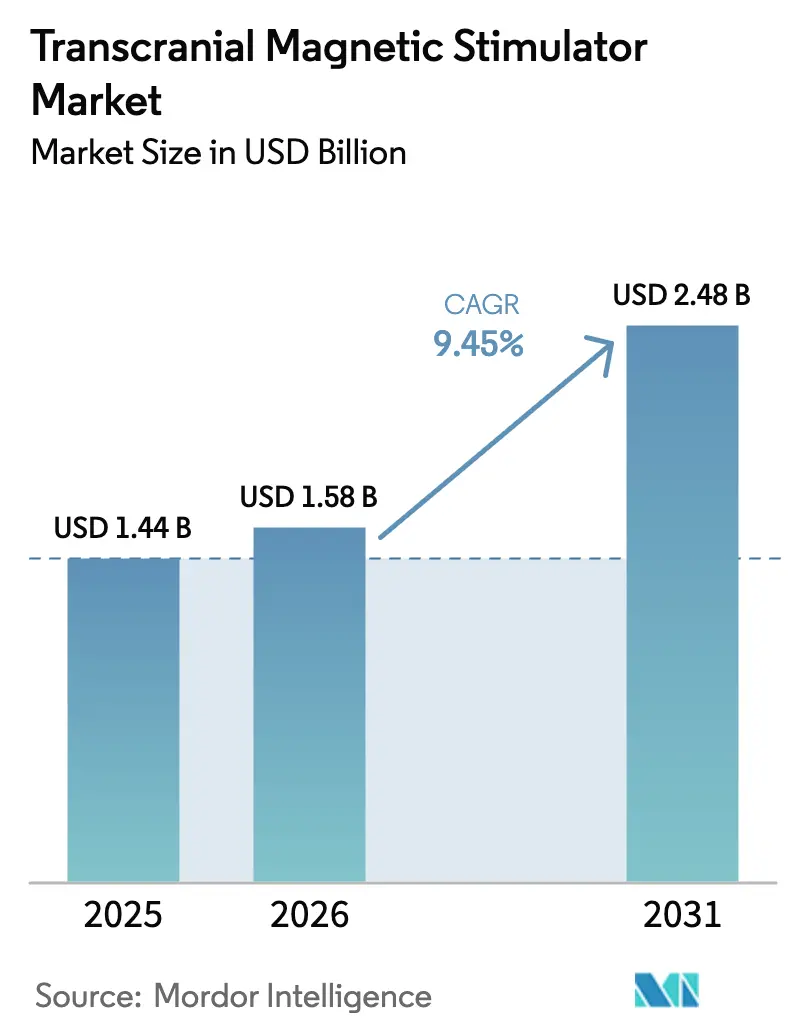

The Transcranial Magnetic Stimulator market size is expected to grow from USD 1.44 billion in 2025 to USD 1.58 billion in 2026 and is forecast to reach USD 2.48 billion by 2031 at 9.45% CAGR over 2026-2031.

This growth mirrors a decisive transition of the transcranial magnetic stimulator market from an adjunct psychiatric intervention toward a mainstream neurostimulation platform that serves both psychiatric and neurological conditions. Expansion in adolescent approvals, led by NeuroStar Advanced Therapy’s 2024 clearance for patients aged 15-21, immediately widened the eligible population pool by roughly 35% and underscored regulators’ confidence in the modality. A related driver is the accelerating adoption of service-integrated delivery models; manufacturers are acquiring clinic networks so that treatment accessibility, rather than hardware specification, becomes the primary competitive lever. Fast-growing deep TMS systems, portable devices for post-acute care, and AI-guided coil-positioning collectively enhance therapeutic precision, cut treatment times, and lower staffing burdens. Finally, the regional demand shift toward Asia-Pacific reflects health-system modernization, easing device approval pathways, and heightened awareness of non-pharmacological therapies.

Key Report Takeaways

- By product type, repetitive TMS captured 57.71% of the transcranial magnetic stimulator market share in 2025, while deep TMS is projected to expand at a 13.29% CAGR through 2031.

- By application, depression accounted for 45.05% share of the transcranial magnetic stimulator market size in 2025 and Alzheimer’s disease is advancing at a 16.61% CAGR through 2031.

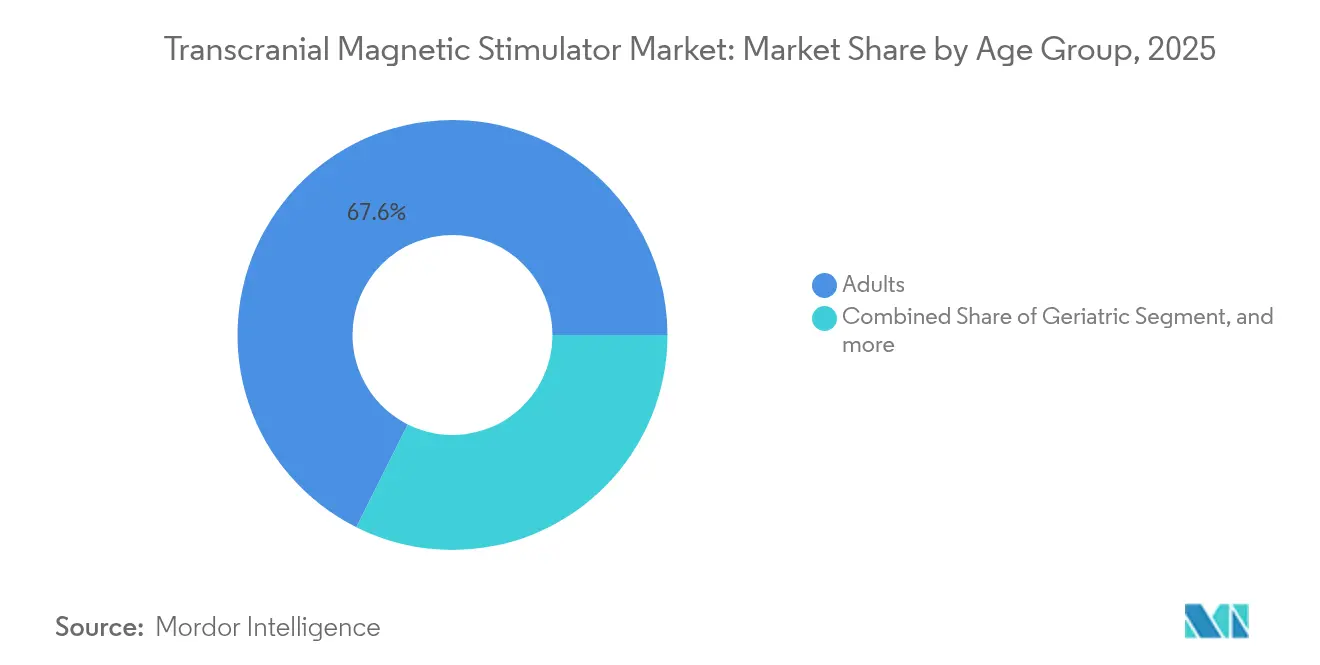

- By age group, adults held 67.62% share of the transcranial magnetic stimulator market size in 2025; the geriatric segment is forecast to grow at 9.74% CAGR to 2031.

- By end user, hospitals led with 52.11% revenue share in 2025, whereas specialty clinics are poised to rise at an 11.72% CAGR during the forecast window.

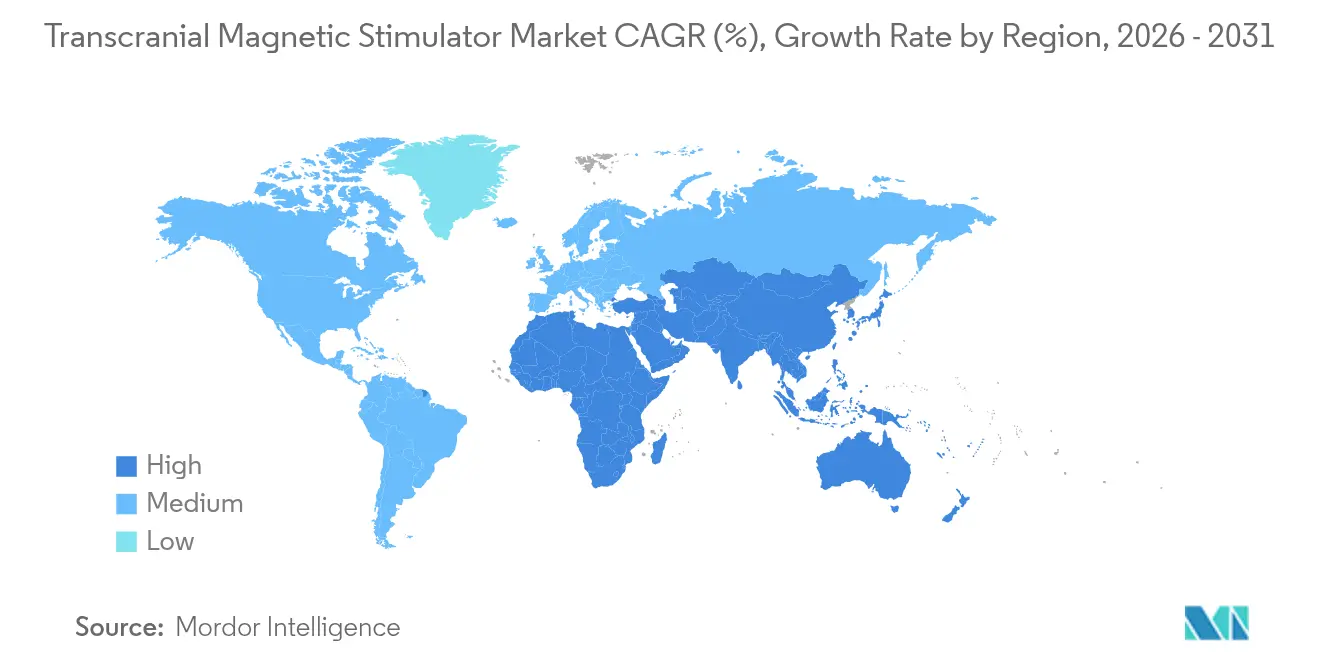

- By geography, North America commanded 44.58% revenue share in 2025; Asia-Pacific is predicted to post the fastest 12.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Transcranial Magnetic Stimulator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of treatment-resistant depression & expanded FDA clearances | +2.1% | Global, earliest uptake in North America & EU | Medium term (2-4 years) |

| Rapidly aging population elevating neurodegenerative disease burden | +1.8% | Global, highest in developed regions | Long term (≥ 4 years) |

| Favorable insurance reimbursement in developed nations | +1.4% | North America & EU | Short term (≤ 2 years) |

| AI-guided coil positioning & closed-loop stimulation enhancing outcomes | +1.2% | Global, technology hubs in North America | Medium term (2-4 years) |

| Portable & home-use TMS devices unlocking post-acute care channels | +0.9% | Initially developed markets, spreading worldwide | Long term (≥ 4 years) |

| Cross-specialty adoption in pain, addiction & neuro-rehabilitation clinics | +0.8% | Global with regulatory variation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Treatment-Resistant Depression & Expanded FDA Clearances

Treatment-resistant depression affects about 30% of major depressive disorder patients, creating an urgently addressable pool for TMS therapy. NeuroStar Advanced Therapy’s 2024 FDA clearance for adolescents aged 15-21 marked the first non-pharmacological option for this group and achieved 78% clinical improvement in a 1,169-patient cohort.[1]Neuronetics Inc., “FDA Expands NeuroStar Label to Adolescents,” neuronetics.com BrainsWay subsequently received an expanded label for late-life depression, supporting broader geriatric coverage. As major insurers mirrored these FDA decisions, covered lives multiplied and reimbursement friction declined.

Rapidly Aging Population Elevating Neurodegenerative Disease Burden

The rising share of citizens aged 65 and above in Europe, North America, and parts of Asia has intensified demand for disease-modifying interventions. A 52-week personalized repetitive TMS protocol targeting the precuneus slowed cognitive decline in mild-to-moderate Alzheimer’s cases as evidenced by improved Clinical Dementia Rating scores. In parallel, 10 days of rTMS improved motor function in Parkinson’s disease by modulating inflammatory regulatory T-cells, maintaining benefit for 40 days post-treatment. These clinical gains, coupled with the transcranial magnetic stimulator market’s maturing reimbursement pathways, reinforce the modality’s neurological expansion.

Favorable Insurance Reimbursement in Developed Nations

In 2025, Medicare Part B reimburses TMS for severe major depressive disorder under standardized CPT code 90867, bringing average patient co-payments in line with routine outpatient visits.[2]Centers for Medicare & Medicaid Services, “National Coverage Determination for Transcranial Magnetic Stimulation,” cms.gov Private insurers such as Cigna now extend coverage to both initial treatment courses and maintenance regimens for qualified patients, lowering out-of-pocket costs that previously ranged USD 10,000–15,000 per series. Consistent billing rules, published medical policies, and value-based care incentives improve clinic cash flow and underpin broader device adoption.

AI-Guided Coil Positioning & Closed-Loop Stimulation Enhancing Outcomes

Spatial inconsistency has long limited TMS reproducibility. Neuronavigation systems like Soterix Medical’s Neural Navigator achieve <1 mm spatial error while remaining immune to line-of-sight constraints common in optical tracking. Stanford’s SAINT protocol employs functional MRI-guided targeting and accelerated delivery to nearly double remission rates versus standard protocols.[3]Nature, “Stanford Accelerated Intelligent Neuromodulation Therapy (SAINT) Study,” nature.com Image-guided robotic arms further reduce rotational error, paving the way for fully closed-loop systems that adapt stimulation in real time.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preference for Electroconvulsive Therapy (ECT) & Deep Brain Stimulation (DBS) | -1.6% | Global, with regional variations in clinical practice | Medium term (2-4 years) |

| High Capital Cost & Technician Shortage | -1.2% | Emerging markets primarily, with spillover effects | Short term (≤ 2 years) |

| Outcome Variability Due to Coil Placement Inconsistency | -0.9% | Global, with higher impact in non-specialized centers | Medium term (2-4 years) |

| Pediatric Cognitive-Safety Concerns Tightening Regulatory Oversight | -0.7% | Developed markets with stringent regulatory frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Preference for Electroconvulsive Therapy (ECT) & Deep Brain Stimulation (DBS)

ECT maintains superior remission rates in severe mood disorders and can limit TMS adoption in tertiary psychiatric centers. The ASCERTAIN-TRD trial reported a mean MADRS score improvement of -17.39 for rTMS versus -13.22 for pharmacological switching, an important benefit yet still below established ECT benchmarks. Moreover, manufacturers of implantable DBS systems such as the Vercise PC list TMS as a contraindication because of interference risks, obliging clinicians to choose one modality per patient. Closed-loop DBS innovations with real-time neural feedback widen this performance gap.

High Capital Cost & Technician Shortage

System prices ranging USD 100,000–300,000 stretch budgets of smaller facilities, particularly in lower-income economies. UnitedHealthcare’s policy mandates that treatments occur under qualified supervision, emphasizing the need for specially trained staff. Workforce constraints, therefore, can throttle throughput even where devices are installed, tempering near-term growth in the transcranial magnetic stimulator market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Deep TMS Disrupts Repetitive TMS Dominance

Repetitive TMS held a 57.71% transcranial magnetic stimulator market share in 2025, reflecting three decades of clinical validation and the breadth of FDA-cleared psychiatric indications. Commercial familiarity, favorable reimbursement, and declining device prices keep the modality a default entry point for new providers. Deep TMS nevertheless records a 13.29% CAGR, the fastest within the segment hierarchy. Its H-coil architecture penetrates limbic and subcortical areas unreachable by figure-8 coils, supporting approvals for depression, obsessive-compulsive disorder, and nicotine addiction. Therapeutic interest is further reinforced as real-world registries link deeper stimulation targets to reduced relapse rates in treatment-resistant cohorts.

Accelerated protocols are reshaping clinical throughput. Stanford’s SAINT regimen compresses 50 sessions into 5 days, a six-fold reduction in patient visits and associated indirect costs. Concurrently, theta-burst stimulation produces equivalent outcomes to standard 10 Hz series in one-third the time, supporting operational scalability. Navigated TMS adds imaging data to coil positioning, thereby reducing outcome variability. Finally, R&D activity in closed-loop and multi-focal stimulation promises dynamic, patient-specific waveform adjustments aligned to cortical excitability measured in real time. Combined, these sub-segments show how therapeutic innovation continues to widen the transcranial magnetic stimulator market opportunity.

By Application: Alzheimer’s Disease Drives Neurological Expansion

Depression kept a 45.05% slice of the transcranial magnetic stimulator market size in 2025, buoyed by robust reimbursement, extensive safety history, and over 6.9 million delivered treatments worldwide. Despite its central role, sentiment is shifting toward neurodegenerative targets. Alzheimer’s disease posts a 16.61% CAGR thanks to data showing that precuneus-targeted repetitive TMS slows cognitive decline relative to control arms. Health-technology-assessment agencies now factor these results into coverage discussions, accelerating uptake.

Parkinson’s disease benefits from adjunctive rTMS protocols that dampen neuro-inflammation and enhance cortical-subcortical connectivity, delivering measurable motor-score improvements for up to 40 days. Chronic pain applications expand beyond neuropathic indications into fibromyalgia, while stroke-rehabilitation trials find theta-burst strategies promoting motor-cortex plasticity superior to standard physiotherapy alone. OCD remains a steady niche courtesy of both repetitive and deep TMS FDA approvals. The overall breadth of indications buffers revenue streams and cushions the transcranial magnetic stimulator market against reimbursement or clinical-guideline shifts in any single disease area.

By Age Group: Geriatric Segment Accelerates Amid Demographic Shifts

Adults accounted for 67.62% of the transcranial magnetic stimulator market size in 2025 and continue to form the core demographic for psychiatric care. Nonetheless, the geriatric segment is the fastest-rising at 9.74% CAGR. Aging populations drive prevalence of late-life depression, Alzheimer’s, and Parkinson’s disease, all of which respond favorably to stimulation and carry lower seizure risk compared with pharmacotherapy. BrainsWay’s geriatric-label expansion in 2024 addressed tolerability and polypharmacy constraints prevalent in older cohorts.

Conversely, pediatric and adolescent uptake pivoted upward following the 2024 NeuroStar clearance. Clinics now report 78% symptom improvement among teenagers under standardized protocols, offering a non-pharmacological alternative amid rising adolescent depression post-pandemic. While volumes are still nascent, cumulative life-time treatment value per patient is high, reinforcing long-term demand visibility for the transcranial magnetic stimulator market.

By End User: Specialty Clinics Challenge Hospital Dominance

Hospitals controlled 52.11% revenue in 2025 by leveraging multidisciplinary teams, integrated billing systems, and co-located imaging. Yet specialty clinics are advancing at an 11.72% CAGR, favored for shorter wait times, focused staff expertise, and patient-friendly environments. Neuronetics’ USD 129.8 million acquisition of Greenbrook TMS in December 2024 consolidated 130 treatment centers, unlocking USD 22 million in projected annual cost synergies and demonstrating the strategic value of vertically integrated networks.

Academic institutes remain essential incubators for protocol refinement, exemplified by multi-locus stimulation studies at university neuro-engineering labs that shape next-generation parameter sets. Meanwhile, portable devices are enabling supervised home-care pilots that shorten inpatient stays and expand follow-up capacity. Collectively, these dynamics diversify delivery pathways and lift utilization rates across the transcranial magnetic stimulator market.

Geography Analysis

North America retained 44.58% revenue leadership in 2025 owing to early FDA approvals, broad insurance coverage, and concentrated manufacturer headquarters. Stable reimbursement, a mature clinical-research ecosystem, and the growing share of service-based TMS networks underpin steady procedure volumes. The United States also pioneers novel payment models, including bundled outpatient episodes, that align incentives for efficient care delivery.

Europe holds the second-largest revenue base, supported by CE-marked devices and harmonized regulations under the Medical Device Regulation framework. Several member states have integrated TMS into national guidelines for depression and OCD, facilitating regional convergence. Reimbursement heterogeneity persists, but high-income nations such as Germany and France reimburse up to 30 daily sessions per index course, reinforcing adoption momentum.

Asia-Pacific is the transcranial magnetic stimulator market’s fastest-growing region at 12.05% CAGR. Japan’s specialized TMS clinics demonstrate high-volume models aided by health-insurance reimbursement. China’s hospital-modernization drive and domestic manufacturing capacity reduce acquisition costs, while private-health spend in India unlocks demand among urban populations. South America and the Middle East & Africa follow in early-stage growth corridors, where neurological disease burden rises against expanding tertiary-care capacity.

Competitive Landscape

The transcranial magnetic stimulator market shows moderate consolidation. The top manufacturers pursue vertical integration to secure procedure volumes and recurring service revenue. Neuronetics’ Greenbrook buyout established the world’s largest integrated TMS network and exemplified the shift from device sales toward patient-journey ownership. This model unlocks utilization synergies, facilitates data collection for payer evidence dossiers, and shields manufacturers from device-price compression.

BrainsWay differentiates via H-coil deep TMS technology that targets subcortical structures, now covering depression, OCD, and smoking addiction indications. Series-B companies such as Magnus Medical focus on accelerated protocols like SAINT, which promise higher remission within compressed timelines. Emerging entrants include Motif Neurotech, which raised USD 18.7 million to develop implantable stimulators addressing treatment-resistant depression.

Product development centers on AI-guided positioning, real-time adaptive waveforms, and multi-site stimulation. Leading suppliers also roll out subscription pricing, training academies, and cloud-based patient-engagement portals that embed switching costs. Overall, competitive intensity rotates away from pure hardware features toward ecosystem control encompassing clinics, protocols, data, and payer relations.

Transcranial Magnetic Stimulator Industry Leaders

BrainsWay

Magstim

MagVenture A/S

eNeura Inc.

Neuronetics (NeuroStar)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Fasikl received FDA clearance for its AI-powered Felix NeuroAI Wristband designed for essential tremor treatment, representing a breakthrough in wearable neurostimulation technology with personalized stimulation therapy based on real-time feedback.

- June 2025: BrainsWay announced a USD 5 million minority-stake investment in Stella MSO, LLC, expanding its service delivery network and strengthening market presence in the integrated care model.

- January 2025: QuantalX Neuroscience received FDA clearance for its Delphi stimulator employing high-resolution magnetic pulses for diagnosing brain conditions including stroke, dementia, and Parkinson's disease.

- December 2024: Neuronetics completed acquisition of Greenbrook TMS, creating the largest integrated TMS treatment network with over 130 centers and projected annual cost synergies exceeding USD 22 million.

Global Transcranial Magnetic Stimulator Market Report Scope

As per the scope of the report, transcranial magnetic stimulation (TMS) is a non-invasive process of brain stimulation that practices magnetic induction forces focusing on a critical area of the brain. The electromagnetic induction is produced from a coil using electricity, and these pulses go through the cranium to its particular receptor area of the brain.

The transcranial magnetic stimulation market is segmented by type (deep transcranial magnetic stimulation, repetitive transcranial magnetic stimulation, and other types) and application (Alzheimer’s disease, depression, Parkinson’s disease, epilepsy, and other applications). Age group (adults and children) and geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally.

The report offers the value (in USD) for the above segments.

| Deep TMS |

| Repetitive TMS |

| Accelerated TMS |

| Theta-Burst Stimulation |

| Navigated TMS |

| Other Types |

| Depression |

| Alzheimer’s Disease |

| Parkinson’s Disease |

| Epilepsy |

| Chronic Pain |

| Obsessive-Compulsive Disorder |

| Stroke Rehabilitation |

| Other Applications |

| Adults |

| Pediatric & Adolescents |

| Geriatric |

| Hospitals |

| Specialty Clinics |

| Research & Academic Institutes |

| Home-Care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Deep TMS | |

| Repetitive TMS | ||

| Accelerated TMS | ||

| Theta-Burst Stimulation | ||

| Navigated TMS | ||

| Other Types | ||

| By Application | Depression | |

| Alzheimer’s Disease | ||

| Parkinson’s Disease | ||

| Epilepsy | ||

| Chronic Pain | ||

| Obsessive-Compulsive Disorder | ||

| Stroke Rehabilitation | ||

| Other Applications | ||

| By Age Group | Adults | |

| Pediatric & Adolescents | ||

| Geriatric | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Research & Academic Institutes | ||

| Home-Care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected growth rate of the transcranial magnetic stimulator market through 2031?

The global market is forecast to rise from USD 1.58 billion in 2026 to USD 2.48 billion by 2031, reflecting a 9.45% CAGR.

Which product segment shows the fastest expansion?

Deep TMS systems exhibit a 13.29% CAGR, outpacing other modalities due to deeper brain-structure coverage and multi-indication FDA clearances.

How significant is depression within current TMS applications?

Depression accounts for 45.05% of 2025 revenue, making it the dominant indication supported by extensive reimbursement and clinical evidence.

Which region is emerging as the fastest-growing market for TMS?

Asia-Pacific leads with a 12.05% CAGR, driven by healthcare infrastructure upgrades and regulatory harmonization.

Why are specialty clinics gaining share over hospitals?

Focused TMS clinics deliver shorter wait times, streamlined workflows, and integrated follow-up, supporting an 11.72% CAGR that challenges hospital dominance.

How is AI influencing TMS treatment outcomes?

AI-guided neuronavigation achieves sub-millimeter coil placement accuracy, while closed-loop systems adapt stimulation in real time, collectively boosting efficacy and consistency.

Page last updated on: