Wireless Brain Sensors Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

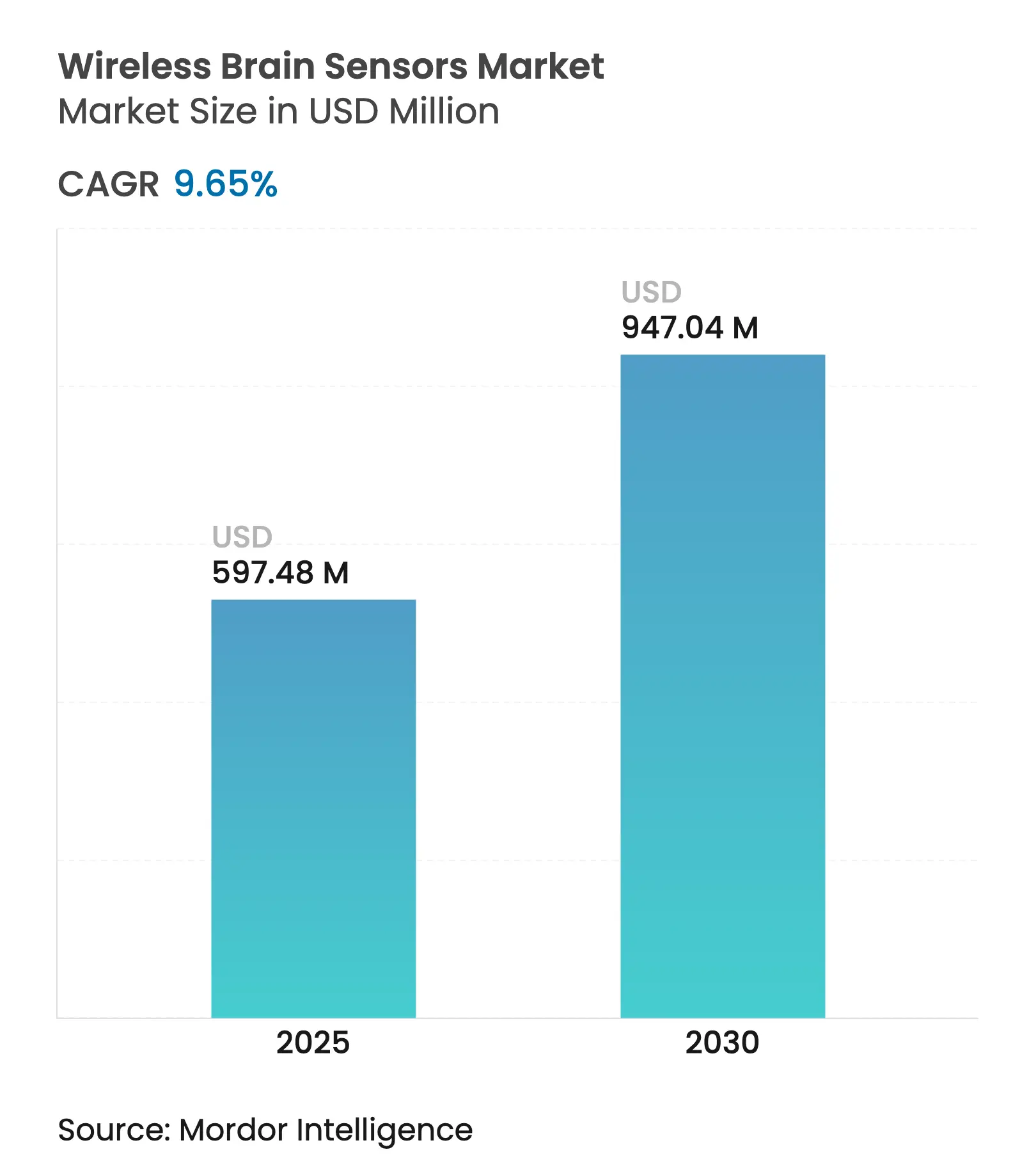

| Market Size (2025) | USD 597.48 Million |

| Market Size (2030) | USD 947.04 Million |

| Growth Rate (2025 - 2030) | 9.65 % CAGR |

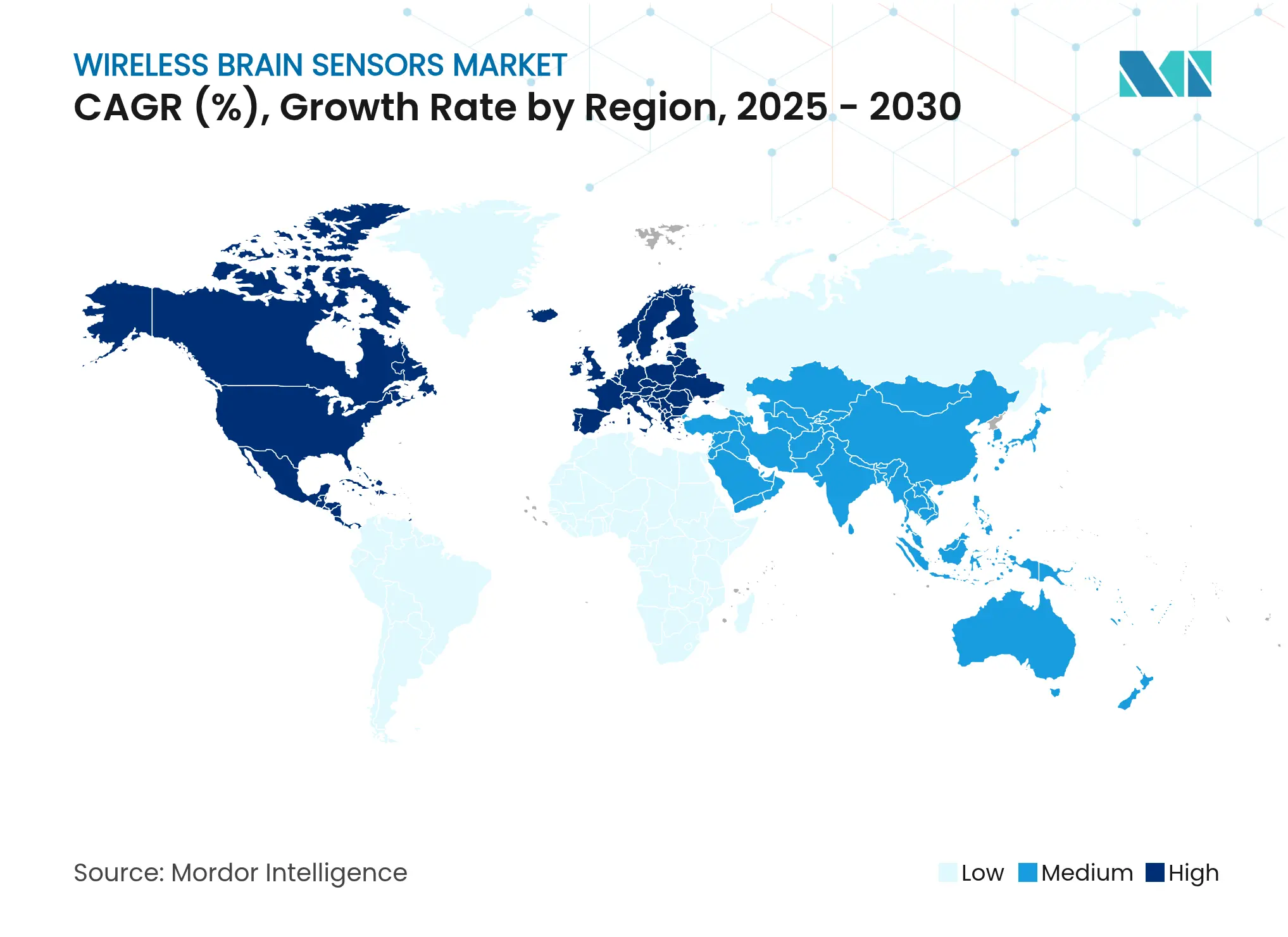

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

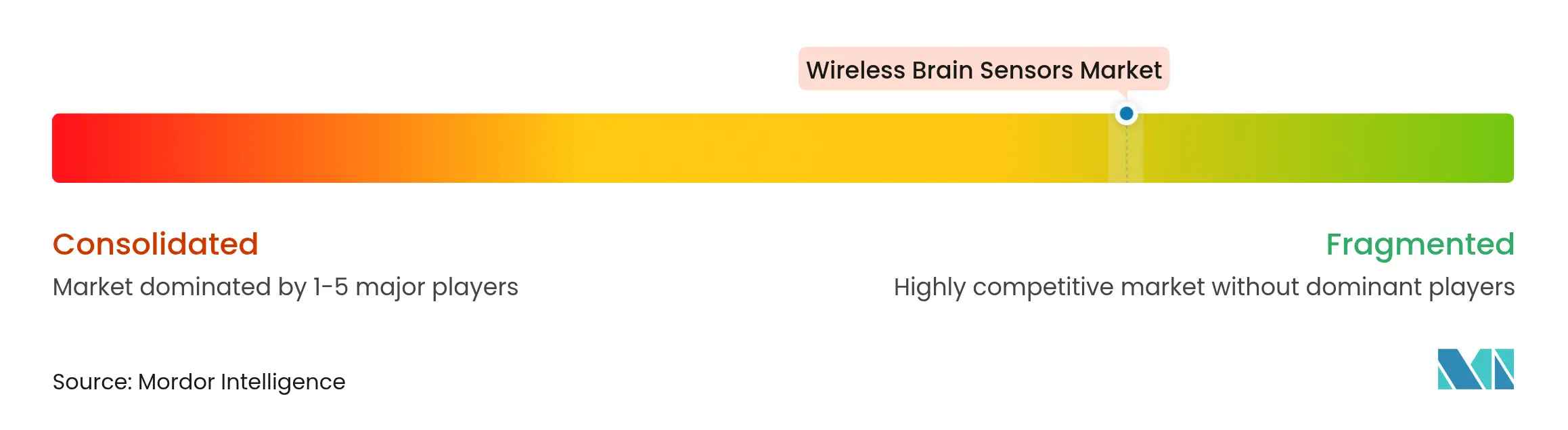

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Wireless Brain Sensors Market Analysis by Mordor Intelligence

The wireless brain sensors market size reached USD 597.48 million in 2025 and is forecast to climb to USD 947.04 million by 2030, advancing at a 9.65% CAGR. Innovation in battery-free implants, rapid sensor miniaturization, and supportive FDA breakthrough designations are expanding clinical and consumer use cases, allowing continuous patient assessment inside and outside the hospital. Growing neurological disease prevalence, now affecting 3.4 billion people, is shifting health-system budgets toward technologies that can spot deterioration hours before standard checks and avoid costly readmissions. Strategic alliances between device makers and semiconductor firms are accelerating integration into earbuds, smartwatches, and ICU platforms, creating fresh revenue streams in telehealth, digital therapeutics, and even space-flight medicine. Venture capital funding remains buoyant despite tighter capital markets, underscoring confidence that wireless monitoring will displace wired rigs in both research and routine care. Near-term growth will hinge on resolving cybersecurity obligations and clarifying reimbursement for remote neuromonitoring, two factors that still temper adoption in developed markets.

Key Report Takeaways

- By product type, devices held 67.45% of wireless brain sensors market share in 2024; accessories are projected to rise at a 10.11% CAGR to 2030.

- By modality, non-invasive systems dominated with 78.21% revenue share in 2024, while minimally-invasive and implantable sensors are poised for the fastest 10.79% CAGR through 2030.

- By end user, hospitals and clinics commanded 48.71% share of the wireless brain sensors market size in 2024, yet home-care settings will pace the field with an 11.05% CAGR over the outlook period.

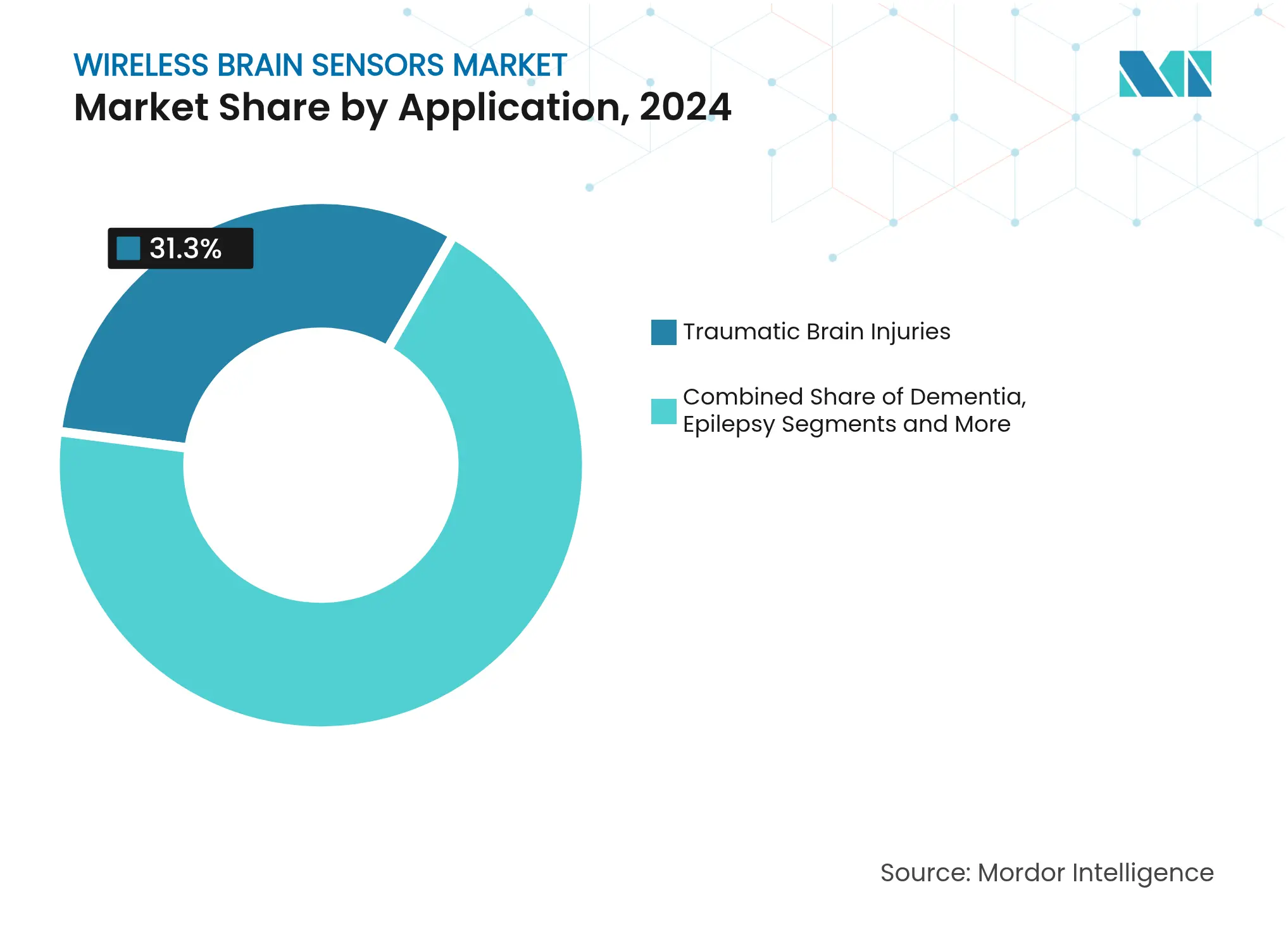

- By application, traumatic brain injury monitoring led with 31.34% of the wireless brain sensors market share in 2024; epilepsy monitoring is forecast to expand at 10.84% CAGR to 2030.

- By technology, Bluetooth Low Energy remained the leading protocol in 2024, although Wi-Fi enabled solutions are set to record the highest adoption growth among high-bandwidth applications.

- By geography, North America remained the largest regional market with 43.16% share in 2024, whereas Asia-Pacific will post the fastest 11.25% CAGR through 2030.

Global Wireless Brain Sensors Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing prevalence of neurological disorders

Growing prevalence of neurological disorders

| +2.1% | Global, highest in sub-Saharan Africa and aging economies | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

+2.1%

|

Geographic Relevance

:

Global, highest in sub-Saharan Africa and aging economies

|

Impact Timeline

:

Long term (≥ 4 years)

|

Rising R&D spend and rapid sensor miniaturization

Rising R&D spend and rapid sensor miniaturization

| +1.8% | North America & EU lead, APAC catching up | Medium term (2-4 years) | |||

ICU shift toward continuous, wireless neuro-monitoring

ICU shift toward continuous, wireless neuro-monitoring

| +1.5% | Global, early adoption in developed markets | Short term (≤ 2 years) | |||

Consumer neuro-wearables gaining mainstream traction

Consumer neuro-wearables gaining mainstream traction

| +1.2% | North America & APAC core markets | Medium term (2-4 years) | |||

Convergence with brain-computer interfaces & digital

therapeutics

Convergence with brain-computer interfaces & digital

therapeutics

| +0.9% | US and China spearhead | Long term (≥ 4 years) | |||

Space-flight related neuro-monitoring demand surge

Space-flight related neuro-monitoring demand surge

| +0.3% | US, EU, China space programs | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Growing Prevalence of Neurological Disorders

Neurological disorders generated 443 million DALYs in 2023, an 18.2% jump since 1990, making them the world’s leading cause of disability and mortality. As stroke, migraine, and Alzheimer’s incidence climb alongside global aging, hospitals face pressure to replace episodic checks with always-on surveillance that can flag secondary injury in real time. Diabetes-linked neuropathies tripled during the same period, underscoring the merging of metabolic and neural health and widening the potential addressable base for continuous multimodal sensors. Forecasts showing 4.9 billion people living with neurological conditions by 2050 indicate current penetration of the wireless brain sensors market is only a fraction of future need. Clinical guidelines are therefore being rewritten to embed continuous monitoring into standard care pathways, accelerating procurement cycles in both public and private systems.

Rising R&D Spend and Rapid Sensor Miniaturization

University and corporate labs are shrinking brain sensors to salt-grain scale while keeping clinical-grade fidelity, enabling unobtrusive placement between hair follicles or within biodegradable matrices [1]Stefanie Dede et al., “Ultra-Small Wireless Neural Motes,” brown.edu. Brown University demonstrated burst-mode protocols that mimic neuronal signaling, trimming radio use to conserve energy and cut electromagnetic noise. The University of Nottingham added optically pumped magnetometers to lightweight helmets, delivering laboratory-level imaging to pediatric wards without sedation or bulky shielding. Georgia Tech hit 96.4% visual-stimulus classification accuracy with nearly invisible epidermal sensors powered by far-field radio harvesting. This cascade of breakthroughs converts wireless prototypes into durable medical devices suitable for year-long trials and broad commercial rollouts.

ICU Shift Toward Continuous, Wireless Neuro-Monitoring

Meta-analyses show 59% of neuro-critical patients achieved favorable outcomes when multimodal wireless monitoring was deployed versus 23% under intermittent regimes [2]National Library of Medicine, “Wireless Multimodal Monitoring Improves ICU Outcomes,” pubmed.ncbi.nlm.nih.gov . Bittium’s rapid-attach EEG caps reduce setup time to under 2 minutes, removing conductive gel and technician bottlenecks while allowing immediate triage in emergency departments. Epiminder secured the first FDA authorization for a months-long implantable EEG system for epilepsy, establishing precedent for long-duration hospital-to-home surveillance. As value-based reimbursement spreads, hospital groups increasingly consider 24/7 neuro-monitoring mandatory for TBI, stroke, and post-aneurysm care pathways.

Consumer Neuro-Wearables Gaining Mainstream Traction

Consumer neuro-wearables generated USD 247.8 million in 2021 and are projected to rise at a 12.33% CAGR through 2030. Apple patents covering EEG, EOG, and EMG measurements inside next-generation AirPods suggest Big Tech aims to turn earbuds into neural dashboards for stress and cognition checks. Timex, STMicroelectronics, and Pison are embedding neural-intent sensors into fitness watches that translate micro-muscle signals into touch-free gesture control. EMOTIV’s investment in MYndspan pairs clinic-grade MEG analytics with at-home EEG headsets, creating a pipeline from consumer health to neurology clinics. The result is rising demand for miniaturized, low-power SoCs, a boon to component suppliers and contract manufacturers alike.

Convergence With Brain-Computer Interfaces & Digital Therapeutics

The FDA issued detailed guidance on implanted BCIs in February 2023, clarifying performance, cybersecurity, and biocompatibility benchmarks and awarding breakthrough labels to Neuralink, Precision Neuroscience, and others. This certainty spurs cross-over projects where wireless brain sensors not only track neural states but also feed algorithms that trigger closed-loop stimulation or software-based digital therapeutics. Precision’s Layer 7 cortical array contains 1,024 electrodes on a 25-micron-thick film that can reside 30 days, blurring lines between diagnostic sensor and therapeutic electrode. Pharma sponsors now bundle longitudinal neural biomarkers into Alzheimer’s and depression trials to gain early efficacy signals, expanding commercial demand for research-grade wireless kits.

Space-Flight Related Neuro-Monitoring Demand Surge

NASA, ESA, and CNSA are funding EEG programs to understand microgravity-induced neuroplasticity during deep-space missions, creating niche but influential demand for low-profile, radiation-tolerant sensors that can stream through spacecraft telemetry esa.int. Findings from these programs often cascade into terrestrial spin-offs such as fatigue prediction for pilots and truck drivers, enlarging the total addressable wireless brain sensors market over the long term.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Stringent regulatory scrutiny for neuro devices

Stringent regulatory scrutiny for neuro devices

| -1.4% | Global, variable by region | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

-1.4%

|

Geographic Relevance

:

Global, variable by region

|

Impact Timeline

:

Medium term (2-4 years)

|

Data-security & patient-privacy concerns

Data-security & patient-privacy concerns

| -1.1% | EU (GDPR), US (HIPAA) | Short term (≤ 2 years) | |||

Battery-life & thermal limits of implantables

Battery-life & thermal limits of implantables

| -0.8% | Global | Long term (≥ 4 years) | |||

Unclear reimbursement for remote neuro-monitoring

Unclear reimbursement for remote neuro-monitoring

| -0.7% | Primarily US, some EU | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Stringent Regulatory Scrutiny for Neuro Devices

The FDA now classifies EEG-based devices as Class II, mandating special controls from software validation to biocompatibility, stretching commercialization timelines to as long as 7 years [3]US Federal Register, “Neurological Devices; Reclassification Final Rule,” federalregister.gov. Europe’s Medical Device Regulation demands post-market surveillance that many startups lack infrastructure to support, pushing them toward partnerships with larger OEMs. China’s NMPA imposes distinct data-hosting and animal-testing rules, forcing Western firms to tailor parallel designs, duplication that lifts costs and complicates global launches. Startups face the choice of targeting wellness markets first or investing in extensive multi-site trials to secure medical labeling.

Data-Security & Patient-Privacy Concerns

Neural data expose intimate cognitive patterns, prompting EU and US regulators to tighten breach reporting and encryption demands. Academic penetration tests showed malware could manipulate stimulation thresholds in implanted BCIs, posing direct patient harm if authentication fails. Power-budget constraints complicate inclusion of robust AES-256 or quantum-resistant protocols, spurring silicon vendors to develop sub-milliwatt cryptographic engines that still meet HIPAA thresholds. Failure to reassure health systems on privacy can stall procurement even when clinical performance is proven.

Battery-Life & Thermal Limits of Implantables

Lithium-iodide cells have finite capacity and dissipate heat, with FDA guidelines capping tissue temperature rises at 2 °C. Researchers are refining ultrasound or inductive recharge links, yet coverage falls when patient posture changes, limiting adoption for multi-year implants. Until batteryless energy harvesting matures, clinicians may prefer semi-implantable or short-term patch devices for chronic conditions.

Segment Analysis

By Product Type: Devices Sustain Revenue Leadership While Accessories Accelerate Innovation

Devices represented 67.45% of the wireless brain sensors market size in 2025 and are forecast to grow at an 8.9% CAGR through 2030 as hospitals refresh aging wired EEG and MEG fleets. Electroencephalography headsets account for the largest slice, helped by Zeto’s FDA-cleared ONE system that provides 21 dry electrodes and AI seizure detection in a single lightweight form factor. Clinicians value reduced setup times, higher patient comfort, and cloud connectivity that speeds expert review. Implantable depth-electrode platforms, while smaller in revenue today, attract outsized venture funding because they promise month-long intracranial data without frequent clinic visits.

Accessories, though only 32.55% of 2024 revenue, will expand 10.11% annually as low-power amplifiers, dry-electrode caps, and Bluetooth Low Energy transceivers unlock truly untethered operation. Electrode manufacturers are shifting from silver-chloride to graphene coatings that cut impedance and survive hundreds of sterilization cycles, important for reuse in high-volume epilepsy centers. Startups are commercializing nanoparticle antenna-sprays that turn existing caps into wireless hubs, a lean upgrade path for budget-constrained hospitals. As AI analytics migrate to the edge, demand rises for micro-controllers that can pre-filter artifacts before cloud upload, keeping bandwidth and privacy overhead low. These trends confirm that the accessories category is the innovation engine of the wider wireless brain sensors market.

By Modality: Non-Invasive Solutions Dominate but Implantables Deliver Superior Growth

Non-invasive systems held 78.21% revenue in 2024, favored for their safety profile and simpler regulatory path. Home-approved headsets such as Cumulus Neuroscience’s at-home EEG enable longitudinal Alzheimer’s trials without site visits, cutting attrition and boosting data quality. Wearable MEG helmets free patients from cryogenic rooms, expanding functional imaging to pediatrics and sports medicine. This broad utility cements non-invasive dominance across hospital, research, and consumer channels.

Implantables, however, will outpace overall market growth at 10.79% CAGR. FDA clearance for Precision Neuroscience’s 1,024-channel Layer 7 array and Epiminder’s multi-month Minder EEG prove regulators now accept temporary cortical devices for long-term diagnostics. Biodegradable hydrogel sensors that vanish after 6 weeks remove explant surgery costs, appealing to stroke and TBI cases needing only finite monitoring. Wireless power links based on ultrasound recharge further extend placement times. Given these breakthroughs, investors anticipate that minimally-invasive systems will steadily erode the share of external caps, especially in epilepsy and ICU markets.

Clinical sentiment is shifting toward a hybrid model where non-invasive sensors screen large populations, and implantables offer deep characterization for complex cases. This complementary dynamic ensures both modalities thrive, collectively driving the wireless brain sensors market forward.

By End User: Hospitals Remain Core Buyers but Home-Care Emerges as Growth Engine

Hospitals and clinics controlled 48.71% of revenue in 2024 due to established neurology budgets and reimbursement codes for inpatient EEG. Emergency departments deploy rapid-attach caps to triage stroke mimics within the critical 30-minute window, while neuro-ICUs integrate wireless multimodal probes to manage intracranial pressure and oxygenation simultaneously. Ambulatory surgery centers also invest in wireless cortical mapping kits for epilepsy resection planning.

Home-care settings are projected to rise 11.05% annually as payers reward prevention over admission. Zeto’s cloud platform lets neurologists supervise long-term EEG from any location, lowering rural care gaps. Consumer wearables cross over into medical pathways; for example, an athlete’s smartwatch that detects abnormal cognitive fatigue can prompt teleconsults before concussion risk escalates. Regulators support this trajectory: the FDA now grants 510(k) clearance for devices initially intended for home sleep monitoring. These developments confirm that home-based adoption is not a niche but an inevitable extension of patient-centric medicine.

Successful vendors customize logistics for home delivery, data hosting, and technical support, thereby transforming device sales into recurring service revenues that lift lifetime value in the wireless brain sensors market.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Application: TBI Leads Today While Epilepsy Anchors Future Upside

Traumatic brain injury monitoring generated the largest slice of 2024 revenue at 31.34% as military, sports, and auto-accident cases drive ICU deployments. Wireless probes that detect spreading depolarizations can alert clinicians six hours before CT scans reveal edema, improving Glasgow Outcome Scores and saving rehabilitation costs. Stroke monitoring follows closely, leveraging continuous perfusion metrics to predict vasospasm after subarachnoid hemorrhage.

Epilepsy will post the fastest 10.84% CAGR. Epiminder’s Minder allows neurologists to record seizure cycles for months, guiding targeted resection or neuromodulation therapy. Cloud AI can analyze terabytes of EEG to forecast seizure likelihood, letting patients pre-empt high-risk periods. Sleep disorder diagnostics, dementia progression tracking, and space-flight monitoring form additional layers of demand, each exploiting the same core capabilities of untethered, high-fidelity brain sensing.

Note: Segment shares of all individual segments available upon report purchase

By Technology: BLE Retains Primacy While Wi-Fi Scales High-Bandwidth Use Cases

Bluetooth Low Energy controllers powered 68.14% of devices shipped in 2024 because they sustain multiday operation on coin-cell batteries and integrate easily with smartphones. Sampling rates of 14.4 kS/s suffice for most EEG bands, meeting clinical thresholds while consuming under 10 mW. Near-field communication occupies specialized niches such as batteryless implants that harvest power through thin-skin layers over the mastoid.

Wi-Fi is catching up with 10.80% CAGR as algorithms increasingly run on edge gateways that need raw, uncompressed data. Platforms offering 56.8 kS/s per channel may stream high-density electrocorticography during awake neurosurgery, a workflow previously limited by tethered hardware. Dual-mode chips that auto-switch between BLE for baseline monitoring and Wi-Fi during critical events maximize power while safeguarding data quality. Exploratory research into ultrasonic and body-area-network links hints at a future where the term wireless brain sensors market encompasses multiple overlapping communication stacks tuned to specific clinical circumstances.

Geography Analysis

North America commanded 43.16% of revenue in 2024, buoyed by FDA-backed breakthrough device pathways and USD 650 million in fresh capital for Neuralink’s Series E round. US academic hospitals deploy multimodal probes as part of value-based care bundles for stroke and TBI, while Canada’s single-payer system pilots home EEG reimbursement in Ontario. Start-ups such as IDUN Technologies partner with Analog Devices in Boston to craft earbud sensors, illustrating a robust pipeline from Silicon Valley to MedTech Valley. Reimbursement gaps remain for at-home reviews, but lobbying by neurology societies is gaining traction.

Asia-Pacific will grow at an 11.25% CAGR through 2030 as China subsidizes BCI commercialization and Japan confronts rapid aging. Beijing’s Institute for Brain Research completed three semi-invasive human implants priced at USD 902 each, undercutting Western alternatives and spurring domestic adoption. Japan’s PMDA approved Medtronic’s Percept PC tremor stimulator, validating regulatory openness to advanced neuro devices. India is digitizing tertiary hospitals under Ayushman Bharat, earmarking funds for neuro-telemetry that should accelerate volume shipments. South Korea and Australia leverage 5G coverage to trial cloud EEG that streams directly to neurologists on call.

Europe holds a significant stake thanks to MDR harmonization and Horizon Europe grants. Germany and the United Kingdom co-finance university–industry consortia that pioneer wearable MEG and graphene electrodes, bolstering regional intellectual property. The European Health Data Space initiative could let cross-border clinical trials collect standardized brain data, a boon for vendors that deliver interoperable APIs. Italy and Spain adopt wireless probes to manage the world’s second-oldest populations, while Eastern European hospitals leapfrog to wireless systems to avoid legacy cable infrastructure. Strict GDPR compliance adds cost but also differentiates vendors that can verify end-to-end encryption, fostering trust among public hospitals and research ethics boards.

Competitive Landscape

Market Concentration

The wireless brain sensors market hosts a mix of entrenched device giants and agile neuro-startups, producing a moderately fragmented competitive matrix. Medtronic, Philips, and Natus leverage vast regulatory and service footprints to win hospital tenders; yet their refresh cycles can lag, giving innovators a foothold with bleeding-edge features. Zeto offers an EEG-as-a-service subscription that bundles hardware, cloud analytics, and neurologist interpretation, enticing community hospitals lacking in-house specialists. EMOTIV serves both consumer and research communities with modular sensor arrays, cultivating brand loyalty among early adopters.

Investment momentum highlights the stakes. Blackrock Neurotech secured USD 200 million from Tether to commercialize implantable BCIs for paralysis, validating investor appetite for deep-tech neurobiology. Pison and STMicroelectronics integrate neural-intent detection into Timex watches, broadening addressable markets beyond medical billing codes. IDUN Technologies collaborates with Analog Devices to deliver ultra-low-noise front-end ASICs for brain-sensing earbuds, signaling semiconductor majors’ belief in mass-market adoption.

Strategic positioning increasingly hinges on three elements: 1) proprietary AI that cleans and interprets data in real time, 2) secure device-to-cloud pipelines that satisfy evolving privacy statutes, and 3) upgradable firmware that can unlock new applications without replacing hardware. Companies that master this triad convert one-off capital sales into sticky software revenue, improving margins and investor appeal. Pediatric neurology remains underserved, presenting a white-space niche for entrants who can scale headsets to infant cranial sizes. Price sensitivity in emerging markets spurs interest in open-source firmware and locally assembled electrode arrays, favouring flexible supply chains and regional joint ventures.

Wireless Brain Sensors Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Researchers from China and Singapore unveiled an implantable miniaturized sensor that transmits ultrasonic intracranial pressure readings wirelessly, reducing the need for invasive cables during neurosurgery.

- September 2022: Amazon introduced Halo Rise, a bedside radar-based sleep monitor that tracks sleep duration and quality without wearable contact.

- September 2022: Sleepme Inc. launched Hiber-AI and a non-wearable sleep tracker that pairs with the Dock Pro Sleep System to adjust mattress temperature in real time to improve sleep quality.

Table of Contents for Wireless Brain Sensors Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Growing Prevalence Of Neurological Disorders

- 4.2.2Rising R&D Spend And Rapid Sensor Miniaturisation

- 4.2.3ICU Shift Toward Continuous, Wireless Neuro-Monitoring

- 4.2.4Consumer Neuro-Wearables Gaining Mainstream Traction

- 4.2.5Convergence With Brain-Computer Interfaces & Digital Therapeutics

- 4.2.6Space-Flight Related Neuro-Monitoring Demand Surge

- 4.3Market Restraints

- 4.3.1Stringent Regulatory Scrutiny For Neuro Devices

- 4.3.2Data-Security & Patient-Privacy Concerns

- 4.3.3Battery-Life & Thermal Limits Of Implantables

- 4.3.4Unclear Reimbursement For Remote Neuro-Monitoring

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Product Type

- 5.1.1Devices

- 5.1.1.1Electroencephalography Devices

- 5.1.1.2Sleep Monitoring Devices

- 5.1.1.3Implantable Neural Monitoring Devices

- 5.1.1.4Other Devices

- 5.1.2Accessories

- 5.1.2.1Electrode Caps

- 5.1.2.2Signal Amplifiers

- 5.1.2.3Wireless Transceivers

- 5.1.2.4Other Accessories

- 5.2By Modality

- 5.2.1Non-Invasive

- 5.2.2Minimally-Invasive / Implantable

- 5.3By End User

- 5.3.1Hospitals & Clinics

- 5.3.2Ambulatory Surgical Centers

- 5.3.3Research & Academic Institutes

- 5.3.4Home-Care Settings

- 5.4By Application

- 5.4.1Traumatic Brain Injuries

- 5.4.2Stroke & Cerebrovascular Monitoring

- 5.4.3Dementia

- 5.4.4Epilepsy

- 5.4.5Sleep Disorders

- 5.4.6Other Applications

- 5.5By Technology

- 5.5.1Bluetooth Low Energy (BLE)

- 5.5.2Wi-Fi

- 5.5.3Near-Field Communication (NFC)

- 5.5.4Other Wireless Technologies

- 5.6By Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2Japan

- 5.6.3.3India

- 5.6.3.4Australia

- 5.6.3.5South Korea

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4Middle East & Africa

- 5.6.4.1GCC

- 5.6.4.2South Africa

- 5.6.4.3Rest of Middle East & Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Advanced Brain Monitoring Inc.

- 6.3.2EMOTIV

- 6.3.3NeuroSky

- 6.3.4Medtronic PLC

- 6.3.5Koninklijke Philips NV

- 6.3.6Natus Medical Incorporated

- 6.3.7Cadwell Industries Inc.

- 6.3.8Neuroelectrics

- 6.3.9NeuroPace Inc.

- 6.3.10BrainScope Company Inc.

- 6.3.11Compumedics Limited

- 6.3.12NeuroWave Systems Inc.

- 6.3.13BioSignal Group Corp.

- 6.3.14Kernel

- 6.3.15Neurable

- 6.3.16InteraXon Inc.

- 6.3.17Masimo Corporation

- 6.3.18Nihon Kohden Corporation

- 6.3.19Cognionics Inc.

- 6.3.20G.Tec Medical Engineering GmbH

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Wireless Brain Sensors Market Report Scope

Wireless brain sensors are devices that help to observe the temperature, sense intracranial pressure, and record brain signaling in the form of brain waves. The essential aim of this wireless brain sensor is to secure the person from emergency situations. The devices are mainly used for patients suffering from sleep disorders, traumatic brain injury, dementia, Parkinson's disease, and other neurological conditions.

The wireless brain sensors market is segmented by product type (devices and accessories), application (traumatic brain injuries, dementia, sleep disorders, and other applications), and geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values in USD million for all the above-mentioned segments.