Next Generation Network Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

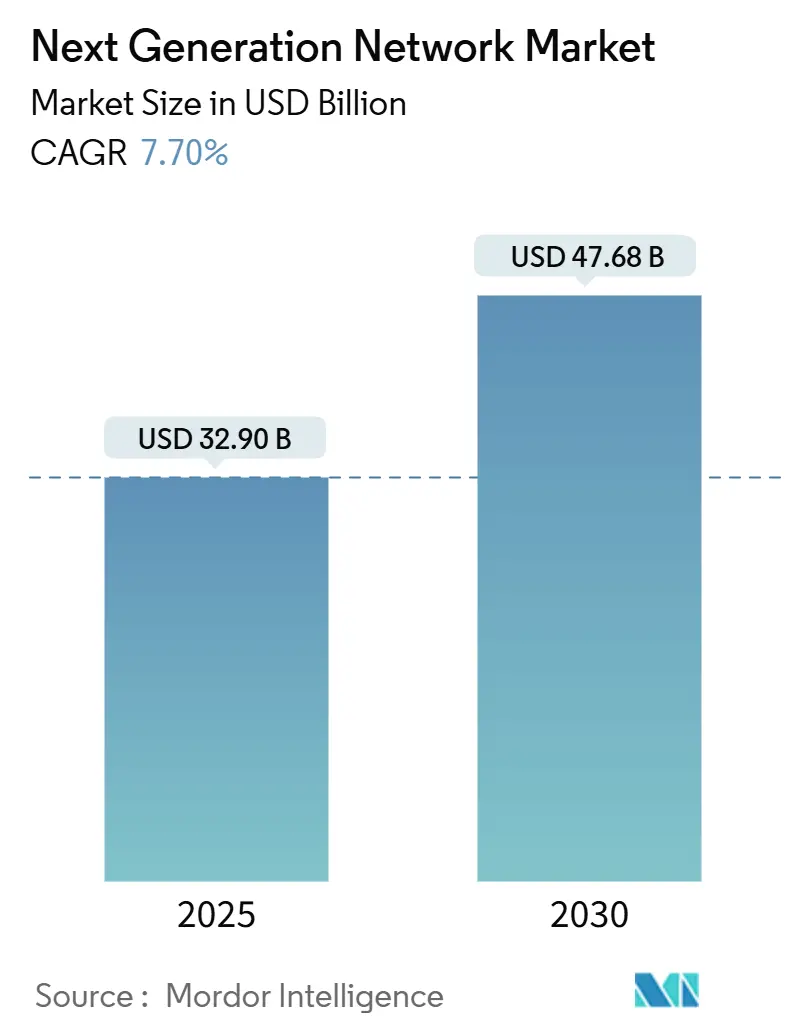

| Market Size (2025) | USD 32.90 Billion |

| Market Size (2030) | USD 47.68 Billion |

| Growth Rate (2025 - 2030) | 7.70% CAGR |

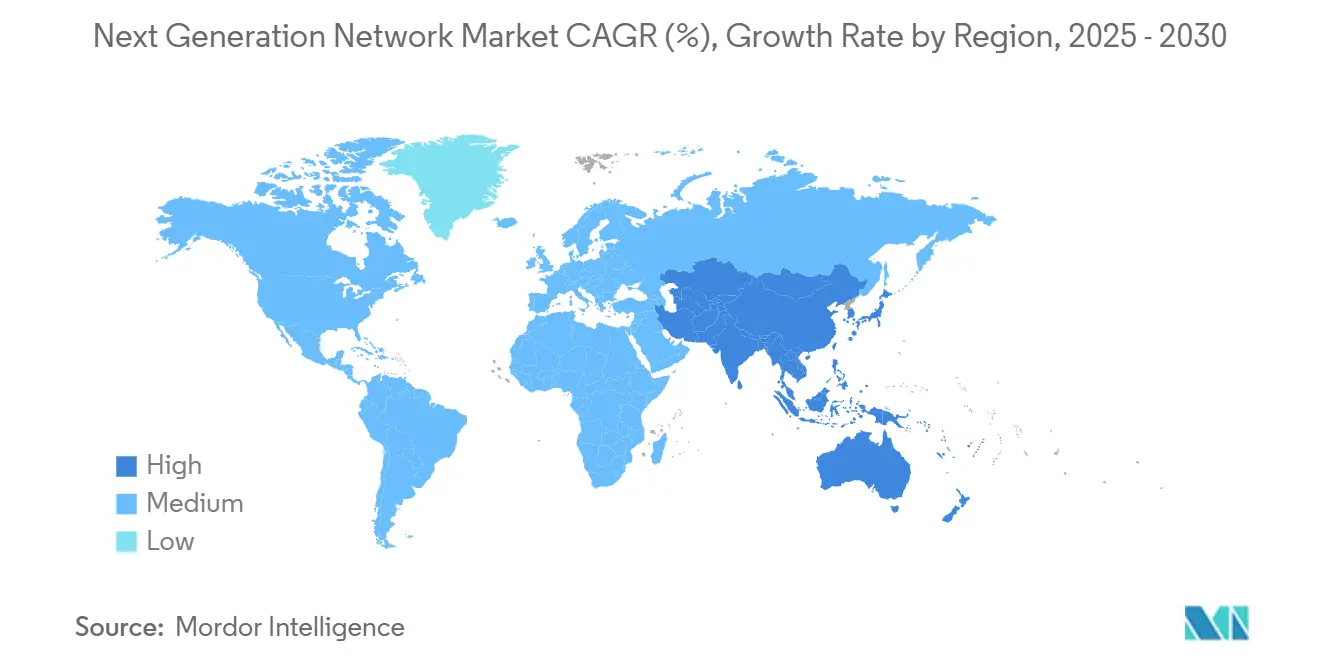

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Next Generation Network Market Analysis by Mordor Intelligence

The Next Generation Network Market size is estimated at USD 32.90 billion in 2025, and is expected to reach USD 47.68 billion by 2030, at a CAGR of 7.70% during the forecast period (2025-2030).

This expansion reflects enterprises shifting from legacy architectures to cloud-native, software-defined infrastructures capable of supporting latency-sensitive, data-intensive workloads. Hyperscaler capital expenditure is expected to hit USD 417 billion in 2025, private 5G is proliferating across manufacturing and healthcare, and network slicing is evolving into a revenue-generating model for telecom operators. Hardware retains an outsized presence, yet accelerating growth in managed services underscores a preference for operating-expense models that offload complexity to specialists. Competitive intensity is rising as traditional vendors race to embed AI-driven automation and merge with cloud divisions while new entrants promote intent-based networking platforms that promise faster service rollout and lower operating costs.

Key Report Takeaways

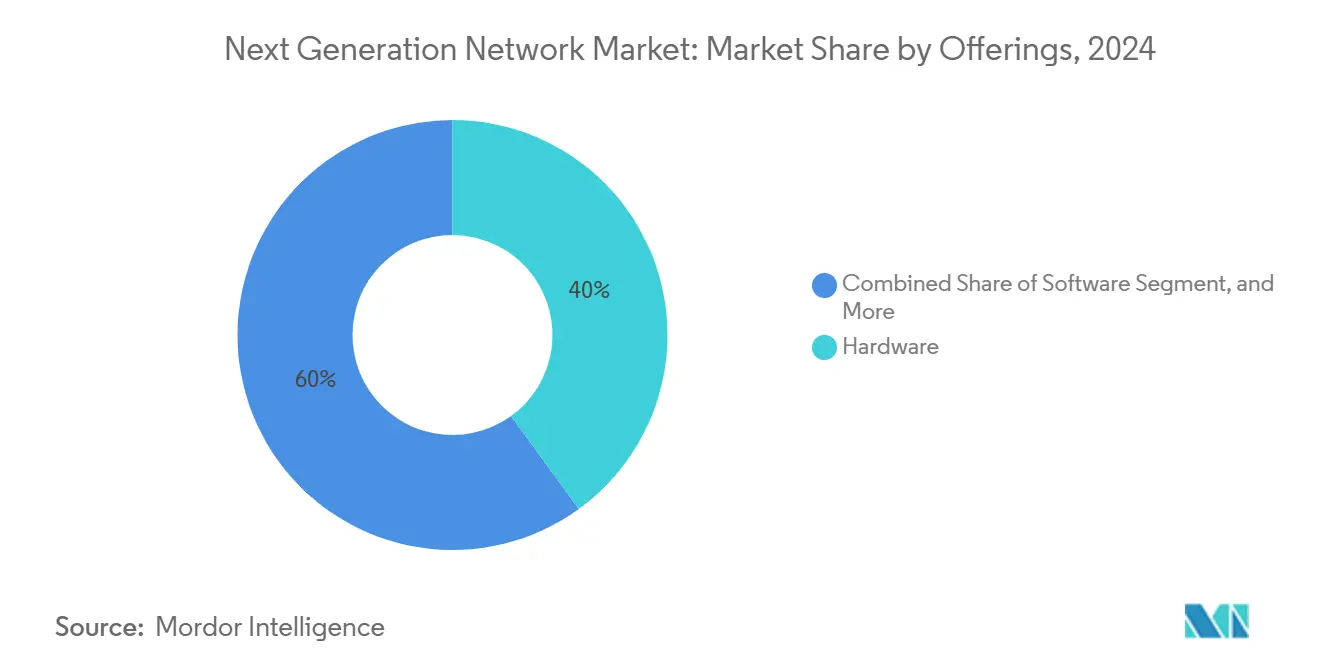

- By offering, Hardware led with a 40% share of the Next Generation Network market share in 2024, whereas Services are set to expand at a 9.2% CAGR through 2030.

- By end user, Telecom and Internet Service Providers held 36.5% of the Next Generation Network market size in 2024, but Cloud Service Providers are advancing at a 10.4% CAGR to 2030.

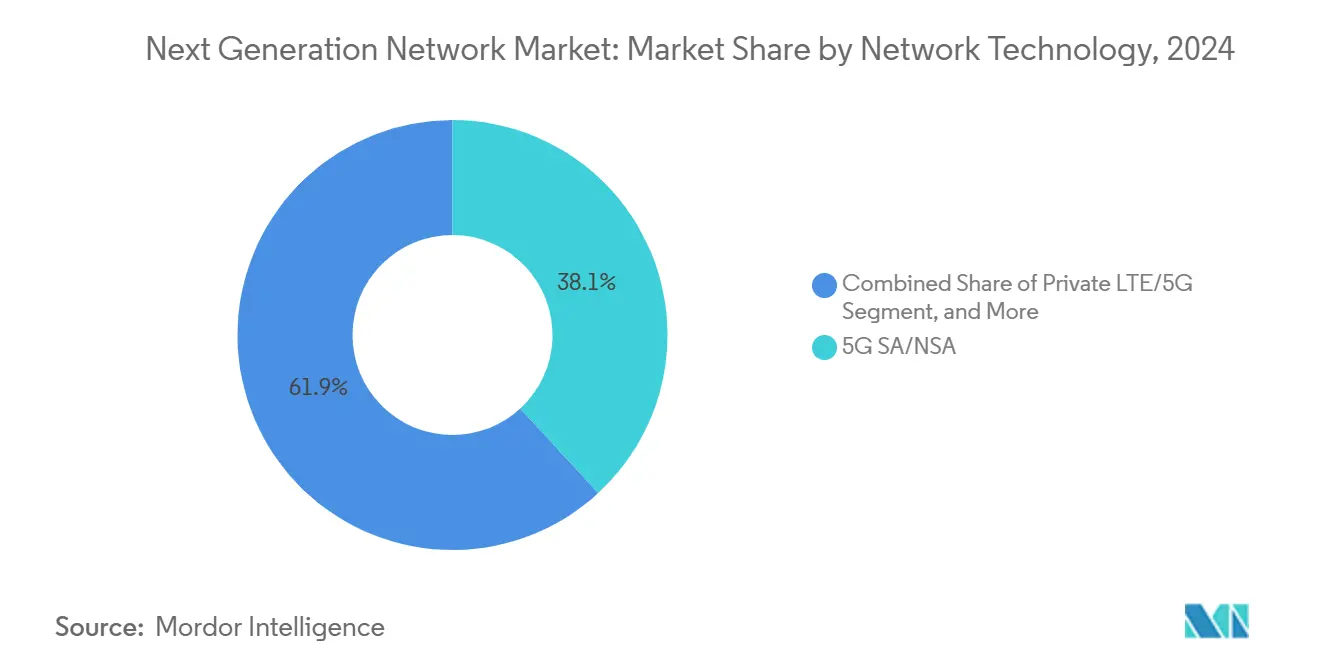

- By network technology, 5G SA/NSA captured 38.1% revenue share in 2024, while Network Slicing is projected to grow at an 11.2% CAGR through 2030.

- By deployment mode, Cloud/Virtualized models commanded 58.3% of the Next Generation Network market share in 2024 and will continue rising at a 9.8% CAGR over the forecast horizon.

- By geography, North America accounted for 35.4% of the Next Generation Network market size in 2024; Asia-Pacific is forecast to expand at a 10.6% CAGR to 2030.

Global Next Generation Network Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding data traffic and low-latency demand | +2.1% | Global, concentrated in North America & APAC | Medium term (2-4 years) |

| Rapid rollout of 5G and private networks | +1.8% | APAC core, spill-over to North America & Europe | Short term (≤ 2 years) |

| Adoption of SDN/NFV for agile operations | +1.4% | Global, led by North America & Europe | Medium term (2-4 years) |

| Generative-AI cluster bandwidth needs | +1.6% | North America & Europe, expanding to APAC | Short term (≤ 2 years) |

| Spectrum liberalization for industrial NGNs | +0.9% | Europe & APAC, selective North America markets | Long term (≥ 4 years) |

| Shift toward consumption-based NaaS models | +1.3% | Global, led by North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Exploding Data Traffic and Low-Latency Demand

Global IP traffic is scaling rapidly as generative-AI, 8K streaming, augmented reality, and IoT sensors flood networks with continuous data streams that legacy infrastructure cannot handle efficiently. Operators respond by deploying edge computing nodes and advanced traffic engineering to cut latency to sub-millisecond levels. T-Mobile’s network-slicing service for Disney Studios shows how dedicated slices guarantee performance for mission-critical workloads. Monetization therefore shifts from bandwidth toward latency- and reliability-based service-level agreements, redefining network economics. [1]“T-Mobile, Disney test 5G network slicing on set,” T-Mobile, t-mobile.com

Rapid Rollout of 5G and Private Networks

Private 5G adoption is accelerating in manufacturing, healthcare, and logistics where deterministic performance and data sovereignty are vital. Airtel’s plant-wide 5G deployment for Indian factories enables real-time automation and predictive maintenance. Singtel has commercialized national consumer network slicing, proving carriers can charge premiums for differentiated 5G services. Enterprises gain direct control of configuration and security, reducing reliance on traditional telcos and aligning connectivity precisely to operational needs.[2]Surajeet Das Gupta, “Airtel’s private 5G for factories,” The Economic Times, economictimes.indiatimes.com

Adoption of SDN/NFV for Agile Operations

Software-defined networking centralizes policy control, automates configuration, and lowers operational overhead. Combined with network-function virtualization where firewalls, load balancers, and intrusion detection run on commodity hardware enterprises launch services faster and curb capex. SDN/NFV also streamlines multivendor environments, allowing consistent security enforcement across distributed assets while shortening maintenance windows.

Generative-AI Cluster Bandwidth Needs

Training large language models requires synchronized, high-throughput links among GPU farms, pushing hyperscalers to install 800 Gigabit Ethernet and InfiniBand fabrics. Light Reading reports 800 G port shipments doubling in 2025 as AI workloads dominate data-center network design. Vendors are building AI-optimized switching silicon and optical transceivers that ensure deterministic latency and near-lossless performance across thousands of parallel flows. [3]800G shipments soar on AI demand,” Light Reading, lightreading.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex for fiber and small-cell build | -1.2% | Global, acute in rural North America & developing APAC | Medium term (2-4 years) |

| Legacy-to-cloud integration complexity | -0.8% | North America & Europe | Short term (≤ 2 years) |

| Shortage of AIOps/intent-based talent | -0.6% | Global, most severe in North America & Europe | Long term (≥ 4 years) |

| Regulatory compliance for multi-cloud data | -0.5% | Europe & parts of Asia where data-sovereignty laws are stringent | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex for Fiber and Small-Cell Densification

5G relies on dense fiber backhaul and urban small-cell grids, requiring operators to install radios every few hundred meters, a cost burden that pushes telecom capex growth below revenue expansion. Rural regions become viable only when governments subsidize digs or carriers pool infrastructure through neutral-host agreements, slowing coverage timelines and delaying monetization.

Legacy-to-Cloud Integration Complexity

Enterprises juggling mainframes, on-prem data centers, and multiple clouds face policy sprawl, dual-stack management, and inconsistent security postures. Migration often proceeds in phases to avoid downtime, but parallel operations inflate costs and extend schedules. Retraining staff and refactoring workflows add hidden expenses that restrain modernization velocity, especially for regulated industries with mission-critical legacy systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Drive Transformation

Services contributed the fastest 9.2% CAGR, underscoring how enterprises outsource design, deployment, and ongoing management while hardware still held a 40% slice of the Next Generation Network market share in 2024. Professional Services dominate as clients engage consultants for architecture blueprints, migration roadmaps, and integration of 5G, SDN, and edge platforms. Managed Services follow as companies off-load day-to-day operations, freeing internal talent for innovation. The Next Generation Network market size for Network-as-a-Service is scaling alongside pay-as-you-go models that eliminate large capital outlays.

Software revenue climbs steadily, propelled by SDN controllers, AI-based analytics, and converged security suites. Modern OSS/BSS stacks orchestrate 5G slices and automate billing, while unified platforms combine traffic engineering with threat detection to simplify policy enforcement. As networking and security converge, integrated solutions reduce vendor sprawl and cut mean-time-to-repair, enhancing resilience for distributed workloads.

By End User: Cloud Providers Accelerate

Telecom/ISPs retained 36.5% of the Next Generation Network market size in 2024, but hyperscale Cloud Service Providers are growing at 10.4% CAGR through 2030. Amazon’s USD 100 billion expansion budget reflects an arms race to meet AI and edge-computing demand. Manufacturing is the most aggressive enterprise adopter, leveraging private 5G for deterministic control loops and asset tracking. BFSI upgrades networks to process real-time transactions under strict compliance, and healthcare rolls out telemedicine with stringent uptime requirements.

Government agencies digitize citizen services and roll out smart-city networks, demanding low-latency connections and rigorous data-sovereignty guarantees. Public sector budgets increasingly factor in resilience against cyber threats, expanding opportunities for sovereign cloud and encrypted transport solutions within the Next Generation Network market.

By Network Technology: Slicing Gains Momentum

5G SA/NSA comprised 38.1% revenue share in 2024, laying the groundwork for programmable services, while network slicing is soaring at an 11.2% CAGR. Ericsson projects slicing could unlock USD 300 billion in carrier revenue by 2030. Private LTE/5G delivers high reliability and secure campus coverage, favored by factories and ports. SD-WAN adoption remains brisk as enterprises pivot away from MPLS, optimizing cloud traffic and suppressing costs.

IP Multimedia Subsystem upgrades converge voice and data, enabling integrated communication packages. Operators bundle IMS with slicing to sell tailored voice-and-video services to verticals such as public safety. Integrated platforms that meld SDN, slicing, and edge computing help enterprises align connectivity to application performance objectives inside the Next Generation Network market.

By Deployment Mode: Cloud Dominance

Cloud/Virtualized modes represented 58.3% of the Next Generation Network market share in 2024 and are forecast to climb at a 9.8% CAGR. Enterprises value elastic scale, API-driven provisioning, and zero-touch automation, spinning up capacity in minutes rather than months. Traffic bursts from AI training, seasonal e-commerce, or event streaming can be absorbed without permanent over-build.

On-premises deployments remain for data-sovereign or ultra-low-latency workloads, yet even these footprints now use virtual network functions on commodity hardware. Hybrid frameworks blend local control with cloud agility, orchestrated by a single policy engine to maintain consistent security and quality-of-service across disparate domains within the Next Generation Network market.

Geography Analysis

North America held 35.4% of the Next Generation Network market size in 2024, sustained by hyperscaler build-outs, enterprise AI adoption, and vibrant private-network pilots. Federal funding for rural broadband and spectrum auctions accelerates 5G coverage, while edge-computing nodes follow e-commerce distribution hubs to minimize delivery latency.

Asia-Pacific is advancing fastest at a 10.6% CAGR, powered by China’s industrial-internet roadmap and India’s production-linked incentives that steer factories toward automation. Southeast Asian governments auction mid-band spectrum and streamline licensing to encourage private 5G, enticing global manufacturers to relocate supply chains and deploy secure campus networks.

Europe emphasizes regulatory compliance and sustainability, prompting carriers to retrofit infrastructure with energy-efficient radios and carbon-aware orchestration. Data-sovereignty mandates push enterprises to adopt localized edge computing clusters, fueling demand for micro-data centers and encrypted backbone links. Middle East and Africa concentrate spending on economic diversification zones and smart-city corridors, whereas South America expands fiber rings around metropolitan areas, inching forward despite fiscal constraints.

Competitive Landscape

Competition is moderate yet intense, with legacy vendors buying AI-native firms to defend share. HPE’s USD 14 billion Juniper acquisition adds Mist AI analytics to HPE’s edge portfolios. Cisco pledges USD 28 billion for AI-centric switching R&D, pursuing intent-based automation while VMware integrates security into multi-cloud networking stacks. Arista rides hyperscaler demand for 400 G and 800 G leaf-spine fabrics, posting record revenue quarter after quarter.

Emerging players use open-source NOSs, disaggregated white-box hardware, and cloud-native CI/CD pipelines to undercut incumbents on price and agility. Private-5G specialists partner with system integrators to offer turnkey kits that bundle radios, core software, and edge compute in subscription packages, nibbling at the perimeter of the Next Generation Network market. Strategic alliances among chipmakers, optics vendors, and cloud providers shorten innovation cycles, forcing traditional equipment makers to accelerate product roadmaps or risk obsolescence.

Next Generation Network Industry Leaders

Cisco Systems, Inc.

Huawei Technologies Co., Ltd.

ZTE Corporation

Ciena Corporation

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Hewlett Packard Enterprise closed its USD 14 billion purchase of Juniper Networks, combining edge-to-cloud hardware with AI-driven networking software.

- January 2025: VIAVI Solutions finalized a USD 1.7 billion Spirent Communications takeover, bolstering 5G and cloud-testing capabilities.

- December 2024: T-Mobile introduced commercial network-slicing packages for U.S. enterprises, offering dedicated resources for manufacturing, healthcare, and public safety.

- November 2024: Cisco pledged USD 28 billion over three years for AI-optimized networking R&D, covering switching, routing, and automation platforms.

Global Next Generation Network Market Report Scope

The next-generation network market is defined based on the revenues generated from the sale of hardware, software, and services by key vendors across the world.

The next-generation network market is segmented by offering (hardware, software, and services), end user (telecom and internet service providers, government, and other end users), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The report offers market forecasts and size in value (USD) for all the above segments.

| Hardware | Network Infrastructure (Routers and Switches) |

| Optical Communication Equipment | |

| Wireless RAN (5G/Small Cell) | |

| Edge Computing Hardware | |

| Software | Network Virtualization (SDN/NFV) |

| Network Security (NGFW, SASE) | |

| Network Analytics and Orchestration | |

| OSS/BSS Platforms | |

| Services | Professional Services |

| Managed Services | |

| Network-as-a-Service (NaaS) |

| Telecom and Internet Service Providers | |

| Enterprises | Manufacturing |

| BFSI | |

| Healthcare | |

| Energy and Utilities | |

| Government and Public Sector | |

| Cloud Service Providers | |

| Other End-users |

| 5G SA/NSA |

| Private LTE/5G |

| SDN |

| SD-WAN |

| Network Slicing |

| IP Multimedia Subsystem (IMS) |

| On-Premises |

| Cloud / Virtualized |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Israel | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Egypt | ||

| Rest of Africa | ||

| By Offering | Hardware | Network Infrastructure (Routers and Switches) | |

| Optical Communication Equipment | |||

| Wireless RAN (5G/Small Cell) | |||

| Edge Computing Hardware | |||

| Software | Network Virtualization (SDN/NFV) | ||

| Network Security (NGFW, SASE) | |||

| Network Analytics and Orchestration | |||

| OSS/BSS Platforms | |||

| Services | Professional Services | ||

| Managed Services | |||

| Network-as-a-Service (NaaS) | |||

| By End User | Telecom and Internet Service Providers | ||

| Enterprises | Manufacturing | ||

| BFSI | |||

| Healthcare | |||

| Energy and Utilities | |||

| Government and Public Sector | |||

| Cloud Service Providers | |||

| Other End-users | |||

| By Network Technology | 5G SA/NSA | ||

| Private LTE/5G | |||

| SDN | |||

| SD-WAN | |||

| Network Slicing | |||

| IP Multimedia Subsystem (IMS) | |||

| By Deployment Mode | On-Premises | ||

| Cloud / Virtualized | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Israel | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the Next Generation Network market by 2030?

The market is forecast to reach USD 47.68 billion by 2030, reflecting a 7.70% CAGR from 2025.

Which segment will expand fastest in terms of offering?

Services will grow at a 9.2% CAGR as enterprises favor managed and Network-as-a-Service models.

How quickly is Asia-Pacific growing in this space?

Asia-Pacific is advancing at a 10.6% CAGR thanks to regulatory support for private 5G and manufacturing digitization.

Why is network slicing important for carriers?

It enables differentiated, SLA-based services and could unlock USD 300 billion in operator revenue by 2030.

What drives cloud providers’ involvement in next-gen networking?

Hyperscalers are investing heavily to meet AI workload demands and to extend low-latency edge services worldwide.

Page last updated on: