Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 16.80 Billion |

| Market Size (2031) | USD 33.57 Billion |

| Growth Rate (2026 - 2031) | 14.86% CAGR |

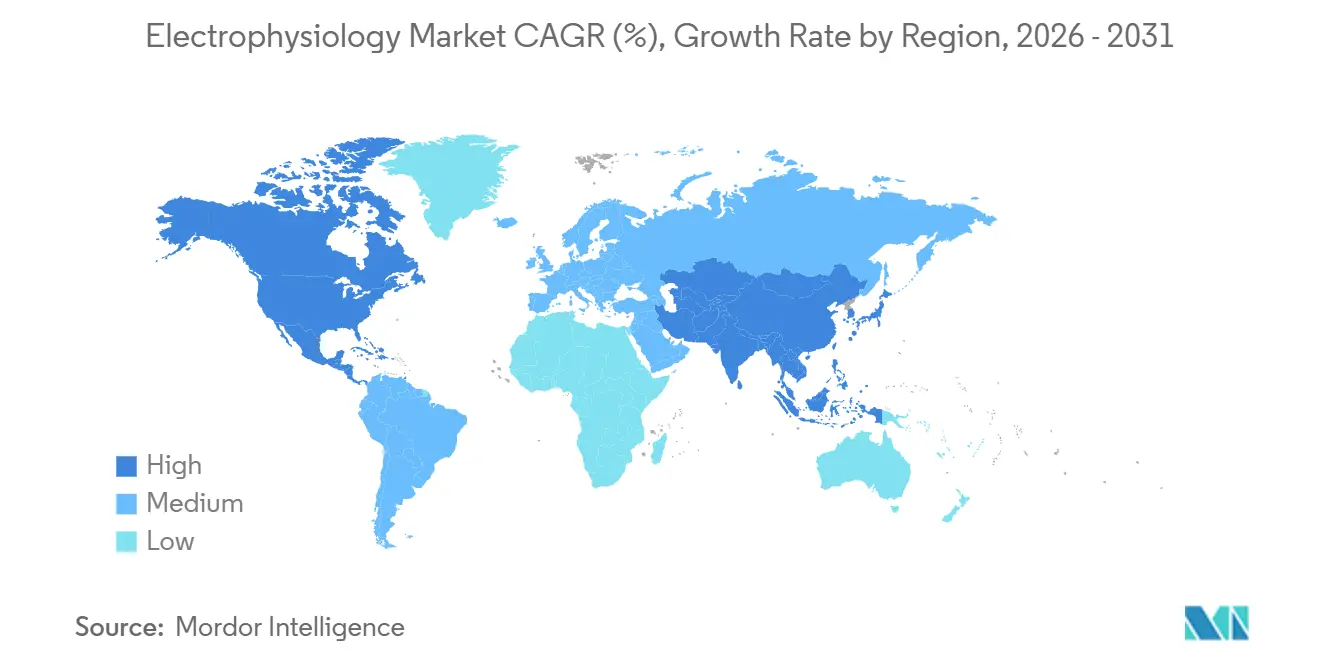

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electrophysiology Market Analysis by Mordor Intelligence

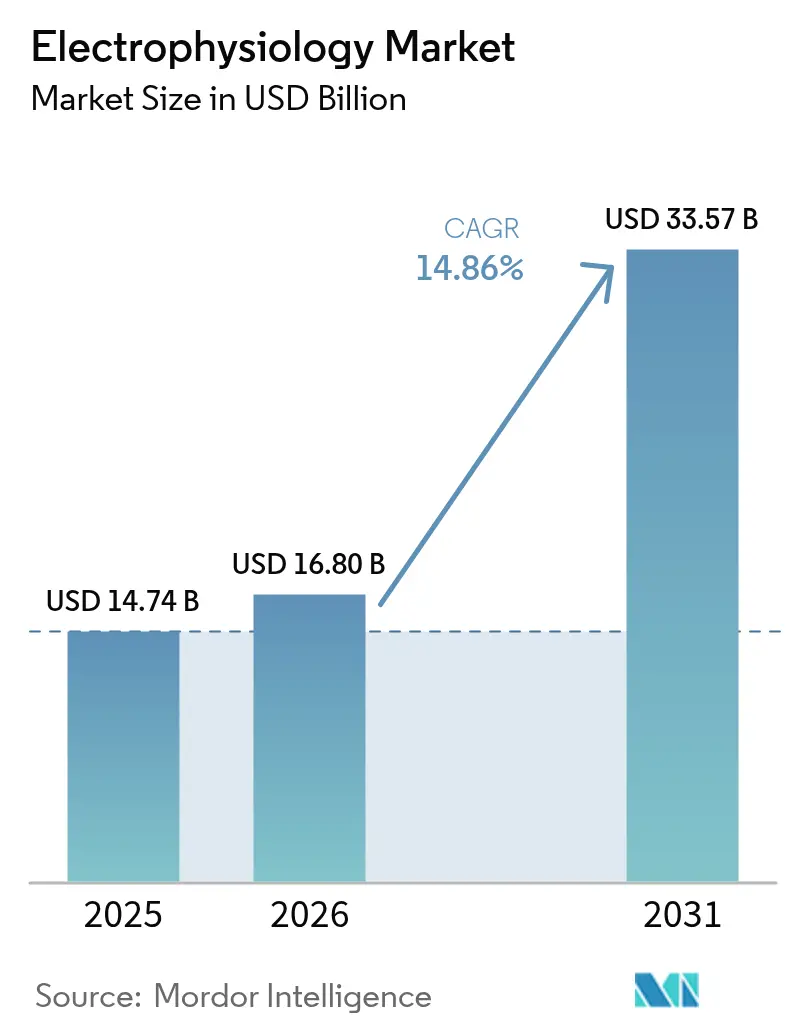

The Electrophysiology Market size is expected to grow from USD 14.74 billion in 2025 to USD 16.80 billion in 2026 and is forecast to reach USD 33.57 billion by 2031 at 14.86% CAGR over 2026-2031.

This growth rests on swift adoption of pulsed field ablation (PFA) technologies, rising procedural volumes tied to aging populations, and the steady shift of atrial fibrillation cases to outpatient settings. Broader reimbursement, especially from Medicare, is sustaining capital investment in advanced laboratories while industry consolidation concentrates intellectual property in the hands of a few large device makers. Asia-Pacific is adding new capacity at a faster pace than any other region, but North America still delivers the largest revenue pool. Collectively, these factors position the electrophysiology market to outpace many other cardiovascular device categories through 2030.

Key Report Takeaways

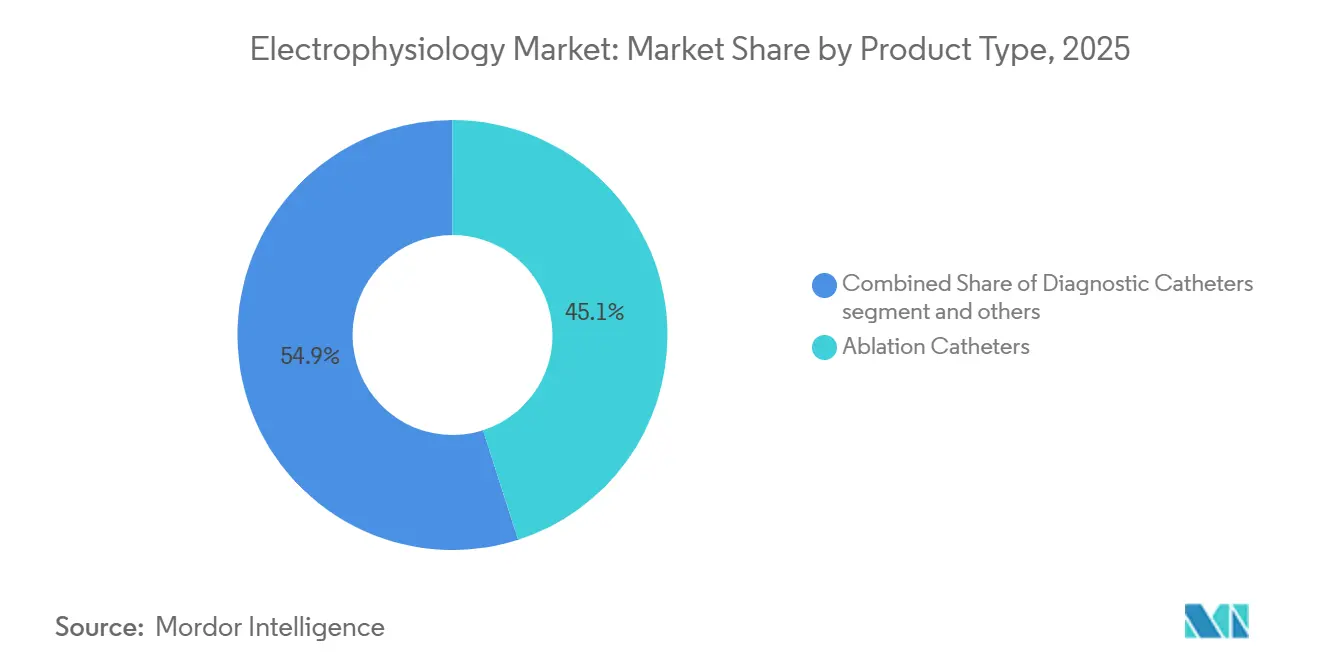

- By product type, ablation catheters held 45.06% of the electrophysiology market share in 2025; mapping & navigation systems are projected to grow at a 15.80% CAGR through 2031.

- By indication, atrial fibrillation accounted for 62.46% of the electrophysiology market size in 2025 and is growing at a 14.75% CAGR.

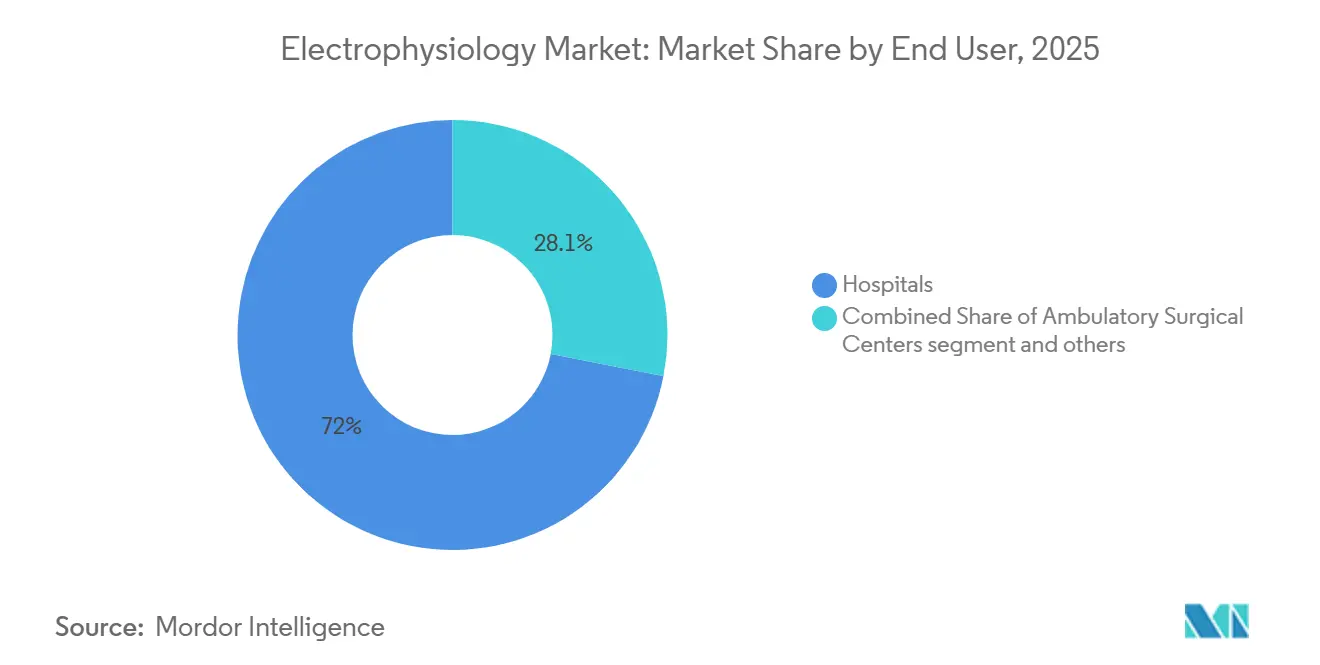

- By end user, hospitals accounted for 71.95% of the electrophysiology market in 2025, while ambulatory surgical centers are expanding at a 16.54% CAGR through 2031.

- By geography, North America led with a 42.54% revenue share in 2025; Asia-Pacific is forecast to post a 15.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electrophysiology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of atrial fibrillation & other arrhythmias | +3.2% | Global, highest in North America & Europe | Long term (≥ 4 years) |

| Rapid technology innovation in ablation & mapping systems | +2.8% | Global, led by North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Growing preference for minimally-invasive catheter procedures | +2.1% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Accelerated adoption of pulsed field ablation (PFA) systems | +2.4% | North America & EU leading, rapid APAC uptake | Short term (≤ 2 years) |

| Broader reimbursement & EP-lab build-outs in emerging markets | +1.9% | APAC core, spill-over to MEA & Latin America | Long term (≥ 4 years) |

| Hybrid "one-stop" EP-OR centers lifting procedure throughput | +1.3% | North America & Europe, selective APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Atrial Fibrillation

Atrial fibrillation incidence is climbing as populations age, with European prevalence expected to double over the next three decades.[1]Abbott Communications, “Volt Pulsed Field Ablation System Clinical Data,” Abbott, abbott.com Younger cohorts in emerging countries are now presenting with arrhythmias tied to sedentary lifestyles, expanding the candidate pool beyond traditional demographics. Persistent forms of the disease are driving demand for sophisticated mapping and dual-energy systems that shorten procedure time and improve lesion quality. Government-funded screening programs in Asia-Pacific detect more undiagnosed cases, adding volume to already strained electrophysiology laboratories. Stroke prevention costs of more than USD 45,000 per patient per year provide payers with a strong financial rationale to approve early ablation interventions.[2]Boston Scientific Corp., “FARAPULSE System Reaches 125,000 Patients,” Boston Scientific, bostonscientific.com

Rapid Innovation in Ablation & Mapping Systems

PFA is the most disruptive modality since radiofrequency ablation. Its tissue-selective properties avoid thermal injury, improving safety margins and boosting operator confidence. Artificial-intelligence-guided mapping software reduces planning time and raises first-pass isolation rates.[3]Volta Medical SAS, “AI-Guided Ablation Outperforms Standard Mapping,” Volta Medical, volta-medical.comDual-energy catheters now permit single-session treatment of complex arrhythmias, lowering repeat ablation incidence below 10%. Leadless pacing developments, such as left bundle branch area pacing, remove hardware complications and open new procedural pathways. Together, these advances expand the electrophysiology market by reducing barriers to physician adoption.

Growing Preference for Minimally-Invasive Catheter Procedures

Same-day discharge expectations push providers toward shorter and safer techniques. PFA procedures last 60-120 minutes versus 3-4 hours for traditional thermal systems, enabling higher daily throughput in ambulatory surgical centers. Non-fluoroscopic navigation now guides 25% of ablations, cutting radiation exposure and paving the way for outpatient approval. Hospital systems favor catheter approaches that reduce length of stay and free operating rooms for higher-acuity cases. Hybrid methods combining minimally invasive and surgical techniques further widen treatment eligibility, particularly for persistent atrial fibrillation patients.

Accelerated Adoption of Pulsed Field Ablation Systems

Survey data indicate PFA will eclipse radiofrequency volumes by 2025. The PULSED AF trial documented 80% arrhythmia-free survival at 1 year, outperforming older modalities. Even newly trained operators report >95% durable isolation, underlining the modest learning curve. Lower complication rates drive a 15-20% total cost-of-care reduction, motivating hospital procurement teams. Regulators recognize the shift, granting multiple breakthrough designations, while Japan and the United States approved the earliest commercial systems by Boston Scientific and Medtronic

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of trained electrophysiologists and EP nurses | -2.1% | Global, most acute in North America & Europe | Long term (≥ 4 years) |

| High capital cost of state-of-the-art EP labs | -1.8% | Emerging markets primarily, selective impact in developed markets | Medium term (2-4 years) |

| Payer caution over long-term PFA safety/efficacy evidence | -1.2% | North America & Europe, limited APAC impact | Short term (≤ 2 years) |

| Radiation-dose scrutiny delaying fluoroscopy-based installs | -0.9% | Global, with regulatory focus in EU & North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Trained Electrophysiologists and EP Nurses

Fellowship programs accommodate 3-4 trainees annually when 8-10 graduates are needed, constraining growth. New PFA technologies still require 50-100 supervised cases to reach competence. Hospitals are piloting cross-training curricula that shorten onboarding to eight months, but unfilled positions can reduce departmental revenue by up to USD 3 million per year. Professional societies propose two-plus-two training models to accelerate certification. Meanwhile, AI-driven automation of documentation tasks frees existing specialists to handle more procedures.

High Capital Cost of State-of-the-Art EP Labs

A fully equipped electrophysiology suite costs USD 3–5 million, a figure that doubles once room renovation and shielding are included. Import duties lift expenditure by 25–40% in India and Brazil, slowing adoption despite rising demand. Vendors now market subscription pricing tied to procedure volumes, shifting spend from capital budgets to operating budgets. Modular systems allow phased upgrades, extending useful life without large one-time investments. Most high-volume centers still recoup capital outlays within 18–24 months as lab utilization climbs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PFA Catheters Drive Innovation

Clinical evidence confirming PFA’s superior safety is diverting capital budgets away from legacy radiofrequency and cryo platforms. Mapping and navigation systems gain momentum because AI integration delivers faster point-by-point guidance, boosting procedure efficiency. Recording systems shift to cloud-based formats, allowing off-site interpretation and lowering staffing needs. Diagnostic catheters grow slowly as they bundle into full-service platforms rather than independent devices. Laboratory imaging hardware rises in tandem with hybrid operating room installations, anchoring hospital investment cycles in the electrophysiology industry.

Competitive differentiation is moving from individual devices to system-level integration. Suppliers that offer seamless software-hardware ecosystems lock in hospital preferences and create recurring revenue from consumables. Access devices remain necessary but mostly commoditized; suppliers leverage them to complete portfolios rather than drive profit. Overall, the electrophysiology market benefits from product convergence that simplifies purchasing decisions and accelerates technology refresh.

By Indication: Atrial Fibrillation Dominance Accelerates

Persistent cases require intricate lesion sets, increasing revenue per procedure and attracting investment in advanced mapping. Ventricular tachycardia ablation shows double-digit growth now that dual-energy catheters can ablate deep myocardial substrates. Atrial flutter remains stable and is often treated during the same session as atrial fibrillation, marginally raising average selling prices.

Early-intervention data persuade clinicians to ablate before anti-arrhythmic drug failure, enlarging the pool of eligible patients and supporting expansion of the electrophysiology market. Emerging technologies for supraventricular tachycardia and niche arrhythmias introduce premium pricing for specialty catheters, but their absolute contribution stays small. Evidence backing first-line ablation feeds payer confidence and broadens coverage, anchoring long-term demand growth in the electrophysiology industry.

By End User: ASC Growth Reshapes Delivery

PFA’s short case times and low complication rates fit ASC workflows, motivating investment in smaller mobile mapping carts and single-use catheters. Specialty cardiac centers combine hospital-grade imaging with ASC-like efficiency, bridging the gap until regulatory frameworks allow more complex ablations in stand-alone facilities.

Economic modeling favors ASCs because labor and overhead run 30% lower than hospital averages. Medicare has yet to add catheter ablation to its ASC-covered list, limiting public-payer volume, but commercial insurers approve outpatient settings for most straightforward cases. Vendors address capital barriers by renting equipment on a per-procedure basis, helping smaller ASCs join the electrophysiology market without multimillion-dollar outlays.

Geography Analysis

North America is supported by broad insurance coverage and high device adoption. Physician fee-schedule cuts of 2.93% in 2025 temper growth, yet procedure volumes stay resilient due to rising atrial fibrillation incidence. Europe follows a mature pattern, with standardization under the Medical Device Regulation easing technology migration across member states. Hospital consolidation concentrates purchasing power, encouraging volume-based discounts but also accelerating refresh cycles for mapping systems.

Asia-Pacific records the fastest CAGR, as China’s Healthy China 2030 initiative subsidizes catheter-laboratory construction and reimburses advanced ablation procedures. India’s private sector invests heavily in catheter labs, with one leading chain adding 2,200 beds and AI-enabled EP suites. Japan maintains high per-capita procedure rates and recently cleared Boston Scientific’s FARAPULSE, signaling quick regulatory acceptance for new PFA systems.

The Middle East targets medical tourism, with the United Arab Emirates increasing healthcare spending from 5% to 5.4% of GDP, bolstering demand for complex ablations. Latin America offers selective promise: Brazil’s economic rebound lifts capital budgets, but import duties and licensing requirements slow roll-outs of newer platforms. Local manufacturing partnerships and flexible financing mitigate these hurdles, keeping the electrophysiology market on a steady upward trajectory across diverse regions.

Competitive Landscape

Competitive intensity is high but remains in the hands of a few multinationals that wield extensive patent portfolios. Johnson & Johnson reshaped the field by acquiring Abiomed for USD 16.6 billion and Shockwave Medical for USD 13 billion, integrating mechanical circulatory support and intravascular lithotripsy into its electrophysiology offerings. Boston Scientific gained a first-mover edge with the FARAPULSE PFA system, treating more than 125,000 patients worldwide and securing early contracts with high-volume centers.

Medtronic counters with two distinct PFA platforms, offering physicians a choice between focal and lattice energy delivery, while its newly approved OmniaSecure lead addresses defibrillation longevity and reliability. Abbott leverages breakthrough device designations for leadless left bundle branch pacing, creating procedural synergies with its Volt PFA platform. Smaller innovators, such as Field Medical, target niche indications with nanosecond-pulse generators that promise deeper lesion depth. Partnerships between software firms and imaging giants, exemplified by Volta Medical and GE HealthCare, integrate AI across the procedure continuum, underscoring that data science is now central to the electrophysiology market’s competitive narrative.

Barriers to entry remain significant due to regulatory scrutiny and the need for multi-center outcome data, but the reward for differentiation is clear. With PFA still in early adoption and leadless pacing nascent, technology leadership can rapidly translate into double-digit share gains. Overall, incumbent consolidation, combined with agile start-up innovation, shapes a dynamic landscape where size and speed both determine strategic success.

Electrophysiology Industry Leaders

Abbott Laboratories

Boston Scientific Corporation

Medtronic

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Boston Scientific received FDA approval for the VARIPULSE Platform, marking the company's entry into the variable-loop pulsed field ablation market with integrated CARTO 3 mapping capabilities

- March 2025: Abbott received CE Mark approval for its Volt Pulsed Field Ablation System, achieving 99.1% pulmonary vein isolation success rates in European clinical trials

- January 2024: Boston Scientific Corporation obtained approval from the United States Food and Drug Administration (FDA) for its FARAPULSE Pulsed Field Ablation (PFA) System. This FARAPULSE PFA System is intended for the isolation of pulmonary veins in patients with drug-refractory, recurrent, symptomatic, paroxysmal (intermittent) atrial fibrillation (AF). It offers an alternative to traditional thermal ablation treatments.

- January 2024: CardioFocus, Inc., a medical device firm focused on enhancing ablation treatments for cardiac arrhythmias, acquired the electrophysiology technology division from Galvanize Therapeutics. Key assets in this acquisition comprise the CENTAURI System pulsed electric field generator, which holds CE marking and is actively marketed in the European Union and the United Kingdom, alongside the QuickShot catheter ablation system, which is presently under development.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global electrophysiology market as all capital equipment, single-use catheters, navigation software, recording units, and ancillary access devices that enable the mapping, diagnosis, and catheter-based ablation of cardiac arrhythmias across hospitals, dedicated EP labs, and ambulatory surgical centers. According to Mordor Intelligence, this definition captures both disposable and durable hardware that directly supports an intracardiac EP procedure.

Scope exclusion: Non-cardiac neuro-muscular electrophysiology devices (EEG, EMG), implantable pacemakers/ICDs sold outside an ablation procedure, and after-sales service contracts are excluded.

Segmentation Overview

- By Product Type

- Ablation Catheters

- Diagnostic Catheters

- Laboratory Devices

- Mapping & Navigation Systems

- EP Recording Systems

- Access Devices

- Other Products

- By Indication

- Atrial Fibrillation

- Atrial Flutter

- AV Nodal Re-entry Tachycardia (AVNRT)

- Ventricular Tachycardia

- Other Arrhythmias

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Cardiac Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Conversations with electrophysiologists, EP-lab managers, reimbursement consultants, and regional distributors across North America, Europe, Asia-Pacific, and Latin America enabled Mordor analysts to stress-test secondary findings, refine penetration rates, and sense-check pricing and adoption curves of emerging pulsed-field platforms.

Desk Research

We began with open datasets that track arrhythmia prevalence and procedure volumes, such as WHO cardiovascular statistics, the American Heart Association's annual EP update, the European Heart Rhythm Association catheter ablation registry, and UN Comtrade export codes for ablation catheters. Company 10-Ks, FDA 510(k) summaries, and trade-association whitepapers then grounded average selling prices and installed lab counts. Paid databases like D&B Hoovers and Dow Jones Factiva helped us benchmark supplier revenue splits by geography. These illustrations are not exhaustive; many additional sources were assessed for nuance, validation, and clarification.

Market-Sizing & Forecasting

We built a top-down model beginning with annual ablation and diagnostic procedure volumes by arrhythmia type, overlaid unit-per-procedure factors, and verified ASPs to reach 2025 revenue. Supplier shipment roll-ups and sampled channel checks provided bottom-up guardrails that prompted calibrations where gaps surfaced. Key variables include atrial-fibrillation prevalence, EP-lab capacity additions, disposable catheter pull-through ratios, pulsed-field adoption curves, reimbursement code inflation, and capital equipment replacement cycles. Five-year forecasts apply multivariate regression blended with scenario analysis, and we leaned on our primary-research panel to weight technology-shift assumptions.

Data Validation & Update Cycle

Outputs pass variance checks against independent procedure audits, import data, and public earnings. Senior reviewers interrogate anomalies before sign-off. Reports refresh annually, while material events trigger interim updates; a final pre-delivery sweep assures clients receive the most current baseline.

Why Mordor's Electrophysiology Market Baseline Remains Steadfastly Dependable

Published values often diverge because firms vary device scope, base years, ASP assumptions, and refresh cadence.

Key gap drivers include whether mapping systems are counted, inclusion of implantables, breadth of emerging-market coverage, and the rigor of primary validation. Mordor's disciplined scope selection and annual refresh, in our view, narrow uncertainty and yield a balanced baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.27 B (2025) | Mordor Intelligence | - |

| USD 6.9 B (2024) | Global Consultancy A | Focuses mainly on ablation catheters and omits mapping hardware; older base year |

| USD 12.77 B (2025) | Industry Data Provider B | Adds implantable pacing/ICD devices and service revenue; blends global ASPs without regional weightings |

| USD 9.06 B (2024) | Regional Trade Journal C | Includes some neuro-muscular EP products and applies single exchange-rate snapshot |

These contrasts show that when scope and variables shift, totals swing widely; Mordor Intelligence offers a repeatable, transparently sourced baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the electrophysiology market?

The electrophysiology market was valued at USD 16.80 billion in 2026 and is projected to grow to USD 33.57 billion by 2031 at a 14.86% CAGR.

Which product segment leads the electrophysiology market?

Ablation catheters lead with 45.06% revenue share in 2025, although mapping & navigation systems are projected to grow at a 15.80% CAGR through 2031.

Why is pulsed field ablation gaining traction?

PFA avoids thermal damage, cuts procedure times to 60-120 minutes, and shows 80% arrhythmia-free survival at 12 months, making it attractive for physicians and payers.

Which region is growing fastest?

Asia-Pacific posts the fastest regional CAGR of 15.41% through 2031 due to major investments in hospital infrastructure and favorable government policies.

What limits growth in the electrophysiology market?

Key constraints include a global shortage of trained electrophysiologists and the high capital cost of equipping advanced laboratories.

How are ambulatory surgical centers impacting market dynamics?

ASCs are growing at a 16.54% CAGR because PFA’s safety profile supports same-day discharge, lowering procedure costs and expanding patient access.

Page last updated on: